non-conventional gas supply … gadde - unconventional supply… · 2 delivering commercial insight...

TRANSCRIPT

www.woodmac.com

Delivering commercial insight to the global energy industry

Non-Conventional Gas Supply Impacts on the Energy Picture

2

Delivering commercial insight to the global energy industry

www.woodmac.com

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

2000 2005 2010 2015 2020

mm

cfd

UnconventionalConventional

34% 75%

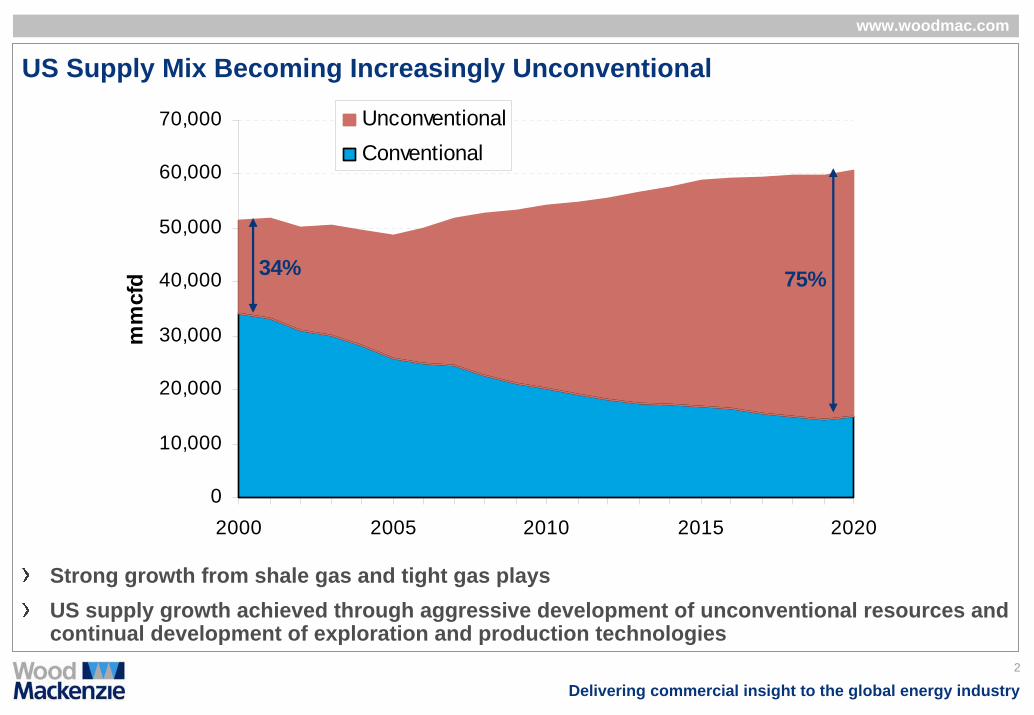

US Supply Mix Becoming Increasingly Unconventional

Strong growth from shale gas and tight gas playsUS supply growth achieved through aggressive development of unconventional resources and continual development of exploration and production technologies

3

Delivering commercial insight to the global energy industry

www.woodmac.com

0

4,000

8,000

12,000

16,000

2000 2005 2010 2015

mm

cfd

Antrim Lewis/Mancos/Mowry Appalachia DevonianBarnett Fayetteville WoodfordHaynesville Marcellus

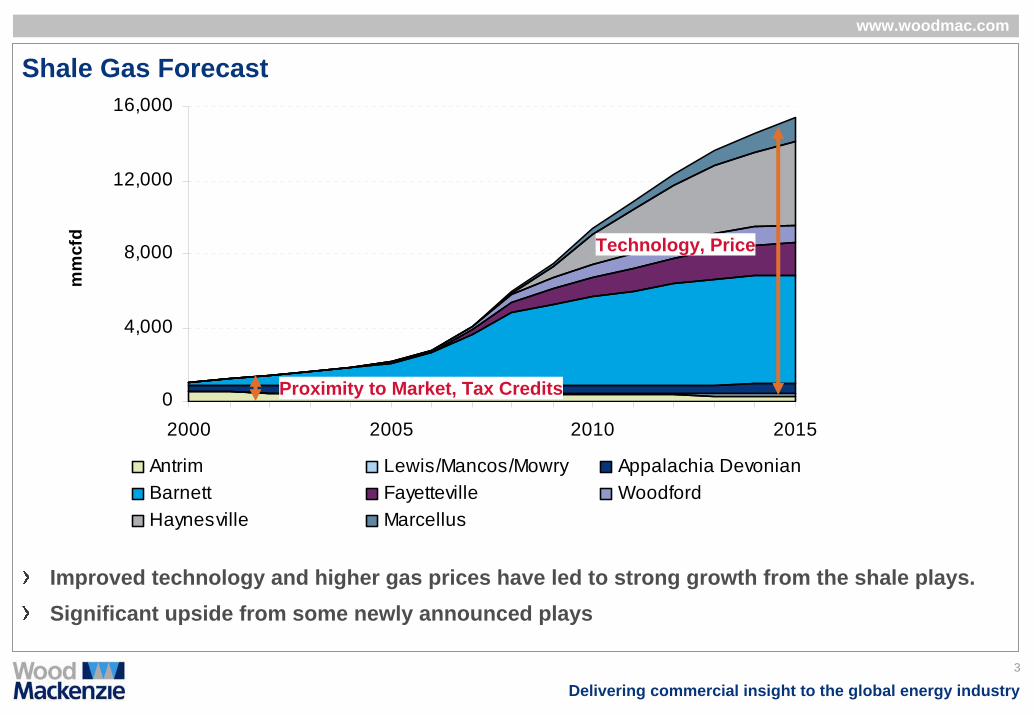

Shale Gas Forecast

Improved technology and higher gas prices have led to strong growth from the shale plays.Significant upside from some newly announced plays

Technology, Price

Proximity to Market, Tax Credits

4

Delivering commercial insight to the global energy industry

www.woodmac.com

What is Shale Gas?

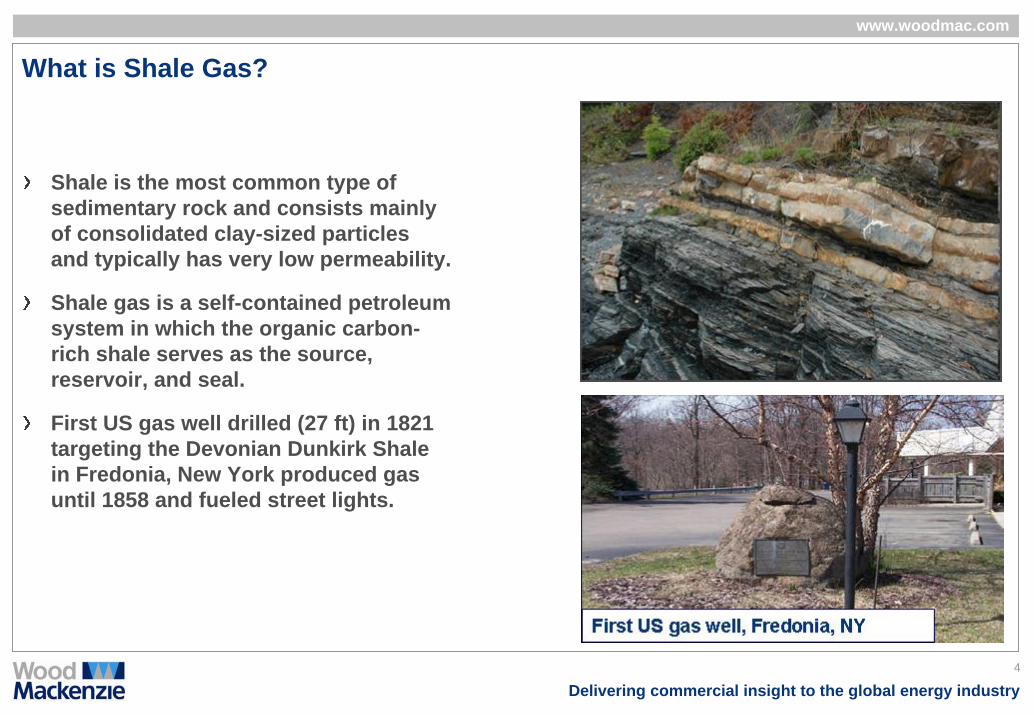

Shale is the most common type of sedimentary rock and consists mainly of consolidated clay-sized particles and typically has very low permeability.

Shale gas is a self-contained petroleum system in which the organic carbon-rich shale serves as the source, reservoir, and seal.

First US gas well drilled (27 ft) in 1821 targeting the Devonian Dunkirk Shale in Fredonia, New York produced gas until 1858 and fueled street lights.

