newzoo italian games market summary report 2012

TRANSCRIPT

2012 Country Summary Report

Italy

Wybe Schutte | Manager New Business | [email protected] Peter Warman | CEO Newzoo | [email protected]

November 2012 © 2012 Newzoo | www.newzoo.com

Featuring fresh research results on The Italian Games Market

© 2012 Newzoo www.newzoo.com

US EU* UK GER FR IT ES BE NL RU BR PL TR AUS JP CN

supported by

Italy Summary Report Fresh data on the gaming market in Italy

About this Italian Summary Report This report gives a high-level overview of the Italian Games Market based on fresh research and analysis of Newzoo and partners. Find out where the growth will be in Italy and how the games market develops. Most of the data is derived from our Newzoo Data Explorer that our clients use to cross-analyze over 200 topics across all business models and market segments. This document also includes data plotted on our new Screen Segmentation ModelTM comparing Italy with Europe across the typical screens that consumers use to play games.

Peter Warman CEO Newzoo,

[email protected] +31 (0)20 6635816

linkedin.com/in/warman

Content of the report 1. Overview of the market 2. Key trends: EU vs Italy 3. Gamers vs Screens: EU vs Italy 4. Mobile gaming 5. All research topics 6. Subscription offer 7. Newzoo & Contact

© 2012 Newzoo 2

Newzoo We combines Consumer, Transactional & Financial data to provide our clients with The Total Picture and Client-Specific Business Insights required to make smart strategio, development and commercial decisions. Find more info and free stuff on www.newzoo.com.

© 2012 Newzoo 3 © 2012 Newzoo 3

1. Italian Games Market | 2012 High-level overview of players, time and money

© 2012 Newzoo 4

Console games very popular 72% of 18.6M Italian Gamers

© 2012 Newzoo 5

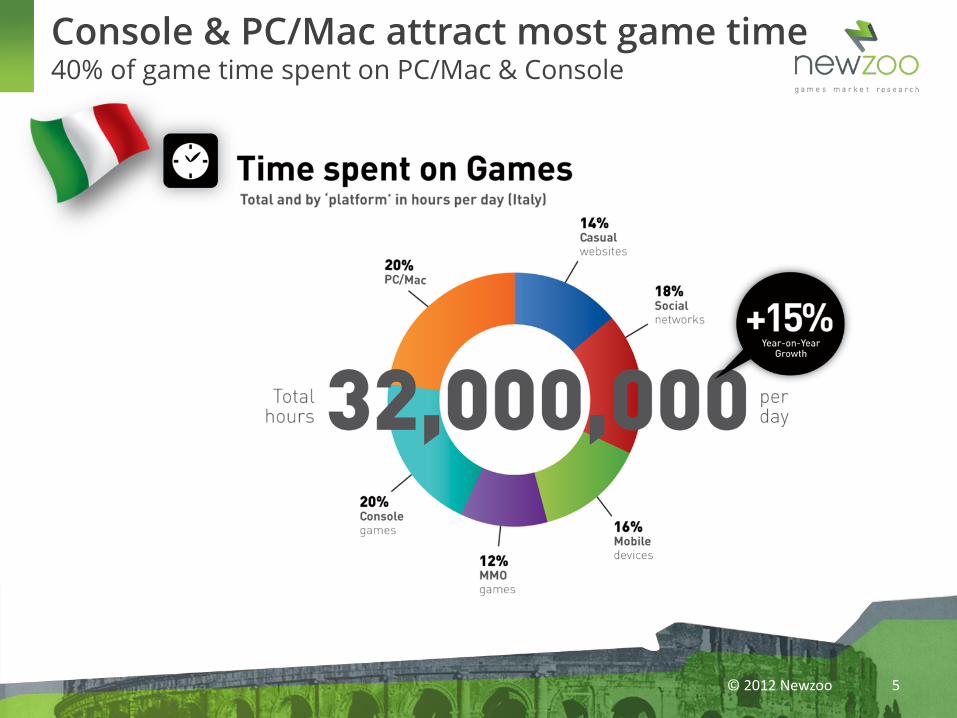

Console & PC/Mac attract most game time 40% of game time spent on PC/Mac & Console

© 2012 Newzoo 6

Console spending still important factor Consoles take 40% of money incl. second-hand, import, DLC

© 2012 Newzoo 7 © 2012 Newzoo 7

2. Key Trends Monitoring & Understanding Change

Monitoring Change | KPIs To size and seize future growth opportunities

Games Market Growth

Most reports on the games market focus on number of players and/or money. To monitor and understand the changes in the games market this is not enough, especially now free-to-play business models are becoming so dominant. We always also report on Time and number of Paying Gamers (Payers) to provide more perspective.

