nexia – eurostatus s.a. update on greek tax changes by charitini xydia

TRANSCRIPT

Nexia – Eurostatus S.A.Nexia – Eurostatus S.A.

Update on Greek Tax ChangesUpdate on Greek Tax Changes

by Charitini Xydiaby Charitini Xydia

New Tax Law 3842/2010“Restoration of fiscal justice and

confrontation of tax evasion”voted on April 15th 2010

1. Income Tax ( Personal and Corporate)2. Transfer Pricing3. Code of Books and Records4. Taxes on Capital 5. VAT

The new Law seeks to bring Fundamental Changes to the Greek Tax Framework and mainly to :

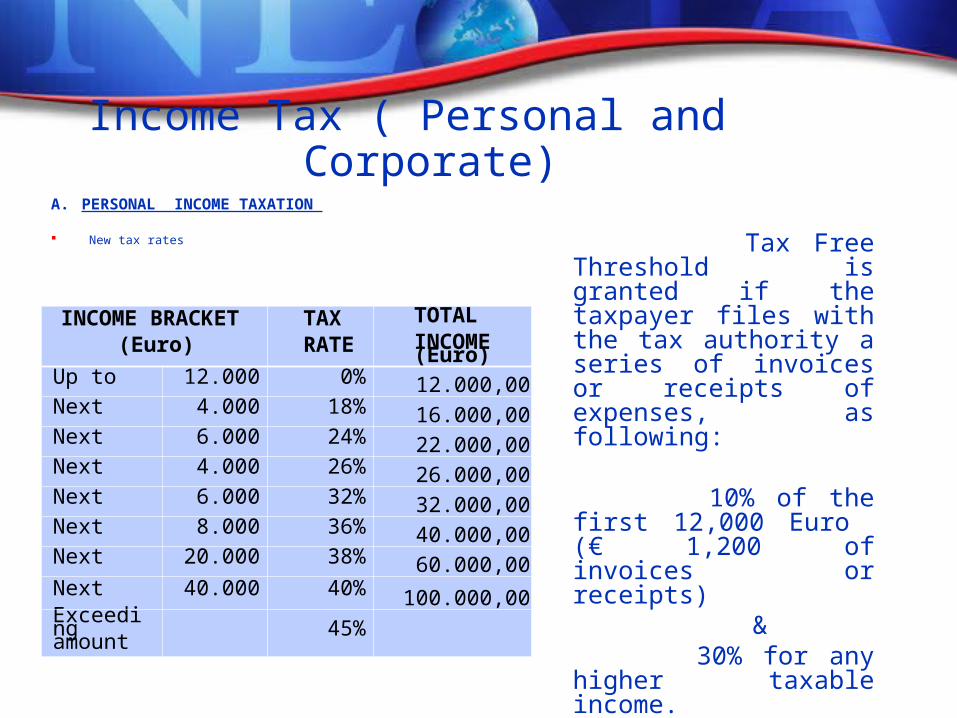

Income Tax ( Personal and Corporate)A. PERSONAL INCOME TAXATION

New tax rates

INCOME BRACKET (Euro)

TAX RATE

TOTAL INCOME (Euro)

Up to 12.000 0% 12.000,00Next 4.000 18% 16.000,00Next 6.000 24% 22.000,00Next 4.000 26% 26.000,00Next 6.000 32% 32.000,00Next 8.000 36% 40.000,00Next 20.000 38% 60.000,00Next 40.000 40% 100.000,00Exceeding amount 45%

Tax Free Threshold is granted if the taxpayer files with the tax authority a series of invoices or receipts of expenses, as following:

10% of the first 12,000 Euro (€ 1,200 of invoices or receipts)

& 30% for any higher taxable

income.

