nielsen investor overview -...

TRANSCRIPT

This artwork was created using Nielsen data.

Copyright © 2018 The Nielsen Company (US), LLC. Confidential and proprietary. Do not distribute.

1Q 2018

NIELSEN INVESTOR OVERVIEW

2Cop

yri

gh

t ©

20

18

Th

e N

iels

en

Com

pa

ny (

US

), L

LC

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry. D

o n

ot d

istr

ibu

te.

FORWARD LOOKING STATEMENTSThe following discussion contains forward-looking statements, including those about Nielsen’s outlook and prospects, within

the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements are those which are not

historical facts and may be identified by words such as “will”, “intend” “expect”, “estimates,” “anticipates”, “should”, “could”,

“shall” and similar expressions. These and other statements that relate to future results and events are based on Nielsen’s

current expectations as of April 26, 2018.

These statements are subject to risks and uncertainties, and actual results and events could differ materially from what

presently is expected. Factors leading thereto may include, without limitation, general economic conditions, conditions in

the markets Nielsen is engaged in, behavior of customers, suppliers and competitors, technological developments, as well

as legal and regulatory rules affecting Nielsen’s business and specific risk factors discussed in press releases and public

filings made by Nielsen (including those described in the forward-looking statements can be found under the section

entitled “Part I—Item 1A. Risk Factors” of the company’s Annual Report on Form 10-K for the fiscal year ended December

31, 2017 and our other filings with the Securities and Exchange Commission). This list of factors is not intended to be

exhaustive. Such forward-looking statements only speak as of the date of these materials, and we assume no obligation to

update any written or oral forward-looking statement made by us or on our behalf as a result of new information, future

events or other factors, except as required by law.

Our outlook is provided for the purpose of providing information about current expectations for 2018 and our long term

framework.

NON-GAAP INFORMATION

The following discussion contains certain non-GAAP financial measures. See the Appendix for additional information

regarding the definition and use of these measures, including a reconciliation of these measures to financial information

presented in accordance with GAAP.

3Cop

yri

gh

t ©

20

18

Th

e N

iels

en

Com

pa

ny (

US

), L

LC

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry. D

o n

ot d

istr

ibu

te.

NIELSEN AT A GLANCE

Market Cap and Dividend Yield are reported as of 4/26/18

Adjusted EBITDA presented on a constant currency basis

Market Cap $11.4B

Cash Returned to Shareholders (2012-2017) $4.3B

2017 Total Company Revenue $6.6B

2017 Free Cash Flow $863M

2017 Adj. EBITDA Margin Growth 15bps

Dividend Yield 4.2%

Revenue Recurring in Nature ~70%

2017 Total Revenues

Measurement and analytics

for content, advertising and

activity for television, digital,

social and audio

Watch

2017 Revenue:

~$3.3B

Adj. EBITDA Margin: 44%

Watch

51%

Buy

49%

Market share

measurement and

analytics for fast moving

consumer goods,

manufacturers and

retailers

2017 Revenue:

~$3.2B

Adj. EBITDA Margin: 18%

Buy

FOCUS: DRIVE SHAREHOLDER VALUE THROUGH GROWTH, PROFITABILITY, AND FREE CASH FLOW

4Cop

yri

gh

t ©

20

18

Th

e N

iels

en

Com

pa

ny (

US

), L

LC

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry. D

o n

ot d

istr

ibu

te.

NIELSEN’S BUSINESS STRATEGY &

OBJECTIVES

QUALITY

INTEGRITY

NEUTRALITY

OUR VALUES

OPEN

CONNECTED

USEFUL

PERSONAL

OUR BRAND

Expand coverage of consumer purchase

behavior globally

Capture Total Audience across all screens and

platforms

Help clients understand how individuals’ viewing behavior impacts purchase behavior

BUY

WATCH

MARKETING EFFECTIVENESS

EXECUTION OF OUR STRATEGY DRIVES SHAREHOLDER VALUE

THROUGH THE CYCLES

5Cop

yri

gh

t ©

20

18

Th

e N

iels

en

Com

pa

ny (

US

), L

LC

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry. D

o n

ot d

istr

ibu

te.

WHY INVEST IN NIELSEN?

Unmatched global footprint of 100+ countries

“Mission critical” measurement and analytics embedded in client workflows

Syndicated, scalable products and services

Strategic investments to drive continued and future growth opportunities

Proven track record of growth and economic resilience

Strong free cash flow generation and compelling capital allocation strategy

WE ARE A GLOBAL, INDEPENDENT MEASUREMENT AND DATA

COMPANY FOR FAST MOVING CONSUMER GOODS AND MEDIA

6Cop

yri

gh

t ©

20

18

Th

e N

iels

en

Com

pa

ny (

US

), L

LC

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry. D

o n

ot d

istr

ibu

te.

OUR GLOBAL FOOTPRINT

Our focus is relentless on our pursuit to provide clients with the most complete understanding

of what consumers buy and watch in 100+ countries…

~20% of revenues in

emerging markets

Buy Coverage Only Watch & Buy Coverage

…UNDERSCORED BY A GLOBAL EMPLOYEE BASE OF TALENTED ASSOCIATES WE

WORK HARD TO ATTRACT, DEVELOP, AND RETAIN

7Cop

yri

gh

t ©

20

18

Th

e N

iels

en

Com

pa

ny (

US

), L

LC

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry. D

o n

ot d

istr

ibu

te.

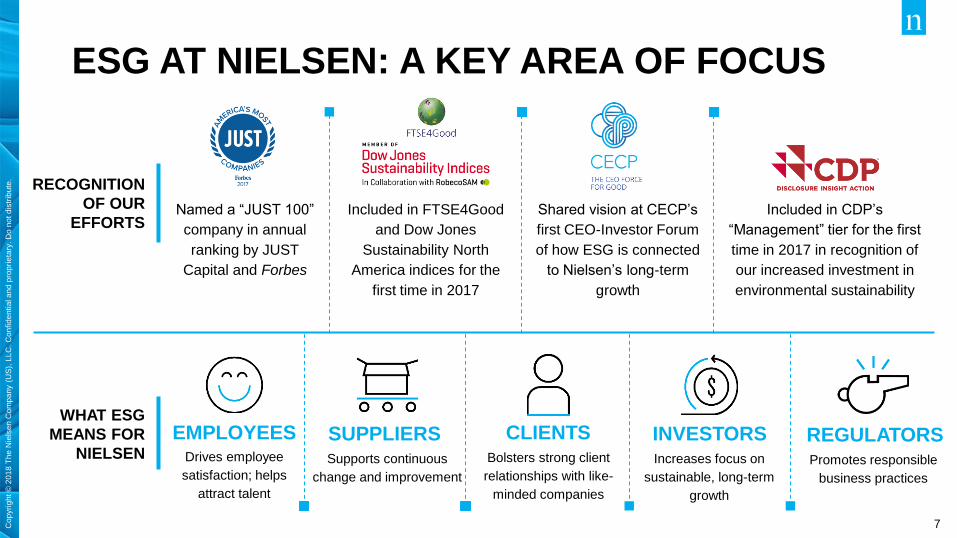

ESG AT NIELSEN: A KEY AREA OF FOCUS

EMPLOYEESDrives employee

satisfaction; helps

attract talent

INVESTORSIncreases focus on

sustainable, long-term

growth

REGULATORSPromotes responsible

business practices

SUPPLIERS Supports continuous

change and improvement

Named a “JUST 100”

company in annual

ranking by JUST

Capital and Forbes

Shared vision at CECP’s

first CEO-Investor Forum

of how ESG is connected

to Nielsen’s long-term

growth

Included in CDP’s

“Management” tier for the first

time in 2017 in recognition of

our increased investment in

environmental sustainability

WHAT ESG

MEANS FOR

NIELSEN

RECOGNITION

OF OUR

EFFORTSIncluded in FTSE4Good

and Dow Jones

Sustainability North

America indices for the

first time in 2017

Bolsters strong client

relationships with like-

minded companies

CLIENTS

8Cop

yri

gh

t ©

20

18

Th

e N

iels

en

Com

pa

ny (

US

), L

LC

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry. D

o n

ot d

istr

ibu

te.

