non banking financial company

TRANSCRIPT

MIS PresentationMIS Presentation

Non Banking Financial Company (NBFC)Non Banking Financial Company (NBFC)

9/9/20099/9/2009Non Banking Financial Company (NBFC)Non Banking Financial Company (NBFC)

11

MIS PresentationMIS Presentation

Non Banking Financial Company (NBFC)Non Banking Financial Company (NBFC)

GROUPGROUP AJAY K. DHAMIJAAJAY K. DHAMIJA NN--11 MANDEEP SINGH REKHIMANDEEP SINGH REKHI NN--2727 RAGHAV RAJ BUDHIRAJARAGHAV RAJ BUDHIRAJA NN--3939 RAVINDER SINGHRAVINDER SINGH NN--4141 TRIPAT PREET SINGHTRIPAT PREET SINGH NN--4343 SNEHAL SONISNEHAL SONI NN--4747 KUNAL KAPURKUNAL KAPUR NN--6969

9/9/20099/9/2009Non Banking Financial Company (NBFC)Non Banking Financial Company (NBFC)

22

AJAY K. DHAMIJAAJAY K. DHAMIJA NN--11 MANDEEP SINGH REKHIMANDEEP SINGH REKHI NN--2727 RAGHAV RAJ BUDHIRAJARAGHAV RAJ BUDHIRAJA NN--3939 RAVINDER SINGHRAVINDER SINGH NN--4141 TRIPAT PREET SINGHTRIPAT PREET SINGH NN--4343 SNEHAL SONISNEHAL SONI NN--4747 KUNAL KAPURKUNAL KAPUR NN--6969

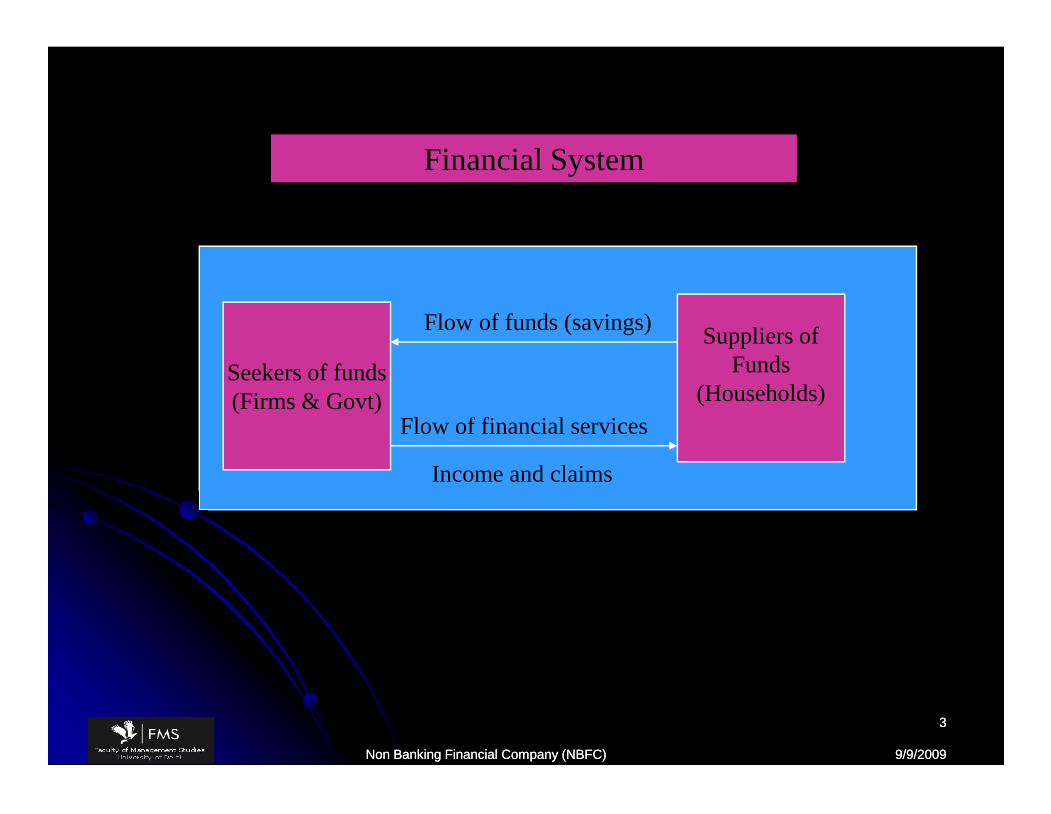

Financial System

Seekers of funds(Firms & Govt)

Suppliers ofFunds

(Households)

Flow of funds (savings)

Flow of financial services

9/9/20099/9/2009Non Banking Financial Company (NBFC)Non Banking Financial Company (NBFC)

33

Seekers of funds(Firms & Govt)

Suppliers ofFunds

(Households)Flow of financial services

Income and claims

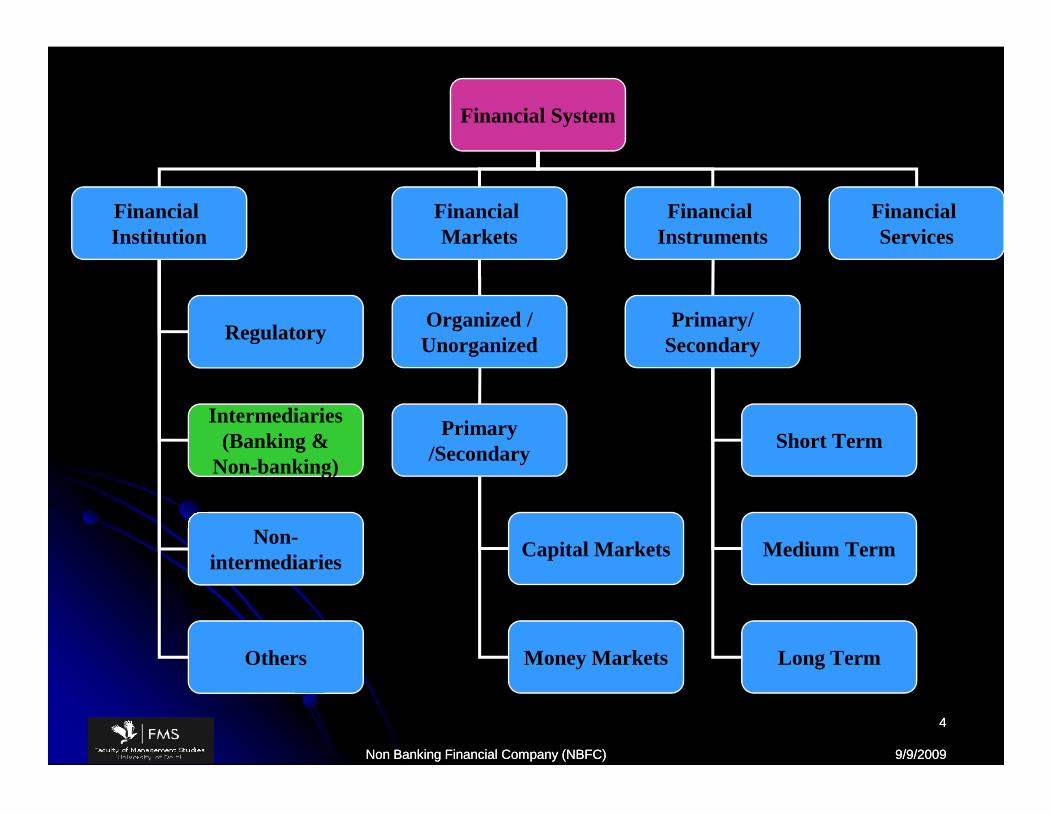

Financial System

FinancialInstitution

FinancialMarkets

FinancialInstruments

FinancialServices

Regulatory

Intermediaries(Banking &

Non-banking)

Organized /Unorganized

Primary/Secondary

9/9/20099/9/2009Non Banking Financial Company (NBFC)Non Banking Financial Company (NBFC)

44

Intermediaries(Banking &

Non-banking)

Non-intermediaries

Others

Primary/Secondary

Capital Markets

Money Markets

Short Term

Medium Term

Long Term

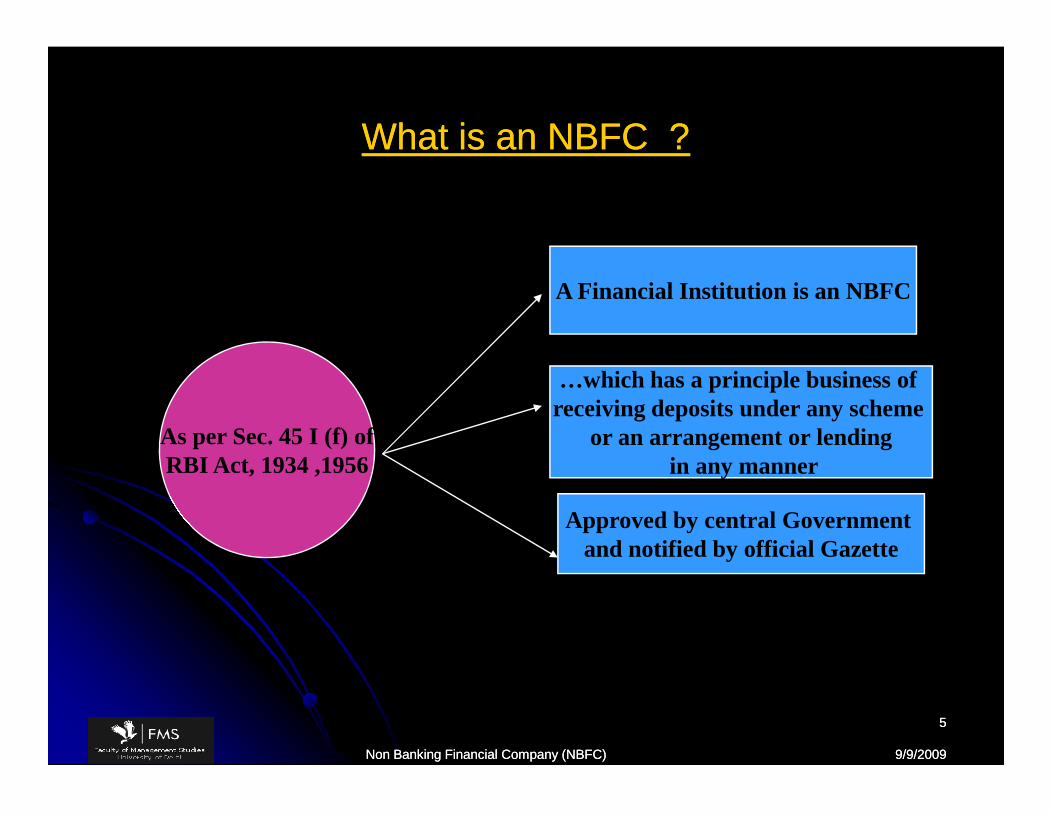

What is an NBFC ?What is an NBFC ?

A Financial Institution is an NBFC

…which has a principle business ofreceiving deposits under any scheme

or an arrangement or lendingin any manner

9/9/20099/9/2009Non Banking Financial Company (NBFC)Non Banking Financial Company (NBFC)

55

As per Sec. 45 I (f) ofRBI Act, 1934 ,1956

…which has a principle business ofreceiving deposits under any scheme

or an arrangement or lendingin any manner

Approved by central Governmentand notified by official Gazette

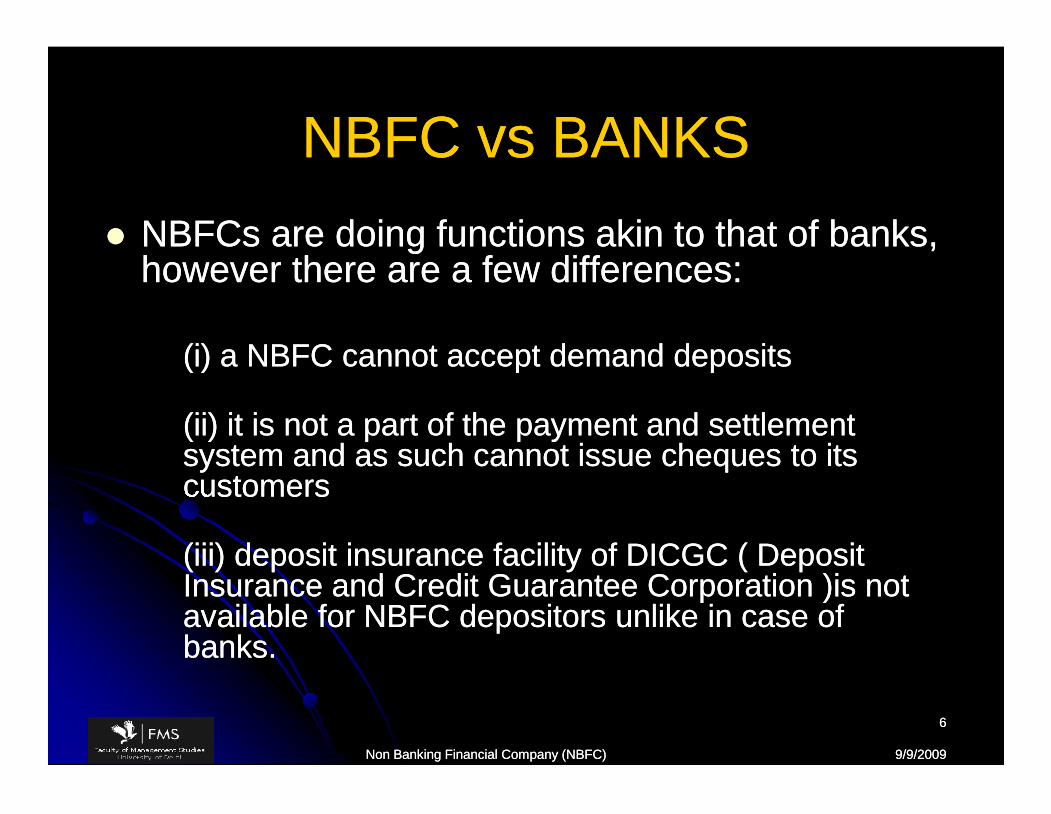

NBFC vs BANKSNBFC vs BANKS NBFCs are doing functions akin to that of banks,NBFCs are doing functions akin to that of banks,

however there are a few differences:however there are a few differences:

(i) a NBFC cannot accept demand deposits(i) a NBFC cannot accept demand deposits

(ii) it is not a part of the payment and settlement(ii) it is not a part of the payment and settlementsystem and as such cannot issue cheques to itssystem and as such cannot issue cheques to itscustomerscustomers

(iii) deposit insurance facility of DICGC ( Deposit(iii) deposit insurance facility of DICGC ( DepositInsurance and Credit Guarantee Corporation )is notInsurance and Credit Guarantee Corporation )is notavailable for NBFC depositors unlike in case ofavailable for NBFC depositors unlike in case ofbanks.banks.

