no. 12-55926

TRANSCRIPT

No. 12-55926 Consolidated with Case No. 12-56197 and

Case No. 12-56288

UNITED STATES COURT OF APPEALS FOR THE NINTH CIRCUIT

Federal Trade Commission, Plaintiff and Cross-Appellant,

v.

BurnLounge, Inc., Juan Alexander Arnold, and John Taylor, Defendants and Appellants.

and

Rob DeBoer, Defendant.

Appeal from the United States District Court for the Central District of California

Case No. 2:07-03654 Hon. George Wu

APPELLANTS’ OPENING BRIEF BY BURNLOUNGE, INC. AND JUAN ALEXANDER ARNOLD

BUCHALTER NEMER, P.C. Lawrence B. Steinberg (State Bar No. 101966)

Efrat M. Cogan (State Bar No. 132131) 1000 Wilshire Boulevard, Suite 1500 Los Angeles, California 90017-2457

Telephone: (213) 891-0700 Facsimile: (213) 896-0400

Attorneys for Defendants and Appellants BURNLOUNGE, INC. and JUAN ALEXANDER ARNOLD

Case: 12-55926 01/04/2013 ID: 8462489 DktEntry: 21-1 Page: 1 of 69

i

TABLE OF CONTENTS PAGE

SUMMARY OF FACTS AND ARGUMENT ......................... 1 I.

STATEMENT OF ISSUES...................................................... 3 II.

STATEMENT OF FACTS ...................................................... 5 III.

Multi-Level Marketing ................................................... 5 A.

The Appellants ............................................................... 7 B.

1. BurnLounge, Inc. ................................................. 7

2. Juan Alexander Arnold ........................................ 8

BurnLounge’s Products and Their Costs. ....................... 9 C.

1. The Customizable E-Store and Related Software .............................................................. 9

2. BurnLounge Magazine ........................................10

3. BurnLounge Presents ..........................................10

4. BurnLounge University ......................................11

5. Live Nation Event Pass .......................................11

BurnLounge’s Policies and Procedures and D.Compensation Plan .......................................................11

BurnLounge in Operation .............................................15 E.

1. Salaries Paid .......................................................15

2. Income Claims ....................................................15

Sales .............................................................................16 F.

The FTC Secretly Begins an Investigation of G.BurnLounge and Then Shuts it Down ...........................18

Case: 12-55926 01/04/2013 ID: 8462489 DktEntry: 21-1 Page: 2 of 69

ii

TABLE OF CONTENTS (cont.) PAGE

PROCEDURAL HISTORY ..........................................20 H.

1. The Claims in Issue.............................................20

2. Trial ....................................................................20

3. Vander Nat Testimony ........................................20

4. Nolte Testimony .................................................22

5. The Trial Court’s Denial of BurnLounge’s Daubert Motion to Exclude Vander Nat’s Testimony ...........................................................24

6. Statement of Decision .........................................25

7. The Judgment, Post-Judgment Motions, and this Appeal ...................................................29

ARGUMENT..........................................................................29 IV.

The District Court Did Not Correctly Apply the A.Koscot/Omnitrition Test for Analyzing the Existence of a Pyramid. ................................................29

1. The Pyramid Test ................................................30

2. The FTC Had the Burden of Proving the Products and Product Packages Lacked Value and/or Did Not Constitute Legitimate Sales ........33

a. The Amway Decision, and the FTC’s Own Staff Advisory Opinion, Demonstrate The FTC’s Failure to Prove the Existence of a Pyramid ..............34

Case: 12-55926 01/04/2013 ID: 8462489 DktEntry: 21-1 Page: 3 of 69

iii

TABLE OF CONTENTS (cont.) PAGE

b. The Other Pyramid Cases Relied on by the District Court Are Distinguishable and by those Distinctions, Show that BurnLounge is Not a Pyramid ...................37

c. BurnLounge did not Share Any of the Improper Characteristics of Omnitrition, Five Star Auto or Holiday Magic ..............39

3. The FTC Likewise Failed to Prove that Those Who Purchased Product Packages Were Not Motivated, at Least in Part, By the Value of the Products ........................................................41

4. The District Court Impermissibly Shifted The Burden of Proof on Product Value and Consumer Motivation to BurnLounge in the First Instance ......................................................42

Vander Nat’s Testimony, Both In Support of Pyramid B.and Damages, Was Inadmissible ...................................43

The District Court’s Award of Monetary Relief Was C.Unauthorized By Statute and Excessive ........................45

1. The FTC Was Not Entitled to any Award of Monetary Relief ..................................................45

a. The FTC may Not Pursue Any Monetary Award Pursuant to 15 U.S.C. Section 53(b) ............................45

b. Even if the Trial Court Were Authorized to Award Some Form of Monetary Relief, the Award at Issue Impermissibly Constituted Legal, Not Equitable, Relief .......................................49

Case: 12-55926 01/04/2013 ID: 8462489 DktEntry: 21-1 Page: 4 of 69

iv

TABLE OF CONTENTS (cont.) PAGE

2. Arnold May Not Be Held Jointly and Severally Liable with BurnLounge for the Monetary Award. ................................................................51

3. The Amount of the Monetary award is Excessive. ...........................................................52

a. The District Court Erred in Assessing Any Monetary Award Because There Was No Pyramid Liability and/or Because There were No Competent Evidence of “Damages” Flowing From a Pyramid. ......52

b. Even if The District Court Could Have Awarded Some Monetary Relief, The Reasoning that Supported Its Award Demonstrates That the Award Was Excessive. .................................................54

4. There Was No Evidence Introduced to Justify a $1.6 Million Disgorgement Award Against Arnold.................................................................56

CONCLUSION ......................................................................56 V.

Case: 12-55926 01/04/2013 ID: 8462489 DktEntry: 21-1 Page: 5 of 69

v

TABLE OF AUTHORITIES PAGE

Cases

Arch Ins. Co. v. Precision Stone, Inc., 584 F.3d 33 (2d Cir. 2009) ....................................................................45

Blackwell v. Strain, 2012 U.S. App. LEXIS 19186 (10th Cir. 2012) .....................................41

Branch v. Smith, 538 U.S. 254, 123 S. Ct. 1429, 155 L. Ed. 2d 407 (2003) ......................46

California First Amendment Coalition v. Calderon, 150 F.3d 976 (9th Cir. 1998) .................................................................30

Cano v. Cont'l Airlines, Inc., 193 Fed. Appx. 664 (9th Cir. 2006) .......................................................44

Coleman v. Quaker Oates Co., 232 F.3d 1271 (9th Cir. 2007) ...............................................................41

Daubert v. Merrell Dow Pharmaceuticals, Inc., 43 F.3d 1311 (9th Cir. 1995) (Daubert II) .............................................44

DeSaracho v. Custom Food Machinery, Inc., 206 F.3d 874 (9th Cir. 2000) .................................................................43

Dhillon v. BBC Holdings, Inc., 2009 U.S. Dist. LEXIS 28865 (W.D. Wash. 2009) ................................33

Erlenbaugh v. United States, 409 U.S. 239, 93 S. Ct. 477, 34 L. Ed. 2d 446 (1972) ............................46

Export Group v. Reef Indus., Inc., 54 F.3d 1466 (9th Cir. 1995) .................................................................48

FTC v. Amy Travel Serv., Inc., 875 F.2d 564 (7th Cir. 1989) .................................................................48

FTC v. H. N. Singer, Inc., 668 F.2d 1107, 1111 (9th Cir. 1982) ......................................... 47, 48, 49

Case: 12-55926 01/04/2013 ID: 8462489 DktEntry: 21-1 Page: 6 of 69

vi

TABLE OF AUTHORITIES (cont.) PAGE

FTC v. Kuykendall,

371 F.3d 745 (10th Cir. 2004) ...............................................................45

FTC v. Publ’g Clearing House, Inc. 104 F.3d 1168 (9th Cir. 1996) ......................................................... 51, 52

GE v. Joiner, 522 U.S. 136 (1997) ..............................................................................43

Great-West Life & Annuity Ins. Co. v. Knudson, 534 U.S. 204, 122 S. Ct. 708, 151 L. Ed. 2d 635 (2002) .................. 49, 50

Green Mt. Chrysler Plymouth Dodge Jeep v. Crombie, 508 F.Supp.2d 295 (D. Vt. 2007) ..........................................................44

Honolulu Joint Apprenticeship and Training Comm. v. Foster, 332 F.3d 1234 (9th Cir. 2003) ...............................................................50

In re Ger-Ro-Mar, Inc., 518 F.2d 22 (2nd Cir. 1975) ........................................................... passim

Kokkonen v. Guardian Life Ins. Co. of Am., 511 U.S. 375, 114 S. Ct. 1673, 128 L. Ed. 2d 391 (1994) ......................49

Kumho Tire Co. v. Carmichael, 526 U.S. 137 (1999) ........................................................................ 24, 43

Meghrig v. KFC Western, Inc., 516 U.S. 479, 116 S. Ct. 1251, 134 L. Ed. 2d 12 (1996) ........................49

Purcell v. Gonzalez, 549 U.S. 1 (2006) ..................................................................................30

Torres-Lopez v. May, 111 F.3d 976 (9th Cir. 1997) .................................................................30

Turner v. FTC, 580 F.2d 701 (D.C. Cir. 1978) ......................................................... 20, 31

Case: 12-55926 01/04/2013 ID: 8462489 DktEntry: 21-1 Page: 7 of 69

vii

TABLE OF AUTHORITIES (cont.) PAGE

United States v. Hinkson,

484 F.3d 1247 (9th Cir. 2009) ...............................................................30

United States v. Pend Orieille County Pub. Util. Dist No. 1, 135 F.3d 602 (9th Cir. 1998) .................................................................45

Whole Living, Inc. v. Tolman, 344 F.Supp.2d 739 (D. Utah 2004) .................................................. 30, 36

Statutes

15 U.S.C. § 45(a) ....................................................................................... 5

15 U.S.C. § 57b .................................................................................. 46, 48

15 U.S.C. § 57b(e) ....................................................................................48

28 U.S.C. § 1391........................................................................................ 5

OtherAuthorities

Peter C. Ward, Restitution for Consumers Under the Federal Trade Commission Act 41 Am. U. L. Rev. 1139 (1992) .............................................................47

S. Conf. Rep. No. 93-1408 (1974) .............................................................47

S.Rep. No. 93-151 ....................................................................................47

Case: 12-55926 01/04/2013 ID: 8462489 DktEntry: 21-1 Page: 8 of 69

viii

CORPORATE DISCLOSURE STATEMENT

Appellant BurnLounge, Inc. is a corporation organized under

the laws of the State of Delaware. Appellant Juan Alexander Arnold

is an individual and was Chief Executive Officer of BurnLounge, Inc.

