non-confidential government of india ministry of … ramdev metal mart 11 ... containing essential...

TRANSCRIPT

1

Non-Confidential Government of India

Ministry of Commerce & Industry Department of Commerce

(Directorate General of Anti Dumping and Allied Duties) Udyog Bhawan, New Delhi

Dated, the 11th October, 2011

FINAL FINDINGS

Subject: Anti dumping investigation concerning imports of Hot Rolled Flat Products of Stainless Steel of ASTM Grade 304 with all its variants, originating in or exported from European Union, Korea RP, South Africa, Taiwan and USA

1. No.14/12/2010-DGAD - Having regard to the Customs Tariff Act 1975 as amended

from time to time (hereinafter referred to as the Act) and the Customs Tariff (Identification, Assessment and Collection of Anti-Dumping Duty on Dumped Articles and for Determination of Injury) Rules, 1995, (hereinafter referred to as the Rules) thereof, M/s JSL Ltd. on behalf of the domestic industry (herein after referred to as the Applicant) has filed an application before the Designated Authority (hereinafter referred to as Authority), in accordance with the Customs Tariff Act, 1975 as amended from time to time and Customs Tariff (Identification, Assessment and Collection of Anti Dumping Duty on Dumped Articles and for Determination of Injury) Rules, 1995 as amended from time to time (herein after referred as Rules), alleging dumping of Hot Rolled Flat Products of Stainless Steel of ASTM Grade 304 with all its variants, (hereinafter also referred to as the subject goods), originating in or exported from European Union, Korea RP, South Africa, Taiwan and USA (hereinafter referred to as subject countries).

2. The Authority on the basis of sufficient evidence submitted by the Applicant to justify

initiation of the investigation, issued a public notice dated 12th

April 2010 published in the Gazette of India, Extraordinary, initiating Anti-dumping investigation concerning imports of the subject goods originating in or exported from the subject countries, in accordance with the Rule 6(1) of the AD Rules to determine the existence, degree and effect of alleged dumping and to recommend the amount of anti-dumping duty, which, if levied, would be adequate to remove the injury to the domestic industry. The Authority notified High Commission/Embassies of the subject countries in India about the receipt of the application claiming, inter alia, allegations of dumping and consequent injury to the domestic industry before proceeding to initiate the investigation in accordance with Rule 5(5) of the AD Rules.

A.

Procedure

3. In these proceedings the procedure described herein below has been followed: i. The Designated Authority (hereinafter referred to as the Authority), under the

above Rules, received a written application from JSL Limited on behalf of the domestic industry, alleging dumping of Hot Rolled Flat Products of Stainless

2

Steel of ASTM Grade 304 with all its variants, (hereinafter also referred to as the subject goods), originating in or exported from European Union, Korea RP, South Africa, Taiwan and USA (hereinafter referred to as subject countries/territories).

ii. The High Commission/Embassies of the subject countries in India were informed about the initiation of the investigation, in accordance with Rule 6(2) of the AD Rules.

iii. The Authority on the basis of sufficient evidence submitted by the applicant on

behalf of the domestic industry issued a public notice dated 12th April 2010 published in the Gazette of India, Extraordinary, initiating Anti-Dumping investigations concerning imports of ‘subject goods’ originating in or exported from subject countries, in accordance with the sub-Rule 6(1) of the AD Rules to determine the existence, degree and effect of alleged dumping and to recommend the amount of anti-dumping duty, which, if levied, would be adequate to remove the injury to the domestic industry.

iv. The Designated Authority sent copies of the initiation notification dated 12th

April 2010 to the High Commission/Embassies of the subject countries in India, known exporters from the subject countries, known importers and other interested parties, and the domestic industry, as per the information available with it. Parties to this investigation were requested to file the questionnaire responses and make their views known in writing within the prescribed time limit. Copies of the letter and questionnaires sent to the exporters were also sent to the High Commission/Embassies of the subject countries along with a list of known exporters/producers with a request to advise the exporters/ producers from the subject countries to respond to the questionnaires within the prescribed time.

v. Copy of the non-confidential version of the application filed on behalf of the

domestic industry was made available to the known exporters and the High Commission/Embassies of the subject countries in accordance with Rule 6(3) of the AD Rules.

vi. Questionnaires were sent to the following known exporters from the subject

countries in accordance with Rule 6(4) of the AD Rules to elicit relevant information: 1. ALZ NV 2. Ugine (Division of Usinar) 3. Acerinox SA 4. A.K. Steel Corporation 5. Allegheny Ludlum 6. North American Stainless 7. J & L Specialty Steel, Inc 8. Yieh United Steel Corporation (YUSCO) 9. Columbus Stainless (Pty) Ltd. 10. POSCO

3

vii. In response to the initiation notification, the following exporters/producers from subject countries have responded:

1. Acerionox Malaysia Sdn Bhd , Malaysia 2. Acerionox SA, Spain 3. Columbus Stainless, South Africa 4. Outokumpu Stainless AB-Sweden 5. Outokumpu Stainless OY-Finland 6. Yieh United Steel Corporation (YUSCO) 7. Arcelor Mittal – Stainless Belgium 8. Arcelor Mittal – Stainless France

viii. Questionnaires were sent to the following known importers/users of subject

goods in India calling for necessary information in accordance with Rule 6(4):

1. Ratnamani Metals & Tubes Ltd. 2. Bhandari Foils & Tubes Ltd. 3. Prakash Steelage Ltd. 4. Rajendra Mechanical Industries Ltd 5. Phoenix Foils Pvt. Ltd. 6. Domet Trading Pvt. Ltd 7. Sangeeta Metal (India) 8. Ramani Steel House 9. Nishant Infin Pvt. Ltd. 10. A. C. Steel Shop 11. Quality Foils (India) (P) Ltd.

ix. Following importers /users have responded:

1. Godrej & Boyce Manufacturing Co. Ltd. 2. G. R. Engineering Private Limited, Mumbai 3. Sulzer India Limited, Pune 4. ISGEC, Yamunanagar, Haryana 5. Metal & Stainless Steel Merchant’s Association, Mumbai 6. Global Trading, Mumbai 7. ANGEL Pipes and Tubes Pvt Ltd, Mumbai 8. ALFA Laval India Limited, Mumbai 9. Riddhi Siddhi Metals, Bangalore 10. Shri Ramdev Metal Mart 11. Reliance Stainless Steel 12. Honest Enterprise Limited 13. M/s. Ratnamani Metals & Tube Limited’ 14. Prakash Steelage Ltd 15. Remi Edelstahi Tubulars Ltd 16. Bhandari Foils & Tubes Ltd 17. Siddhivinayak Steel 18. Honesty Impex 19. Pacific Metal Trading Company 20. Maxgrow Corporation 21. Navnidhi Steel & Engg. Co. Pvt. Ltd

4

22. Precision Impex

x. The Authority made available non-confidential version of the evidence presented by various interested parties in the form of a public file kept open for inspection by the interested parties;

xi. Optimum cost of production and cost to make & sell the subject goods in India

based on the information furnished by the domestic industry on the basis of Generally Accepted Accounting Principles (GAAP) was worked out so as to ascertain if anti-dumping duty lower than the dumping margin would be sufficient to remove injury to the domestic Industry.

xii. Investigation was carried out for the period starting from 1st April 2008 to 30th September 2009 (hereinafter also referred to as the POI). The examination of trends, in the context of injury analysis, covers the periods April 2005-March 2006, April 2006-March 2007, April 2007-March 2008, and the POI.

xiii. Verification of the data and the information submitted by the interested parties

in the prescribed format has been carried out to the extent considered necessary.

xiv. Information provided by interested parties on confidential basis was examined

with regard to sufficiency of the confidentiality claims. On being satisfied, the Authority has accepted the confidentiality claims, wherever warranted and such information has been considered confidential and not disclosed to other interested parties. Wherever possible, parties providing information on confidential basis were directed to provide sufficient non-confidential version of the information filed on confidential basis.

xv. Wherever an interested party has refused access to, or has otherwise not

provided necessary information during the course of the present investigation, or has significantly impeded the investigation, the Authority has recorded these findings on the basis of the facts available.

xvi. Request was made to the Directorate General of Commercial Intelligence and

Statistics (DGCI&S) to arrange details of imports of subject goods for the past three years, including the period of investigation.

xvii. The authority conducted an oral hearing of interested parties on 9th August,

2011, subsequent to which written submissions and rejoinders have been submitted by the interested parties. These submissions, to the extent relevant, have been duly examined/addressed in these findings.

xviii. In accordance with Rule 16 of the Rules supra, a disclosure statement

containing essential facts to form the basis of this final findings was issued on 5-10-2011. The comments received thereon to the extent relevant have been examined in these findings.

