north slope gas & lng symposium -...

TRANSCRIPT

North Slope Gas & LNG Symposium

Anchorage, AK

August 5-9, 2013

North Slope Gas & LNG Symposium | © PFC Energy 2013 | Page 2 | August 2013

Conventional versus Unconventional Resources

1. Unconventional oil and gas are down the resource pyramid – more

difficult and expensive

2. Very few, if any, outright dry holes, but many disappointing wells that

fail to break even

3. Within an unconventional play, there is enormous variability between

winners from losers

4. Operational competence is important but rarely a source of long-term

comparative advantage as best practices and technology spread

easily

5. Value creation is mostly captured in the initial de-risking phases

6. Unconventional assets are extremely modular – companies can stop

and start without impacting project economics

North Slope Gas & LNG Symposium | © PFC Energy 2013 | Page 3 | August 2013

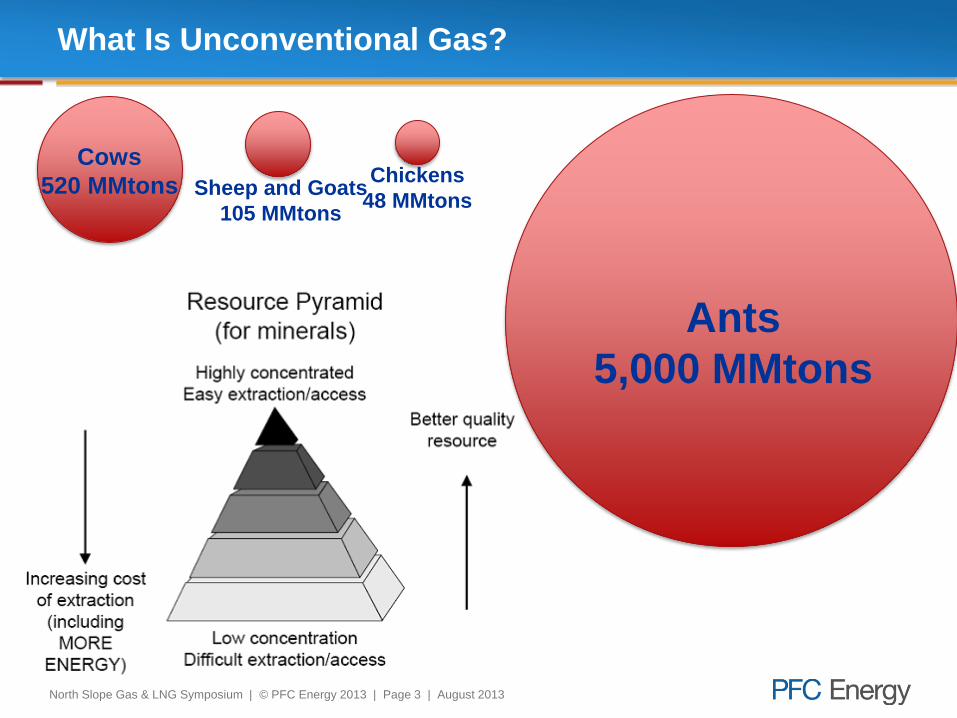

Chickens

48 MMtons Sheep and Goats

105 MMtons

Cows

520 MMtons

Ants

5,000 MMtons

What Is Unconventional Gas?

North Slope Gas & LNG Symposium | © PFC Energy 2013 | Page 4 | August 2013

Better Technology to the Rescue

The Solution

The Problem with Ants (and Unconventional Resources):

If you pick

them up and

eat them one at

a time, energy

output is

greater than

input.

Horizontal

Drilling

Life Stage and Value Creation Framework

Ingredients of Successful Plays

Skill Sets

Play Reviews

Table of Contents

North Slope Gas & LNG Symposium | © PFC Energy 2013 | Page 6 | August 2013

Plays pass through distinct life stages as they mature.

Pace of maturation varies tremendously

Life Stages of Unconventionals

Life Stages of Unconventional Plays

Prove It (Infancy)

~100 wells

Optimize It (Adolescence)

~1000-1500 wells

Standardize It (Adulthood)

Re-invent It (2nd Career)