LONG-TERM, BEST-IN-CLASS CLIENT BASE

BUY WATCH

• 20,000+ clients

• Relationships with top 5 clients

for over 30 years

• Long-term contracts provide

stable, recurring revenues –

average length of 3-7 years

• No client represents more than

4% of 2017 revenues.

HIGHLIGHTS

PARTNERSHIPS

FOR MORE THAN 90 YEARS, WE HAVE BEEN AT THE FOREFRONT OF MEASURING

CONSUMERS AROUND THE WORLD, HELPING CLIENTS DRIVE BETTER BUSINESS

DECISIONS AND PROFITABLE GROWTH OVER TIME

9Cop

yri

gh

t ©

20

18

Th

e N

iels

en

Com

pa

ny (

US

), L

LC

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry. D

o n

ot d

istr

ibu

te.

CREATING OPPORTUNITIES Driving growth and efficiency as our markets evolve

MARKET DYNAMICS

• Media fragmentation

• Ad spend shifting to digital

• Audience-based buying

• Growth in emerging markets

• Cost focus in developed markets

• Shift toward “always on” analytics

WATCH: Total Audience

BUY: Connected System

OPERATIONS: Automation

KEY STRATEGIC INITIATIVES

BUY

WATCH

LEVERAGING CHANGE AS A MEANS FOR PROGRESS

10Cop

yri

gh

t ©

20

18

Th

e N

iels

en

Com

pa

ny (

US

), L

LC

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry. D

o n

ot d

istr

ibu

te.

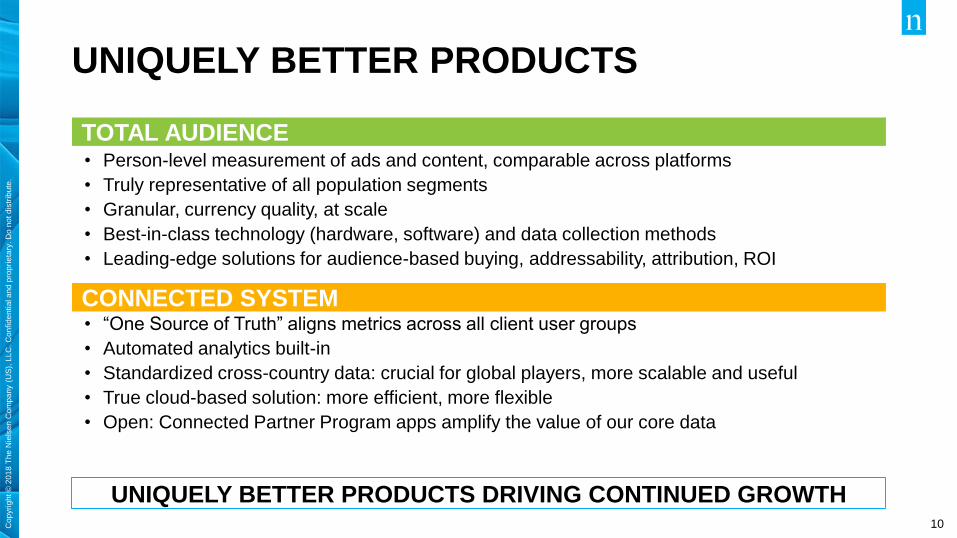

UNIQUELY BETTER PRODUCTS DRIVING CONTINUED GROWTH

UNIQUELY BETTER PRODUCTS

• Person-level measurement of ads and content, comparable across platforms

• Truly representative of all population segments

• Granular, currency quality, at scale

• Best-in-class technology (hardware, software) and data collection methods

• Leading-edge solutions for audience-based buying, addressability, attribution, ROI

• “One Source of Truth” aligns metrics across all client user groups

• Automated analytics built-in

• Standardized cross-country data: crucial for global players, more scalable and useful

• True cloud-based solution: more efficient, more flexible

• Open: Connected Partner Program apps amplify the value of our core data

CONNECTED SYSTEM

TOTAL AUDIENCE

11Cop

yri

gh

t ©

20

18

Th

e N

iels

en

Com

pa

ny (

US

), L

LC

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry. D

o n

ot d

istr

ibu

te.

DEPLOYING MARKET-TESTED, PROVEN CAPABILITIES

Automate data collection

Increased efficiency, speed, quality

EFFICIENCY: A GOLD MINE OF OPPORTUNITY

What are we doing? How are we doing it?

Automate data operations

Nano Meter, remote monitoring

Consolidate operations & platforms

Greater use of machine learning

$400M in annualized operations

& technology cost savings

by 2020

Automate Buy Data Collection

Super Hubs & Platforms

Connected System

Client Service Transformation

Centers of ExcellenceSG&A Efficiencies

Automate Watch Operations

$100Min annualized SG&A

cost savings by 2020

12Cop

yri

gh

t ©

20

18

Th

e N

iels

en

Com

pa

ny (

US

), L

LC

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry. D

o n

ot d

istr

ibu

te.

THE PATH TO 2020

GROWTH AND MARGIN EXPANSION FOR NIELSEN

DELIVERING INCREMENTAL VALUE FOR CLIENTS AND SHAREHOLDERS

Fundamental StrengthsUniquely Better

ProductsIncreased Efficiency

• Total Audience

• Connected System

• Integrated Analytics

• Gracenote

• Continuous innovation

• Automation

• Machine learning

• Super hubs

• Headcount productivity

• More scalable growth

• Global

• Complete coverage

• Wealth of metadata

• Unmatched client base

• Open approach

13Cop

yri

gh

t ©

20

18

Th

e N

iels

en

Com

pa

ny (

US

), L

LC

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry. D

o n

ot d

istr

ibu

te.

WATCH: MEASURING THE TOTAL

AUDIENCETotal 2017 Revenue: ~$3.3B… Over 80% recurring in nature

• Watch measurement capabilities in 59 countries

• Digital measurement, audience analytics and consumer research

• Grossed and de-duplicated total reporting across all devices,

access points and business models

• Separate measurement for content and ads

• Strategic relationships (Adobe, Experian, Facebook, Twitter, Roku,

DISH, Charter, Comcast, OpenAP)

• Gold standard, MRC accredited panel

• Marketing Effectiveness, fastest growing segment in 2017

69%

15%

11%

5%

Audience Measurement (Video & Text)

Audio

Marketing Effectiveness

Corporate/Other Watch

2017 Total Watch Revenue Breakdown

Video

Ratings

Audio

Ratings

Text

RatingsCross Platform Measurement

websitesprinted press

14Cop

yri

gh

t ©

20

18

Th

e N

iels

en

Com

pa

ny (

US

), L

LC

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry. D

o n

ot d

istr

ibu

te.

WATCH: MEASURING FRAGMENTING AUDIENCES

Total Audience Measurement: Only Nielsen

Digital in TV Ratings: Amazon Prime Video Channels, Verizon Fios, Philo

Digital Ad Ratings: Adopted by top 7 global agency holding companies

Expanding the currency: C3/C7 + DAR to cover linear & dynamic ads

Audience analytics: Leveraging Gracenote Smart TV data

15Cop

yri

gh

t ©

20

18

Th

e N

iels

en

Com

pa

ny (

US

), L

LC

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry. D

o n

ot d

istr

ibu

te.