9/9/20099/9/2009Non Banking Financial Company (NBFC)Non Banking Financial Company (NBFC)

66

NBFCs are doing functions akin to that of banks,NBFCs are doing functions akin to that of banks,however there are a few differences:however there are a few differences:

(i) a NBFC cannot accept demand deposits(i) a NBFC cannot accept demand deposits

(ii) it is not a part of the payment and settlement(ii) it is not a part of the payment and settlementsystem and as such cannot issue cheques to itssystem and as such cannot issue cheques to itscustomerscustomers

(iii) deposit insurance facility of DICGC ( Deposit(iii) deposit insurance facility of DICGC ( DepositInsurance and Credit Guarantee Corporation )is notInsurance and Credit Guarantee Corporation )is notavailable for NBFC depositors unlike in case ofavailable for NBFC depositors unlike in case ofbanks.banks.

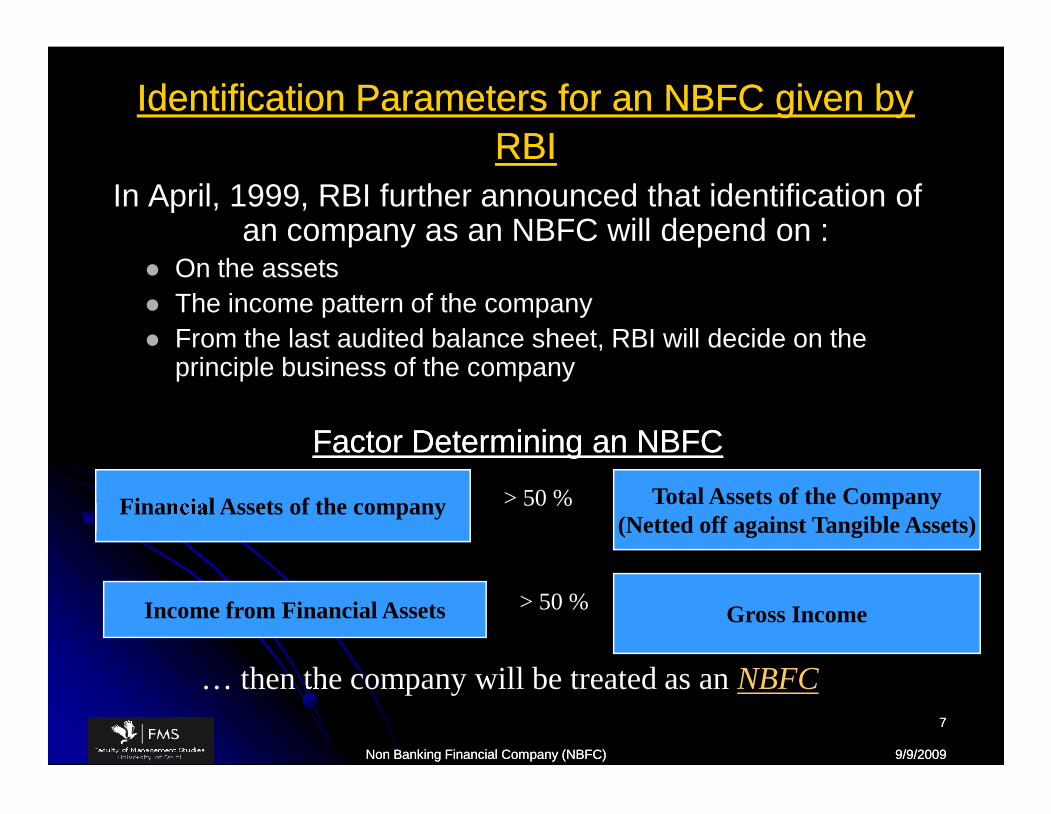

In April, 1999, RBI further announced that identification ofan company as an NBFC will depend on :

On the assets The income pattern of the company From the last audited balance sheet, RBI will decide on the

principle business of the company

Factor Determining an NBFCFactor Determining an NBFC

Identification Parameters for an NBFC given byIdentification Parameters for an NBFC given byRBIRBI

9/9/20099/9/2009Non Banking Financial Company (NBFC)Non Banking Financial Company (NBFC)

77

In April, 1999, RBI further announced that identification ofan company as an NBFC will depend on :

On the assets The income pattern of the company From the last audited balance sheet, RBI will decide on the

principle business of the company

Factor Determining an NBFCFactor Determining an NBFC

Financial Assets of the company Total Assets of the Company(Netted off against Tangible Assets)

Income from Financial Assets Gross Income

> 50 %

> 50 %

… then the company will be treated as an NBFC

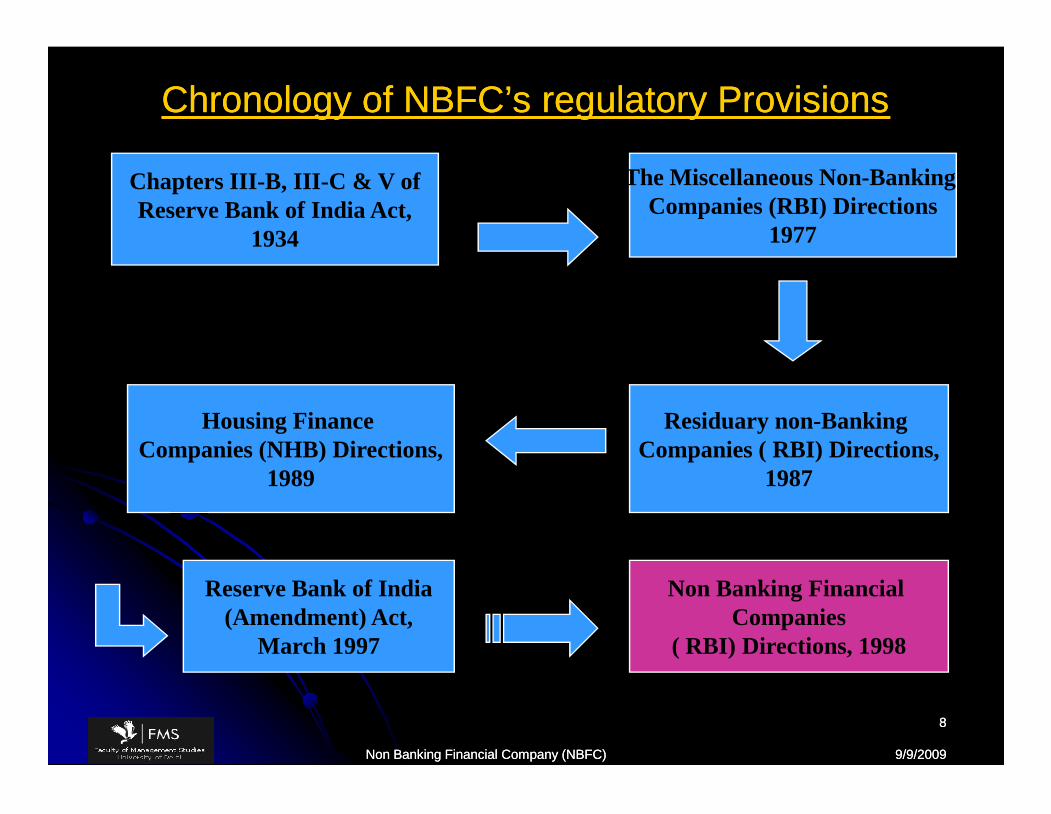

Chronology of NBFC’s regulatory ProvisionsChronology of NBFC’s regulatory Provisions

Chapters III-B, III-C & V ofReserve Bank of India Act,

1934

The Miscellaneous Non-BankingCompanies (RBI) Directions

1977

Housing FinanceCompanies (NHB) Directions,

1989

Residuary non-BankingCompanies ( RBI) Directions,

1987

9/9/20099/9/2009Non Banking Financial Company (NBFC)Non Banking Financial Company (NBFC)

88

Housing FinanceCompanies (NHB) Directions,

1989

Residuary non-BankingCompanies ( RBI) Directions,

1987

Reserve Bank of India(Amendment) Act,

March 1997

Non Banking FinancialCompanies

( RBI) Directions, 1998

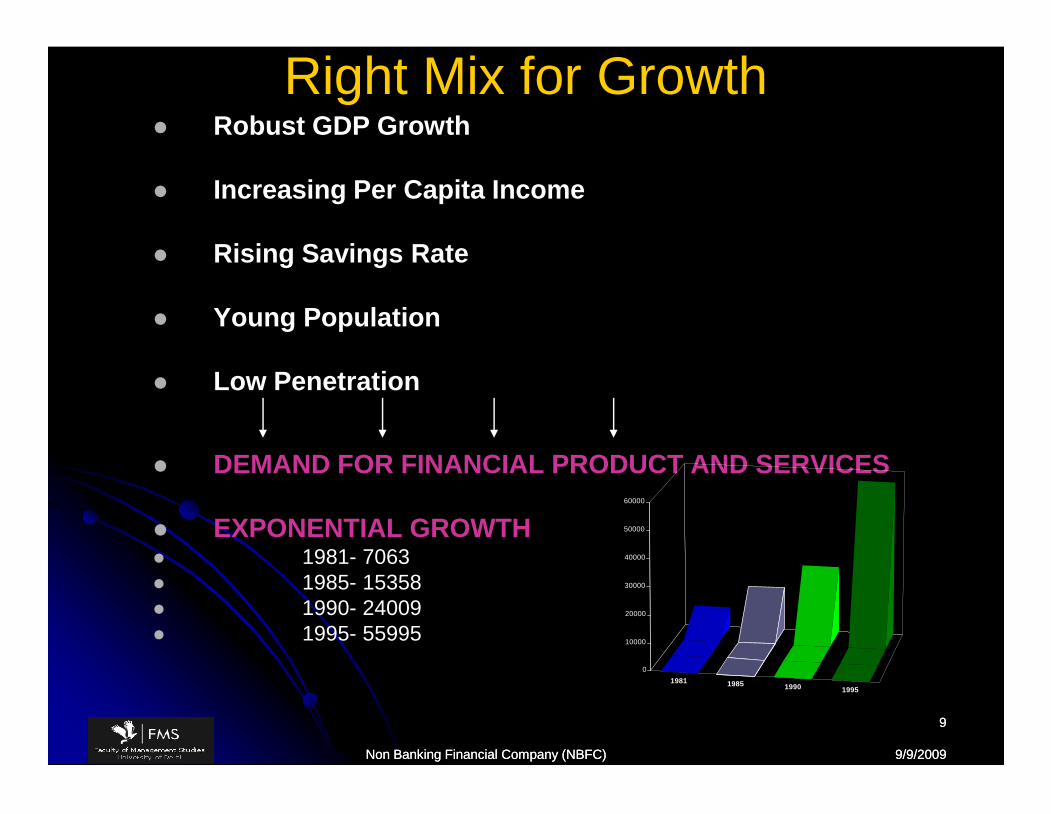

Right Mix for Growth Robust GDP Growth

Increasing Per Capita Income

Rising Savings Rate

Young Population

Low Penetration

DEMAND FOR FINANCIAL PRODUCT AND SERVICES

EXPONENTIAL GROWTH 1981- 7063 1985- 15358 1990- 24009 1995- 55995

9/9/20099/9/2009Non Banking Financial Company (NBFC)Non Banking Financial Company (NBFC)

99

Robust GDP Growth

Increasing Per Capita Income

Rising Savings Rate

Young Population

Low Penetration

DEMAND FOR FINANCIAL PRODUCT AND SERVICES

EXPONENTIAL GROWTH 1981- 7063 1985- 15358 1990- 24009 1995- 55995

1981 1985 1990 1995

0

10000

20000

30000

40000

50000

60000

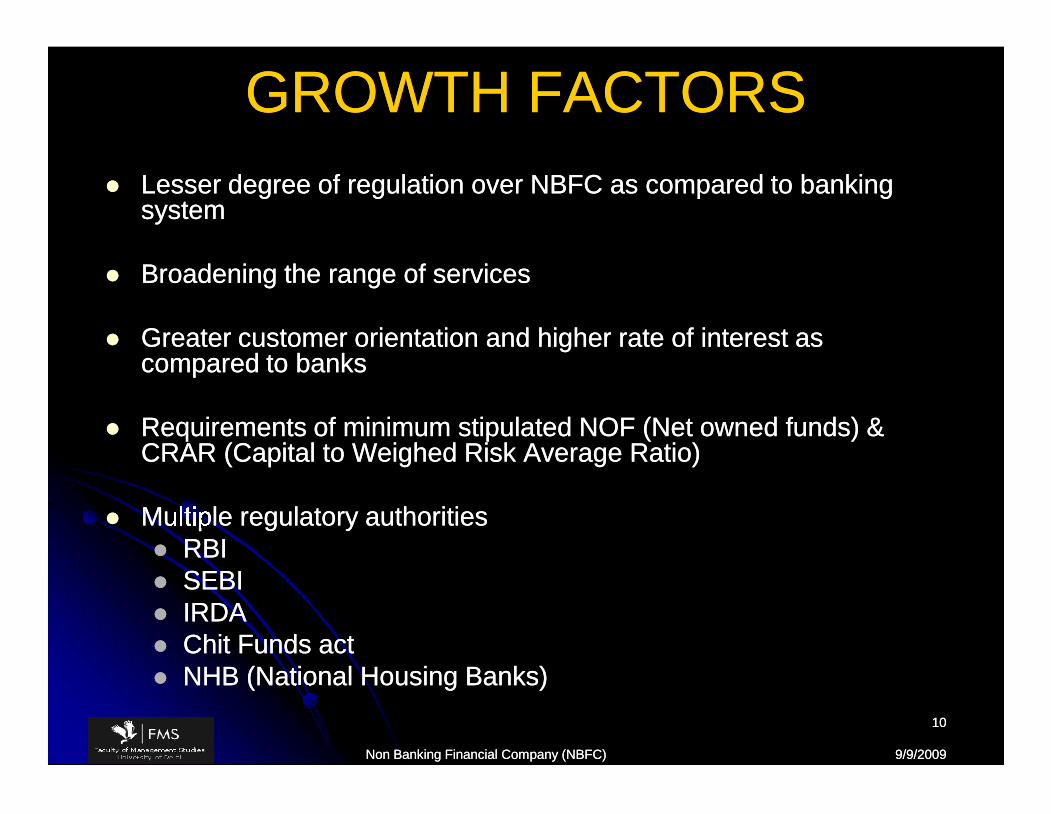

GROWTH FACTORSGROWTH FACTORS Lesser degree of regulation over NBFC as compared to bankingLesser degree of regulation over NBFC as compared to banking

systemsystem

Broadening the range of servicesBroadening the range of services

Greater customer orientation and higher rate of interest asGreater customer orientation and higher rate of interest ascompared to bankscompared to banks

