north american steel industry recent market developments, future prospects … · ·...

TRANSCRIPT

1

North American Steel Industry

Recent Market Developments, Future

Prospects and Key Challenges

OECD Steel Committee

June 8-9, 2009

Paris, France

*American Iron and Steel Institute (AISI)

Steel Manufacturers Association (SMA)

Specialty Steel Industry of North America (SSINA)

Canadian Steel Producers Association (CSPA)

Mexican Steel Producers Association (CANACERO)

2

Presentation Summary

I. NAFTA Economic Conditions and Outlook

II. NAFTA Steel Market Conditions and Outlook

III. NAFTA Steel Trade Challenges and Concerns

2

3

I. NAFTA Economic Conditions and Outlook

4

NAFTA Region Continues in Serious Recession

NAFTA Real GDP Since 2007

-6.3

-1.8

0

-5.7

-5.4

-5.9-8

-6

-4

-2

0

2

4

6

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

2007 2008 2009

Qu

arte

rly

% c

ha

ng

e

USA Canada Mexico

Sources: Bureau of Economic Analysis (US) , Statistics Canada, Canacero

3

55Sources: Bureau of Economic Analysis (US) ,CSSPA, Canacero

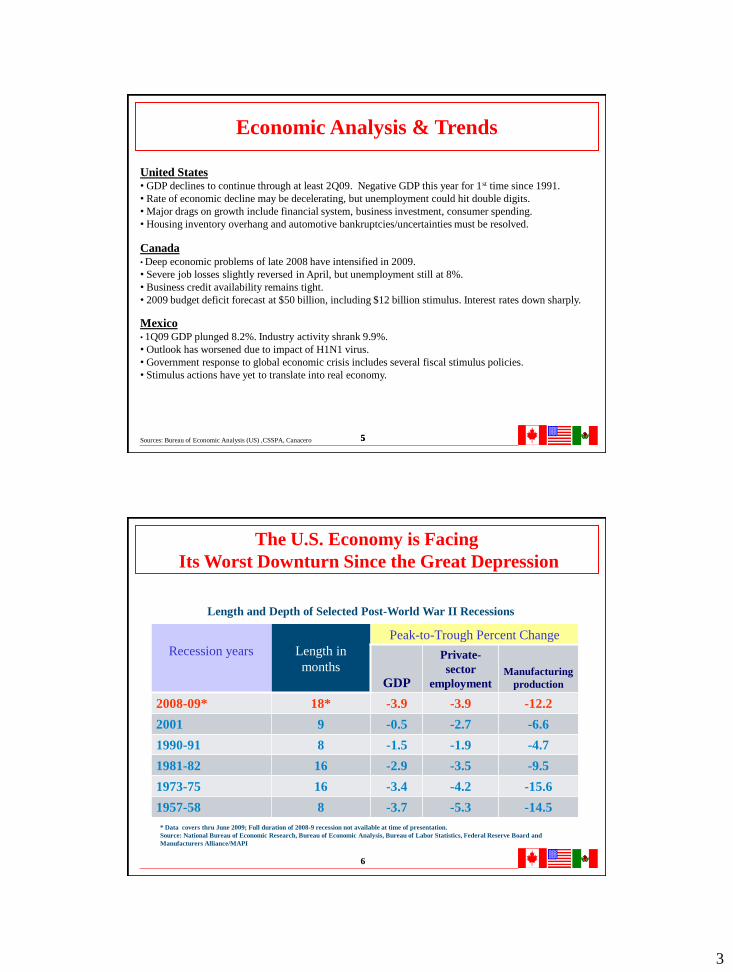

United States• GDP declines to continue through at least 2Q09. Negative GDP this year for 1st time since 1991.

• Rate of economic decline may be decelerating, but unemployment could hit double digits.

• Major drags on growth include financial system, business investment, consumer spending.

• Housing inventory overhang and automotive bankruptcies/uncertainties must be resolved.

Canada• Deep economic problems of late 2008 have intensified in 2009.

• Severe job losses slightly reversed in April, but unemployment still at 8%.

• Business credit availability remains tight.

• 2009 budget deficit forecast at $50 billion, including $12 billion stimulus. Interest rates down sharply.

Mexico• 1Q09 GDP plunged 8.2%. Industry activity shrank 9.9%.

• Outlook has worsened due to impact of H1N1 virus.

• Government response to global economic crisis includes several fiscal stimulus policies.

• Stimulus actions have yet to translate into real economy.

Economic Analysis & Trends

6

Length and Depth of Selected Post-World War II Recessions

Recession years Length in

months

Peak-to-Trough Percent Change

GDP

Private-

sector

employmentManufacturing

production

2008-09* 18* -3.9 -3.9 -12.2

2001 9 -0.5 -2.7 -6.6

1990-91 8 -1.5 -1.9 -4.7

1981-82 16 -2.9 -3.5 -9.5

1973-75 16 -3.4 -4.2 -15.6

1957-58 8 -3.7 -5.3 -14.5

The U.S. Economy is Facing

Its Worst Downturn Since the Great Depression

* Data covers thru June 2009; Full duration of 2008-9 recession not available at time of presentation.