5

xix. *** in this notification represents information furnished by an interested party on confidential basis, and so considered by the Authority under the Rules.

B. Product Under Consideration and Like Article

4. The product under consideration as per the petition filed by domestic industry is Hot Rolled Flat Products of Stainless Steel of ASTM Grade 304 with all its variants including products of equivalent specifications in other standards like UNS, IS, Chinese DIN, JIS, BIS, EN, etc. The subject goods are used for manufacture of process equipments, re-rolling, reactor vessels, material handling equipments, railways, pipes & tubes, automotive components, rolled formed sections, architecture, building & construction, industrial fabrication, etc.

5. The subject goods are classified under Chapter Heading 7219.11, 7219.12, 7219.13, 7219.14, 7219.21, 7219.22, 7219.23, 7219.24, 7220.11 and 7220.12 of Customs Tariff Act. The customs classification is, however, only indicative and in no way binding on the scope of the present investigation.

Submissions made by the Interested Parties

6. As regards Product Under Consideration, the interested parties have submitted as follows:

i. The domestic industry cannot produce the subject goods of widths beyond

1250mm and therefore, the subject goods with widths above 1250mm are required to be excluded from the purview of the present investigation as has been done in the previous case of CR coils. The interested parties have further stated that the subject goods of widths of 2 meter for coils and 3 meter for plates are not manufactured by the domestic industry.

ii. The HR coils of thicknesses1.5mm to 2.5mm & 6.1mm to 14mm are to be

excluded from the purview of the product under consideration as the same are not manufactured by the domestic industry. Similarly, HR plates of thicknesses above 70mm and HR plates of lengths above 6300mm are to be excluded from the purview of the product under consideration as the same are also not manufactured by the domestic industry.

iii. M/s Godrej & Boyce Manufacturing Co. Ltd. has stated that SS plates 304 and

304L of width higher than 1250 mm are not domestically manufactured. They have referred to their email dated 6.5.2010 sending an enquiry to JSL. JSL is claimed to have confirmed by email that they could not supply SS Plates having width over 1280 mm.

iv. The interested parties have placed on record evidence of a demand of 50MT of

the subject goods of 1350mm width on the domestic industry during the POI and the domestic industry has offered only 1250mm width. Another piece of evidence in the form of a copy of email from JSL Ltd. has been furnished wherein the domestic industry has stated that they can offer 1250 mm only.

6

v. The interested parties have further stated that the subject goods of widths of 2

meter for coils and 3 meter for plates are not manufactured by the domestic industry

Submissions made by the domestic industry

7. The domestic industry has submitted as follows: i. The interested parties have made unsubstantiated statements and have not

provided any evidence in support of their submissions. The domestic industry manufactures the subject goods of widths above 1250mm and the same can go up to 1600mm. It has also been demonstrated to the Authority during the verification that the domestic industry is manufacturing the subject goods of widths as high as 1570mm. Therefore, there is no merit in the submissions of the interested parties for exclusion of widths above 1250mm.

ii. The domestic industry stated that the interested parties have not provided the

details of the applications where the widths of 2 meter coils and 3 meter plates are used. They further stated that the subject goods of widths above 1600 mm including tolerance even though not manufactured by the applicant are not to be excluded from the purview of the product under consideration for the reason that the subject goods of widths above 1600 mm and widths 1600 mm or below are commercially and technically substitutable for each other. In cases where subject goods of widths above 1600 mm are to be used, the same can be substituted with the subject goods of widths 1600 mm or below by the simple process of welding two narrower widths. It may also be noted that welding is a necessary operation the only difference being that there could be some minor cost saving on account of additional welding in certain specific applications. That does not dilute the fact that the wider widths are completely (both commercially and technically) substitutable to smaller widths particularly for reason of price. For instance, in cases of widths 1600mm or below, the user is required to incur a nominal additional cost for welding only. In other cases, where subject goods of widths 1600 mm or below are to be used, the same can be substituted with the widths above 1600 mm by slitting them into narrower widths. In such cases also, the nominal cost of slitting only would be incurred by them. Thus, it is clear that the subject goods of widths 1600 mm or lower are commercially and technically be used in place of the subject goods of widths above 1600 mm and vice versa. In view of the above, the Authority is requested to include all widths as part of the product under consideration.

iii. The interested parties have made unsubstantiated statements and have not

provided any evidence in support of their submissions. The domestic industry has indeed manufactured and sold all the thicknesses and length of the subject goods including thicknesses 1.5mm to 2.5mm, 6.1mm to 14mm & thicknesses above 70mm and lengths of the subject goods above 6300mm. In support, the sales invoices for the abovementioned thicknesses and lengths are provided by the domestic industry.

7

Examination by the Authority

8. The Authority has examined the submissions of interested parties as follows:

i. The Authority notes that the scope of the investigation was defined while

initiating the investigation. The Authority has taken note of the claims and counterclaims made by the interested parties with respect to PUC, including those in respect of exclusion of widths above 1250mm, certain thicknesses and lengths.

ii. The Authority notes that the Domestic Industry has the facility to

manufacture HR products of width up to 1550 mm. However, no evidence was provided in support of having actually produced or sold the widths above 1250 mm during POI. The Authority considers the aspect of actual production / sales of the product with width above 1250 mm as crucial for the purpose of its inclusion/exclusion within the scope of PUC. The Authority notes that the user industry will buy the PUC in the required width for the end use applications to economise the cost and remain competitive. Thus even though it may be technically feasible for the consumers/end users to cut the PUC into smaller width or weld the smaller width to the required higher width, it has not been established that the same is commercially feasible at the end of the consumer/end user. The Authority considers that both technical as well as commercial substitutability of the product is important to establish that the product offered by the Domestic Industry is like article to the product imported. Further, the Authority notes from the evidence placed on record by the interested parties that the domestic industry has not been able to offer/supply subject goods of more than 1250 mm width when a demand has been raised for the same. The Authority therefore finds no merit in the submission of the domestic industry that they did not supply the subject goods of more than 1250mm width due to lack of demand. The Authority further notes that in an earlier investigation concerning Mid-Term Review of Cold Rolled Flat Products of Stainless Steel of width 600mm to 1250mm, the Authority allowed width tolerance for trim edge and mill edge materials separately as per ISO standard which is an international standard. Therefore, the Authority considers it appropriate to indicate width tolerance in respect of the subject goods in the present investigation as per the same ISO standard. The width tolerance indicated in ISO standard for Hot Rolled plates/sheets and strips is +20 mm (for Mill Edge) and +5mm (for Trimmed Edge).

9. In view of the above, the Authority holds that the PUC for the purpose of the

present investigation is as follows:

Hot Rolled Flat Products of Stainless Steel of width up to 1250 mm (width tolerance of +20 mm for Mill Edge and +5mm for Trimmed Edge) of ASTM Grade 304 with all its variants including products of equivalent specifications in other standards like UNS, IS, Chinese DIN, JIS, BIS, EN, etc.

8

SCOPE OF DOMESTIC INDUSTRY & STANDING

10. The Application for the present investigation has been filed by M/s JSL Ltd. on behalf of the domestic industry. According to the applicant, there are two other producers of the like Article in the country during the period under examination.

11. As per the evidence available on record, production of M/s JSL Ltd. accounts for a

major proportion of the domestic production of like article, being more than 50% of Indian production. The application thus satisfies the requirements of Rule 2(b) and Rule 5(3) of the AD Rules. The Authority notes that no interested party has disputed the ‘standing’ of the applicant. Therefore, the applicant M/s JSL Ltd. is being treated as ‘domestic industry’ within the meaning of Rule 2(b) read along with Rule 2(d) of the AD Rules for the purpose of the present investigation.

CONFIDENTIALITY Submissions made by the domestic industry

12. The exporters have claimed excessive confidentiality without any proper justification. Further, non-confidential version of the questionnaire response has not been given for all the information contained in the confidential version without assigning proper reasons. It was obligatory for the exporters to give proper statement of reasons as to why confidentiality was claimed and why summarization was not possible for certain information. Even, the non-confidential version is not in sufficient detail to permit a reasonable understanding of the substance of the information submitted in confidence. This has resulted in depriving us a legitimate right to make effective submissions as contemplated under the object and scope of framing of provisions on confidentiality.

13. Since, the exporters have not made a lot of crucial information available, the domestic industry is not in a position to offer comments on the information required to be filed strictly as per prescribed formats. The exporters have not only failed to provide the meaningful response but they have also failed to give any valid reasons for claiming such excessive confidentiality.

14. The domestic industry has provided with the details in respect of each of the responding exporters regarding confidentiality and the deficiencies in the response of the exporters.

