northland power investor presentation

TRANSCRIPT

Investor Presentation

September 2012

1

Forward Looking Information Disclaimer

This written and accompanying oral presentation contains certain forward‐looking statements which are provided for the purpose of presenting information about management’s current expectations and plans. Readers are cautioned that such statements may not be appropriate for other purposes. Forward‐looking statements include statements that are predictive in nature, depend upon or refer to future events or conditions, or include words such as “expects,” “anticipates,” “plans,” “believes,” “estimates,” “intends,” “targets,” “projects,” “forecasts” or negative versions thereof and other similar expressions, or future or conditional verbs such as “may,” “will,” “should,” “would” and “could.” These statements may include, without limitation, statements regarding future EBITDA, cash flows and dividend payments, the construction, completion, attainment ofcommercial operations, cost and output of development projects, plans for raising capital, and the operations, business, financial condition, priorities, ongoing objectives, strategies and outlook of Northland and its subsidiaries. This information is based upon certain material factors or assumptions that were applied in developing the forward looking statements includingbased upon certain material factors or assumptions that were applied in developing the forward‐looking statements, including the design specifications of development projects, the provisions of contracts to which Northland or a subsidiary is a party, management’s current plans, its perception of historical trends, current conditions and expected future developments, as well asother factors that are believed to be appropriate in the circumstances.

Although these forward‐looking statements are based upon management’s current reasonable expectations and assumptions, they are subject to numerous risks and uncertainties. Some of the factors that could cause results or events to differ from current expectations include, but are not limited to, construction risks, counterparty risks, operational risks, the variability of revenues from generating facilities powered by intermittent renewable resources and the other factors described in the “Risks and Uncertainties” section of Northland’s 2011 Annual Report and 2011 Annual Information Form, which are both filed electronically at www.sedar.com and Northland’s website www.northlandpower.ca. Northland’s actual results could differ materially from th d i i li d b th f d l ki t t t d di l b i th t f ththose expressed in, or implied by, these forward‐looking statements and, accordingly, no assurances can be given that any of theevents anticipated by the forward‐looking statements will transpire or occur. The forward‐looking statements contained in this presentation are based on assumptions that were considered reasonable at time of delivery. Other than as specifically required by law, Northland undertakes no obligation to update any forward‐looking statements to reflect events or circumstances after such date or to reflect the occurrence of unanticipated events, whether as a result of new information, future events or results, or otherwise

2

or otherwise.

Northland Overview

Develop Build Own OperateFinance

Canadian‐based Independent Power Producer since 1987

Well‐diversified across many clean and green technologies andWell diversified across many clean and green technologies and geographical jurisdictions

Full lifecycle developers, owners and operators of our facilities

Strategic and disciplined organic growth platform

Stable, long‐term contracted (non‐merchant) projects with creditworthy counterparties

S&P debt rating BBB– positive outlook

3

Focus on contracted low risk cash flow streams; little interest in taking positions on commodities, FX and interest rates

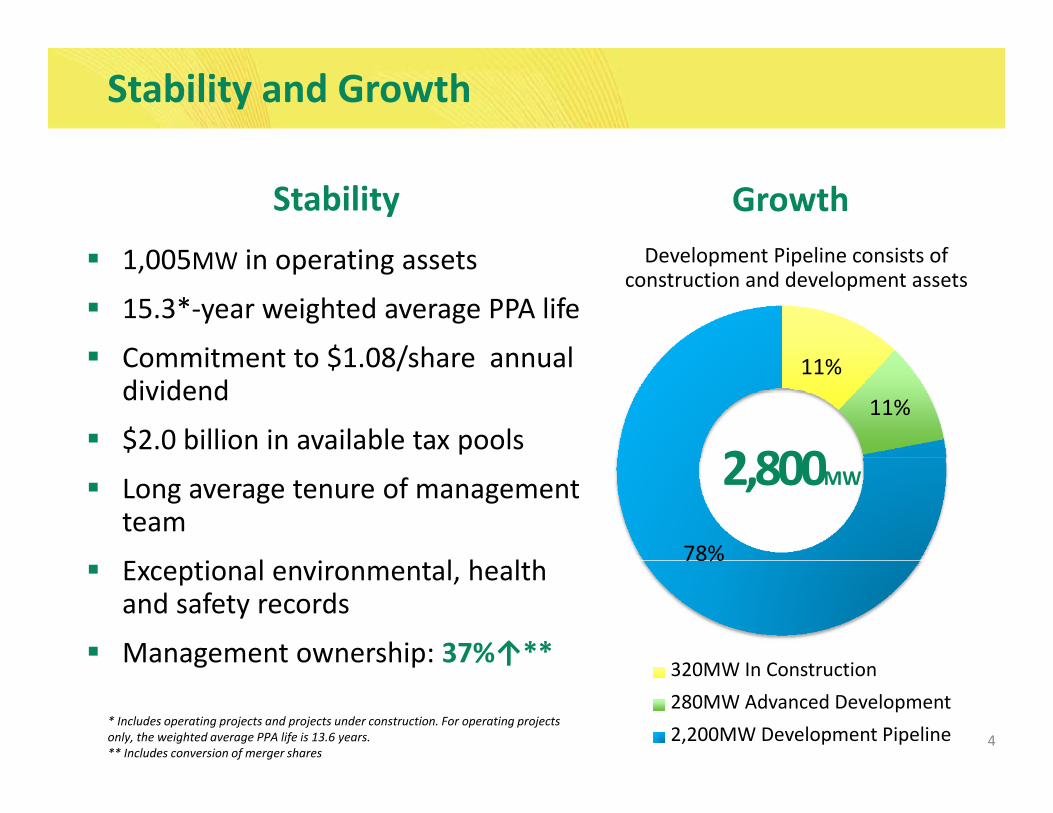

Stability and Growth

Stability

1 005MW i ti t

GrowthDevelopment Pipeline consists of1,005MW in operating assets

15.3*‐year weighted average PPA life

Commitment to $1 08/share annual

Development Pipeline consists of construction and development assets

Commitment to $1.08/share annual dividend

$2.0 billion in available tax pools

11%

11%

2800Long average tenure of management team

i l i l h l h78%

2,800MW

Exceptional environmental, health and safety records

Management ownership: 37%↑**

78%

320MW I C i

4

g p ↑

* Includes operating projects and projects under construction. For operating projects only, the weighted average PPA life is 13.6 years.** Includes conversion of merger shares

