northeast forum on regional energy solutions … investigation/eversource...northeast forum on...

TRANSCRIPT

1

Northeast Forum on Regional Energy Solutions Remarks by Gordon van Welie, President & CEO, ISO New England

April 23, 2015

Introduction

My name is Gordon van Welie. I am president and chief executive officer of ISO New England. We are

responsible for operating New England’s power grid and wholesale electricity markets, and planning to

ensure the future reliability of the system.

Thank you for inviting me to participate in the Northeast Forum on Regional Energy Solutions.

ISO New England has a long-standing relationship with the New England Governors and is committed to

working with the states as they formulate solutions to the region’s energy infrastructure needs.

Dramatic Transformation of the Generation Fleet

The region is undergoing a dramatic transformation of the generation fleet, and this is due to a number

of economic and environmental factors. (See Slide 2)

Over the last 15 years, the region has seen a major shift toward natural-gas-fired generation. Last year,

we produced nearly half of our electricity with natural gas, up from 15% in 2000.

The combined use of coal and oil has fallen dramatically over the same period (from 40% to 6%), and

these resources only operate during the summer when electricity demand is highest, and in the winter

when natural gas pipelines are constrained.

The shift in New England’s resource mix is the result of two primary factors. Low-priced natural gas, for

most of the year, is making it uneconomic for coal and oil plants to operate in the energy market. And

policymakers are seeking to reduce carbon and other power-plant emissions through environmental

policies.

These factors are driving major generator retirements in the region. In the past few years, 10% of our

generating capacity announced plans to retire within five years. This includes coal, oil and nuclear power

plants. And that is just the beginning.

Many more coal- and oil-fired power plants (another 6,000 MW) are “at risk” of retirement.

The timeframe for these retirements is uncertain and will depend on investments in transmission and

gas pipelines, as well as environmental policies, but our best guess is that this will occur over the next

decade or so.

This will only increase our dependence on natural gas for power generation.

As the generation fleet turns over, we recognize that the states are looking to influence the future

resource mix toward energy efficiency, distributed resources, and non-carbon renewable resources.

000029

Docket No. IR 15-124 Comments of Eversource Energy

Attachment 3 Page 1 of 13

2

The Future Resource Mix

The ISO’s markets and planning processes fully recognize the states’ investments in energy efficiency.

According to our energy-efficiency forecast, overall electricity demand in New England has essentially

flattened over the next decade, and this is largely because of the billions of dollars being spent by the

states on energy-efficiency measures.

As you consider further resource needs, it appears your clear priority is to develop non-carbon,

renewable energy resources, and this is driving significant investments in solar photovoltaics (PV) and

wind.

Solar PV resources have been coming online rapidly and we expect the current amount (900 MW) to

nearly triple within a decade (2,400 MW by 2024).

Wind power supplies about 1% of our annual electricity needs, but almost half of proposed generation

in New England is wind power. Many of these projects are proposed to be built in areas where the

transmission system is already constrained, and some in areas where there is no transmission at all.

This is like building a manufacturing plant in an area where there is no transportation system to move

the products to market.

If the New England states want to improve the deliverability of existing wind resources, develop new

wind resources, or access more hydropower from eastern Canada, then they will need to invest in

additional electric transmission to deliver that energy, which is largely sourced in the north, to where it

is consumed, which for the most part is in southern New England.

I am aware that the southern New England states are evaluating a solicitation for projects that could

address some of these clean energy goals.

(See Slide 3) There are a number of transmission proposals by private developers vying to move clean

energy supplies from Newfoundland and Labrador, Québec, and northern New England, particularly

Maine, to southern New England. Some of these transmission proposals, as well as other proposals, may

come forward in the states’ solicitation. While these are not considered reliability projects, the ISO’s role

is to study these proposals to ensure they can interconnect reliably.

The projects listed on Slide 3 reflect publicly available information as of November 2013 and are not

intended to be a comprehensive list of the elective transmission proposals in our interconnection queue.

They are intended to be representative of the types of transmission projects emerging inside and

outside the region in response to the states’ clean energy goals.

