norfolk pension fund · 2016-10-12 · this presentation discusses the current issues in the lgps...

TRANSCRIPT

Hymans Robertson LLP is authorised and regulated by the Financial Conduct Authority

Norfolk Pension Fund

Governance, Freedom and Choice, Auto Enrolment, Employer Responsibility

John Wright

26 November 2014

2

What will be covered ?

New Governance Regime

Freedom and Choice

Auto Enrolment

Employer Responsibility

New Governance Regime

5

Outcome

Pension board (1) “establishment of a board” (a) “secure compliance with the LGPS” (b) secure compliance with requirements imposed…by the Pensions Regulator. (c) other matters.

Public Services Pensions Act 2013 - Regulation 5

6

Established by…

1 April 2015

First meeting by 31 August 2015

7

Current Fund governance structure Secretary of State

(Communities and Local Government)

Administering Authority Technical professional advice and guidance

(e.g. LGE, CIPFA) Pension Committee (s.101 responsibility - decision making,

funding strategy, etc)

Officers (carrying out actions on behalf of panel

and S151 responsibility)

8

Future LGPS governance structure HM Treasury

Responsible Authority (Secretary of State)

tPR (codes of practice on governance,

administration, etc.)

National Scheme Advisory Board

Qualified person

Administering Authority Technical professional advice and guidance

(e.g. LGE, CIPFA)

Sub groups

Pension Committee (s.101 responsibility)

Officers (s.151 responsibility)

Pension Board

9

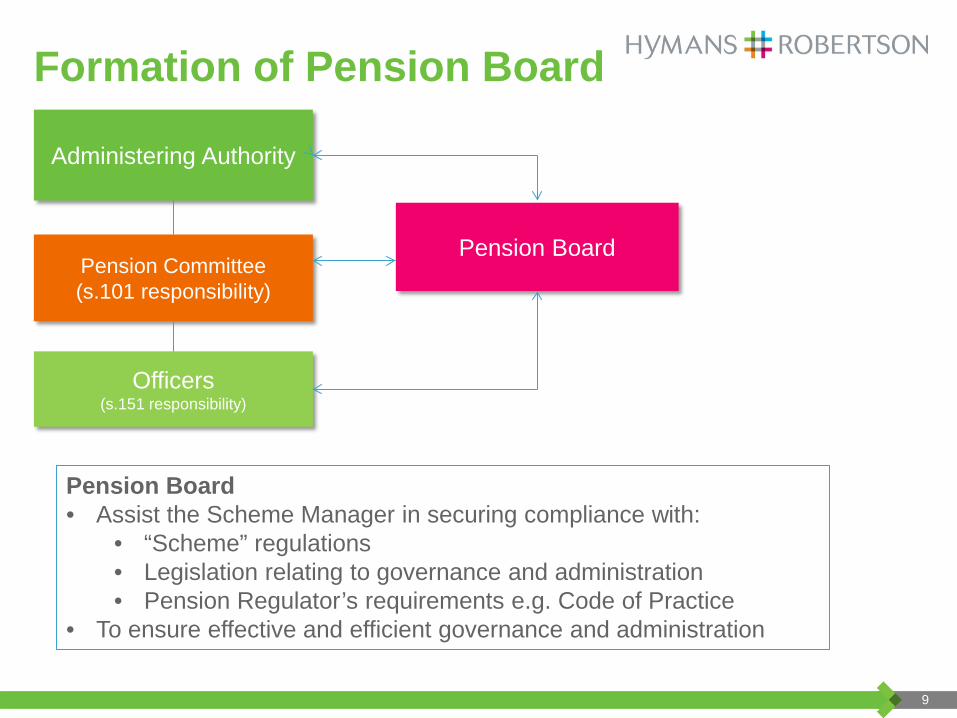

Formation of Pension Board

Pension Board • Assist the Scheme Manager in securing compliance with:

• “Scheme” regulations • Legislation relating to governance and administration • Pension Regulator’s requirements e.g. Code of Practice

• To ensure effective and efficient governance and administration

Administering Authority

Pension Committee (s.101 responsibility)

Officers (s.151 responsibility)

Pension Board

10

Pension Board Requirements • Prescribed in scheme rules • Assists the Scheme Manager in securing

compliance

• Equal number of scheme member and employer representatives

• No conflict of interest

• Experience and capacity

11

Local pension board cont’d Have regard to guidance issued by Secretary of State

Purpose – roles & responsibilities Determining constituencies for representation Appointments / terms of office / attendance / terminations Number of meetings Reporting requirements Whistle blowing mechanisms Information Payments

Complying with the Pension Regulator’s Code of Practice

(Scheme advisory board may provide further guidance)

12

What does this all mean?