Ga

ss

y

<

Flu

id T

yp

e>

O

ily

Granite Wash

Barnett

Tuscaloosa

Fayetteville

Bakken

Haynesville

DJ Niobrara Eagleford Oil

Eagleford

Gas

Utica

Bone Spring Smackover

Wolfcamp

Mississippian

Pinedale/

Jonah Marcellus

Cline

Monterey

PRB Niobrara

Uinta Tight Oil

North Slope Gas & LNG Symposium | © PFC Energy 2013 | Page 7 | August 2013

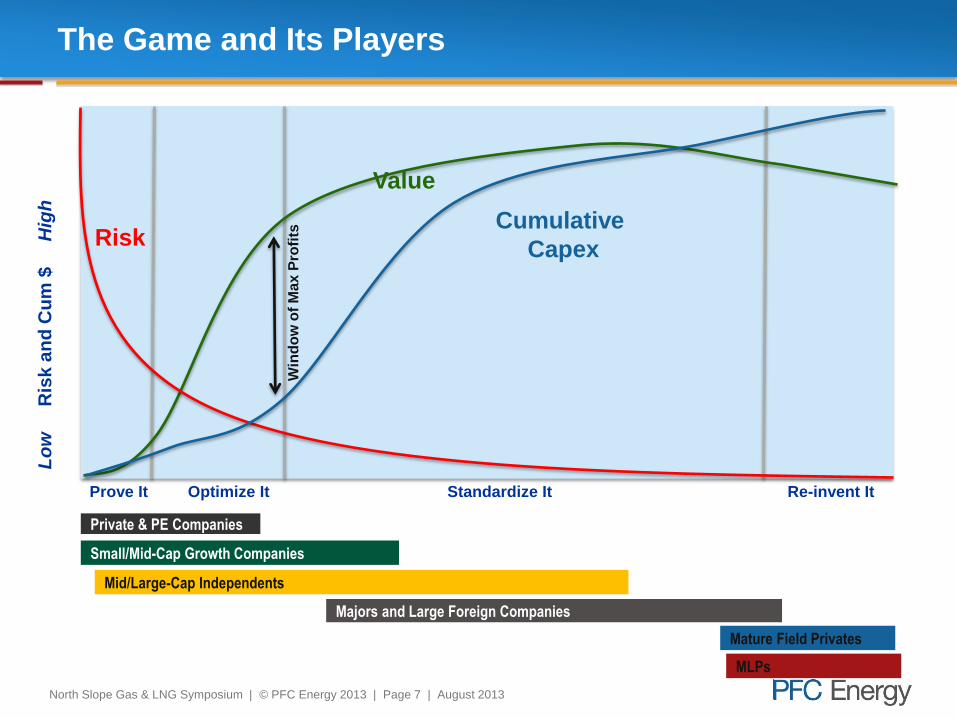

The Game and Its Players L

ow

R

isk

an

d C

um

$

H

igh

Risk

Prove It Optimize It Standardize It Re-invent It

Value

Cumulative

Capex

Private & PE Companies

Small/Mid-Cap Growth Companies

Mid/Large-Cap Independents

Majors and Large Foreign Companies

Mature Field Privates

MLPs

Win

do

w o

f M

ax P

rofi

ts

North Slope Gas & LNG Symposium | © PFC Energy 2013 | Page 8 | August 2013

Lo

w

R

isk a

nd

Cu

m $

Hig

h

The Game and Its Players

Prove It Optimize It Standardize It Re-invent It

High-grade Migration Low-grade

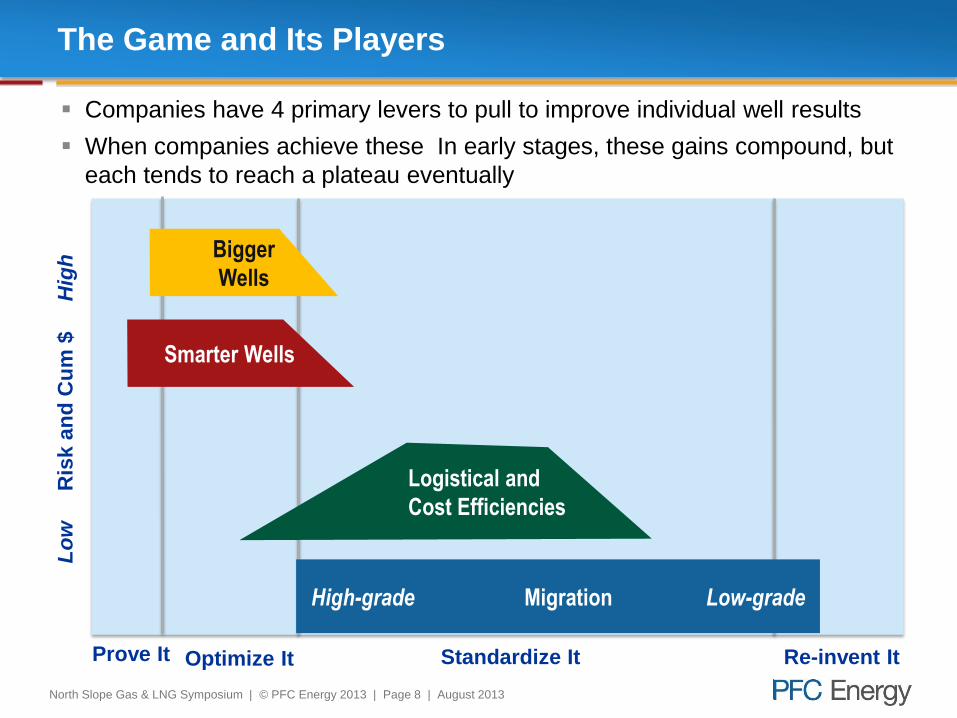

Companies have 4 primary levers to pull to improve individual well results

When companies achieve these In early stages, these gains compound, but

each tends to reach a plateau eventually

Bigger

Wells

Smarter Wells

Logistical and

Cost Efficiencies

Life Stage and Value Creation Framework

Ingredients of Successful Plays

Skill Sets

Play Reviews

Table of Contents

North Slope Gas & LNG Symposium | © PFC Energy 2013 | Page 10 | August 2013

Big 4 US Shale Gas Type Well Curves

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31 33 35 37 39 41 43 45 47

Production Month

(mcf/mo)

Haynesville Fayetteville Marcellus Barnett Core Barnett non-Core

• Petrophysics means that production is front-loaded

– Enhances NPV significantly by reducing payout time

• Profile creates treadmill effect, forcing constant reinvestment to avoid decline

Characteristics of Shale/Tight Gas Plays

Declines moderate, eventually

settling at 3-5% per year.

Well life often 30+ years.

There is debate about

industry estimates of well

reserves and life

PFC analysis suggests

– Core areas volumes are in

line with company claims

– Different areas within play

can diverge sharply

– Well life should be

measured in decades

Ⓒ PFC Energy 2012

North Slope Gas & LNG Symposium | © PFC Energy 2013 | Page 11 | August 2013

Three Kinds of Factors Seem Necessary for

Success

Geo-technical Potential

Macro Enablers

Pace Accelerants / Retardants

North Slope Gas & LNG Symposium | © PFC Energy 2013 | Page 12 | August 2013

The Top Ten Countries with Largest Shale Gas Resources

While there is a large range in the distribution of shale gas resources among

the top ten, no single country is overwhelmingly dominant.