TOTAL AUDIENCE FRAMEWORKFlexible Measurement Solutions for Content Ads

Consistent and

comparable metrics for

content and

ads provides

transparency for the

media ecosystem

CONTENT

MEASUREMENT

AD

MEASUREMENT

COMMERCIALS IN

CONTENT

MEASUREMENT

16Cop

yri

gh

t ©

20

18

Th

e N

iels

en

Com

pa

ny (

US

), L

LC

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry. D

o n

ot d

istr

ibu

te.

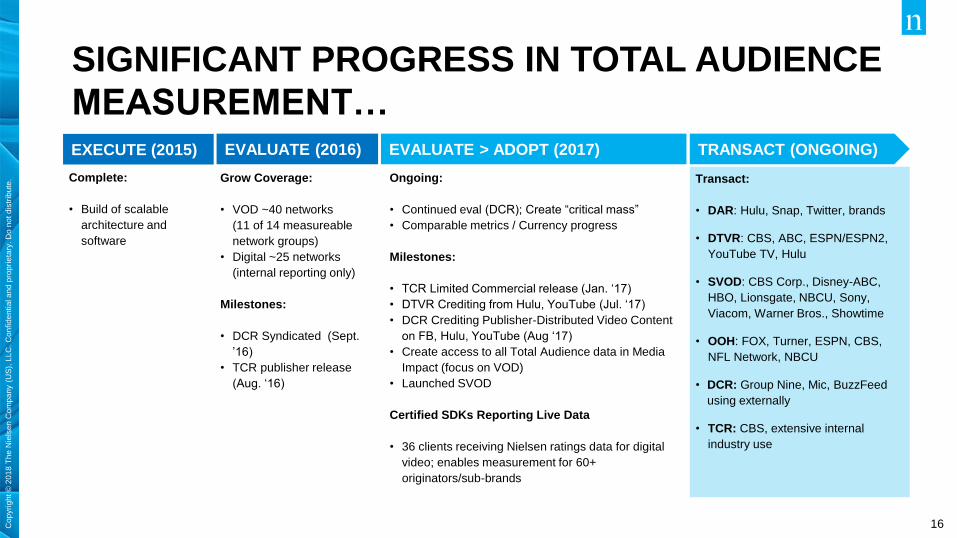

SIGNIFICANT PROGRESS IN TOTAL AUDIENCE

MEASUREMENT…

Complete:

• Build of scalable

architecture and

software

Grow Coverage:

• VOD ~40 networks

(11 of 14 measureable

network groups)

• Digital ~25 networks

(internal reporting only)

Milestones:

• DCR Syndicated (Sept.

’16)

• TCR publisher release

(Aug. ‘16)

Ongoing:

• Continued eval (DCR); Create “critical mass”

• Comparable metrics / Currency progress

Milestones:

• TCR Limited Commercial release (Jan. ‘17)

• DTVR Crediting from Hulu, YouTube (Jul. ‘17)

• DCR Crediting Publisher-Distributed Video Content

on FB, Hulu, YouTube (Aug ‘17)

• Create access to all Total Audience data in Media

Impact (focus on VOD)

• Launched SVOD

Certified SDKs Reporting Live Data

• 36 clients receiving Nielsen ratings data for digital

video; enables measurement for 60+

originators/sub-brands

Transact:

• DAR: Hulu, Snap, Twitter, brands

• DTVR: CBS, ABC, ESPN/ESPN2,

YouTube TV, Hulu

• SVOD: CBS Corp., Disney-ABC,

HBO, Lionsgate, NBCU, Sony,

Viacom, Warner Bros., Showtime

• OOH: FOX, Turner, ESPN, CBS,

NFL Network, NBCU

• DCR: Group Nine, Mic, BuzzFeed

using externally

• TCR: CBS, extensive internal

industry use

EXECUTE (2015) EVALUATE (2016) EVALUATE > ADOPT (2017) TRANSACT (ONGOING)

17Cop

yri

gh

t ©

20

18

Th

e N

iels

en

Com

pa

ny (

US

), L

LC

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry. D

o n

ot d

istr

ibu

te.

NIELSEN HAS ALIGNED TO SERVE

THE MODERN MEDIA ECOSYSTEM

TRADITIONAL/REACH

ADVERTISING

(LINEAR BUYS)

COMPARABLE CROSS PLATFORM REACH (POPULATION)

EFFECTIVENESS & ROI

AUDIENCE VALIDATION

TARGETED ADVERTISING

(AUDIENCE BUYS)

MEDIA OWNER AGENCY ADVERTISER

NO ADVERTISING

(SUBSCRIPTIONS)

Subscriber

DISTRIBUTOR

AD

BRANDED INTEGRATIONS

(PRODUCT PLACEMENT)

CONTENT (AD)CONTENT

Pet-Lover

AD

Beer Drinker

AD

Avid Hiker

AD

Car Buyer

[

AD+ + +

18Cop

yri

gh

t ©

20

18

Th

e N

iels

en

Com

pa

ny (

US

), L

LC

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry. D

o n

ot d

istr

ibu

te.

AUDIENCE BUYING IN LINEAR TV DEPENDS ON

NIELSEN DATA…

AUDIENCE

SEGMENTS

AUDIENCE

MEASUREMENT

TV INVENTORY

Other 3rd Parties

19Cop

yri

gh

t ©

20

18

Th

e N

iels

en

Com

pa

ny (

US

), L

LC

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry. D

o n

ot d

istr

ibu

te.

INVESTING TO SUPPORT AUDIENCE

BUYING IN DIGITAL

REACH VALIDATION ROI MEASUREMENTPLANNING & ACTIVATION

DIGITAL AD

RATINGS

MARKETING CLOUD

20Cop

yri

gh

t ©

20

18

Th

e N

iels

en

Com

pa

ny (

US

), L

LC

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry. D

o n

ot d

istr

ibu

te.

MARKETING EFFECTIVENESS FRAMEWORKNielsen Marketing Effectiveness framework leverages best in class data, technology and analytics to

provide our clients the resources they need to answer their business questions.

ACTIVATE MEASURE PERFORMANCE MEASURE OUTCOME

Brand Effect:

Creative, Competitive and

media impact

Digital & Total Ad

Ratings:

Reach, Frequency and

Audience Verification

PLAN

Ad Intel:

Competitive Intelligence for

Cross-Media Advertising

Consumer Neuroscience:

Copy quality and creative

drivers

NCS Sales Effect:

Campaign level sales

performance and drivers

Multi-Touch Attribution:

Media measurement across

Paid and Owned digital

touch-points

Marketing Mix:

Holistic Marketing Plan

evaluation across all

channels

Nielsen Catalina

Solutions: Audience

Segments for Targeted

Advertising

Nielsen Marketing

Cloud: DMP

Manage aggregated first

and third party data

SUPPORTING EVERY STEP OF CAMPAIGN MEASUREMENT

21Cop

yri

gh

t ©

20

18

Th

e N

iels

en

Com

pa

ny (

US

), L

LC

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry. D

o n

ot d

istr

ibu

te.

KEY MESSAGES

ONLY NIELSEN CAN

Nielsen will be the digital currency

Nielsen will further expand the definition of TV currency in 2018

Nielsen has invested in key areas to drive future high-margin growth

22Cop

yri

gh

t ©

20

18

Th

e N

iels

en

Com

pa

ny (

US

), L

LC

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry. D

o n

ot d

istr

ibu

te.