DATED: January 4, 2013

Respectfully submitted,

BUCHALTER NEMER, P.C. Lawrence B. Steinberg

Efrat M. Cogan

By: /s/ Efrat M. Cogan Attorneys for Defendants and Appellants

BURNLOUNGE, INC. and JUAN ALEXANDER ARNOLD

Case: 12-55926 01/04/2013 ID: 8462489 DktEntry: 21-1 Page: 9 of 69

1

SUMMARY OF FACTS AND ARGUMENT I.

BurnLounge, Inc. was a multi-level marketing (MLM)

company. Using cutting-edge technology developed at great cost,

BurnLounge allowed consumers who were music fans and musicians

(a) to customize individual webpages and online store portals by

choosing the layout, appearance and featured music, and (b) to sell

music downloads and music related products to other like-minded

consumers who visited their webpages. At a point in time when social

networking was still in its infancy, BurnLounge provided a user

experience which combined social networking (like MySpace and

Facebook) and entrepreneurship (like eBay), using an MLM model

(like many other legal MLMs) that allowed consumers to earn

commissions on the sale of legally licensed music and music products,

if they so chose.

A consumer could participate in BurnLounge in several ways.

He could simply buy products, or set up his own website and become

a “retailer” eligible to sell products in exchange for points.

Alternatively, for a small monthly fee, he could become a “Mogul”

eligible to convert points into cash compensation. As is the case with

all MLMs, Moguls received cash commissions on both their own

direct product sales and on product sales of those in their sales teams.

However, unlike many other MLMs, BurnLounge’s products were not

intended for resale (a characteristic of many MLMs that have been

deemed to be illegal pyramids). Commissions were not paid on

inventory sales to middlemen who then re-sold the products.

Case: 12-55926 01/04/2013 ID: 8462489 DktEntry: 21-1 Page: 10 of 69

2

BurnLounge Moguls earned commissions only by selling products to

the ultimate consumer of those products.

The FTC sued BurnLounge, its CEO Juan Alexander Arnold,

and two of its independent distributors, alleging that (a) BurnLounge

was an illegal pyramid, and, separately, (b) that defendants made

misleading income claims. The FTC did not put on any evidence

concerning the value of the products sold by BurnLounge, claiming

this was irrelevant to liability. The FTC also failed to present

evidence of consumer motivation – i.e., evidence that the products

were not purchased for their use. Consequently, the FTC failed to

show (in the words of the applicable legal test) that rewards for

recruiting were “unrelated to” the sale of products to ultimate users.

While the FTC agreed that the value of products would reduce

the amount of consumer harm, it claimed that the value of the

products was “negligible.”

So for Moguls who received commissions in a sum less than the

amount of their initial investment (the so called “losers”), the FTC

sought to recover the total amount that the Moguls had paid for

product purchases and fees, without any deduction for the value of

what was received. The FTC thus insisted that the entire purchase

price for products was equivalent to a consumer’s “investment” in the

BurnLounge business opportunity.

Similarly, the FTC refused to allow any credit for the amount of

commissions paid to Moguls, assessing damages in an amount equal

to the gross amount of money paid by the Mogul, even if those

Moguls received cash commissions back from BurnLounge.

Case: 12-55926 01/04/2013 ID: 8462489 DktEntry: 21-1 Page: 11 of 69

3

The district court found that BurnLounge was an illegal

pyramid and that the company and its CEO (Arnold) were jointly and

severally liable for approximately $16.2 million. The district court

also found that defendants made false and misleading representations

regarding what a consumer could expect to earn if he participated in

the BurnLounge business opportunity as a Mogul (so-called “income

claims”).1

The district court’s judgment should be reversed for myriad

reasons, principal among them: (1) The court did not properly apply

the test for determining the existence of a pyramid; (2) It improperly

shifted the burden of proof from the FTC to BurnLounge; (3) It relied

on inadmissible and incompetent “expert testimony”; (4) It ordered

damages which were unauthorized by statute, not restitutionary in

nature, and which were excessive in any event.

STATEMENT OF ISSUES II.

(1) Did the district court properly apply the pyramid test,

which provides that before an MLM can be deemed an illegal

pyramid, there must be a finding that rewards for recruitment are

unrelated to the sale of products to ultimate users?

1 For purposes of this appeal, BurnLounge does not challenge

the finding that false and/or misleading income claims were made at some presentations and telephone conference calls. However, significantly, neither the FTC nor the district court made any calculations arising from “income claims.”

Case: 12-55926 01/04/2013 ID: 8462489 DktEntry: 21-1 Page: 12 of 69

4

(2) Did the district court err in adjudging BurnLounge a

pyramid, by relying on characteristics of the BurnLounge

compensation system that are present in both legal and illegal MLMs?

(3) Did the district court err when it found BurnLounge to be a

pyramid even after its own finding that, for at least some consumers,

the products BurnLounge sold had at least as much value as the

amount being charged?

(4) Did the district court err when it used a methodology in

adjudging BurnLounge a pyramid that, in effect, shifted the burden of

proof from the FTC to defendants?

(5) Did the district court err in allowing in the testimony of the

FTC’s expert?

(6) May the FTC seek monetary relief when it proceeds solely

pursuant to 15 U.S.C. Section 53(b) – allowing for injunctive relief?

(7) Does the FTC’s failure to equitably trace any monies to

BurnLounge and/or to Arnold bar the FTC’s claim for equitable relief

such that the trial court erred in awarding any monetary relief at all?

(8) Did the trial court err in finding Arnold jointly and

severally liable for monetary relief when the FTC did not establish

that Arnold acted with the requisite scienter?

(9) Did the trial court err in finding Arnold liable for restitution

in the amount of $1,664,566.45 when the only evidence in the record

demonstrates that Arnold received salaries and bonuses from

BurnLounge only in the amount of $593,732.01?

(9) Was the monetary award of $16,245,799.70 excessive?

Case: 12-55926 01/04/2013 ID: 8462489 DktEntry: 21-1 Page: 13 of 69

5

STATEMENT OF FACTS III.

The FTC’s suit alleges that the defendants violated 15 U.S.C.

Section 45(a) (Section 5(a) of the FTC Act) by: (1) “promot[ing] a

pyramid scheme” (2) making misleading income claims to promote

the BurnLounge business, and (3) concealing from Moguls that they

were not likely to make substantial income. {1 ER.}2 Venue and

jurisdiction in the district court was proper pursuant to 15 U.S.C.

Section 53 and 28 U.S.C. Section 1391. {5 ER 45.}

MULTI-LEVEL MARKETING A.

Multi-level marketing3 is “a way of distributing products or

services in which independent distributors earn income from their

own direct retail sales as well as from the sales made by their direct

and indirect recruits.” {Tr. Ex. 1130:24 ER 531.} The multi-level

marketing company, or MLM, generates sales through an independent

sales force, and the sales force is paid by commissions on those sales.

{Ibid.} It rewards its retailers both for being entrepreneurs and for

recruiting others into the company. By rewarding distributors in

2 Unless otherwise noted, references to the excerpts of record

shall be as follows: [Tab No.] ER [page no.] as necessary. 3 This summary comes from an article written by the FTC’s

expert, Vander Nat (Tr. Ex. 1130: 24 ER.), on how to distinguish between legal MLMs and illegal pyramids. BurnLounge neither accepts or adopts the test nor the author’s interpretation of the law. But Vander Nat’s article does contain certain admissions concerning the characteristics in common between MLMs and illegal pyramids.

Case: 12-55926 01/04/2013 ID: 8462489 DktEntry: 21-1 Page: 14 of 69

6

hierarchical fashion4 for direct and indirect sales, MLMs incentivize

distributors to engage in recruitment: “Distributors are rewarded for

personal sales and are motivated by the entrepreneurial aspect of

being an independent contractor who builds a ‘downline’ of

distributors.” {24 ER 531} “Both MLMs and pyramid schemes

involve distributors as consumers, recruiters and retailers.” {Id. at p.