900 - 1200

600 - 900

300 - 600

0 -

300

Shale Gas

(trillion cubic feet)

0

200

400

600

800

1,000

1,200

tcf Top 10 Countries By Technically

Recoverable Shale Gas Resources

Source: EIA Report, June 10 2013

North Slope Gas & LNG Symposium | © PFC Energy 2013 | Page 13 | August 2013

0

1

2

3

4

5

6

7

8

9

10C

anad

aU

nite

d K

ing

dom

Austr

alia

No

rwa

yU

nite

d S

tate

sG

reen

lan

dU

rug

uay

Qata

rU

AE

Fre

nch G

uia

na

Trin

ida

d &

Tob

ago

Ch

ileC

ypru

sC

hin

aM

ala

ysia

Bra

zil

Peru

Tha

iland

Om

an

Cu

ba

Tim

or-

Leste

Saud

i A

rabia

Co

lom

bia

Gha

na

Bahra

inR

ussia

Guyan

aM

adag

asca

rM

exic

oA

ze

rbaija

nE

qua

toria

l G

uin

ea

South

Afr

ica

Co

ngo

Bra

zzavill

eK

uw

ait

Phili

ppin

es

Gab

on

Mo

za

mb

iqu

eK

azakhsta

nK

urd

ista

n (

Iraq

)In

dia

Tan

za

nia

Ango

laT

urk

men

ista

nP

apu

a N

ew

Guin

ea

Le

ban

on

Boliv

iaV

ietn

am

Kenya

Ma

urita

nia

Indon

esia

Sao T

om

e &

Prin

cip

eA

lge

ria

Ug

and

aC

ote

d'Iv

oire

Arg

entina

Egypt

Surin

am

eC

am

bo

dia

Ira

qB

ang

lad

esh

Lib

ya

Pakis

tan

Myan

ma

rY

em

en

Ecu

ado

rS

outh

Suda

nIr

an

Ch

ad

Vene

zu

ela

Suda

nS

yri

aD

RC

Nig

eri

a

PRM 2013 Overall Risk Scores

Top 10 Shale Oil and Gas Resources: Span the Gamut

of Above-Ground Risk

Countries identified by the EIA with the largest unconventional resources vary

widely in terms of overall above-ground risk – but those in the top ten for both

shale gas and shale oil are mostly found in the top half of the risk range.

Low Risk

High Risk

Top 10 Shale Oil and Gas

Top 10 Shale Oil

Top 10 Shale Gas

North Slope Gas & LNG Symposium | © PFC Energy 2013 | Page 14 | August 2013

Top 10 Shale Gas Countries per EIA Study

Shale gas resources are concentrated in the countries with the most

manageable above-ground risk as well as strong infrastructure/service sector

capacity. The two main outliers are Argentina and South Africa.

Low Risk

Environment High Risk

Environment

Significant Service

Sector/Logistical

Capacity

Minimal Service

Sector/Logistical

Capacity

Canada

United States

Australia Argentina

Mexico

Brazil

China

Algeria

Russia

South Africa

Size of bubble denotes size of

resources according to the EIA

North Slope Gas & LNG Symposium | © PFC Energy 2013 | Page 15 | August 2013

Unconventional Success Has Resulted from a Complex

System of Favorable Factors

Critical Ingredients of the System Lwr-48 China Alaska Geo-

tech

Macro

Enabler

Pace

Governor

Rock characteristics/ resource base quality X

Resource base quantity X

Responsiveness to frack X

Well control X

Land Tenure/Parcel Size X

Local advocates and beneficiaries X

Lease structure forcing establishment of

production X

High number of operators/dispersion X

Company ability /willingness to spend significant

capital quickly X

High company risk appetite for trial and error X

Service sector availability X

Rapid transmission of learnings via leaky service

sector and external company orientation X

Pipes, Gathering to allow processing/delivery X

Water and other essential frac materials X

Skilled oil and gas labor pool X

Favorable natural gas prices and available markets X

Cooperative governments and incentives X

Life Stage and Value Creation Framework

Ingredients of Successful Plays

Skill Sets

Play Reviews

Table of Contents

North Slope Gas & LNG Symposium | © PFC Energy 2013 | Page 17 | August 2013

• What is Happening?

– Companies proving the reservoir will flow in likely commercial quantities.

• Major Activities

– Geoscience/ Basin studies

– Land acquisition

– Pilot wells

• Strategies for Success: Violate the Usual Rules of Oil and Gas

– Run a Science Experiment

– Attract other operators

– Capture acreage even where geo scientists don’t suspect sweet spot

– Select service sector partner based on science/experience, not cost

• Key Metrics to Evaluate

– $/acre of land acquired

– Quantity and distribution of leasehold

– Reservoir information derived from each drilling dollar

Stage 1: Prove It

North Slope Gas & LNG Symposium | © PFC Energy 2013 | Page 18 | August 2013

• What is Happening?

– Derive the optimal recipe for drilling and fracing wells in this particular

play

– Establish the limits and quality map of the play

• Major Activities

– Try everything

– Gain scale & scope

– Ramp drilling/create hubs

• Strategies for Success: Creative Engineering for Peak Efficiency

– Integrate diverse data streams and draw correct conclusions

– Orient externally: collect and share information and scout heavily

– Choose multiple service sector companies to maximize creativity

• Key Metrics to Evaluate

– $/acre paid during consolidation of companies w/ weaker results

– Change in standard deviation of frac techniques and results

– Slope of IP evolution

Stage 2: Optimize It

North Slope Gas & LNG Symposium | © PFC Energy 2013 | Page 19 | August 2013

• What is Happening?