Examination by the Authority

15. Information provided by interested parties on confidential basis was examined with

regard to sufficiency of the confidentiality claims. On being satisfied, the Authority has accepted the confidentiality claims, wherever warranted and such information has been considered confidential and not disclosed to other interested parties. Wherever

9

possible, parties providing information on confidential basis were directed to provide sufficient non-confidential version of the information filed on confidential basis and the non-confidential version of the responses was placed in the public file which was open for inspection by the interested parties.

NORMAL VALUE, EXPORT PRICE AND DUMPING MARGIN

16. The Authority sent questionnaire to the known exporters/producers from the subject

countries, advising them to provide information in the form and manner prescribed. Response to the questionnaires was received from the following companies –

1. Acerinox Malaysia Sdn Bhd , Malaysia 2. Acerinox SA, Spain 3. Columbus Stainless (PTY) Ltd., South Africa 4. Outokumpu Stainless OY-Finland 5. Yieh United Steel Corporation (YUSCO)

Submissions made by Domestic Industry 17. The following submissions have been made by the domestic industry.

a. With regard to Acerinox, Spain, it has been mentioned that the subject goods

to India are either directly sold to India or through the related company Acerinox Malaysia. It is submitted that under such a situation there should be levied a single duty only for Acerinox Spain and no duty is separately required to be determined for a combination of Acerinox Spain and Acerinox Malaysia.

b. Outokumpu Stainless OY and Outokumpu Stainless AB from EU have responded to the present initiation. With regard to other related companies which are engaged in the activity of production and sale of subject goods, they have not provided any details. It is submitted that in case, it is found that there are other related companies which are engaged in the activity of the subject goods in any of the subject countries who have not given response to the present investigation, the response of the aforesaid exporters are required to be rejected and not to be considered for the purpose of determination of dumping margin. Without prejudice, it is also submitted that since the aforesaid companies are related, only single dumping margin is required to be determined considering the concept of single economic entity. Therefore, no separate dumping margin is to be determined for the aforesaid companies.

c. M/s Columbus has not provided the details of the export sales to India made through an agent. In the absence of such details, the individual dumping margin is not required to be determined for such exporter. Examination by the Authority Normal Value

18. The authority has examined the responses/submissions of the exporters/producers and other interested parties in regard to Normal value and determined the Normal value

10

based on the information contained in their submissions and verified to the extent considered necessary. The Normal value has been arrived at as per the methodology prescribed under the Rules.

EUROPEAN UNION

19. Acerinox SA, Spain has submitted information reporting the domestic sales in EU

during the POI indicating the volume and invoice value of domestic sales. Adjustments have been claimed on account of ocean freight, inland transport, handling charges, insurance, commission, interest charges and VAT and normal value at ex-factory level is claimed as US$ ***/ MT. The same has been duly verified and, upon verification, normal value has been calculated by considering only those EU transactions which are in ordinary course of trade under the rules. Accordingly, the weighted average invoice value of Euro ***/MT of EU sales is adopted for the determination of normal value. The adjustments claimed on the aforesaid heads have also been duly verified. Accordingly, normal value at the ex-factory level is determined at Euro ***/ MT i.e. US$ ***/ MT.

20. Outokumpu Stainless OY, Finland has submitted information reporting the domestic

sales in EU during the POI indicating the volume and invoice value of domestic sales. Adjustments have been claimed on account of Transport, packing, insurance & credit cost and normal value at ex-factory level is claimed as US $ *** per MT. The information of Outokumpu is duly verified and upon verification, normal value has been calculated by considering only those EU transactions which are in ordinary course of trade (OCT) under the rules. The Authority during verification found that the basis of allocation of expenses between PUC and non-PUC has not been made on reasonable basis and therefore not considered for the purpose of OCT test. The Authority has considered the best available cost data on record in respect of EU sales for the purpose of determining the transactions in ordinary course of trade. Accordingly, the weighted average invoice value of Euro ***/ MT of EU sales of Outokumpu is proposed to be adopted for the determination of normal value. The adjustments claimed on the aforesaid heads have also been duly verified. Accordingly, normal value at ex-factory level is determined for Outokumpu Stainless OY, Finland at Euro *** per MT i.e. US$ *** /MT.

21. The authority notes that no other exporter/producer from EU has responded to the Questionnaire. The Authority, for the residual category, adopts the highest of the normal values determined for the cooperative exporters of EU and accordingly Normal value for residual producers/exporters is determined at US$ ***/ MT.

KOREA RP

22. No exporter/producer from Korea has responded to the Questionnaire. The Authority has determined the Normal value for all exporters/producers of Korea RP at US$ ***/MT based on the information available on record.

11

SOUTH AFRICA

23. Columbus Stainless (PTY) Ltd., South Africa has submitted information reporting the domestic sales during the POI indicating the volume and invoice value of domestic sales. The Authority notes from the information submitted by the exporter that the domestic sales transactions are in ordinary course of trade. Accordingly, the weighted average invoice value of US$ ***/MT is adopted for the purpose of determination of normal value. Adjustments claimed on account of discount, inland transport, credit cost and other miscellaneous expenses have been admitted and accordingly, normal value at ex-factory level of US$ ***/ MT has been adopted by the Authority.

24. No other exporter/producer from South Africa has responded to the Questionnaire.

The Authority has determined the Normal value for the residual category at the same level as that of the cooperative exporter, i.e. at US$ ***/ MT.

TAIWAN

25. Yieh United Steel Corporation (YUSCO) has submitted information reporting the

domestic sales in Taiwan during the POI indicating the volume and invoice value of domestic sales. Adjustments have been claimed on account of packing, inland freight, quantity rebate, contract honouring, further manufacturing rebate, price difference, other rebate and warranty. The Authority has adopted the weighted average invoice value of subject goods of all specifications amounting to US$ ***/MT. As regards the adjustments claimed by the exporter, the Authority notes that substantial amounts have been claimed on account of quantity rebate, contract honouring, further manufacturing rebate and price difference which are normally not claimed nor admitted as adjustments on normal value. Further, it is noted that no such adjustments have been claimed on export price. Therefore, the Authority admitted only the adjustments on account of packing, inland freight, other rebate and warranty. Accordingly, normal value for YUSCO at ex-factory level is determined at US$ ***/ MT.

26. The Authority notes that no other exporter/producer from Taiwan has responded to

the Questionnaire. The Authority has determined the Normal value for residual exporters at US$ ***/MT based on the facts available on record.

USA

27. The Authority notes that no exporter/producer from USA has responded to the

Questionnaire. The Authority has determined the Normal value for all exporters/producers of USA at US$ *** per MT based on the information available on record.

Export Price:

EUROPEAN UNION

12

28. From the responses received, it is noted that Acerinox SA, Spain has exported the subject goods to India during the POI both directly as well as indirectly through its related company, namely, Acerinox Malaysia Sdn Bhd, Malaysia.

29. Acerinox SA, Spain has furnished invoice-wise details of exports made to India

directly including the invoice value which the Authority treats as the basis of export price. Adjustments in respect of their direct sales to Indian customers are claimed on account of ocean freight, inland transport, handling charges, customs expenses, insurance, rebate, commission and credit expenses. Upon verification the Authority considered the weighted average invoice value of US$ ***/MT for the purpose of determination of export price. The Authority during verification of the information of Acerinox, SA Spain has noted an item of expense incurred by the exporter in the export transactions, i.e. the bank charges @ ***% of the invoice value, which was not claimed in the Exporter’s questionnaire response. The same has been adjusted from the export price in addition to the aforesaid adjustments claimed by the exporter and duly verified. Accordingly, the Authority has determined the net export price at US$ *** per MT for Acerinox SA, Spain.

30. Acerinox Malaysia Sdn Bhd, Malaysia has also submitted separately the exporters’

questionnaire response giving invoice-wise details of exports to India of the subject goods produced by Acerinox SA, Spain including the invoice value. Adjustments have been claimed on bank charges, agent commission, inland transportation, ocean freight, port handling and ocean insurance which are incurred at the end of Acerinox, Malaysia. In addition, adjustment has been claimed for expenses at the end of Acerinox SA, Spain on ocean freight, inland transport, handling charges, customs expenses, insurance and credit expenses incurred by Acerinox SA, Spain (producer) for the exports made to India through its related exporter. The Authority has admitted the weighted average invoice value of US$ ***/MT as well as the adjustments claimed by Acerinox Malaysia and Acerinox SA, Spain for the purpose of determination of net export price. The Authority has also deducted the profit of the exporter i.e. Acerinox Malaysia @ ***% of export price to arrive at the export price at ex-factory level. Accordingly, the Authority has determined the net export price at US $ ***/MT for the exports to India made by Acerionox SA, Spain through Acerinox Malaysia Sdn Bhd, Malaysia.