320MW In Construction280MW Advanced Development2,200MW Development Pipeline

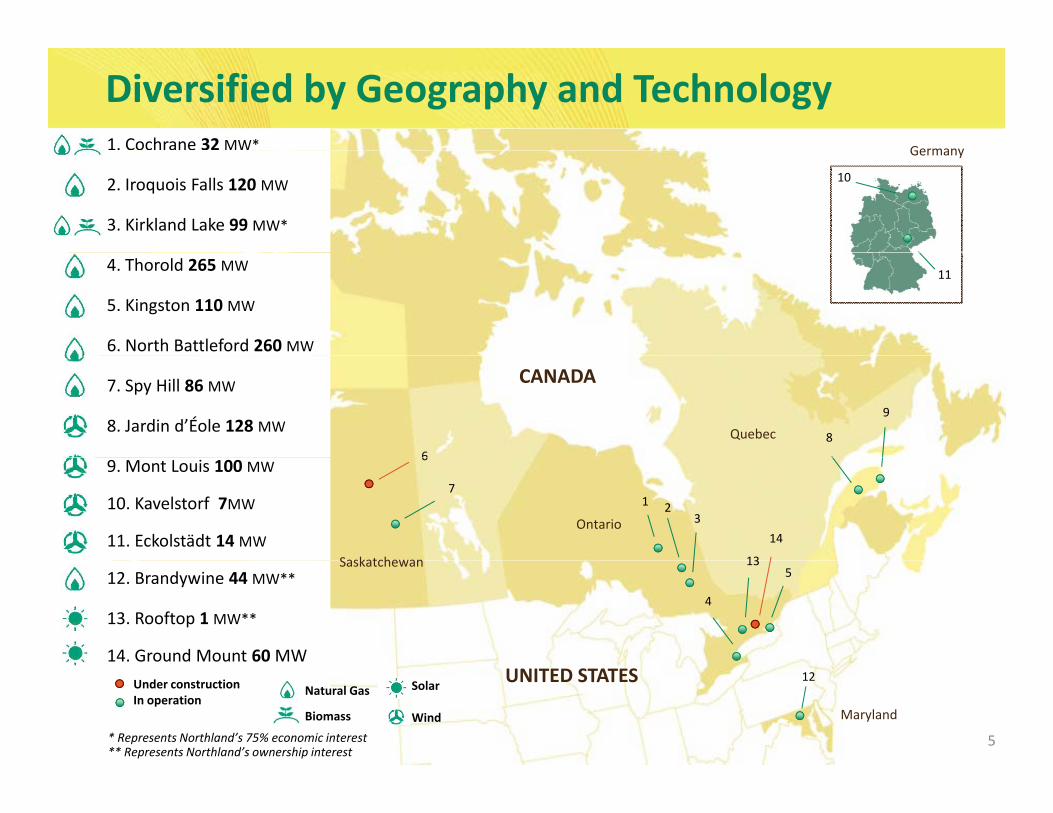

Diversified by Geography and Technology1. Cochrane 32 MW* Germany

2. Iroquois Falls 120 MW

3. Kirkland Lake 99 MW*

Germany

10

4. Thorold 265 MW

5. Kingston 110 MW

6. North Battleford 260 MW

11

7. Spy Hill 86 MW

8. Jardin d’Éole 128 MW Quebec 8

9

6

CANADA

9. Mont Louis 100 MW

10. Kavelstorf 7MW

11. Eckolstädt 14 MWSaskatchewan

Ontario

1 23

13

6

7

14

12. Brandywine 44 MW**

13. Rooftop 1 MW**

14. Ground Mount 60MW

Saskatchewan

4

513

5

Maryland

Under constructionIn operation

12

* Represents Northland’s 75% economic interest** Represents Northland’s ownership interest