532.}

A number of well-known companies use a multi-level

marketing approach, including Arbonne, Avon, Herbalife, and Mary

Kay. {Vander Nat: 70 ER 1025:19-1026:25; Luce: 57 ER 766.1:21-

766.3:4.}

At trial, the parties agreed that legal MLMs and illegal

pyramids share certain common characteristics. They both: (1)

compensate for direct and indirect sales; (2) encourage recruiting and

entrepreneurship; and (3) encourage downline recruitment, creating

progressively widening layers of grown as the company grows. And

in both legal MLMs and pyramids, most participants may not generate

enough commissions to “recoup their investment” in the business.

{Vander Nat: 70 ER 1034:16-24; 69 ER 978:14-21, 979:1-3, 983:16-

984:5; Luce: 57 ER 767:20-769:20); see e.g., 70 ER 1017:23-25

4 In other words, a distributor makes commissions on his own

sales, the sales of and by those he recruits, and on the sales that his recruits sponsor. These are known as a distributor’s “downline.” The hierarchy resembles a “pyramid” in shape. As the trial court recognized, the terms “pyramid” or “pyramid scheme” are often used generally to refer to MLMs, whether or not legal. For purposes of this brief, the term pyramid will only refer to illegal pyramids. {See e.g., 5 ER 45, fn.1.}

Case: 12-55926 01/04/2013 ID: 8462489 DktEntry: 21-1 Page: 15 of 69

7

(Vander Nat TT: “high failure rate does not prove . . . pyramid

scheme.”}

THE APPELLANTS B.

1. BURNLOUNGE, INC.

BurnLounge was a multi-level marketing company that

provided legal, downloadable music and product packages through

customized member websites (or BurnPages). {5 ER 46-47.} Sales

of music and music related products were made through the member

websites. BurnLounge retailers who sold music downloads (single

songs or albums) or packages of music products earned points on both

their direct sales and on the sales of those in their downline sales team

(indirect sales). The points (akin to frequent flier miles) could be used

toward the purchase of music and merchandise by the retailers.

Separately, a retailer who wanted to earn cash rather than points could

become a Mogul by paying a monthly $6.95 Mogul Fee. {5 ER 48.];

Tr. Ex. 8 and 10 [ER, Tabs 56 and 55]; See also Section ___, infra.}

BurnLounge did not require, and did not allow, retailers to

purchase product packages for resale. {Vander Nat: 70 ER 1018:17-

18, 67 ER 955:11-25; Luce: 57 ER 773:1-11.} There was no evidence

that anyone purchased more than a single product package. As

demonstrated below, the products were designed and intended for

personal consumption. A retailer’s sales of product to others, though

made through the retailer’s BurnPage, was fulfilled by BurnLounge to

the ultimate purchaser. {Vander Nat: 67 ER 955:16-25.} Thus, a

BurnLounge retailer never bought any additional product beyond the

Case: 12-55926 01/04/2013 ID: 8462489 DktEntry: 21-1 Page: 16 of 69

8

single product package purchased for his own personal consumption,

and did not carry any inventory. {Vander Nat: 69 ER 988:1:22-23, 67

ER 960:10-13 [no one pressured to buy products].}

At its peak, BurnLounge had approximately 70 employees,

most of which had no prior experience with MLMs. {Dadd: 63 ER

896:9-897:4} Its principal officers included: Ryan Dadd, COO;

Steven Murray, President of Entertainment; and Kevin Keranen,

Executive VP of Retailer Systems and Operations.5

2. JUAN ALEXANDER ARNOLD

Arnold was BurnLounge’s CEO and Chairman of its Board. {5

ER 45.} Arnold earned $593,732.01 in salary and bonuses during his

2½ years tenure. {Ibid.; see also, Piemonte: 61 ER 866:9-869:17,

870:10-17 and Tr. Ex. 1135: [W-2 forms].} Arnold advanced money

to help fund various company expenses for which he was reimbursed.

{Arnold: 72 ER 1040:2-1041:12.} There was no contention that

these expense reimbursements were for anything other than legitimate

BurnLounge business expenses. The FTC did not establish the

amount of the reimbursements at trial, and the precise amount of the

reimbursement is not contained in the trial record. {See e.g. 5 ER p.

46, [referencing fact of reimbursable expenses but not amount].}

5 Dadd, among other things, contracted with entertainment and

technology companies to develop the products sold by BurnLounge retailers. {Dadd: 66 ER 951.} Murray was responsible for BurnLounge marketing and its Artists & Repertoire (A&R) department. {Murray: 67 ER 962:6-966:7, 967-970.} and Keranen had responsibility for BurnLounge’s compensation and for retailer operations. {Keranen TT: 63 ER 908:9-909:11.}

Case: 12-55926 01/04/2013 ID: 8462489 DktEntry: 21-1 Page: 17 of 69

9

BURNLOUNGE’S PRODUCTS AND THEIR COSTS. C.

BurnLounge sold music downloads and three different product

packages, each of which consisted of various music related products:

the Basic Package ($29.95), the Exclusive Package ($129.95) and the

VIP Package ($429.95). {5 ER 48.}6

Through contracts with two aggregators of licensed music,

BurnLounge obtained the right to legally sell music distributed by all

of the major record labels and most of the independent labels.

Ultimately, BurnLounge sold substantially the same catalog of songs

as iTunes. {Murray: 67 ER 970:21-971:6; 66 ER 935:15-33, 936:16-

25, 937:5-938:5 and Tr. Ex. 1088 [29 ER].} These licensing

arrangements cost in excess of $1,450,000. {Tr. Ex. 1086-87, 1091-

92 [ER: Tabs 31, 31, 28 and 27].}

In addition to music downloads, BurnLounge sold the following

products which were bundled for sale in the three different product

packages.

1. THE CUSTOMIZABLE E-STORE AND RELATED

SOFTWARE

Included in all three of BurnLounge’s product packages (Basic,

Exclusive and VIP) was the customizable website and e-store, through

which individuals could engage in social networking, promote their

6 By 2007, BurnLounge was contracting to expand the products

it had for sale to include licensed films and television shows, portable media players and related accessories, and digital “lifestyle” content. {See, 63 ER 989:16-902:13 [Cinema Now and Archos], 63 ER 903-904 [iAmplify].}

Case: 12-55926 01/04/2013 ID: 8462489 DktEntry: 21-1 Page: 18 of 69

10

favorite music and music artists, and sell music downloads and

product packages. {Tr. Ex. 10: 55 ER 686-687; 5 ER 48.}

BurnLounge paid more than $850,000 to third-party developers to

design this technology. {Tr. Exs. 1157A [20 ER], 1076-77 [ER, Tabs

37 and 36], 1080-81 [ER, Tabs 35 and 34], 1163-64 [ER, Tabs 19 and

18].}

2. BURNLOUNGE MAGAZINE

BurnLounge Magazine was a high quality magazine which

focused on trends and developments in the music industry; it did not

include any articles about BurnLounge or the BurnLounge business

opportunity. Initially the magazine issued quarterly; in January 2007

it issued on a monthly basis. {Murray: 66 ER 931.2:15-931.4:10;

Piemonte: 61 ER 864:15-19, 865:16-19; Tr. Ex. 1063 [19 ER].}

Costs incurred by BurnLounge in connection with the magazine

totaled approximately $1.5 million. {Piemonte: 61 ER 862:20-

863:17; Murray: 66 ER 931.5:13-931.7:15 and Tr. Exs. 1082-83 [ER:

Tabs 33 and 32.]} One issue was included in the BurnLounge Basic

Package; a yearly subscription was included in the Exclusive and the

VIP Packages. {Tr. Ex. 10 [55 ER 686-687; 5 ER 48.}

3. BURNLOUNGE PRESENTS

BurnLounge Presents (BLP) consisted of a monthly selection of

10 songs and a music DVD, chosen by BurnLounge’s A&R

Department. {75 ER 1058:23-1059:6; 66 ER 932:22-934:12; 63 ER

906:1-9, 907:8-13; Tr. Ex. 1129 [25 ER], 1062 [39 ER: list of songs

featured on BLP]; 67 ER 968:16-969:8; 66 ER 932:22-933:5 and

Case: 12-55926 01/04/2013 ID: 8462489 DktEntry: 21-1 Page: 19 of 69

11

Tr. Ex. 1129 [25 ER].} BLP was included in the Exclusive and VIP

Packages. {Tr. Ex. 10 [55 ER 687; 5 ER 48.}

4. BURNLOUNGE UNIVERSITY

BurnLounge University was a six disc documentary DVD about

the entertainment business and the music industry. {Murray: 66 ER

938:11-15, 939:1-24 [indicating portions played during trial].} It was

included in the VIP Package. {Tr. Ex. 10 [55 ER 687]; 5 ER 48.}

5. LIVE NATION EVENT PASS

Included in the VIP Package was an Event Pass to live music

concert performances sponsored by Live Nation, the largest concert

promoter in the U.S. {5 ER 48; 66 ER 940:1-6.} The Pass allowed a

concertgoer to (a) go to the head of the line (a valuable benefit since

many Live Nation events do not have pre-assigned seating) and

(b) obtain access to roped off VIP sections. {Burruss: 66 ER 941:22-

944:19.} Each Pass was worth hundreds of dollars. {Burruss: 66 ER

125:19-126:5.}

BurnLounge paid a total of $625,000 to Live Nation so that its

VIP members could have these privileges. {Burruss: 66 ER 946-947,

949-950 and Tr. Exs. 271 [49 ER], 272 [48 ER], 1156 [21 ER], 1157A

[20 ER].}

BURNLOUNGE’S POLICIES AND PROCEDURES AND D.COMPENSATION PLAN

A BurnLounge retailer did not buy inventory for resale.