31. Outokumpu Stainless OY-Finland has submitted invoice-wise details of their export

transactions to India including invoice-value of exports. Adjustments have been claimed on account of handling and clearance, international freight, international insurance and interest charges. The Authority upon verification of the export sales data of the exporter to India, has adopted the weighted average invoice value of US$ ***/MT as well as the adjustments on account of clearing and forwarding, credit cost, transport and duty and insurance for the purpose of determination of export price in respect of Outokumpu Stainless OY-Finland. Accordingly, the Authority has determined the net export price for Outokumpu Stainless OY-Finland at US$ *** per MT.

32. No other exporter and producer from European Union has responded to the

Questionnaire. The Authority has determined net export price for the residual exporters at US$ ***/ MT on the basis of representative lowest export price of the cooperative exporter as per information available on record.

13

KOREA RP

33. The Authority notes that no exporter/producer from Korea has responded to the

Questionnaire. Therefore the Authority has determined the Export price for all exporters/producers of Korea RP at US$ *** per MT based on the information available on record.

SOUTH AFRICA 34. Columbus Stainless, South Africa has furnished invoice-wise details of exports made

to India directly including the invoice value which the Authority treats as the basis of export price. Adjustments in respect of their direct sales to Indian customers are claimed on account of interest charges, bank charges, ocean freight, insurance, inland freight and port charges. The Authority has admitted the weighted average invoice value of US$ ***/MT and adjustments claimed by the exporter. Accordingly, the Authority has determined the net export price at US $ *** per MT for Columbus Stainless, South Africa.

35. Acerinox Malaysia Sdn Bhd, Malaysia has also submitted invoice-wise details of exports to India of the subject goods produced by Columbus Stainless, South Africa including the invoice value. Adjustments have been claimed on bank charges, agent commission, inland transportation, ocean freight, port handling and ocean insurance. In addition, adjustments have been claimed for expenses incurred by Columbus Stainless, South Africa (producer), namely credit cost, bank charges, ocean freight, ocean insurance, inland freight and port handling charges for the exports made to India through its related exporter. The Authority has admitted the weighted average invoice value of US$ ***/MT as well as the adjustments claimed by Acerinox Malaysia on expenses incurred at its end and at the end of Columbus, South Africa. In addition to the said adjustments, the Authority also deducted the Profit @ ***% of export price of the exporter to arrive at the export price at ex-factory level. Accordingly, the Authority determines the net export price at US $ *** per MT for the exports to India made by Columbus Stainless, South Africa through Acerinox Malaysia Sdn Bhd, Malaysia.

36. It is noted that no other exporter and producer from South Africa has responded to the

Questionnaire. The Authority has determined net export price for the residual exporters at US$ ***/ MT on the basis of representative lowest export price of the cooperative exporter as per information available on record.

TAIWAN

37. Yieh United Steel Corporation (YUSCO), Taiwan has furnished invoice-wise details

of exports made to India including the invoice value which the Authority treats as the basis of export price. Adjustments in respect of their sales to Indian customers are claimed on account of packing expenses, inland freight, ocean freight, ocean insurance, commission, handling and brokerage, harbor maintenance fee, trade promotion fee, notarization charges and bank charges. The Authority has admitted

14

the weighted average invoice value of US$ ***/MT and the adjustments claimed by the exporter for the purpose of determination of export price. Accordingly, the authority has determined the net export price at US$ *** per MT for Yieh United Steel Corporation (YUSCO), Taiwan.

38. The Authority notes that no other exporter/producer from Taiwan has responded to

the Questionnaire. The Authority has determined the export price for residual category at US$ ***/MT on the basis of the representative lowest export price of the co-operative exporter.

USA

39. The Authority notes that no exporter/producer from USA has responded to the Questionnaire. Therefore, the Authority has determined the Export price for all exporters/producers at US$ *** per MT based on the information available on record.

DUMPING MARGIN

40. Comparing the Normal values and Export prices as determined above, the dumping

margins have been worked out as under: Value in US$/MT

Country/Territory

Producer Exporter NV NEP DM DM (%)

EU Acerinox SA, Spain

Acerinox SA, Spain

*** *** *** 50-60

Acerinox SA, Spain

Acerinox Malaysia Sdn Bhd, Malaysia

*** *** *** 60-70

Outokumpu Stainless OY-Finland

Outokumpu Stainless OY-Finland

*** *** *** 50-60

Any other combination of producer/exporter

*** *** *** 110-120

Korea RP

Any producer/exporter *** *** *** 10-20

South Africa

Columbus Stainless

Columbus Stainless

*** *** *** 135-145

Columbus Stainless

Acerinox Malaysia Sdn Bhd, Malaysia

*** *** *** 115-125

Any other combination of producer/exporter

*** *** *** 170-180

Taiwan Yieh United Steel Corporation

Yieh United Steel Corporation

*** *** *** 50-60

15

Any other combination of producer/exporter

*** *** *** 70-80

USA Any producer/exporter *** *** *** 35-45 Assessment of Injury and examination of causal link

Cumulative assessment

41. Para (iii) of Annexure II of the AD Rules provides that in case imports of a product from more than one country are being simultaneously subjected to anti-dumping investigations, the Designated Authority will cumulatively assess the effect of such imports, in case it determines that: -

a. the margin of dumping established in relation to the imports from each country is more than two percent expressed as percentage of export price and the volume of the imports from each country is three percent of the import of like article or where the export of individual countries is less than three percent, the imports collectively accounts for more than seven percent of the import of like article and

b. cumulative assessment of the effect of imports is appropriate in the light of the conditions of competition between the imported article and the like domestic articles.

42. The Authority observes that

i. The margins of dumping from each of the subject countries are more than the limits prescribed above;

ii. The volume of imports from each of the subject countries is more than the limits prescribed;

iii. Cumulative assessment of the effects of imports is appropriate since the exports from the subject countries directly compete with the like articles offered by the domestic industry in the Indian market. This is evident from the fact that the domestic product and imported product are like Article; imports from each of the subject countries are above the prescribed de-minimis limits; the goods produced by the Indian Producers and the subject goods imported from the subject countries are in direct competition; common parties are resorting to use of imported material and domestic material; Indian Producers’ customers are using the domestic material and imported material interchangeably; the exporters from the subject countries and the applicant have sold the same product in the same periods to the same set of customers, etc.

43. In view of the above, the Authority considers that it would be appropriate to assess

injury to the domestic industry cumulatively from the subject countries.

44. Annexure-II of the AD Rules provide for an objective examination of both, (a) the volume of dumped imports and the effect of the dumped imports on prices, in the domestic market, for the like articles; and (b) the consequent impact of these imports on domestic producers of such product. While examining the volume effect of the

16

dumped imports, the Authority is required to examine whether there has been a significant increase in dumped imports, either in absolute terms or relative to production or consumption in India. With regard to the price effect of the dumped imports, the Authority is required to examine whether there has been significant price undercutting by the dumped imports as compared to the price of the like product in India, or whether the effect of such imports is otherwise to depress the prices to a significant degree, or prevent price increases, which would have otherwise occurred to a significant degree.

45. As regards the impact of the dumped imports on the domestic industry, para (iv) of

Annexure-II of the AD Rules states as follows. “The examination of the impact of the dumped imports on the domestic industry

concerned, shall include an evaluation of all relevant economic factors and indices having a bearing on the state of the Industry, including natural and potential decline in sales, profits, output, market share, productivity, return on investments or utilization of capacity; factors affecting domestic prices, the magnitude of margin of dumping actual and potential negative effects on cash flow, inventories, employment, wages, growth, ability to raise capital investments.”

Submissions made by the interested parties

46. The submissions made by the exporters/importers and other interested parties are

summarized as follows to the extent they have been found to be relevant. It has been, inter alia, stated that:

(i) The imports from subject countries as a percentage of domestic demand and as a

percentage of total imports have come down in POI as compared to base year. (ii) The trend of changes in domestic selling prices and landed price of imports is

very similar to trend of changes in nickel prices and therefore, the fall in prices is on account of decrease in prices of nickel and not on account of imports.

(iii) The selling prices of the domestic industry have increased by about 30% in the

POI as compared to base year 2005-06. (iv) The market share of the domestic industry has increased by 10% in POI as

compared to previous year 2007-08. (v) The production of the domestic industry has substantially increased over injury

investigation period and the lower levels of capacity utilization are primarily on account of shutdown in Hisar and addition of massive new capacity. Further, the reduction in export sales have resulted in decreased capacity utilization.

