nordic local government funding agencies - kommuninvest · lending margins reduced from q4-2014....

TRANSCRIPT

1

Nordic Local GovernmentFunding Agencies

Tokyo, February 2016

INVESTOR PRESENTATIONFebruary 2016

Executive Summary

23 February 2016

AAA/Aaa rated Danish Local Government funding agency, established in 1899

Association (membership organization) with direct, joint and several guarantee of the

Danish Local Governments

Strong guarantee structure based on the entire taxpaying population of Denmark

0% BIS risk weighting in several jurisdictions

Closest proxy to Danish sovereign risk

Excellent asset quality

Strong capitalisation

No loan losses in more than 117 years of operation

Prudent risk management

LCR: Confirmed level 1 by the Danish FSA

Page 3

Kingdom of Denmark

23 February 2016

Source: IMF World Economic Outlook, Oct 2015)

Population 5.6m

Capital Copenhagen

Credit Rating AAA/Aaa

Currency DKK

EU- Exceptions: Currency, defense and

judicial cooperation

Member 1973

Real GDP growth 2015 1.6%

Unemployment 2015 6.2%

Current Account to GDP 2015 7.0%

General Gov Debt to GDP 2015

Net Gov Debt to GDP 2015

47%

6.3%

Deficit 2015 2.7%

Page 4

23 February 2016

New CEO as of 1 September 2015

Downward adjustment of expectations on profit for 2015

• Adjustment of the accounting estimate for valuation

• No effect on KommuneKredit’s liquidity or ability to repay debts

• Profit forecast excluding value adjustments has been raised to DKK 400m

KommuneKredit is confirmed HQLA Level 1 asset by the Danish FSA

News in KommuneKredit

Page 5

23 February 2016

Organization

KommuneKredit is by law organized as an

association (membership organization) in 1899

Members are directly, jointly and severally

liable for all of KommuneKredit’s obligations

Municipalities have an unlimited right to levy

taxes on income and property

Currently all Municipalities and Regions are

members of KommuneKredit and thereby

represent the entire population of Denmark

The guarantee of the members can be called

upon any member without a preceding court

decision – the guarantee has never been

exercised

Substantial reserves

The entireDanish

population

5 Regions

98 Municipalities

All

members of

KommuneKredit

Page 6

23 February 2016

Local Government Sector in Denmark

Danish Local Governments are defined by law

and their autonomy is secured through the

constitution and other legislation.

The current Local Government structure is a

result of a reform in 2007.

Municipalities and Regions are responsible for

the majority of the services provided in the

Danish welfare system.

The Local Government Sector expenditures

amount to 2/3 of total public expenditures and

approx. 26% of GDP.

Central GovernmentForeign policy, defense, police, universities, major roads,

railways, supervision and equalisation

5 Regions

Hospitals and healthcare, regional

development and specialized social

institutions

98 Municipalities

Childcare, care for elderly, primary schools, public transportation, utilities,

environment and employment

Page 7

23 February 2016

Local Government Sector in Denmark

Revenues and supervision

Main source of revenue is income tax

The Local Governments are closely monitored

and supervised by the Ministry of Social Affairs

and the Interior

Balanced budgets required

Default not allowed

Borrowing is highly regulated – only allowed for

capital investments

Equalisation system in place

Low debt level – approx. 5.5% of GDP

Source: Statistics Denmark

15,8

1,1 1,2

0,5

6,2

13,7

13,4

26,5

70,3

51,3

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Municipalities Regions

Income tax

Grants

General charges

Property tax

New loans

Corporate tax

Charges from themunicipalities

Page 8

23 February 2016

Funding of KommuneKredit

Budget

Maximum pre-funding position set by the Ministry of Social Affairs and the Interior at 25% of the

total loan portfolio

Total long-term funding budget for 2016: EUR 6-8bn

Sizeable short-term funding budget

Europe; 67%

Denmark; 13%

North - and SouthAmerica; 12%

Asia; 6%

Africa and MiddleEast; 2%

USD; 29%

DKK; 26%

EUR; 12%

CHF; 2%

JPY; 4%

GBP; 17%

Other; 10%

Funding by markets in 2015 Funding by currency in 2015

Page 9

Swedish Local Government

Debt Office

KOMMUNINVEST

Version: 3 February 2016

Photo

: E

ric L

indvall,

Im

ageB

ankS

we

de

n

Bloomberg ticker: KOMINS

KOMMUNINVEST

Swedish Local Government Debt Office

www.kommuninvest.org 11

• Founded 1986 by ten local governments. Currently

280 owners/members (total=310), of which 272

municipalities and 8 county councils/regions.

