nonprofit financial

TRANSCRIPT

Nonprofit and Human Resources Update Tuesday, September 25th, 2018

Nonprofit Financial and Human Resources Update

Tuesday, September 25th, 2018

Conference i/o

aemcpas.cnf.io

CPE

aemcpas.cnf.io

• 3.5 hours of CPE credit is being offered for this seminar

• Remember to sign out at the end of the day

• Certification will be emailed within 2 weeks after this seminar

Agenda

8:00am – 8:30am Registration and Breakfast

8:30am Introductions

8:30am – 9:00am How to Thrive & Survive Under the New Tax Law Changes

9:00am – 9:45am Understanding the New Rules Around Contributions and Exchange Transactions

9:45am – 10:00am Break

10:00am – 11:00am New Liquidity Footnote Workshop

11:00am – 11:45 am Employee, Independent Contractors, and Volunteers: Making the Right Classification, Avoiding Common Missteps, and Implementing Best Practices

11:45am – 12:00am Q & A

12:00pm – 1:00pm Lunch & Networking

aemcpas.cnf.io

Steven Anseth

Partner, CPA Nonprofit Leader

20+ Years in Accounting Industry20+ Years Nonprofit Experience

Nonprofit and Human Resources Update Tuesday, September 25th, 2018

How to Thrive and Survive Under the New Tax Law Changes

Steven Anseth

Main Change Impacting Nonprofits

aemcpas.cnf.io

•Double standard deduction and eliminate personal exemptionso Estimates are that 90-95% of taxpayers will not itemizeo This reduces the amount that have an incentive to giveo Estimate reduced giving in the neighborhood of $10 – 20

billion/year

Main Change Impacting Nonprofits

aemcpas.cnf.io

• Only 30-35% itemized before the tax change

• Minnesota allows taxpayers to deduct charitable contributions even if they do not itemize

• Large donors may benefit from making occasional large contributions rather than annual contributions

How to Respond

aemcpas.cnf.io

• Not seeing a drop in giving at our June 30 clients

• Continue to focus on outcomes

• Appeal to corporations for contributions

How to Respond

aemcpas.cnf.io

• Bunching contributions into one period

• Set up Donor Advise Funds (DAF)o At a community foundationo At your organizationo Risks/rewards

How to Respond

aemcpas.cnf.io

• Minnesota allows taxpayers to deduct charitable contributions even if they do not itemize

• Taxpayers can deduct contributions up to 60% of AGI (up from 50%)

• Itemized deductions no longer phase out at higher levels.

Other Tax Law Impacts

aemcpas.cnf.io

• Some changes to 990-T/Unrelated Business Income Taxo No longer allow grouping of UBIT activitieso Tax at new lower corporate rates

• Certain Parking/Transportation employee benefits are now UBIT

Functional Expense

Statement Disclosure

aemcpas.cnf.io

• All organizations are now required to include a statement of functional expenses in their financials

• Needs to include:o Which specific expenses are allocatedo The method used to determine the allocation

Questions? Submit your questions to

aemcpas.cnf.io

Derek Halvorson Senior Manager, CPA

12 Years in Accounting Industry12 Years Nonprofit Experience

Nonprofit and Human Resources Update Tuesday, September 25th, 2018

Understanding the New Rules Around Contributions and Exchange Transactions

FASB ASU 2018-08

Derek Halvorson

Why the Update?

aemcpas.cnf.io

• Diversity in applying GAAPo The same grant would be considered an exchange transaction

by one and a contribution by another

• Distinguish which guidance to applyo Exchange – Topic 606 Revenue from Contracts with Customerso Contributions – Topic 958 Not-for-Profit Entities

• Difficulty in determining when a contribution is conditional

Effective Dates

aemcpas.cnf.io

•Contributions received guidanceo Annual periods beginning after

December 15, 2018o If conduit debt or publicly-traded: annual

periods beginning after June 15, 2018

•Contributions made guidanceo Annual periods beginning after December 15, 2019o If conduit debt or publicly-traded: annual periods beginning after

December 15, 2018

•Revenue from contracts with customerso Annual periods beginning after December 15, 2018o If conduit debt or publicly-traded: annual periods beginning after