Natural Gas

Biomass

Solar

Wind

UNITED STATES

5

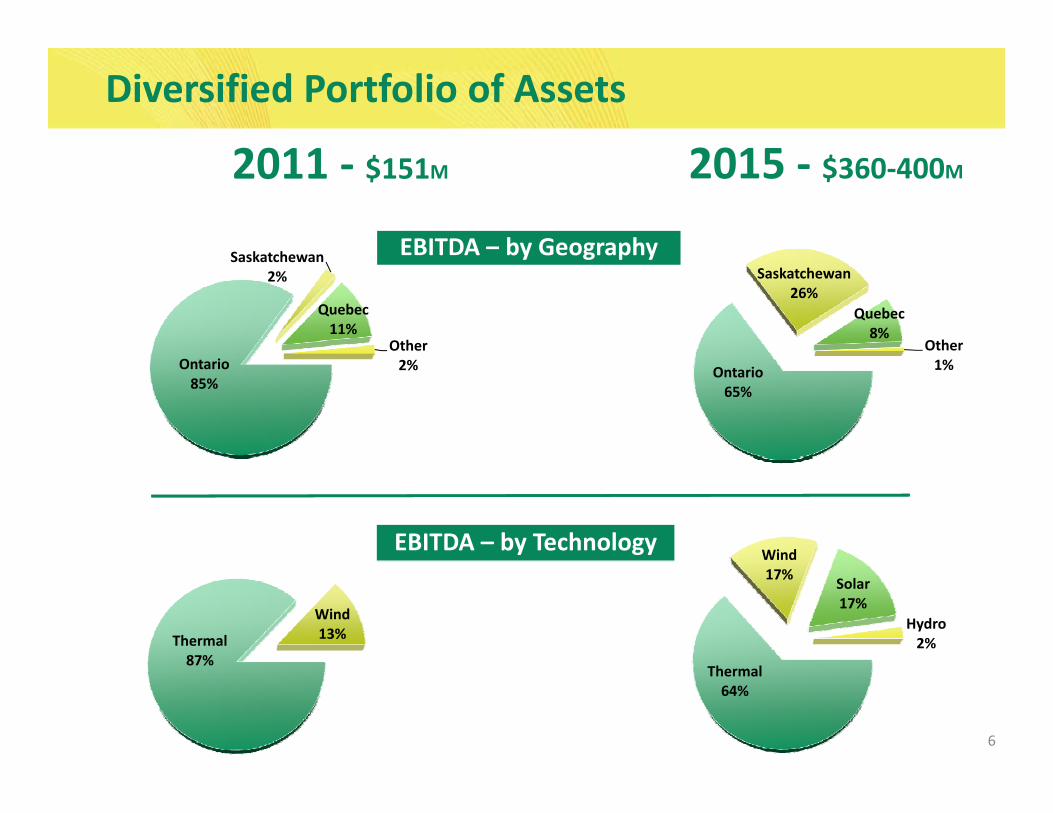

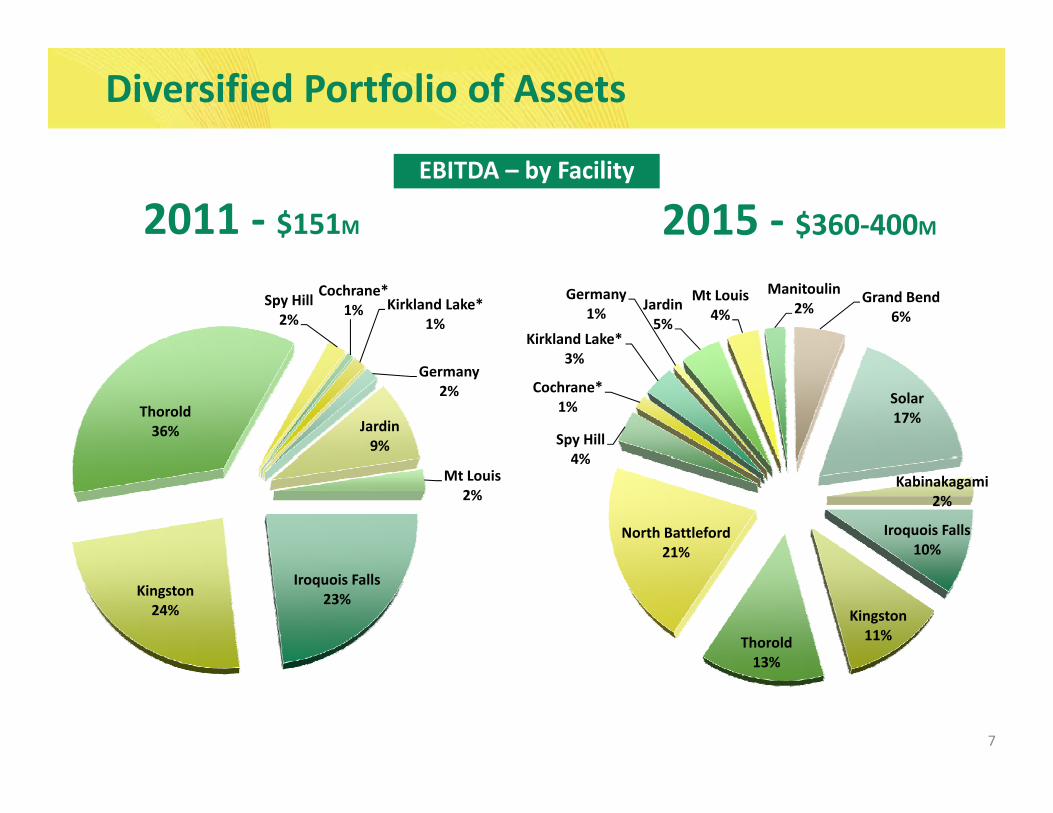

Diversified Portfolio of Assets

2011 2015

S k t h EBITDA – by Geography

2011 ‐ $151M 2015 ‐ $360‐400M

Saskatchewan2%

Quebec11%

Other

Saskatchewan26%

Quebec8%

Other

EBITDA by Geography

Ontario85%

2% Ontario65%

1%

Wind EBITDA – by Technology

Thermal87%

Wind 13%

17% Solar17%

Hydro2%

6

87%Thermal64%

Diversified Portfolio of Assets

EBITDA – by Facility

2011 ‐ $151M 2015 ‐ $360‐400MSpy Hill2%

Cochrane*1% Kirkland Lake*

1%Kirkland Lake*

3%

Germany1% Jardin

5%

Mt Louis4%

Manitoulin2%

Grand Bend6%

Thorold36%

Germany2%

Jardin9% Spy Hill

4%

Cochrane*1%

3%

Solar17%

Mt Louis2%

Iroquois Falls10%

North Battleford21%

4%Kabinakagami

2%

Iroquois Falls23%Kingston

24% Kingston11%Thorold

13%

7

13%

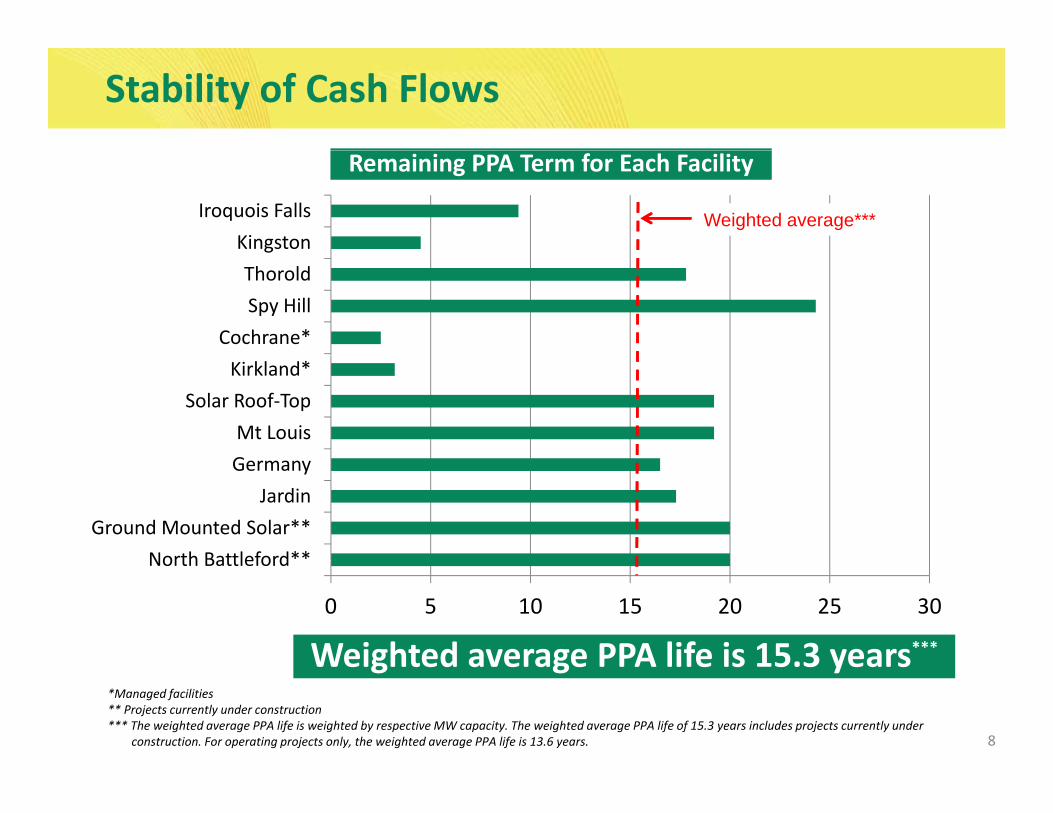

Stability of Cash Flows

KingstonIroquois Falls

Remaining PPA Term for Each Facility

Weighted average***

Cochrane*Spy HillThorold

GMt Louis

Solar Roof‐TopKirkland*

North Battleford**Ground Mounted Solar**

JardinGermany

Weighted average PPA life is 15.3 years***0 5 10 15 20 25 30

North Battleford

8

Weighted average PPA life is 15.3 years*Managed facilities** Projects currently under construction*** The weighted average PPA life is weighted by respective MW capacity. The weighted average PPA life of 15.3 years includes projects currently under

construction. For operating projects only, the weighted average PPA life is 13.6 years.

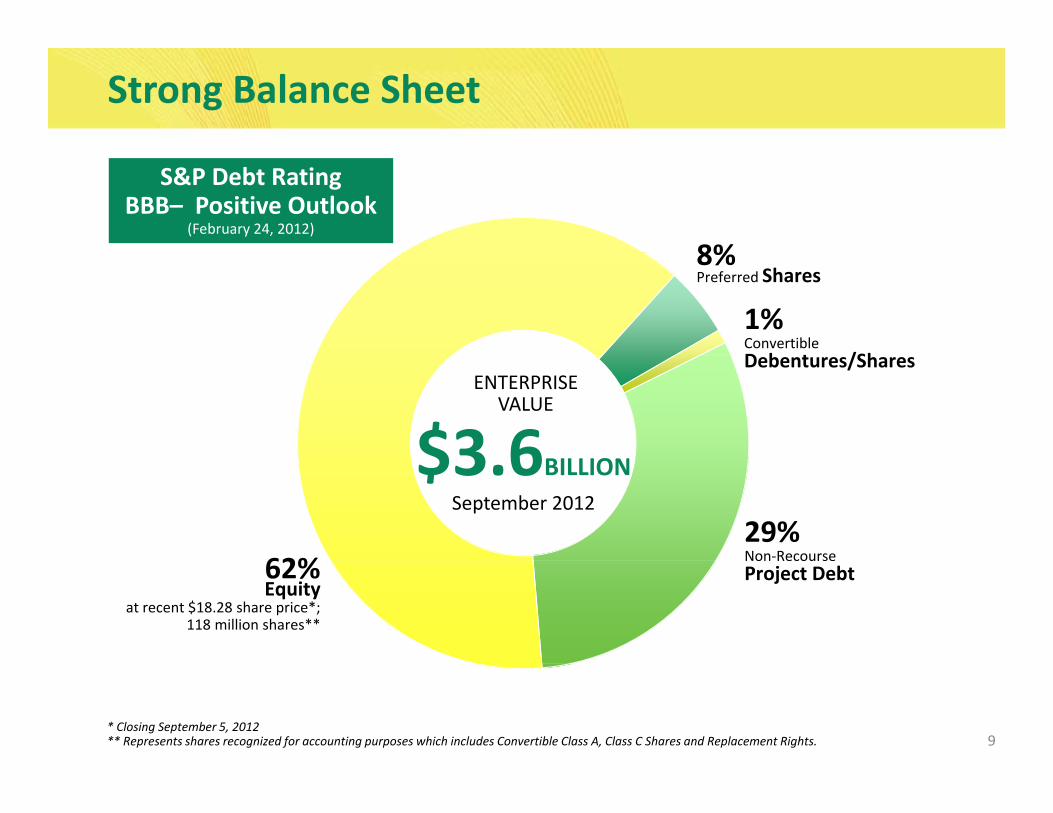

Strong Balance Sheet

8%

S&P Debt RatingBBB– Positive Outlook

(February 24, 2012)

8%Preferred Shares

1%Convertible D b t /Sh

$3 6 O

ENTERPRISEVALUE

Debentures/Shares

$3.6BILLIONSeptember 2012

29%Non‐Recourse62% Non RecourseProject Debt62%

Equityat recent $18.28 share price*;

118 million shares**

9* Closing September 5, 2012** Represents shares recognized for accounting purposes which includes Convertible Class A, Class C Shares and Replacement Rights.