A. PERSONAL INCOME TAXATION

Calculation of deemed income on the basis of “Objective Living Expenses”

Main “Objective Living Expenses”: - General Annual objective living expenses standard is set at €3,000 for Singles and €5,000 for a married couple. - Surface of the primary and secondary residence (owned or rented) - Engine capacity of cars (owned or rented) - Aircrafts, vessels, swimming pool’s - private education, private schools tuitions fees, remuneration of house maids, private drivers, private teachers and other household personnel)

A. PERSONAL INCOME TAXATION Special Incentives

Encouragement for capital Repatriation for which there was either a declaration obligation or a tax payment liability in Greece, and

are deposited abroad by individuals or legal entities what are subject to Greek Taxation. Effective from 15.4.2010 and for 6 months The origin of the Capital in not examined

5% tax on the value of the deposits with exhaustion of any further tax liability if the capital is repatriated and placed in a time deposit in Greece for at least 1 year

8% tax on the value of the deposits with exhaustion of any further tax liability if the capital remains abroad.

50% tax refund if the capital in invested in Real Estate, Mutual Funds or Greek Bonds

A. PERSONAL INCOME TAXATION

For Free Lancers

As of 1.1.2010, net income of Architects and Engineers is determined based on Accounting Principles

Trading Losses are carried forward for 5 years to be offset against

profits As of 1.1.2011 freelancers income is considered as acquired upon

provision of the respective services, instead of the actual collection of their fees, to be in line with new VAT regulation

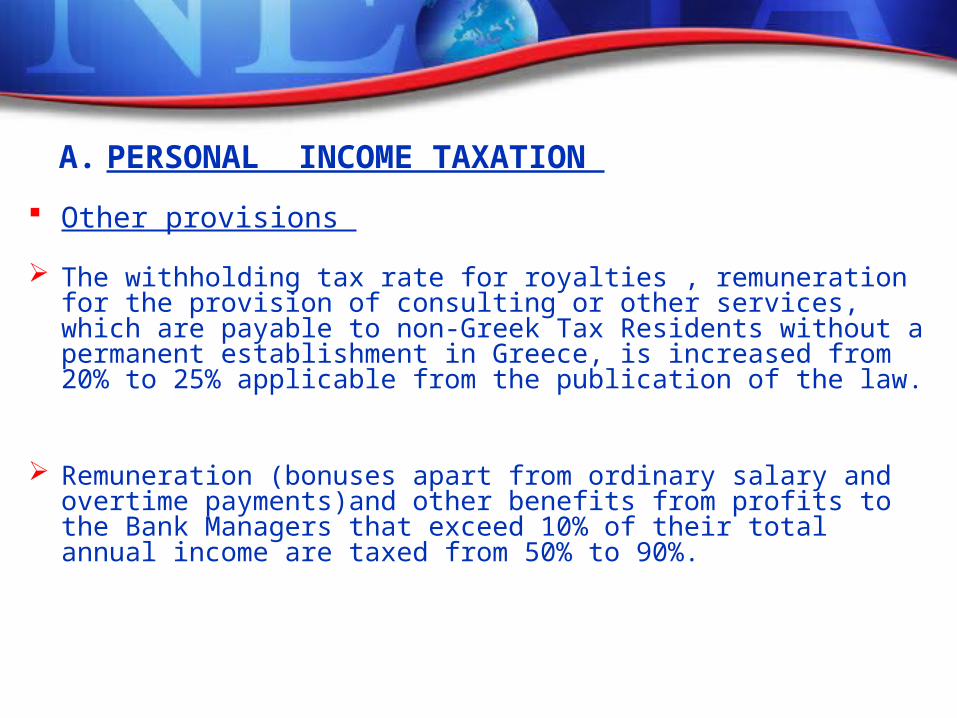

A. PERSONAL INCOME TAXATION

Other provisions

The withholding tax rate for royalties , remuneration for the provision of consulting or other services, which are payable to non-Greek Tax Residents without a permanent establishment in Greece, is increased from 20% to 25% applicable from the publication of the law.

Remuneration (bonuses apart from ordinary salary and overtime payments)and other benefits from profits to the Bank Managers that exceed 10% of their total annual income are taxed from 50% to 90%.