December 15, 2017

Transition Guidance-

Contributions

aemcpas.cnf.io

•Early adoption is permitted

•No restatement of prior periods

•No cumulative-effect adjustment to the opening balance of net assets

•Apply only to the portion that has not been recognized before the effective date to the following agreements:

o Not completed as of the effective dateo Entered into after the effective date

•Required disclosures – year of changeo Nature of and reason for the accounting changeo Reason for significant change for each financial

statement line item

Transition Guidance-Exchange

aemcpas.cnf.io

• Full retrospective applicationo January 1, 2019 apply the revenue recognition standard to all contractso 2017 and 2018 restate all contractso Date of cumulative adjustment: January 1, 2017o FASB has issued optional practical expedients that can be elected

• Modified retrospective applicationo January 1, 2019 apply the revenue recognition standard to all contracts o 2017 and 2018 no contracts restated, continue to report on legacy

accountingo Date of cumulative adjustment: January 1, 2019o Disclose the impact of the application for each financial statement line

item

Transition approaches

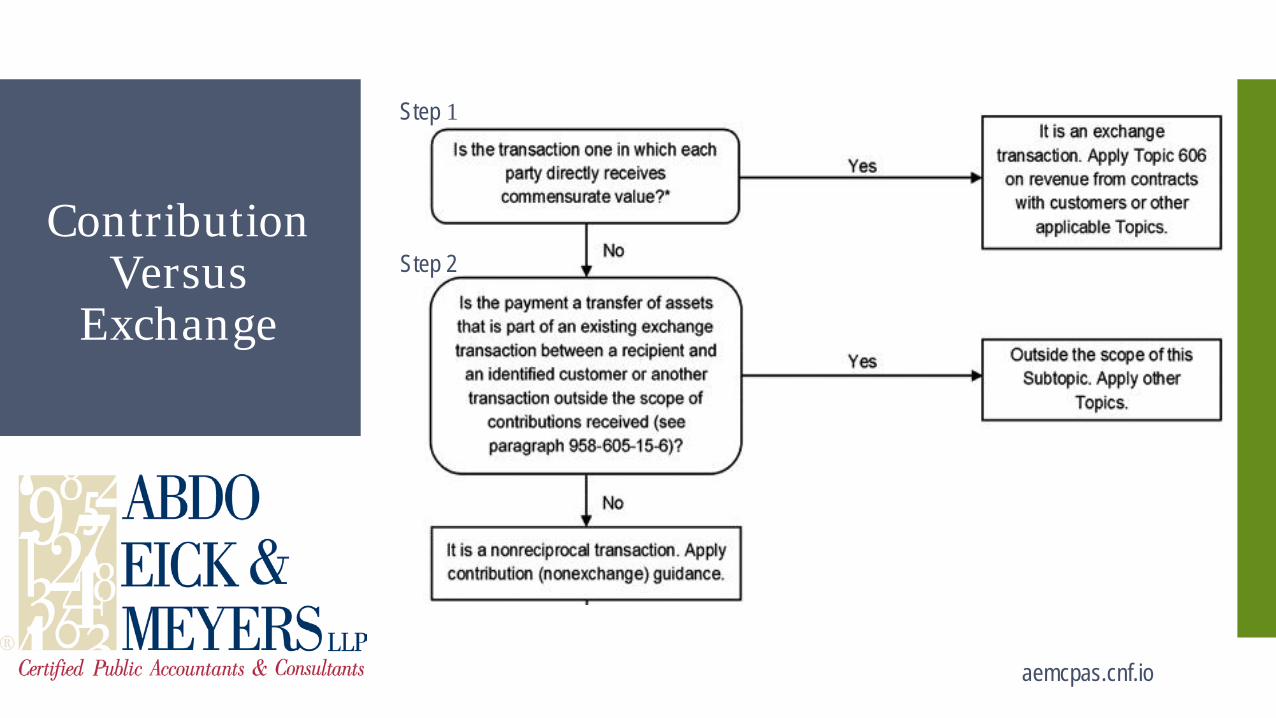

Contribution Versus

Exchange

aemcpas.cnf.io

Step 1

Step 2

Step 1

aemcpas.cnf.io

Is the Transaction One in which Each Party Directly Receives Commensurate Value?