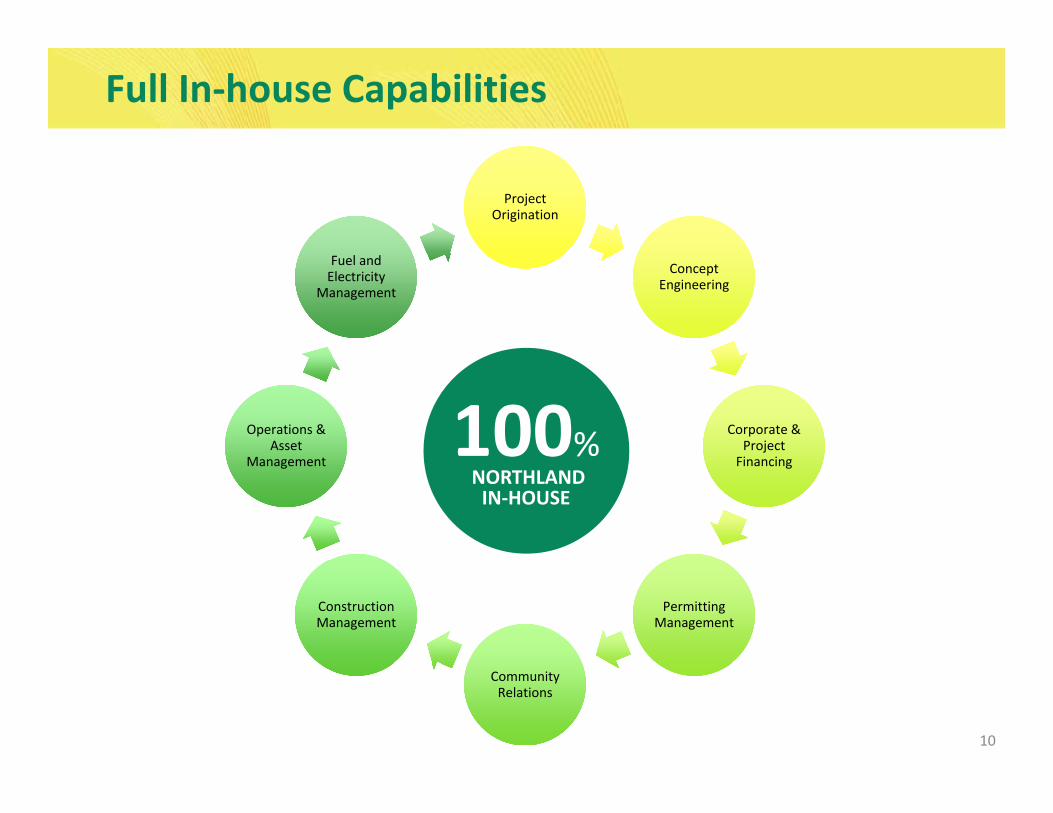

Full In‐house Capabilities

Project OriginationProject

Origination

Concept EngineeringConcept

Engineering

Fuel and Electricity

Management

Fuel and Electricity

Management

Corporate & Project Fi i

Corporate & Project Fi i

Operations & Asset

M t

Operations & Asset

M t100%

FinancingFinancingManagementManagementNORTHLANDIN‐HOUSE

Permitting ManagementPermitting

ManagementConstruction ManagementConstruction Management

10

Community RelationsCommunity Relations

Growth Pipeline

Construction

ConstructionAdvanced DevelopmentAdvanced DevelopmentDevelopment

ConstructionDevelopment ConstructionAdvanced DevelopmentDevelopment

11

Development11

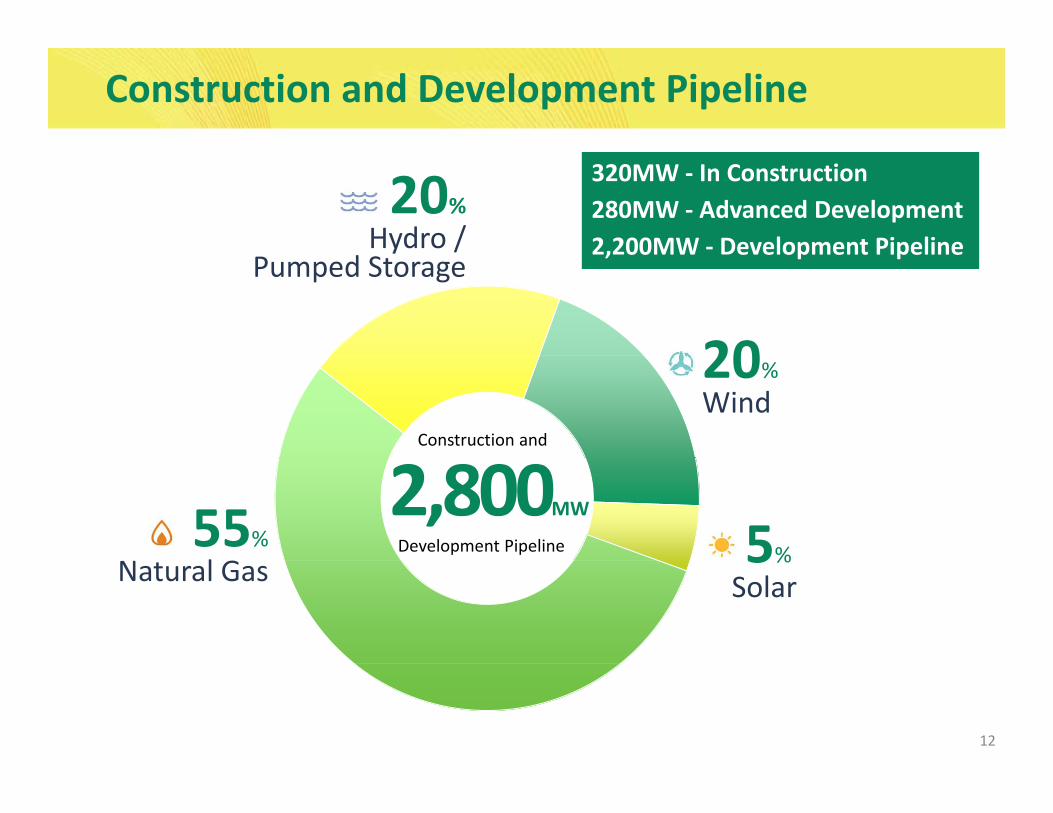

Construction and Development Pipeline

20%Hydro /

320MW ‐ In Construction280MW ‐ Advanced Development2,200MW ‐ Development Pipeliney

Pumped Storage

20

2,200MW Development Pipeline

20%Wind

Construction and

55%l G

2,800MW

5%Development Pipeline

Natural Gas 5%Solar

12

Projects Under Construction

On track for

North Battleford, Saskatchewan, Canada

Q2 2013 completion

260MW260MWgas‐fired combined cycle plant

20‐yearPPAPPA

$677MExpected project cost

ConstructionKiewit

COD guarantee

13

Q4 2013

Projects Under Construction

Expected l i

Ground Mounted Solar, Ontario, Canada

completion Q1‐Q3 2013

60MW60MWX6 10MW ground mount solar farms

20 year20‐yearPPA

$285MExpected project cost

Construction

Aecon – Miwel

14

Construction: On‐time, On‐budget

Northland’s track record is on‐time, on‐budget project delivery

Facility COD Location MW Budget (M)