Requirements of minimum stipulated NOF (Net owned funds) &Requirements of minimum stipulated NOF (Net owned funds) &CRAR (Capital to Weighed Risk Average Ratio)CRAR (Capital to Weighed Risk Average Ratio)

Multiple regulatory authoritiesMultiple regulatory authorities RBIRBI SEBISEBI IRDAIRDA Chit Funds actChit Funds act NHB (National Housing Banks)NHB (National Housing Banks)

9/9/20099/9/2009Non Banking Financial Company (NBFC)Non Banking Financial Company (NBFC)

1010

Lesser degree of regulation over NBFC as compared to bankingLesser degree of regulation over NBFC as compared to bankingsystemsystem

Broadening the range of servicesBroadening the range of services

Greater customer orientation and higher rate of interest asGreater customer orientation and higher rate of interest ascompared to bankscompared to banks

Requirements of minimum stipulated NOF (Net owned funds) &Requirements of minimum stipulated NOF (Net owned funds) &CRAR (Capital to Weighed Risk Average Ratio)CRAR (Capital to Weighed Risk Average Ratio)

Multiple regulatory authoritiesMultiple regulatory authorities RBIRBI SEBISEBI IRDAIRDA Chit Funds actChit Funds act NHB (National Housing Banks)NHB (National Housing Banks)

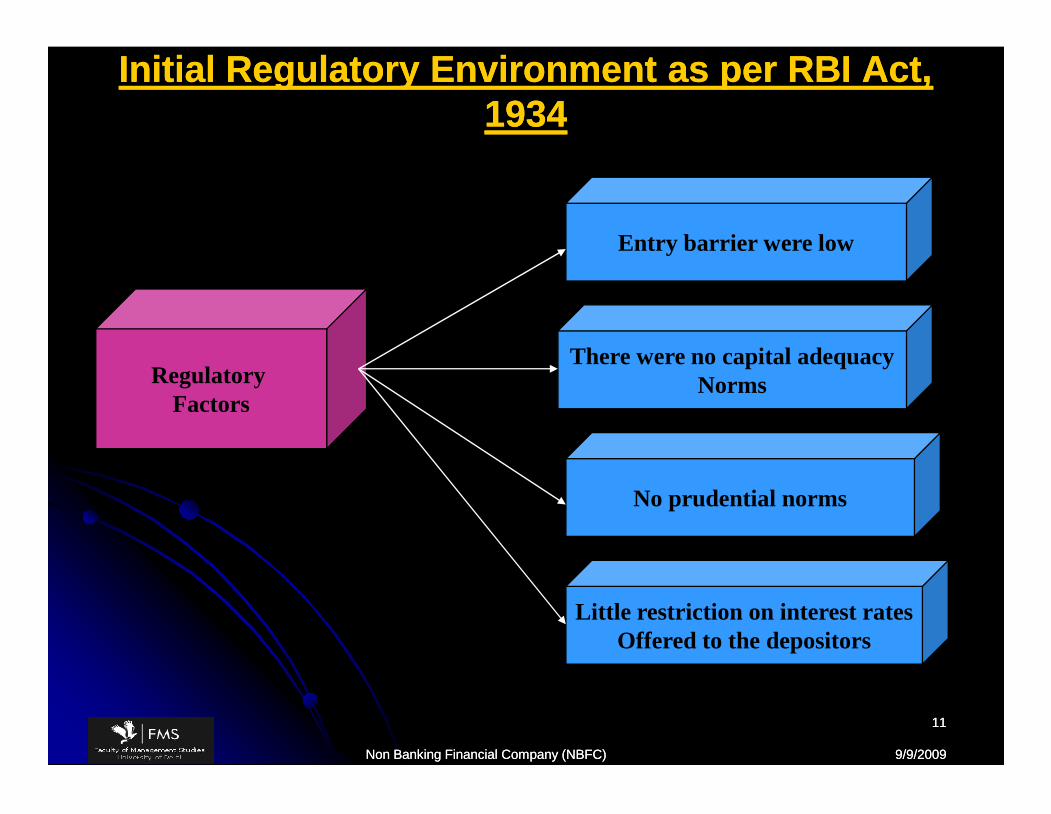

Initial Regulatory Environment as per RBI Act,Initial Regulatory Environment as per RBI Act,19341934

RegulatoryFactors

Entry barrier were low

There were no capital adequacyNorms

9/9/20099/9/2009Non Banking Financial Company (NBFC)Non Banking Financial Company (NBFC)

1111

RegulatoryFactors

No prudential norms

Little restriction on interest ratesOffered to the depositors

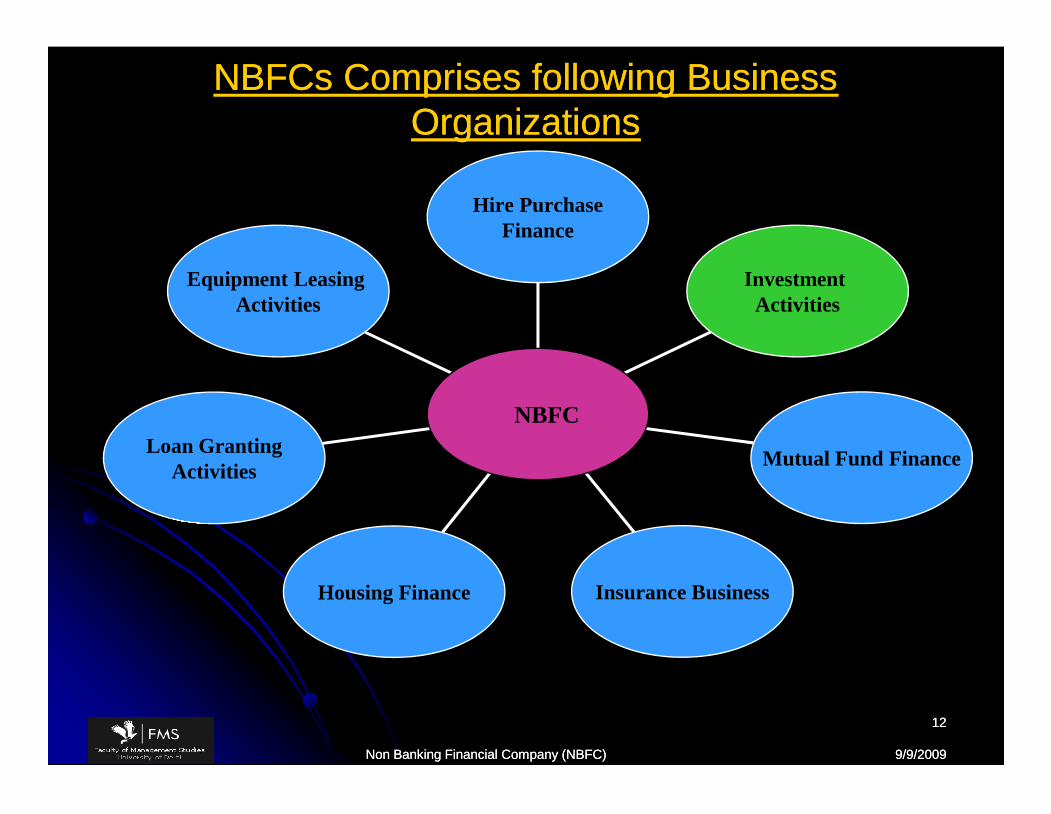

NBFCs Comprises following BusinessNBFCs Comprises following BusinessOrganizationsOrganizations

Equipment LeasingActivities

InvestmentActivities

Hire PurchaseFinance

NBFC

9/9/20099/9/2009Non Banking Financial Company (NBFC)Non Banking Financial Company (NBFC)

1212

Loan GrantingActivities

Housing Finance Insurance Business

Mutual Fund Finance

NBFC

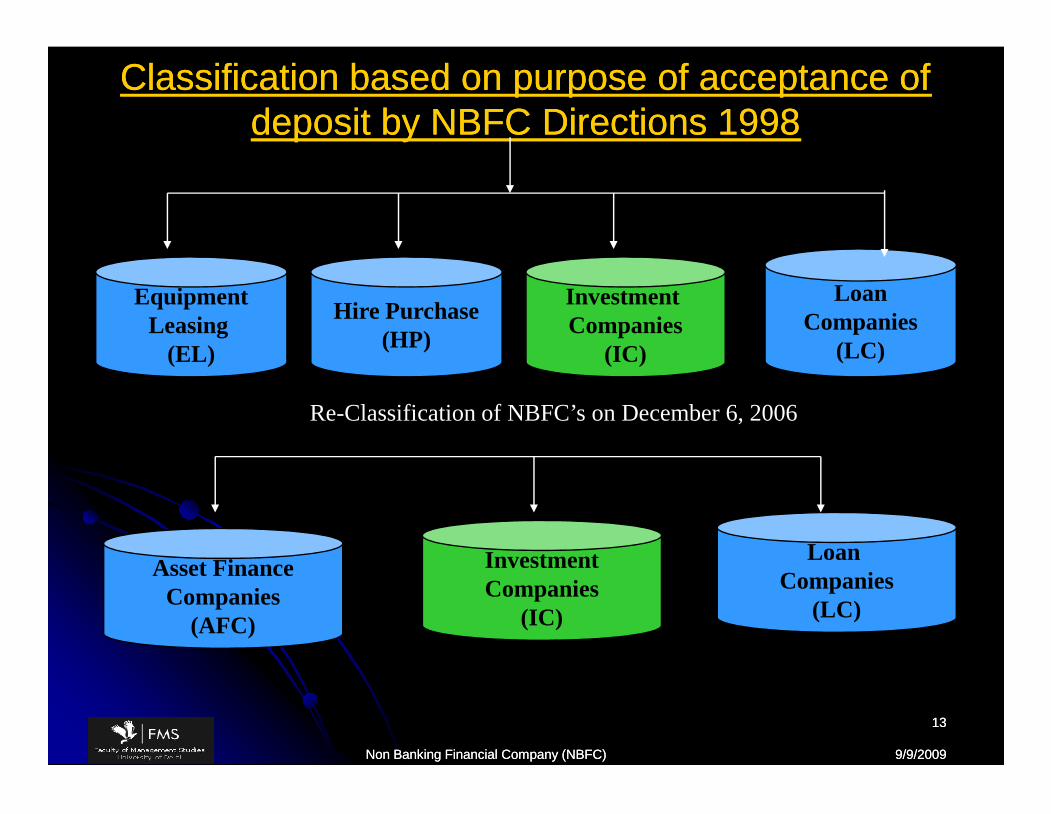

Classification based on purpose of acceptance ofClassification based on purpose of acceptance ofdeposit by NBFC Directions 1998deposit by NBFC Directions 1998

EquipmentLeasing

(EL)

Hire Purchase(HP)

InvestmentCompanies

(IC)

LoanCompanies

(LC)

Re-Classification of NBFC’s on December 6, 2006

9/9/20099/9/2009Non Banking Financial Company (NBFC)Non Banking Financial Company (NBFC)

1313

Asset FinanceCompanies

(AFC)

InvestmentCompanies

(IC)

LoanCompanies

(LC)

Re-Classification of NBFC’s on December 6, 2006

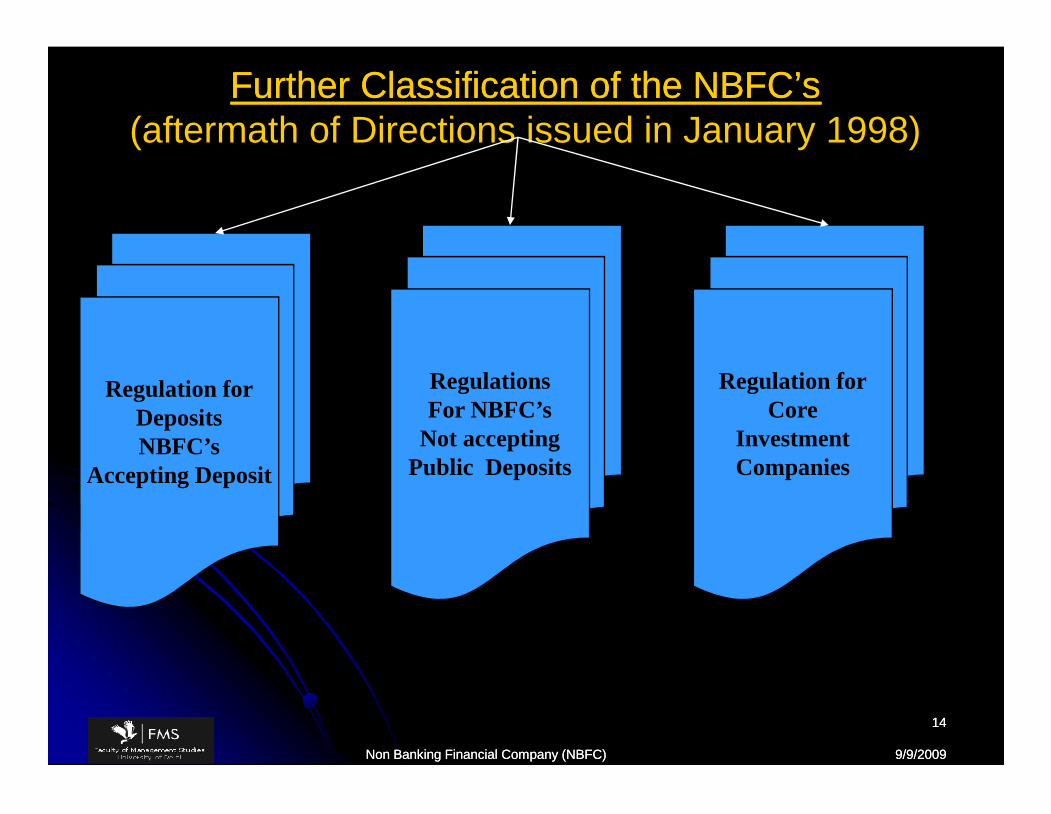

Further Classification of the NBFC’sFurther Classification of the NBFC’s(aftermath of Directions issued in January 1998)