5

Delivering commercial insight to the global energy industry

www.woodmac.com

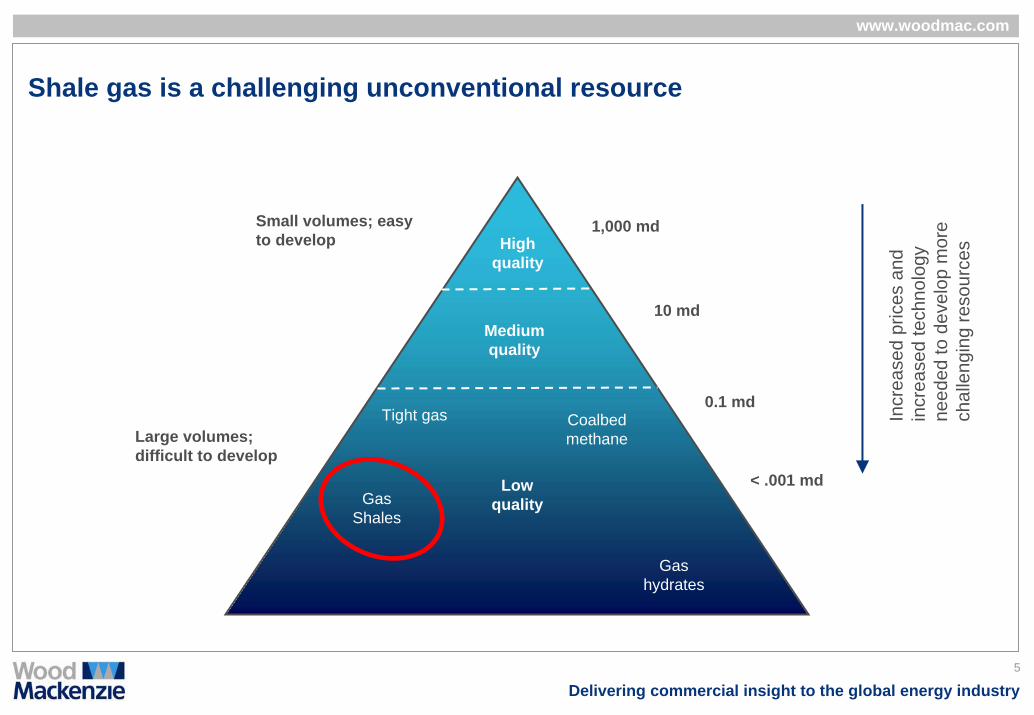

Shale gas is a challenging unconventional resource

Small volumes; easy to develop

Large volumes; difficult to develop

High quality

Medium quality

Low quality

Gas hydrates

Gas Shales

Coalbed methane

Tight gas

1,000 md

10 md

0.1 md

< .001 md

Incr

ease

d pr

ices

and

in

crea

sed

tech

nolo

gy

need

ed to

dev

elop

mor

e ch

alle

ngin

g re

sour

ces

6

Delivering commercial insight to the global energy industry

www.woodmac.com

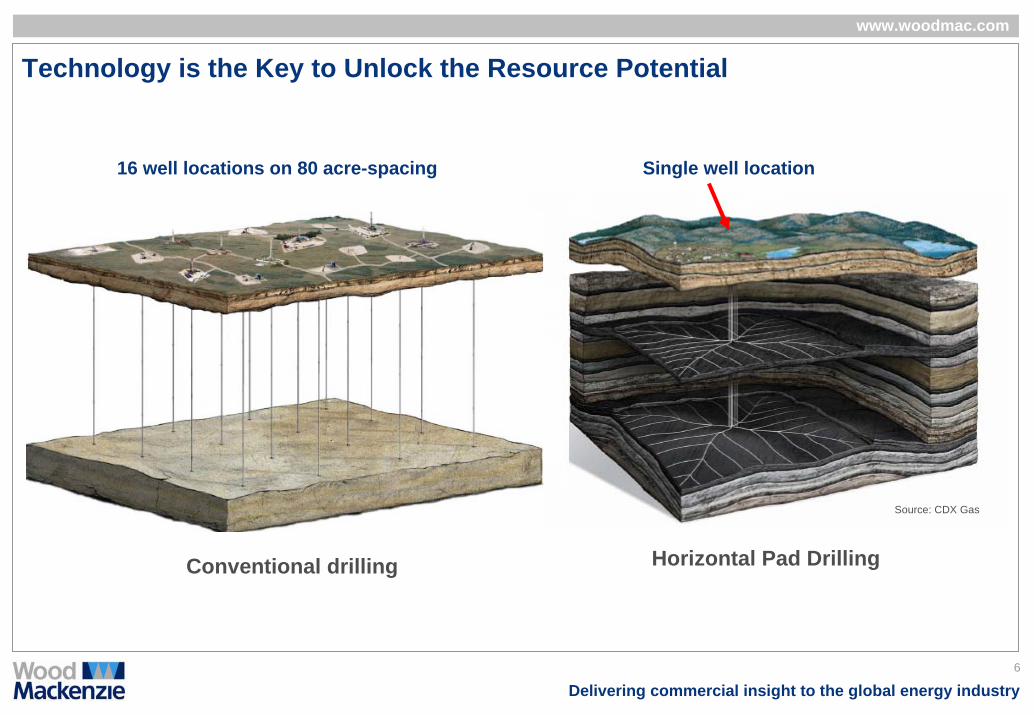

Single well location

Horizontal Pad Drilling

Source: CDX Gas

16 well locations on 80 acre-spacing

Conventional drilling

Technology is the Key to Unlock the Resource Potential

7

Delivering commercial insight to the global energy industry

www.woodmac.com

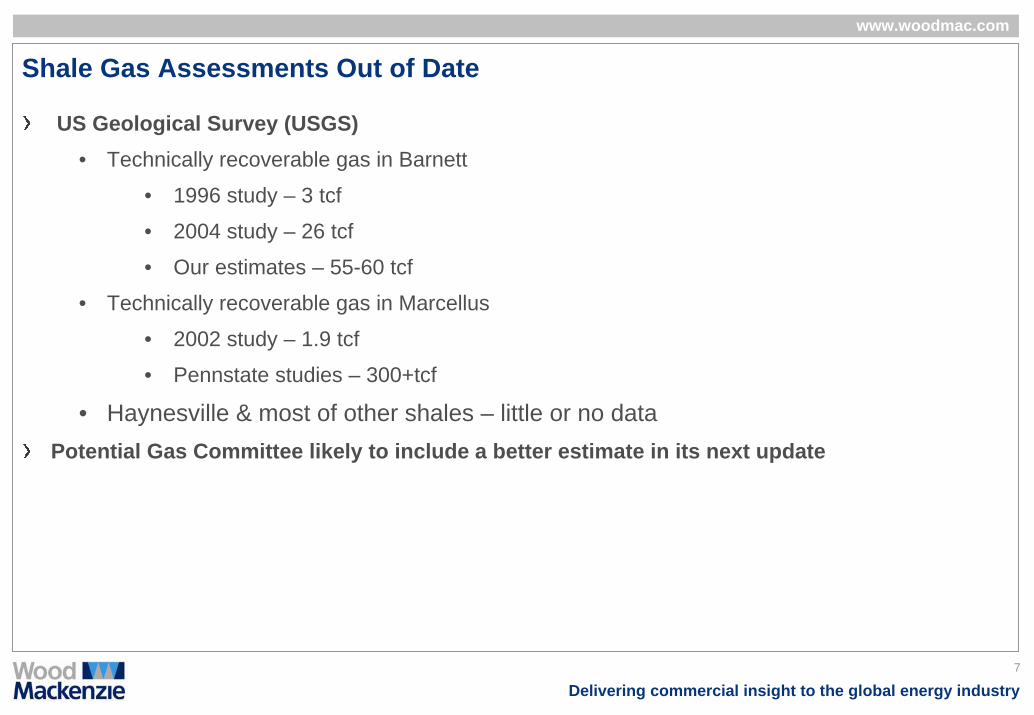

Shale Gas Assessments Out of Date

US Geological Survey (USGS)• Technically recoverable gas in Barnett

• 1996 study – 3 tcf

• 2004 study – 26 tcf

• Our estimates – 55-60 tcf

• Technically recoverable gas in Marcellus

• 2002 study – 1.9 tcf

• Pennstate studies – 300+tcf

• Haynesville & most of other shales – little or no dataPotential Gas Committee likely to include a better estimate in its next update

8

Delivering commercial insight to the global energy industry

www.woodmac.com

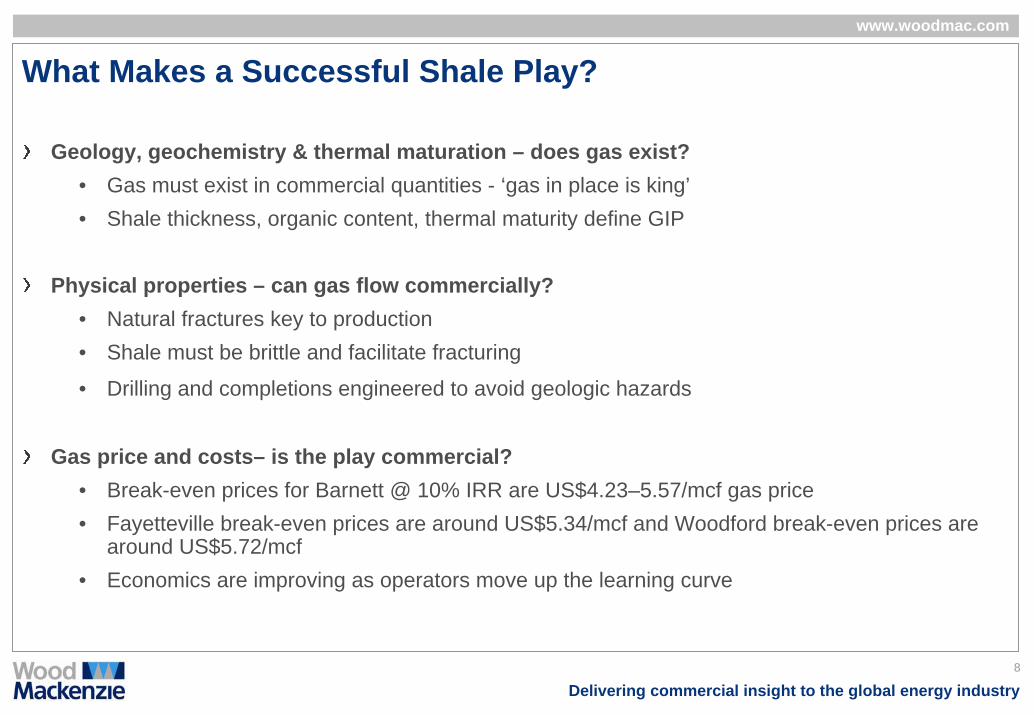

What Makes a Successful Shale Play?

Geology, geochemistry & thermal maturation – does gas exist?• Gas must exist in commercial quantities - ‘gas in place is king’• Shale thickness, organic content, thermal maturity define GIP

Physical properties – can gas flow commercially? • Natural fractures key to production• Shale must be brittle and facilitate fracturing

• Drilling and completions engineered to avoid geologic hazards

Gas price and costs– is the play commercial?• Break-even prices for Barnett @ 10% IRR are US$4.23–5.57/mcf gas price• Fayetteville break-even prices are around US$5.34/mcf and Woodford break-even prices are

around US$5.72/mcf• Economics are improving as operators move up the learning curve

9

Delivering commercial insight to the global energy industry

www.woodmac.com

Common Themes of Successful Shale Gas Projects

Large developments with significant upfront investment Economies of scale required for aggressive cost control Operator size matters – development dominated by larger operatorsNot all acreage is equal – “sweet spots” and early mover advantageShale gas plays require continuous technical feedback loop – need to customize general technology to fit each shale

10

Delivering commercial insight to the global energy industry

www.woodmac.com

Shales Survive Drastic CutsOperators have made significant investments in acquiring acreage

• Drilling expected to be robust to hold acreageHaynesville

• Petrohawk and Chesapeake to maintain Haynesville activity at previously planned levels despite cuts elsewhere

Fayetteville • Southwestern increased spending by $0.5 billion. Chesapeake expected to maintain 20 rigs in the play –

nearly double early 2008 levels but 3 rigs below previous estimates. Petrohawk to run 11 rigs, higher than 2008 average.

Woodford• Newfield to increase rig count from 12 to 14 – 3 rigs below previous estimates.

Barnett• Quicksilver reduced rigs from 14 to 9. Chesapeake had laid /moved 10 rigs. Rig reductions so far around 20%

BC shale• Apache to invest US$260 Million in the play. EnCana, Quicksilver and EOG also committing capital to further

test and develop the play.Marcellus

• Range and several others stepping up activity. Range deploying six fit-for-purpose rigs. Chesapeake planning to reach 20 rigs in the play by end of 2009

11

Delivering commercial insight to the global energy industry

www.woodmac.com

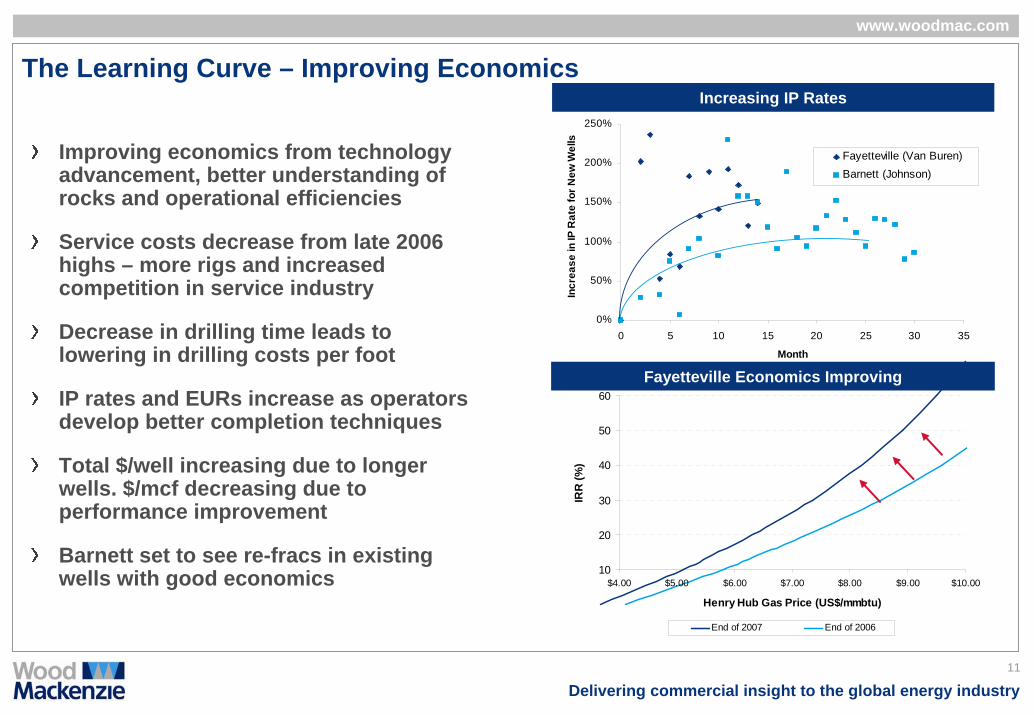

The Learning Curve – Improving Economics

Improving economics from technology advancement, better understanding of rocks and operational efficiencies

Service costs decrease from late 2006 highs – more rigs and increased competition in service industry

Decrease in drilling time leads to lowering in drilling costs per foot

IP rates and EURs increase as operators develop better completion techniques

Total $/well increasing due to longer wells. $/mcf decreasing due to performance improvement

Barnett set to see re-fracs in existing wells with good economics

0%

50%

100%

150%

200%

250%

0 5 10 15 20 25 30 35

Month

Incr

ease

in IP

Rat

e fo

r New

Wel

ls

Fayetteville (Van Buren)Barnett (Johnson)

Increasing IP Rates

10

20

30

40

50

60

$4.00 $5.00 $6.00 $7.00 $8.00 $9.00 $10.00

Henry Hub Gas Price (US$/mmbtu)

IRR

(%)