Key Growth Indicators | With Key Trends In Between

players

time payers

money

2011-2012

+8%

2011-2012

+18%

2011-2012

+3%

2011-2012

+15%

2011-2012

+16%

2011-2012

+19%

2011-2012

+6%

2011-2012

+17%

© 2012 Newzoo 9

Key Growth Indicators | With Key Trends In Between

players

time payers

money

access

screens

free

biz

z m

od

els

organisation

services

pro

fit

valu

e

© 2012 Newzoo 10

The 4 Key Trends

Luxembourg, here we are This place is about more than money….

screens

access

bizz models

free

organisation

service

profit

value

Consumers want continuous access games that are, in principle, free. Ideally, their game continuously improves and expands, as a service. If the game gives them value, they are more than willing to spend money.

Game companies need to make their games accessible via all screens as well as adapt their business models. The latter requires organisational change and a continuous balancing act between consumer value and company profit. Hard but it is the only way to remain profitable in this competitive market.

© 2012 Newzoo 11

“free-to-play is not a business model but a way

to run your business” - Peter Warman, CEO Newzoo

Key Take-Away Why big publishers struggle amidst all the change

© 2012 Newzoo 12

© 2012 Newzoo 13 © 2012 Newzoo 13

3. Gamers and their Screens Italy versus Europe

Consumers vs Screens Newzoo Screen Segmentation Model TM

22% of US gamers (2012) play on all four screens

21% of EU gamers (2012) play on all four screens

market growth All Screens Connected By: • Social Networks • The Cloud • The Real World

23% of Italian gamers (2012) play on all four screens

© 2012 Newzoo 14

940M euro

51%

70% payers

6.6M

17.1M players

92%

64% hrs/week

143M

The Computer Screen | 2012 Newzoo Screen Segmentation Model TM

487M euro

26%

72% payers

6.8M

11.9M players

64%

13% hrs/week

28.7M

The Entertainment Screen | 2012 Newzoo Screen Segmentation Model TM

140M euro

8%

32% payers

3.8M

12.1M players

65%

12% hrs/week

27.6M

The Personal Screen | 2012 Newzoo Screen Segmentation Model TM

272M euro

15%

46% payers

4.3M

7.5M players

40%

10% hrs/week

23.0M

The Floating Screen | 2012 Newzoo Screen Segmentation Model TM

© 2012 Newzoo 19 © 2012 Newzoo 19

4. Mobile Gaming Smartphones, Tablets & Handheld Consoles

Mobile Gaming | EU vs Italy 2012 Work in Progress | Smartphones vs Tablets vs Handhelds

Source: Newzoo Mobile Trend Report, October 2012

Smartphones

Tablets

Handheld consoles

46% 4.5M

25% 2.4M

9% 0.9M

7% 0.7M

5% 0.5M

2% 0.3M

6% 0.5M

Smartphones

Tablets

Handheld consoles

42% 26.4M

19% 12.1M

4% 2.4M

7% 4.1M

3% 1.9M

20% 12.3M

5% 3.2M

62.4M European* Gamers (47% of all gamers) |9.7M Italian Gamers (52%) Smartphone, Tablet or Handheld Console Gamers

* Aggregate of UK, GER, FR, NL, BE, IT

Rank Game Last Month Publisher

1 The Simpsons™: Tapped Out 425 Electronics Art

2 Kingdoms of Camelot: Battle for the North 2 Kabam

3 Clash of Clans 13 Supercell

4 CSR Racing 1 NaturalMotion

5 Poker by Zynga 5 Zynga

Top 5 Games Italy September 2012 Based on total iPad, iPhone and Google Play store revenues

Rank Game Last Month Publisher

1 Kingdoms of Camelot: Battle for the North 1 Kabam

2 Clash of Clans 5 Supercell

3 The Simpsons™: Tapped Out 479 Electronics Art

4 CSR Racing 2 NaturalMotion

5 Ice Age Village 3 Gameloft

Rank Game Last Month Publisher

1 Slotomania - slot machines 1 Playtika LTD

2 Ice Age Village 4 Gameloft

3 Airport City 3 Game Insight International

4 Rage of Bahamut 6 Mobage

5 Arcane Empires NEW Kabam

© 2012 Newzoo 21

© 2012 Newzoo/Distimo

© 2012 Newzoo 22

5. All Research Topics Available on the Italian games market

Demographics Base: Total online population aged 10-65 Gender Age Education* Income Work situation Home situation Hobbies and general interests