•Factors that do not result in commensurate value:o A general public benefit, even if resource provider receives

indirect value incidental to the public benefit (i.e. government grants)

o Execution of resource provider’s mission or positive sentiment

o Resource provider has full discretion in determining the amount

o Failure to comply with agreement results in return of unspent amount

•If yes, exchange transaction and follow Topic 606 guidanceo Reciprocal transfers in which each party receives and

sacrifices approximately commensurate value

•If no, continue to Step 2

Step 1Example 1

Research Grant

aemcpas.cnf.io

•Facts:o NFP A is a large research university with a cancer

research centero NFP A regularly conducts cancer research and

receives supporto NFP A receives funding from a pharmaceutical entity

(PE) to finance a clinical trial of an experimental cancer drug the PE developed

o The PE specifies the protocol of the testing and requires a detailed report of the test outcome at the conclusion

o The PE receives the proprietary rights to the research

•Exchange or Contribution?o Exchange: The clinical trial has commercial value to

the PE, resulting in a commensurate value for the PE

Step 1Example 2Building Purchase

aemcpas.cnf.io

•Facts:o Donor sells a building to a not-for-profit for $100,000

and the fair market value is $500,000o No unstated rights or privileges are involved

•Exchange or Contribution?o Both: There would be a contribution of $400,000 and

the $100,000 paid would be considered an exchange

Step 2

aemcpas.cnf.io

•If yes, outside the scope of this Subtopic. Apply other Topics.

•If no, it is a nonreciprocal transaction. Apply contribution guidance.

Is the payment a transfer of assets that is part of an existing exchange transaction between a recipient and an

identified customer or another transaction outside the scope of contributions received?

Step 2 Example 3 Grant for Tuition

aemcpas.cnf.io

• Facts:o Student L is enrolled in University Ao Total tuition for the semester is $30,000o Student L receives a $2,000 grant to use

toward tuitiono The grant is paid directly to University A

• Exchange or Contribution?o Exchange for University A: The grant was awarded to Student L, not to

University A University A entered into an exchange

transaction with Student L The grant represents partial payment against the

$30,000 due Student L is an identified customer receiving the

benefit from the grant

Step 2 Example 4 Medicare Payment

aemcpas.cnf.io

•Facts:o Patient R is a patient at Hospital Bo Total amount due for services is $10,000o Patient R has Medicare and covers $8,000 of the

services paid directly to the hospitalo Hospital B bills Patient R for $2,000

•Exchange or Contribution?o Exchange for Hospital B: Hospital B has a contract with Patient R in the

amount of $10,000 The Medicare payment of $8,000 and patient

payment of $2,000 serve as a payment source for the services rendered

When to Recognize a Contribution

aemcpas.cnf.io

Step 3

Step 3

aemcpas.cnf.io

•Donor-imposed condition must have both:o One or more barriers that must be overcome before the

recipient is entitled to the assets transferred or promised.

o Failure to overcome the barrier results in a right of return of the asset or a right of release from its obligation.

•If yes, it is conditional. Recognize revenue when the condition or conditions are met.

•If no or once conditions are met, it is unconditional. Recognize revenue in appropriate net asset class in Step 4

Is there a donor-imposed condition or conditions present (a barrier and a right of return/right of release must exist)?

Step 3 Barriers

aemcpas.cnf.io

•Barriero Evaluate the facts and circumstances of the agreemento A barrier often places specific requirements about the

use of the transferred assetso A probability assessment regarding the likelihood of

meeting the stipulations is not a factoro Ambiguous donor stipulations are presumed to be a

conditional contribution

Step 3 Indicators of a

Barrier

aemcpas.cnf.io

•Measurable performance-related barrier or other measurable barrier

o Specified level of serve: grant requires the entity to provide 1,000 meals per week

o Specific output or outcome: students must achieve a minimum test score

o Matching: donor specifies an entity must raise $100,000 of matching funds

o Outside event: a foundation promises to contribute 5% of investment income if the foundation’s net assets reaches $5,000,000

Step 3 Indicators of a

Barrier (Continued)

aemcpas.cnf.io

•Limited discretion by the Recipient on the conduct of an activity

o More specific than a donor-imposed restriction which may restrict to an activity, but not on how the activity is performed

o For example, an agreement specifies the recipient should incur qualifying expenses in accordance with Uniform Guidance