{Taylor: 77 ER 1067:3-5; Vander Nat: 72 ER 1047:13-16.} Product

Case: 12-55926 01/04/2013 ID: 8462489 DktEntry: 21-1 Page: 20 of 69

12

packages were not purchased in quantity for resale and then resold.

No evidence was presented of multiple purchases of products

packages by retailers.

Under the Policies and Procedures and Compensation Plan, a

“retailer” earned points from the sale of music and product packages,

and those points could be used for the future purchase of songs and

merchandise. {Tr. Ex. 8 [56 ER 700, 719-29]; Tr. Ex. 10 [55 ER

688].} Retailers could become “Moguls” entitled to convert their

points into cash if they paid a monthly $6.95 Mogul Fee. {Tr. Ex. 8

[56 ER 287]; Ex. 10 [55 ER 687-688.} The decision of whether to

become a Mogul was a separate decision made by retailers.

{Vander Nat: 69 ER 985:3-12.}

When one registered with BurnLounge, one did so through a

sponsoring retailer. {Tr. Ex. 8 [56 ER 700].} And retailers signing

up through a retailer became part of that retailer’s downline and sales

team. {74 ER 1053:21-1054:5.}

Retailers were prohibited from marketing BurnLounge other

than as set forth in official BurnLounge literature. {Tr. Ex. 8 [56 ER

702.} Retailers/Moguls were prohibited from producing and using

their own promotional materials. {Ibid.} The Policies and Procedures

expressly precluded making income claims – i.e. claims about the

amount of money that a Mogul could or would make if he or she

participated in the Mogul program. {Id. at 707,711,717.}

Because the FTC’s challenge to BurnLounge’s business model

related to the Mogul portion of the program, and the district court only

Case: 12-55926 01/04/2013 ID: 8462489 DktEntry: 21-1 Page: 21 of 69

13

found that portion to be a pyramid,7 the following description

addresses the Mogul (or cash) portion of the program.8

A Mogul earned commissions on his own sale of music and

product packages (direct sales) and on product sales made by

members of his sales team (indirect sales). {Tr. Ex. 8 [56 ER 719-

20]; Tr. Ex. 10 [55 ER 687-688].} Commissions included Concentric

Retail rewards, Product Package rewards, and Mogul Team Bonuses.

{Tr. Ex. 10 [55 ER 689-694].}

Concentric Retail: A Mogul earned commissions on his own

personal sales. Moguls could also receive commissions for sales of

their team members for six levels at decreasing percentages.

{Tr. Ex. 10 [55 ER 690].}

Product Package Bonuses: In order to receive product package

bonuses, a Mogul had to have sold at least two albums-worth of music

in the previous month. {Tr. Ex. 10 [55 ER 691].} Moguls were paid

a $10.00 bonus for the sale of a Basic Package, a $25.00 bonus for the

sale of an Exclusive Package, and a $50.00 bonus for the sale of a VIP

Package.9

Mogul Team Bonuses: In order to qualify for this bonus, a

Mogul had to sell at least two Exclusive or VIP Packages (a one-time

qualification requirement), and had to sell two albums of music each

7 5 ER 65. 8 See also 5 ER 54-59. 9 Of these sums, $5.99 was paid through Concentric Retail, and

the remainder ($4.01, $14.01 or $44.01, respectively) was paid as bonus. {Tr. Ex. 10 [55 ER 691].}

Case: 12-55926 01/04/2013 ID: 8462489 DktEntry: 21-1 Page: 22 of 69

14

month. {Tr. Ex. 10 [55 ER 691].} Additionally, depending on the

type of package purchased, a Mogul had to meet certain minimum

music sales volume (“MSV”) requirements:

• A Basic Mogul had to sell at least $500 in music to be

eligible to receive the $25.00 bonus, and at least $1,000

to be eligible for the $50.00 bonus. {Tr. Ex. 8 [56 ER

724]; Tr. Ex. 10 [55 ER 891-692].}

• Until November 1, 2006 (when the program requirements

were amended), an Exclusive Mogul did not have any

MSV requirements to be eligible to receive Mogul Team

Bonuses. {Tr. Ex. 321 [46 ER 636]; Tr. Ex. 318 [47 ER

644-645: 11/17/05 compensation plan].}10 Until that

date, there were no differences in MSV requirements for

Exclusive and VIP Moguls. After November 1, 2006,

Exclusive Moguls had to sell at least $500.00 in music to

be eligible for the $50.00 bonus; until meeting this

requirement, an Exclusive Mogul was eligible to only

earn the $25.00 bonus. {Tr. Ex. 8 [56 ER 724], Tr. Ex. 10

[55 ER 691-692].}

10 This November 1, 2006 change in the qualification

requirements was not acknowledged by the district court in its Statement of Decision, although this fact was central to the court’s methodology for calculating damages. As discussed below, the methodology relied upon by the district court relied on the erroneous understanding that a VIP Mogul had less onerous MSV requirements than an Exclusive Mogul, a factor which was not true prior to November 1, 2006. (See, Section IV.C.3.b., infra.)

Case: 12-55926 01/04/2013 ID: 8462489 DktEntry: 21-1 Page: 23 of 69

15

• A VIP Mogul did not have a MSV requirement to be

eligible for Mogul Team Bonuses. {Tr. Ex. 8 [56 ER

724; Tr. Ex. 10 [55 ER 691-692].}

BURNLOUNGE IN OPERATION E.

1. SALARIES PAID

BurnLounge grew from about 20 employees to 68 employees.

{Dadd: 63 ER 896:9-16:9-16.} The company paid $5 million in

salaries during its two years in operation; about 80% of those salaries

went to employees who developed products and technology. {Dadd:

63 ER 905:15-22.}

2. INCOME CLAIMS

The district court found that individual defendants made

income claims at meetings and during live and pre-recorded telephone

conferences. {5 ER 60-63.} The investigators did not know whether

the audience consisted of prospective or already registered retailers.

At best they were able to estimate that the audience consisted of an

approximate, collective 590 persons, and even then, they did not know

how many of those were double-counted (for having attended more

than one meeting or conference.)11

11 {FTC investigators: 78 ER 1071:18-1071.1:23 [one meeting

with 8-10 people], 78 ER 1072:19-1073:30 [1 meeting, 80 people], 78 ER 1075:10-1077:4 [1 meeting, 100 people], 78 ER 1078:20-1084:1 [four meetings with a total maximum of 400 people].}

Case: 12-55926 01/04/2013 ID: 8462489 DktEntry: 21-1 Page: 24 of 69

16

The trial court found some statements to be untrue or

misleading. {5 ER 62.} Defendants BurnLounge and Arnold do not

challenge that these statements were made.

SALES F.

Sales of products (music and product packages) were sufficient

to pay for employee salaries and cash commissions paid to Moguls.

{Piemonte: 61 ER 857:1-18, 855:20-25, 856:9-857:2 and Tr. Exs. 64

[54 ER] and 66 [53 ER].} 12

The total commission payout for calendar year 2006 averaged

about 75.4% of revenues {Piemonte: 61 ER 853:15-854:24.} In

2006, commissions paid were $12,491,342, of which 63% were for

Mogul Team bonuses and 37% were for rewards under concentric

retail and product package bonuses as well as promotions. {Piemonte:

61 ER 858:21-859:19, 861:11-21 and Tr. Ex. 258 [50 ER].}

During BurnLounge’s operation, there were 118,357 people

who were customers, retailers and/or Moguls. {5 ER 59, incl. fn. 30.}

56,017 persons were never a Mogul and never purchased a product

package (and so only purchased music or merchandise); 62,250 were

retailers, and of that number, 1,980 never became a Mogul, while

60,270 were Moguls for some portion of time. {5 ER 59, Section (j);

12 Over the course of its operations, BurnLounge generated

monthly revenue reports to track sales and revenues. {Piemonte: 61 ER 848:11-849:20, 850:10 and see Tr. Ex. 178 [51 ER], an exemplar.} The music sales were calculated on a net basis (meaning music sales, minus royalties and less the transactional costs). {Piemonte: 61 ER 850:23-852:21, 860:13-14 and Tr. Ex. 258 [50 ER].}

Case: 12-55926 01/04/2013 ID: 8462489 DktEntry: 21-1 Page: 25 of 69

17

Tr. Ex. 330 (at p. 1),13 1051 [40 ER], and 422 [52 ER].} The average

Mogul was only a Mogul for 6.8 out of BurnLounge’s 17 months of

operation (or only 40% of the time). {Vander Nat: 69 ER 1010:6-20,

1011:9-12.}

Additionally, 40% of those who were ever a Mogul (whether

continuously or for a month) never earned any cash commissions.