Source: National Bureau of Economic Research, Bureau of Economic Analysis, Bureau of Labor Statistics, Federal Reserve Board and

Manufacturers Alliance/MAPI

4

77

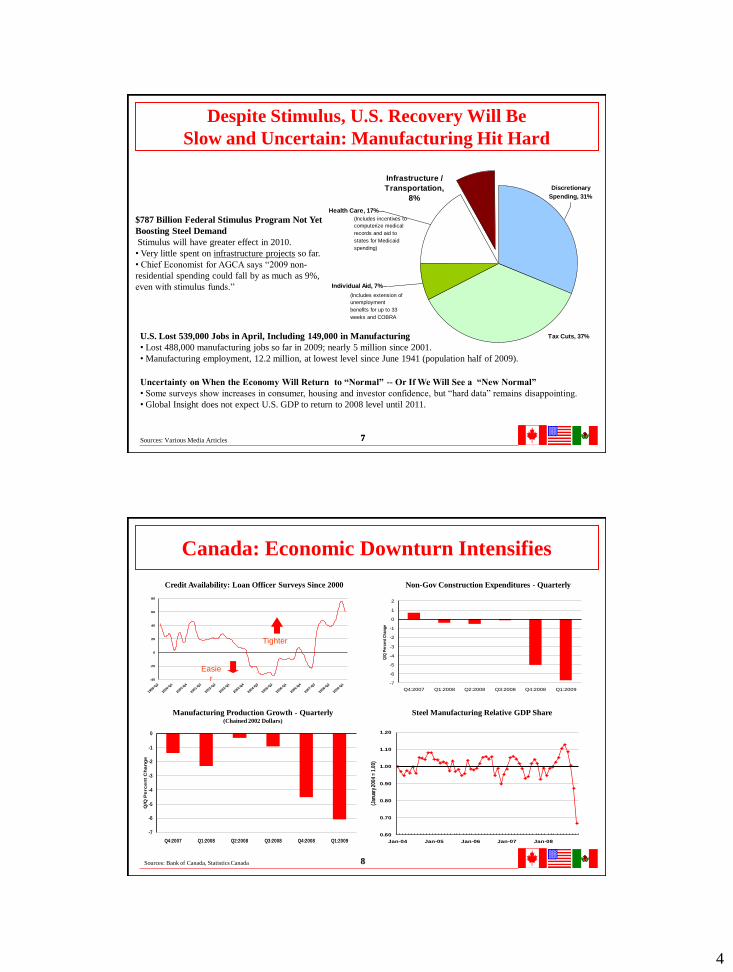

Despite Stimulus, U.S. Recovery Will Be

Slow and Uncertain: Manufacturing Hit Hard

$787 Billion Federal Stimulus Program Not Yet

Boosting Steel Demand

Stimulus will have greater effect in 2010.

• Very little spent on infrastructure projects so far.

• Chief Economist for AGCA says “2009 non-

residential spending could fall by as much as 9%,

even with stimulus funds.”

U.S. Lost 539,000 Jobs in April, Including 149,000 in Manufacturing

• Lost 488,000 manufacturing jobs so far in 2009; nearly 5 million since 2001.

• Manufacturing employment, 12.2 million, at lowest level since June 1941 (population half of 2009).

Sources: Various Media Articles

Uncertainty on When the Economy Will Return to “Normal” -- Or If We Will See a “New Normal”

• Some surveys show increases in consumer, housing and investor confidence, but “hard data” remains disappointing.

• Global Insight does not expect U.S. GDP to return to 2008 level until 2011.

Infrastructure /

Transportation,

8%

Health Care, 17%

Individual Aid, 7%

Tax Cuts, 37%

Discretionary

Spending, 31%

(Includes incentives to

computerize medical

records and aid to

states for Medicaid

spending)

(Includes extension of

unemployment

benefits for up to 33

weeks and COBRA

subsidy)

8

-40

-20

0

20

40

60

80

1999:Q

2

2000:Q

1

2000:Q

4

2001:Q

3

2002:Q

2

2003:Q

1

2003:Q

4

2004:Q

3

2005:Q

2

2006:Q

1

2006:Q

4

2007:Q

3

2008:Q

2

2009:Q

1

0.60

0.70

0.80

0.90

1.00

1.10

1.20

Jan-04 Jan-05 Jan-06 Jan-07 Jan-08

(Jan

uary

200

4 =

1.00

)

Canada: Economic Downturn Intensifies

Sources: Bank of Canada, Statistics Canada

Credit Availability: Loan Officer Surveys Since 2000 Non-Gov Construction Expenditures - Quarterly

Steel Manufacturing Relative GDP Share

-7

-6

-5

-4

-3

-2

-1

0

Q4:2007 Q1:2008 Q2:2008 Q3:2008 Q4:2008 Q1:2009

Q/Q

Pe

rc

en

t C

ha

ng

e

Manufacturing Production Growth - Quarterly(Chained 2002 Dollars)