• AAA/Aaa, stable outlook.

• BIS 0% risk-weighting. LCR Level 1 in the EU,

Switzerland and UK.

• Balance sheet: USD ~42 bn, lending portfolio: USD

~31 bn.

• Funding on international and domestic capital

markets. Lending in Sweden.

• Mission: provide members with cost-efficient and

stable investment funding.

Bloomberg ticker: KOMINS

KOMMUNINVEST

Financial highlights 2011– 2015

www.kommuninvest.org 12

FY 2011 FY 2012 FY 2013 FY2014 HY2015

Lending, USDbn 20.4 24.4 25.3 27.0 29.4

Balance sheet total, USDbn 28.4 34.4 33.7 37.9 42.6

Net interest income, USDm 69.5 93.7 117.7 111.1 45.0

Operating profit, USDm 48.1 30.2 92.0 88.5 8.4

Leverage Ratio, reported according to CRR*, % n.a. 0.33 0.57 0.76 0.67

Leverage Ratio, including subordinated loan**, % n.a. 0.65 0.91 1.09 0.96

Total capital ratio 45.7% 30.4% 59.5% 49.3% 53.1%

Tier 1 capital

Note: Increase in share capital during

2015 must be approved by Swedish

FSA before inclusion as core Tier 1

capital. Approval was obtained on 24

August 2015.

SEK/USD = 8.2389 (30 Jun 2015)

* Tier 1 capital in relation to total assets and commitments (exposures).

** Tier 1 capital and subordinated loan issued by Kommuninvest Cooperative Society,

in relation to total assets and commitments (exposures).

Lending margins reduced from Q4-2014.

Future capital build-up to be based on direct

capital injections rather than income statement.

Bloomberg ticker: KOMINS

2015 highlights – “Growth and Green”

www.kommuninvest.org 13

• Continued capital build-up ahead of leverage ratio

implementation in 2018.

• Rebound in lending – municipal investment levels

remain elevated

• Commitment to USD/SEK benchmark markets and

the Uridashi market

• LCR Level 1 also in the UK

• Green Loans offered to clients from June 2015

Bloomberg ticker: KOMINS

Growth in capital

• Kommuninvest aims to reach prescribed leverage ratio

level through

- profit build-up

- additional contribution capital from members/

owners and,

- if required, other capital instruments.

• Aims for at least 1.5 % leverage ratio by 1 Jan, 2018.

• Members/owners’ preference is to be sole providers of

capital. SEK 2.6 bn capital injection Q3-4 2015,

members to inject additional SEK ~1.5 bn until 2017.

• If final leverage ratio set at higher than expected level,

Kommuninvest has possibility to issue AT1 capital

instruments to members /owners or external parties.

www.kommuninvest.org 14

Bloomberg ticker: KOMINS

Growth in investments & lending

www.kommuninvest.org 15

SEK BillionShare of GDP

Local government loan debt

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

0

200

400

600

800

1000

1200

Debt SEK billion Share of GDP

Local government investments

Bloomberg ticker: KOMINS

”Green”

www.kommuninvest.org 16

Bloomberg ticker: KOMINSwww.kommuninvest.org 17

Growth in funding

Funding plan 2016

Long-term funding: USD 15-17 bn• Focus on USD and SEK benchmark programmes,

• Uridashi

Short-term funding: • ECP, domestic CP, short-term

• Uridashi

____________________________________________________

What impacts funding volume during the year?

• Revisions to lending forecast

• Early redemptions in outstanding borrowings

Change in funding need – Impact on funding programmes

USD benchmark programme No impact (strategic programme)

SEK benchmark programme No impact (strategic programme)

Uridashi No impact (strategic programme)

Private placements More / fewer transactions

ECP Issuance adapted to cover early redemptions in outstanding

borrowings or to adapt to increase/fall in short-term lending

Bloomberg ticker: KOMINS

Borrowing per currency 2011 – 2015, USD bn

excl. commercial paper borrowing

Funding strategy - diversification and core benchmark markets

www.kommuninvest.org 18

Eligible

currencies

AUD, BRL, CAD,

CHF, DKK,

EUR, GBP,

HKD, JPY,

KRW, MXN,

NOK, NZD,

SEK, TWB,

ZAR, USD

• Diversification -

currencies, investors,

instruments

• Flexibility

• Benchmark sizes

• Liquid curves

• 50 percent in SEK

Major transactions 2016/2015 (fixed)