Actual (M)

%Under

OnTime

Iroquois Falls cogeneration plant 1997 ON 110 $158 $151 4.18%

I i F ll t bi l t 2003 ON 80 $24 $23 2 13%Iroquois Falls gas turbine replacement 2003 ON 80 $24 $23 2.13%

Kirkland Lake peaker facility 2004 ON 30 $30 $30 1.33%

Mont Miller wind farm 2005 QC 54 $98 $93 5.11%

Jardin d’Éole wind farm 2009 QC 128 $268 $268 0.22%

Thorold cogeneration facility 2010 ON 265 $520 $509 2.12%

Mont Louis wind farm 2011 QC 100 $181 $173 4.42%

Spy Hill peaker facility 2011 SK 86 $141 $137 2.83%

North Battleford and six ground mount solar projects currently under construction are within budget and on schedule

15

under construction are within budget and on schedule

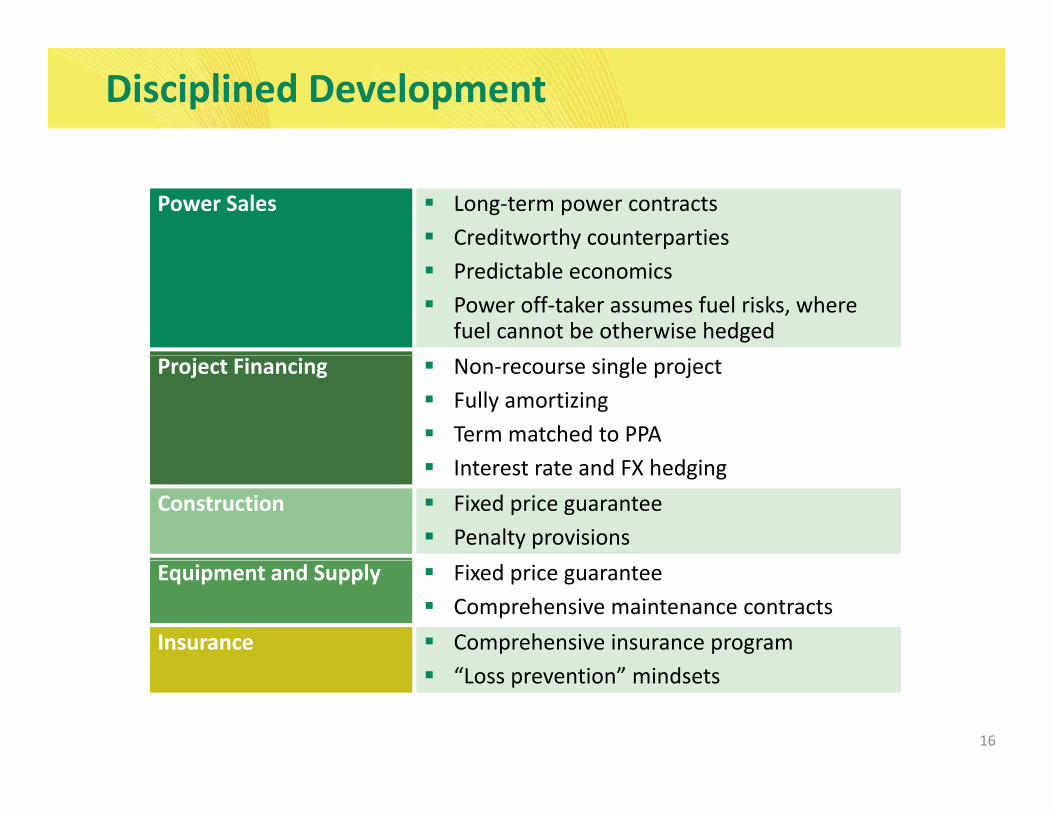

Disciplined Development

Power Sales Long‐term power contractsCreditworthy counterpartiesPredictable economicsPower off‐taker assumes fuel risks, where fuel cannot be otherwise hedged

Project Financing Non‐recourse single projectFully amortizingTerm matched to PPAInterest rate and FX hedging

Construction Fixed price guaranteePenalty provisions

Equipment and Supply Fixed price guaranteeComprehensive maintenance contracts

Insurance Comprehensive insurance program

16

“Loss prevention” mindsets

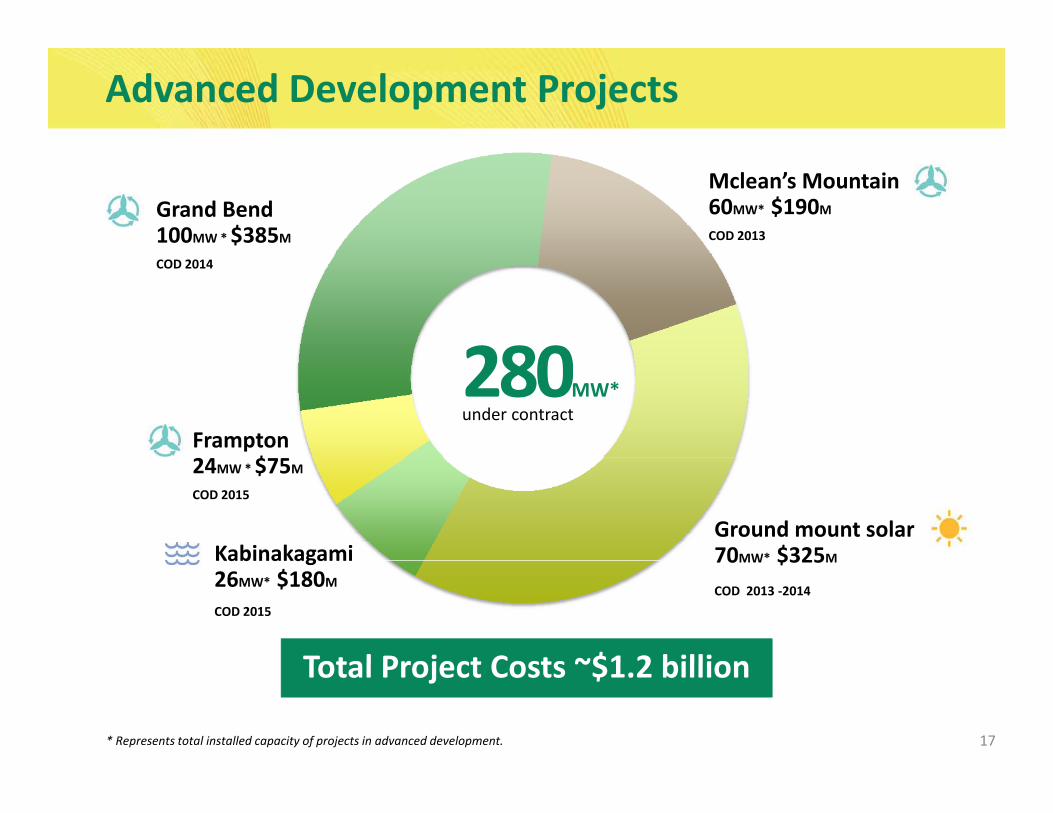

Advanced Development Projects

Mclean’s Mountain60MW* $190M

COD 2013

Grand Bend100MW * $385M

280

COD 2014

280MW*under contract

Frampton2 $

KabinakagamiGround mount solar70MW* $325M

24MW * $75M

COD 2015

Kabinakagami26MW* $180M

COD 2015

70MW $325M

COD 2013 ‐2014

Total Project Costs ~$1 2 billion

17

Total Project Costs ~$1.2 billion

* Represents total installed capacity of projects in advanced development.