Step 3 Indicators of a

Barrier (Continued)

aemcpas.cnf.io

•Stipulations that are related to the purpose of the agreemento If a stipulation is unrelated to the purpose of the

agreement such as trivial or administrative stipulations, it would not indicate a barrier

o If administrative tasks required, more likely there are other requirements that would be more indicative of a barrier

o Generally providing a report to a resource provider is to provide information the transferred assets were used in accordance with the agreement, rather than impact the extent to which the recipient is entitled to the contribution

Step 3 Example 5

Contribution by Foundation

aemcpas.cnf.io

•Facts:o Foundation A gives NFP D a grant in the amount of

$400,000 to provide career training to veteranso The grant requires NFP D to provide training to at least

8,000 veterans per year and at least 2,000 per quartero Foundation A specifies a right of release and will pay

$100,000 each quarter if at least 2,000 veterans receive career training during that period

•Conclusion:o Conditional: contains a right of release and a

measurable performance-related barrier of 2,000 veterans per quarter

Step 3 Example 6

Contribution Includes

Qualifying Expenses

aemcpas.cnf.io

•Facts:o NFP B is a hospital that has a research programo NFP B receives a $300,000 Federal grant for cancer researcho NFP B must incur expenses in compliance with Uniform Guidanceo Cost-reimbursement grant initiated by NFP Bo Any unused assets are forfeited and unallowable cost refunded

•Conclusion:o Conditional:

Barrier to entitlement as a result of qualifying expenses under Uniform Guidance limits NFP B’s discretion about how to use the assets

Release of obligation for unused and refund unallowable costs

Recognize revenue in the period qualifying expenses are incurred

Step 3Example 7

Capital Campaign

aemcpas.cnf.io

•Facts:o NFP G is conducting a capital campaign to build new

dormso NFP G receives a $10,000 upfront grant from a

foundationo The agreement contains a right of return if not used for

the new dormso The foundation doesn’t include any specifications on

construction or how other improvements should be made

•Conclusion:o Unconditional:

The agreement places limits only on the specific activity being funded, but not on construction or other stipulations

Would be considered a donor-restricted grant

Step 3Example 8

Contributions to a Homeless

Shelter

aemcpas.cnf.io

•Facts:o NFP J operates a homeless sheltero NFP J receives an upfront grant of $75,000 from the

city for its meal programo Grant requires to provide at least 5,000 meals to the

homelesso Contains a right of return for meals not served

•Conclusion:o Conditional:

Agreement contains a measurable performance-related barrier of 5,000 meals and right of return

In advance of providing the meals, record a refundable advance liability of $75,000

Step 3Example 9

Contributions to a Recreational Organization

aemcpas.cnf.io

•Facts:o NFP H is a recreational organization that provides

various sports programs to childreno NFP H receives an upfront grant of $40,000 for it tennis

programo The agreement includes specific guidelines on how

they could use the assets (i.e. hire 10 tennis instructors, provide 9 weeks of camp)

o Grant contains a right of return for funds not spent

•Conclusion:o Unconditional:

Agreement contains guidelines on how they could spend the funds, but the agreement doesn’t make the funds dependent on meeting those guidelines

Step 4

aemcpas.cnf.io

Are restrictions present (that is, limited purpose or timing)?

•Donor-imposed restriction:o Donor stipulation that specifies a use for a contributed

asset that is more specific than broad limits resulting from the following:

The nature of the NFP The environment in which it operates The purposes specified in its organizing

documentso Donor stipulation that resources are to be used after a

specified date or to be maintained in perpetuity

•If yes, it is unconditional with donor restrictions

•If no, it is unconditional and without donor restrictions

Step 4 Simultaneous

Release Option

aemcpas.cnf.io

•Contributions whose restrictions are met in the same reporting period as the revenue is recognized as support within net asset without donor restrictions

o NFP needs to have a similar policy for reporting investment gains and income

o Report consistently from period to periodo Disclose as an accounting policy

•An NFP may elect the simultaneous release option for donor-restricted contributions that were initially conditional contributions without making the election for other donor restricted contributions or investment gains and income