A. PERSONAL INCOME TAXATION Other provisions

Part of the Factory Value of the first year of circulation of rented or owned company cars is taxed as EMPLOYMENT INCOME of the individual that uses it (e.g. BoD members, directors etc), as follows:

Benefits deriving from STOCK OPTIONS is determined throw a new method: NOW: The stock exchange price taken into account is the one applicable at the time the right is actually exercised BEFORE : The one applicable at the time the right was granted. if the beneficiary has left the company due to retirement, change of employment etc the said benefit is taxed as

freelancers’ income.

Factory Value Income

15,000-22,000 15% F.V.

22.001-30.000 25% F.V.

>30.000 30% F.V.

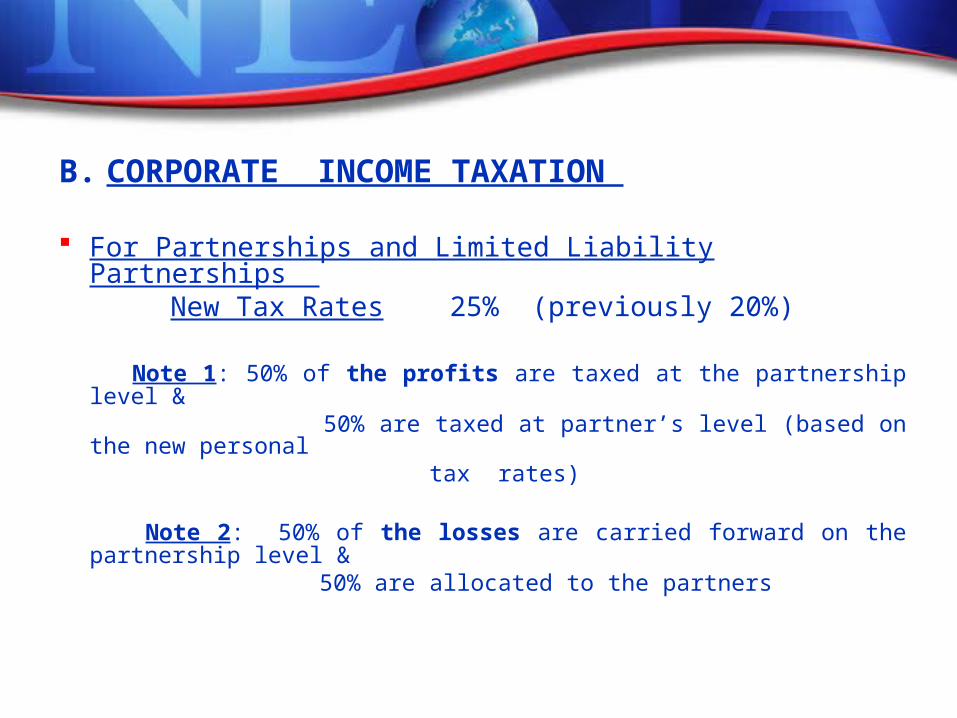

B. CORPORATE INCOME TAXATION

For Partnerships and Limited Liability Partnerships New Tax Rates 25% (previously 20%)

Note 1: 50% of the profits are taxed at the partnership level & 50% are taxed at partner’s level (based on the new personal tax rates)

Note 2: 50% of the losses are carried forward on the partnership level & 50% are allocated to the partners

B. CORPORATE INCOME TAXATION New Tax Rates For Limited Liability Companies (LTD) and Limited Liability

Companies with shares (Société Anonyme- SA)

Dividends: there is no withholding tax, but are tax under the general provisions of personal taxation for the shareholders, with the right to offset the corporate tax levied on these profits.

On Distributed or Capitalized Profits

40%

(NOTE: This is NOT a withholding tax on dividends, therefore the DTTs and Parent Subsidiary Directory is not applicable for

distribution of profits from Greek Companies to their EU or Treaty Members Shareholders

and the 40% Tax will still be paid!!)

B. CORPORATE INCOME TAXATIONDetermination of Enterprises’ Net Income

The gross income of Greek Companies selling goods through individuals or legal entities of any kind that are established in countries that do not co-operate with Greece regarding information exchange in taxation matters is increased when :

1. The Goods are sold to a foreign party –without having been originally transferred abroad- and are further resold to another Greek Company (Triangle Transaction) at a price greater that the one applicable to the original transaction. The difference between the two prices will be regarded as income for the Greek seller.