(vi) The domestic industry has made heavy investments especially during the period

of investigation shows that the domestic industry has not suffered material injury.

17

Submissions made by the domestic industry

47. The domestic industry has stated the following: (i) It is not necessary that the imports must necessarily show an increase in

comparison to total imports or total demand. It is sufficient, if the same has increased in absolute terms. It may be seen from the para (ii) of Annexure II that the imports may either increase in absolute terms or relative to production or consumption in India and there is no condition that the imports has to show an increase both in absolute terms as well as in relation to production, demand or total imports.

(ii) It is immaterial whether the import prices have come down due to fall in raw

material prices or otherwise. What is relevant is to be seen whether the import prices have affected the domestic prices. It may be seen that the domestic prices have been undercut by the dumped imports from the subject countries throughout the injury investigation period.

(iii) With regard to domestic selling prices, the domestic industry has contended

that the analysis of injury parameters on the basis of end-point to end-point comparison is not conclusive and therefore, the changes in the POI as compared to recent years would also be seen to analyze the effect of imports on the injury. It is submitted that the interested parties did not mention the fact that the selling prices of the domestic industry in POI as compared to previous years 2006-07 and 2007-08 have significantly come down by about 21% and 37% respectively. Thus, in comparison to recent years the prices of the domestic industry in POI have been significantly affected.

(iv) With regard to the market share, the domestic industry stated that the

interested parties are comparing the performance for injury factors sometimes with the base year and sometimes with the other previous years without going into the merits for an increase. It is submitted that the interested parties have ignored the fact that prior to increase in market share in POI as compared to previous year, the market share of the domestic industry in 2007-08 has come down by about 8% as compared to previous year 2006-07 whereas at the same time the market share of imports from subject countries has increased by more than 9%. It may also be seen that the market share of the domestic industry in POI went up as compared to previous year solely due to the reduction in its selling prices significantly by about 37% due to the presence of severely dumped imports.

(v) With regard to the capacity utilisation, it is stated that the interested parties

have ignored the fact that the applicant while analyzing this factor has already submitted that since there is no separate capacity available for the product under consideration, the analysis of capacity utilization has been done on the basis of total production of all the products taken together. The applicant has also mentioned the fact in the application that the analysis of this factor may not provide guidance for the actual effect of injury suffered by the domestic industry.

18

(vi) With regard to making heavy investments in capacity expansion, the domestic

industry has stated that the anti-dumping investigations are restricted to product concerned and increase in the capacity or financial improvement with respect to other products has no bearing. It is further submitted that the capacity expansion involves long term planning and cannot be done in a short period of time. Therefore, to allege that the domestic industry has made heavy investments in the POI for capacity expansion is to be seen with reference to the start of the work but not with respect to completion of the project.

Examination by the Authority

48. The Authority has examined the injury parameters objectively taking into account the facts and the submissions of the interested parties.

i Volume Effect of dumped imports and Impact on domestic industry The details relating to imports from all the subject countries and other countries are given below in the following table:

2005-06 2006- 07 2007 – 08 POI Annualized

Imports from Subject Countries (MT) 18067 15683 10565 23783 Imports from Other Countries (MT) 2859 6519 21314 7060 Total Imports (MT) 20927 22202 31879 30843 % Share of Subject countries 86% 71% 33% 77%

Trend in Imports from Subject Countries

100 87 58

132

Trend in Imports from other countries

100 228 746

247

Trend in total Imports

100 106 152

147

Total Demand (MT) 59333 64536 75657 100320 % Share of Subject Countries in demand

30% 24% 14% 24%

It is noted that the imports from the subject countries in absolute terms have increased during POI compared to the base year.

19

ii. Demand and Market share

2005-06 2006 – 07 2007 – 08

POI-Annua-

lized Domestic Industry Sales (MT) 30406 33334 34778 58143 Sales of Other Domestic Producer 8000 9000 9000 11333 Total Domestic Sales in India (MT) 38406 42334 43778 69477 Imports from Subject Countries (MT) 18067 15683 10565 23783 Imports from Other Countries (MT) 2859 6519 21314 7060 Total Imports (MT) 20927 22202 31879 30843 Total Demand (MT) 59333 64536 75657 100320 Domestic Industry's Market Share in demand 51% 50% 45% 58% Market Share of Total Domestic Sales in demand 65% 66% 58% 58% % Share of Subject Countries in demand

30% 24% 14% 24%

The Authority notes that the market share of the domestic industry in the total demand has increased during POI compared to the base year. The Authority further notes that for any producer, in case of dumping of the goods, there are two options i.e. either to stick to the prices and lose market share or to reduce the domestic prices and suffer on account of profitability. In the present case, the domestic industry appears to have chosen not to increase the prices commensurate with the increase in costs in order to retain the market share and consequently suffered significant loss.

iii. Capacity, production & capacity utilization The details for the capacity and production of all grades and types of HR SS flat products for the injury investigation period are given in the following table

2005-06 2006 – 07 2007 – 08

POI-Annualized

Capacity (MT) 700000 700000 700000 880000 Production (MT) 538630 554437 562183 547091 Capacity Utilization% 77% 79% 80% 62%

20

The domestic industry has stated that there is no dedicated capacity for the subject goods. The goods other than subject goods are also produced from the same capacity. Therefore, the analysis of injury assessment on this factor may not provide guidance for the actual effect of injury suffered by the domestic industry. In view of the above, the Authority does not consider this factor for injury analysis. iv. Sales The Authority notes that the sales volumes as well as sales values of the domestic industry have increased over the injury investigation period. The Authority further notes that the sales of the domestic industry could increase in POI as a result of offering of the subject goods less than their cost by the domestic industry.

2005-06 2006 - 07 2007- 08

POI Annualised

Total Sales Volume (MT) – Domestic 30406 33334 34778 58143 indexed 100 110 114 191 Sales Value (Rs Lacs) – Domestic *** ***

*** ***

Indexed 100 169 190 247

v. Effect of Dumped Imports on domestic prices The Authority notes that the landed value from the subject countries over the injury investigation period has increased. However, the same has come down significantly in the POI as compared to immediate previous year. The domestic selling prices after rising in the years 2007-08 and 2008-09 have significantly come down in POI due to the presence of dumped imports. It is noted that that the domestic prices have been undercut by imports from Subject Countries throughout the injury investigation period. It is also noted that the prices of the domestic industry has not increased in line with the increase in its costs. It indicates that the prices of the domestic industry have been suppressed and in comparison to the previous two years the prices of the domestic industry in the POI have been depressed.

2005-06 2006 - 07 2007 - 08 POI

Landed Value Rs. / MT *** *** *** ***

Indexed 100 133 149 127 Domestic Selling Price Rs. / MT *** ***

*** ***

Indexed 100 154 166 129

21

Cost Rs./ MT *** *** *** ***

Indexed 100 135 177 149

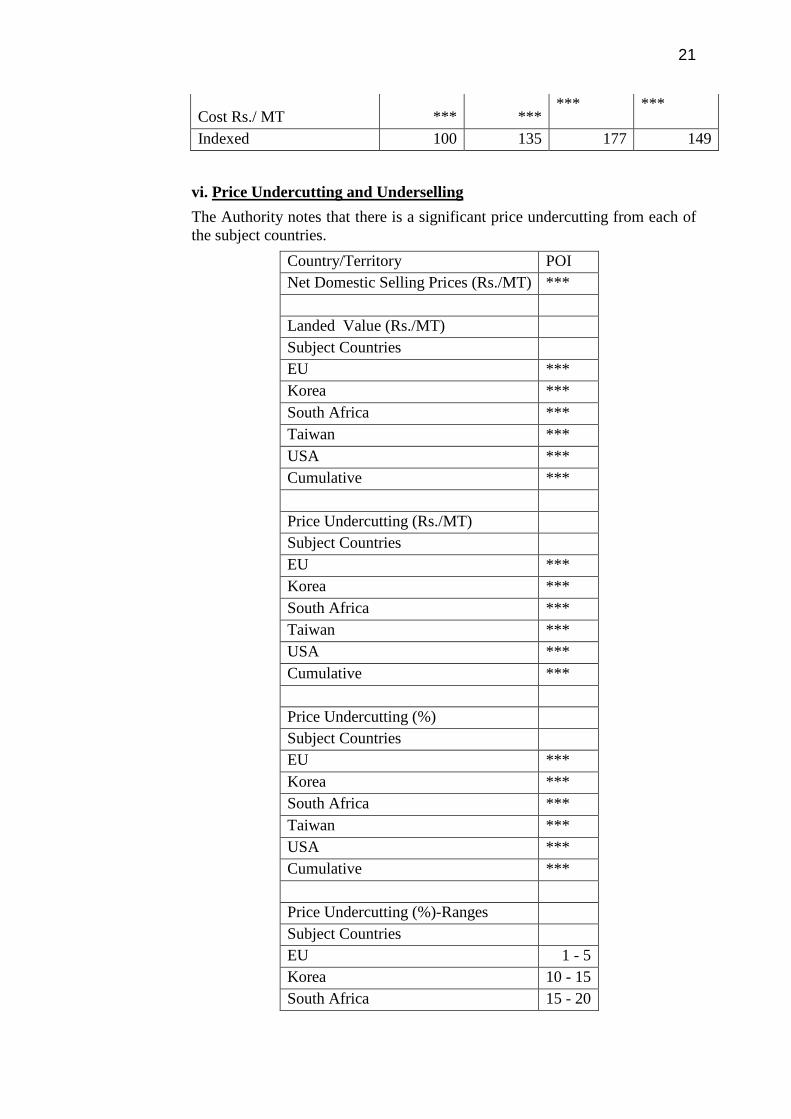

vi. Price Undercutting and Underselling The Authority notes that there is a significant price undercutting from each of the subject countries.