Contributions Made

aemcpas.cnf.io

Topic 606 Revenue from Contracts with

Customers

aemcpas.cnf.io

•Core Principle: o Recognize revenue to depict the transfer of promised

goods or services to customers in an amount that reflects the consideration to which the entity expects to

be entitled in exchange for those goods or services.

o Steps to apply the core principle: Identify contract(s) with the customer Identify performance obligations Determine transaction price Allocate transaction price

o Recognize revenue when/as performance obligation is satisfied

Topic 606 Nonpublic

Entity Disclosures

aemcpas.cnf.io

•Present or disclose revenue and any impairment losses recognized separately from other sources of revenue

•Provide revenue disaggregated according to the timing of transfer of goods or services (point in time vs. over time)

•Disclose the opening and closing balance of receivables, contract assets and contract liabilities

•Information about performance obligations, including types of goods or services, payment terms, typical timing, etc.

Questions? Submit your questions to

aemcpas.cnf.io

Nonprofit and Human Resources Update Tuesday, September 25th, 2018

New Liquidity Footnote Workshop

Steven Anseth

Liquidity Footnote

aemcpas.cnf.io

•The purpose is to provide the reader of financial statements more transparency and insight on the non-profits liquidity

•Allows the reader to better assess the NFP’s ability to meet commitments, debt service or reach its programmatic goals in the next year

Liquidity Footnote

aemcpas.cnf.io

•Qualitative informationo How entity manages its liquid resources (cash, etc.) –

in the notes

•Quantitative informationo Quantitative information that communicates the

availability of an NFP’s financial assets at the balance sheet date to meet cash needs for general expenditures within one year (on the face and/or in the notes)

Implementation

aemcpas.cnf.io

•Identify all financial assets and any limitations on availability for expenditure in the next 12 months

•Determine the format to present the required quantitative disclosure of liquidity information

•Display gross amounts of financial assets, then adjustments to arrive at available for expenditure amounts, or

•Display only the net amounts available for expenditure

Sample Liquidity Footnote

aemcpas.cnf.io

•Availability is affected by nature of the asset, external limitations imposed by donors (donor restricted), contractual agreements, and board designations

•Develop a formal policy for managing the organization’s liquidity needs

o Will be articulated in the qualitative portion of the note disclosure

Sample Liquidity Footnote

aemcpas.cnf.io

Quantitative

aemcpas.cnf.io

•Step 1 – Determine a Starting Pointo Total Financial Assets

oro List Net Liquid Assets

•Starting with Financial Assets will result in more Items to subtract, but is easier to tie back to the Statement of Financial Position (SFP)

•Starting with Net Liquid Assets will have fewer items that need to be subtracted (subtracted behind the scenes), but may be impossible to tie back to SFP

Quantitative

aemcpas.cnf.io

•Step 2 – Subtract Items that are Unavailable to Meet General Expenditures in the Next Fiscal Year. o No additions, only subtractionso Items to Consider: Donor restrictions, board

designation amounts (generally), restricted cash, investments not intended or not available for general operations, receivables not due for more than 12 months, etc.

Quantitative

aemcpas.cnf.io

•What does this number mean?

•Looking at the number you calculated, is this something you’d want to share with major donors? Other stakeholders?

•Would you prefer a different number? Larger or Smaller? Why or why not?

Small Group Discussion

Sample Liquidity Footnote

aemcpas.cnf.io

Not-for-Profit Entity A is substantially supported by restricted contributions. Because a donor’s restriction requires resources to be used in a particular manner or in a future

period, Not-for-Profit Entity A must maintain sufficient resources to meet those responsibilities to its donors. Thus, financial assets may not be available for general

expenditure within one year.

As part of Not-for-Profit Entity A’s liquidity management, it has a policy to structure its financial assets to be available as its general expenditures, liabilities, and other

obligations come due.

In addition, Not-for-Profit Entity A invests cash in excess of daily requirements in short-term investments. Occasionally, the board designates a portion of any operating

surplus to its liquidity reserve, which was $1,300 as of June 30, 20X1. There is a fund established by the governing board that may be drawn upon in the event of financial distress or an immediate liquidity need resulting from events outside the typical life

cycle of converting financial assets to cash or settling financial liabilities.