End of 2007 End of 2006

Fayetteville Economics Improving

12

Delivering commercial insight to the global energy industry

www.woodmac.com

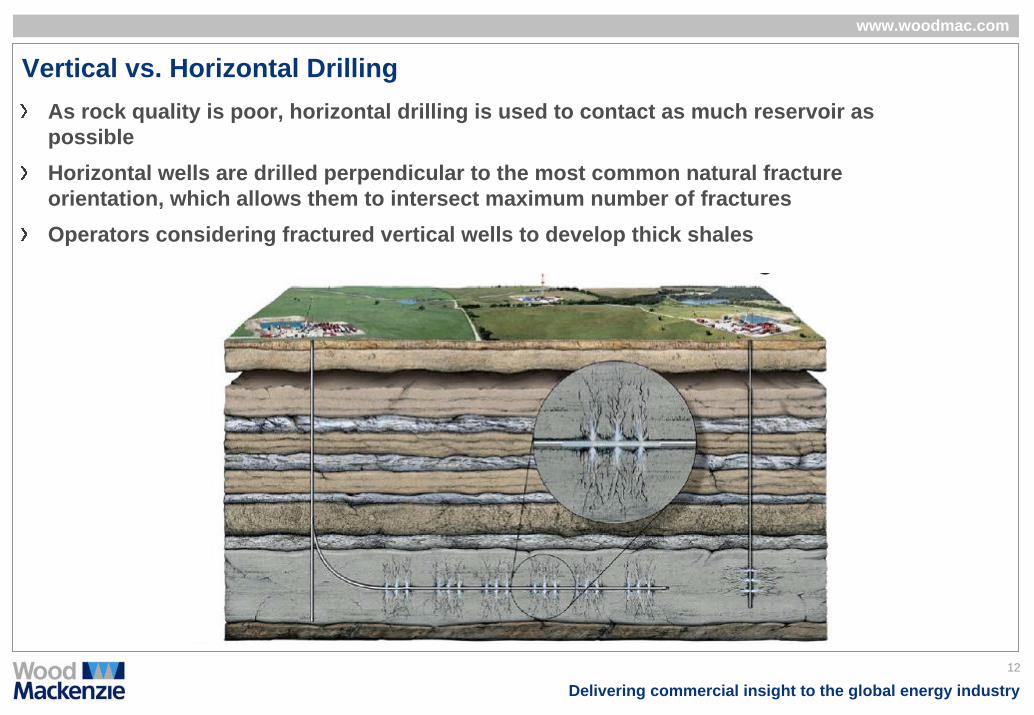

Vertical vs. Horizontal DrillingAs rock quality is poor, horizontal drilling is used to contact as much reservoir as possibleHorizontal wells are drilled perpendicular to the most common natural fracture orientation, which allows them to intersect maximum number of fracturesOperators considering fractured vertical wells to develop thick shales

13

Delivering commercial insight to the global energy industry

www.woodmac.com

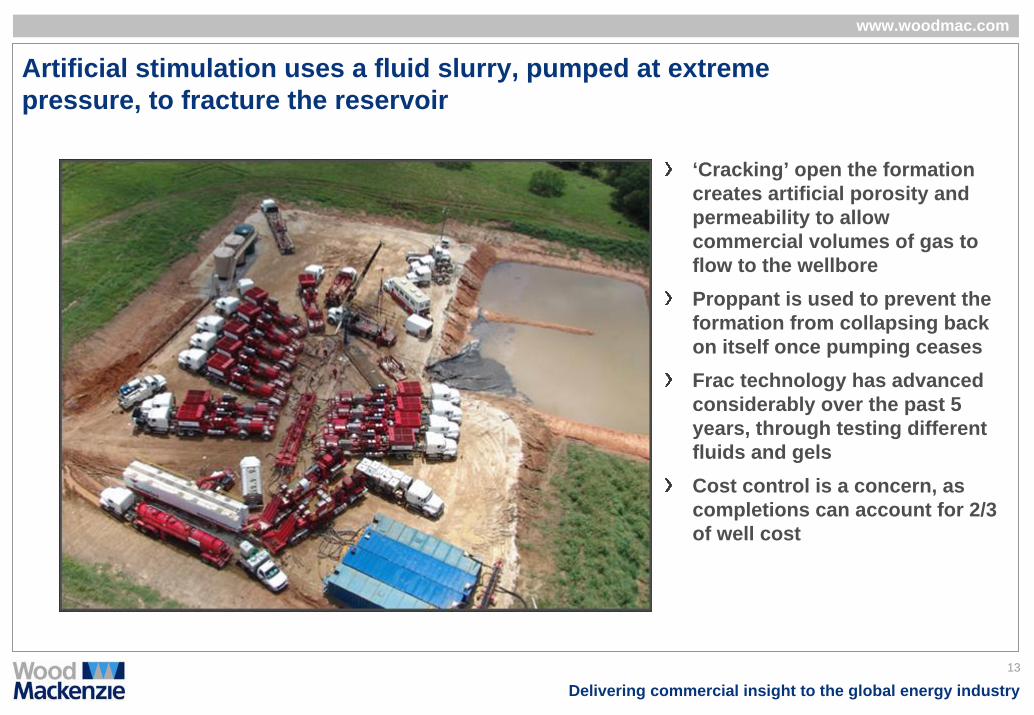

Artificial stimulation uses a fluid slurry, pumped at extreme pressure, to fracture the reservoir

‘Cracking’ open the formation creates artificial porosity and permeability to allow commercial volumes of gas to flow to the wellboreProppant is used to prevent the formation from collapsing back on itself once pumping ceasesFrac technology has advanced considerably over the past 5 years, through testing different fluids and gelsCost control is a concern, as completions can account for 2/3 of well cost

14

Delivering commercial insight to the global energy industry

www.woodmac.com

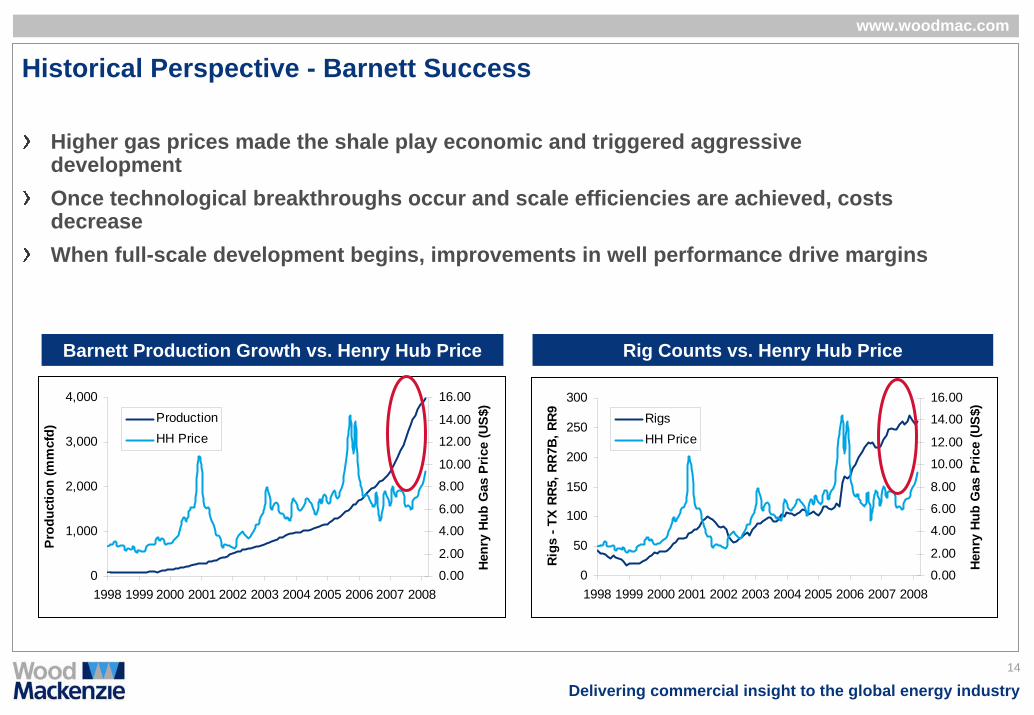

Historical Perspective - Barnett Success

Barnett Production Growth vs. Henry Hub Price Rig Counts vs. Henry Hub Price

Higher gas prices made the shale play economic and triggered aggressive developmentOnce technological breakthroughs occur and scale efficiencies are achieved, costs decreaseWhen full-scale development begins, improvements in well performance drive margins

0

50

100

150

200

250

300

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Rigs

- TX

RR

5, R

R7B,

RR9

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

Henr

y Hu

b G

as P

rice

(US$

)

RigsHH Price

0

1,000

2,000

3,000

4,000

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Prod

uctio

n (m

mcf

d)

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

Henr

y Hu

b G

as P

rice

(US$

)

ProductionHH Price

www.woodmac.com

Delivering commercial insight to the global energy industry

Important Shale Gas Plays

16

Delivering commercial insight to the global energy industry

www.woodmac.com

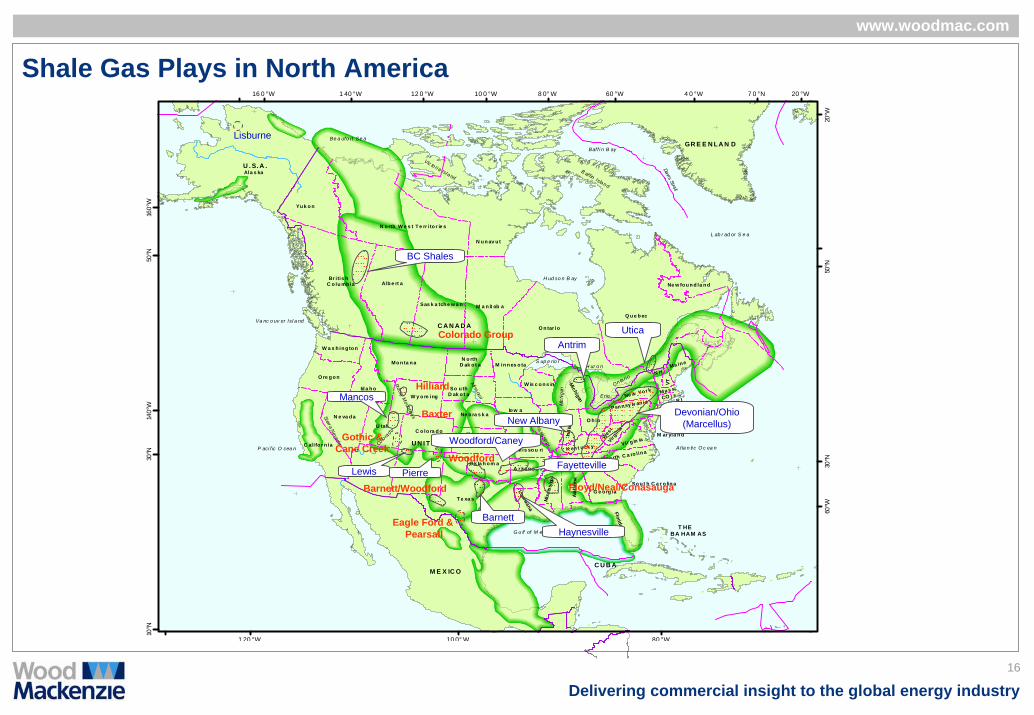

Shale Gas Plays in North America

Br itis hC o lu mb ia Alb e rt a

Sas k a tch e w a n M a n it ob a

O n tar io

Q u e b ec

Ne w fo u n d la n d

W a s h in g to n

O re g o n

C alifo r n ia

N e va d a

A rizo n a N ew M ex ico

T e xa s

O k la h o m a

Louisiana

Mis

siss

ipp

i

Ala

bam

a

G e o rg ia

Florida

So u t h C a r o lin a

N o rth C a ro lin aVir g in iaW

est

Virg

inia

Psn n sy lv an iaNe w Yor k

Ma ine

Ma s s.

R ICO

N H

VTMichigan

U tah

Id a h o

Mo n ta n a N o rthD ak o t a

So u thD ak o t a

K an s a sC o lo ra d o

W y o m ing

K en t u ck y

T e nn e ss e e

Ne b ra s k a

M in n es o ta

W is c o n s in

Io w a

Mis so u ri

A r ka n s a s

Il l in o is O h io

Ind

iana

M ar yla n d

Ne w Je r se y

C A N A D A

U N I TE D S T A TE S O F A M E R I C A

M E X IC O

H ud so n B ay

S up e rio rH ur o n

Mic

higa

n

Erie

On ta rio

Colorado

Missouri

Mississippi

A t la n ti c O c ea n

G u lf of M exi co

P aci f ic O cea n

Sierra Nevada

Rocky M

ountains

C U B A

T HEBA HAM AS

N u n av u t

N o rth W e s t T e rr ito r ie s

Yu k o n

U . S. A .Ala s ka

Be a ufo rt Se a

B affin Island

Vic to ria Island

Baff i n B ay

Davis Strait

L ab r ad or S e a

Va nc o uv er Isl a nd

GR E E N LA N D

1 40 °W16 0 °W

1 20 °W

12 0 °W

10 0° W

10 0 °W 8 0° W

80 °W

60 °W 4 0 °W 20 °W

10°N

30°N

30°N

50°N

50°N

140°

W16

0°W

60°W

20°W

7 0 °N

Baxter

Woodford

Barnett/Woodford

Antrim

Devonian/Ohio (Marcellus)New Albany

Barnett

PierreFayetteville

Woodford/Caney

Floyd/Neal/Conasauga

Lisburne

Eagle Ford & Pearsall

BC Shales

Lewis

Mancos

Colorado Group Utica

Haynesville

Hilliard

Gothic & Cane Creek

Br itis hC o lu mb ia Alb e rt a

Sas k a tch e w a n M a n it ob a

O n tar io

Q u e b ec

Ne w fo u n d la n d

W a s h in g to n

O re g o n

C alifo r n ia

N e va d a

A rizo n a N ew M ex ico

T e xa s

O k la h o m a

Louisiana

Mis

siss

ipp

i

Ala

bam

a

G e o rg ia

Florida

So u t h C a r o lin a

N o rth C a ro lin aVir g in iaW

est

Virg

inia

Psn n sy lv an iaNe w Yor k

Ma ine

Ma s s.