Country/Territory POI Net Domestic Selling Prices (Rs./MT) *** Landed Value (Rs./MT) Subject Countries EU ***

Korea ***

South Africa ***

Taiwan ***

USA ***

Cumulative ***

Price Undercutting (Rs./MT) Subject Countries EU ***

Korea ***

South Africa ***

Taiwan ***

USA ***

Cumulative ***

Price Undercutting (%) Subject Countries EU ***

Korea ***

South Africa ***

Taiwan ***

USA ***

Cumulative ***

Price Undercutting (%)-Ranges Subject Countries EU 1 - 5 Korea 10 - 15 South Africa 15 - 20

22

Taiwan 1 - 5 USA 15 - 20 Cumulative 5 - 10

The details relating to the price underselling are given in the following table:

Country/Territory POI Non-injurious Price (NIP) - Rs./MT *** Landed Value (Rs./MT) Subject Countries/Territory EU ***

Korea ***

South Africa ***

Taiwan ***

USA ***

Cumulative ***

Price Underselling (Rs./MT) Subject Countries EU (***) Korea (***) South Africa *** Taiwan (***) USA *** Cumulative (***) Price Underselling (%) Subject Countries/Territory EU (***) Korea (***) South Africa *** Taiwan (***) USA *** Cumulative (***) Price Underselling (%) - Ranges Subject Countries/Territory EU (5 – 10) Korea (1 – 5) South Africa 5 - 10 Taiwan (5 – 10) USA 5 – 10 Cumulative (1 – 5)

23

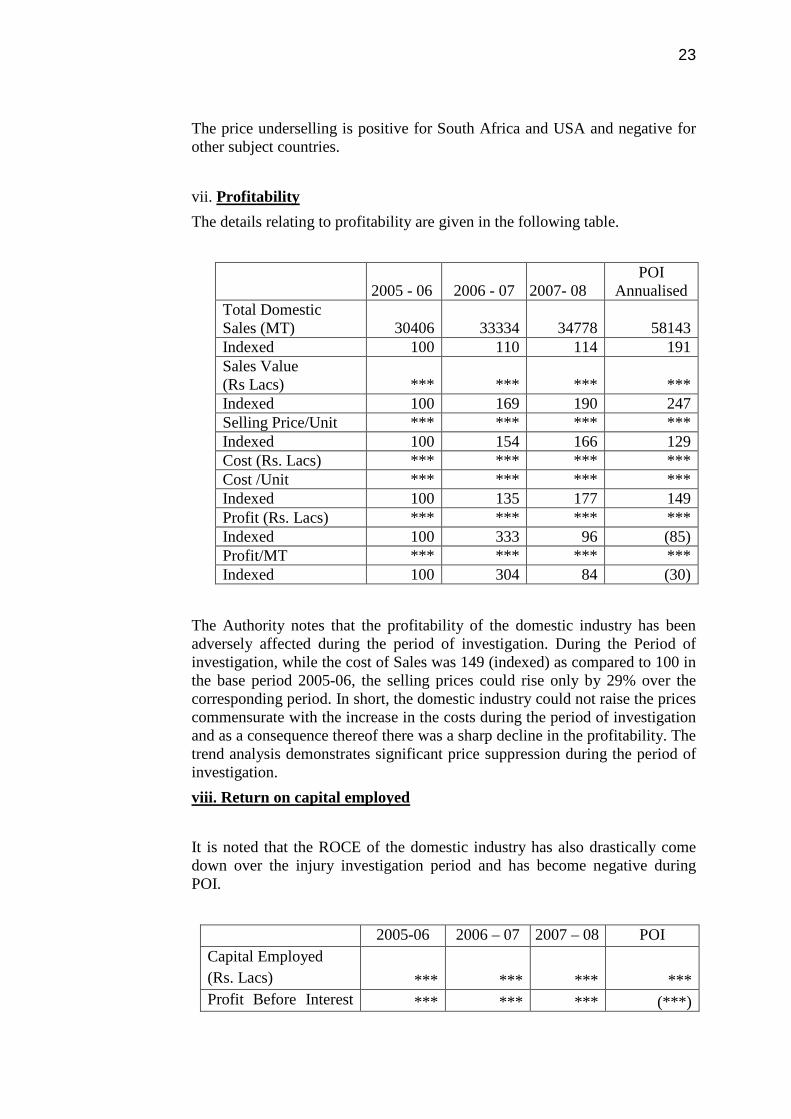

The price underselling is positive for South Africa and USA and negative for other subject countries. vii. Profitability The details relating to profitability are given in the following table.

2005 - 06 2006 - 07 2007- 08 POI

Annualised Total Domestic Sales (MT) 30406 33334 34778 58143 Indexed 100 110 114 191 Sales Value (Rs Lacs) *** *** *** *** Indexed 100 169 190 247 Selling Price/Unit *** *** *** *** Indexed 100 154 166 129 Cost (Rs. Lacs) *** *** *** *** Cost /Unit *** *** *** *** Indexed 100 135 177 149 Profit (Rs. Lacs) *** *** *** *** Indexed 100 333 96 (85) Profit/MT *** *** *** *** Indexed 100 304 84 (30)

The Authority notes that the profitability of the domestic industry has been adversely affected during the period of investigation. During the Period of investigation, while the cost of Sales was 149 (indexed) as compared to 100 in the base period 2005-06, the selling prices could rise only by 29% over the corresponding period. In short, the domestic industry could not raise the prices commensurate with the increase in the costs during the period of investigation and as a consequence thereof there was a sharp decline in the profitability. The trend analysis demonstrates significant price suppression during the period of investigation. viii. Return on capital employed It is noted that the ROCE of the domestic industry has also drastically come down over the injury investigation period and has become negative during POI.

2005-06 2006 – 07 2007 – 08 POI Capital Employed (Rs. Lacs) *** *** *** *** Profit Before Interest *** *** *** (***)

24

(Rs. Lacs) Return on Capital Employed (%) *** *** *** (***) Indexed 100 333 39 (9)

ix. Cash Flow The Authority notes that the cash flow position of the domestic industry also deteriorated during the period of investigation and followed the same trend as that of profitability and ROCE. In fact, cash profit has turned negative during POI.

2005- 06 2006 -07 2007 - 08 POI-Annua-

lized Profit/Loss (Rs. Lacs) *** *** *** (***) Add: Depreciation (Rs. Lacs) *** *** *** *** Cash Flow (In Rs. Lacs) *** *** *** (***) Indexed 100 302 102 (15) Cash Flow/Unit *** *** *** (***) Indexed 100 275 89 (8)

x. Employment and Wages It is noted that the number of employees engaged by the domestic industry as well as the wages paid to them has increased over the injury investigation period.

2005 –06 2006 - 07 2007 - 08 POI-

Annualized No of Employees *** *** *** *** Indexed 100 78 123 138 Wages Total (Rs. Lacs) *** *** *** *** Indexed 100 92 173 474

xi. Productivity The productivity per employee during the period of investigation has increased over the injury investigation period. It is noted that productivity is not a cause of injury to the domestic industry.

25

2005 –06 2006 - 07 2007 - 08 POI-

Annualized Production (MT) 36864 27640 39802 57096 Employees *** *** *** *** Production per Employee (MT) *** *** *** *** Indexed 100 97 88 113

xii. Growth It is noted that the demand in the country has increased during the injury investigation period whereas the profitability, ROCE and cash flow have deteriorated over the injury investigation period. It indicates that the growth the domestic industry has been affected.