Regulation forDepositsNBFC’s

Accepting Deposit

Regulation forCore

InvestmentCompanies

RegulationsFor NBFC’s

Not acceptingPublic Deposits

9/9/20099/9/2009Non Banking Financial Company (NBFC)Non Banking Financial Company (NBFC)

1414

Regulation forDepositsNBFC’s

Accepting Deposit

Regulation forCore

InvestmentCompanies

RegulationsFor NBFC’s

Not acceptingPublic Deposits

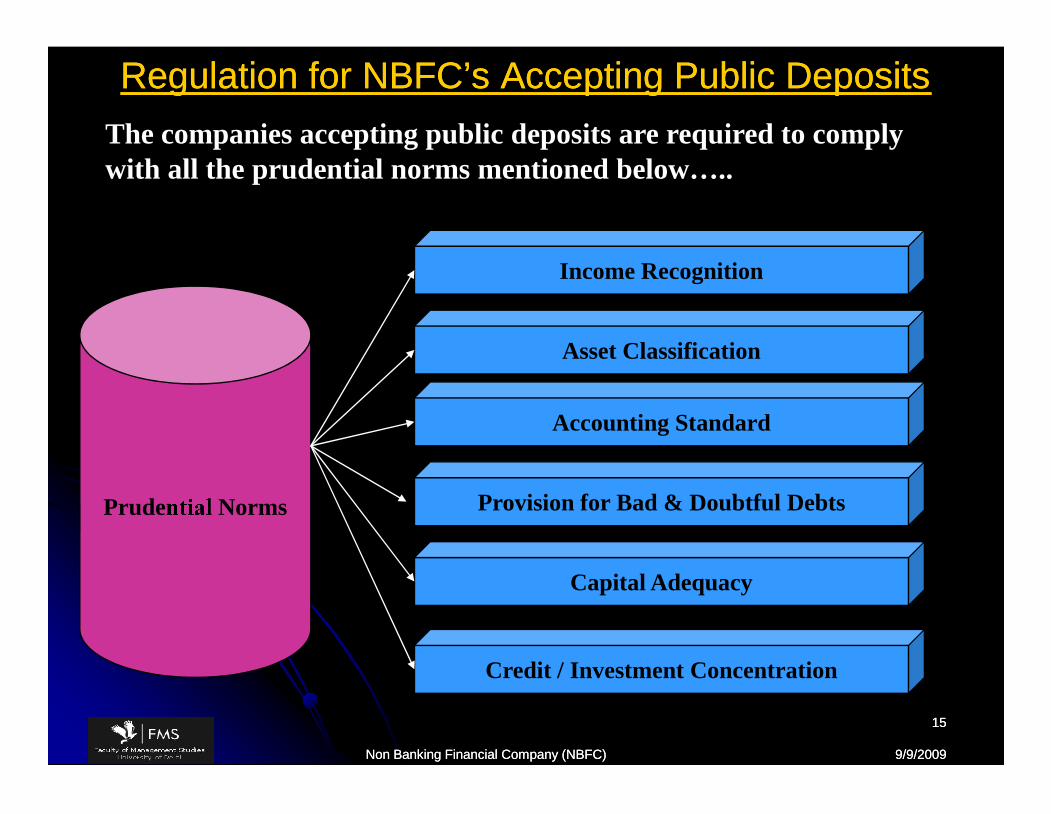

Regulation for NBFC’s Accepting Public DepositsRegulation for NBFC’s Accepting Public DepositsThe companies accepting public deposits are required to complywith all the prudential norms mentioned below…..

Income Recognition

Asset Classification

Accounting Standard

9/9/20099/9/2009Non Banking Financial Company (NBFC)Non Banking Financial Company (NBFC)

1515

Prudential Norms

Accounting Standard

Provision for Bad & Doubtful Debts

Capital Adequacy

Credit / Investment Concentration

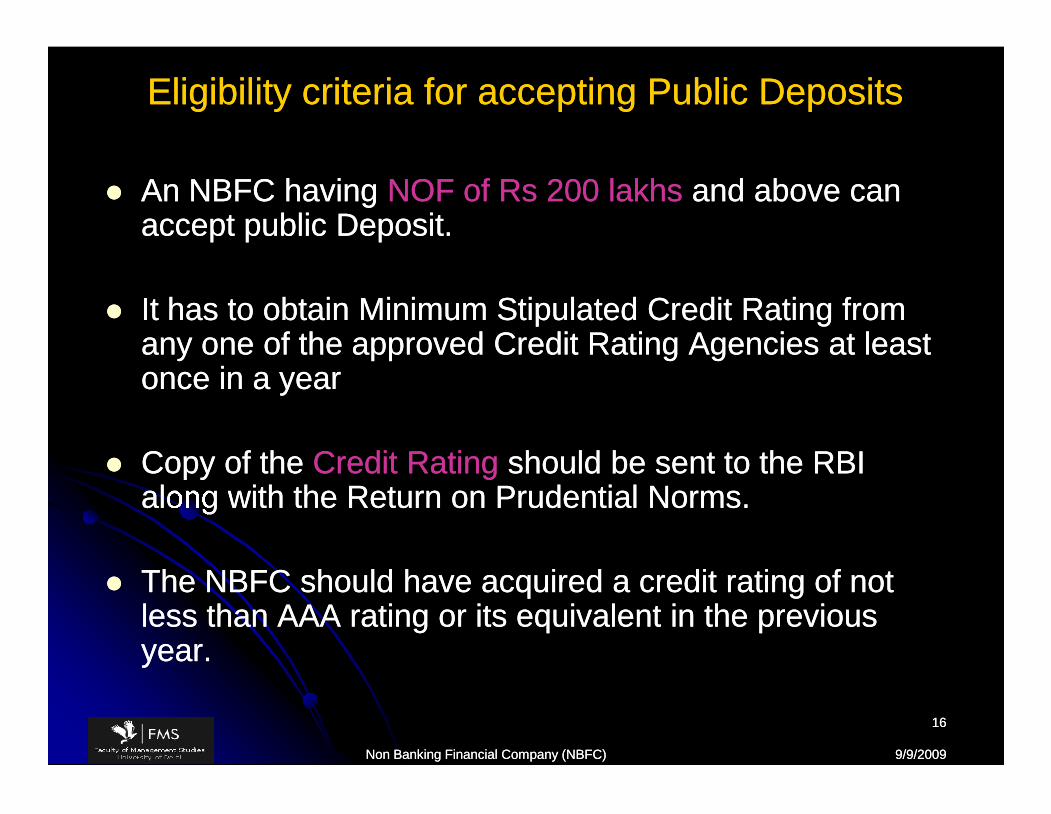

Eligibility criteria for accepting Public DepositsEligibility criteria for accepting Public Deposits

An NBFC havingAn NBFC having NOF of Rs 200 lakhsNOF of Rs 200 lakhs and above canand above canaccept public Deposit.accept public Deposit.

It has to obtain Minimum Stipulated Credit Rating fromIt has to obtain Minimum Stipulated Credit Rating fromany one of the approved Credit Rating Agencies at leastany one of the approved Credit Rating Agencies at leastonce in a yearonce in a year

Copy of theCopy of the Credit RatingCredit Rating should be sent to the RBIshould be sent to the RBIalong with the Return on Prudential Norms.along with the Return on Prudential Norms.

The NBFC should have acquired a credit rating of notThe NBFC should have acquired a credit rating of notless than AAA rating or its equivalent in the previousless than AAA rating or its equivalent in the previousyear.year.

9/9/20099/9/2009Non Banking Financial Company (NBFC)Non Banking Financial Company (NBFC)

1616

An NBFC havingAn NBFC having NOF of Rs 200 lakhsNOF of Rs 200 lakhs and above canand above canaccept public Deposit.accept public Deposit.

It has to obtain Minimum Stipulated Credit Rating fromIt has to obtain Minimum Stipulated Credit Rating fromany one of the approved Credit Rating Agencies at leastany one of the approved Credit Rating Agencies at leastonce in a yearonce in a year

Copy of theCopy of the Credit RatingCredit Rating should be sent to the RBIshould be sent to the RBIalong with the Return on Prudential Norms.along with the Return on Prudential Norms.

The NBFC should have acquired a credit rating of notThe NBFC should have acquired a credit rating of notless than AAA rating or its equivalent in the previousless than AAA rating or its equivalent in the previousyear.year.

Eligibility criteria for accepting Public DepositsEligibility criteria for accepting Public Deposits

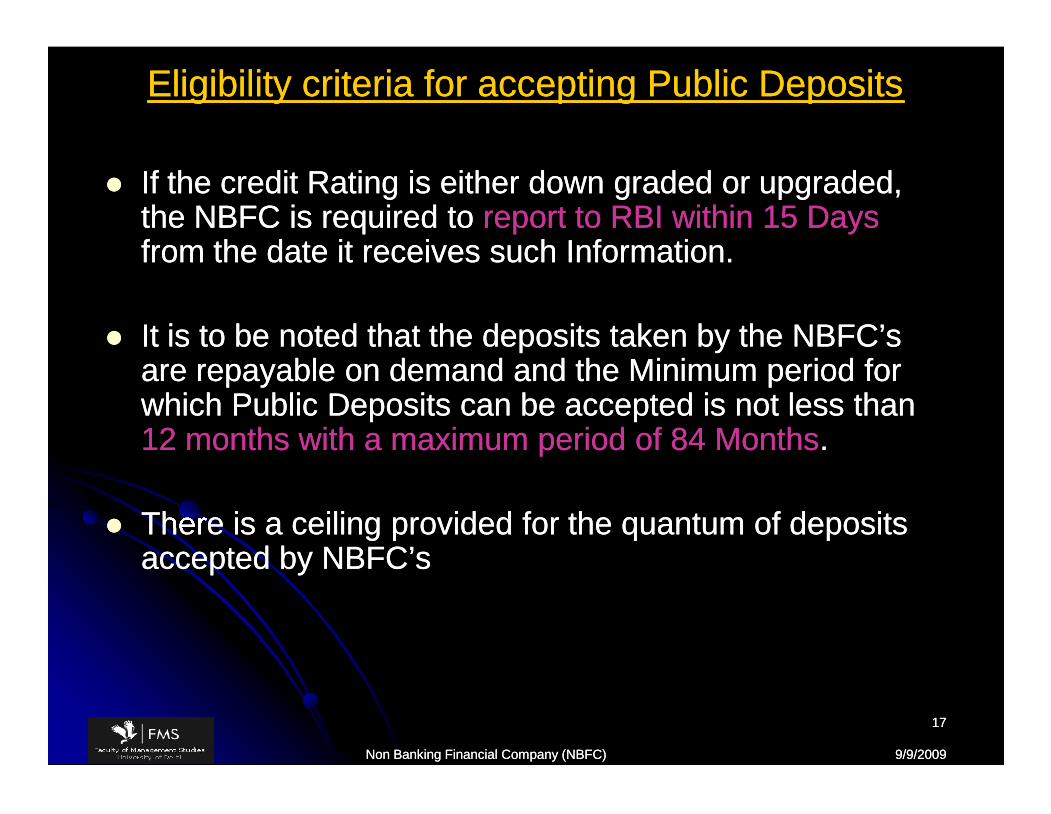

If the credit Rating is either down graded or upgraded,If the credit Rating is either down graded or upgraded,the NBFC is required tothe NBFC is required to report to RBI within 15 Daysreport to RBI within 15 Daysfrom the date it receives such Information.from the date it receives such Information.

It is to be noted that the deposits taken by the NBFC’sIt is to be noted that the deposits taken by the NBFC’sare repayable on demand and the Minimum period forare repayable on demand and the Minimum period forwhich Public Deposits can be accepted is not less thanwhich Public Deposits can be accepted is not less than12 months with a maximum period of 84 Months12 months with a maximum period of 84 Months..

There is a ceiling provided for the quantum of depositsThere is a ceiling provided for the quantum of depositsaccepted by NBFC’saccepted by NBFC’s

9/9/20099/9/2009Non Banking Financial Company (NBFC)Non Banking Financial Company (NBFC)

1717

If the credit Rating is either down graded or upgraded,If the credit Rating is either down graded or upgraded,the NBFC is required tothe NBFC is required to report to RBI within 15 Daysreport to RBI within 15 Daysfrom the date it receives such Information.from the date it receives such Information.

It is to be noted that the deposits taken by the NBFC’sIt is to be noted that the deposits taken by the NBFC’sare repayable on demand and the Minimum period forare repayable on demand and the Minimum period forwhich Public Deposits can be accepted is not less thanwhich Public Deposits can be accepted is not less than12 months with a maximum period of 84 Months12 months with a maximum period of 84 Months..