R ICO

N H

VTMichigan

U tah

Id a h o

Mo n ta n a N o rthD ak o t a

So u thD ak o t a

K an s a sC o lo ra d o

W y o m ing

K en t u ck y

T e nn e ss e e

Ne b ra s k a

M in n es o ta

W is c o n s in

Io w a

Mis so u ri

A r ka n s a s

Il l in o is O h io

Ind

iana

M ar yla n d

Ne w Je r se y

C A N A D A

U N I TE D S T A TE S O F A M E R I C A

M E X IC O

H ud so n B ay

S up e rio rH ur o n

Mic

higa

n

Erie

On ta rio

Colorado

Missouri

Mississippi

A t la n ti c O c ea n

G u lf of M exi co

P aci f ic O cea n

Sierra Nevada

Rocky M

ountains

C U B A

T HEBA HAM AS

N u n av u t

N o rth W e s t T e rr ito r ie s

Yu k o n

U . S. A .Ala s ka

Be a ufo rt Se a

B affin Island

Vic to ria Island

Baff i n B ay

Davis Strait

L ab r ad or S e a

Va nc o uv er Isl a nd

GR E E N LA N D

1 40 °W16 0 °W

1 20 °W

12 0 °W

10 0° W

10 0 °W 8 0° W

80 °W

60 °W 4 0 °W 20 °W

10°N

30°N

30°N

50°N

50°N

140°

W16

0°W

60°W

20°W

7 0 °N

Baxter

Woodford

Barnett/Woodford

Antrim

Devonian/Ohio (Marcellus)New Albany

Barnett

PierreFayetteville

Woodford/Caney

Floyd/Neal/Conasauga

Lisburne

Eagle Ford & Pearsall

BC Shales

Lewis

Mancos

Colorado Group Utica

Haynesville

Hilliard

Gothic & Cane Creek

17

Delivering commercial insight to the global energy industry

www.woodmac.com

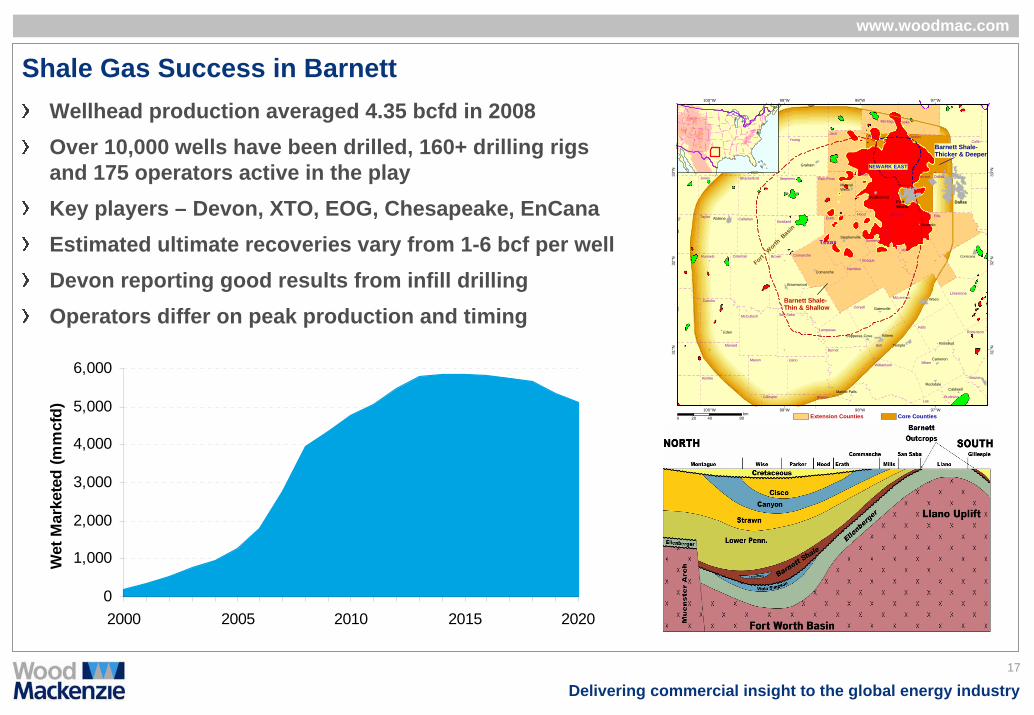

Shale Gas Success in BarnettWellhead production averaged 4.35 bcfd in 2008Over 10,000 wells have been drilled, 160+ drilling rigs and 175 operators active in the play Key players – Devon, XTO, EOG, Chesapeake, EnCanaEstimated ultimate recoveries vary from 1-6 bcf per wellDevon reporting good results from infill drillingOperators differ on peak production and timing

WeatherfordDallas

Corsicana

MineralWells

Alvarado

FortWorth

Abilene

Temple

Rockdale

Copperas Cove

Marble Falls

Killeen

Waco

Gatesville

Eden

Brownwood

Comanche

Graham

Stephenville

T

Rosebud

Cameron

Caldwell

Throckmorton

Collin

Dallas

Cooke

Jack

Tarrant

Montague

Wise

Ellis

Denton

Johnson

Palo Pinto

Somervell

Parker

McLennan

Erath

Bosque

Hood

Hill

Coryell

RobertsonFalls

Limestone

Hamilton

Brazos

LeeBurlesonBlancoGillespie

Kimble

Jones Shackelford

Runnels

TaylorEastland

Coleman

Callahan

ComancheBrown

MillsConcho

McCulloch

Menard

Mason

Burnet

Llano

San Saba

Stephens

Lampasas

MilamWilliamson

Bell

Youngnewall Haskell Throckmorton

Fort W

orth B

asin

Texas

NEWARK EAST

Barnett Shale-Thicker & Deeper

Barnett Shale-Thin & Shallow

100°W

100°W

99°W

99°W

98°W

98°W

97°W

97°W

31°N

31°N

32°N

32°N

33°N

33°N

0 40 8020km

!

! !

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!!

!!

!

!

!

!

!! !

!

!

!

!

!

!

!

!

!

!

!

!

!

!!

!!

!

!

!

!

!

!

!

!

!

!

!

!!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

!

! !

!

!

!

!

!

!

!

!

! !

!

!

!!

!

!

!

!!

!

!

!

!

!

!

!

!

!

!

!!

!

!

!!

!

!

!

!

!

! !!

!

!

!

!

!

!

!!

!

!

!!

!

!

!

!

!

!

!

!

!

! !

!

! !

!

!

!

!

!

!

!

!

!

!

!

!!

!

!

!

!

!!

!

Core CountiesExtension Counties

0

1,000

2,000

3,000

4,000

5,000

6,000

2000 2005 2010 2015 2020

Wet

Mar

kete

d (m

mcf

d)

18

Delivering commercial insight to the global energy industry

www.woodmac.com

The Future of the Barnett Shale Play

Tighter spacing: 50-acre to 20-acreRe-fracturing of existing vertical wellsExpansion of drilling success to the West and SouthMajority of expansion in Core area will be in increasingly urban setting

• Isolated, small drilling pads require high performance drilling rigs

• Quiet operations

• Fast (modular, top-drives)

• Small footprint (i.e. fit for purpose)

19

Delivering commercial insight to the global energy industry

www.woodmac.com

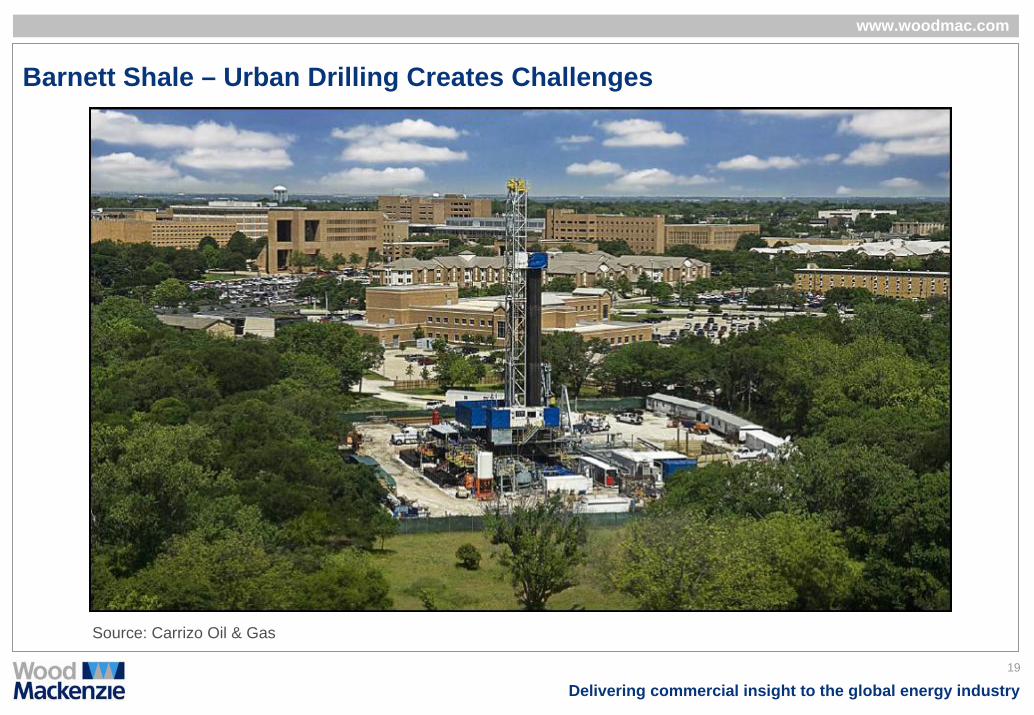

Barnett Shale – Urban Drilling Creates Challenges

Source: Carrizo Oil & Gas

20

Delivering commercial insight to the global energy industry

www.woodmac.com

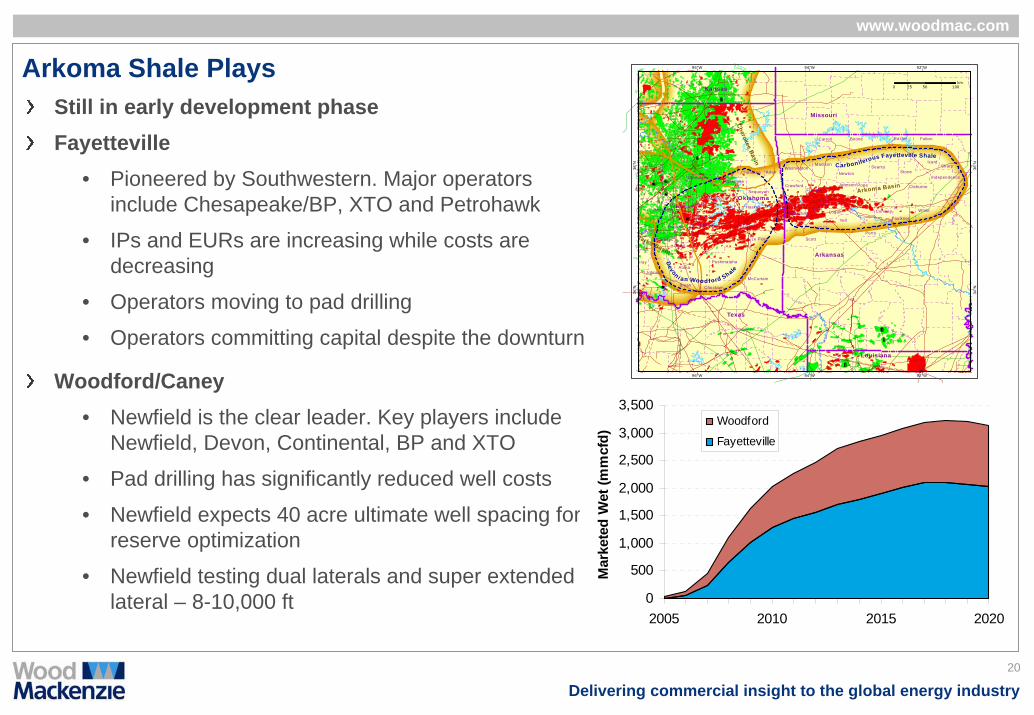

Arkoma Shale PlaysStill in early development phaseFayetteville

• Pioneered by Southwestern. Major operators include Chesapeake/BP, XTO and Petrohawk