BUY: MEASURING THE TOTAL CONSUMERTotal 2017 Revenue: ~$3.2B… Approximately 60% recurring in nature

Retail sales measurement, market share information

and advanced analytical capabilities

• Presence in 100+ countries

• Measure billions of monthly point-of-sale transactions

• Store level data from nearly 2 million stores,

supplemented from proprietary household level data

from 240K households

• Demand for Everyday Analytics: Pricing, Promotion and

Assortment

Developed

Corporate

62%

36%2%

2017 Total Buy Revenue

Emerging

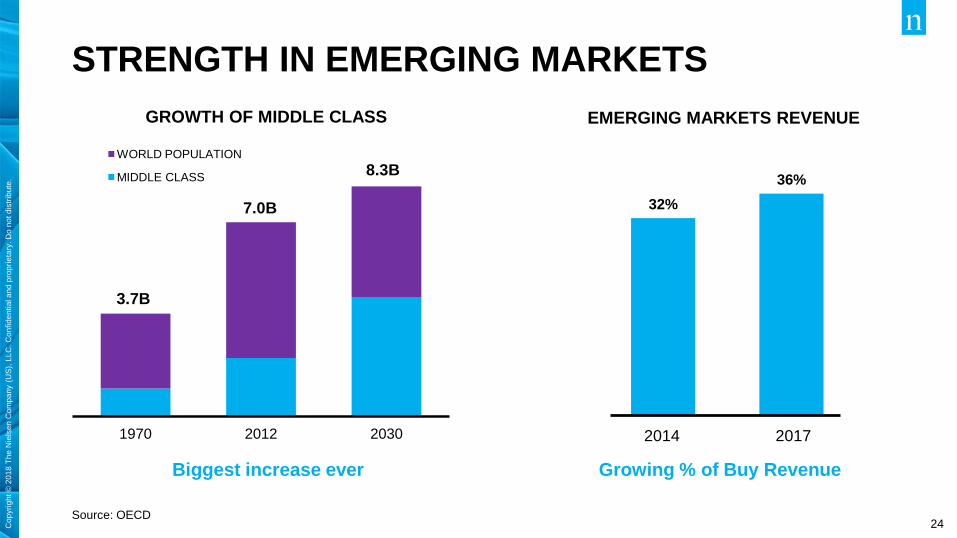

GROWTH THROUGH DIFFERENTIATION, STICKINESS, & SCALE

23Cop

yri

gh

t ©

20

18

Th

e N

iels

en

Com

pa

ny (

US

), L

LC

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry. D

o n

ot d

istr

ibu

te.

BUY: TRANSFORMATION PROGRESSING

Connected System

• On track to engage with 100 clients by the end of 2018

• Connected Partner Program…45 partners, usage growing

• 219 clients using at least one component of the Connected System

Key wins with retailers

• “Walmart One Version of Truth” launched February 1st

o 50+ manufacturers signed up…global and regional brands

• Expanded Sam’s Club relationship

Total Consumer Measurement

• Total Food offering provides view of total store

• E-commerce…aligning offline and online sales for total consumer view

Key Growth Initiatives

• Balanced client portfolio, global footprint…key competitive advantages

• Ongoing investments in measurement coverage and penetration

Emerging Markets

24Cop

yri

gh

t ©

20

18

Th

e N

iels

en

Com

pa

ny (

US

), L

LC

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry. D

o n

ot d

istr

ibu

te.

STRENGTH IN EMERGING MARKETS

Source: OECD

Growing % of Buy Revenue

1970 2012 2030

WORLD POPULATION

MIDDLE CLASS

~36%

LOCALS

~64%

GLOBAL

MNCs

Biggest increase ever

3.7B

7.0B

8.3B

GROWTH OF MIDDLE CLASS EMERGING MARKETS REVENUE

32%

36%

20172014

25Cop

yri

gh

t ©

20

18

Th

e N

iels

en

Com

pa

ny (

US

), L

LC

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry. D

o n

ot d

istr

ibu

te.

INNOVATING TO CAPITALIZE ON MARKET

TRANSFORMATION

KEY MARKET TRENDS

1. Long-tail and store brands growth

2. Shift to green/organic

3. Retail disruption: e-commerce,

omni-channel, discounters

4. Personalization driving analytics

& data integration

5. Zero-based budgeting

THE CONNECTED SYSTEM

WHAT’S HAPPENING?

WHY?WHAT NEXT?

DATA EXCHANGE

26Cop

yri

gh

t ©

20

18

Th

e N

iels

en

Com

pa

ny (

US

), L

LC

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry. D

o n

ot d

istr

ibu

te.

CONNECTED SYSTEM

BUSINESS INTELLIGENCE & VISUALIZATION APPS

DATA ENRICHMENT & INTEGRATION APPS

API

DATA

NIELSEN

CONNECTED

PARTNER DATA

TOTAL

CONSUMER

TOTAL

AUDIENCE

CLIENT

DATA

PUBLIC

DATA

ECOSYSTEM

What’s

Next? PLANNING, SIMULATION & ACTIVATION APPS

What’s

Happening

& Why

What’s

Happening

Data

Exchange

PERFECTLY ALIGNED WITH CLIENT NEEDS

27Cop

yri

gh

t ©

20

18

Th

e N

iels

en

Com

pa

ny (

US

), L

LC

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry. D

o n

ot d

istr

ibu

te.

CONNECTED SYSTEM: ONGOING, AGILE

DEVELOPMENT AND ROLLOUT

Build the foundations with

charter clientsEngaged with 25 clients Expand to engage with

~100 clients

2016 2017 2018

28Cop

yri

gh

t ©

20

18

Th

e N

iels

en

Com

pa

ny (

US

), L

LC

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry. D

o n

ot d

istr

ibu

te.

CONNECTED SYSTEM: RETURNING

DEVELOPED BUY MARKETS TO GROWTH

Client Wins

Connected

Partner

Program

Increased

Analytics

Penetration

(Europe)

29Cop

yri

gh

t ©

20

18

Th

e N

iels

en

Com

pa

ny (

US

), L

LC

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry. D

o n

ot d

istr

ibu

te.

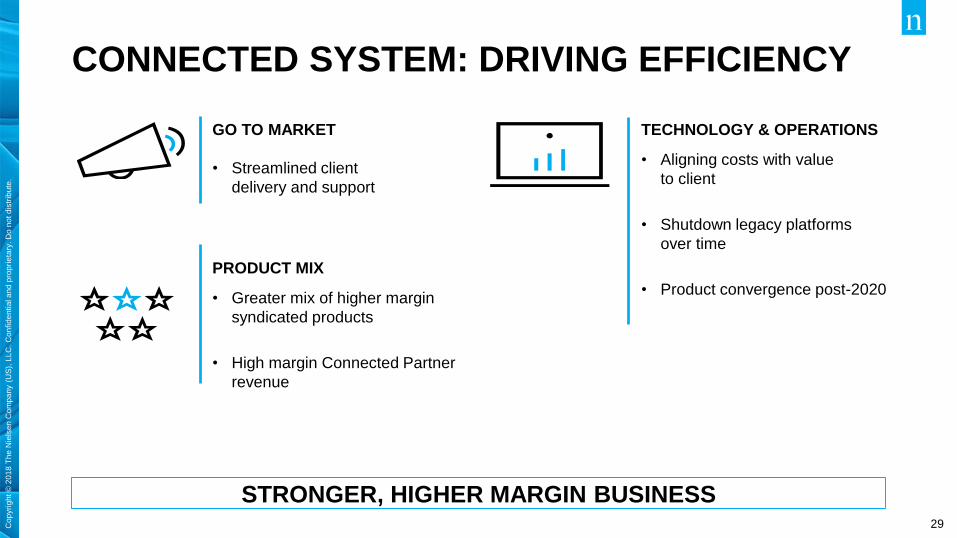

CONNECTED SYSTEM: DRIVING EFFICIENCY

GO TO MARKET

• Streamlined client

delivery and support

PRODUCT MIX

• Greater mix of higher margin

syndicated products

• High margin Connected Partner

revenue

TECHNOLOGY & OPERATIONS

• Aligning costs with value

to client

• Shutdown legacy platforms

over time

• Product convergence post-2020

STRONGER, HIGHER MARGIN BUSINESS

30Cop

yri

gh

t ©

20

18

Th

e N

iels

en

Com

pa

ny (

US

), L

LC

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry. D

o n

ot d

istr

ibu

te.