There is a ceiling provided for the quantum of depositsThere is a ceiling provided for the quantum of depositsaccepted by NBFC’saccepted by NBFC’s

Eligibility criteria for accepting Public DepositsEligibility criteria for accepting Public Deposits

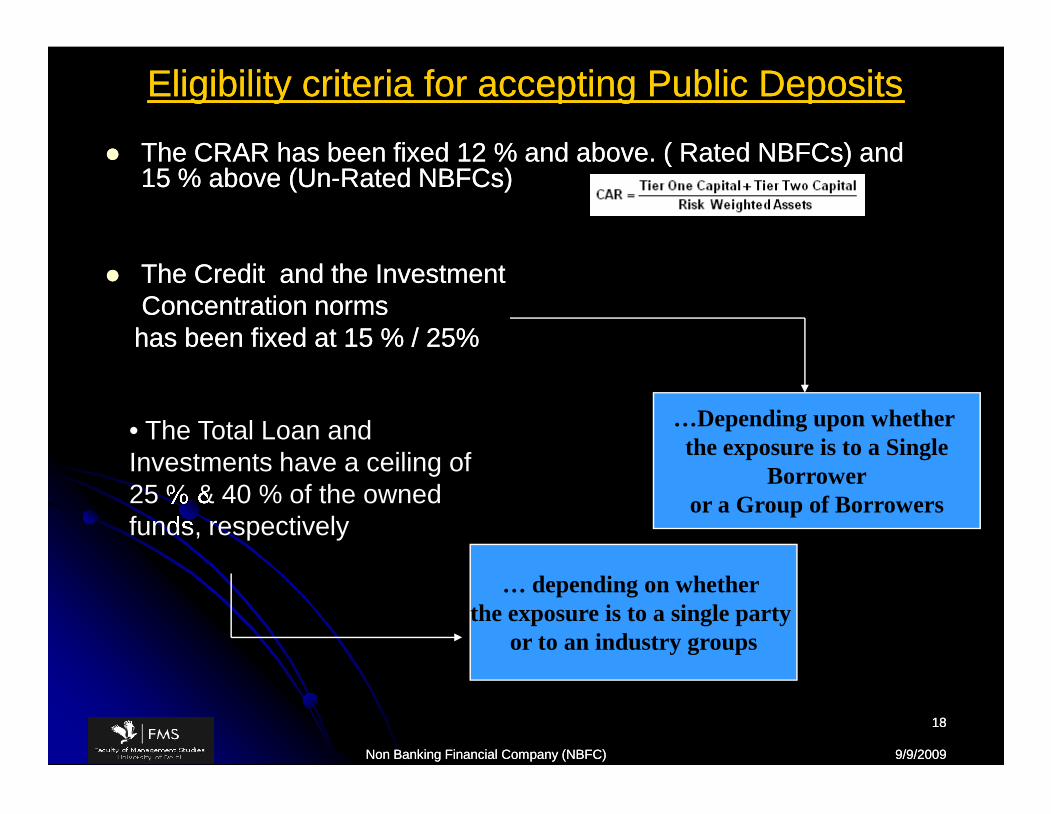

The CRAR has been fixed 12 % and above. ( Rated NBFCs) andThe CRAR has been fixed 12 % and above. ( Rated NBFCs) and15 % above (Un15 % above (Un--Rated NBFCs)Rated NBFCs)

The Credit and the InvestmentThe Credit and the InvestmentConcentration normsConcentration normshas been fixed at 15 % / 25%has been fixed at 15 % / 25%

…Depending upon whetherthe exposure is to a Single

Borroweror a Group of Borrowers

• The Total Loan andInvestments have a ceiling of25 % & 40 % of the ownedfunds, respectively

9/9/20099/9/2009Non Banking Financial Company (NBFC)Non Banking Financial Company (NBFC)

1818

… depending on whetherthe exposure is to a single party

or to an industry groups

…Depending upon whetherthe exposure is to a Single

Borroweror a Group of Borrowers

• The Total Loan andInvestments have a ceiling of25 % & 40 % of the ownedfunds, respectively

RBI Guidelines for UnRBI Guidelines for Un--Rated NBFC’sRated NBFC’s

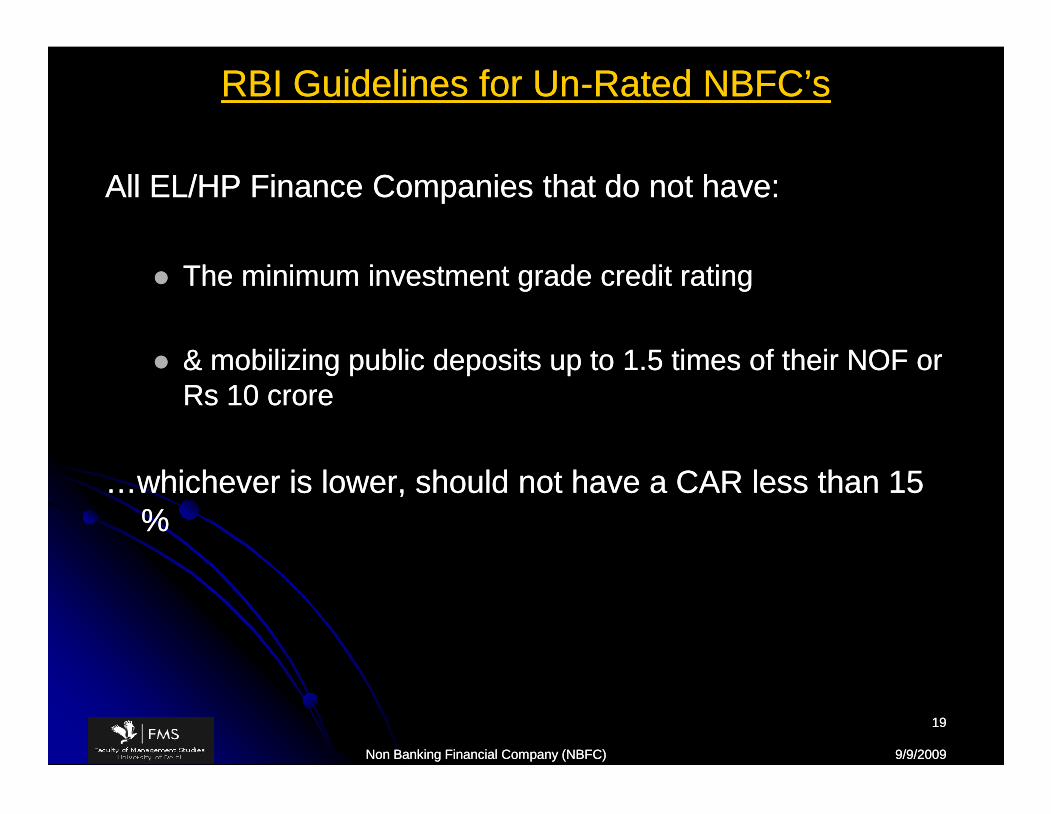

All EL/HP Finance Companies that do not have:All EL/HP Finance Companies that do not have:

The minimum investment grade credit ratingThe minimum investment grade credit rating

& mobilizing public deposits up to 1.5 times of their NOF or& mobilizing public deposits up to 1.5 times of their NOF orRs 10 croreRs 10 crore

…whichever is lower, should not have a CAR less than 15…whichever is lower, should not have a CAR less than 15%%

9/9/20099/9/2009Non Banking Financial Company (NBFC)Non Banking Financial Company (NBFC)

1919

All EL/HP Finance Companies that do not have:All EL/HP Finance Companies that do not have:

The minimum investment grade credit ratingThe minimum investment grade credit rating

& mobilizing public deposits up to 1.5 times of their NOF or& mobilizing public deposits up to 1.5 times of their NOF orRs 10 croreRs 10 crore

…whichever is lower, should not have a CAR less than 15…whichever is lower, should not have a CAR less than 15%%

Regulations for NBFC’s not Accepting PublicRegulations for NBFC’s not Accepting PublicDepositsDeposits

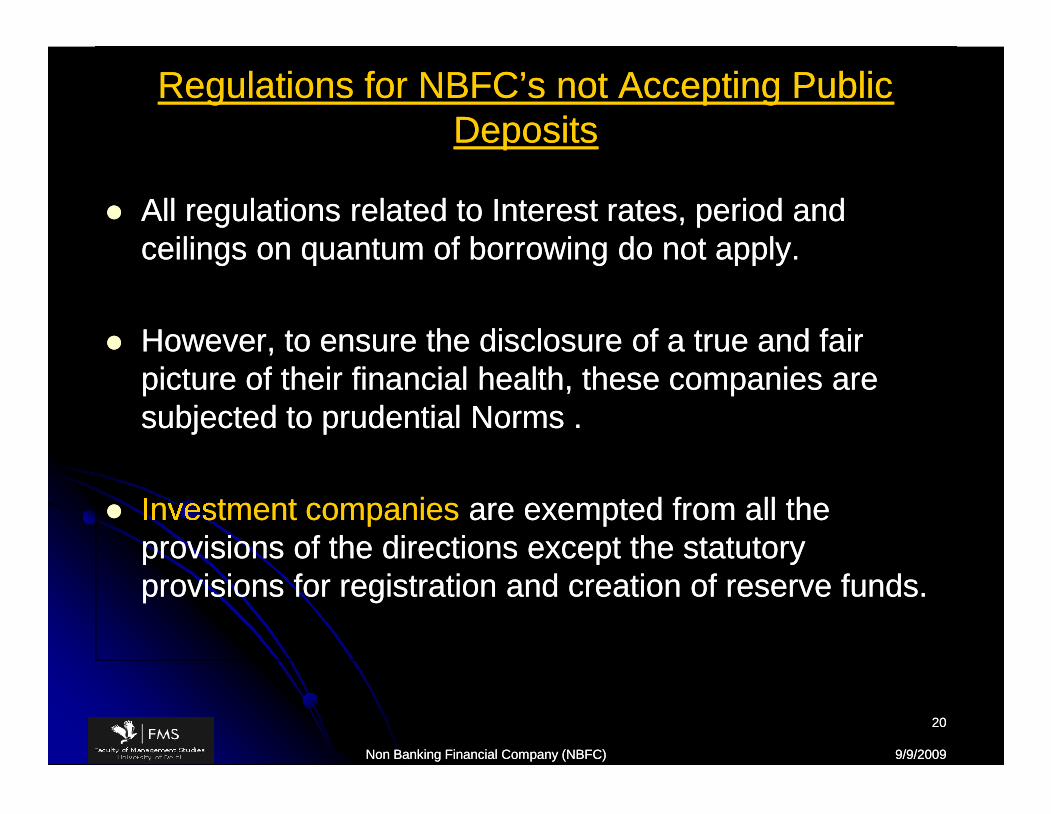

All regulations related to Interest rates, period andAll regulations related to Interest rates, period andceilings on quantum of borrowing do not apply.ceilings on quantum of borrowing do not apply.

However, to ensure the disclosure of a true and fairHowever, to ensure the disclosure of a true and fairpicture of their financial health, these companies arepicture of their financial health, these companies aresubjected to prudential Norms .subjected to prudential Norms .

Investment companiesInvestment companies are exempted from all theare exempted from all theprovisions of the directions except the statutoryprovisions of the directions except the statutoryprovisions for registration and creation of reserve funds.provisions for registration and creation of reserve funds.

9/9/20099/9/2009Non Banking Financial Company (NBFC)Non Banking Financial Company (NBFC)

2020

All regulations related to Interest rates, period andAll regulations related to Interest rates, period andceilings on quantum of borrowing do not apply.ceilings on quantum of borrowing do not apply.

However, to ensure the disclosure of a true and fairHowever, to ensure the disclosure of a true and fairpicture of their financial health, these companies arepicture of their financial health, these companies aresubjected to prudential Norms .subjected to prudential Norms .

Investment companiesInvestment companies are exempted from all theare exempted from all theprovisions of the directions except the statutoryprovisions of the directions except the statutoryprovisions for registration and creation of reserve funds.provisions for registration and creation of reserve funds.

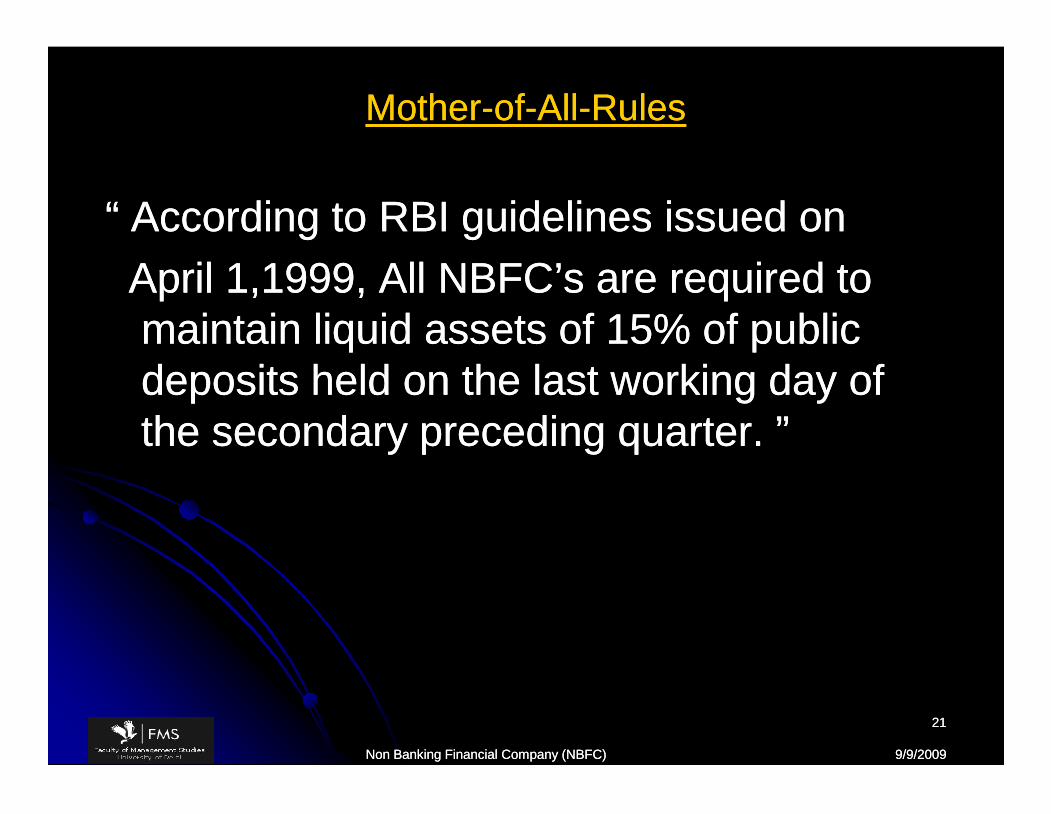

MotherMother--ofof--AllAll--RulesRules

“ According to RBI guidelines issued on“ According to RBI guidelines issued onApril 1,1999, All NBFC’s are required toApril 1,1999, All NBFC’s are required tomaintain liquid assets of 15% of publicmaintain liquid assets of 15% of publicdeposits held on the last working day ofdeposits held on the last working day ofthe secondary preceding quarter. ”the secondary preceding quarter. ”