– Play is turned from potential into cash flow by massive investment with

cookie cutter approach

• Major Activities

– Large, steady programs

– Focus on above ground efficiencies

• Strategies for Success: Standardize to Grind Down Unit Costs

– Coordinate chain of resources and companies flawlessly

– Ensure ancillary infrastructure such as midstream and transport

– Apply no-frills approach to service partners & seek volume discount

• Key Metrics to Evaluate

– Cost of capital and free cash flow at bottom of cycle

– Spud to market timing efficiency

– Speed of convergence vs. peers and predictability of well results

– Sequential unit cost reduction (opex and capex)

Stage 3: Industrialize It

North Slope Gas & LNG Symposium | © PFC Energy 2013 | Page 20 | August 2013

• What is Happening?

– Rejuvenate the play and manage its operations

• Major Activities

– Transfer of ownership

– Choose between three paths

Downspace further Rework and refrac Expansion

• Strategies for Success: Sweat the Small Stuff… and Bring

Imagination

– Keep it cheap and focus

– Leverage existing well bores, infrastructure, and field personnel

– Find new zones and new technology

• Key Metrics for Investors to Evaluate

– $/boe attributed to probables and possibles

– Use of existing wellbores and infrastructure

– Success rate in finding overlooked sweet spots

– Change in rate of base decline

Stage 4: Rethink It

North Slope Gas & LNG Symposium | © PFC Energy 2013 | Page 21 | August 2013

• All of these athletes won gold medals in London. Guess the sport.

What Does It Take to Win?

Deep excellence comes from thorough-going specialization, but that also

shapes the entity in a way that makes it difficult to succeed in a different contest.

• If the London gold medal decathlete had entered all the event finals,

he would have placed last in 8 and in the bottom half of the other two.

• Retraining is difficult (think Michael Jordan in baseball or Lance

Armstrong in the NYC marathon).

100m Sprint

Marathon

Weightlifting

Life Stage and Value Creation Framework

Ingredients of Successful Plays

Skill Sets

Play Reviews

Table of Contents

North Slope Gas & LNG Symposium | © PFC Energy 2013 | Page 23 | August 2013

Lower 48 Map of Producing Wells

Woodford

Fayetteville

Marcellus

Eagleford

Bakken

Haynesville

Barnett

North Slope Gas & LNG Symposium | © PFC Energy 2013 | Page 24 | August 2013

Lower 48 Shale Gas is Primary Contributor to Growth

Marcellus production, primarily in Pennsylvania, is projected to be a

key driver of growth in domestic natural gas through 2020.

67.669.7 70.6

72.4 72.1 71.8 72.173.9

75.377.3

79.280.9

82.283.6 83.8 84.4 84.7 85.5 85.8 86.3

0

10

20

30

40

50

60

70

80

90

100

Ja

n-1

1

Ap

r-11

Ju

l-11

Oct-

11

Ja

n-1

2

Ap

r-1

2

Ju

l-1

2

Oct-

12

Ja

n-1

3

Ap

r-1

3

Ju

l-1

3

Oct-

13

Ja

n-1

4

Ap

r-1

4

Ju

l-1

4

Oct-

14

Ja

n-1

5

Ap

r-1

5

Ju

l-1

5

Oct-

15

Ja

n-1

6

Ap

r-1

6

Ju

l-1

6

Oct-

16

Ja

n-1

7

Ap

r-1

7

Ju

l-1

7

Oct-

17

Ja

n-1

8

Ap

r-1

8

Ju

l-1

8

Oct-

18

Ja

n-1

9

Ap

r-1

9

Ju

l-1

9

Oct-

19

Ja

n-2

0

Ap

r-2

0

Ju

l-2

0

Oct-

20

Production in bcf/d

Lwr-48 Gross Natural Gas Production Estimate

Haynesville DUC

Marcellus DUC

Marcellus PA

Marcellus WV

Eagleford

Granite Wash

Haynesville

Woodford

Pinedale

Fayetteville

Barnett

GOM Deepwater

GOM Shelf

CBM

Oil (Other)

Gassy Oil (Other)

Wet Gas (Other)

Dry Gas (Other)