Growth as compared to the base year 2005 - 06 2006 - 07 2007 - 08

POI-Annualized

Profit (Rs. Lacs) *** *** *** (***) % of Growth over previous year - 233 (71) (159) Cash Profit (Rs. Lacs) *** *** *** (***) % of Growth over previous year - 202 (66) (115) Return on Capital Employed (%) *** *** *** (***) % of Growth over previous year - 233 (88) (123)

xiii. Inventory The average inventories of the domestic industry have increased over the injury investigation period in spite of significant suppression of domestic selling price of the domestic industry.

2006 - 07 2007 - 08 2008 - 09 POI

Opening Stock (MT) *** *** *** *** Indexed 100 562 90 506 Closing Stock (MT) *** *** *** *** Indexed 100 16 90 67 Average Stock (MT) *** *** *** *** Indexed 100 98 90 133

26

xiv. Ability to raise capital / investment The Authority notes that the domestic industry has increased its capacity in the year 2008-09. The Authority also notes that since the demand of the subject goods in India is rising and the capacity expansion would be required in future. However, the profitability parameters do not favorably support the domestic industry to raise capital from market for further expansion in near future.

49. Magnitude of injury and injury margin

The Authority, on the basis of the comparison of the landed value of imports from the subject countries/territory with the Non-injurious price (NIP) determined for the domestic industry, has determined the injury margin for the co-operative and non-co-operative exporters/producers of subject countries/territory as under:

Country/ Territory

Producer Exporter NIP (US$)/MT

LV (US$)/MT

IM (US$)/ MT

IM as % of Landed value

EU Acerinox SA, Spain

Acerinox SA, Spain

*** *** (***) (10-20)

Acerinox SA, Spain

Acerinox Malaysia Sdn Bhd, Malaysia

*** *** (***) (1-10)

Outokumpu Stainless OY-Finland

Outokumpu Stainless OY-Finland

*** *** (***) (10-20)

Any other combination of producer/exporter

*** *** *** 30-40

Korea RP Any producer/exporter *** *** (***) (1-10)

South Africa

Columbus Stainless

Columbus Stainless

*** *** *** 1-10

Columbus Stainless

Acerinox Malaysia Sdn Bhd, Malaysia

*** *** *** 1-10

Any other combination of producer/exporter

*** *** *** 70-80

Taiwan Yieh United Steel Corporation

Yieh United Steel Corporation

*** *** *** 20-30

Any other combination of producer/exporter

*** *** *** 30-40

27

USA Any producer/exporter *** *** *** 1-10

CAUSAL LINK

50. It was examined whether other parameters listed under the AD Rules could have

contributed to injury to the domestic industry. It was found as follows:

a. Imports from Third Countries: - The imports of subject goods from sources other than the subject countries except China are below de-minimis during the period of investigation. However, the prices from China are more than the prices offered by the Subject Countries. Thus, based on the available information on record, it can be inferred that the imports from Subject Countries are being made at dumped prices and are above the de minimis limits causing cumulatively material injury to the domestic industry.

b. Contraction in Demand: - It is noted that there is no contraction in the

demand during the period under consideration. On the contrary, the overall demand has increased by over 80% over the injury investigation period.

c. Pattern of consumption: - No significant change in the pattern of

consumption has been observed.

d. Conditions of competition: - The applicant has claimed that conditions of competition or trade restrictive practices are not responsible for the claimed injury to the domestic industry. No interested party has refuted this claim.

e. Developments in technology: - The applicant has claimed that there is no

significant change in technology, which could have caused injury to the domestic industry. No interested party has disputed this claim.

f. Export performance of the domestic industry: - The export performance

of the domestic industry in no way has affected the financial and economic situation of the applicant in the domestic market. In any case, the foregoing injury analysis in respect of the petitioner is restricted only to their domestic performance.

51. The Authority notes that while other known factors examined above have not caused

injury to the domestic industry, following parameters show that injury to the domestic industry has been caused by dumped imports:

a. Imports from subject countries have increased in absolute terms as well as

in relation to domestic production in India.

b. The prices of the domestic industry have been suppressed despite increase in demand.

28

c. The profitability, ROCE and cash flow of the domestic industry has significantly deteriorated over the injury investigation period.

d. There is a significant price undercutting from each of the subject

countries. e. There is a significant dumping margin from each of the subject countries.

52. Post disclosure comments of interested parties: i) The claim of the petitioner that they had manufactured and sold materials of all

thicknesses and length is contrary to facts. Such claims are unverified. ii) Black coil has to be excluded from product scope as it differs from PUC in terms of

production process, mechanical and chemical characteristics, cost of production, end uses, etc,.

iii) There is no adverse volume effect on domestic industry as the share of subject imports has fallen from 30% in the base year to 24% during POI, while the share of domestic industry during the same period has risen from 51% to 58%. Further, increase in imports from subject countries is lower compared to increase in total demand.

iv) There is no adverse price effect also. A cumulative price underselling implies that the landed value of imports from the subject countries taken cumulatively is higher than NIP of the domestic industry. When imports are entering at a price higher than NIP, the question of adverse price effect does not arise.

v) Price underselling for EU and Taiwan are negative. There cannot be any duty on imports from these countries.

vi) Causal link between imports and injury gets broken when the landed value of dumped imports is higher than the NIP. If losses are incurred by domestic industry despite selling above NIP, it has to be for reasons other than dumped imports.

vii) Though there were minor negative movements in certain factors, those negative or adverse movements were not strong enough to undermine the positive trends recorded in other factors. Despite a negative trend in profits, domestic industry was not ‘materially’ injured as they were selling above NIP and the injury margin or price underselling was negative.

viii) On behalf of Yusco, Taiwan it has been submitted that the authority unreasonably rejected rebates claimed by Yusco without providing a legitimate reason. In the initial exporters questionnaire response Yusco submitted the sample rebate documents, which include the internal memo and the external rebate certificates issued to the customers.

ix) It is unreasonable for the authority to compare weighted average export price to India with the weighted average normal value without taking into consideration the size differences sold in the two markets. Such comparison has distorted dumping margin because it does not compare the prices of goods sold by Yusco to India with the prices of comparable products sold in domestic market.

x) It is not the capability to supply, but the actual supply which should be the definitive test.

xi) It is neither commercially viable nor technically feasible for the user industry to substitute subject goods of widths of 1250 mm in applications requiring wider widths.

29

There are certain applications such as tanks/railway rakes, etc, which do not clearly have the tensile strength to hold based on wielding smaller widths together. Slitting and welding the products would have a significant commercial cost on the end product.

xii) Special grade variants such as 304N, 304LN, 304H, 304B4, 304B7 required for special applications in Nuclear Power Plant, Thermal Power Plant, Aerospace and Defence applications should be excluded from the purview of this investigation. Grades with thickness > 80 mm as per ASTM specification should be excluded from the scope of the present investigation as grades with thickness > 80 mm as per ASTM specification are not produced in India.

xiii) The Designated Authority may disclose the evidence in regard to the Petitioner having major proportion of domestic production being more than 50% of the Indian production and names of other producers whose data has been considered.

xiv) The volume and price data for the subject countries in question has not been disclosed.

xv) The methodology adopted for calculating the Non-injurious Price is generalized and no specific details have been provided. There is no disclosure as to why 22% has been granted to the Petitioners.

xvi) Malaysia, which accounts for approximately 8% of the imports of the subject goods into India at prices lower than the prices from the subject country, has been excluded from the scope of the present investigation. Hence, causal link between the alleged injury to domestic industry and the imports of the subject goods from the subject countries is not established.

xvii) The basis for difference between the imports reported by the Petitioner and the imports finally considered by the designated authority must be clarified to the interested parties.

xviii) The Petitioner has not suffered from any price suppression/depression and has not faced any injury on this parameter.

xix) The decline in profitability and ROCE is not attributable to any of the imports of the subject goods but are due to other factors enumerated in the annual report of the petitioner for the year 2008-09.

xx) There is no evidence placed on record to establish that the Petitioner has sold below cost.

53. Post disclosure submissions by domestic industry.

i) Domestic Industry has cited several cases including polypropylene, MDF, SDH

equipment, etc. in which the authority is claimed to have used the concept of capability of the domestic industry to produce certain types of the PUC and not the fact of actual production or sales. On this basis the authority cannot exclude widths of over 1250 mm on the ground that the same were not offered by the domestic industry during the POI.

ii) Domestic industry in the written submissions dated 16th August 2011 had claimed that total cost of slitting including wastage is not more than Rs.1000/MT. There is no finding or observation by DA which contradicts the said submission of the domestic industry.