9/9/20099/9/2009Non Banking Financial Company (NBFC)Non Banking Financial Company (NBFC)

2121

“ According to RBI guidelines issued on“ According to RBI guidelines issued onApril 1,1999, All NBFC’s are required toApril 1,1999, All NBFC’s are required tomaintain liquid assets of 15% of publicmaintain liquid assets of 15% of publicdeposits held on the last working day ofdeposits held on the last working day ofthe secondary preceding quarter. ”the secondary preceding quarter. ”

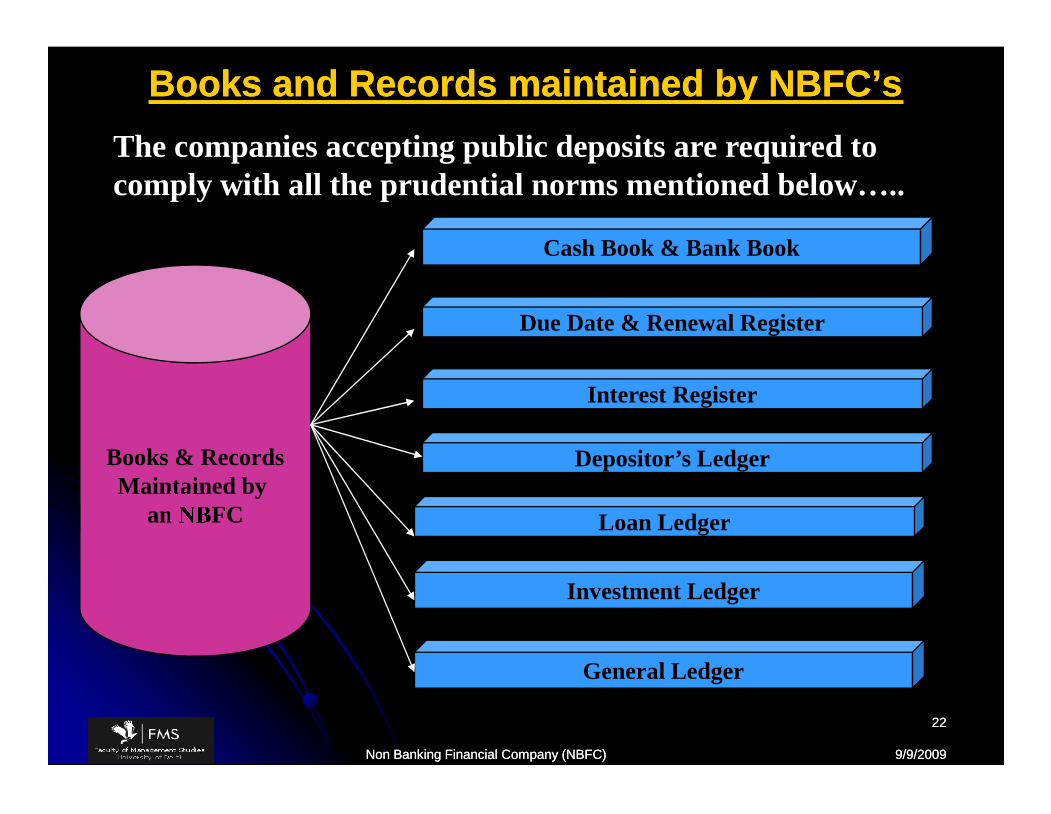

Books and Records maintained by NBFC’sBooks and Records maintained by NBFC’sThe companies accepting public deposits are required tocomply with all the prudential norms mentioned below…..

Cash Book & Bank Book

Due Date & Renewal Register

Interest Register

9/9/20099/9/2009Non Banking Financial Company (NBFC)Non Banking Financial Company (NBFC)

2222

Books & RecordsMaintained by

an NBFC

Interest Register

Depositor’s Ledger

Loan Ledger

Investment Ledger

General Ledger

9/9/20099/9/2009Non Banking Financial Company (NBFC)Non Banking Financial Company (NBFC)

2323

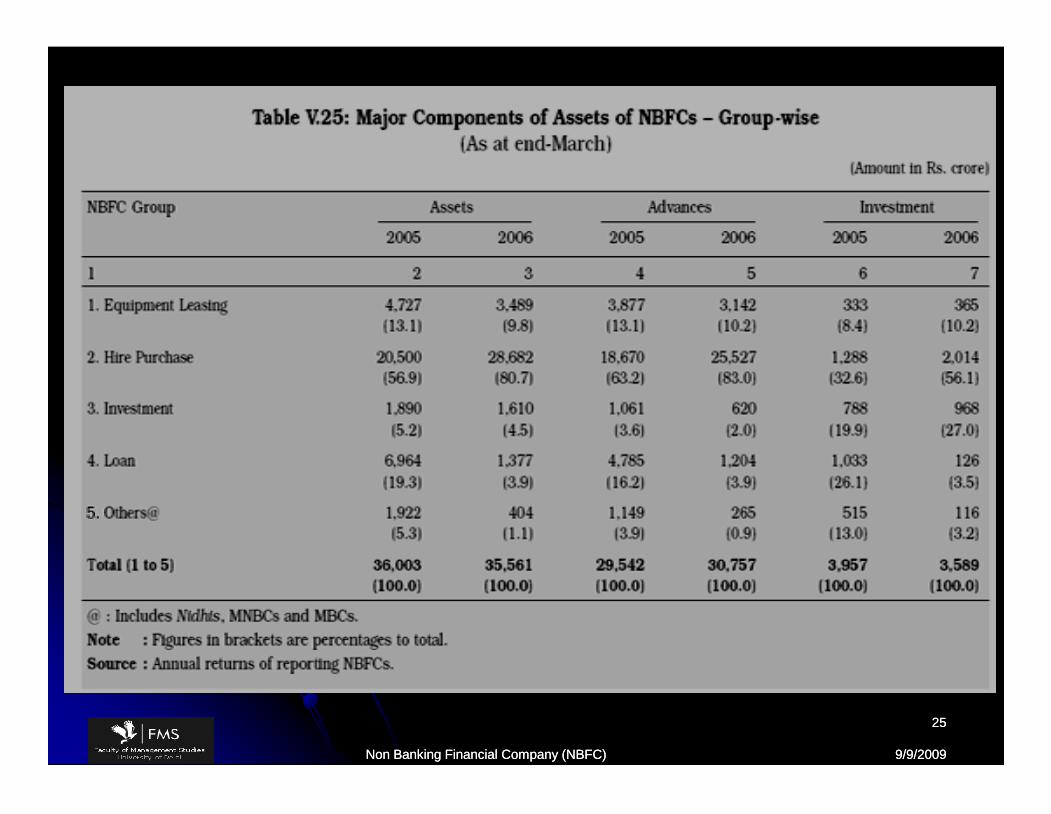

9/9/20099/9/2009Non Banking Financial Company (NBFC)Non Banking Financial Company (NBFC)

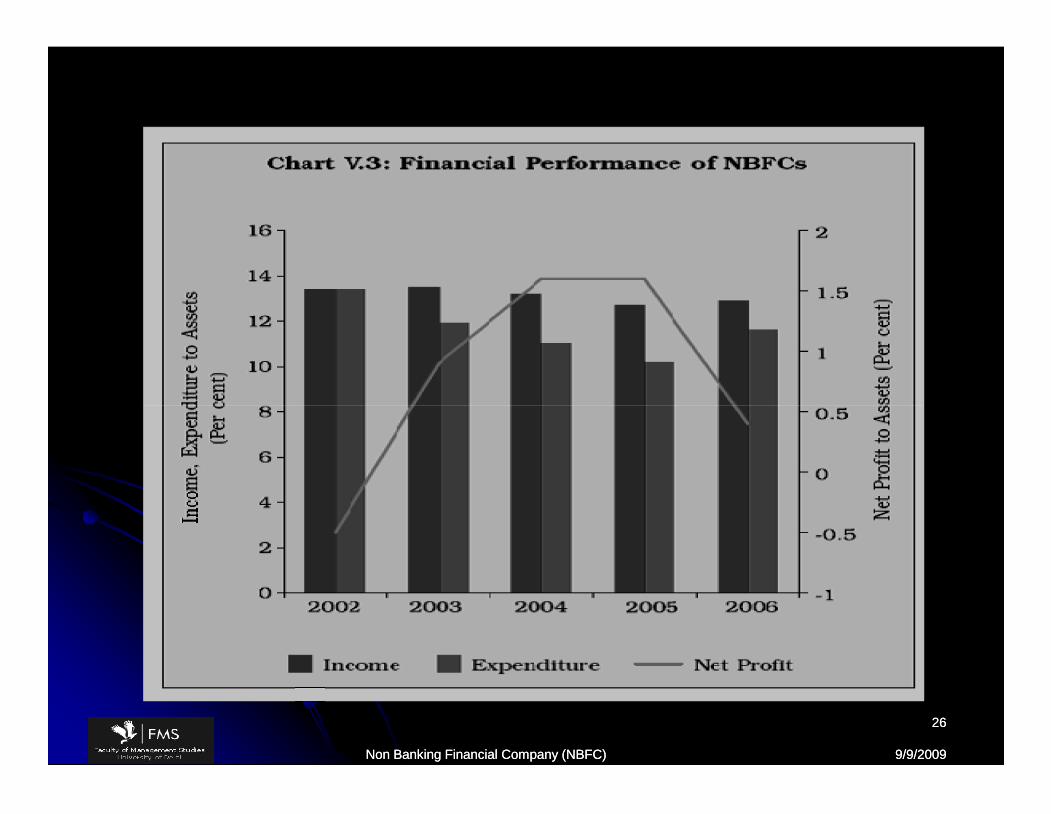

2424

9/9/20099/9/2009Non Banking Financial Company (NBFC)Non Banking Financial Company (NBFC)

2525

9/9/20099/9/2009Non Banking Financial Company (NBFC)Non Banking Financial Company (NBFC)

2626

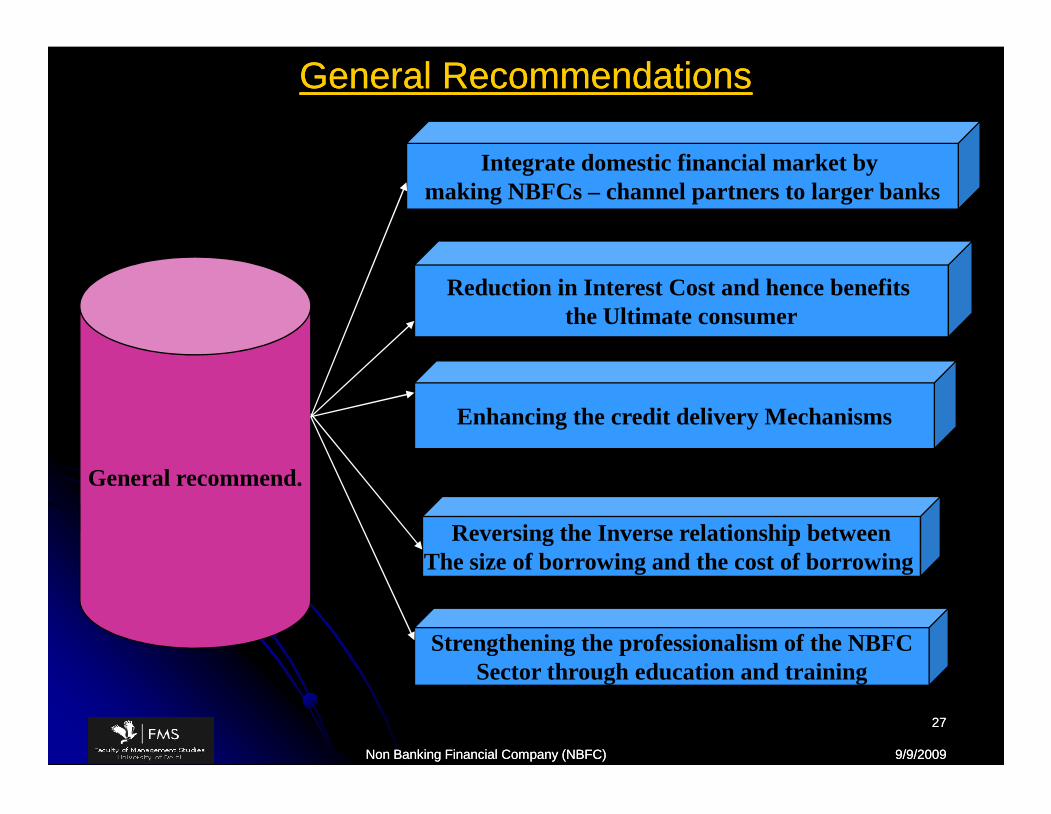

General RecommendationsGeneral Recommendations

Integrate domestic financial market bymaking NBFCs – channel partners to larger banks

Reduction in Interest Cost and hence benefitsthe Ultimate consumer

Enhancing the credit delivery Mechanisms

9/9/20099/9/2009Non Banking Financial Company (NBFC)Non Banking Financial Company (NBFC)

2727

General recommend.