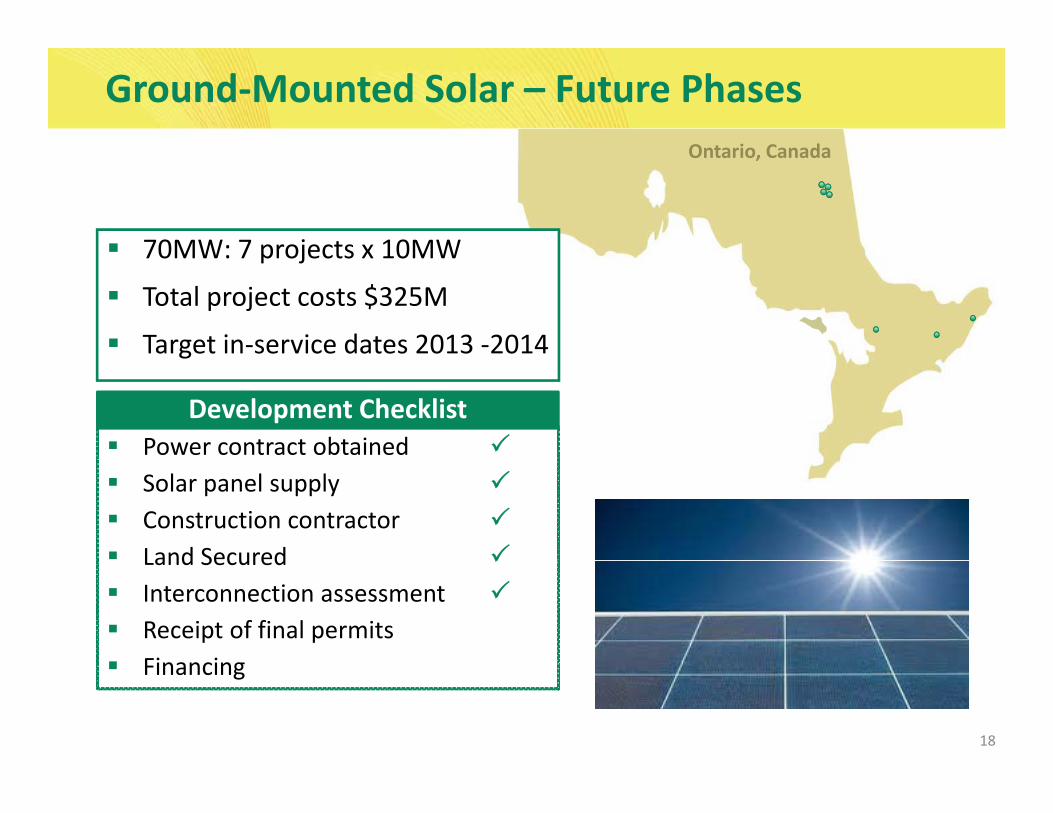

Ontario Canada

Ground‐Mounted Solar – Future Phases Ontario, Canada

70MW: 7 projects x 10MW70MW: 7 projects x 10MW

Total project costs $325M

Target in‐service dates 2013 ‐2014g

Power contract obtained Development Checklist

Solar panel supplyConstruction contractor Land SecuredLand Secured Interconnection assessmentReceipt of final permitsFinancing