Total

North Slope Gas & LNG Symposium | © PFC Energy 2013 | Page 25 | August 2013

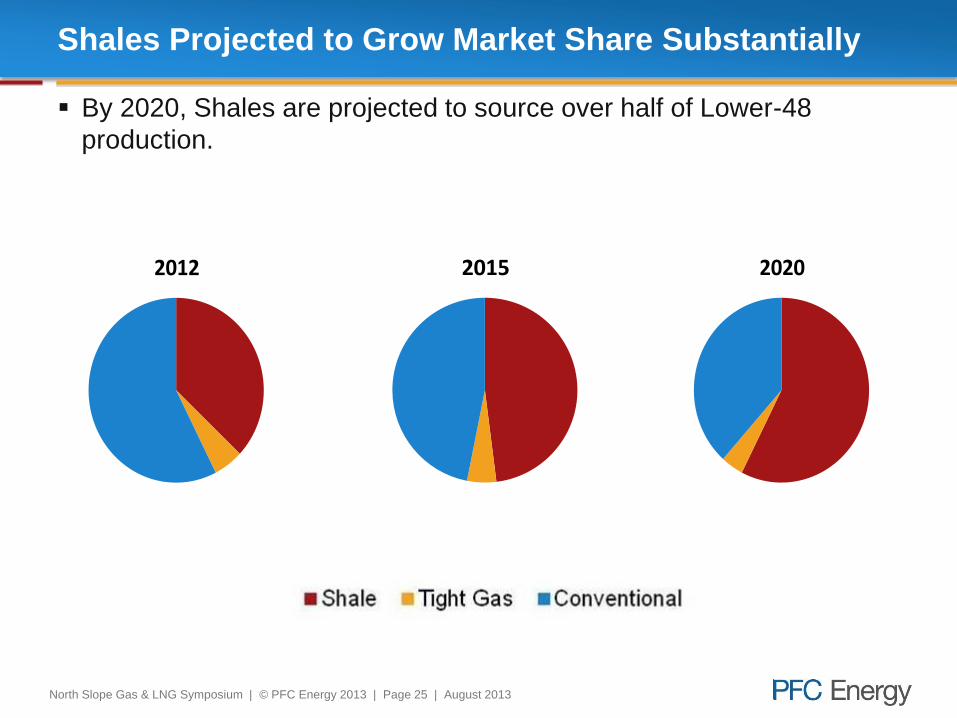

Shales Projected to Grow Market Share Substantially

By 2020, Shales are projected to source over half of Lower-48

production.

2012 2015 2020

Haynesville Shale Play

North Slope Gas & LNG Symposium | © PFC Energy 2013 | Page 27 | August 2013

Haynesville: Key Facts

Life Cycle Though the Haynesville has a large inventory of wells still to be

drilled, low gas prices are not incentivizing operators to return to

the play. Thus, though it has quite mature technologically, it may

never reach its full potential.

Well Count By March of 2013, nearly 3,500 wells were producing from the

Haynesville.

Competitive

Landscape

Over 40 operators have producing assets, though the larges six

operators hold nearly 50% of the wells

Oil vs. Gas Haynesville production is more than 98% gas.

Sweet Spot Activity in the sweet spot of the play has nearly exhausted the

inventory of best acreage. Given the current pricing environment,

focused activity is expected to continue.

Productivity

Distribution

1st quintile wells are 1.5 times as productive as 2nd quintile wells

and 4.3 times more productive than 5th quintile.

Type Curve Trends Minor improvements in peak production are still observed, while

newer vintage wells outperform older wells nearly 7-to-1 after 12

months (2011 vs. 2007).

North Slope Gas & LNG Symposium | © PFC Energy 2013 | Page 28 | August 2013

Highly Concentrated Area of Peak Productivity

Centralized Activity

Most efficient wells are concentrated geographically in a very small

area in LA. Rock productivity decreases significantly in a radial

manner as operators have delineated the expanses of the play.

North Slope Gas & LNG Symposium | © PFC Energy 2013 | Page 29 | August 2013

Peak Gas Production Has Hit Plateau

Productivity in the play is at best stagnant being that it has not

improved and operator results are converging on the plays inherent

average. Additionally recent trends have shown operators are high-

grading within their individual portfolios which further supports a

bearish outlook. Avg. Peak mcf/d

Avg. Peak mcf/d

North Slope Gas & LNG Symposium | © PFC Energy 2013 | Page 30 | August 2013

Lateral Lengths Showing Incremental Gains Only

Despite operators having determined an optimal lateral length for the

play during attractive gas prices. The decline in pricing has seen

operators attempt multilaterals as an effort to buoy economic results.

Lateral Length (ft)

Lateral Length (ft)

North Slope Gas & LNG Symposium | © PFC Energy 2013 | Page 31 | August 2013

Well Productivity per Lateral Foot is Highly Predictable

Resulting from longer laterals and stagnant peak rates, peak

productivity has slightly declined. Operators are drilling more lower

quintile assets showing possible exhaustion of higher quintile sites.

mcf/d/latft mcf/d/latft

Marcellus Shale Play

North Slope Gas & LNG Symposium | © PFC Energy 2013 | Page 33 | August 2013

Marcellus: Play Conclusions

Life Cycle Developing in two main sub-regions, operators have found their

best results in the northeast and southwest extents of

Pennsylvania. Though much of the geographical footprint remains

undeveloped, the core areas are clearly seeing standardized

operations.

Well Count The latest data, capturing the majority of the play through the end

of 2012, accounted for over 5,600 producing wells.

Competitive

Landscape

130 operators generate volumes from the Marcellus, though only

seven operators have more than 200 wells

Oil vs. Gas Though some operators have found substantial NGL volumes,

Marcellus production is more than 96% gas at the wellhead

Sweet Spot Operators have found the most economic production in the

northeast and southwest portions of Pennsylvania.

Productivity

Distribution

1st quintile wells are 2 times as productive as 2nd quintile wells and

8 times more productive than 5th quintile.

Type Curve Trends Type curves have shown no meaningful improvements in the past

3 years.

North Slope Gas & LNG Symposium | © PFC Energy 2013 | Page 34 | August 2013

Marcellus: Map of Peak/Latft Gas Quintiles

Despite the large areal extent of the play, high quality wells are

concentrated in the northeast and southwest regions of the play.

Operators continue to delineate the most productive areas of the

play, leaving the middle portion of Pennsylvania largely undeveloped.

North Slope Gas & LNG Symposium | © PFC Energy 2013 | Page 35 | August 2013

Marcellus: Peak Gas

Peak rates have shown incredible consistency since early 2012,

though the variance in peaks has increased. Omitting the “super

wells”, mainly drilled by Cabot and EQT, the play’s average peak has

slightly declined.