TOTAL CONSUMER

Source: Nielsen e-commerce measurement, 52 weeks ending July 1, 2017. Projected from ~1MM e-commerce FMCG consumers and cooperating ePOS

retailers based on reported commodity groups that may not match prior custom or syndicated category definitions.

27%

26%

13%

11%

9%

3%

2%

2%

1%

1%

1%

1%

Beauty Care

Pet Care

Health Care

Personal Care

Household Care

Packaged Grocery

Produce

Meat

Dairy

Beer and Wine

Bakery

Frozen Foods

NON-FOOD

FOOD & BEVERAGE

2017 ACCOMPLISHMENTS

E-commerce launched in the US

E-commerce measurement

available in 17 countries

Expanded traditional trade

coverage

Measuring discount channel

with consumer-sourced data

E-COMMERCE SHARE OF SALES

31Cop

yri

gh

t ©

20

18

Th

e N

iels

en

Com

pa

ny (

US

), L

LC

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry. D

o n

ot d

istr

ibu

te.

KEY MESSAGES

Strength in Emerging Markets

Connected System positioned to drive growth and efficiency

Expanding coverage through Total Consumer initiatives

Transformative wins enhancing value for retailers/manufacturers

THIS IS NIELSEN BUY 2020

32

This artwork was created using Nielsen data.

Copyright © 2018 The Nielsen Company (US), LLC. Confidential and proprietary. Do not distribute.

FINANCIALS

33Cop

yri

gh

t ©

20

18

Th

e N

iels

en

Com

pa

ny (

US

), L

LC

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry. D

o n

ot d

istr

ibu

te.

COMPELLING FINANCIAL PERFORMANCE: 2012-2017

Note: revenue CAGR represented in constant currency

REVENUE GROWTH

• 6% CAGR

• 47 quarters of consecutive growth

• Investing in growth platforms

FREE CASH FLOW

• 15% CAGR

• $4.3B generated 2012-2017

CAPITAL ALLOCATION

• ~$3.6B returned to shareholders

• Tremendous flexibility to invest in growth

• Tuck-in M&A

• New product launches

MARGIN EXPANSION

• ~3.1 pts of EBITDA margin expansion

• Disciplined pricing

• Efficiency and cost out

FREE CASH FLOW CAPITAL ALLOCATION

REVENUE GROWTH MARGIN EXPANSION

DELIVERING STRONG RETURNS

34Cop

yri

gh

t ©

20

18

Th

e N

iels

en

Com

pa

ny (

US

), L

LC

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry. D

o n

ot d

istr

ibu

te.

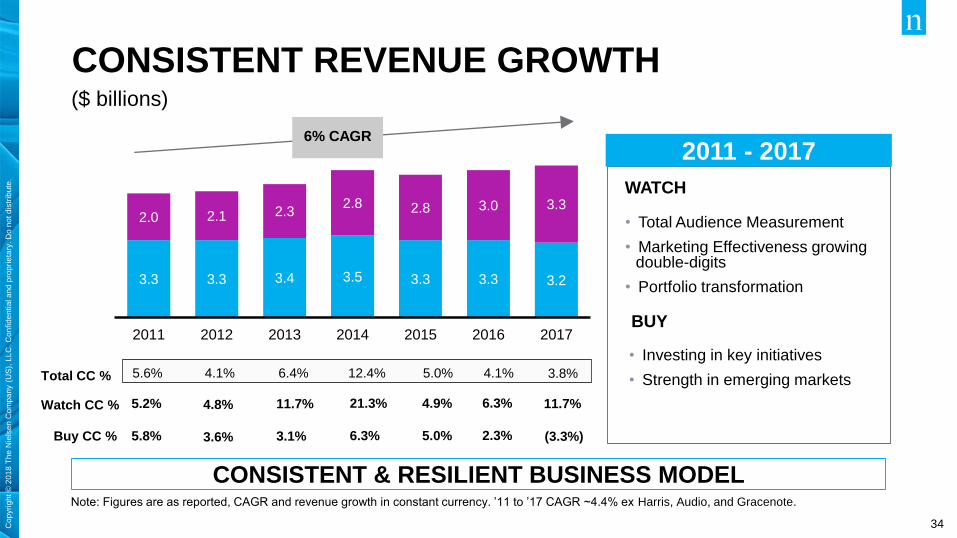

CONSISTENT REVENUE GROWTH($ billions)

Note: Figures are as reported, CAGR and revenue growth in constant currency. ’11 to ’17 CAGR ~4.4% ex Harris, Audio, and Gracenote.

6% CAGR

Total CC % 5.6% 4.1% 6.4% 12.4% 5.0% 4.1%

Watch CC % 5.2% 4.8% 11.7% 21.3% 4.9% 6.3%

Buy CC % 5.8% 3.6% 3.1% 6.3% 5.0% 2.3%

3.3 3.3 3.4 3.5 3.3 3.3 3.2

2.0 2.1 2.32.8 2.8 3.0 3.3

2011 2012 2013 2014 2015 2016 2017BUY

WATCH

• Investing in key initiatives

• Strength in emerging markets

• Total Audience Measurement

• Marketing Effectiveness growing double-digits

• Portfolio transformation

2011 - 2017

3.8%

11.7%

(3.3%)

CONSISTENT & RESILIENT BUSINESS MODEL

35Cop

yri

gh

t ©

20

18

Th

e N

iels

en

Com

pa

ny (

US

), L

LC

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry. D

o n

ot d

istr

ibu

te.

2018 BUY REVENUE FRAMEWORK(Percentages reflected as constant currency)

Emerging Markets: 8-10%

+ Coverage and penetration

+ Strong market demographic and income trends

+ Local and multinationals are investing

Developed Markets: (2)% to (4)%

- Low growth environment for large manufacturers

- Competitive environment pressuring clients

• Hard discounters

• Smaller brands gaining share

+ More investment in retail data and analytics

Corporate: ~(50)%

- Carryover from 2017 pruning activities

KEY DYNAMICS

(1)% to 1%

2017

$3.2B

2018E: TOTAL BUY (1)% TO 1%

36Cop

yri

gh

t ©

20

18

Th

e N

iels

en

Com

pa

ny (

US

), L

LC

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry. D

o n

ot d

istr

ibu

te.

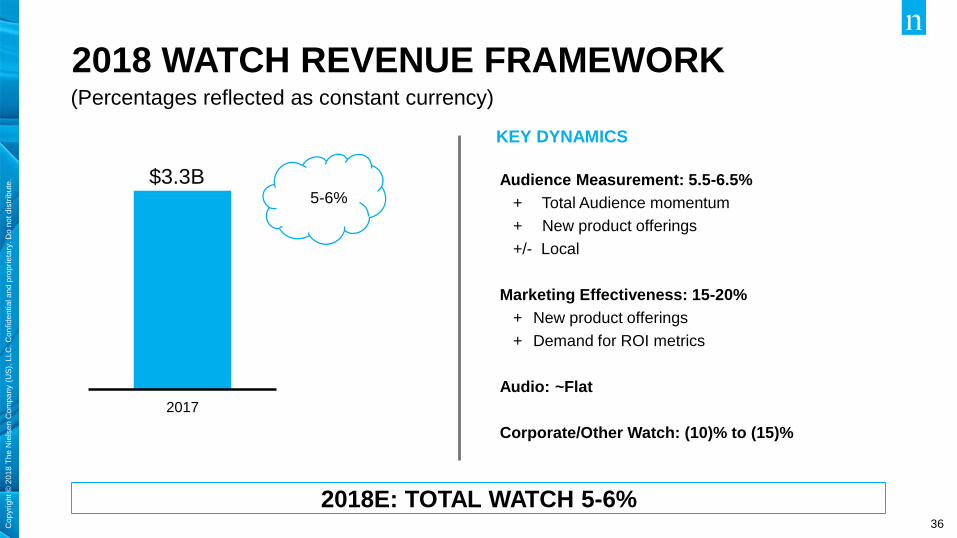

2018 WATCH REVENUE FRAMEWORK(Percentages reflected as constant currency)

KEY DYNAMICS

2017

$3.3B Audience Measurement: 5.5-6.5%

+ Total Audience momentum

+ New product offerings

+/- Local

Marketing Effectiveness: 15-20%

+ New product offerings

+ Demand for ROI metrics

Audio: ~Flat

Corporate/Other Watch: (10)% to (15)%

5-6%

2018E: TOTAL WATCH 5-6%

37Cop

yri

gh

t ©

20

18

Th

e N

iels

en

Com

pa

ny (

US

), L

LC

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry. D

o n

ot d

istr

ibu

te.