Oversight and attention of the pension board and help with tPR requirements.

Changes intended to raise standards elsewhere in the LGPS.

13

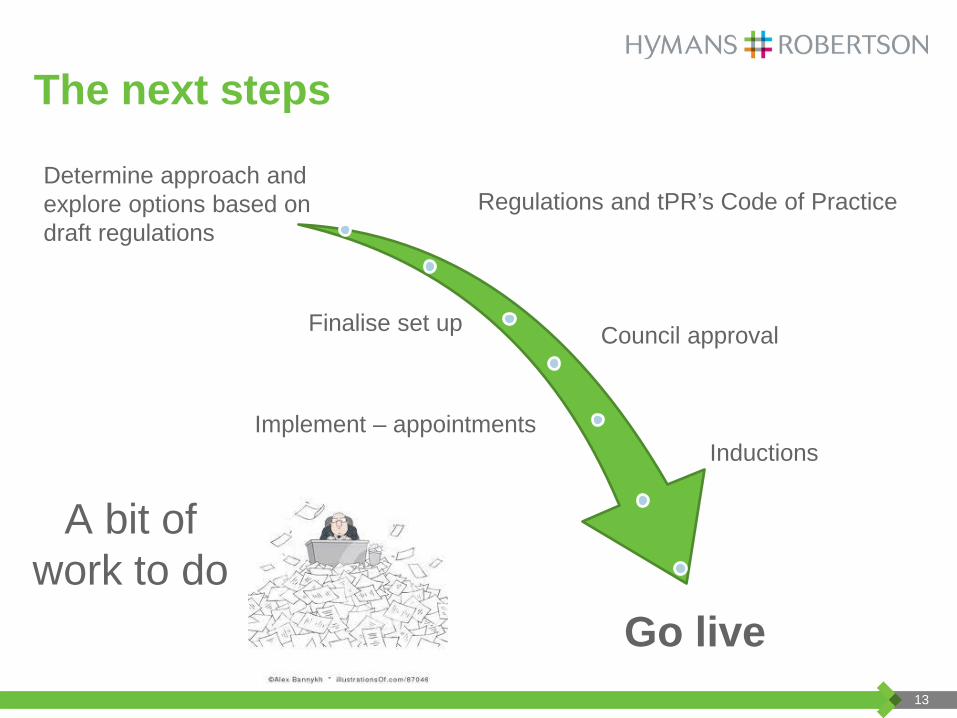

The next steps

Go live

Determine approach and explore options based on draft regulations

Regulations and tPR’s Code of Practice

Finalise set up

Implement – appointments

Council approval

Inductions

A bit of work to do

Freedom and Choice

15

Remember me?

Introduced auto enrolment Ending contracting out Freedom and choice Higher state pension

16

How does it work?

Individual in Defined Benefit

scheme at age 55

Unlock cash via Defined Contribution

scheme

Individual in Defined

Contribution scheme at age 55

Tax considerations Freedom and choice

17

Example

Transfer of entire pension pot of approximate value £150,000

(ignores tax)

Employee currently aged 55

£10,000 p/a

DB pension from age 65

18

Who will it benefit?

Flexibility will be attractive to significant minority Bring spending forward Different ‘shape’ of spending Flexibility Control Investment returns

Inheritance Supporting younger or older generations Tax free cash typically 25% higher Integrating with part time work and phased retirement Pay off debts/mortgage

19

Impact on scheme employers

Scheme and employer considerations Getting best value for members from existing spend Members making right choices for them Risk reduction tool Workforce management tool for employer Potential savings

Flexibility will become commonplace: a win-win if terms set fairly

20

Which schemes are affected?

Private sector

PAYG public e.g. teachers

Funded public e.g. LGPS

21

Putting flexibility in place in the private sector Key considerations

Guidance for members

Terms of offer

Target membership

Communications

Investment strategy

Pensions Committee

Ensure employees make the most of their benefits

22

Impact on LGPS

Similar to private sector?