This means they did not sell even a single song which, automatically,

would have entitled them to some cash compensation. {Vander Nat:

69 ER 1013:1-7.}

Exhibit 422 – prepared by FTC expert Vander Nat − reflects

that, of the 1,980 retailers who were never a Mogul, about 65%

purchased the Basic Package, while the remainder about equally split

between purchasing the Exclusive and VIP Packages. {42 ER.} Of

retailers who became Moguls, 67% purchased the VIP Package, 29%

purchased the Exclusive Package, and 4% purchased the Basic

Package. {Ibid.}

13 For all of their data and calculations, the parties and the

district court all relied upon the same Master Spreadsheet of BurnLounge data. This spreadsheet, in the form of an electronic Excel spreadsheet, was admitted into evidence as both Tr. Ex. 330 and Tr. Ex. 1052; a summary sheet taken from the first page of the spreadsheet was separately admitted as Tr. Ex. 1051[40 ER]. So that this court has access to the same data used by the district court, appellants are filing, concurrently with this opening brief, a motion to accept as part of the record on appeal, a CD containing an electronic version of Tr. Ex. 330.

Case: 12-55926 01/04/2013 ID: 8462489 DktEntry: 21-1 Page: 26 of 69

18

Persons who were never Moguls and never bought a music

package spent $1,005,544 for music downloads and other

merchandise. {Tr. Ex. 1051 [50 ER].}

In about April 2007, BurnLounge launched a free version of

its website through which one could sell music and product packages,

and earn cash commissions without having to buy a product package.

{Murray: 67 ER 972:23-973:9, 66 ER 931.1:1-25.}

In total, BurnLounge took in $28,386,280 in gross revenues.14

Of this amount, it paid out to its Moguls $17,458,276 in commissions.

{Tr. Ex. 330 (see fn. 13, supra.); Tr. Ex. 1051 [40 ER]} The

difference (approximately $10 million) went to salaries and the costs

associated with developing BurnLounge’s technology and website

platform, and developing and manufacturing the products sold . {See

Section III.C., supra.}

THE FTC SECRETLY BEGINS AN INVESTIGATION OF G.BURNLOUNGE AND THEN SHUTS IT DOWN

Beginning in mid-2006, the FTC sent covert investigators into

the field to attend various retailer meetings, and to record retailer

telephone conference calls. (See fn. 11.) The FTC’s expert and in-

house economist, Peter Vander Nat, spent two months of concentrated

work reviewing the material before reaching his conclusion that

BurnLounge was a pyramid. {Vander Nat: 72 ER 1042-1044; 70 ER

1019:3-1024:24.}

14Tr. Ex. 1051 [40 ER].

Case: 12-55926 01/04/2013 ID: 8462489 DktEntry: 21-1 Page: 27 of 69

19

While Vander Nat considered consumer declarations to be

material, he did not receive any with this investigation and so left

them out of his analysis. {Vander Nat: 69 ER 933-1000 and

Tr. Ex. 1166 [17 ER].} He did not ask that a consumer survey be

prepared – although it would have provided him with evidence of

consumer motivation ‒ claiming it would be too costly. {Vander Nat:

69 ER 1001-1004.}

Vander Nat was aware that the Direct Sellers Association

(DSA) had prepared its own surveys determining why consumers

joined multi-level marketing companies (MLMs), but he did not

consider those. {Vander Nat: 10 ER 1005:12-1006:11.} Alan Luce,

BurnLounge’s MLM expert, testified that these DSA studies showed

that approximately 40-60% of those who join MLM companies do so

for reasons having nothing to do with earning income. {Luce: 57 ER

770:3-772:4.}

Vander Nat relied on marketing and promotional material to

determine how BurnLounge was marketed but conceded at trial that

the promotional material he reviewed was that of independent retailers

and not authorized by BurnLounge. He never asked whether what he

received was a representative sample of what was available. {69 ER

1009:6-10.} And during testimony, he could not identify any

corporate-created promotional material at all. {Vander Nat: 69 ER

1007:23-1008:4.}

Before he had any company sales and financial data,

Vander Nat opined that BurnLounge was a pyramid. {See e.g. 90 ER

1214-1295 [excerpted declaration identifying factors considered].}

Case: 12-55926 01/04/2013 ID: 8462489 DktEntry: 21-1 Page: 28 of 69

20

PROCEDURAL HISTORY H.

1. THE CLAIMS IN ISSUE

The FTC claimed that BurnLounge was a pyramid, that

defendants made misleading income claims to promote the pyramid,

and that defendants concealed from Moguls that they were not likely

to make substantial income. {91 ER 1296-1306.} Shortly after the

complaint was filed, the parties stipulated to a preliminary injunction

prohibiting BurnLounge from operating the Mogul program. {89

ER.}

2. TRIAL

The non-jury trial took nine days. {ER, Tabs 59, 62, 64, 68, 71,

73, 76, 79, 80 [minute orders reflecting minutes of trial days]; see

also ER Tabs 15 and 60 [collectively lists of exhibits admitted at trial]

and 13 ER as amended by 4 ER 43 [list of disputed exhibits and court

ruling re: same].}

3. VANDER NAT TESTIMONY

At trial, Vander Nat testified that BurnLounge was a pyramid,

using his own four-pronged test (not the Koscot or the Omnitrition15

test). Vander Nat’s personal test considered (1) the terms of the

BurnLounge model (as enunciated by its Policies and Procedures and

Compensation Plan), (2) marketing materials by retailers, (3) his

15 In re Koscot Interplanetary, Inc., 86 F.T.C. 1106, 1181

(1975), aff’d mem. sub. nom Turner v. FTC, 580 F.2d 701 (D.C. Cir. 1978), and Webster v. Omnitrition International, 79 F.3d 776 (9th Cir. 1996)

Case: 12-55926 01/04/2013 ID: 8462489 DktEntry: 21-1 Page: 29 of 69

21

version of an optimal scenario pursuant to which participants are

trying to achieve the highest levels of rewards, and (4) company

financial data. {Vander Nat: 72 ER 1045:16-1046:6.} Vander Nat

admitted that he did not know whether the test would create results

consistent with the Koscot test {Vander Nat: 70 ER 1031:2-1032:5.}

and did not know whether his test could be applied in a way that

would ever differentiate between a legal MLM and an illegal pyramid.

{Vander Nat: 70 ER 1027:25-1028:4.} He had never studied any

legal MLM in depth, and using his test, he had yet to find any MLM

legal. He likewise admitted that this test had never been published.

{Vander Nat: 70 ER 1030:12-16.}

Vander Nat had published an article about how to distinguish

between legal MLMs and illegal pyramids. {Tr. Ex. 1130 [34 ER].}

In it, as well as in his trial testimony, he admitted to a number of

characteristics common to MLMs and illegal pyramids, including that

they both compensate for direct and indirect sales, encourage

recruitment, and operate through geometric progression. In both,

there are usually more “losers” than “winners.” 16 {Vander Nat: 69

ER 980:3-22, 981:15-18, 982:9-983:19; Tr. Exs. 417 [44 ER], 420 [43

ER]; See also Section III.A., summarizing the article’s concessions.}

16 Vander Nat assumed ‒ without any analysis or supporting

evidence ‒ that the amounts Moguls paid for the product packages and fees constituted an investment in the business. If Moguls did not receive more in commissions than they “invested,” they were “losers.” If their commissions exceeded their “investment,” they were “winners.” {69 ER 982:2-9.}