• IPs and EURs are increasing while costs are decreasing

• Operators moving to pad drilling

• Operators committing capital despite the downturn

Woodford/Caney• Newfield is the clear leader. Key players include

Newfield, Devon, Continental, BP and XTO

• Pad drilling has significantly reduced well costs

• Newfield expects 40 acre ultimate well spacing for reserve optimization

• Newfield testing dual laterals and super extended lateral – 8-10,000 ft

Arkoma Basin

Cherokee Basin

darko Basin

Texas

Oklahoma

Arkansas

Missouri

Kansas

Carboniferous Fayetteville Shale

Devon i an Wood ford Sh ale

Louisiana

SearcyStone

Independence

SharpIzard

Baxter FultonBooneCarroll

Madison

Newton

Johnson Pope

White

Cleburne

Faulkner

Conway

Yell

Logan

Perry

FranklinCrawford

WashingtonAdairCherokee

Haskell

Sequoyah

Le Flore Scott

Sebastian

PushmatahaAtoka

Johnston

rray

Hughes

McIntosh

MuskogeeOkmulgee

Pittsburg Latimer

OkfuskeeSeminole

CoalPontotoc

Bryan Choctaw

McCurtain

96°W

96°W

94°W

94°W

92°W

92°W

34°N

34°N

36°N

36°N

0 50 10025km

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2005 2010 2015 2020M

arke

ted

Wet

(mm

cfd)

Woodford

Fayetteville

21

Delivering commercial insight to the global energy industry

www.woodmac.com

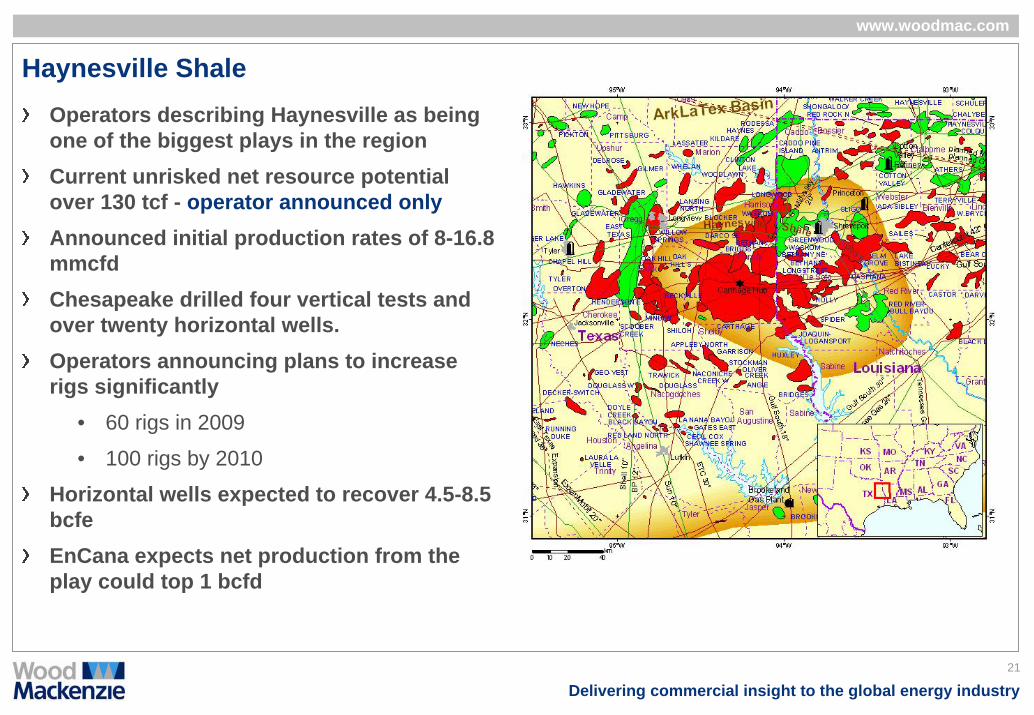

Haynesville ShaleOperators describing Haynesville as being one of the biggest plays in the region Current unrisked net resource potential over 130 tcf - operator announced onlyAnnounced initial production rates of 8-16.8 mmcfdChesapeake drilled four vertical tests and over twenty horizontal wells. Operators announcing plans to increase rigs significantly

• 60 rigs in 2009

• 100 rigs by 2010

Horizontal wells expected to recover 4.5-8.5 bcfeEnCana expects net production from the play could top 1 bcfd

22

Delivering commercial insight to the global energy industry

www.woodmac.com

How the Heck Did Aubrey Come up with 250 tcf Anyway?

180 bcf/section in Core and Tier 1 areas of Haynesville8 wells per section expected – 80 acre spacing.

• Note in Barnett it is 40 acres in some areas

Wells estimated to recover up to 52 bcf/section. Recovery of ~ 29% of OGIP. • In Barnett, operators are talking of higher recovery %. However, with more wells per

section

3 million acres or 4,700 sections in the core areas

4,700 sections x 52 bcf/section = 245 tcf of recoverable gas

23

Delivering commercial insight to the global energy industry

www.woodmac.com

Haynesville Shale

Areal extent – Sweet spots still to be determined. Deeper to the South and East and thins to the north. Thins to the West and transitions into a deep Bossier sand/shale playOperators drilling vertical/horizontal wells to delineate/hold acreage. Full-field development not yet commencedWells still in science phase. First micro-seismic fracture mappings being completedkey variables that make Haynesville successful

• Shale is thick (150-300’)

• Overpressured (increases recovery rates, gas-in-place, and the odds of natural fracturing)

• Quartz rich and low expandable clay content – important for successful fracture stimulations

24

Delivering commercial insight to the global energy industry

www.woodmac.com

Haynesville Shale – Advantages

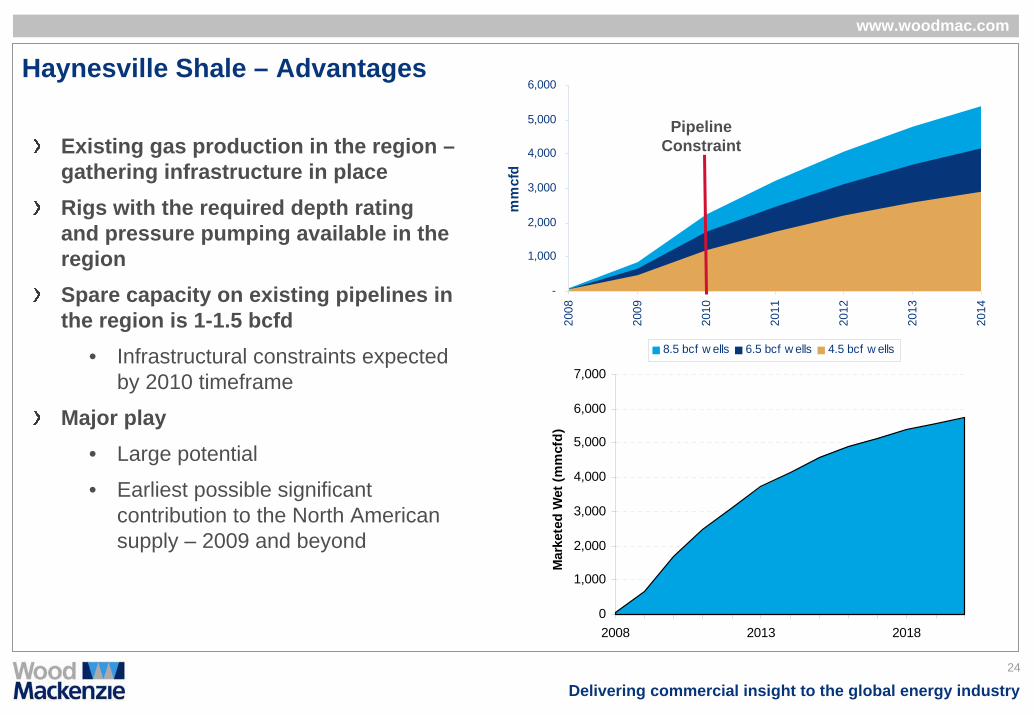

Existing gas production in the region –gathering infrastructure in placeRigs with the required depth rating and pressure pumping available in the regionSpare capacity on existing pipelines in the region is 1-1.5 bcfd

• Infrastructural constraints expected by 2010 timeframe

Major play• Large potential

• Earliest possible significant contribution to the North American supply – 2009 and beyond

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2008 2013 2018

Mar

kete

d W

et (m

mcf

d)

-

1,000

2,000

3,000

4,000

5,000

6,000

2008

2009

2010

2011

2012

2013

2014

mm

cfd

8.5 bcf w ells 6.5 bcf w ells 4.5 bcf w ells

Pipeline Constraint

25

Delivering commercial insight to the global energy industry

www.woodmac.com

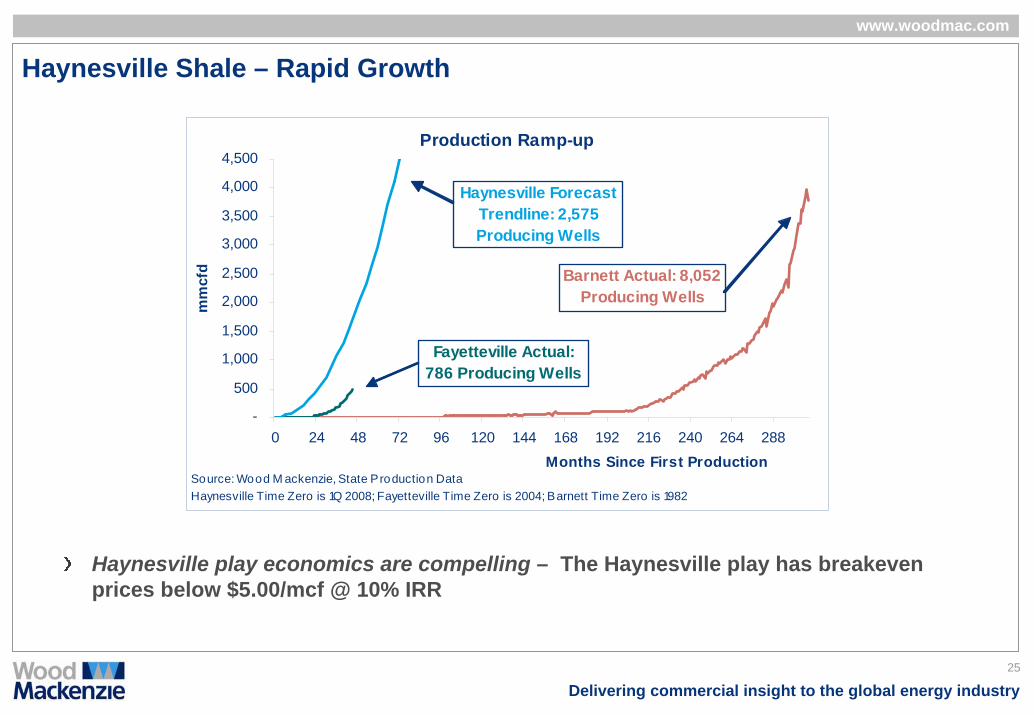

Haynesville Shale – Rapid Growth

Production Ramp-up

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

0 24 48 72 96 120 144 168 192 216 240 264 288

Months Since First Production

mm

cfd

Source: Wood M ackenzie, State Production DataHaynesville Time Zero is 1Q 2008; Fayetteville Time Zero is 2004; Barnett Time Zero is 1982

Barnett Actual: 8,052 Producing Wells

Haynesville Forecast Trendline: 2,575 Producing Wells

Fayetteville Actual: 786 Producing Wells

Haynesville play economics are compelling – The Haynesville play has breakeven prices below $5.00/mcf @ 10% IRR