While the region is transitioning to more renewable energy, we are experiencing environmental and

cost impacts associated with constraints on the natural gas pipeline system. These impacts have been

most severe during the last few winters.

000030

Docket No. IR 15-124 Comments of Eversource Energy

Attachment 3 Page 2 of 13

3

Natural Gas Pipeline Infrastructure

Because natural gas represents such a large portion of the region’s generating fleet, availability of

natural gas for power generation has a profound impact on grid reliability and production costs.

New England has limited natural gas pipeline infrastructure serving the region and these pipes are

reaching maximum capacity, especially during the winter months when demand for natural gas to heat

homes and businesses is at its highest.

New England’s natural gas infrastructure has not kept pace with the tremendous growth in natural gas-

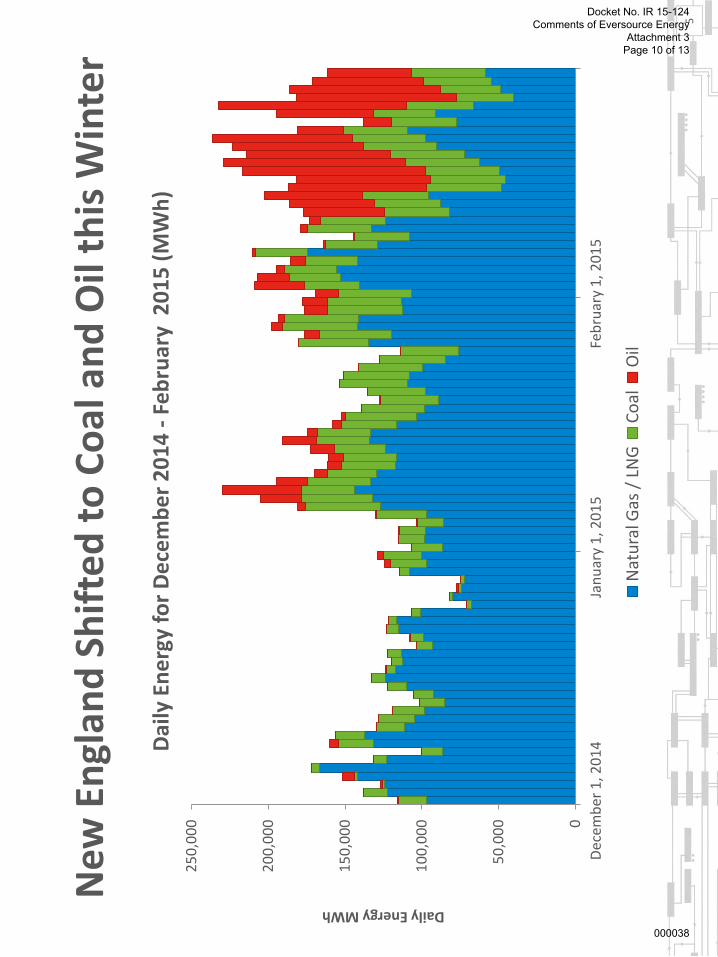

fired generation and the increasing demand for natural gas as a heating fuel. (See Slide 4)

When natural gas supply to generators is constrained, the ISO must commit other generating resources

to maintain system reliability, and these resources are often coal- and oil-fired power plants. Coal and

oil have made vital contributions to the fuel mix during high gas demand days over the past few winters.

(See Slide 5)

These resources are still important to keeping the lights on, but they are retiring. And we understand

that New England policymakers do not like the increase in emissions that occurs when they run, or the

impact on electricity prices resulting from high fuel costs.