-7

-6

-5

-4

-3

-2

-1

0

1

2

Q4:2007 Q1:2008 Q2:2008 Q3:2008 Q4:2008 Q1:2009

Q/Q

Per

cen

t C

han

ge

Easie

r

Tighter

5

9

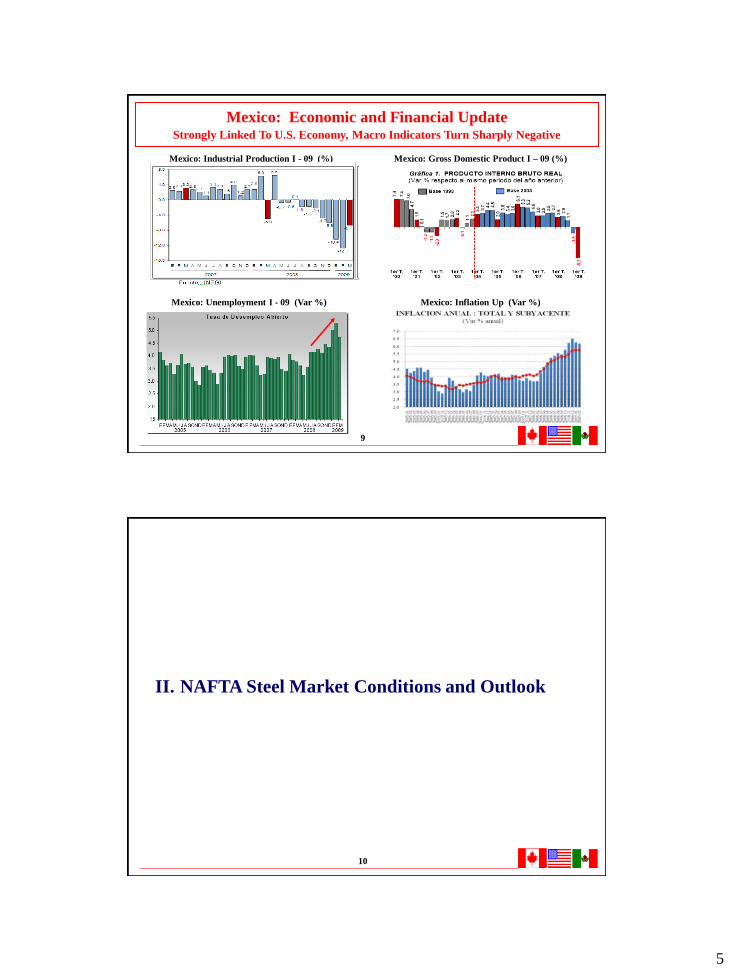

Mexico: Economic and Financial UpdateStrongly Linked To U.S. Economy, Macro Indicators Turn Sharply Negative

Mexico: Industrial Production I - 09 (%)

Mexico: Inflation Up (Var %)

Mexico: Gross Domestic Product I – 09 (%)

Mexico: Unemployment I - 09 (Var %)

10

II. NAFTA Steel Market Conditions and Outlook

6

11

“Improvement in steel consumption

for the second half of 2009 will

depend on the effects of government

stimulation packages, the continued

stabilization of financial systems

and a return of some consumer

confidence” - Daniel Novegil,

Chairman, Worldsteel Economic

Committee, 26/4/09

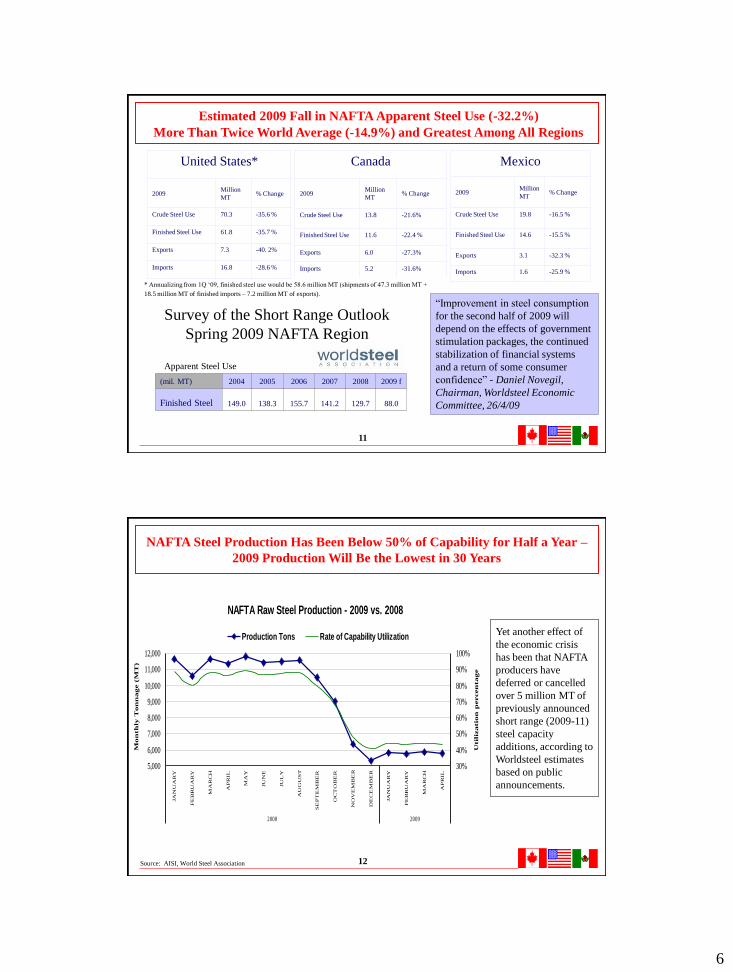

Estimated 2009 Fall in NAFTA Apparent Steel Use (-32.2%)

More Than Twice World Average (-14.9%) and Greatest Among All Regions

(mil. MT) 2004 2005 2006 2007 2008 2009 f

Finished Steel 149.0 138.3 155.7 141.2 129.7 88.0

Apparent Steel Use

Survey of the Short Range Outlook

Spring 2009 NAFTA Region

United States*

2009Million

MT% Change

Crude Steel Use 70.3 -35.6 %

Finished Steel Use 61.8 -35.7 %

Exports 7.3 -40. 2%

Imports 16.8 -28.6 %

Canada

2009Million

MT% Change

Crude Steel Use 13.8 -21.6%

Finished Steel Use 11.6 -22.4 %

Exports 6.0 -27.3%

Imports 5.2 -31.6%

Mexico

2009Million

MT% Change

Crude Steel Use 19.8 -16.5 %

Finished Steel Use 14.6 -15.5 %

Exports 3.1 -32.3 %

Imports 1.6 -25.9 %

* Annualizing from 1Q „09, finished steel use would be 58.6 million MT (shipments of 47.3 million MT +

18.5 million MT of finished imports – 7.2 million MT of exports).