18

Financing

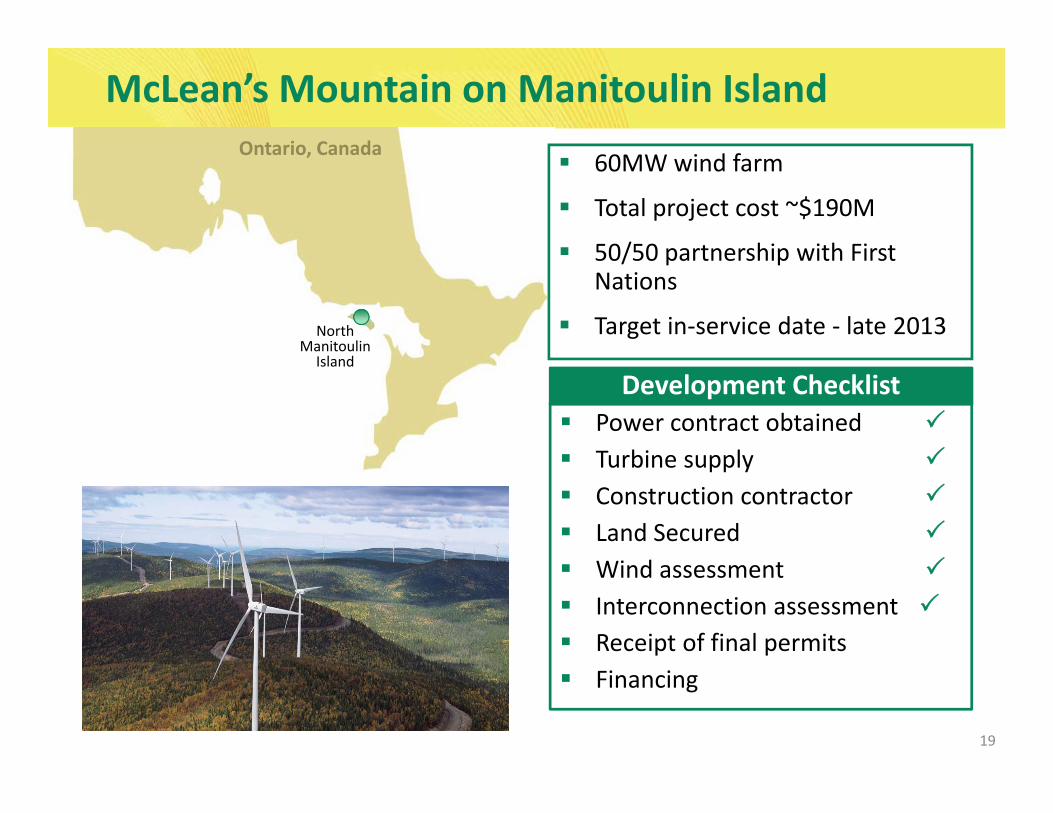

McLean’s Mountain on Manitoulin IslandOntario Canada 60MW wind farm

Total project cost ~$190M

50/50 partnership with First

Ontario, Canada

50/50 partnership with First Nations

Target in‐service date ‐ late 2013North Manitoulin

Island

Power contract obtained Turbine supply

Development Checklist

Turbine supplyConstruction contractor Land Secured i dWind assessment

Interconnection assessment Receipt of final permits

19

Financing

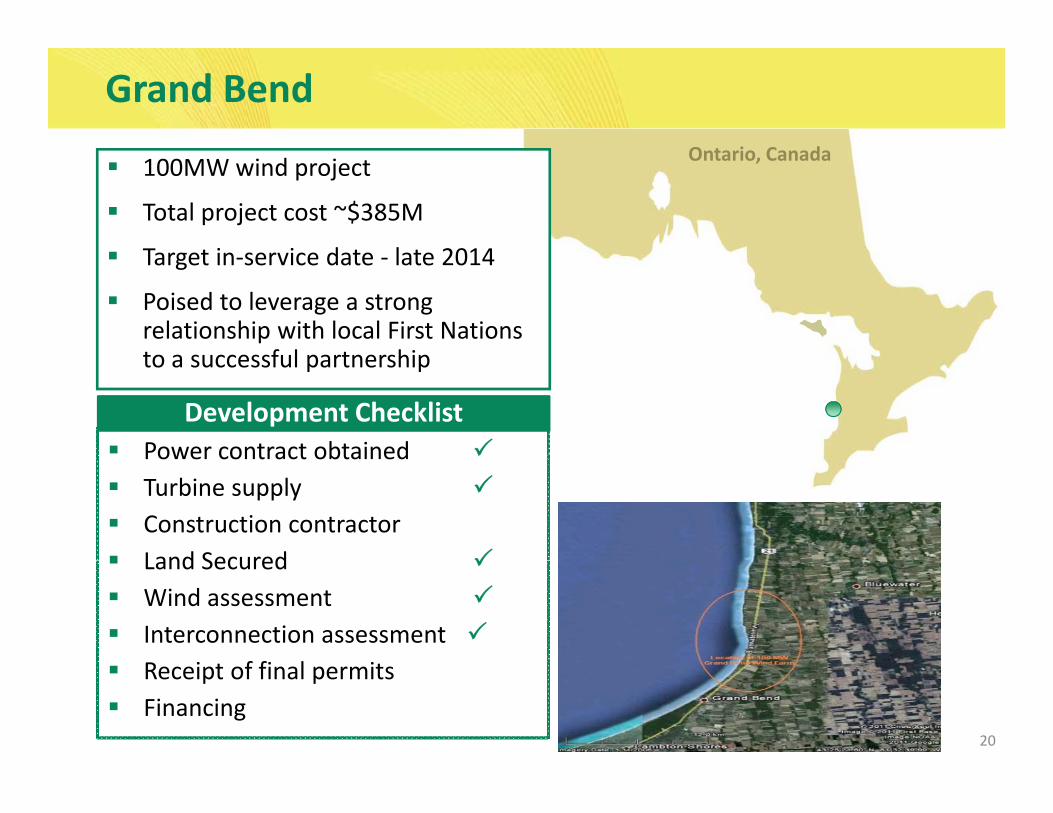

Grand BendOntario CanadaOntario, Canada100MW wind project

Total project cost ~$385M

Target in service date late 2014Target in‐service date ‐ late 2014

Poised to leverage a strong relationship with local First Nations to a successful partnershipto a successful partnership

Power contract obtainedDevelopment Checklist

Power contract obtained Turbine supplyConstruction contractor Land SecuredLand Secured Wind assessmentInterconnection assessment R i f fi l i

20

Receipt of final permitsFinancing

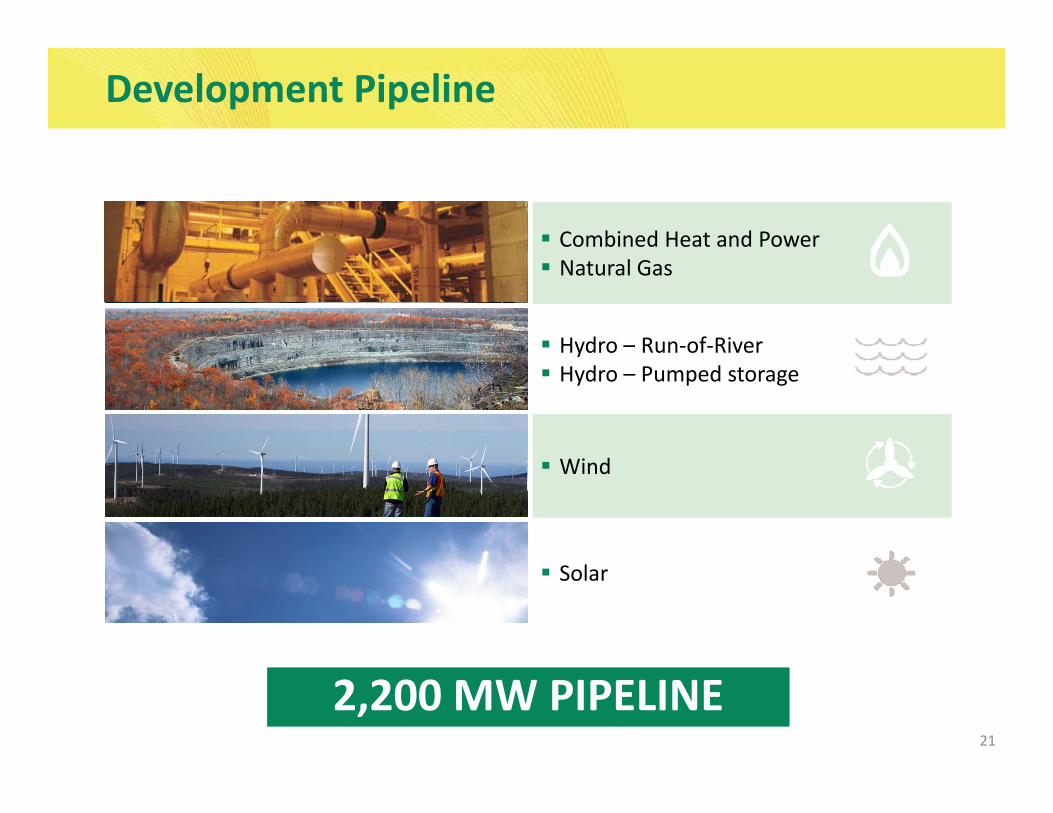

Development Pipeline

Combined Heat and PowerNatural Gas

Hydro – Run‐of‐RiveryHydro – Pumped storage

dWind

Solar

21

2,200 MW PIPELINE

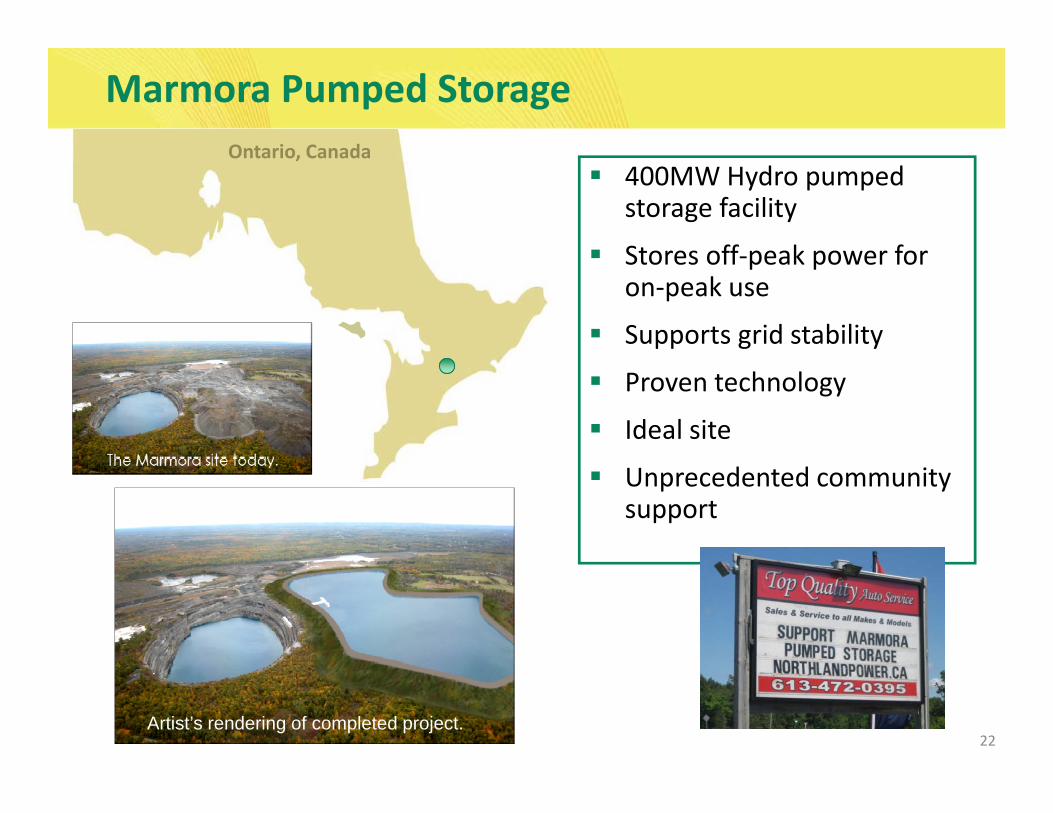

Marmora Pumped Storage Ontario Canada

400MW Hydro pumped storage facility

Stores off peak power for

Ontario, Canada

Stores off‐peak power for on‐peak use

Supports grid stability

Proven technology

Ideal site

Unprecedented community support

22Artist’s rendering of completed project.