Avg Peak mcf/d

North Slope Gas & LNG Symposium | © PFC Energy 2013 | Page 36 | August 2013

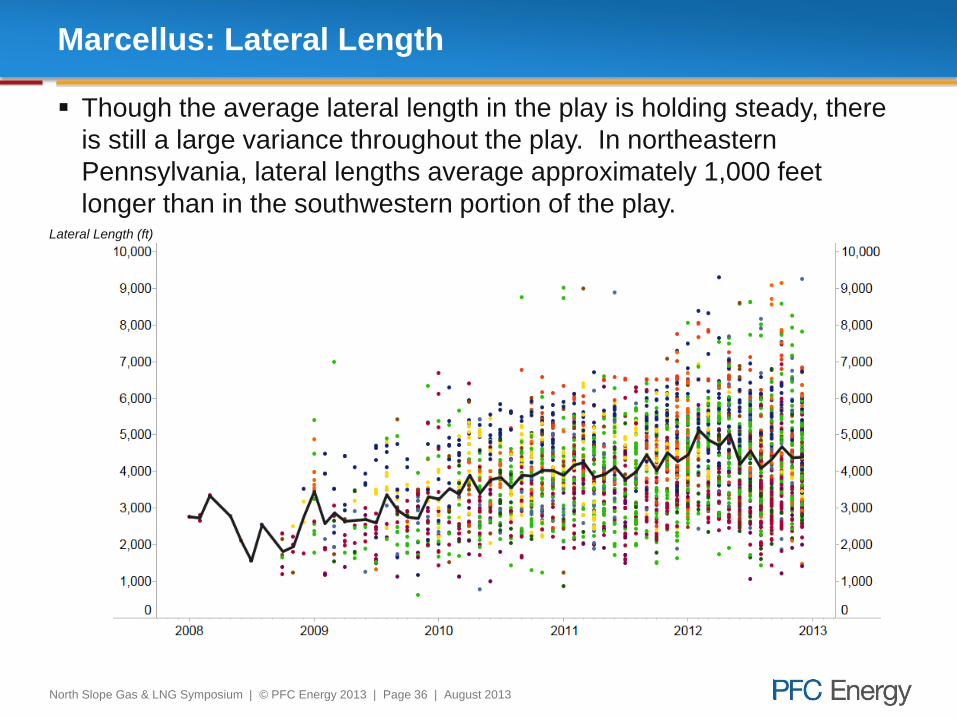

Marcellus: Lateral Length

Though the average lateral length in the play is holding steady, there

is still a large variance throughout the play. In northeastern

Pennsylvania, lateral lengths average approximately 1,000 feet

longer than in the southwestern portion of the play. Lateral Length (ft)

North Slope Gas & LNG Symposium | © PFC Energy 2013 | Page 37 | August 2013

Marcellus: Peak/Latft Gas

The natural result of peak production rates and lateral lengths both

holding steady is that peak per lateral foot has been flat as well.

Operators have largely delineated and held quality acreage and are

content to develop those areas and hope for higher gas prices to

justify more exploration. Avg Peak mcf/d/1000latft

Barnett Shale Play

North Slope Gas & LNG Symposium | © PFC Energy 2013 | Page 39 | August 2013

Barnett: Key Facts

Life Cycle The Barnett is well into the optimization phase, and may be

experiencing some sweet spot exhaustion. Liquids production in

the northern portion counties have breathed new life into the play.

Well Count Since 2001, over 17,000 wells have begun production in the play.

Competitive

Landscape

Since 2008, over 130 operators have drilled at least one active

well. However, of the 9,000 wells drilled since 2008, Chesapeake,

Devon, EOG, and ExxonMobil combine to account for 6,000 of

them.

Oil vs. Gas Over 91% of the wells in the Barnett produce dry gas (wellhead

volumes >90% gas at 6-1 conversion). However, in the northern

reaches of the play, liquids production has been increasing.

Sweet Spot The sweet spot in parts of Wise, Johnson, and Tarrant counties

have seen the most activity, though activity in all three has been

decreasing from the peak in 2008.

Productivity

Distribution

1st quintile wells in the Barnett are nearly twice as productive as 2nd

quintile wells, and are 8 times as productive as 5th quintile wells.

Type Curve Trends 2012 was the first year the Barnett type curves did not improve.

North Slope Gas & LNG Symposium | © PFC Energy 2013 | Page 40 | August 2013

Core Located on Eastern Edge of Play, With

Productivity Delineations Clearly Visible to the West

As the oldest unconventional play in the US, the Barnett has seen

over 18,000 wells produce volumes. Though overall production has

grown, an exhaustion of best drill sites and a reduction in activity

point to a possible decline in production.

North Slope Gas & LNG Symposium | © PFC Energy 2013 | Page 41 | August 2013

Peak Production Rates Still Holding Steady

As operators are unable to drill top producing wells, overall gas

productivity has experienced a significant decline in recent years.

Avg. Peak mcf/d

North Slope Gas & LNG Symposium | © PFC Energy 2013 | Page 42 | August 2013

Lateral Lengths Continue to Grow, Despite Play’s Age

Lateral lengths in the play have been trending upwards, as operators

seek to generate more production per well bore by drilling larger

wells. The current average is nearly 4,000 feet, though some

operators have clearly experimented with multi-laterals Ft

North Slope Gas & LNG Symposium | © PFC Energy 2013 | Page 43 | August 2013

Production per Lateral Foot Falling, Partly Driven by

Longer Lateral Lengths

As operators drill longer laterals with lower peak gas rates, the

compounding effect has eroded overall productivity in the play. As

sweet-spot exhaustion becomes more of an issue in the play,

operators will have to drill a larger number of wells to compensate for

lower productivity.