2. When the Goods are sold to the foreign company at a lower price than the one normally applicable the difference is regarded as gross income derived by the Greek Company.

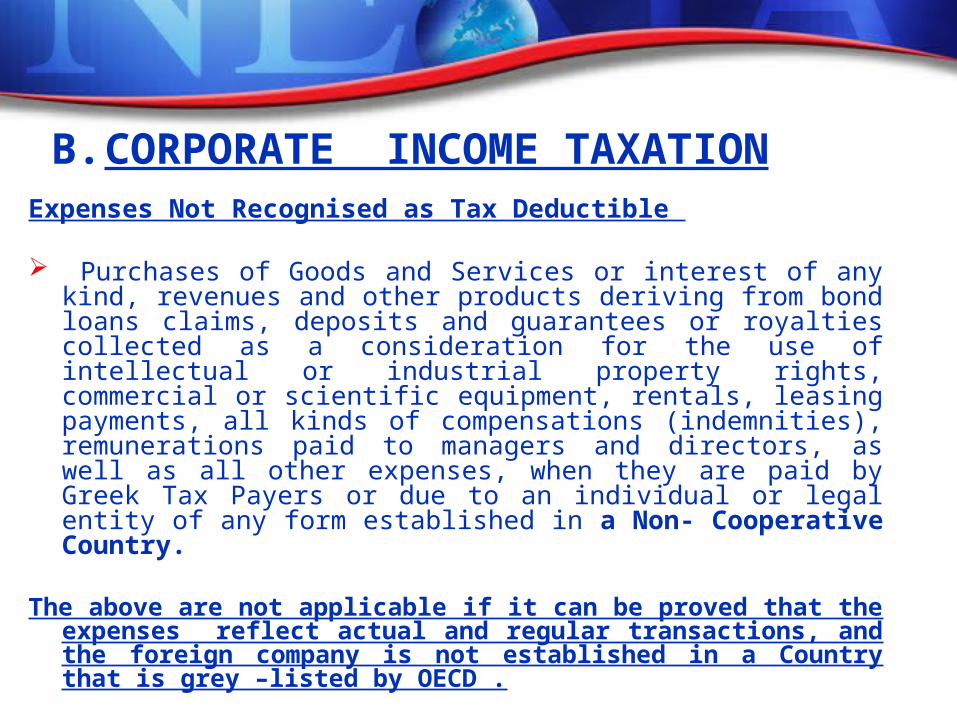

B. CORPORATE INCOME TAXATIONExpenses Not Recognised as Tax Deductible

Purchases of Goods and Services or interest of any kind, revenues and other products deriving from bond loans claims, deposits and guarantees or royalties collected as a consideration for the use of intellectual or industrial property rights, commercial or scientific equipment, rentals, leasing payments, all kinds of compensations (indemnities), remunerations paid to managers and directors, as well as all other expenses, when they are paid by Greek Tax Payers or due to an individual or legal entity of any form established in a Non- Cooperative Country.

The above are not applicable if it can be proved that the expenses reflect actual and regular transactions, and the foreign company is not established in a Country that is grey –listed by OECD .

B. CORPORATE INCOME TAXATIONDetermination of Enterprises’ Net Income

Countries that do not co-operate with Greece = Countries that are Grey Listed by the OECD Countries that have not entered into an administrative assistance agreement

with Greece or that do not respect it, and that will be determined by a decision issued by the Ministry of Finance or

Countries which are characterised by a beneficial tax regime.

Beneficial Tax Regime An entity is considered to be established in an beneficial tax regime even if the Company is established in a EU member-state either when it is tax exempt or when it is subject to income or capital tax amounting to less than 50% of the Tax applicable in Greece (i.e. Corporate tax rate < 10% )

B. CORPORATE INCOME TAXATION

Thin Capitalization Rules The scope of Thin Capitalization Rules is extended to bond loans and loans

granted by third parties for which guarantees of any kind have been provided by associated enterprises.