Case: 12-55926 01/04/2013 ID: 8462489 DktEntry: 21-1 Page: 30 of 69

22

Vander Nat did not use the test he developed in his own article. {67

ER 956:12-25.}

Vander Nat admitted that each of the items included in the

Basic, Exclusive and VIP packages were “products” {Vander Nat: 69

ER 987:1-988:16}, and that commissions paid on sales of those

packages were “related” to the sale of products. {Vander Nat: 69 ER

986:5-25.} However, he did not value the BurnLounge products,

claiming the inquiry irrelevant. {Vander Nat: 69 ER 989:14-992:9.}

He determined damages for operating an illegal pyramid by

comparing “money in” and “money out” for BurnLounge retailers,

and he calculated damages as the net losses resulting. Vander Nat did

not do any analysis to determine injury suffered by consumers on the

income claims, and he admitted that he did not know what the

damages for the making of income claims would be. {Vander Nat: 67

ER 957:24-959:1; 69 ER 1012:9-13.}

4. NOLTE TESTIMONY

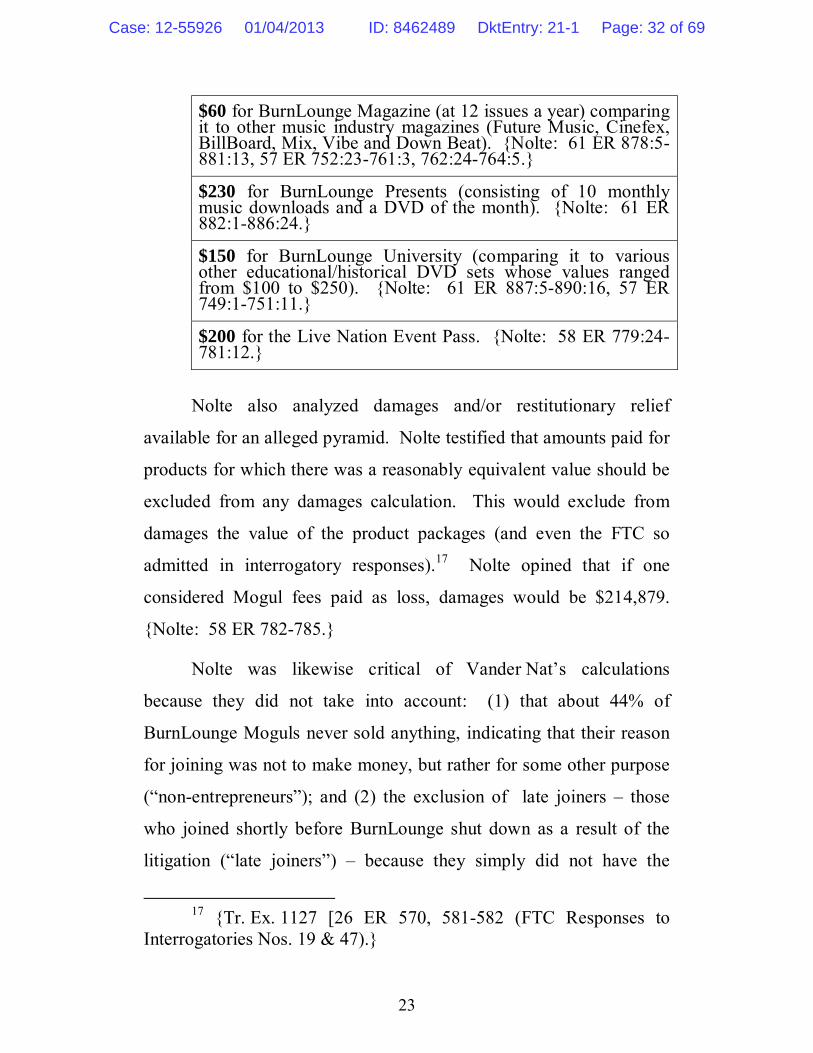

Defense expert David Nolte used a market approach, valuing

the individual products included in each of the three product packages

based on similar guideline transactions. {Nolte: 61 ER 871:8-9,

872:24-874:13.}

Nolte valued the various items in the product packages as

follows:

$400 for the e-store, comparing it to the e-stores by PayPal and Amazon. {Nolte: 61 ER 875:3-877:11; 57 ERT 746:7-748:4.}

Case: 12-55926 01/04/2013 ID: 8462489 DktEntry: 21-1 Page: 31 of 69

23

$60 for BurnLounge Magazine (at 12 issues a year) comparing it to other music industry magazines (Future Music, Cinefex, BillBoard, Mix, Vibe and Down Beat). {Nolte: 61 ER 878:5-881:13, 57 ER 752:23-761:3, 762:24-764:5.}

$230 for BurnLounge Presents (consisting of 10 monthly music downloads and a DVD of the month). {Nolte: 61 ER 882:1-886:24.}

$150 for BurnLounge University (comparing it to various other educational/historical DVD sets whose values ranged from $100 to $250). {Nolte: 61 ER 887:5-890:16, 57 ER 749:1-751:11.}

$200 for the Live Nation Event Pass. {Nolte: 58 ER 779:24-781:12.}

Nolte also analyzed damages and/or restitutionary relief

available for an alleged pyramid. Nolte testified that amounts paid for

products for which there was a reasonably equivalent value should be

excluded from any damages calculation. This would exclude from

damages the value of the product packages (and even the FTC so

admitted in interrogatory responses).17 Nolte opined that if one

considered Mogul fees paid as loss, damages would be $214,879.

{Nolte: 58 ER 782-785.}

Nolte was likewise critical of Vander Nat’s calculations

because they did not take into account: (1) that about 44% of

BurnLounge Moguls never sold anything, indicating that their reason

for joining was not to make money, but rather for some other purpose

(“non-entrepreneurs”); and (2) the exclusion of late joiners – those

who joined shortly before BurnLounge shut down as a result of the

litigation (“late joiners”) – because they simply did not have the

17 {Tr. Ex. 1127 [26 ER 570, 581-582 (FTC Responses to

Interrogatories Nos. 19 & 47).}

Case: 12-55926 01/04/2013 ID: 8462489 DktEntry: 21-1 Page: 32 of 69

24

opportunity to recoup their investment {Nolte: 58 ER 792:26-795:23;

Tr. Exs. 1051 [40 ER, 1139 [23 ER], 1140 [22 ER]; 57 ER 764-766.}

According to Nolte, if one started with Vander Nat’s methodology,

but then deducted for non-entrepreneurs and/or late joiners, the

resulting damages would be far less than Vander Nat’s calculations.

{Nolte: 58 ER 792:16-795:23 and Tr. Exs. 1139 [23 ER] and 1140

[22 ER].}

5. THE TRIAL COURT’S DENIAL OF BURNLOUNGE’S

DAUBERT MOTION TO EXCLUDE VANDER NAT’S

TESTIMONY

BurnLounge and Arnold moved to exclude Vander Nat’s

testimony pursuant to Daubert v. Merrell Dow Pharms., 509 U.S.579-

594 (1993) and Kumho Tire Co. v. Carmichael, 526 U.S. 137 (1999).

{65 ER 911-927.} The court heard Vander Nat’s testimony, reserving

jurisdiction to hear the motion. {16 ER 438.}

The court did not rule on appellants’ Daubert motion until

September 27, 2011{4 ER 42}, three months after the court had issued

its Statement of Decision {5 ER}, and 34 months after the conclusion

of trial. The “after-the-fact” order denying the motion is barely one

paragraph long, contains no reasoning as to why the court found

portions of Vander Nat’s testimony to be admissible; the order simply

states, in conclusory fashion, that, it found portions of the testimony to

be “credible/persuasive.”

Neither the order nor the Statement of Decision expressly states

what portions of Vander Nat’s testimony were deemed admissible and

what portions were not. However, the Statement of Decision shows

Case: 12-55926 01/04/2013 ID: 8462489 DktEntry: 21-1 Page: 33 of 69

25

that the court did, in fact, use the precise four-pronged test advocated

by Vander Nat (plan documents, marketing, optimal scenario and

company financial data) in order to make its pyramid finding. {5 ER

53-63.}

6. STATEMENT OF DECISION

The district court stated that under Koscot and Omnitrition, the

sine qua non of an illegal pyramid is “recruitment with rewards

unrelated to product sales.” {Id. at 63-64.} According to the court, it

had to determine what the business’ primary purpose was: whether to

sell or market products or to give rewards for recruitment of more

marketers or recruiters. {Id. at 64.} The court assumed that rewards

for recruitment and rewards for the sale of the product were mutually

exclusive.

The court found retailers could only achieve significant

financial returns through recruitment. {Id. at 67.} According to the

district court, this was evidenced by BurnLounge’s promotional

materials and by the representations of its independent retailers,

i.e., Exhibits 40 and 43, neither of which was prepared or circulated

by BurnLounge. {5 ER 64.}

The court found that the Mogul portion of the business

constituted a pyramid scheme. With respect to the Basic Package, the

court found that because participation in the program required the

purchase of a product package and Moguls earned commissions for

selling product packages to those they sponsored, these Moguls

received compensation for recruiting others into the program. The

Case: 12-55926 01/04/2013 ID: 8462489 DktEntry: 21-1 Page: 34 of 69

26

court acknowledged that the webstore could be considered a product

and the purchaser could be an end use of the product; however, the

court did not find these descriptions useful. According to the court,

this ignored the nature of the use – a tool for sales and for

recruitment. {5 ER 65.}18

The Exclusive and VIP Packages, beyond the first $29.95

charged, were not prerequisites for participation as a Mogul {id. at

66.}, but the court found that these two higher-priced packages were

also part of the pyramid structure because the value of the products in

the packages was extremely limited (without identifying a value), and

the purchase of these packages gave their purchasers the opportunity

to more quickly collect Mogul team bonuses:

“Specifically, the Exclusive and VIP Packages allowed participants to bypass the album-sales requirements to obtain higher Mogul Team Bonuses. . . In other words, a Basic Mogul could earn a $50 Mogul Team Bonus only after selling $1000 worth of music, but an Exclusive Mogul could earn the same after selling only $500 worth. A VIP Mogul could earn the $50 bonus from the start.” {Id. at 66-67.}

According to the court this was a part of the “business opportunity”

because it gave prospective Moguls reason to buy the

18The court continued that when BurnLounge began offering a

free basic package and untied the business opportunity from the Basic Package, the sales and fees related to the Basic Package were no longer linked to recruiting. {Id. at 66.}

Case: 12-55926 01/04/2013 ID: 8462489 DktEntry: 21-1 Page: 35 of 69

27

premium package without regard for the value received from the

products bundled within it. {5 ER 66-67.}19

The court also found that consumers were harmed by

BurnLounge’s pyramidal structure. But in making that finding, the

court found that consumer motivation in purchasing packages was

vital to the calculation of consumer harm:

“Because BurnLounge tied legitimate sales of products so closely with illegitimate pyramidal business opportunity, the motivation of consumers in purchasing the product packages [was] vital to the calculation of consumer harm.” {Id. at 69.}

The court noted that no party presented any kind of survey evidence

concerning consumer motivation. The court rejected the FTC’s claim

that consumers only sought the business opportunity, just as it rejected

BurnLounge’s claim that consumers primarily sought the value of the

product packages. {Id. at 69.}

Notwithstanding the conceded lack of evidence regarding

consumer motivation, the court elected to make its own estimates of

harm based on its own formula, adopting a mathematical formula not

advanced by any of the parties. {Id. at 69-70.} First, the court

factored out all Moguls that made a profit, concluding that those

Moguls were not harmed. With respect to the remainder, the court

assumed that the product packages each had some intrinsic value to

their purchasers, and that some purchasers purchased them for that

19 The court also found that misleading income statements were

made. {Id. at 67-68.} That finding is not being challenged here.