Avg. Peak

mcf/d/1000 lat ft

Fayetteville Shale Play

North Slope Gas & LNG Symposium | © PFC Energy 2013 | Page 45 | August 2013

Fayetteville: Key Facts

Life Cycle With the play dominated by one operator, Southwestern,

standardized operations have been seen for several years.

However, Southwestern appears to have recently ceased acreage

holding activities and is now focusing on infill drilling

Well Count 5,500 wells currently generate production in the Fayetteville

Competitive

Landscape

Southwestern rules the play with nearly 60% of producing assets.

Oil vs. Gas No liquids are found in the Fayetteville

Sweet Spot Several areas of highly productive rock have been identified,

though no core sweet spot has been determined.

Productivity

Distribution

1st quintile wells are 1.5 times more productive than 2nd quintile

wells and five times as productive as 5th quintile.

Type Curve Trends Type curves have shown no significant improvements since 2010,

though if Southwestern’s acreage holding is complete, high-

grading is expected.

North Slope Gas & LNG Symposium | © PFC Energy 2013 | Page 46 | August 2013

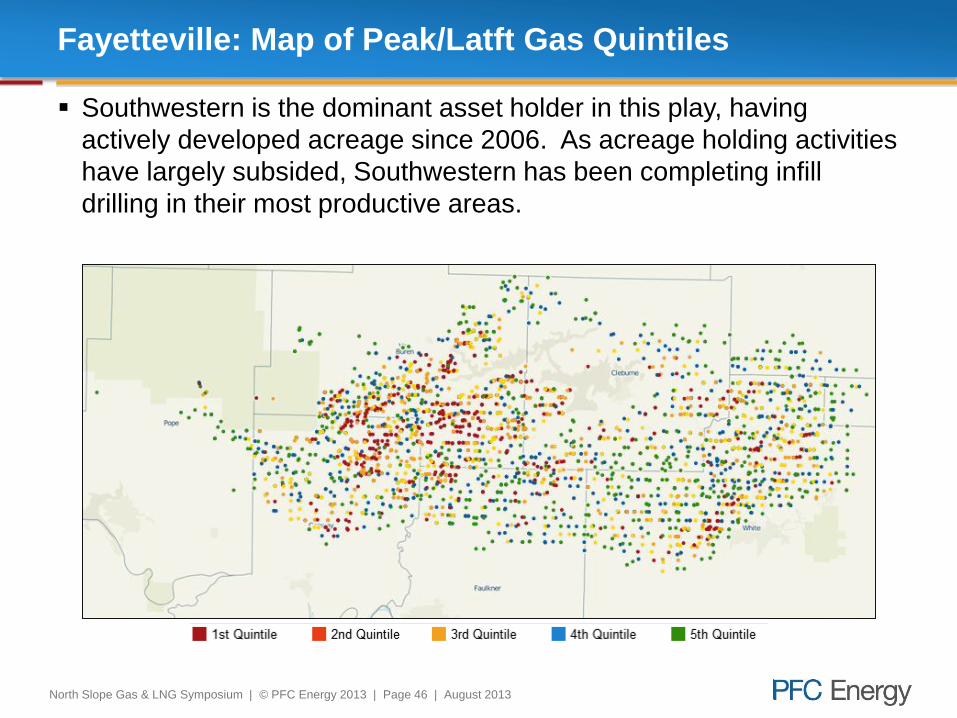

Fayetteville: Map of Peak/Latft Gas Quintiles

Southwestern is the dominant asset holder in this play, having

actively developed acreage since 2006. As acreage holding activities

have largely subsided, Southwestern has been completing infill

drilling in their most productive areas.

North Slope Gas & LNG Symposium | © PFC Energy 2013 | Page 47 | August 2013

Fayetteville: Peak Gas

Operators have shown small but steady improvements in peak gas

rates. Additionally, the variance in peak rate is decreasing, implying

operators have been at least modestly successful in high-grading

efforts.