12Source: AISI, World Steel Association

NAFTA Steel Production Has Been Below 50% of Capability for Half a Year –

2009 Production Will Be the Lowest in 30 Years

NAFTA Raw Steel Production - 2009 vs. 2008

5,000

6,000

7,000

8,000

9,000

10,000

11,000

12,000

JA

NU

AR

Y

FE

BR

UA

RY

MA

RC

H

AP

RIL

MA

Y

JU

NE

JU

LY

AU

GU

ST

SE

PT

EM

BE

R

OC

TO

BE

R

NO

VE

MB

ER

DE

CE

MB

ER

JA

NU

AR

Y

FE

BR

UA

RY

MA

RC

H

AP

RIL

2008 2009

Mon

th

ly T

on

nage (

MT

)

30%

40%

50%

60%

70%

80%

90%

100%

Util

izatio

n p

ercen

tage

Production Tons Rate of Capability UtilizationYet another effect of

the economic crisis

has been that NAFTA

producers have

deferred or cancelled

over 5 million MT of

previously announced

short range (2009-11)

steel capacity

additions, according to

Worldsteel estimates

based on public

announcements.

7

13

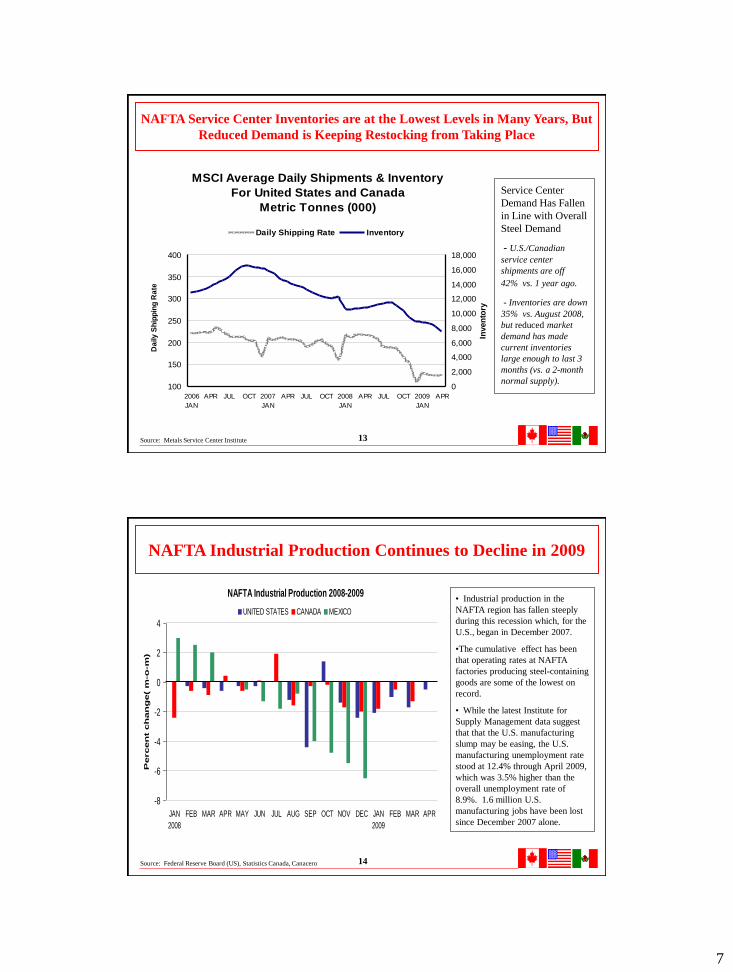

MSCI Average Daily Shipments & Inventory

For United States and Canada

Metric Tonnes (000)

100

150

200

250

300

350

400

2006

JAN

APR JUL OCT 2007

JAN

APR JUL OCT 2008

JAN

APR JUL OCT 2009

JAN

APR

Da

ily

Sh

ipp

ing

Ra

te

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

Inven

tory

Daily Shipping Rate Inventory

Source: Metals Service Center Institute

NAFTA Service Center Inventories are at the Lowest Levels in Many Years, But

Reduced Demand is Keeping Restocking from Taking Place

Service Center

Demand Has Fallen

in Line with Overall

Steel Demand

- U.S./Canadian

service center

shipments are off

42% vs. 1 year ago.

- Inventories are down

35% vs. August 2008,

but reduced market

demand has made

current inventories

large enough to last 3

months (vs. a 2-month

normal supply).

14Source: Federal Reserve Board (US), Statistics Canada, Canacero

NAFTA Industrial Production Continues to Decline in 2009

NAFTA Industrial Production 2008-2009

-8

-6

-4

-2

0

2

4

JAN

2008

FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC JAN

2009

FEB MAR APR

Percen

t c

han

ge( m

-o

-m

)

UNITED STATES CANADA MEXICO

• Industrial production in the

NAFTA region has fallen steeply

during this recession which, for the

U.S., began in December 2007.

•The cumulative effect has been

that operating rates at NAFTA

factories producing steel-containing

goods are some of the lowest on

record.

• While the latest Institute for

Supply Management data suggest

that that the U.S. manufacturing

slump may be easing, the U.S.

manufacturing unemployment rate

stood at 12.4% through April 2009,

which was 3.5% higher than the

overall unemployment rate of

8.9%. 1.6 million U.S.

manufacturing jobs have been lost

since December 2007 alone.