Jan ’16: 3yr USD 1 bn RegS/144A benchmark bond due January 2019

Jan ’16: 3.5 yr GBP 400 mn bond due September 2019

Oct ’15: 3yr USD 1.25bn RegS/144A benchmark bond due October 2018

Apr ‘15: 6yr SEK 7.1bn benchmark bond due Sept 2021 (SEK 9.4 bn outstanding)

Apr ‘15: 2yr USD 500m bond due Apr 2017 & 10.5 yr AUD 100m due Oct 2025

Jan ’15: 3yr USD 1.25 bn RegS/144A benchmark bond due January 2018

SEK/USD= 8.3459 as of 31 December 2015

Exchangeable Bond

- Stocks included in Nikkei 225 &

JPX400 (Market cap 1 bn USD)

- ETF Nikkei225

Uridashi - Structured products

www.kommuninvest.org 19

Fixed

- Plain Vanilla

- Step up

FX Linked

- Linked to approved currencies

- Non-deliverable currencies

Dual Currency (DC)

- Reverse DC

- Switchable DC

- Power Reverse DC

Index Linked – Basket of Indices,

Bermudan callable (KOKI),

Worst of Indices

- Nikkei225

- Hang Seng

- Dow Jones

- EuroStoxx

- S&P 500

- Topix

Currencies approved for payment:

- AUD, CAD, CHF, DKK, EUR, GBP,

JPY, MXN, NOK, NZD, SEK, TRY,

USD, ZAR

Currencies approved as underlying*:

- AUD, BRL, CAD, CHF, CNY, DKK,

EUR, GBP, HKD, JPY, KRW, MXN,

NOK, NZD, SEK, TWB, ZAR, USD

*given adequate market data and critical volume

of the trade.

Bloomberg ticker: KOMINS

KOMMUNINVEST

Summary

www.kommuninvest.org 20

• AAA/Aaa, “closest proxy” to Swedish sovereign risk.

0% risk-weighted.

• Explicit, irrevocable, unlimited, joint and several guarantee by

member local governments. Constitutional right for members

to levy income tax.

• Prudent risk management, significant high-quality liquidity

reserve and access to central bank funding.

• Accepted as collateral and repo with numerous central banks.

In Sweden, eligible as Level 1 assets with 100% weighting in

LCR calculation.

• Equal to Swedish government bonds from a domestic

regulatory risk perspective*.

* Clarification letter from Swedish FSA is included in the Kommuninvest Investor Factbook

Bloomberg ticker: KOMINS

Mr. Anders GångeHead of Funding & Treasury

Tel: +46 (0)10 470 87 12

Contacts

www.kommuninvest.org 21

Mr. Carl-Henrik AroseniusHead of Investor Relations

Tel: +46 (0)10 470 88 81

Mr. Per AdolfssonFunding Officer

Tel: +46 (0)10 470 88 66

Ms. Maria ViimneDeputy CEO/Chief Operating Officer

Tel: +46 (0)10 470 87 11

Mr. Karl AigéusFunding Officer

Tel: +46 (0)10 470 88 84

Investor Relations – [email protected]

Mr. Björn BergstrandSenior Investor Relations Manager

Tel: +46 (0)10 470 87 31

Mr. Kanichiro HirataSenior Advisor, Japan/Asia Rep.

Tel: +81 90 2758 0222

Funding – [email protected]

Mr. Tobias LandströmSenior Funding Officer

Tel: +46 (0)10 470 88 83

Ms. Ulrika Gonzalez HedqvistSenior Funding Officer

Tel: +46 (0)10 470 88 82

Bloomberg ticker: KOMINSwww.kommuninvest.org 22

The Kommuninvest Investor

Factbook contains in-depth

information material on

Kommuninvest and the Swedish

local government sector, including

financial reports, rating reports

and legal documentation. The

Factbook is specifically designed

to facilitate investor/counterparty

credit approval and review

processes.

All documents included in the

Factbook are available for download at

Kommuninvest’s website

www.kommuninvest.org

Investor Relations

Financial information.