30

iii) Foreign exporters have opened service centres which carry out the slitting operations, as submitted by Posco in the CR 400 Series case. There are various service centres who are engaged in slitting of 1500 mm width coils. A sample bill is enclosed showing that the cost of slitting is about 50 paise a kilo.

iv) The authority in the disclosure statement has not dealt with the case of MDF which was cited by the domestic industry at various stages of investigation. It has been urged that the authority give due consideration to existing jurisprudence as well as past precedents and practices in regard to restricting the PUC to 1250 mm + tolerance.

v) The e-mail relied upon by the DA to infer that the domestic industry has not been able to offer/supply of subject goods of more than 1250 mm width when a demand has been raised is dated 6.5.2010, which is outside the POI.

vi) Cost of process raw materials must be included in the computation of NIP due to the following reasons. a) Copper and molybdenum are used by the domestic industry as process raw

materials to preserve the corrosion resistance/austenitic properties of grade 304. The usage of these materials is technology related issue which may vary from plant to plant. There is nothing in the law to exclude cost of certain raw materials on the ground that their use is not mandatory.

b) Merely because certain exporters use different process materials cannot be a ground for including the cost of material actually used by the domestic industry.

c) Exclusion of raw material on the ground that it is not necessary on the basis of opinion of the competitors is not in accordance with the principles of natural justice and the settled jurisprudence on the issue of NIP.

d) Exporters also use copper as one of the process materials for preserving the austenitic properties.

e) Evidence submitted by the domestic industry regarding use of similar materials by other producers has not been considered.

f) The cost of process raw materials are reflected in the audited accounts as cost of PUC and are duly audited from time to time by the company auditors.

vii) The approach adopted by the authority in using the capacity utilisation of a period other than POI is contrary to the decision of the Hon’ble Supreme Court in the case of Reliance Industries Vs Designated Authority (2006(202)ELT23). It is also mentioned that the capacities of different types of HR flat products is common and the specific capacity for the PUC is indeterminate. The amendment to the Rules does not in any manner alter or affect the ratio of the decision of the Hon’ble Supreme Court.

viii) The injury margin computed for Korea cannot be negative as the landed value for Korea computed by the domestic industry is lower than the NIP computed by the Authority, which is disputed by the domestic industry.

54. Examination of post disclosure submissions by Authority i) It is noted that the Petitioners has submitted evidence of manufacturing the subject

goods of different thicknesses. ii) The Authority notes that Black coil is a hot rolled product and the same is also sold

by the domestic industry. Therefore, Black coil is not excluded from the PUC.

31

iii) The volume analysis proposed in the disclosure statement has already arrived at the figures mentioned by the interested parties relating to the comparative market share of subject countries and that of the domestic industry in total demand.

iv) As regards price effect, price undercutting and price suppression effects on domestic industry, which are injury parameters laid down in the rules, are found positive in the present investigation. Price underselling is not an injury parameter under the Anti Dumping Rules.

v) Anti dumping duty is determined by the authority on the basis of dumping margin or injury margin, whichever is lower. Injury margin calculation for residual exporters of a country/territory follows a methodology different from that adopted for price underselling which is determined in respect of a country/territory as a whole. The basis of calculation of landed value which is a factor in injury margin is duly spelt out in these findings.

vi) Magnitude of injury and injury margin is assessed country-wise and exporter-wise (where there is cooperation by the exporters/producers of a subject country). In the present case, injury margin is positive in certain instances and negative in certain other instances. Thus causal link is not broken.

vii) As regards Yusco, Taiwan, it is noted that the sample copies of documents submitted by the exporter in support of their rebate claims for adjustments on domestic selling price do not corroborate with the domestic sales nor any reference of sales invoices mentioned in the documents submitted to the Authority. The consultants of Yusco, Taiwan have also not been able to corroborate the claims vis-a-vis the sales documents in person.

viii) As regards comparison of weighted average export price to India with the weighted average normal value without considering the size differences sold in the two markets, as brought out by Yusco, it is noted that mere size differences in PUC do not warrant PCN wise dumping analysis. It is further noted that neither the domestic industry nor other interested parties have provided information for dumping analysis PCNwise.

ix) Special grade variants required for special applications in nuclear power plant, thermal power plant, etc. and claimed for exclusion from the purview of PUC have not been duly corroborated nor supported by evidence.

x) The issue relating to domestic industry standing of the Petitioner is an issue addressed in the initiation notification itself. The same has not been controverted nor contested by any interested party during the entire course of investigation. The said issue at this belated stage is not considered relevant by the Authority.

xi) The volume and price data of imports for the subject countries have been drawn from DGCI&S source and adopted for injury analysis as well as for determining dumping and injury margin for those countries from which no exporter/producer has cooperated.

xii) The methodology adopted for calculating the NIP has been disclosed as per the standard practice being followed and 22% return on investment has been granted to the Petitioner as per the consistent practice followed in this regard.

xiii) As regards imports from Malaysia, it is noted that DGCI&S’s data during the POI has reported the highest volume of imports of the subject goods and the same has been adopted for the purpose of present investigation. The DGCI&S’s data has been corroborated with the IBIS data and it is noted that as per both the sources, the imports from Malaysia is below deminimis. Hence, the question of causal link not

32

being established between injury to domestic industry and the subject imports due to exclusion of Malaysia does not arise. This also explains the difference between the import data reported by the Petitioner (from Cybex source) and that considered by the DA.

xiv) The price suppression effect on the domestic industry in the present investigation has been established as reflected in the appropriate part of these findings.

xv) The decline in profitability and ROCE as a result of dumped imports is suitably addressed in the injury and causal link analysis.

xvi) As regards domestic industry’s claim for not excluding widths above 1250 mm in the light of past precedents including the case of MDF, it is noted that there are also past cases in which the Authority has excluded certain grades/specifications from PUC as the same were not manufactured by the domestic industry during the relevant period. These cases notwithstanding, the Authority holds that the past cases cannot be the guide when the jurisprudence in this regard is otherwise. Authority’s position in this regard is supported by the available jurisprudence in the matter placed on record by interested parties. In this regard, the Authority relies upon the orders of Hon’ble CESTAT in the following cases:- a) Magnet User Association Vs. Designated Authority (2003.9157 ELTD 150 (Tri-Del)):

“...................... There is no justification for including grades of ring magnets which are not produced in India for the purpose of imposition of anti-dumping duty. Exclusion of such products from the scope of anti-dumping duty is warranted. Customs Notification is required to be suitably modified for this purpose”. (relevant part of the judgement has been quoted).

b) Oxo Alcohols Industries Association Vs. Designated Authority [2001(130) ELT 58]:

In this case, the Hon’ble CESTAT held that if the products are not manufactured by the domestic industry, the import of the same product cannot cause injury to domestic industry. The relevant portion of the judgement is quoted as under:-

“....................... Further, normal Hexanol is not one manufactured or produced by domestic industry. So its import cannot cause injury to domestic industry. Therefore, anti-dumping duty imposed on normal Hexanol imported into India is only to be vacated and we do so”.

xvii) The Authority notes that an e-mail dated 24.12.2008 (which falls in POI) evidencing that the domestic industry has not been able to offer/supply the subject goods of more than 1250 mm width when demand has been raised, has also been placed on record by the interested parties.

xviii) The slitting operations mentioned by the domestic industry are not commercially feasible at the end of the consumers/end users.

xix) The Authority has not considered the cost of molybdenum, copper, etc., claimed to have been consumed in the manufacture of the PUC by the domestic industry not only on the basis of usage of raw materials by other exporters but also primarily on the basis of technical advice received from Ministry of Steel, Government of India, the nodal ministry for the steel industries.

xx) While the disputed materials could have been consumed by JSL and accounted for in its books of accounts, their usage in manufacture of the PUC has not been

33

conclusively proved as the details of raw material consumption provided by domestic industry initially showed consumption of negligible quantity of these subject materials as against consumption of large quantity of such materials worked out on apportionment basis at a later stage.

xxii) With regard to the contention of the domestic industry that other exporters also use copper and other materials like Titanium and Columbium in lieu of molybdenum, the Authority notes as under: (a) The document downloaded from the website of www.atimetals.com show that

there are 3 types of 304 Grade SS products viz 304/304L and AL304DA. It is noted from the details that while 304/304L/AL304DA grade do not include Copper or molybdenum, AL304DA includes traces of Titanium and Columbium. It is also seen that AL304 DA is a patented product produced by Allegheny Ludlum and it comprises of 40% 304 grade SS and 60% stabilised carbon steel. In view of the above, the authority holds that the evidence submitted by the domestic industry in this regard does not support its contention that molybdenum and copper are required for the manufacture of PUC.