2018 MARGIN DRIVERS

2017

Adj. EBITDA

Margin

2018E

Adj. EBITDA

Margin

RETAILER

INVESTMENTS

(140) bps

Walmart

E-Commerce

PRODUCT

INVESTMENTS

(30) bps

Total Audience

Connected

System

110 bps

Automation

Super Hubs

Digitizing data

collection

NET EFFICIENCY GROWTH INITIATIVES

31%

~(60) bps

Constant

currency

INVESTING FOR EFFICIENCY AND GROWTH

38Cop

yri

gh

t ©

20

18

Th

e N

iels

en

Com

pa

ny (

US

), L

LC

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry. D

o n

ot d

istr

ibu

te.

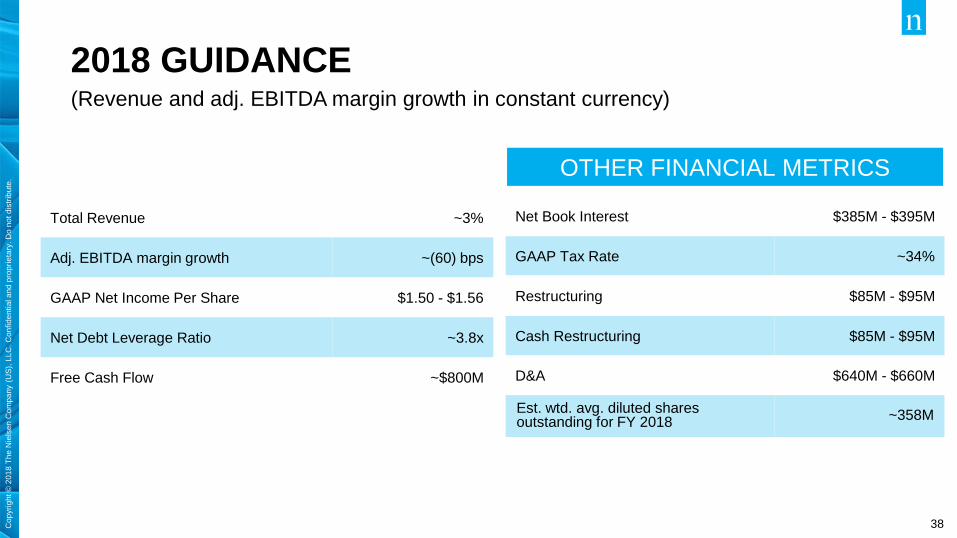

2018 GUIDANCE(Revenue and adj. EBITDA margin growth in constant currency)

Net Book Interest $385M - $395M

GAAP Tax Rate ~34%

Restructuring $85M - $95M

Cash Restructuring $85M - $95M

D&A $640M - $660M

Est. wtd. avg. diluted shares outstanding for FY 2018

~358M

Total Revenue ~3%

Adj. EBITDA margin growth ~(60) bps

GAAP Net Income Per Share $1.50 - $1.56

Net Debt Leverage Ratio ~3.8x

Free Cash Flow ~$800M

OTHER FINANCIAL METRICS

39Cop

yri

gh

t ©

20

18

Th

e N

iels

en

Com

pa

ny (

US

), L

LC

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry. D

o n

ot d

istr

ibu

te.

310

180

4060

140140

80

-20

3050

1Q18 2Q18E 3Q18E 4Q18E FY18E

Rev (bps) EBITDA (bps)

FOREIGN CURRENCY IMPACT

(a) Projected impact assumes rates in effect at 04/25/18 remain in effect for the balance of 2018.

Note: We report on a constant currency basis to reflect operating performance

57%

11%

3%3%3%

23%

USD EUR CNY CAD GBP Other

CURRENCY PROFILE - REVENUEPROJECTED FX IMPACT(a):

REPORTED VS CONSTANT CURRENCY

40Cop

yri

gh

t ©

20

18

Th

e N

iels

en

Com

pa

ny (

US

), L

LC

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry. D

o n

ot d

istr

ibu

te.

~$2

2017 2020E

31%

~35%

2017 2020E

~$3B

2018E - 2020E

2017 2020E

THE PATH TO 2020

$1.20

Grow revenue

• Drive mid-single digit growth

• Execute on growth initiatives

Expand margins… Efficiency

• ~+4pts by 2020

• Consolidate operations centers

• Automation and innovation

• Reduce SG&A

Deploy capital to create value

• Bolster growth via tuck-in M&A & capex

• Grow dividend in line with earnings

• Deploy excess capital to share repurchase

THREE PILLARSREVENUE

CUMULATIVE FREE CASH FLOW GAAP EPSDouble-digit

CAGR

EBITDA MARGINS~4%

CAGR

~+4

points

$6.6B

~$7.4B I.

II.

III.

Note: CAGR represented in constant currency

*Excluding impact of Tax Cuts and Jobs Act (“TCJA”), FY 2017 NI per share was $1.49

41Cop

yri

gh

t ©

20

18

Th

e N

iels

en

Com

pa

ny (

US

), L

LC

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry. D

o n

ot d

istr

ibu

te.

THE PATH TO 2020: GROW REVENUE

BUY

• Emerging Markets: high-single digit growth

• Developed Markets: return to growth

• Connected System

• Retailers

• Coverage: E-commerce

WATCH

• AM of Video & Text: mid-single digit growth

• Total Audience Measurement

• Digital Currency

• Audience-based Buying

• Marketing Effectiveness: double-digit growth

• New product launches

• Tuck-in M&A

• Audio: flat

GROWTH PLAYBOOK

2017 2020E

WATCH BUY

$6.6B

~$7.4B~4%

CAGR

(Percentages reflected as constant currency)

42Cop

yri

gh

t ©

20

18

Th

e N

iels

en

Com

pa

ny (

US

), L

LC

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry. D

o n

ot d

istr

ibu

te.

THE PATH TO 2020: EXPAND MARGINS

2017 2020E

~35%

Adjusted EBITDA Margin

• ~$500M in annualized cost savings by 2020E

• ~$280M cumulative restructuring from 2018E-2020E

OPERATIONS & TECHNOLOGY:

~$400M in cost out

• Automation/innovation

• Platforms and Super Hubs

SG&A: ~$100M in cost out

• Connected System + Client Service transformation

• Reduce corporate costs

• Leverage shared centers of excellence

SEGMENT DYNAMICS

• Watch: ~+2-2.5 points by 2020

• Buy: ~+4 points by 2020

PERMANENTLY REDUCING OPERATING COSTS

31%

~+4

points

DRIVING EFFICIENCY…WELL-DEFINED PROJECTS… FULL MANAGEMENT COMMITTMENT

43Cop

yri

gh

t ©

20

18

Th

e N

iels

en

Com

pa

ny (

US

), L

LC

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry. D

o n

ot d

istr

ibu

te.