Investor Factbook

Bloomberg ticker: KOMINSwww.kommuninvest.org 23

23

/02/2016

Co

pyrigh

t Mu

nicip

ality Finan

ce

23

Municipality Finance plcFebruary 2016

23

/02/2016

Co

pyrigh

t Mu

nicip

ality Finan

ce

24

2

An overview of MuniFin

Agenda

3

4

1

Latest Developments

Funding

Appendices

23

/02/2016

Co

pyrigh

t Mu

nicip

ality Finan

ce

3

1. An Overview of MuniFin

23

/02/2016

Co

pyrigh

t Mu

nicip

ality Finan

ce

4

Municipality Finance – The leading provider of financial services to Finland’s local government and public housing sectors

Aaa (Neg) / AA+ (Neg) rated by Moody’s and S&P, with senior unsecured funding guaranteed by the Municipality Guarantee Board

Explicitly guaranteed by MGB (Aaa (Neg) / AA+ (Neg))

100% Finnish public sector-owned credit institution

Lending only to the Finnish public sector and public housing sector

53%31%

16%

Ownership Structure

Municipalities Keva Republic of Finland

23

/02/2016

Co

pyrigh

t Mu

nicip

ality Finan

ce

5

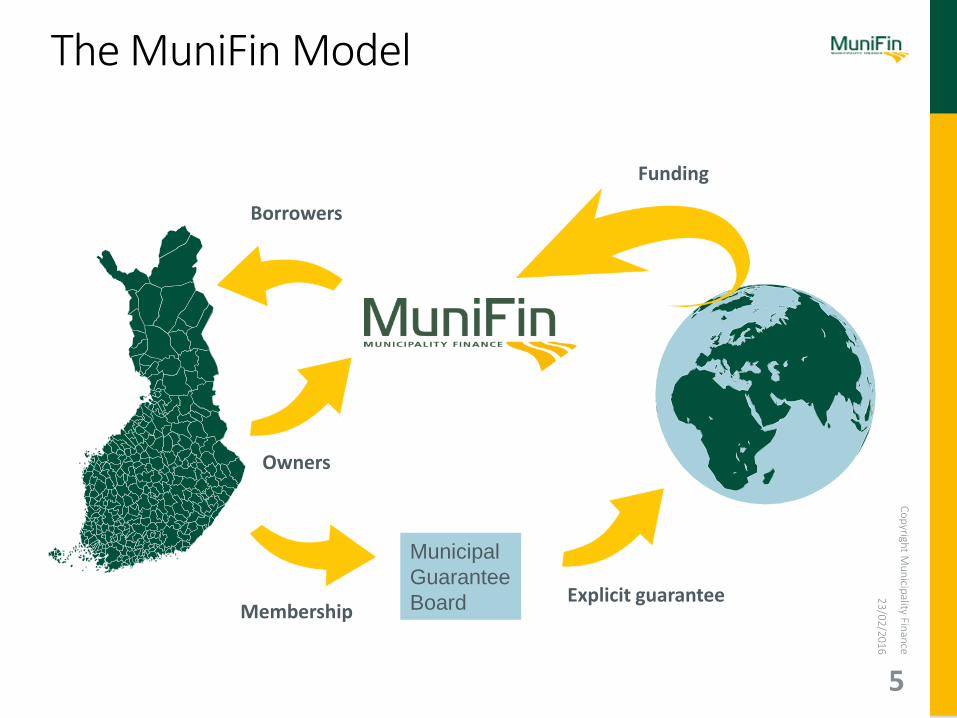

MembershipExplicit guarantee

Municipal

Guarantee

Board

Borrowers

Owners

Funding

The MuniFin Model

23

/02/2016

Co

pyrigh

t Mu

nicip

ality Finan

ce

6

MuniFin’s strategy

23

/02/2016

Co

pyrigh

t Mu

nicip

ality Finan

ce

7

Latest Developments

23

/02/2016

Co

pyrigh

t Mu

nicip

ality Finan

ce

8

MuniFin’s Satement in NLFGA’s presentation in Tokyo in *2011

• Minimum capital requirement (2018/2019)

• Tier 1 Capital (6 %) Not a problem

– 16.90 % (June 30, 2011)

• Leverage ratio (3 %) Challenging requirement

• Support from the Government, understanding also on the EU level

• MuniFin will

1) continue to through economical growth to minimize the need of additional capital;

2) continue actively to promote Directive level exemption for public sector credit institutions;

3) continue to evaluate the need and scope of the possible specialized legislation for MuniFin.