8

15

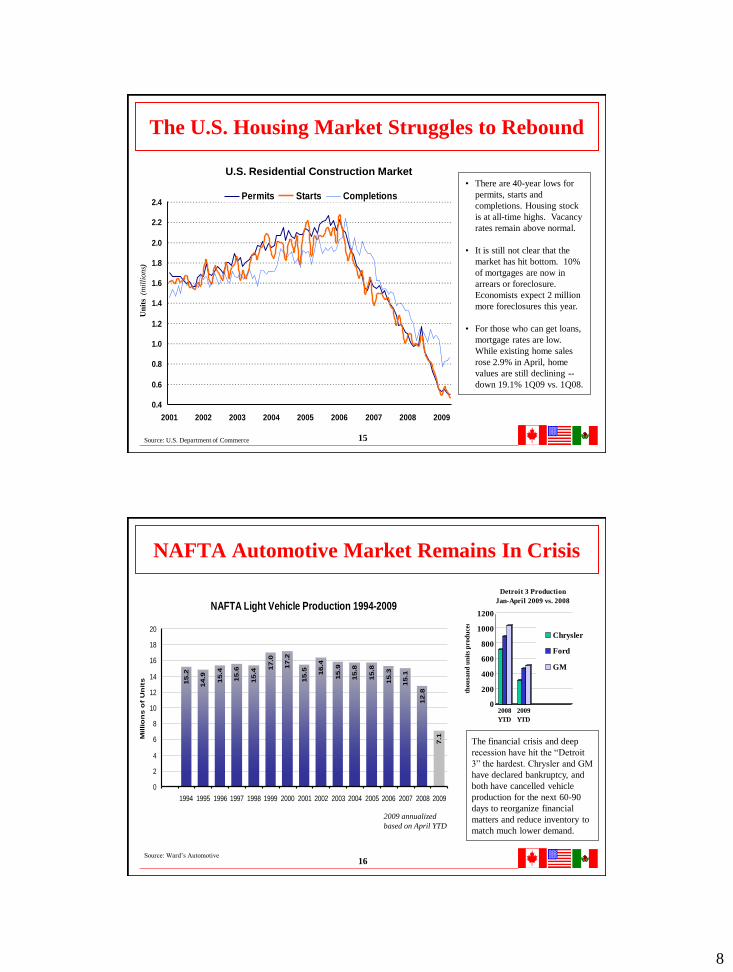

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2.2

2.4

2001 2002 2003 2004 2005 2006 2007 2008 2009

Permits Starts Completions

• There are 40-year lows for

permits, starts and

completions. Housing stock

is at all-time highs. Vacancy

rates remain above normal.

• It is still not clear that the

market has hit bottom. 10%

of mortgages are now in

arrears or foreclosure.

Economists expect 2 million

more foreclosures this year.

• For those who can get loans,

mortgage rates are low.

While existing home sales

rose 2.9% in April, home

values are still declining --

down 19.1% 1Q09 vs. 1Q08.

U.S. Residential Construction Market

The U.S. Housing Market Struggles to Rebound

Source: U.S. Department of Commerce

Un

its

(m

illi

ons)

16

NAFTA Automotive Market Remains In Crisis

0

200

400

600

800

1000

1200

thou

san

d u

nit

s p

rod

uce

d

2008

YTD

2009

YTD

Detroit 3 Production

Jan-April 2009 vs. 2008

Chrysler

Ford

GM

The financial crisis and deep

recession have hit the “Detroit

3” the hardest. Chrysler and GM

have declared bankruptcy, and

both have cancelled vehicle

production for the next 60-90

days to reorganize financial

matters and reduce inventory to

match much lower demand.

2009 annualized

based on April YTD

Source: Ward‟s Automotive

NAFTA Light Vehicle Production 1994-2009

15.2

14.9

15.4

15.6

15.4

17.0

17.2

15.5 16.4

15.9

15.8

15.8

15.3

15.1

12.8

7.1

0

2

4

6

8

10

12

14

16

18

20

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Millio

ns o

f U

nit

s

9

17

Source: NAFTA Steel Trade Monitor, US Department of Commerce,

Canacero and World Trade Atlas.