26

Delivering commercial insight to the global energy industry

www.woodmac.com

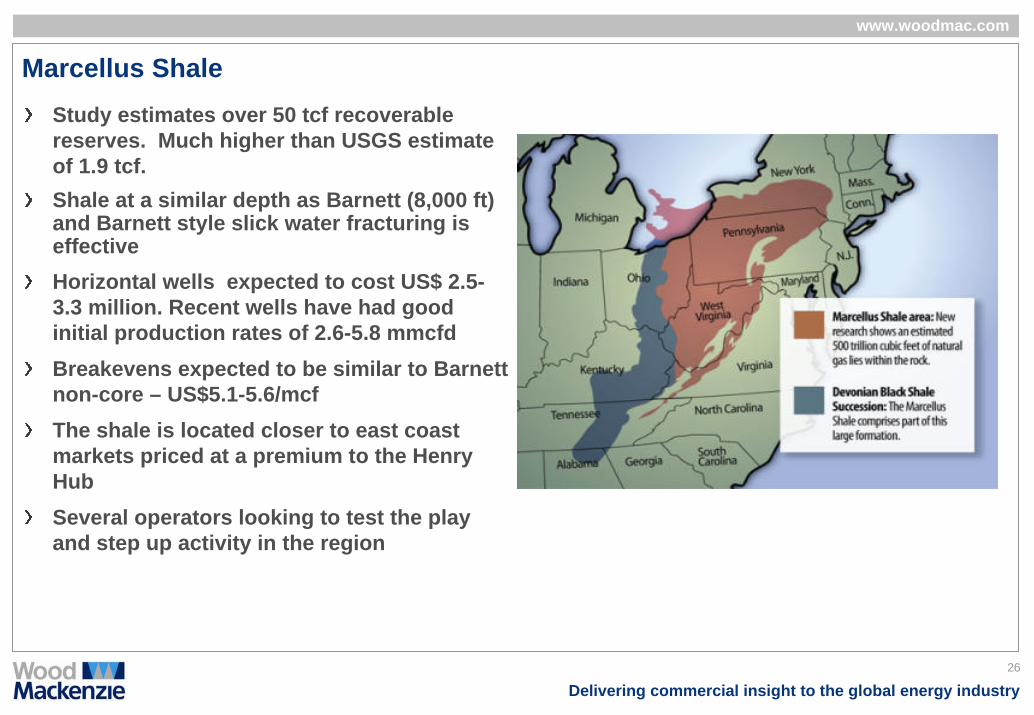

Marcellus ShaleStudy estimates over 50 tcf recoverable reserves. Much higher than USGS estimate of 1.9 tcf.Shale at a similar depth as Barnett (8,000 ft) and Barnett style slick water fracturing is effectiveHorizontal wells expected to cost US$ 2.5-3.3 million. Recent wells have had good initial production rates of 2.6-5.8 mmcfdBreakevens expected to be similar to Barnett non-core – US$5.1-5.6/mcfThe shale is located closer to east coast markets priced at a premium to the Henry HubSeveral operators looking to test the play and step up activity in the region

27

Delivering commercial insight to the global energy industry

www.woodmac.com

Marcellus Shale

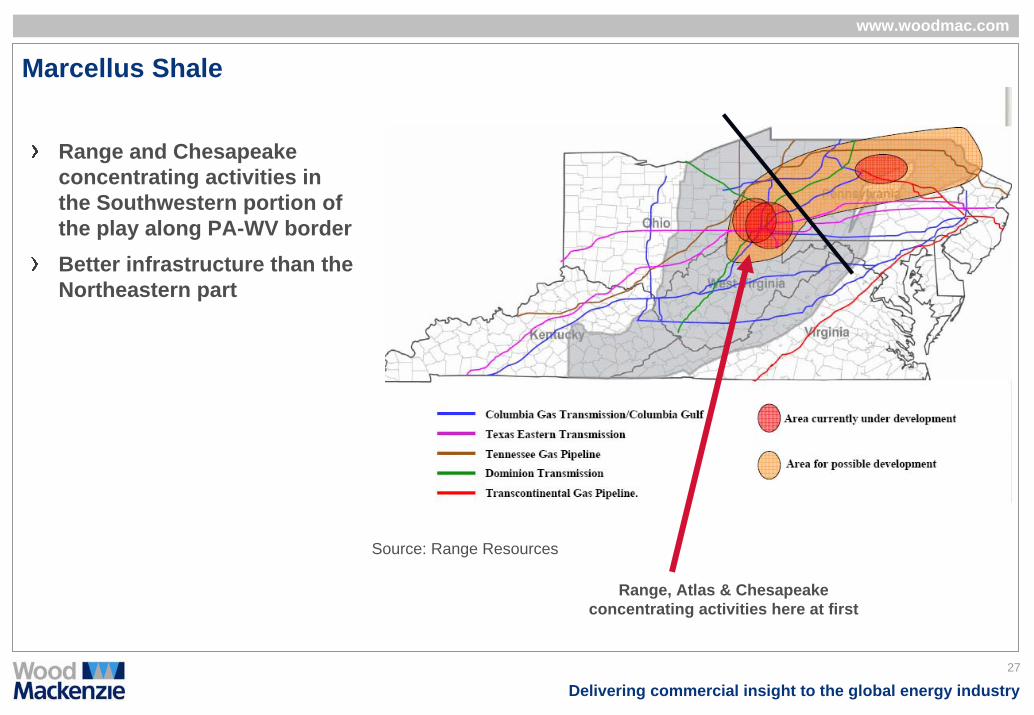

Source: Range Resources

Range and Chesapeake concentrating activities in the Southwestern portion of the play along PA-WV borderBetter infrastructure than the Northeastern part

Range, Atlas & Chesapeake concentrating activities here at first

28

Delivering commercial insight to the global energy industry

www.woodmac.com

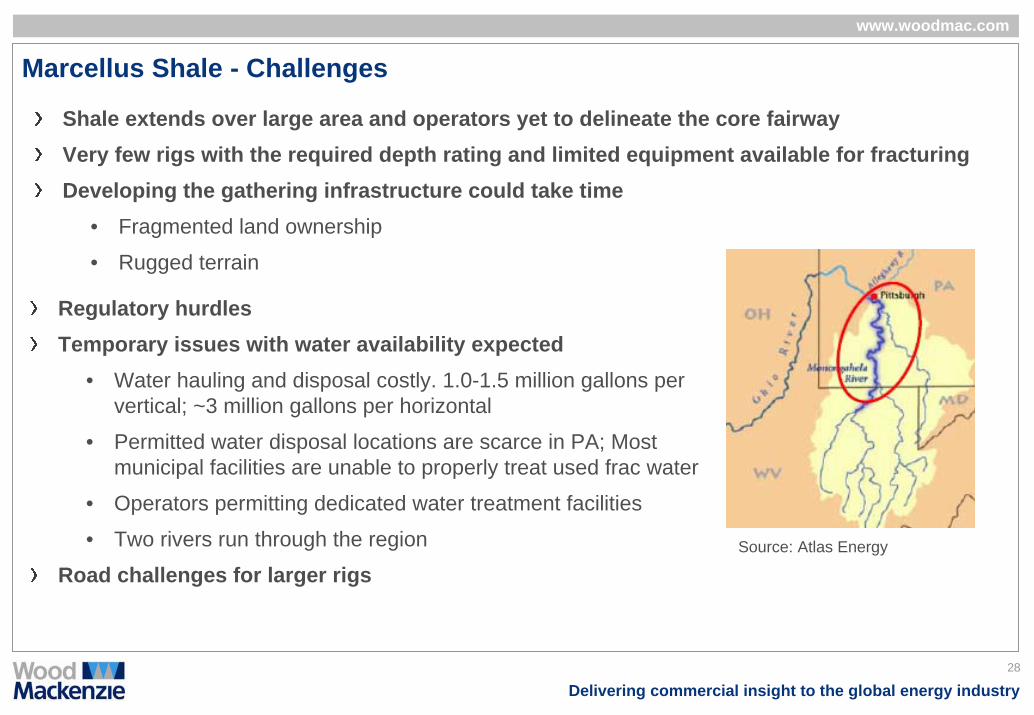

Marcellus Shale - Challenges

Shale extends over large area and operators yet to delineate the core fairwayVery few rigs with the required depth rating and limited equipment available for fracturingDeveloping the gathering infrastructure could take time

• Fragmented land ownership

• Rugged terrain

Regulatory hurdlesTemporary issues with water availability expected

• Water hauling and disposal costly. 1.0-1.5 million gallons per vertical; ~3 million gallons per horizontal

• Permitted water disposal locations are scarce in PA; Most municipal facilities are unable to properly treat used frac water

• Operators permitting dedicated water treatment facilities

• Two rivers run through the region

Road challenges for larger rigsSource: Atlas Energy

29

Delivering commercial insight to the global energy industry

www.woodmac.com

Barnett vs. Marcellus

Source: Range Resources

30

Delivering commercial insight to the global energy industry

www.woodmac.com

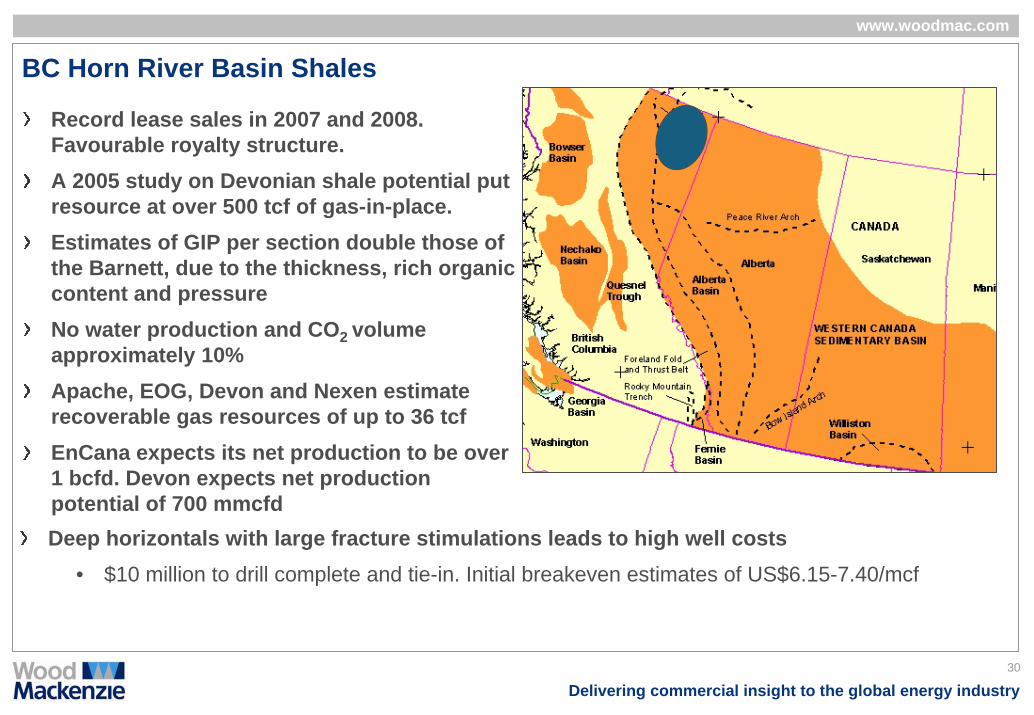

BC Horn River Basin Shales

Record lease sales in 2007 and 2008. Favourable royalty structure. A 2005 study on Devonian shale potential put resource at over 500 tcf of gas-in-place.Estimates of GIP per section double those of the Barnett, due to the thickness, rich organic content and pressureNo water production and CO2 volume approximately 10%Apache, EOG, Devon and Nexen estimate recoverable gas resources of up to 36 tcf EnCana expects its net production to be over 1 bcfd. Devon expects net production potential of 700 mmcfdDeep horizontals with large fracture stimulations leads to high well costs

• $10 million to drill complete and tie-in. Initial breakeven estimates of US$6.15-7.40/mcf

31

Delivering commercial insight to the global energy industry

www.woodmac.com

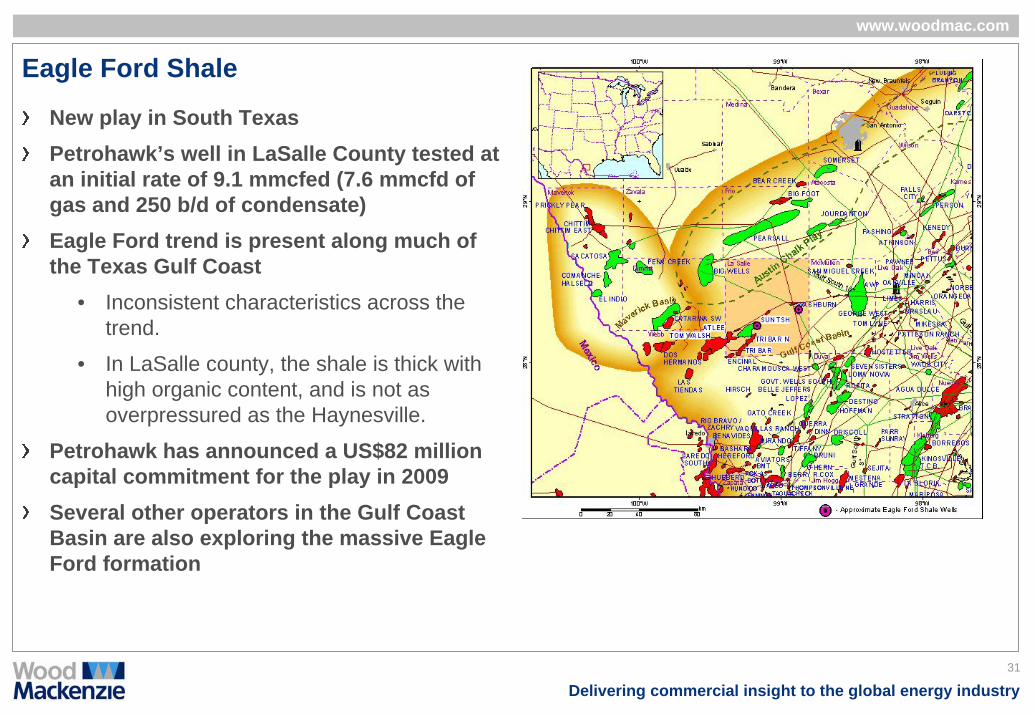

Eagle Ford Shale

New play in South Texas Petrohawk’s well in LaSalle County tested at an initial rate of 9.1 mmcfed (7.6 mmcfd of gas and 250 b/d of condensate)Eagle Ford trend is present along much of the Texas Gulf Coast

• Inconsistent characteristics across the trend.