Impact on Natural Gas and Wholesale Electricity Prices

Over the last three winters, New England experienced significant price spikes in both natural gas and

wholesale electricity. (See Slide 6)

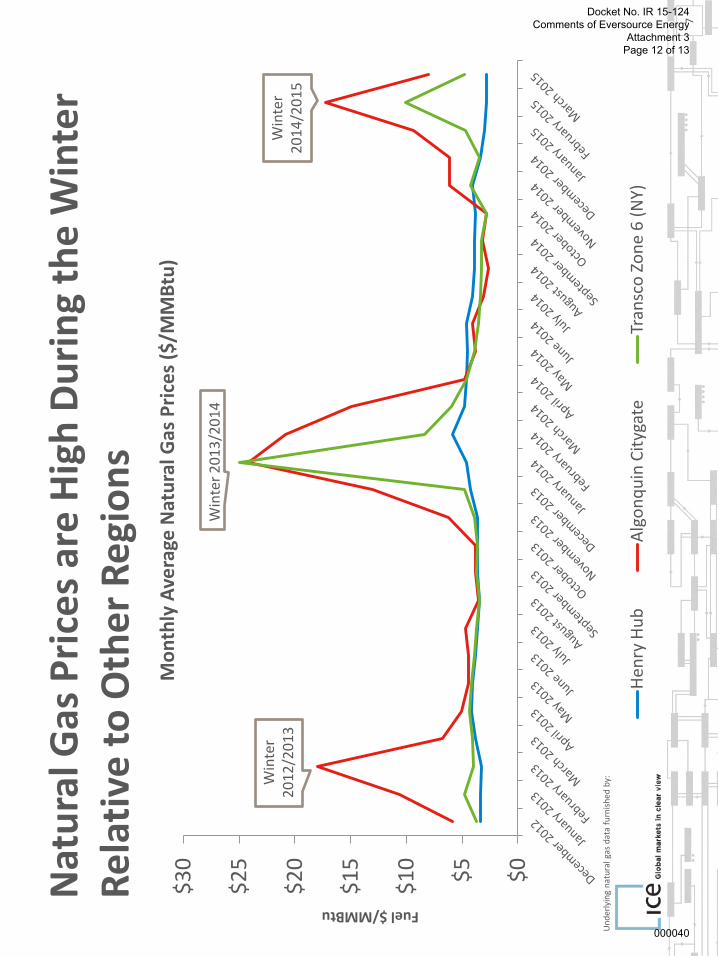

Constraints on the natural gas pipeline system drove gas prices to record levels. This volatility in the

New England gas markets was the direct cause of volatility in the wholesale electricity markets.

Natural gas prices were less volatile this winter, but we still saw many days in February with spot gas

prices in the $20 – $30 per MMBtu range, which is very high by historical standards. And significantly

higher than areas of the country where the gas system is unconstrained. (See Slide 7)

This week, the U.S. Department of Energy released the first installment of the Quadrennial Energy

Review (QER), which shines a spotlight on natural gas infrastructure constraints in the northeast.

The QER points out that despite large volumes of gas available from the Marcellus Shale in nearby

Pennsylvania, pipeline constraints restrict sufficient supplies of this gas from reaching New England,

putting upward pressure on gas prices in the wintertime. The New York metropolitan area, by contrast,

has alleviated some of the winter congestion it faced by adding new pipeline capacity.

This winter, the region’s power grid operated well through cold weather and, due to a confluence of

regional and global factors, natural gas and wholesale electricity prices were lower on average than last

winter.

000031

Docket No. IR 15-124 Comments of Eversource Energy

Attachment 3 Page 3 of 13

4

That said, February 2015 still ranked as the third-highest monthly average for wholesale electricity

prices in New England since 2003. The highest and second-highest prices were logged the previous

winter, during January and February 2014.

Why were prices less volatile this winter? (See Slide 8)

A number of factors helped ensure power system reliability and keep price volatility in check this winter.

First, we ran a winter reliability program that provided incentives for power plants to have oil inventory

stored on site, or to have a contract for LNG deliveries to supplement pipeline gas supplies before the

start of the winter. This meant that resources had the fuel they needed to run when dispatched by the

ISO.

Second, December was mild, and the coldest winter weather didn’t arrive until February, when days

were longer and electricity consumption was down.

High natural gas prices last winter and high forward prices for delivery this winter attracted liquefied

natural gas (LNG) supplies to New England.