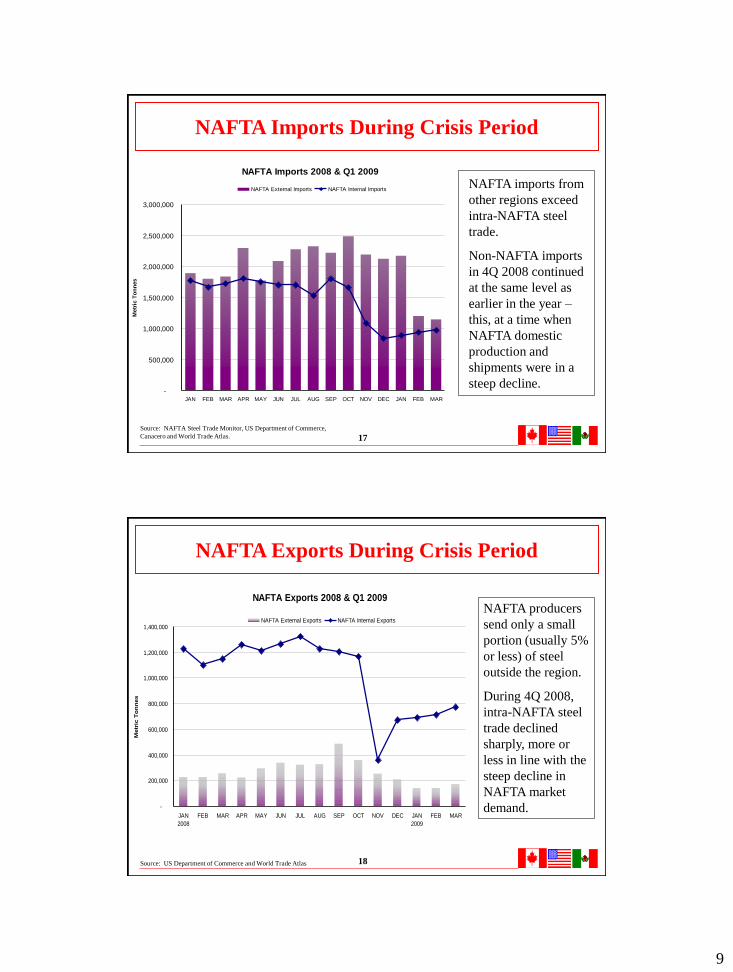

NAFTA Imports During Crisis Period

NAFTA Imports 2008 & Q1 2009

-

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC JAN FEB MAR

Metr

ic T

on

nes

NAFTA External Imports NAFTA Internal ImportsNAFTA imports from

other regions exceed

intra-NAFTA steel

trade.

Non-NAFTA imports

in 4Q 2008 continued

at the same level as

earlier in the year –

this, at a time when

NAFTA domestic

production and

shipments were in a

steep decline.

18Source: US Department of Commerce and World Trade Atlas

NAFTA Exports During Crisis Period

NAFTA Exports 2008 & Q1 2009

-

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

JAN

2008

FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC JAN

2009

FEB MAR

Metr

ic T

on

nes

NAFTA External Exports NAFTA Internal Exports

NAFTA producers

send only a small

portion (usually 5%

or less) of steel

outside the region.

During 4Q 2008,

intra-NAFTA steel

trade declined

sharply, more or

less in line with the

steep decline in

NAFTA market

demand.

10

19

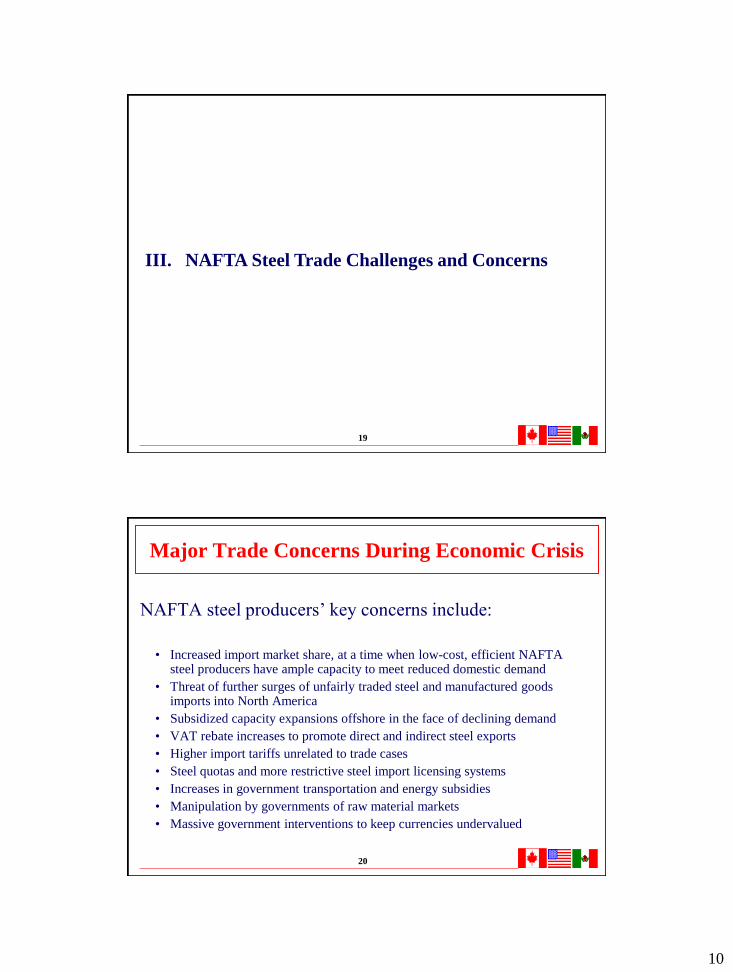

III. NAFTA Steel Trade Challenges and Concerns

20

Major Trade Concerns During Economic Crisis

NAFTA steel producers‟ key concerns include:

• Increased import market share, at a time when low-cost, efficient NAFTA steel producers have ample capacity to meet reduced domestic demand

• Threat of further surges of unfairly traded steel and manufactured goods imports into North America