DEPLOY CAPITAL TO CREATE VALUE

• Fund growth initiatives

• Total Audience

• Marketing Effectiveness

• Emerging Markets

• Connected System

• Coverage / Total Consumer

• Tuck-in M&A

• Grow dividend in line with earnings

• Deploy excess capital to share

repurchase

PRIORITIESLONG TERM

FCF DEPLOYMENT

Repurchase/

Tuck-in M&A

~40%

Dividend

~45%

Mandatory

Debt

~15%

CUMULATIVE FCF

~$3B

2018E - 2020E

DELIVERING SHAREHOLDER VALUE

44Cop

yri

gh

t ©

20

18

Th

e N

iels

en

Com

pa

ny (

US

), L

LC

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry. D

o n

ot d

istr

ibu

te.

NIELSEN ACQUISITIONS & JOINT VENTURES

Company Capabilities

2014

Nielsen Innovate Israel based incubator investing in startups that help Nielsen clients (10 countries)

Harris U.S. custom surveys

Nexium Retail shelf image identification technologies that replace manual inventory management systems

MMRD (JV) RMS in Myanmar

Czech TAM (JV) Television audience measurement

Affinova Intuitive user interface platform and automated analytics capabilities; Nielsen’s Innovation Practice

2015 eXelate Digital Marketing Platform (DMP) that helps facilitate the buying/selling of advertising

2016

Pointlogic Global leader in marketing decision support systems that improve precision and allocation

Repucom Global leader in sports measurement, evaluation and intelligence

2017

Gracenote Industry’s largest provider of media and entertainment metadata

Vbrand Machine learning-enabled platform measuring brand exposure and impact in sports programming

Visual IQ Leading provider of attribution measurement for digital marketing investments

45Cop

yri

gh

t ©

20

18

Th

e N

iels

en

Com

pa

ny (

US

), L

LC

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry. D

o n

ot d

istr

ibu

te.

LONG TERM OUTLOOK

Note: All growth measures represented on constant currency basis.

CAPITAL ALLOCATION

FREE CASH FLOW CONVERSION

ADJ. EBITDA MARGIN

REVENUE

GAAP EPS

Grow dividend in line with earnings

Flex between M&A and share repurchase

Drive mid-single digit growth

Double digit growth

45-50% Adj. EBITDA

~50 bps

THIS IS NIELSEN

46

This artwork was created using Nielsen data.

Copyright © 2018 The Nielsen Company (US), LLC. Confidential and proprietary. Do not distribute.

APPENDIX

47Cop

yri

gh

t ©

20

18

Th

e N

iels

en

Com

pa

ny (

US

), L

LC

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry. D

o n

ot d

istr

ibu

te.

CERTAIN NON-GAAP MEASURESOverview of Non-GAAP Presentations

We use the non-GAAP financial measures discussed below to evaluate our results of operations, financial condition, liquidity and

indebtedness. We believe that the presentation of these non-GAAP measures provides useful information to investors regarding financial and

business trends related to our results of operations, cash flows and indebtedness and that when this non-GAAP financial information is viewed

with our GAAP financial information, investors are provided with valuable supplemental information regarding our results of operations, thereby

facilitating period-to-period comparisons of our business performance. These non-GAAP measures are also consistent with how management

evaluates the company’s operating performance and liquidity. In addition, these non-GAAP measures address questions the Company

routinely receives from analysts and investors and, in order to assure that all investors have access to similar data, the Company has

determined that it is appropriate to make this data available to all investors. None of the non-GAAP measures presented should be considered

as an alternative to net income or loss, operating income or loss, cash flows from operating activities, total indebtedness or any other

measures of operating performance and financial condition, liquidity or indebtedness derived in accordance with GAAP. These non-GAAP

measures have important limitations as analytical tools and should not be considered in isolation or as substitutes for an analysis of our results

as reported under GAAP. Our use of these terms may vary from the use of similarly-titled measures by others in our industry due to the

potential inconsistencies in the method of calculation and differences due to items subject to interpretation.

Constant Currency Presentation

We evaluate our results of operations on both an as reported and a constant currency basis. The constant currency presentation, which is a

non-GAAP measure, excludes the impact of fluctuations in foreign currency exchange rates. We believe providing constant currency

information provides valuable supplemental information regarding our results of operations, thereby facilitating period-to-period comparisons of

our business performance and is consistent with how management evaluates the company’s performance. We calculate constant currency

percentages by converting our prior-period local currency financial results using the current period exchange rates and comparing these

adjusted amounts to our current period reported results. No adjustment has been made to foreign currency exchange transaction gains or

losses in the calculation of constant currency net income.

Net Debt and Net Debt Leverage Ratio

The net debt leverage ratio is defined as net debt (gross debt less cash and cash equivalents) as of the balance sheet date divided by

Adjusted EBITDA for the twelve months then ended. Net debt and the net debt leverage ratio are commonly used metrics to evaluate and

compare leverage between companies and are not presentations made in accordance with GAAP.

48Cop

yri

gh

t ©

20

18

Th

e N

iels

en

Com

pa

ny (

US

), L

LC

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry. D

o n

ot d

istr

ibu

te.

CERTAIN NON-GAAP MEASURES

Adjusted EBITDA

We define Adjusted EBITDA as net income or loss from our consolidated statements of operations before interest income and

expense, income taxes, depreciation and amortization, restructuring charges, stock-based compensation expense and other non-

operating items from our consolidated statements of operations as well as certain other items that arise outside the ordinary

course of our continuing operations. We use Adjusted EBITDA to measure our performance from period to period both at the

consolidated level as well as within our operating segments, to evaluate and fund incentive compensation programs and to

compare our results to those of our competitors.

Free Cash Flow

We define free cash flow as net cash provided by operating activities, less capital expenditures, net. We believe providing free

cash flow information provides valuable supplemental liquidity information regarding the cash flow that may be available for

discretionary use by us in areas such as the distributions of dividends, repurchase of common stock, voluntary repayment of debt

obligations or to fund our strategic initiatives, including acquisitions, if any. However, free cash flow does not represent residual

cash flows entirely available for discretionary purposes; for example, the repayment of principal amounts borrowed is not

deducted from free cash flow. Key limitations of the free cash flow measure include the assumptions that we will be able to

refinance our existing debt when it matures and meet other cash flow obligations from financing activities, such as principal

payments on debt. Free cash flow is not a presentation made in accordance with GAAP.

(continued)

49Cop

yri

gh

t ©

20

18

Th

e N

iels

en

Com

pa

ny (

US

), L

LC

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry. D

o n

ot d

istr

ibu

te.

2018 GUIDANCE NON-GAAP RECONCILIATIONS($ in millions)

2018 Guidance % V Constant

Currency

2017 Constant

Currency

Total Revenue ~$6,860 ~3% $6,663

REVENUE RECONCILIATION

50Cop

yri

gh

t ©

20

18

Th

e N

iels

en

Com

pa

ny (

US

), L

LC

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry. D

o n

ot d

istr

ibu

te.

2018 GUIDANCE NON-GAAP RECONCILIATIONS($ in millions)

ADJUSTED EBITDA RECONCILIATION

2018 Guidance Range

Revised(a) Original

Net income $535 - $560 $500 - $525

Interest expense, net $385 - $395 $385 - $395

Provision for income taxes $275 - $295 $310 - $330

Depreciation and amortization $640 - $660 $640 - $660

Restructuring charges $85 - $95 $85 - $95

Stock-based compensation and other(b) $80 - $100 $100 - $120

Adjusted EBITDA $2,040 - $2,070 $2,060 - $2,090

FREE CASH FLOW

Net cash provided by operating activities ~$1,300

Less: Capital expenditures, net ~(500)

Free cash flow ~$800

NET DEBT LEVERAGE RATIO

Gross Debt ~$ 8,440

Cash ~$ 600

Net Debt ~$ 7,840

Adjusted EBITDA $2,040 - $2,070

Net Debt Leverage Ratio ~3.8x

(a) The change in Adjusted EBITDA reflects an update for ASU 2017-07, which impacted Adjusted EBITDA but not Net Income, and for the updated impact of foreign exchange if rates were held

constant as of April 25th, 2018.