23

/02/2016

Co

pyrigh

t Mu

nicip

ality Finan

ce

9

Strong Capital Generation Through Profitability

0,00%

0,20%

0,40%

0,60%

0,80%

1,00%

1,20%

1,40%

1,60%

1,80%

2,00%

0

100

200

300

400

500

600

700

2008 2009 2010 2011 2012 2013 2014

Total capital Tier 1 capital Profit from operations Leverage ratioMuniFin has not paidany dividend since2011

23

/02/2016

Co

pyrigh

t Mu

nicip

ality Finan

ce

10

Financial Performance – Consolidated figures

31st December 2011 31st December 2012 31st December 20131 31th December 2014 30th June 2015

Lending Portfolio (€m) 13,625 15,700 17,801 19,205 19,378

Total Assets (€m) 23,842 25,560 26,156 30,009 33,693

Total Own Funds (€m)2 289 429 509 623 683

Net Operating Profit (€m) 65 139 141 144 78*

Cost-to-Income Ratio 0.23 0.14 0.15 0.15 0.15

Return on Equity 27.1% 38.0% 30.6% 21.7% 20.1%**

CET1 Ratio 3, 4 19.0% 26.2% 28.3% 29.9%4 30.1%4

Total Capital Ratio5 24.1% 33.9% 32.5% 33.5%5 31.8%5

Leverage Ratio – – 1.7% 1.8% 1.9%

1 Consolidated key figures for capital adequacy on 31 December 2013 have been recalculated taking into account the changes pursuant to the EU Capital Requirements Regulation (EU 575/2013) effective as of 1 January 2014. Figures of 2014 and 2013 are not comparable with figures of 2012 and 2011.2 The Total Own Funds of the parent company amounted to EUR 682 million at the end of June 2015 and EUR 622 million at the end of December 2014.3 For 2011 and 2012 the figures presented are TIER 1 ratios as EU Capital Requirements Regulation (EU 575/2013) was not effective until 1 January 2014.4 The CET1 Ratio references Municipality Finance Plc, not the parent company. The CET1 ratio of the parent company was 30.2% at the end of June 2015 and 30.0% at the end of December 2014.5 The Total Capital Ratio of the parent company was 31.8% at the end of June 2015 and 33.6% at the end of December 2014.* As of 30 June 2015. ** Annualised as of 30 June 2015

23

/02/2016

Co

pyrigh

t Mu

nicip

ality Finan

ce

11

Highlights in 2015

• In September MuniFin issued AT1 transaction as the first SSA-issuer and thefirst issuer in Finland

– EUR 350 mio 4.5 % PNC 6,5 years

– Strong order book

– Strong participation by owner’s (allocation 43 % of the transaction)

– Good performance in secondary markets

– is estimated to increase it’s leverage ration over the company’s internal min. target of 3,0 %

• Finnish FSA defined MuniFin as nationally significant credit institution in June

– Capital add-on 0,5 %. Is easily fulfilled

• Participated AQR-test by ECP and easily passed all the tests

• Supervised by ECP since January 1, 2016

– 3rd largest credit institution in Finland

– Total Assets over 30 bn.

23

/02/2016

Co

pyrigh

t Mu

nicip

ality Finan

ce

12

Funding

23

/02/2016

Co

pyrigh

t Mu

nicip

ality Finan

ce

13

Funding strategy in 2016

0,00%

20,00%

40,00%

60,00%

80,00%

100,00%

2013 2014 2015

Uridashi Private placements Public deals

We believe success requires:

• Being able to accommodate differentinvestor appetites

• Understanding new market trends and adapting accordingly, example single stocklinked Uridashis

• Investor work and promoting one’s name

• Transparency with dealer banks

EUR / USD Benchmark

Other public markets

RetailPrivate

placements

ECP

0

2 000

4 000

6 000

8 000

10 000

12 000

2008 2009 2010 2011 2012 2013 2014 2015 2016e

(€m) Long-Term Funding program

23

/02/2016

Co

pyrigh

t Mu

nicip

ality Finan

ce

14

Funding highlights in 2015

Uridashi

-record amount of transactions, 225

-Moving to number 1 for Issuer league table in SSA space

-New products; Double Monitor (FX and Equity linked)

Private placements

-Strong support from Investor community in callable structures

-Issuances from 1y up to 30y in maturity

-Broad currency range offered to investors

Public Markets

-2 successfull USD Benchmarks (March 2020 and September 2018)

-New AUD 2026 line

-AT1 transaction in September (EUR 350 MM NC 6,5y)

1. TNS Sifo Prospera Survey conducted in 2015

23

/02/2016

Co

pyrigh

t Mu

nicip

ality Finan

ce

15

Ability to sustain volumes in the Uridashi market

• MuniFin is the only SSA issuer that has been able to maintain and even strengthen its Uridashi volumesin the medium term.

• Maintaining volumes has been difficult for SSA issuers as compressed credit spreads have moveddemand from SSAs more to bank names.