• In LaSalle county, the shale is thick with high organic content, and is not as overpressured as the Haynesville.

Petrohawk has announced a US$82 million capital commitment for the play in 2009Several other operators in the Gulf Coast Basin are also exploring the massive Eagle Ford formation

32

Delivering commercial insight to the global energy industry

www.woodmac.com

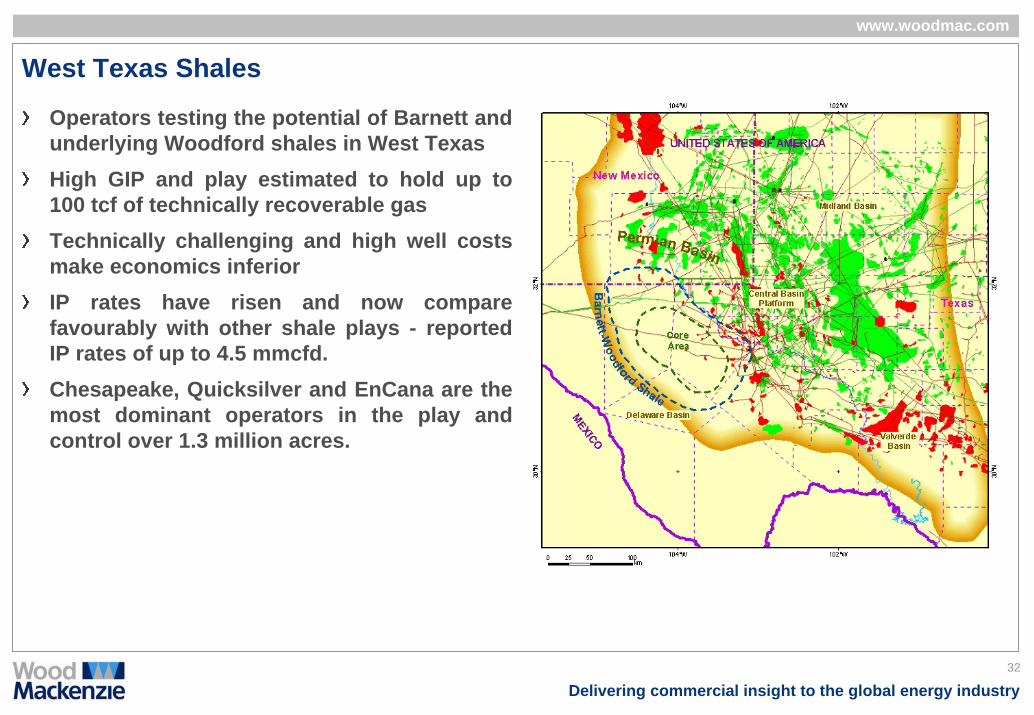

West Texas Shales

Operators testing the potential of Barnett and underlying Woodford shales in West TexasHigh GIP and play estimated to hold up to 100 tcf of technically recoverable gasTechnically challenging and high well costs make economics inferiorIP rates have risen and now compare favourably with other shale plays - reported IP rates of up to 4.5 mmcfd. Chesapeake, Quicksilver and EnCana are the most dominant operators in the play and control over 1.3 million acres.

33

Delivering commercial insight to the global energy industry

www.woodmac.com

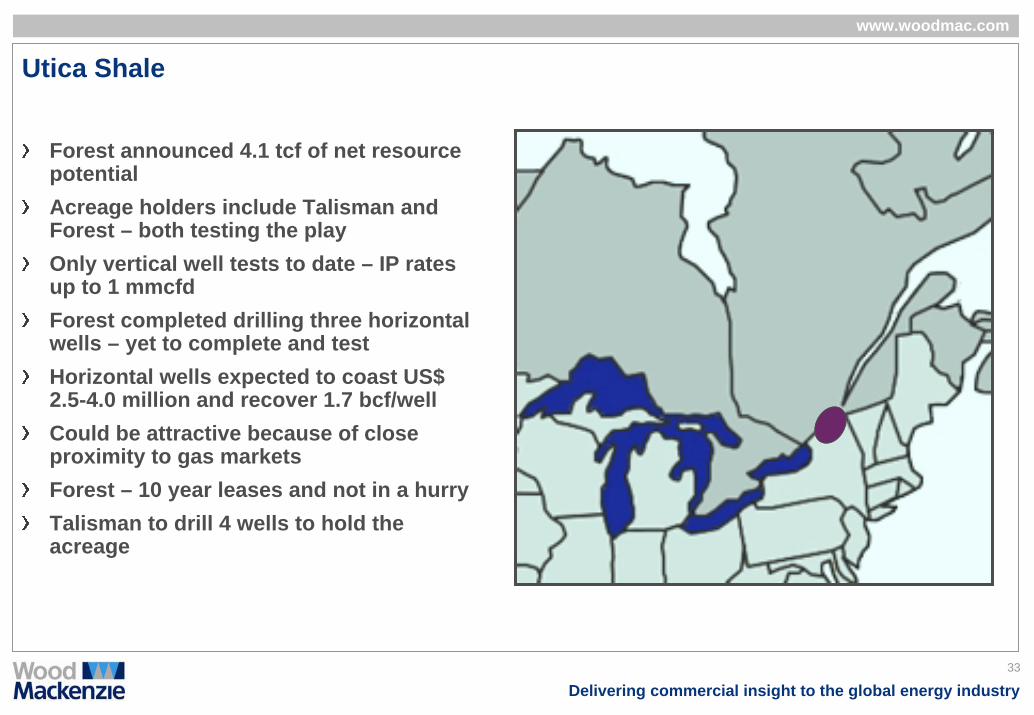

Utica Shale

Forest announced 4.1 tcf of net resource potential Acreage holders include Talisman and Forest – both testing the playOnly vertical well tests to date – IP rates up to 1 mmcfd Forest completed drilling three horizontal wells – yet to complete and testHorizontal wells expected to coast US$ 2.5-4.0 million and recover 1.7 bcf/wellCould be attractive because of close proximity to gas marketsForest – 10 year leases and not in a hurryTalisman to drill 4 wells to hold the acreage

34

Delivering commercial insight to the global energy industry

www.woodmac.com

Developing an Unconventional Shale Play

Identify and map target play – size of the pieAcquire acreageEvaluate technical characteristics and determine commercialityDelineate core fairwayDevelopment

• Develop best practices for drilling & completions

• Pilot test the optimum well spacing

• Full scale development

www.woodmac.com

Delivering commercial insight to the global energy industry

Tight Gas and CBM

36

Delivering commercial insight to the global energy industry

www.woodmac.com

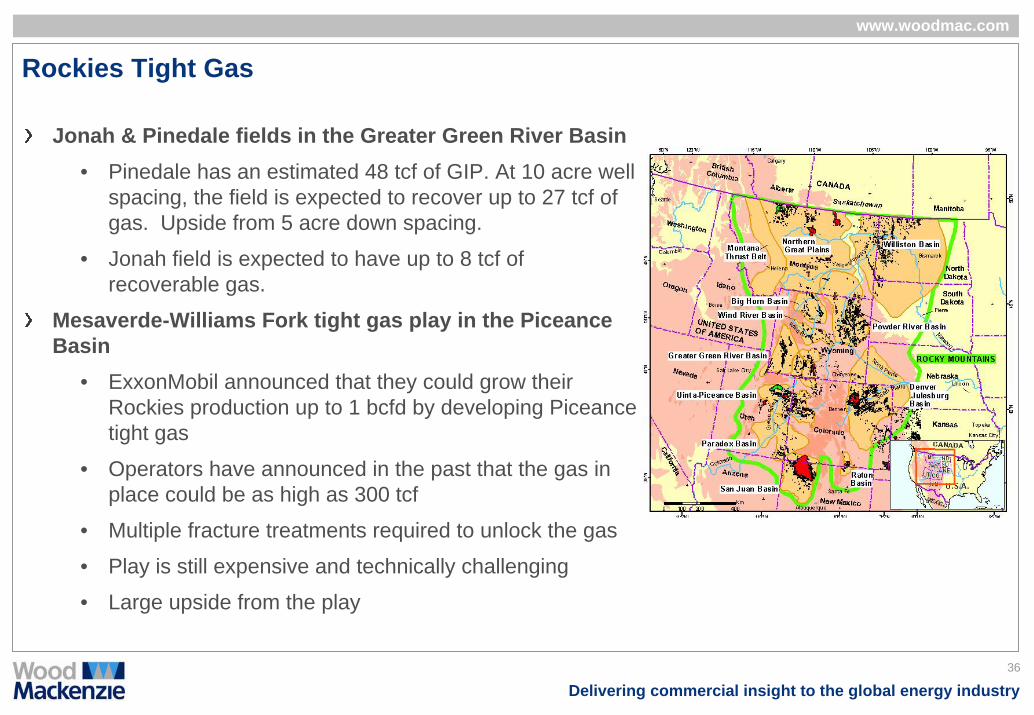

Rockies Tight Gas

Jonah & Pinedale fields in the Greater Green River Basin • Pinedale has an estimated 48 tcf of GIP. At 10 acre well

spacing, the field is expected to recover up to 27 tcf of gas. Upside from 5 acre down spacing.

• Jonah field is expected to have up to 8 tcf of recoverable gas.

Mesaverde-Williams Fork tight gas play in the Piceance Basin

• ExxonMobil announced that they could grow their Rockies production up to 1 bcfd by developing Piceance tight gas

• Operators have announced in the past that the gas in place could be as high as 300 tcf

• Multiple fracture treatments required to unlock the gas

• Play is still expensive and technically challenging

• Large upside from the play

37

Delivering commercial insight to the global energy industry

www.woodmac.com

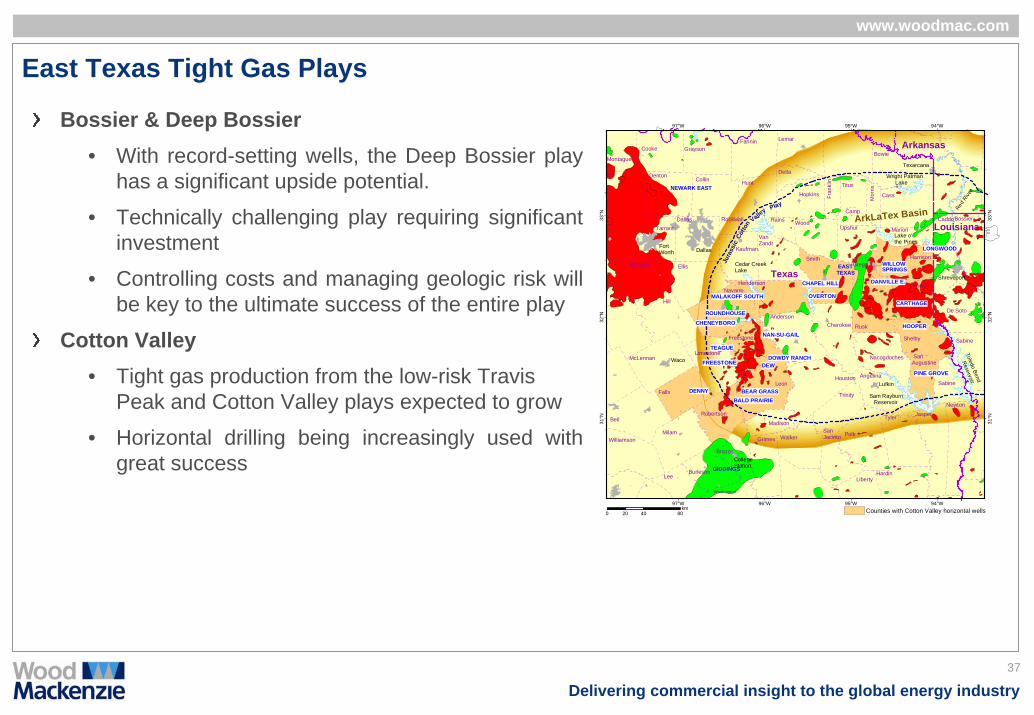

East Texas Tight Gas Plays

Bossier & Deep Bossier• With record-setting wells, the Deep Bossier play

has a significant upside potential.