Global oil prices dropped dramatically, making it more economical at times to burn oil than natural gas.

This dampened gas and electricity price volatility.

And, finally, energy-efficiency measures promoted by the states helped reduce total power consumption

and peak demand. [Our latest forecast shows energy efficiency flattening peak demand growth in the

wintertime.]

The region benefited from the availability of LNG resources this winter, but there is no guarantee that

those same shipments will arrive next winter, or that oil prices will remain low. The region’s pipeline

infrastructure, however, will continue to be constrained as heating demand grows and gas‐fired

generation replaces retiring power plants.

Beyond the winter programs, what actions has the ISO taken to address infrastructure challenges?

In addition to two winter reliability programs, the ISO has taken major steps to increase market

efficiency and improve gas-electric coordination in response to the challenges posed by the region’s

natural gas dependence and infrastructure constraints.

Our longer-term market enhancements, called “Pay for Performance,” will provide strong incentives for

resources to invest in operational improvements and secure fuel arrangements to ensure resource

performance. This will go a long way towards mitigating the reliability risks facing the region.

The response to “Pay for Performance,” however, likely will not ensure investment in natural gas

pipeline capacity. The design gives market participants the flexibility to select the most cost-effective

way to ensure performance.

000032

Docket No. IR 15-124 Comments of Eversource Energy

Attachment 3 Page 4 of 13

5

Gas generators have told us that the most cost-effective solution for them is to continue to utilize the

pipelines when they are unconstrained and to switch to burning oil when gas transportation becomes

unavailable.

While the ISO may be satisfied with this solution from a reliability perspective, the states may not be

satisfied from an environmental perspective. And given that dual fuel will not directly relieve the gas

pipeline constraints, it is unlikely to resolve the issue of gas price volatility during the winter months.

I worry too about the long-term reliability of a system that is so fuel constrained, particularly during the

winter. We are currently maintaining reliability by relying heavily on older oil and coal resources, and we

know that these resources are the most likely to retire in the coming years.

In fact the largest coal and oil generator in New England will retire in June 2017. And the constraints on

the fuel system supplying New England make us that much more vulnerable to the outage of a large

non-gas generator or transmission line during extremely cold weather.

We also observe that it is becoming increasingly difficult for gas generators to obtain permission to

install dual-fuel capability and that the oil supply chain can be fragile under adverse weather conditions.

There are alternatives to burning fossil fuels, such as renewable energy. While these resources can

offset the need for gas, they are unlikely to be developed in sufficient quantity in the timeframe needed.

There is also the operational reality that renewable resources cannot be fully relied upon to produce the

energy we require when our demand is highest in the winter months. The one possible exception is

imported hydro energy, but only if the delivery of that energy has been guaranteed, since our neighbors

to the north also experience high demand for that energy during cold periods.

Concluding Remarks

In summary, all these indicators seem to point in the direction of increasing the capacity of the gas

infrastructure serving New England in order to mitigate the risks facing the region and facilitate the

integration of additional renewable energy.

This raises two questions: who will contract for this infrastructure and how will the costs be recovered?

As I mentioned previously, gas generators are unlikely to contract for the additional gas infrastructure. It

is also unlikely that gas producers will do so, because they typically will only invest in gas infrastructure

when there is a year-round demand for their product. This leaves either the gas distribution companies,

who have traditionally been the contracting party, or the electric distribution companies.

My understanding is that the states are considering a variety of solutions to alleviate the infrastructure

constraints and mitigate the risks facing the region. I believe state policymakers have a very important

role in shaping future infrastructure solutions and we look forward to working with you as you consider

these potential solutions.

Thank you.