• MuniFin ranks number 1 in Uridashi volume in 2015

0

1000

2000

3000

4000

5000

6000

7000

2011 2012 2013 2014 2015

Mill

ion

s, U

SD Annual Uridashi Volumes of SSA peers

Kommunalbanken (KBN)

MuniFin

Kommuninvest

KfW

Svensk Exportkredit (SEK)

Kommunekredit

Source: Bloomberg ticker URID, Uridashi Bonds1. Source: Bloomberg ticker URID, Uridashi Bonds

Plain vanilla Low/Zero coupon

Interest rate

Fixed rateLow coupon, deepdiscount Fixed coupon inflation linked

Fixed European/Bermudan callable

Zero coupon Step up fixed rate

Floating rateZero coupon European/ Fixed to floating rate

Capped Floating rate

Bermudan callable

Fixed to floating European/Bermudan callable

Collared Floating rate Reverse Floating rate

CMS linked

CMS TARN

CMS Range accrual

RMS Range accural

23

/02/2016

Co

pyrigh

t Mu

nicip

ality Finan

ce

16

Accepted structures in the Uridashi market

FX linked Equity/Index/Commodity IndexFX Basket linked Participation index/basket linked

Dual currency Fixed coupon index linked Knock-out/Knock-in

Reverse dualcurrency Digital coupon index linked Knock-out/Knock-in

Power reverse dual currency

Fixed coupon ETF linked Knock-out/Knock-in- also physical delivery

European/Bermudan callable RDC/

Single or basket equity linked - also physical delivery

PRDC Mutual fund linked

Trigger PRDC/RDC CPPI-linked

Target redemption PRDC Dual monitor: FX and equity index linked

Plain vanilla44%

Equity linked24%

Fixed callable

20%

FX linked8%

Index linked

2%

Zero callable, Commod

ity linked, Zero

bullet, Interest rate …

Funding by structure in 2015 YTD

Plain vanilla55%

Equity linked16%

Fixed callable

12%

FX linked10%

Zero callable

4%

Index linked,

Interest rate

linked, Deep

discount, Commo…

Funding by structure in 2014

23

/02/2016

Co

pyrigh

t Mu

nicip

ality Finan

ce

17

Funding breakdown 2015 & 2014

Retail37%

Central Bank/Official

Institution29%

Bank 19%

Asset Manager10%

Insurance5%

Funding by investor type 2015

Asia Pacific44%

Europe23%

Africa and the Middle East

21%

Americas9%

Nordics3%

Funding by region 2015

USD; 37,29%

JPY; 26,02%

GBP; 13,12%

EUR; 12,10%

CLP; 2,89%

AUD; 2,89%

CHF; 1,67%Other; 4,02%

Funding by Currency 2014

Asia Pacific; 39,25%

Europe; 20,82%

Africa and the Middle

East; 18,08%

Americas; 17,22%

Nordics; 4,63%

Funding by Region 2014

Central bank/Official Institution;

34,48%

Retail; 29,41%

Asset manager; 18,21%

Bank; 9,48%

Insurance; 7,89%

Corporate; 0,53%

Funding by Investor Type 2014

23

/02/2016

Co

pyrigh

t Mu

nicip

ality Finan

ce

18

Please visit: www.munifin.fi

Mari Tyster

Head of Legal and Compliance

Tel: +358 9 6803 5626

Pekka Averio

President and CEO

Tel: +358 9 6803 6211

Esa Kallio

Executive Vice PresidentDeputy to CEO

Tel: +358 9 6803 6231

Marjo Tomminen

CFO

Tel: +358 9 6803 5626

Contact information: Senior Management

Karoliina Kajova

Analyst, Funding

Tel: +358 9 6803 6215

Martin Svedholm

Manager, Funding

Tel: +358 9 6803 5685

Joakim Holmström

Head of Funding

Tel: +358 9 6803 5674

Antti Kontio

Manager, Funding

Tel: +358 9 6803 5634

Contact information Funding: [email protected]

Contact information ECP: ([email protected])

Pyry Happonen

Manager, Treasury

Tel: +358 9 6803 5692

Jarno Kosonen

Head of Treasury

Tel: +358 9 6803 5687

Lauri RasiManager, Treasury

Tel: +358 9 6803 5693

Investor relations pages:

• Annual and Interim reports• One Pager (e.g. English,

Deutsch, Mandarin, Japanese...)

• News• Links (e.g. MGB, LGPI)• Contact information