Case: 12-55926 01/04/2013 ID: 8462489 DktEntry: 21-1 Page: 36 of 69

28

intrinsic value. The court calculated damages for those who

purchased the Basic Package by assuming that about 10.8% of

Moguls who purchased that package would have done so anyway

(analogizing from non-Moguls who purchased the Basic Package),

and excluded that percentage from those harmed. The court found

that 89.2% of revenues from Basic Package sales reflected consumer

harm, amounting to $1,422,167.60. The court’s analysis did not

reduce its calculation of consumer harm by the value of the products

or by the amount of cash commissions paid to those Moguls.

The court used the same methodology to calculate consumer

harm to the purchasers of Exclusive and VIP upgrades to the Basic

Package, and came up with damages of $3,539,554.50 and

$9,376,691.40, respectively. Discounting those who likely purchased

Exclusive and VIP packages for their product value, the court found

harm from payment of the BLP monthly fee in the amount of

$1,907,386.20.

Thus the court found total harm to consumers to be

$16,245,799.70. {5 ER 69-70.}

The court held that Arnold was jointly and severally liable for

the above amount because he had the ability to control BurnLounge.

However, the court ruled that, if the FTC does not intend to use

recovered amounts to reimburse individuals who lost their

investments, Arnold would only have to disgorge the monies he

received from BurnLounge, which the court totaled as $1,664,566.45.

{Id. at 71-72.}

Case: 12-55926 01/04/2013 ID: 8462489 DktEntry: 21-1 Page: 37 of 69

29

7. THE JUDGMENT, POST-JUDGMENT MOTIONS, AND

THIS APPEAL

The court entered judgment on March 1, 2012. {3 ER.}

On March 29, 2012, appellants moved pursuant to

Fed.R.Civ.P. 59 to “alter or amend” the judgment in two respects:

(1) the motion argued that the court’s methodology in coming to its

damages number indisputably overstated consumer harm by failing to

take an account the November 1, 2006 amendment to the qualification

requirements under BurnLounge’s MLM compensation plan; and (2)

the motion also argued that the court’s disgorgement award against

Arnold in the amount of $1,664,506.45 was excessive because the

only (and undisputed) evidence in the record showed that Arnold only

received $593,732.01 from BurnLounge. {10 ER; 9 ER.}

The trial court denied appellants’ Rule 59 motion {2 ER; 1 ER

1-21.} This appeal followed. {8 ER.} Co-defendant John Taylor

likewise appealed. {7 ER} The FTC filed a cross-appeal from the

judgment as it applied to Rob DeBoer. {6 ER.} This court

subsequently ordered the appeals consolidated.

ARGUMENT IV.

THE DISTRICT COURT DID NOT CORRECTLY APPLY A.THE KOSCOT/OMNITRITION TEST FOR ANALYZING THE EXISTENCE OF A PYRAMID.

The district court cited a number of cases relating to what type

of business might constitute a pyramid, including Koscot, supra, 86

FTC at 1181; Omnitrition, supra, 79 F.3d at 782, FTC v. Five Star

Auto Club, Inc., 97 F.Supp.2d 502 (S.D.N.Y. 2000), Whole Living,

Case: 12-55926 01/04/2013 ID: 8462489 DktEntry: 21-1 Page: 38 of 69

30

Inc. v. Tolman, 344 F.Supp.2d 739 (D. Utah 2004), and In re Ger-Ro-

Mar, Inc., 518 F.2d 22 (2nd Cir. 1975), among others. {5 ER 63-66.}

But, the district court failed to take into account the critical (and result

determinative) differences between the business models involved in

those cases and BurnLounge’s MLM compensation plan. This failure

caused the district court, (a) to change and/or misapply the test for

what constitutes a pyramid, (b) to find for plaintiff without requiring

the FTC to meet its burden of proof on the elements of a pyramid

claim, and (c) to erroneously conclude that BurnLounge was a

pyramid.20

1. THE PYRAMID TEST

Pyramid schemes are characterized by:

“the payment by participants of money to the company in return for which they receive (1) the right to sell a product and (2) the right to receive in return for recruiting other participants into the program rewards which are unrelated to the sale of the product to ultimate users. Webster v. Omnitrition, 79 F.3d 766, 781 (9th Cir.

20 Whether BurnLounge is a pyramid under the

Koscot/Omnitrition test based on what constitutes a legitimate sale to ultimate users is an issue of law, to be interpreted de novo. See, e.g., Torres-Lopez v. May, 111 F.3d 976, 980 (9th Cir. 1997); California First Amendment Coalition v. Calderon, 150 F.3d 976, 980 (9th Cir. 1998). Whether the evidence adduced was sufficient to shift the burden to BurnLounge and Arnold is likewise a question of law, or at least a mixed question of fact and law, where legal issues predominate, thus requiring de novo review. United States v. Hinkson, 484 F.3d 1247, 1259-1260 (9th Cir. 2009). Where the judgment is dependent on a determination of disputed facts, the issue is reviewed for clear error. Purcell v. Gonzalez, 549 U.S. 1, 5 (2006).

Case: 12-55926 01/04/2013 ID: 8462489 DktEntry: 21-1 Page: 39 of 69

31

1996), quoting In re Koscot Interplanetary, Inc., 86 F.T.C. 1106, 1181 (1975), aff’d mem. sub nom., Turner v. FTC, 580 F.2d 710 (D.C. Cir. 1978).

The test recognizes that in legal MLMs, commissions reward

for dual purposes –for both recruitment and product sales. {See also

Section III.A., supra.} Only when commissions are not related to the

sale of products for legitimate use does an MLM become an illegal

pyramid. In other words, the fact that rewards bear some relationship

to recruitment does not justify a pyramid finding. The crux of the

inquiry is whether the rewards are related to the sale of legitimate

products for use. Were it otherwise, the test would find pyramidal any

business where a retailer is rewarded by commissions on indirect

product sales – a common characteristic of all MLMs.

Hence, if the products sold by an MLM are not a sham, have

value, are purchased by an end user (as opposed to being purchased

for resale), and the quantity purchased is not excessive (so as to raise

an inference that no one could purchase that much for his personal

use) there is no pyramid. The existence and value of the products

being sold is a material element of the test.

The FTC argued that the value of product packages was

irrelevant to pyramid liability, and the district court agreed. Indeed,

the court found that whether items in the product packages were

products, and whether purchasers were ultimate users, was not a

fruitful inquiry. {5 ER 65.} Hence, the court failed to apply the

second (and most important) half of a pyramid analysis: whether

Case: 12-55926 01/04/2013 ID: 8462489 DktEntry: 21-1 Page: 40 of 69

32

rewards for recruitment were unrelated to the sale of products to

ultimate users.

This is despite factual findings demonstrating that rewards paid

by BurnLounge for recruitment were, in fact, related to the sale of

products. Specifically:

1. An individual could purchase a product package for both

the bundled products and for the business opportunity.

{5 ER 60.}

2. The products were not a sham. {Id. at 53.}

3. The webstore was a tool for sales as well as recruitment.

{Id. at 65.}

4. Regardless of how one characterized the business

(pyramid or MLM), BurnLounge tied legitimate sales of

products to the business opportunity. {Id. at 68.}

These district court findings cannot be reconciled with a

determination that the sums paid for product packages did not “relate”

to legitimate retail sales. Nonetheless, the district court’s ultimate

decision ignores these findings; instead, the district court determined

that the value of products, and the character of product package sales

to end users, was irrelevant because such sales also rewarded for

recruitment. This constitutes error. Put more simply, the trial court

misapplied the test. The test does not require rewards to be unrelated

to recruitment; it more rigorously requires that the rewards be

completely unrelated to sales of bona fide products. The test does not

prohibit rewards that are related both to recruitment and to product

Case: 12-55926 01/04/2013 ID: 8462489 DktEntry: 21-1 Page: 41 of 69

33

sales. It is only when rewards for recruitment are unrelated to the sale

of products to the ultimate user that there is a problem of illegality.

The district court’s reasoning materially changes the pyramid

test: i.e., an MLM is a pyramid not when rewards for recruitment are

unrelated to the sale of products to the ultimate user, but when

rewards are solely for the sale of products and recruitment is not

rewarded at all. This would improperly render all MLMs illegal

pyramids since all MLMs (both legal and illegal) reward for

recruitment and for sales. {See Section III.A., supra.}

2. THE FTC HAD THE BURDEN OF PROVING THE

PRODUCTS AND PRODUCT PACKAGES LACKED

VALUE AND/OR DID NOT CONSTITUTE

LEGITIMATE SALES

The FTC has the burden of proving a violation of Section 5 of

the FTC Act. Ger-Ro-Mar, Inc. v. FTC, 518 F.2d 33, 36 (2d Cir.

1975).21 Because the Koscot/Omnitrition test requires that rewards

for recruitment be unrelated to the sale of products, the FTC may not

simply contend that the value of the products at issue here are

irrelevant. The test makes them directly relevant. And in order to

show that product sales were only a sham, the FTC had to prove that

the products sold did not themselves have value or were worthless, or

were purchased in such quantities that no one would buy that quantity

for their own personal consumption.22

21 See also, Dhillon v. BBC Holdings, Inc., 2009 U.S. Dist.

LEXIS 28865 (W.D. Wash. 2009) (“The burden of proof is Plaintiff's to establish all the elements of his claims”).