Enhancing the credit delivery Mechanisms

Reversing the Inverse relationship betweenThe size of borrowing and the cost of borrowing

Strengthening the professionalism of the NBFCSector through education and training

Sector for present study : EquitySector for present study : Equityin Cash/derivativein Cash/derivative

Finding market inefficiencies of theFinding market inefficiencies of themarket and then using the leverage tomarket and then using the leverage togenerate the profitgenerate the profit HedgingHedging ArbitrageArbitrage High LeverageHigh Leverage

9/9/20099/9/2009Non Banking Financial Company (NBFC)Non Banking Financial Company (NBFC)

2828

Finding market inefficiencies of theFinding market inefficiencies of themarket and then using the leverage tomarket and then using the leverage togenerate the profitgenerate the profit HedgingHedging ArbitrageArbitrage High LeverageHigh Leverage

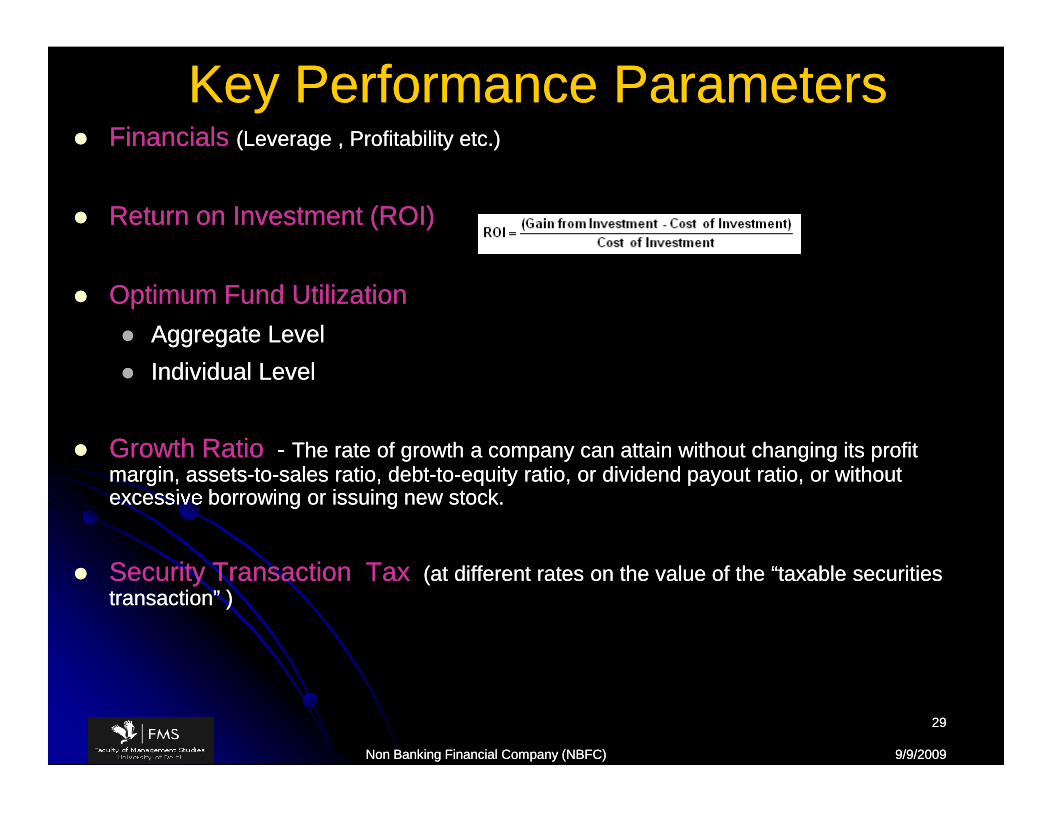

Key Performance ParametersKey Performance Parameters FinancialsFinancials (Leverage , Profitability etc.)(Leverage , Profitability etc.)

Return on Investment (ROI)Return on Investment (ROI)

Optimum Fund UtilizationOptimum Fund Utilization Aggregate LevelAggregate Level Individual LevelIndividual Level

Growth RatioGrowth Ratio -- The rate of growth a company can attain without changing its profitThe rate of growth a company can attain without changing its profitmargin, assetsmargin, assets--toto--sales ratio, debtsales ratio, debt--toto--equity ratio, or dividend payout ratio, or withoutequity ratio, or dividend payout ratio, or withoutexcessive borrowing or issuing new stock.excessive borrowing or issuing new stock.

Security Transaction TaxSecurity Transaction Tax (at different rates on the value of the “taxable securities(at different rates on the value of the “taxable securitiestransaction” )transaction” )

9/9/20099/9/2009Non Banking Financial Company (NBFC)Non Banking Financial Company (NBFC)

2929

FinancialsFinancials (Leverage , Profitability etc.)(Leverage , Profitability etc.)

Return on Investment (ROI)Return on Investment (ROI)

Optimum Fund UtilizationOptimum Fund Utilization Aggregate LevelAggregate Level Individual LevelIndividual Level

Growth RatioGrowth Ratio -- The rate of growth a company can attain without changing its profitThe rate of growth a company can attain without changing its profitmargin, assetsmargin, assets--toto--sales ratio, debtsales ratio, debt--toto--equity ratio, or dividend payout ratio, or withoutequity ratio, or dividend payout ratio, or withoutexcessive borrowing or issuing new stock.excessive borrowing or issuing new stock.

Security Transaction TaxSecurity Transaction Tax (at different rates on the value of the “taxable securities(at different rates on the value of the “taxable securitiestransaction” )transaction” )

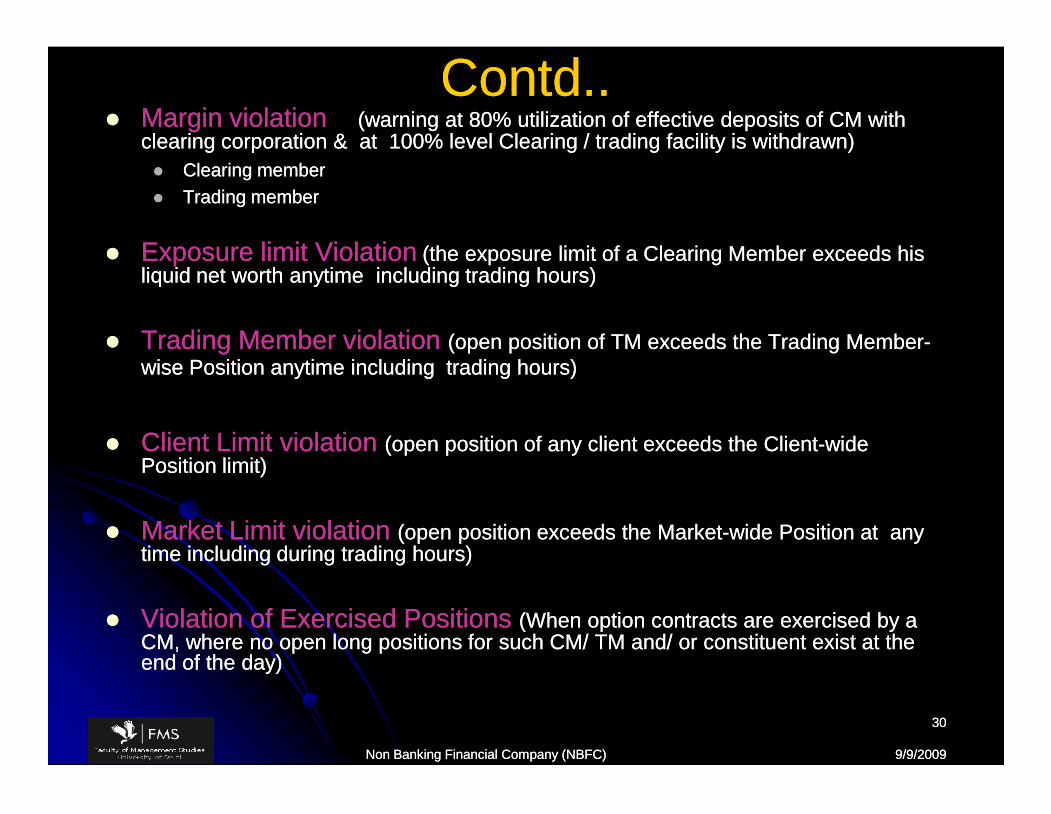

Contd..Contd.. Margin violationMargin violation (warning at 80% utilization of effective deposits of CM with(warning at 80% utilization of effective deposits of CM with

clearing corporation & at 100% level Clearing / trading facility is withdrawn)clearing corporation & at 100% level Clearing / trading facility is withdrawn) Clearing memberClearing member Trading memberTrading member

Exposure limit ViolationExposure limit Violation (the exposure limit of a Clearing Member exceeds his(the exposure limit of a Clearing Member exceeds hisliquid net worth anytime including trading hours)liquid net worth anytime including trading hours)

Trading Member violationTrading Member violation (open position of TM exceeds the Trading Member(open position of TM exceeds the Trading Member--wise Position anytime including trading hours)wise Position anytime including trading hours)

Client Limit violationClient Limit violation (open position of any client exceeds the Client(open position of any client exceeds the Client--widewidePosition limit)Position limit)

Market Limit violationMarket Limit violation (open position exceeds the Market(open position exceeds the Market--wide Position at anywide Position at anytime including during trading hours)time including during trading hours)

Violation of Exercised PositionsViolation of Exercised Positions (When option contracts are exercised by a(When option contracts are exercised by aCM, where no open long positions for such CM/ TM and/ or constituent exist at theCM, where no open long positions for such CM/ TM and/ or constituent exist at theend of the day)end of the day)

9/9/20099/9/2009Non Banking Financial Company (NBFC)Non Banking Financial Company (NBFC)

3030

Margin violationMargin violation (warning at 80% utilization of effective deposits of CM with(warning at 80% utilization of effective deposits of CM withclearing corporation & at 100% level Clearing / trading facility is withdrawn)clearing corporation & at 100% level Clearing / trading facility is withdrawn) Clearing memberClearing member Trading memberTrading member

Exposure limit ViolationExposure limit Violation (the exposure limit of a Clearing Member exceeds his(the exposure limit of a Clearing Member exceeds hisliquid net worth anytime including trading hours)liquid net worth anytime including trading hours)

Trading Member violationTrading Member violation (open position of TM exceeds the Trading Member(open position of TM exceeds the Trading Member--wise Position anytime including trading hours)wise Position anytime including trading hours)

Client Limit violationClient Limit violation (open position of any client exceeds the Client(open position of any client exceeds the Client--widewidePosition limit)Position limit)

Market Limit violationMarket Limit violation (open position exceeds the Market(open position exceeds the Market--wide Position at anywide Position at anytime including during trading hours)time including during trading hours)

Violation of Exercised PositionsViolation of Exercised Positions (When option contracts are exercised by a(When option contracts are exercised by aCM, where no open long positions for such CM/ TM and/ or constituent exist at theCM, where no open long positions for such CM/ TM and/ or constituent exist at theend of the day)end of the day)

Best in class organizationBest in class organization

Reliance Capital Ltd is a part of the Reliance - AnilDhirubhai Ambani Group.

Reliance Capital is one of India’s leading and fastest growingprivate sector financial services companies, and ranks amongthe top 3 private sector financial services and bankingcompanies, in terms of net worth.

Reliance Capital has interests in asset management andmutual funds, life and general insurance, private equity andproprietary investments, stock broking and other activities infinancial services.

9/9/20099/9/2009Non Banking Financial Company (NBFC)Non Banking Financial Company (NBFC)

3131

Reliance Capital Ltd is a part of the Reliance - AnilDhirubhai Ambani Group.

Reliance Capital is one of India’s leading and fastest growingprivate sector financial services companies, and ranks amongthe top 3 private sector financial services and bankingcompanies, in terms of net worth.

Reliance Capital has interests in asset management andmutual funds, life and general insurance, private equity andproprietary investments, stock broking and other activities infinancial services.

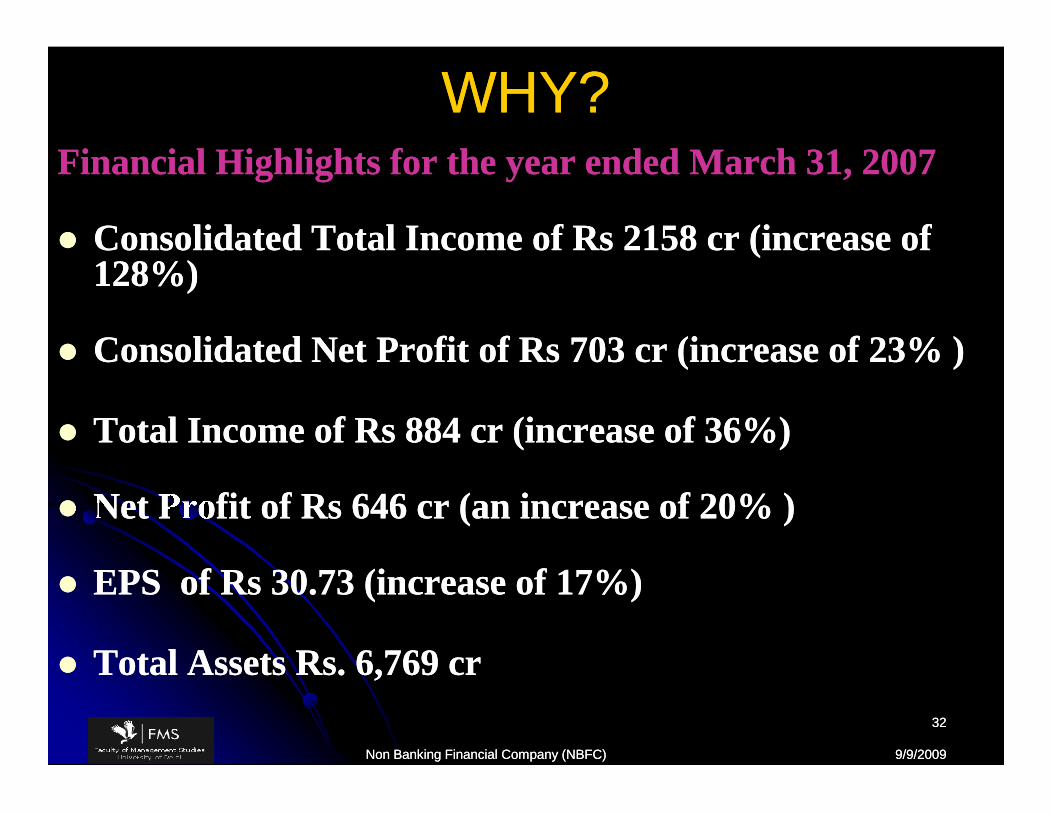

WHY?WHY?Financial Highlights for the year ended March 31, 2007Financial Highlights for the year ended March 31, 2007

Consolidated Total Income of Rs 2158 cr (increase ofConsolidated Total Income of Rs 2158 cr (increase of128%)128%)

Consolidated Net Profit of Rs 703 cr (increase of 23% )Consolidated Net Profit of Rs 703 cr (increase of 23% )

Total Income of Rs 884 cr (increase of 36%)Total Income of Rs 884 cr (increase of 36%)

Net Profit of Rs 646 cr (an increase of 20% )Net Profit of Rs 646 cr (an increase of 20% )