In the event of an unanticipated liquidity need, Not-for-Profit Entity A also could draw upon $10,000 of available lines of credit (as further discussed in Note XX) or its quasi-

endowment fund.

Qualitative

aemcpas.cnf.io

•Draft the note disclosure describing how the entity manages its liquid assets and liquidity needs, including conditions under which certain board-designated net assets may be undesignated, access to the lines of credit or other financing sources, and any other information useful in understanding the entity’s liquidity

Qualitative

aemcpas.cnf.io

•Does your organization have a “Liquidity Policy”?

•Need to say something about managing liquid resources for general expenditures.

•To be meaningful, needs to reflect your organization.

Quantitative

aemcpas.cnf.io

•Do you like what you came up with?

•Will you have your organization adopt a liquidity/cash reserve policy?

Small Group Discussion

Questions? Submit your questions to

aemcpas.cnf.io

Leah Davis President, CPA

13 Years in Accounting Industry5 Years Nonprofit Experience

Employees, Independent Contractors and Volunteers: Making the Right Classification, Avoiding Common Missteps, and Implementing Best Practices

Leah Davis

aemcpas.cnf.io

All materials have been prepared for general information purposes only. Information provided is not legal advice, is not to

be acted on as such, may not be current and is subject to change without notice.

Information presented and provided and your receipt or use of it is not intended to convey or constitute legal advice, and is not a

substitute for obtaining legal advice from a qualified attorney. You should not act upon any such information without first

seeking qualified professional counsel on your specific matter.

LegalDisclaimer

Employees

aemcpas.cnf.io

• Wages reported on annual Form W2

• Primary Regulatory Agencies for Employees:o State and Federal Departments of Labor – employment termso IRS – payroll and compensationo OSHA – workplace safety

• Fair Labor Standards Act (FLSA)o Enterprise Coverageo Individual Coverageo information related to non-profit organizations can be found at US

Dept. of Labor website:https://www.dol.gov/whd/regs/compliance/whdfs14a.pdf

Independent Contractors

aemcpas.cnf.io

• Wages reported annually on Form 1099

• Primary Regulatory Agencies for Independent Contractors:o IRS – 1099 paymentso State taxing authorities – 1099 paymentso VERY hot audit priority

• Each worker classification decision is unique:o Behavioral Controlo Financial Controlo Relationship Considerations

• In general, businesses must support an independent contractor classification by demonstrating that they are only able to control the RESULTS of the work, not the WHAT or HOW.

Volunteers

aemcpas.cnf.io

• Volunteers, by nature, are not compensated and do not report wages.o Not regulated but are reviewed by agencies to identify

misclassifications o Cannot volunteer in a for-profit enterprise (i.e. gift shop)

• A volunteer generally will not be considered an employee if the individual volunteers freely for public service, religious or humanitarian objectives, and without contemplation or receipt of compensation.o Part-timeo Different that normal employee work

Volunteers

aemcpas.cnf.io

• Allowed Volunteer Payments

• “Nominal” Paymentso DOL WHD Opinion FLSA2005-51-

https://www.dol.gov/whd/opinion/FLSA/2005/2005_11_10_51_FLSA.htm

o Not tied to productivity or resultso Must be deemed “incidental or insubstantial”

20% Test

• Expense Reimbursementso Qualified Plan

Volunteers

aemcpas.cnf.io

• It is important not to forget that compensation comes in many formso Watch out for taxable fringe benefits like entertainment,

personal use of organizational automobiles, and tangible gifts or “perks”. While not cash, they can often be considered compensation

• Internso If unpaid, interns must meet the volunteer criteriao If paid at or above minimum wage, treat interns like all other

employeeso If paid below minimum wage, organizations should evaluate the

IRS 7-factor test: https://www.dol.gov/whd/regs/compliance/whdfs71.pdf Must establish that the work is primarily for the benefit of

the worker, not the organization

Important Organizational

Actions

aemcpas.cnf.io

• Take stock and review current worker classifications to identify possible misclassifications

• Review and confirm that your organization is properly insured (work comp, liability, etc.) for the types of workers you engage

• Effectively communicate with workers about potential classification changes and requirements

• Don’t forget that worker classification is not a choice made by the worker and/or the organization based on preference. Always default to employee status and, if possible, work your way out.

Q and A