(b) Other represents certain expenses that arise outside the ordinary course of our continuing operations. Such costs primarily include legal settlements, acquisition related expenses, business

optimization costs and other transaction costs.

51Cop

yri

gh

t ©

20

18

Th

e N

iels

en

Com

pa

ny (

US

), L

LC

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry. D

o n

ot d

istr

ibu

te.

ADJUSTED EBITDA RECONCILIATION – PRE-IMPACT OF ASU 2017-07

($ in millions)

2017 2016 2015 2014 2013 2012

Net income 429 502 570 384 740 273

(Income)/ loss from discontinued operations, net of tax - - - - (305) (30)

Interest expense, net 370 329 307 297 307 386

Provision / (benefit) for income taxes 388 309 383 236 91 122

Depreciation and amortization 640 603 574 573 510 493

EBITDA 1827 1,743 1,834 1,490 1,343 1,244

Equity in net (income)/ loss of affiliates - - 3 4 (2) (5)

Other non-operating loss/(income), net 38 3 (170) 168 30 134

Restructuring charges 80 105 51 89 119 85

Stock-based compensation expense 45 51 48 47 47 34

Other items (a) 45 36 92 39 80 12

Adjusted EBITDA $ 2,035 $ 1,938 $ 1,858 $ 1,837 $ 1,617 $ 1,504

(a) For the twelve months ended December 31, 2017, 2016, and 2015 other items primarily consists of transaction related costs and business optimization costs.

52Cop

yri

gh

t ©

20

18

Th

e N

iels

en

Com

pa

ny (

US

), L

LC

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry. D

o n

ot d

istr

ibu

te.

ADJUSTED EBITDA RECONCILIATION – REFLECTS IMPACT OF ASU 2017-07

($ in millions)

2017 2016 2015 2014 2013 2012

Net income 429 502 570 384 740 273

(Income)/ loss from discontinued operations, net of tax - - - - (305) (30)

Interest expense, net 370 329 307 297 307 386

Provision / (benefit) for income taxes 388 309 383 236 91 122

Depreciation and amortization 640 603 574 573 510 493

EBITDA 1827 1,743 1,834 1,490 1,343 1,244

Equity in net (income)/ loss of affiliates - - 3 4 (2) (5)

Other non-operating loss/(income), net(a) 27 (10) (165) 163 26 130

Restructuring charges 80 105 51 89 119 85

Stock-based compensation expense 45 51 48 47 47 34

Other items (b) 45 36 78 34 80 12

Adjusted EBITDA $ 2,024 $ 1,925 $ 1,849 $ 1,827 $ 1,613 $ 1,500

(a) 2017 - 2012 Adjusted EBITDA numbers are revised to reflect the adoption of ASU 2017-07 - Presentation of Net Periodic Pension Costs.

(b) For the twelve months ended December 31, 2017, 2016, and 2015 other items primarily consists of transaction related costs and business optimization costs.

53Cop

yri

gh

t ©

20

18

Th

e N

iels

en

Com

pa

ny (

US

), L

LC

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry. D

o n

ot d

istr

ibu

te.

FREE CASH FLOW RECONCILIATION($ in millions. Year ended December 31 for all years.)

2017 2016 2015 2014 2013 2012

Net cash provided by operating activities $1,310 $1,296 $1,209 $1,093 $901 $784

Nielsen foundation contribution - 36 – – – –

One-time Arbitron costs - – – – 46 –

Capital expenditures, net (447) (391) (401) (412) (374) (358)

Free Cash Flow $863 $941 $808 $681 $573 $426

54Cop

yri

gh

t ©

20

18

Th

e N

iels

en

Com

pa

ny (

US

), L

LC

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry. D

o n

ot d

istr

ibu

te.

FREE CASH FLOW RECONCILIATION (CONTINUED)($ in millions. Year ended December 31 for all years.)

2018E

Net cash provided by operating activities ~ $1,300

Capital expenditures, net ~(500)

Free Cash Flow ~$800

55Cop

yri

gh

t ©

20

18

Th

e N

iels

en

Com

pa

ny (

US

), L

LC

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry. D

o n

ot d

istr

ibu

te.

GUIDANCE NET DEBT AND NET DEBT

LEVERAGE RATIO RECONCILIATION (CONTINUED)

($ in millions. Year ended December 31 for all years.)

2018E

Gross debt ~$8,440

Less: cash and cash equivalents ~600

Net debt ~$7,840

Adjusted EBITDA $2,040-$2,070

Net debt leverage ratio ~3.8X

56Cop

yri

gh

t ©

20

18

Th

e N

iels

en

Com

pa

ny (

US

), L

LC

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry. D

o n

ot d

istr

ibu

te.

GUIDANCE NET DEBT AND NET DEBT LEVERAGE RATIO

RECONCILIATION (CONTINUED)($ in millions) (unaudited)

FINANCIAL METRICS

1Q 18

Free Cash Flow $(245)

Capital Expenditures, net $128

D&A(b) $167

Net Book Interest $94

Cash Taxes $42

Cash Restructuring $24

Wtd. avg. diluted shares 357.3

BALANCE SHEET – 3/31/18

Gross Debt $8,646

Cash $462

Net Debt $8,184

Net Debt Leverage Ratio(c) 4.04x

CURRENT DEBT MATURITY PROFILE – 3/31/18(a)

$24

$1,401

$818

$1,090

$2,325

$2,126

$-

2018 2019 2020 2021 2022 2023 2024 2025

$499

(a) Excludes revolver ($195M) capital leases ($168M)

(b) Includes $56M of depreciation and amortization associated with tangible and intangible assets acquired in business combinations

(c) Reflects Net Debt (gross debt minus cash), divided by Adjusted EBITDA calculated on last twelve months basis

57Cop

yri

gh

t ©

20

18

Th

e N

iels

en

Com

pa

ny (

US

), L

LC

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry. D

o n

ot d

istr

ibu

te.

DEBT CAPITAL TABLE($ in millions)

(a) Adjusted EBITDA calculated based on last twelve months basis

(b) Reflects Net Debt (gross debt minus cash), divided by Adjusted EBITDA calculated on last twelve months basis

(c) Excludes capital leases

58Cop

yri

gh

t ©

20

18

Th

e N

iels

en

Com

pa

ny (

US

), L

LC

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry. D

o n

ot d

istr

ibu

te.

(Unaudited) FY 2016 GAAP FY 2017 GAAP FY 2017 Adj. for TCJA FY 2017 Adjusted

Income before taxes $816 $828 - $828

Provision for income taxes $309 $388 $(104) $284

Effective tax rate 37.9% 46.9% - 34.3%

Net Income attributable to Nielsen

Stockholders $502 $429 $104 $533

NI per share $1.39 $1.20 $0.29 $1.49

Diluted percent change (13.7%) 7.2%

RECONCILIATION OF GAAP AMOUNTS TO MEASURES EXCLUDING NET

IMPACT OF ENACTMENT OF TCJA($ in millions, except earnings per share)

59Cop

yri

gh

t ©

20

18

Th

e N

iels

en

Com

pa

ny (

US

), L

LC

. C

on

fid

en

tia

l a

nd

pro

pri

eta

ry. D

o n

ot d

istr

ibu

te.

NIELSEN INVESTOR RELATIONS

+1.646.654.4602

http://ir.nielsen.com

Follow @Nielsen

This artwork was created using Nielsen data.

Copyright © 2018 The Nielsen Company (US), LLC. Confidential and proprietary. Do not distribute.

THE SCIENCE BEHIND WHAT’S NEXT TM