000033

Docket No. IR 15-124 Comments of Eversource Energy

Attachment 3 Page 5 of 13

AP

RI

L 2

3,

20

15

|

HA

RT

FO

RD

, C

T

Go

rdo

n v

an W

elie

P

RE

SI

DE

NT

& C

EO

No

rth

east

Fo

rum

on

Reg

ion

al E

ner

gy

Solu

tio

ns

Ch

alle

nge

s Fa

cin

g th

e N

ew

Engl

and

Po

wer

Sys

tem

000034

Docket No. IR 15-124 Comments of Eversource Energy

Attachment 3 Page 6 of 13

New

En

glan

d h

as S

een

Dra

mat

ic C

han

ges

in t

he

En

ergy

Mix

fro

m O

il an

d C

oal

to

Nat

ura

l Gas

31

%

22

%

18

%

15

%

13

%

1.7

%

34

%

1%

5

%

44

%

15

%

1%

Nu

clea

r O

il C

oal

N

atu

ral G

as

Hyd

ro

and

Oth

er

Ren

ewab

les

Pu

mp

ed

Sto

rage

20

00

2

01

4 Pe

rcen

t o

f To

tal E

lect

ric

Ene

rgy

Pro

du

ctio

n b

y Fu

el T

ype

(2

00

0 v

s. 2

01

4)

2

Sou

rce:

ISO

New

En

glan

d N

et E

ner

gy a

nd

Pea

k Lo

ad b

y So

urc

e

Oth

er r

enew

able

s in

clu

de

lan

dfi

ll ga

s, b

iom

ass,

oth

er b

iom

ass

gas,

win

d, s

ola

r, m

un

icip

al s

olid

was

te, a

nd

mis

cella

neo

us

fuel

s

000035

Docket No. IR 15-124 Comments of Eversource Energy

Attachment 3 Page 7 of 13

3

On

- an

d O

ff-s

ho

re T

ran

smis

sio

n P

rop

osa

ls a

re V

yin

g to

M

ove

Re

ne

wab

le E

ne

rgy

to N

ew E

ngl

and

Lo

ad C

en

ters

No

te: T

hes

e p

roje

cts

are

NO

T re

liab

ility

pro

ject

s, b

ut

ISO

Ne

w E

ngl

and

’ s r

ole

is t

o e

nsu

re t

he

relia

ble

inte

rco

nn

ecti

on

of

thes

e ty

pes

of

pro

ject

s.

000036

Docket No. IR 15-124 Comments of Eversource Energy

Attachment 3 Page 8 of 13

Nat

ura

l Gas

Infr

astr

uct

ure

has

No

t K

ep

t P

ace

wit

h

Tre

me

nd

ou

s G

row

th in

Gas

-fir

ed

Ge

ne

rati

on

0

2,0

00

4,0

00

6,0

00

8,0

00

10

,00

0

12

,00

0

14

,00

0 19

97

19

99

20

01

20

03

20

05

20

07

20

09

20

11

20

13

Nat

ura

l Gas

Oil

Bio

mas

s

Fuel

Cel

l

Hyd

ro

Sola

r

Win

d

Nu

clea

r u

pra

te

Cu

mu

lati

ve N

ew G

en

era

tin

g C

apac

ity

in N

ew E

ngl

and

(M

W)

4

Capacity MW

000037

Docket No. IR 15-124 Comments of Eversource Energy

Attachment 3 Page 9 of 13

New

En

glan

d S

hif

ted

to

Co

al a

nd

Oil

this

Win

ter

5

0

50

,00

0

10

0,0

00

15

0,0

00

20

0,0

00

25

0,0

00

Dec

emb

er 1

, 20

14

Ja

nu

ary

1, 2

01

5

Feb

ruar

y 1

, 20

15

Dai

ly E

ne

rgy

for

De

cem

be

r 2

01

4 -

Fe

bru

ary

20

15

(M

Wh

)

Nat

ura

l Gas

/ L

NG

C

oal

O

il

Daily Energy MWh

000038

Docket No. IR 15-124 Comments of Eversource Energy

Attachment 3 Page 10 of 13

$0

$5

$1

0

$1

5

$2

0

$2

5

$3

0

$0

$2

0

$4

0

$6

0

$8

0

$1

00

$1

20

$1

40

$1

60

$1

80

Wh

ole

sale

Ele

ctri

city

at

New

En

glan

d H

ub

(R

eal-

Tim

e LM

P)