Interest is not deductible if intercompany loans exceed 3 times the net equity.

Interest is not deductable in case of financing acquisitions, if acquired shares are held less than 2 years.

This provisions does not apply to leasing companies, factoring companies finance companies and credit institutions operating in Greece.

2. TRANSFER PRICING

In case of sales of goods or provision of services between affiliate companies with the financial term varying from the terms usually agreed between independent parties, the profits that will not be earned by the company due to this reason will be considered as profits earned and will be added to the company's net profits.

Penalty for under/over invoicing/pricing is increased from 10% to 20% on additional net profits, without the right to settle the penalty to 1/3 and irrespective whether this over/under invoicing actually results to the avoidance of taxes.

The threshold is decreased from € 200.000 to € 100.000 Non, inadequate or late submissions are fined with 20% of the value of the

transactions not documented or not properly documented.

3. CODE OF BOOKS AND RECORDS

Most Entrepreneurs are obliged to keep accounting books, even if their annual income is less than € 5.000

e.g. Plumbers, Electricians, gas/petrol stations, kiosks, open-air market traders etc.

Invoices over €3,000 between entrepreneurs should be paid by check or through business bank accounts, NOT CASH.

Invoices over €1.500 for the sale of good to individuals should be paid by check, banks, credit or debit cards, NOT CASH.

4. TAXES ON CAPITALReal Estate Transfer taxes Abolishment of the Automatic Revaluation Tax and Transfer duty of 1% that

was imposed on real estate property acquired by the vendor after 1.1.2006. NEW REAL ESTATE TRASFER TAX RATES

8% for the first € 20,000 and 10% for the exceeding amount of the “objective” value of the property

Annual Real Estate Tax (FAP) Individuals

TOTAL VALUE BRACKET (Euro) TAX RATE

Up to 400.000 0%Next 100.000 0,1%Next 100.000 0,3%Next 100.000 0,6%Next 100.000 0,9%Exceeding amount 100.000 1,0%

Companies0.6% on the taxable value of any property owned by legal entities0.3% on the taxable value of any property owned by welfare, religious or education companies.0.33% for the hotels for 2010-2012

4. TAXES ON CAPITALSpecial Tax on Real Estate Property

15% (previously 3%)This is an additional tax imposed to the taxable value of real estate property

situated in Greece, owned by: legal entities established in Non-EU counties or in countries that Greece has

not signed an Administrative Mutual Assistance Agreement legal entities that do not disclose the physical persons that are the beneficial

owners of the company.

If the ultimate beneficial owner of the above companies is disclosed, the above tax is not due.

Special Provision: Within 6 months from the enforcement of the law, Real estate transfer which are performed by legal entities subject to this tax to physical persons are except from Capital Gains Tax, from the above Special tax on real estate property and from ½ of the donation tax or real estate transfer tax due.

5. VATNew Tax Rates as from 1.7.2010

Standard Rate : 23% (21% from 15 March – 30 June 2010

and 19% in the past)

Reduced Rate : 11% (10% from 15 March – 30 June 2010

(for basic consumer goods) and 9% in the past)

Reduced Rate: 5,5% (5% from 15 March – 30 June 2010

(for books, newspapers, magazines and 4.5% in the past)

and theatre tickets)

Special Reduced rates for certain Greek Islands (4-15%)

5. VAT Incorporation of Directive 2008/117/EC ( from 1.1.2010) Incorporation of Article 3 of Directive 2008/8/EC (from 1.1.2011) Harmonization of the VAT Code with Directive 2006/112/EC

Subject to VAT as from 1.7.2010:

Lawyers, Notary Publics, Non-salaried 23% Land registry officers and process serves

Medical Services (other than State

Hospitals or private doctors) 11% Writers, actors and art performers (for

services supplied to other taxable persons)

Charitini XydiaCharitini XydiaTel: 00 30 210 9008400Tel: 00 30 210 9008400

Email: Email: [email protected]

Nexia – Eurostatus S.A.Nexia – Eurostatus S.A.

THANK YOU THANK YOU

FOR YOUR ATTENTIONFOR YOUR ATTENTION