EPS of Rs 30.73 (increase of 17%)EPS of Rs 30.73 (increase of 17%)

Total Assets Rs. 6,769 crTotal Assets Rs. 6,769 cr

9/9/20099/9/2009Non Banking Financial Company (NBFC)Non Banking Financial Company (NBFC)

3232

Financial Highlights for the year ended March 31, 2007Financial Highlights for the year ended March 31, 2007

Consolidated Total Income of Rs 2158 cr (increase ofConsolidated Total Income of Rs 2158 cr (increase of128%)128%)

Consolidated Net Profit of Rs 703 cr (increase of 23% )Consolidated Net Profit of Rs 703 cr (increase of 23% )

Total Income of Rs 884 cr (increase of 36%)Total Income of Rs 884 cr (increase of 36%)

Net Profit of Rs 646 cr (an increase of 20% )Net Profit of Rs 646 cr (an increase of 20% )

EPS of Rs 30.73 (increase of 17%)EPS of Rs 30.73 (increase of 17%)

Total Assets Rs. 6,769 crTotal Assets Rs. 6,769 cr

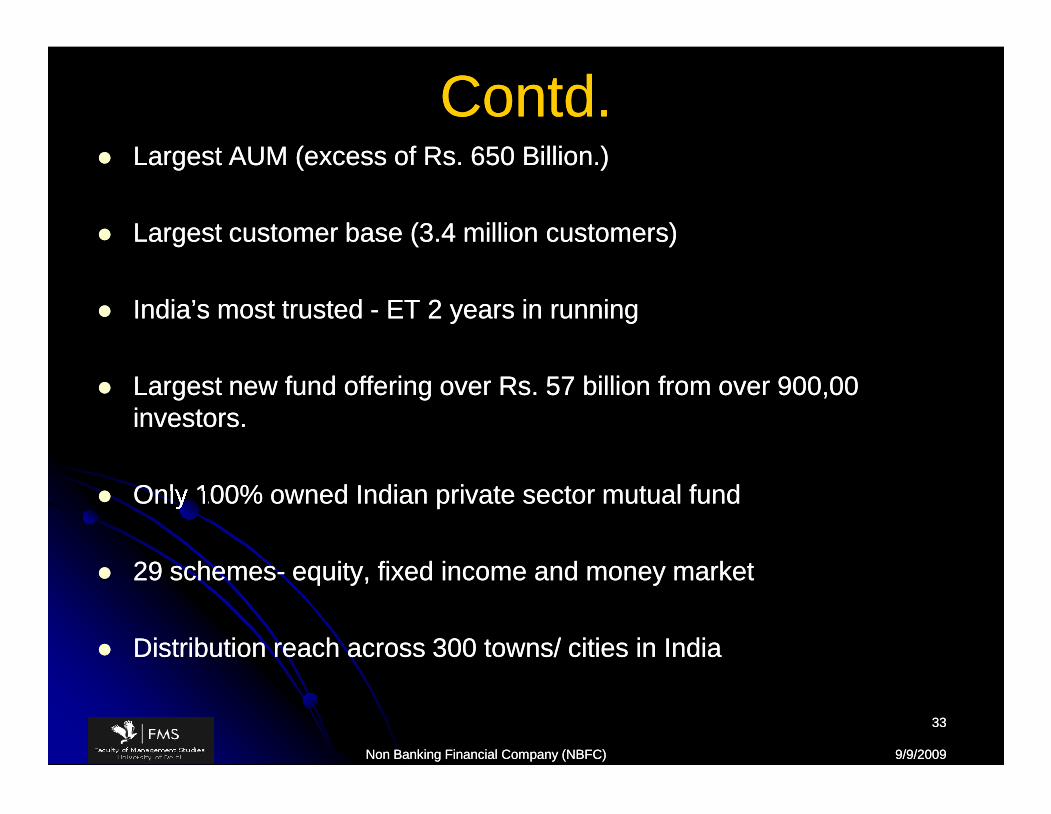

Contd.Contd. Largest AUM (excess of Rs. 650 Billion.)Largest AUM (excess of Rs. 650 Billion.)

Largest customer base (3.4 million customers)Largest customer base (3.4 million customers)

India’s most trustedIndia’s most trusted -- ET 2 years in runningET 2 years in running

Largest new fund offering over Rs. 57 billion from over 900,00Largest new fund offering over Rs. 57 billion from over 900,00investors.investors.

Only 100% owned Indian private sector mutual fundOnly 100% owned Indian private sector mutual fund

29 schemes29 schemes-- equity, fixed income and money marketequity, fixed income and money market

Distribution reach across 300 towns/ cities in IndiaDistribution reach across 300 towns/ cities in India

9/9/20099/9/2009Non Banking Financial Company (NBFC)Non Banking Financial Company (NBFC)

3333

Largest AUM (excess of Rs. 650 Billion.)Largest AUM (excess of Rs. 650 Billion.)

Largest customer base (3.4 million customers)Largest customer base (3.4 million customers)

India’s most trustedIndia’s most trusted -- ET 2 years in runningET 2 years in running

Largest new fund offering over Rs. 57 billion from over 900,00Largest new fund offering over Rs. 57 billion from over 900,00investors.investors.

Only 100% owned Indian private sector mutual fundOnly 100% owned Indian private sector mutual fund

29 schemes29 schemes-- equity, fixed income and money marketequity, fixed income and money market

Distribution reach across 300 towns/ cities in IndiaDistribution reach across 300 towns/ cities in India

An organization in the industryAn organization in the industryIKM Investors Services Limited

Services :-

•Trading in Equities in the cash and derivatives segment (Future and Options) of

National Stock Exchange (NSE) and Bombay Stock Exchange. (BSE)

•Trading in Commodities on Multi-Commodity Exchange (MCX) and National

Commodity Exchange Of India (NCDEX).

•Providing Demat Services on NSDL and CTCL

9/9/20099/9/2009Non Banking Financial Company (NBFC)Non Banking Financial Company (NBFC)

3434

Services :-

•Trading in Equities in the cash and derivatives segment (Future and Options) of

National Stock Exchange (NSE) and Bombay Stock Exchange. (BSE)

•Trading in Commodities on Multi-Commodity Exchange (MCX) and National

Commodity Exchange Of India (NCDEX).

•Providing Demat Services on NSDL and CTCL

An organization in the industryAn organization in the industryIKM Investors Services Limited

Technologies :-

•NEAT (NSE Trading Platform)

•Client/Server (Stratus server at exchange and client SW on PC communicate via V-

SAT/Leased lines)

•At the server end, all trading information is stored in an in-memory database to

achieve minimum response time and maximum system availability for users.

•BOLT (Bombay On Line Trading system)

•ODIN™ Integrated Application: - Multi-Exchange, Multi-Segment Front

Office Trading System

•CTCL (computer to computer Link) trading technology;

9/9/20099/9/2009Non Banking Financial Company (NBFC)Non Banking Financial Company (NBFC)

3535

Technologies :-

•NEAT (NSE Trading Platform)

•Client/Server (Stratus server at exchange and client SW on PC communicate via V-

SAT/Leased lines)

•At the server end, all trading information is stored in an in-memory database to

achieve minimum response time and maximum system availability for users.

•BOLT (Bombay On Line Trading system)

•ODIN™ Integrated Application: - Multi-Exchange, Multi-Segment Front

Office Trading System

•CTCL (computer to computer Link) trading technology;

An organization in the industryAn organization in the industryIKM Investors Services Limited

Technologies :-

• privilege of trading across 5 different markets (NSE-Equity, NSE-Derivatives, BSE-

Equity, MCX & NCDEX) on a single screen.

•ODIN™ supports heterogeneous networks - networks that use a mix of TCP and UDP

traffic

•Real Time Providers of Data / News

•For getting Real Time Data/reports of the various Exchanges spread across the globe

• Bloomberg

•News Wire 18

•E-signal

•All Excel sheet compatibles

9/9/20099/9/2009Non Banking Financial Company (NBFC)Non Banking Financial Company (NBFC)

3636

Technologies :-

• privilege of trading across 5 different markets (NSE-Equity, NSE-Derivatives, BSE-

Equity, MCX & NCDEX) on a single screen.

•ODIN™ supports heterogeneous networks - networks that use a mix of TCP and UDP

traffic

•Real Time Providers of Data / News

•For getting Real Time Data/reports of the various Exchanges spread across the globe

• Bloomberg

•News Wire 18

•E-signal

•All Excel sheet compatibles

An organization in the industryAn organization in the industryIKM Investors Services Limited

Technologies :-

• DDE (Dynamic Data Exchange) (though newer ones are OLE,COM etc.)

•a technology for communication between multiple applications under Microsoft

windows and OS/2

•To share and link the Excel sheet of dealer with the Excel running at server.

•HW

•P IV systems , VSAT IDU , star topology between departments (Arbitrage ,

Demat ,Back office , Client Area)

•X.25 connectivity ( Packet switched WAN using leased/phone/ISDN)

•Trading servers (SMP servers)

9/9/20099/9/2009Non Banking Financial Company (NBFC)Non Banking Financial Company (NBFC)

3737

Technologies :-

• DDE (Dynamic Data Exchange) (though newer ones are OLE,COM etc.)

•a technology for communication between multiple applications under Microsoft

windows and OS/2

•To share and link the Excel sheet of dealer with the Excel running at server.

•HW

•P IV systems , VSAT IDU , star topology between departments (Arbitrage ,

Demat ,Back office , Client Area)

•X.25 connectivity ( Packet switched WAN using leased/phone/ISDN)

•Trading servers (SMP servers)

An organization in the industryAn organization in the industryIKM Investors Services Limited

Need for further Development :-

• Real time data from these Bloomberg/news wire are linked with customized excel

based spread sheets for real time basis analysis based on the pre-programmed logic for

arbitrage calculation. Results are then displayed to our dealers for further execution

through trading terminals. The execution of the trades is done manually by the dealers.

•Need for automation of this intelligence coupled with mathematical models of the

market for an equity, in which the equity's price is a stochastic process

•Binomial Options Pricing Model

•Black–Scholes model

•Put-call parity

•Monte Carlo Options Model

• Subject matter of Stochastic Calculus

9/9/20099/9/2009Non Banking Financial Company (NBFC)Non Banking Financial Company (NBFC)

3838

Need for further Development :-

• Real time data from these Bloomberg/news wire are linked with customized excel

based spread sheets for real time basis analysis based on the pre-programmed logic for

arbitrage calculation. Results are then displayed to our dealers for further execution

through trading terminals. The execution of the trades is done manually by the dealers.

•Need for automation of this intelligence coupled with mathematical models of the

market for an equity, in which the equity's price is a stochastic process

•Binomial Options Pricing Model

•Black–Scholes model

•Put-call parity

•Monte Carlo Options Model

• Subject matter of Stochastic Calculus

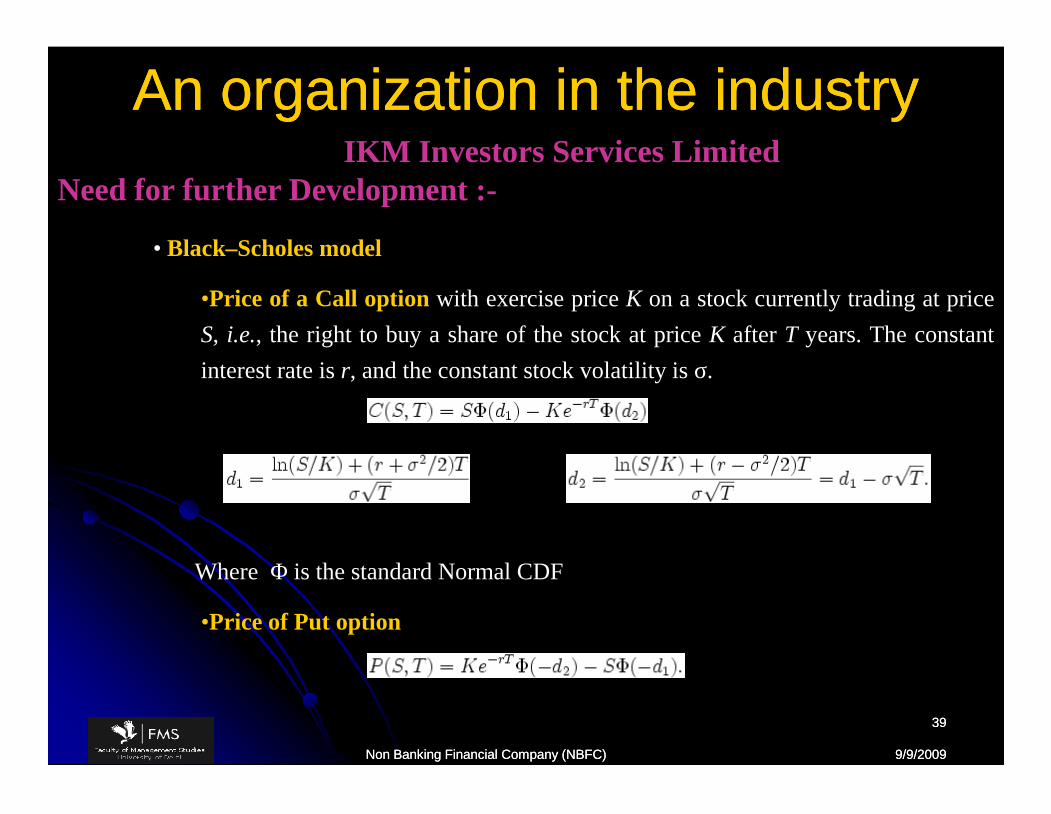

An organization in the industryAn organization in the industryIKM Investors Services Limited

Need for further Development :-

• Black–Scholes model

•Price of a Call option with exercise price K on a stock currently trading at price

S, i.e., the right to buy a share of the stock at price K after T years. The constant

interest rate is r, and the constant stock volatility is σ.

Where Φ is the standard Normal CDF

•Price of Put option

9/9/20099/9/2009Non Banking Financial Company (NBFC)Non Banking Financial Company (NBFC)

3939

Need for further Development :-

• Black–Scholes model

•Price of a Call option with exercise price K on a stock currently trading at price

S, i.e., the right to buy a share of the stock at price K after T years. The constant

interest rate is r, and the constant stock volatility is σ.

Where Φ is the standard Normal CDF

•Price of Put option