Media, Retail & Technology

Base: Total online population Media usage (print, radio, TV, social networks, internet) Social network preference* Mobile phone brand & provider Tablet brands: e.g. iPad, Kindle Fire, Galaxy Tab Use of tablet TV connectivity Preferred TV channels* Preferred generic websites* Preferred retail chains* General use of prepaid cards / gift vouchers / promotional codes

Game behaviour

Base: Total online population / gamers Total number of (non-)gamers Players per market segment: Casual game websites: e.g. Pogo, MiniClip, King.com, Yahoo Social networks: global and local Mobile devices: smartphones and tablets MMO games: F2P/P2P, Browser/Client Consoles: including Vita and DS PC/Mac: downloaded or boxed

*Country-specific topics

Newzoo Data Explorer Topics Consumer Insights across all game business models

Play frequency per marketsegment Time spent playing per market segment Genre preferences per market segment Players of key franchises, including Minecraft, World of Warcraft, Assassins Creed, FarmVille, FIFA, Sims, Bejeweled, GTA, Call of Duty, BattleField, League of Legends, World of Tanks, Zynga Poker, Bubble Shotter, Tetris.

Game spending Base: All gamers

Total number of (non-)paying gamers Paying players per market segment Average money spent per market segment Business model preference per market segment Preferred payment method per market segment

MMO-specific Base: MMO gamers

Free-to-play (F2P) versus Pay-to-Play (P2P) In-game spending in F2P / P2P Browser versus Client Number of MMO games played Preferred MMO type: e.g. RTS, RPG, Shooter, Sports, Battle Arena, Resource/Casual Preferred MMO genre: e.g. Fantasy, Sci-Fi, Realism, Anime, History Preferred MMO graphic style: e.g.2D, 3D, Side-scrolling.

Social/Casual-specific Base: All online casual or social gamers

Preferred online game destinations* Choice of social networks* Social networks as game destination Share of time on socialnetworks spent on games Social franchises: e.g. Ravenwood, Words with Friends Brand awareness of social publishers: e.g. Zynga, Wooga Number of social games played/ tried

© 2012 Newzoo 23

Newzoo Data Explorer Topics Consumer Insights across all game business models

Mobile-specific Base: All tablet and (smart)phone gamers

Mobile device used to play: e.g. tablet, smartphone, iPod Share of spending on multiple devices Popularity of mobile browser games Popularity of pre-installed games Popularity of download / app store games Download source for smartphones and tablets App stores used Share of up-front payment versus in-game spending Reasons for chosing a mobile game Cross-screen gaming: role of mobile device Number of mobile games played

PC/Mac and Console-specific Base: All PC/Mac and/or Console gamers

Boxed vs. Downloaded PC/Mac games Share of Boxed games in total PC/Mac spend Console used & owned Own or play for key franchises: e.g. Skyrim, GTA, CoD Download source PC/Mac games: e.g. Steam, Origin, Filesharing Buying games abroad/ import Share of pre-owned in total spending Share of digital downloads in total spending Importance of game extensions as buying reason

Fresh topics available from October 2012: Time spent on the internet divided over locations Time spent on the internet divided over screens Using/Subscription: Netflix/Digital TV/ Satellite TV/Pay TV/Spotify/Amazon Account Frequency watching TV and: read news paper or magazines, surf the web while TV is on, communicate online or via phone with friends, playing games Awareness new products: iPhone5, Windows 8 operating system, Small screen iPad, Google Nexus 7, Apple TV, Wii U, PlayStation 4, Microsoft Smart Glass, The new Microsoft Xbox, Ouya’s Video Game Console Buying intention: iPhone5, Windows 8 operating system, Small screen iPad, Google Nexus 7, Apple TV, Wii U, PlayStation 4, Microsoft Smart Glass, The new Microsoft Xbox, Ouya’s Video Game Console MMO portals visited past 6 months Populair MMO franchises played (e.g. WoW, LoL, Runescape, World of Tanks, Lineage) Statements about: Engagement Casual games versus TV Reasons to try a new social network game Social franchises played (e.g. FarmVille, CityVille, Words with Friends, MafiaWars, Ravenwood Fair) Brand awareness social game developers (e.g. Zynga, PopCap, Playfish, Wooga) Awareness brand or franchise (e.g. Chillingo, GREE, Mobage, Crime City, Rage of Bahamut, Where’s My Water?) General attitude towards brand or franchises (e.g. Chillingo, GREE, Mobage, Crime City, Rage of Bahamut, Where’s My Water?) Mobile franchises played (e.g. Angry Birds, Ice Age, Draw Something, Kingdoms of Camelot) Statements about: Opinion push notifications mobile games Statements about: Spending, timing and budget for mobile games Statements about: Preference of boxed vs. downloaded PC/Console games *Country-specific topics