Nat

ura

l Gas

The

Re

gio

n h

as E

xpe

rie

nce

d H

igh

Nat

ura

l Gas

an

d

Wh

ole

sale

Ele

ctri

city

Pri

ces

the

Pas

t Fe

w W

inte

rs

6

Hu

rric

anes

h

it t

he

Gu

lf

Bef

ore

th

e

Rec

essi

on

an

d

Mar

cellu

s Sh

ale

gas

bo

om

W

inte

r 2

01

2/2

01

3

Win

ter

20

13

/20

14

Electric Energy $/MWh Fuel $/MMBtu

Mo

nth

ly A

vera

ge N

atu

ral G

as a

nd

Wh

ole

sale

Ele

ctri

city

Pri

ces

in N

ew E

ngl

and

Rec

ord

low

nat

ura

l ga

s an

d w

ho

lesa

le

elec

tric

ity

pri

ces

Win

ter

20

14

/20

15

000039

Docket No. IR 15-124 Comments of Eversource Energy

Attachment 3 Page 11 of 13

Nat

ura

l Gas

Pri

ces

are

Hig

h D

uri

ng

the

Win

ter

Re

lati

ve t

o O

the

r R

egi

on

s

$0

$5

$1

0

$1

5

$2

0

$2

5

$3

0

Mo

nth

ly A

vera

ge N

atu

ral G

as P

rice

s ($

/MM

Btu

)

Hen

ry H

ub

A

lgo

nq

uin

Cit

ygat

e Tr

ansc

o Z

on

e 6

(N

Y)

7

Win

ter

20

12

/20

13

W

inte

r 2

01

4/2

01

5

Win

ter

20

13

/20

14

Un

der

lyin

g n

atu

ral g

as d

ata

furn

ish

ed b

y:

Fuel $/MMBtu

000040

Docket No. IR 15-124 Comments of Eversource Energy

Attachment 3 Page 12 of 13

A C

om

par

iso

n o

f th

e L

ast

Two

Win

ters

Wh

y w

ere

pri

ces

less

vo

lati

le

this

win

ter?

•2

01

4/2

01

5 W

inte

r R

elia

bili

ty

Pro

gram

pro

vid

ed in

cen

tive

s to

fill

ta

nks

bef

ore

th

e st

art

of

the

win

ter

•H

igh

fo

rwar

d p

rice

s, d

ue

to h

igh

p

rice

s th

e p

revi

ou

s w

inte

r, a

ttra

cted

la

rge

sup

plie

s o

f LN

G t

o t

he

regi

on

•O

il p

rice

s w

ere

hal

f w

hat

th

ey w

ere

a ye

ar a

go

•C

old

est

win

ter

wea

ther

hap

pen

ed

in F

ebru

ary,

wh

en d

ays

wer

e lo

nge

r an

d d

eman

d w

as d

ow

n

8

W

inte

r

20

13

/20

14

Win

ter

20

14

/20

15

%

chan

ge

Ave

rage

mo

nth

ly

tem

per

atu

re (°

F)

26

.5

25

.5

- 3

.8%

Tota

l en

ergy

con

sum

pti

on

(GW

h)

33

,99

1

33

,65

4

- 1

.0%

Peak

dem

and

(MW

) 2

1,4

53

2

0,5

56

-

4.2

%

D

ate

of

pea

k 1

2/1

7/2

01

3

1/8

/20

15

-

Ave

rage

wh

ole

sale

ener

gy p

rice

at

Hu

b

($/M

Wh

)

$1

37

.60

$

76

.64

-

44

.3%

Ave

rage

gas

pri

ce a

t

Alg

on

qu

in ($

/MM

Btu

) $

19

.33

$

10

.70

-

44

.6%

Tota

l val

ue

of

ener

gy

mar

kets

(in

bill

ion

s)

$5

.05

B

$2

.77

B

- 4

5.1

%

000041

Docket No. IR 15-124 Comments of Eversource Energy

Attachment 3 Page 13 of 13