22 The district court acknowledged the materiality of these

Case: 12-55926 01/04/2013 ID: 8462489 DktEntry: 21-1 Page: 42 of 69

34

a. The Amway Decision, and the FTC’s Own Staff Advisory Opinion, Demonstrate The FTC’s Failure to Prove the Existence of a Pyramid

In In re Matter of Amway Corporation, Inc., 93 F.T.C. 618

(Initial Decision - 1979), distributors earned commissions (1) on the

sale of inventory – i.e. goods intended for further resale − to their

downline distributors as well as (2) on their downline distributors’

sale of inventory to distributors further downline. Not all of the

inventory was resold to customers. The evidence further showed that

distributors purchased products (to various degrees) for personal use

or consumption. In Re Matter of Amway Corporation, Inc., 93 F.T.C.

618, n.24 & 55-56 (Initial Decision - 1979) (finding that many

Amway distributors became distributors in order to buy the products

for their own consumption at the 30% distributor discount rate).

This was not found to be pyramidal. Amway23 cured the

inventory loading issue by enforcing a rule that distributors must sell a

proportion of their inventory to those outside the distribution tree.

On the district court’s reasoning in this case, Amway should

have been found pyramidal: in Amway, distributors received

commissions on inventory sales which their downline distributors

were required to buy in order that they be qualified to receive cash for

issues to liability in connection with BurnLounge’s summary judgment motion on liability. In the motion, the court found material and disputed (a) the retail value of the products contained within the product packages, and (b) why BurnLounge Moguls purchased the product packages. {83 ER 1123 [citing to the FTC’s fact nos. 20-30] and 1126.}

23 In contrast to Omnitrition, discussed at Section IV.2.b., infra.

Case: 12-55926 01/04/2013 ID: 8462489 DktEntry: 21-1 Page: 43 of 69

35

their own inventory sales, and so on. The rewards the Amway

distributors received were related both to recruitment and to sales.

The inventory sales were tools for recruitment and for sales.

The only difference between Amway and BurnLounge is that

BurnLounge did not require inventory purchases. Moguls did not

purchase more than a single product package, and the BurnLounge

product packages (unlike the inventory purchases in Amway) were

intended for use by the immediate purchaser, and not intended for

resale. Otherwise, as in Amway, the items in the product packages

were consumable products. And of course, even the district court’s

analysis recognizes that (a) there were those who purchased the

product packages without reference to the “business opportunity” and

(b) some individuals bought the product packages for both the value

of the package and the business opportunity.

Under Amway, BurnLounge should not be found a pyramid.

The fact that the items in the product packages purchased both by

non-Moguls and Moguls were intended for use by the purchasers and

not for resale does not convert a legitimate business into an illegal

pyramid.

The FTC’s own Staff Advisory Opinion confirms that the

existence of internal consumption (in this case a Mogul’s purchase of

a product package for use, not resale) does not constitute proof of a

pyramid. The critical question for the FTC was “whether the revenues

that primarily support the commissions paid to all participants are

generated from purchases of goods and services that are not simply

incidental to the purchase of the right to participate in a money-

Case: 12-55926 01/04/2013 ID: 8462489 DktEntry: 21-1 Page: 44 of 69

36

making venture.”24 {Luce: 57 ER 774-775 and Tr. Ex. 1049 [41 ER

623-625].} In order to determine this, the FTC had to show that the

products could not be purchased and used by the Mogul.

Indeed, Whole Living, Inc. v. Tolman confirms “[t]he fact that

the right to receive a commission originates from sponsorship does

not necessarily mean that all subsequent commissions are based

primarily on recruitment. (Whole Living, Inc. v. Tolman, 344 F. Supp.

2d 739, 745 (D. Utah 2004) (emphasis added.))

Instead of proving that BurnLounge’s product packages were a

sham, and would never be purchased for value or for consumption, the

FTC claimed that the products were irrelevant. The FTC relied on

mathematical models by their expert Vander Nat to show that if

Moguls follow the optimal scenario set out in the Compensation Plan,

then the business would grow geometrically and would ensure more

“losers” than “winners.”

As previously discussed, Vander Nat admitted that this could be

the case with a legal MLM as well. And Vander Nat’s evidence of a

pyramid here does not materially differ from the evidence offered by

the FTC in Ger-Ro-Mar – evidence the Ger-Ro-Mar court found

insufficient to prove a pyramid:

The sole evidence to support the Commission's holding that the plan is inherently unfair and deceptive is a mathematical formula, which shows that if each participant in the plan recruited only five new recruits each month and each of those in turn recruited five additional recruits in the following month, and this

24Again requiring evidence of buyer motivation.

Case: 12-55926 01/04/2013 ID: 8462489 DktEntry: 21-1 Page: 45 of 69

37

process were allowed to continue, at the end of only 12 months the number of participants would exceed 244 million, including presumably the entire staff of the FTC. The Commission concludes that this, in effect, is the impossible dream and that the siren song of Symbra'Ette must be stilled. We find no flaw in the mathematics or the extrapolation . . . However, we live in a real world and not fantasyland. Ger-Ro-Mar, supra, 518 F.2d at 37.

Evidence of market saturation is necessary before the FTC’s

theoretical mathematical formula could have any real-life

applications. As in Ger-Ro-Mar, the FTC offered no evidence of

market saturation, and the district court made no such finding.

Additionally, the evidence here showed that of Moguls, 40% were

Moguls only a part of the time. This demonstrated (1) that these

individuals were not consistently interested in or engaged in the

entrepreneurial side of the business; and/or (2) that as in other legal

MLMs, some just decided to drop out and not pursue the business.

The failure to consider market saturation and dropout rates defeats a

pyramid finding. (Compare Ger-Ro-Mar, 518 F.2d at 37 and fn. 4,

criticizing the lower court for not considering market saturation and

dropout rate.)

b. The Other Pyramid Cases Relied on by the District Court Are Distinguishable and by those Distinctions, Show that BurnLounge is Not a Pyramid

Omnitrition, Five Star Auto and Holiday Magic were

“inventory loading” cases.

In the Omnitrition model, “distributors could purchase as much

product as they wanted from the company for use or for resale, and

could purchase the products at a distributor discount. Distributors did

Case: 12-55926 01/04/2013 ID: 8462489 DktEntry: 21-1 Page: 46 of 69

38

not have any quotas of goods they had to buy or sell.25 Supervisors,

on the other hand, could earn monetary rewards. To do so, they were

required to order several thousand dollars’ worth of inventory, and

had to continue to meet that order quota thereafter to remain qualified.

Commissions were paid on downline purchase orders of thousands of

dollars in inventory, and that inventory was intended for resale.

Omnitrition, supra, 79 F.3d at 780-81. The Omnitrition court found

that commissions received on inventory purchases appeared “facially

unrelated” to the sale of products for consumption. Id. at 783. In

light of Omnitrition’s exorbitant inventory loading requirements, the

court held satisfaction of Koscot would require more than proof of

internal consumption. Id. at 783.

Applying Omnitrition’s reasoning, the payment of commissions

on the sale of products to Moguls (if they are the intended end user),

satisfies the requirement that commissions be paid on sales to the

ultimate end user. In BurnLounge, there was never a danger that

“people buy exorbitant amounts of products[ ] that would not be sold

in an average market.” Ibid. Even Vander Nat conceded this. {72 ER

1047:13-16.}

In Five Star Auto, 97 F.Supp.2d 502, a pyramid was found

where participants were promised the ability to purchase or lease a car

for free in the future, based on their sale of memberships into the

organization. Commissions were not paid on the sale of cars, but on

the membership dues paid by downline participants. And these

25 This portion of the business was not considered pyramidal.

Case: 12-55926 01/04/2013 ID: 8462489 DktEntry: 21-1 Page: 47 of 69

39

commissions would never be enough to pay for a vehicle. So the

participants did not receive value, but rather only the promise of

future rewards if they recruited others. Id. at p. 510-512.

By contrast, BurnLounge was able to pay all commissions from

the sale of its products. Everyone who purchased a product package

actually received one. The only fee that was arguably a membership

fee was the $6.95 Mogul Fee that allowed Moguls to convert points

into cash. But that fee, because it was not money generated from the

sale of a product, was expressly not commissionable. {75 ER 1060

34:9-11.}

In re the Matter of Holiday Magic, Inc., 84 F.T.C. 748, 1974

FTC Lexis 56 [Part I],*6-13, *51-63. (1971)26 involved (cosmetics)

inventory loading. To be eligible for commissions, distributors had

to purchase $5,000 of inventory monthly. Commissions were paid on

inventory purchases made by downline distributors, with no regard

for use or sales. Id. at *79-88. Additionally, all distributors were paid

a finder’s fee for each new recruit they brought in. Id. at *77. As

with Omnitrition, there was no evidence that any retail sales occurred

on the exorbitant inventory purchases. 84 F.T.C. [II] at p. 47-48.

c. BurnLounge did not Share Any of the Improper Characteristics of Omnitrition, Five Star Auto or Holiday Magic

In an “inventory loading” case, where products intended for

resale are sold to middlemen, the fact that substantial resale actually

26 Holiday Magic is divided into two parts on Lexis.

References to Part I and II shall be referred to as 84 F.T.C. [I] and [II], respectively, followed by the page number.

Case: 12-55926 01/04/2013 ID: 8462489 DktEntry: 21-1 Page: 48 of 69

40

occurs to consumers who are not MLM members is important to the

determination of whether an MLM is a pyramid. The operative