Endless cross-analysis of all topics across 12+ countries in our Newzoo DataExplorer

US EU* UK GER FR IT ES BE NL RU BR PL TR AUS JP CN

© 2012 Newzoo 24

© 2012 Newzoo 25

6. Subscription offers Consumer Insights & Monthly Mobile Data

Consumer Research Data | Total Picture Analyze, create/export graphs online, based on >200 topics

Export to powerpoint or excel

Select topics & variables Select or compare countries Filters to cross analyze

relative and absolute numbers © 2012 Newzoo

© 2012 Newzoo 26

One year subscription | Free analysis support

€4,000 All Italian Data

Transactional Mobile Games Data Top 200 grossing and top 300 downloaded games (monthly)

Easily select the publisher and see their games in the top 200 gross ranking and top 300 free and paid ranking across all app stores.

Game by game revenues and downloads. Per country and per App store.

Over 30 datapoints per game.

© 2012 Newzoo/Distimo

Stores:

iPhone iPad PlayStore Amazon Windows 8

Early 2013:

© 2012 Newzoo 27

This monthly subscription will be upgraded to the Distimo AppIQ online dashboard early 2013. Excel product available now.

Contact us for the possibilities

© 2012 Newzoo 28

7. Newzoo & Contact Research, Client Portfolio & Contact Details

US EU* UK GER FR IT ES BE NL RU BR PL TR AUS JP CN

Newzoo research portfolio

Newzoo | The Total Picture Consumer, Transactional & Financial Data

© 2012 Newzoo 29

Several US clients cannot be

disclosed.

© 2012 Newzoo 30

Annelies in 't Veld Senior Manager Foreign Investments

City of Amsterdam | Economic Affairs [email protected], +31 (0)20 552 3204

Amsterdam, the perfect city for your game company

Four reasons why game companies such as PerfectWorld, Gamania and DeNA have chosen the Amsterdam Metropolitan Area for their European office. ■ Central location in Europe The Netherlands sits nicely and independently in between Europe’s largest markets: the UK, Germany and France and is known to be a perfect test market for new digital media products. ■ Excellent Infrastructure Amsterdam is home to the Amsterdam Internet Exchange, the world’s largest internet hub in terms of both traffic and members ■ Multilingual Workforce Amsterdam has always been very international in terms of people, languages and business. It is also easy to attract talent from other parts of Europe to spend some years in Amsterdam. ■ Financial Framework Many international companies, such as IKEA have set up their financial HQ in the Netherlands Please contact me to see what advantages apply to your specific situation.

Newzoo Partners Supporting your global business development

Nathan Salisbury Global Market Director - Gaming

GlobalCollect [email protected], +31 (0)23 567 1500

Payments Intelligence, the fastest way to increase your ROI

GlobalCollect is the worlds’ premier provider of local payment services. It processes payments across the globe for the majority of leading game publishers and distributors. > 15 million payments a month In July 2012 GlobalCollect processed over 15M gaming transactions

globally. Gaming payments data and benchmarks are available to clients based

on gaming platform, game type, monetization model and genre. Payment specific data includes global payment method popularity,

average transaction values, fraud benchmarks, currency volume, transaction volume figures etc.

GlobalCollect provides advice on paymentization practices including multi-acquirer management, automated re-routing capabilities and benchmarking for credit card processing to increase revenues.

Recent whitepaper Cross-Screen Monetization of Games http://info.globalcollect.com/monetization-of-games

Contact us Or buy directly online

Order subscriptions online on newzoo.com

Newzoo Wybe Schutte [email protected] +31 20 6635816

Or contact us

© 2012 Newzoo 31