How much gets paid out? CETV’s?

Impact on: Contributions? Funding levels? Cashflows and investment strategy? Risk for employers? AVC’s?

Auto Enrolment

24

Background Fewer workers supporting retired population

10:1 in 1901, expected to fall to 2:1 by 2050 Increased cost of providing State Pensions

Encourage greater private sector retirement saving

New legal duties on employers

Phased in for employers from 1 October 2012 Smallest by April 2017

DWP responsible for roll-out

25

Staging dates

Number of employees in largest PAYE scheme

From October 2012 for larger employers

Consider postponement or transitional period ?

26

When is your staging date? PAYE Scheme size Staging date Alternative staging date 120,000 or more 1 October 2012 1 August 2015 50,000 to 119,999 1 November 2012 1 August 2015 30,000 to 49,999 1 January 2013 1 October 2015 20,000 to 29,999 1 February 2013 1 October 2015 10,000 to 19,999 1 March 2013 1 January 2016 6,000 to 9,999 1 April 2013 1 January 2016 4,100 to 5,999 1 May 2013 1 February 2016 4,000 to 4,099 1 June 2013 1 February 2016 3,000 to 3,999 1 July 2013 1 March 2016 250 to 2,999 1 August 2013 to 1

February 2014 1 March 2016 to 1 July 2016

< 250 1 April 2014 to 31 March 2017

1 July 2016 to 1 April 2017

27

ELIGIBLE JOBHOLDERS AGED 22-SPA EARN £10,000 PLUS AUTO ENROL

NON ELIGIBLE JOBHOLDERS AGED 16-75 EARN £5,772 to £10,000 CAN OPT TO JOIN

ENTITLED WORKERS AGED 16 – 75 EARN LESS THAN £5,772 CAN OPT TO JOIN

Categorising workers

28

Categorising workers

Non-eligible job holders

Entitled workers

Non-eligible job holders

Non-eligible job holders

75

SPA

22

16

£5,772 Lower earnings

threshold

£10,000 Earnings trigger

£41,865 Upper earnings

threshold

Age

Earnings

Opt-in to a scheme (LGPS)

Opt-in to Qualifying Scheme (LGPS)

Auto-enrol to Qualifying Scheme (LGPS)

Qualifying Earnings

Eligible job holders

29

Inducements & prohibited conduct

Effective from 1 July 2012 (so already in place) What’s included

Prohibited recruitment conduct Inducement to opt out of LGPS Unfair treatment of workers

What are the sanctions? Pensions Regulator compliance notice Penalties

30

BIG Money penalties for non compliance Fixed penalty notice of £400 Prohibitive recruitment notice Based on number of workers – but in total no more than £50,000 Escalating penalty notice £50 to £2.500 per day for less than 250 workers £5,000 per day for 250 plus workers £10,000 per day for 500 or more workers Possible imprisonment

Equates to £70,000 per week or £3.64 million per year !

31

Financial Impact on Employers

Before auto-enrolment: Approximately 70% of employees were in the scheme

After auto-enrolment: Approximately 90% of employees are in the scheme More cash required, around 30%!!

Employer Responsibility

33

Your responsibilities

Data

Record Keeping

Procedures documented

Monitoring

Corrective procedure

34

Every one has a part to play

Get contributions right

Paying the right pension

Sticking to procedures

Keep the people who need to know informed

Meet deadlines

Data is up to date and relevant

35

More important than ever

Greater tPR oversight

Complexities of new CARE scheme Greater emphasis on yearly record keeping Less flexibility for adjustments to be made at date of retirement

Any questions? Thank you

37

Reliances and Limitations This presentation is addressed to Norfolk County Council for its sole use as Administering Authority and not for the purposes of advice to any other party; Hymans Robertson LLP makes no representation or warranties to any third party as to the accuracy or completeness.

This presentation discusses the current issues in the LGPS and was prepared purely for illustration to employers. Hymans Robertson LLP accepts no liability for any other purpose of this presentation, for instance employers considering their own auto-enrolment requirements.

The following Technical Actuarial Standards* are applicable in relation to this presentation and have been complied with where material:

TAS R – Reporting; TAS D – Data; TAS M – Modelling; and Pensions TAS.

* Technical Actuarial Standards (TASs) are issued by the Financial Reporting Council and set standards for certain items of actuarial work, including the information and advice contained here.