• Subsidized capacity expansions offshore in the face of declining demand

• VAT rebate increases to promote direct and indirect steel exports

• Higher import tariffs unrelated to trade cases

• Steel quotas and more restrictive steel import licensing systems

• Increases in government transportation and energy subsidies

• Manipulation by governments of raw material markets

• Massive government interventions to keep currencies undervalued

11

21

1,000

1,050

1,100

1,150

1,200

1,250

1,300

1,350

1,400

1,450

1,500

1Q

2005

2Q

2005

3Q

2005

4Q

2005

1Q

2006

2Q

2006

3Q

2006

4Q

2006

1Q

2007

2Q

2007

3Q

2007

4Q

2007

1Q

2008

2Q

2008

3Q

2008

4Q

2008

1Q

2009

Millio

ns o

f M

T

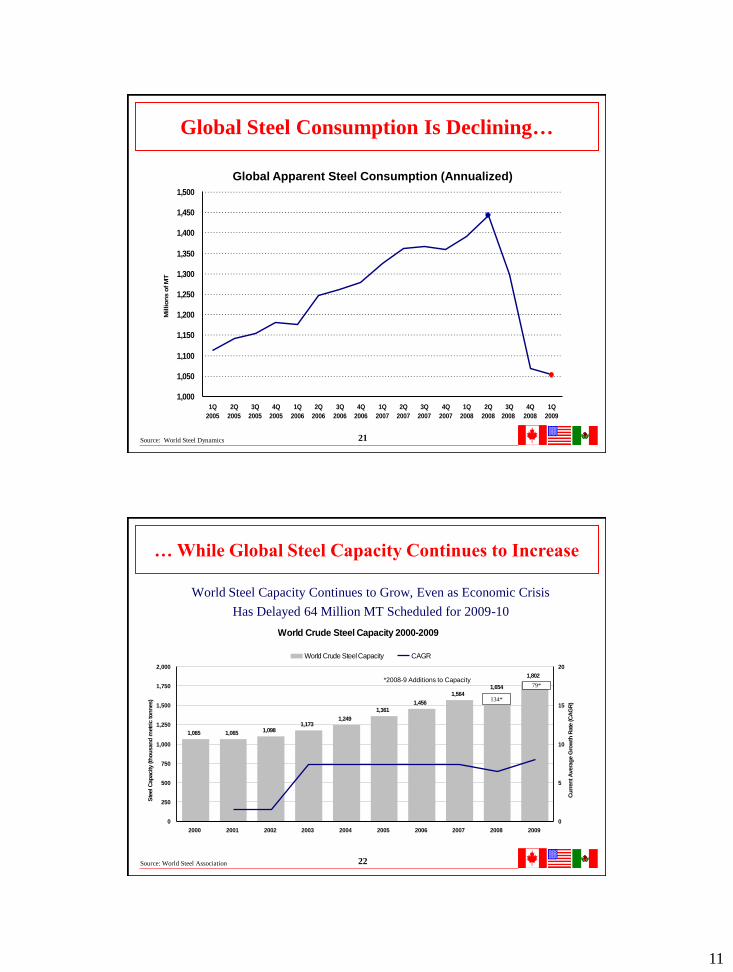

Global Apparent Steel Consumption (Annualized)

Source: World Steel Dynamics

Global Steel Consumption Is Declining…

22

World Steel Capacity Continues to Grow, Even as Economic Crisis

Has Delayed 64 Million MT Scheduled for 2009-10

Source: World Steel Association

… While Global Steel Capacity Continues to Increase

World Crude Steel Capacity 2000-2009

1,065 1,065 1,0981,173

1,249

1,361

1,456

1,564

1,802

1,654

0

250

500

750

1,000

1,250

1,500

1,750

2,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Ste

el C

ap

acity (th

ou

san

d m

etr

ic to

nn

es)

0

5

10

15

20

Cu

rren

t A

vera

ge G

row

th R

ate

(C

AG

R)

World Crude Steel Capacity CAGR

134*

*2008-9 Additions to Capacity79*

12

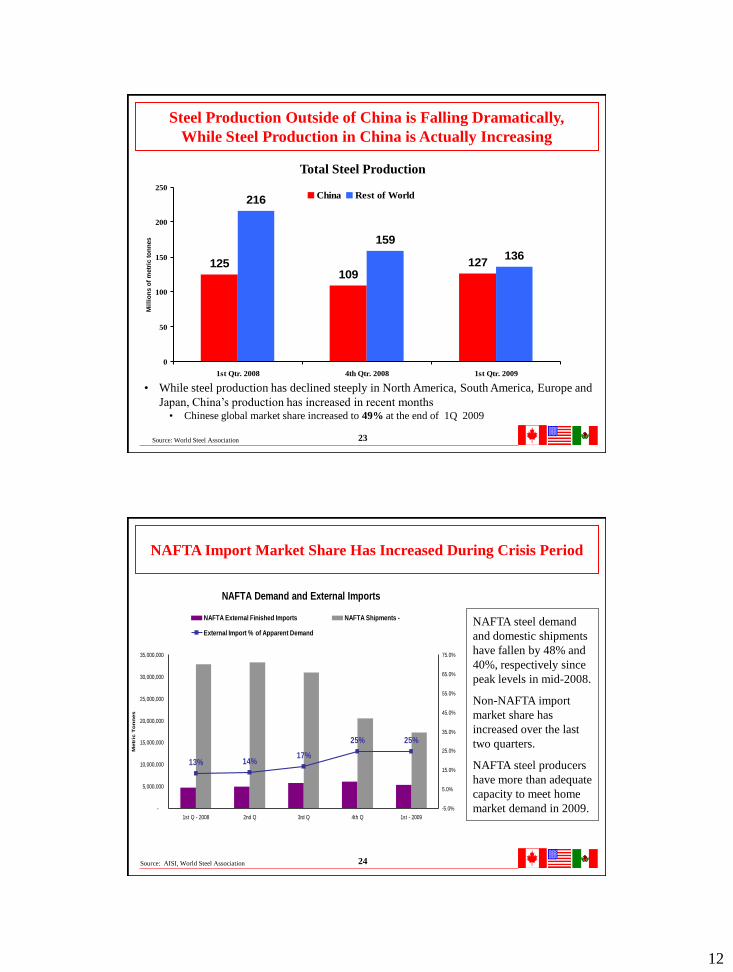

23

125109

127

216

159

136

0

50

100

150

200

250

1st Qtr. 2008 4th Qtr. 2008 1st Qtr. 2009

Mil

lio

ns o

f m

etr

ic t

on

nes

China Rest of World

Total Steel Production

Source: World Steel Association

Steel Production Outside of China is Falling Dramatically,

While Steel Production in China is Actually Increasing

• While steel production has declined steeply in North America, South America, Europe and