• Technically challenging play requiring significant investment

• Controlling costs and managing geologic risk will be key to the ultimate success of the entire play

Cotton Valley• Tight gas production from the low-risk Travis

Peak and Cotton Valley plays expected to grow

• Horizontal drilling being increasingly used with great success

EASTTEXAS

DOWDY RANCH

BALD PRAIRIE

FREESTONE

BEAR GRASS

CARTHAGE

TEAGUE

LONGWOOD

NAN-SU-GAILHOOPER

PINE GROVE

ROUNDHOUSE

CHENEYBORO

DEW

DENNY

MALAKOFF SOUTH

NEWARK EAST

Texas

Texarcana

Jura

ssic

Cotto

n Valley Play

GIDDINGS

Louisiana

Liberty

Tyler

SanJacinto

Jasper

Hardin

Trinity

Angelina

SanAugustine

Shreveport

Waco

CHAPEL HILL

OVERTON

DANVILLE E.

WILLOWSPRINGS

Newton

Polk

Nacogdoches

Rusk

Gregg

Cherokee

Shelby

Panola

Upshur

Smith

Sabine

Fran

klin

Camp

Titus

Harrison

Cass

Wood

Mor

ris

Fannin

Bowie

Lemar

Delta

Marion

Grayson

Collin

Rockwall Rains

Kaufman

Dallas

VanZandt

Hopkins

Hunt

Cooke

Tarrant

Montague

Wise

Ellis

Denton

Johnson

McLennan

Hill

Robertson

Falls

Navarro

Limestone

Henderson

Anderson

Freestone

Walker

Madison

Houston

Brazos

Grimes

Leon

Washington

LeeBurleson

MilamWilliamson

Bell

CaddoBossier

Sabine

De Soto

ArkLaTex Basin

Arkansas

Lake o'the Pines

Wright Patman Lake

Cedar CreekLake

Toledo Bend

Reservoir

CollegeStation

Lufkin

Sam Rayburn Reservoir

Red R

iver

FortWorth Dallas

97°W

97°W

96°W

96°W

95°W

95°W

94°W

94°W

31°N

31°N

32°N

32°N

33°N

33°N

0 40 8020km Counties with Cotton Valley horizontal wells

38

Delivering commercial insight to the global energy industry

www.woodmac.com

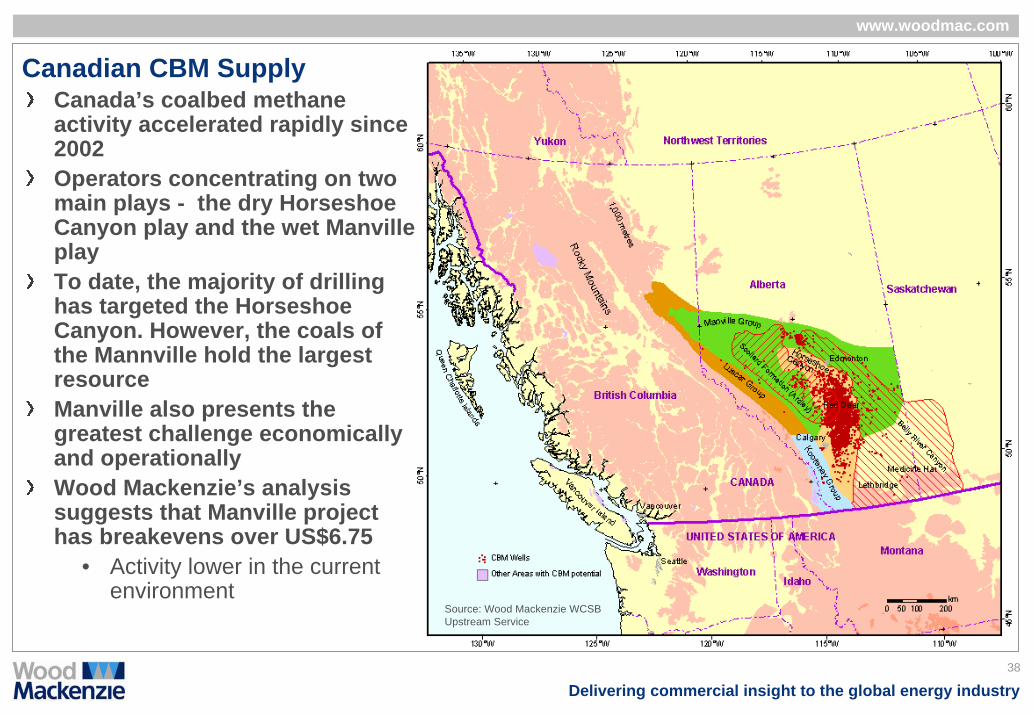

Canadian CBM Supply Canada’s coalbed methane activity accelerated rapidly since 2002Operators concentrating on two main plays - the dry Horseshoe Canyon play and the wet Manville playTo date, the majority of drilling has targeted the Horseshoe Canyon. However, the coals of the Mannville hold the largest resourceManville also presents the greatest challenge economically and operationallyWood Mackenzie’s analysis suggests that Manville project has breakevens over US$6.75

• Activity lower in the current environment

Source: Wood Mackenzie WCSB Upstream Service

www.woodmac.com

Delivering commercial insight to the global energy industry

Shale Gas Reduces LNG Imports & Leads to Unrealized Supply

40

Delivering commercial insight to the global energy industry

www.woodmac.com

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

2003

2005

2007

2009

2011

2013

2015

2017

2019

mm

cfd

Neptune

New England Gatew ay

Manzanillo

Altamira

Energy Bridge

Canaport

Baja

Cameron

Gulf (Pascagoula)

Sabine Cheniere

Golden Pass

Freeport

Elba

Cove

Everett

Lake Charles

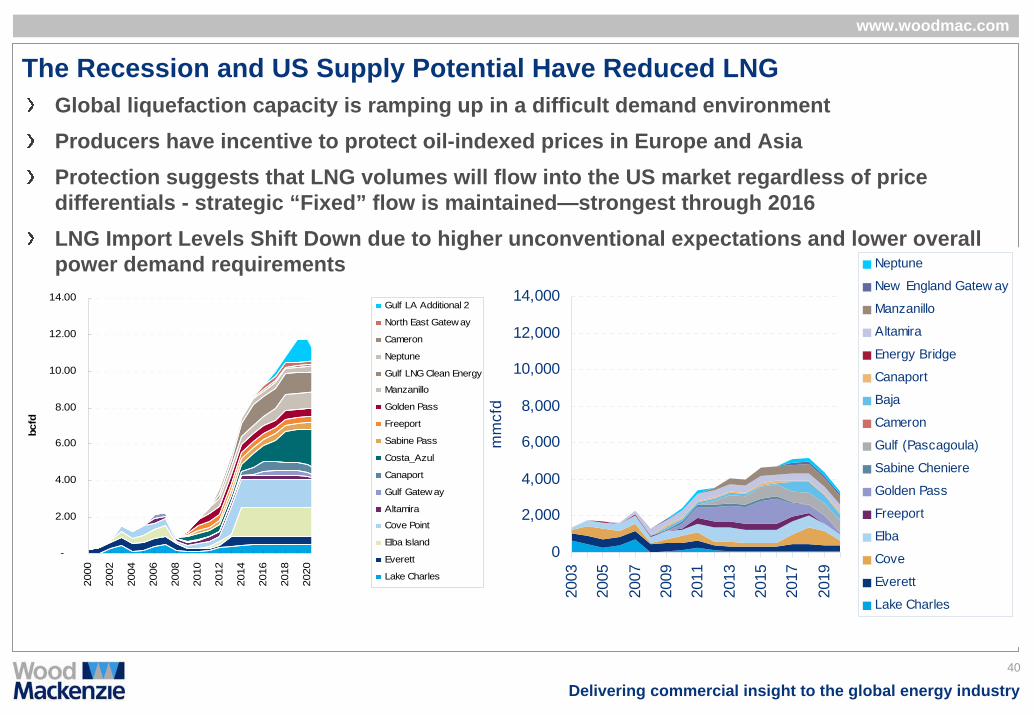

The Recession and US Supply Potential Have Reduced LNGGlobal liquefaction capacity is ramping up in a difficult demand environmentProducers have incentive to protect oil-indexed prices in Europe and AsiaProtection suggests that LNG volumes will flow into the US market regardless of price differentials - strategic “Fixed” flow is maintained—strongest through 2016 LNG Import Levels Shift Down due to higher unconventional expectations and lower overall power demand requirements

-

2.00

4.00

6.00

8.00

10.00

12.00

14.00

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

2020

2022

2024

bcfd

Gulf LA Additional 2

North East Gateway

Cameron

Neptune

Gulf LNG Clean Energy

Manzanillo

Golden Pass

Freeport

Sabine Pass

Costa_Azul

Canaport

Gulf Gateway

Altamira

Cove Point

Elba Island

Everett

Lake Charles

41

Delivering commercial insight to the global energy industry

www.woodmac.com

-

10.0

20.0

30.0

40.0

50.0

60.0

70.0

2008 2010 2012 2014

bcfd

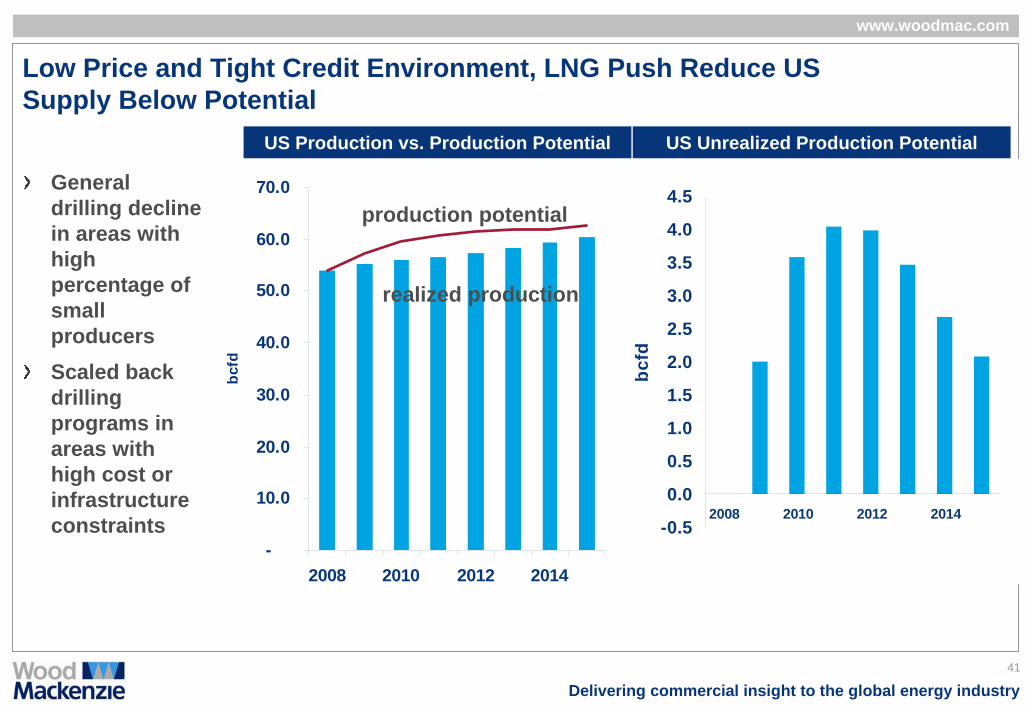

Low Price and Tight Credit Environment, LNG Push Reduce US Supply Below Potential

General drilling decline in areas with high percentage of small producersScaled back drilling programs in areas with high cost or infrastructure constraints

US Production vs. Production Potential US Unrealized Production Potential

production potential

realized production

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

2008 2010 2012 2014

bcfd

42

Delivering commercial insight to the global energy industry

www.woodmac.com

Conclusions

Successful development of the recently announced shales would lead to a paradigm shift in North American supplyThe new shales benefit from technological and operational breakthroughs in existing successful shale playsSeveral other plays being tested across the country

• West Texas shales, Baxter, Hilliard, Gothic, Pierre, Niobrara, Chattanooga …..

Development of these shales ultimately depends on access to capital, operator commitment, technological improvements and commodity prices