Avg. Peak mcf/dAvg. Peak mcf/d

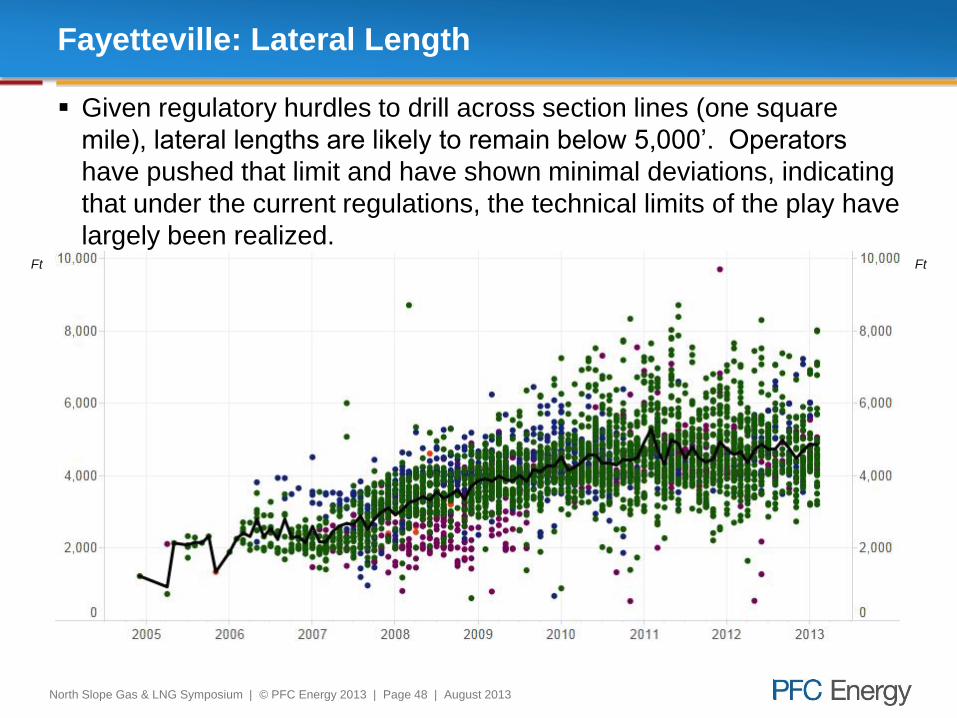

North Slope Gas & LNG Symposium | © PFC Energy 2013 | Page 48 | August 2013

Fayetteville: Lateral Length

Given regulatory hurdles to drill across section lines (one square

mile), lateral lengths are likely to remain below 5,000’. Operators

have pushed that limit and have shown minimal deviations, indicating

that under the current regulations, the technical limits of the play have

largely been realized. Ft Ft

North Slope Gas & LNG Symposium | © PFC Energy 2013 | Page 49 | August 2013

Fayetteville: Peak/Latft Gas

Peak productivity has remained predictable, and in much the same

as peak rates and lateral lengths, the variability in results has

decreased. As Southwestern continues a methodological

development of the play, results will maintain their predictability.

Avg. Peak

mcf/d/1000 latft

Avg. Peak

mcf/d/1000 latft

Pinedale-Jonah Play

North Slope Gas & LNG Symposium | © PFC Energy 2013 | Page 51 | August 2013

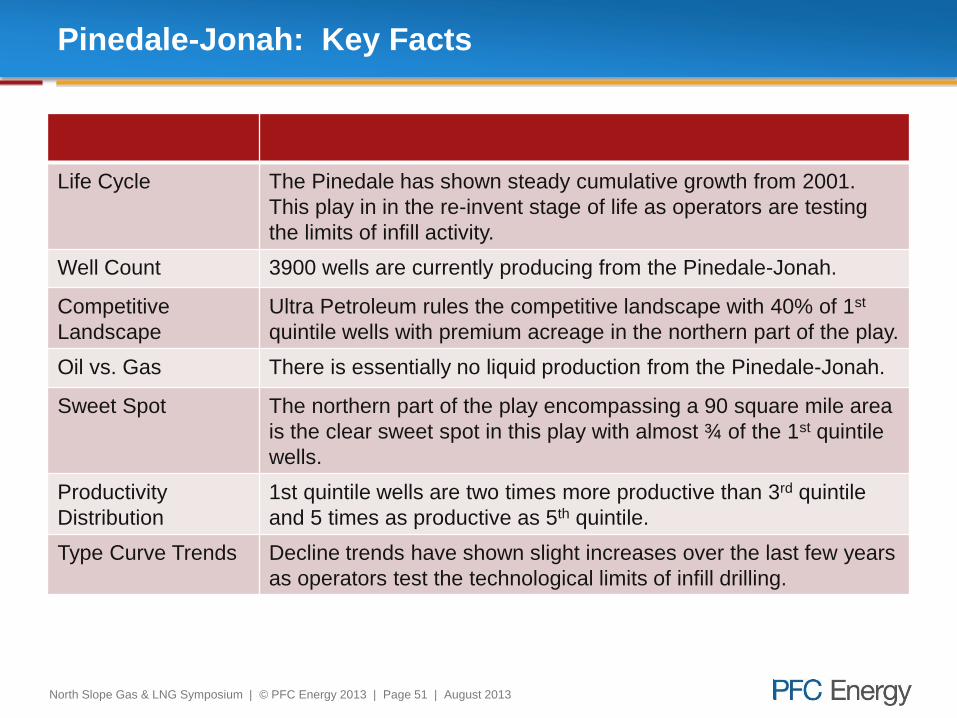

Pinedale-Jonah: Key Facts

Life Cycle The Pinedale has shown steady cumulative growth from 2001.

This play in in the re-invent stage of life as operators are testing

the limits of infill activity.

Well Count 3900 wells are currently producing from the Pinedale-Jonah.

Competitive

Landscape

Ultra Petroleum rules the competitive landscape with 40% of 1st

quintile wells with premium acreage in the northern part of the play.

Oil vs. Gas There is essentially no liquid production from the Pinedale-Jonah.

Sweet Spot The northern part of the play encompassing a 90 square mile area

is the clear sweet spot in this play with almost ¾ of the 1st quintile

wells.

Productivity

Distribution

1st quintile wells are two times more productive than 3rd quintile

and 5 times as productive as 5th quintile.

Type Curve Trends Decline trends have shown slight increases over the last few years

as operators test the technological limits of infill drilling.

North Slope Gas & LNG Symposium | © PFC Energy 2013 | Page 52 | August 2013

Pinedale-Jonah: Map of Peak/Boe Gas Quintiles

The Pinedale field dominates this play with almost 75% of the 1st

quintile wells. Ultra Petroleum operates the majority of the Pinedale

wells, while Encana is the dominant operator in the Jonah.

Pinedale

Jonah

North Slope Gas & LNG Symposium | © PFC Energy 2013 | Page 53 | August 2013

Pinedale-Jonah: Peak Gas

As the play has been experiencing infill drilling, peak rates have

slightly declined due to communication and interference between

wells. This, combined with low gas prices, has led to a significant

reduction in activity in the play.

Avg. Peak mcf/d Avg. Peak mcf/d