Japan, China‟s production has increased in recent months• Chinese global market share increased to 49% at the end of 1Q 2009

24Source: AISI, World Steel Association

NAFTA Import Market Share Has Increased During Crisis Period

NAFTA Demand and External Imports

13% 14%17%

25% 25%

-

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

35,000,000

1st Q - 2008 2nd Q 3rd Q 4th Q 1st - 2009

Metr

ic T

on

nes

-5.0%

5.0%

15.0%

25.0%

35.0%

45.0%

55.0%

65.0%

75.0%

NAFTA External Finished Imports NAFTA Shipments -

External Import % of Apparent Demand

NAFTA steel demand

and domestic shipments

have fallen by 48% and

40%, respectively since

peak levels in mid-2008.

Non-NAFTA import

market share has

increased over the last

two quarters.

NAFTA steel producers

have more than adequate

capacity to meet home

market demand in 2009.

13

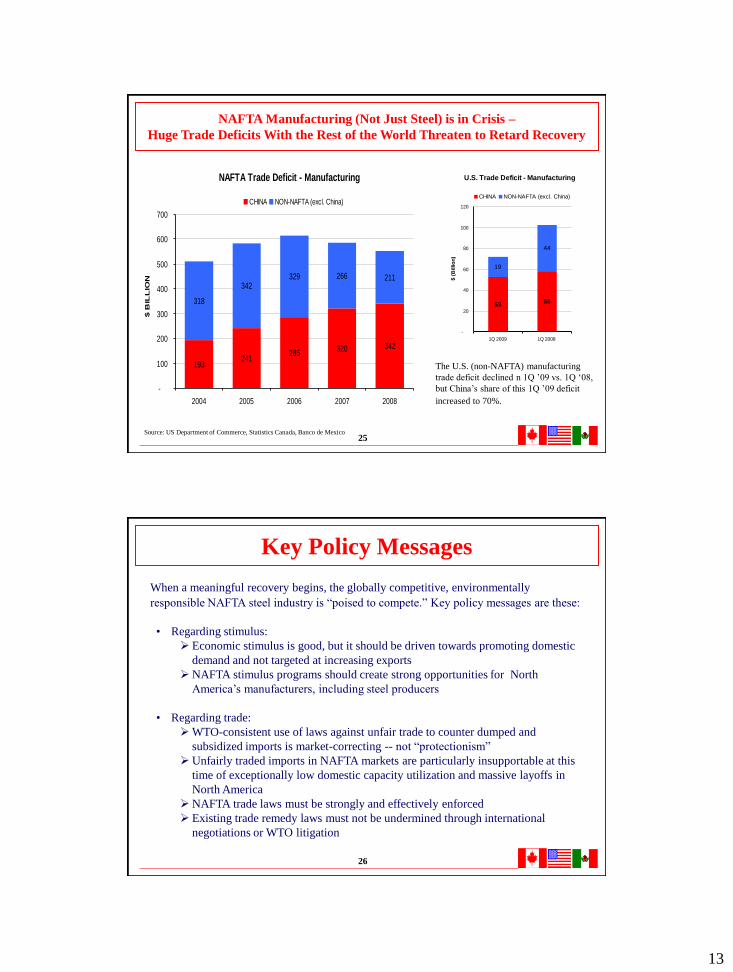

25Source: US Department of Commerce, Statistics Canada, Banco de Mexico

NAFTA Manufacturing (Not Just Steel) is in Crisis –

Huge Trade Deficits With the Rest of the World Threaten to Retard Recovery

NAFTA Trade Deficit - Manufacturing

193241

285320 342

318

342329 266 211

-

100

200

300

400

500

600

700

2004 2005 2006 2007 2008

$ B

ILL

ION

CHINA NON-NAFTA (excl. China)

U.S. Trade Deficit - Manufacturing

5358

19

44

-

20

40

60

80

100

120

1Q 2009 1Q 2008

$ (

Billio

n)

CHINA NON-NAFTA (excl. China)

The U.S. (non-NAFTA) manufacturing

trade deficit declined n 1Q ‟09 vs. 1Q „08,

but China‟s share of this 1Q ‟09 deficit

increased to 70%.

26

Key Policy Messages

When a meaningful recovery begins, the globally competitive, environmentally

responsible NAFTA steel industry is “poised to compete.” Key policy messages are these:

• Regarding stimulus:

Economic stimulus is good, but it should be driven towards promoting domestic

demand and not targeted at increasing exports

NAFTA stimulus programs should create strong opportunities for North

America‟s manufacturers, including steel producers

• Regarding trade:

WTO-consistent use of laws against unfair trade to counter dumped and

subsidized imports is market-correcting -- not “protectionism”

Unfairly traded imports in NAFTA markets are particularly insupportable at this

time of exceptionally low domestic capacity utilization and massive layoffs in

North America

NAFTA trade laws must be strongly and effectively enforced

Existing trade remedy laws must not be undermined through international

negotiations or WTO litigation