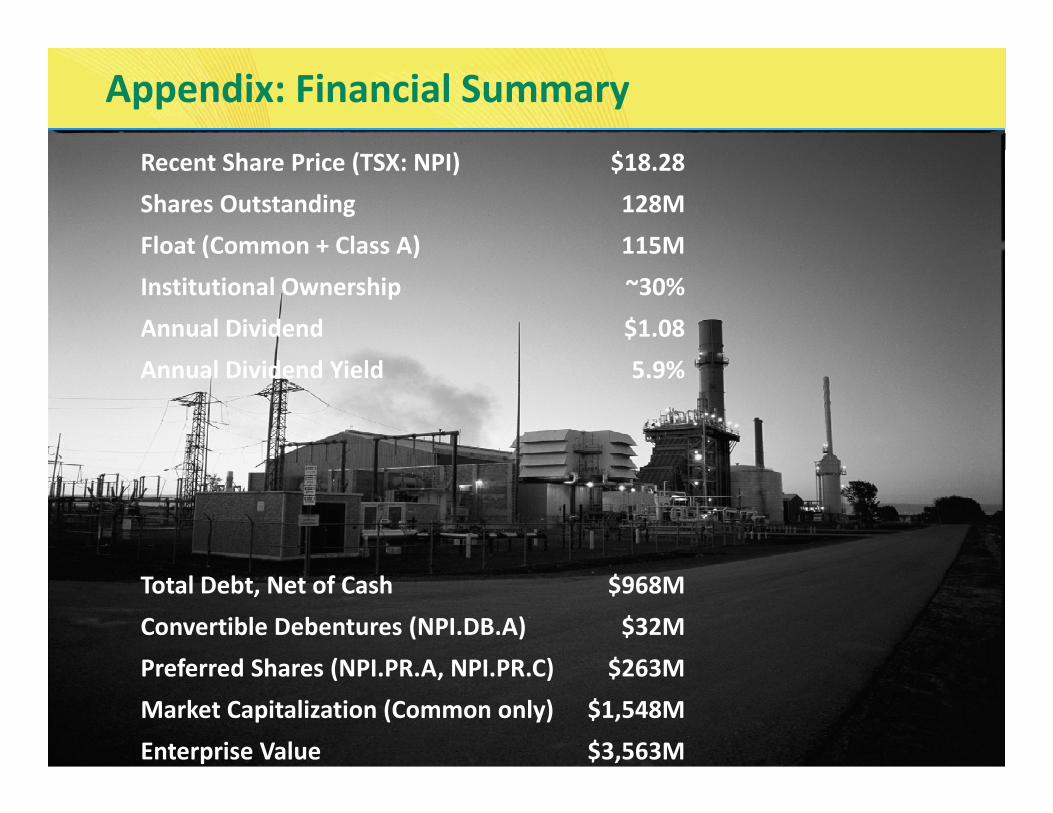

Appendix: Financial Summary

Recent Share Price (TSX: NPI) $18.28Shares Outstanding 128MFloat (Common + Class A) 115MFloat (Common Class A) 115MInstitutional Ownership ~30%Annual Dividend $1.08Annual Dividend Yield 5.9%

Total Debt, Net of Cash $968MConvertible Debentures (NPI.DB.A) $32MP f d Sh (NPI PR A NPI PR C) $263M

23

Preferred Shares (NPI.PR.A, NPI.PR.C) $263MMarket Capitalization (Common only) $1,548MEnterprise Value $3,563M

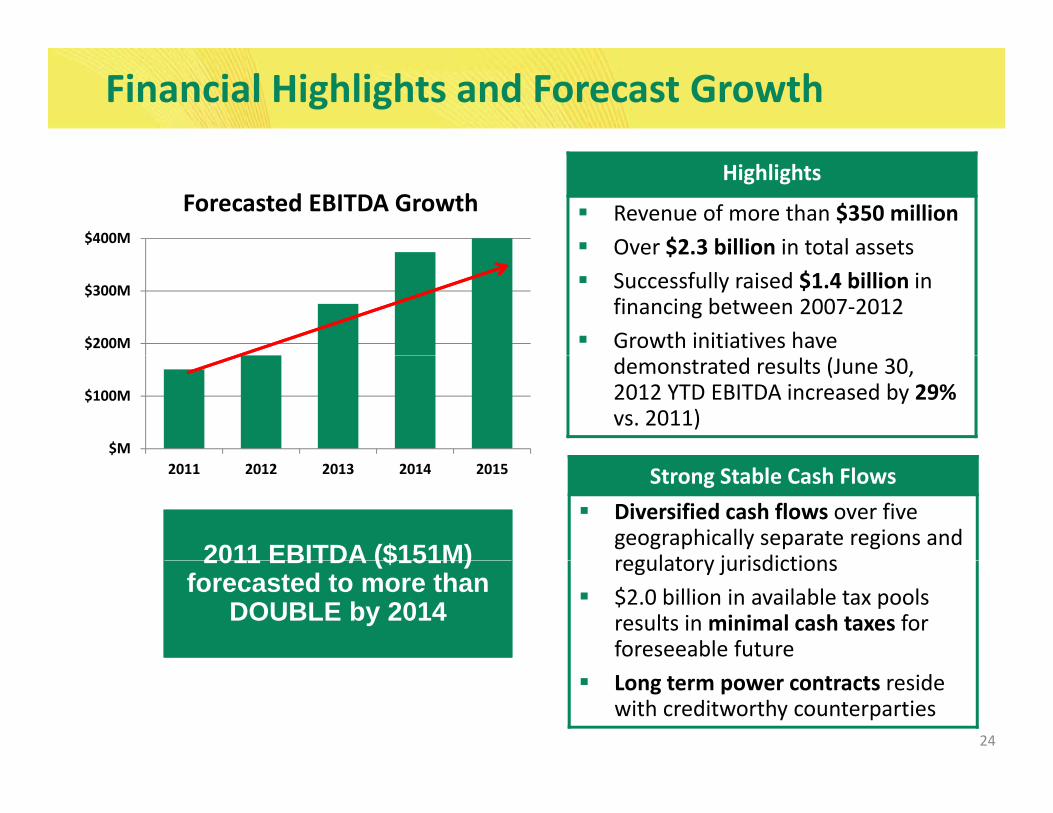

Financial Highlights and Forecast Growth

$400M

Forecasted EBITDA GrowthHighlights

Revenue of more than $350 million Over $2.3 billion in total assets

$200M

$300M

Over $2.3 billion in total assetsSuccessfully raised $1.4 billion in financing between 2007‐2012Growth initiatives have

$M

$100M

demonstrated results (June 30, 2012 YTD EBITDA increased by 29%vs. 2011)

2011 2012 2013 2014 2015 Strong Stable Cash FlowsDiversified cash flows over five geographically separate regions and regulatory jurisdictions2011 EBITDA ($151M) regulatory jurisdictions$2.0 billion in available tax pools results in minimal cash taxes for foreseeable future

2011 EBITDA ($151M) forecasted to more than

DOUBLE by 2014

24

Long term power contracts reside with creditworthy counterparties

Illustration of Payout Ratio*

Northland is committed to

Free Cash Flow required to service equity raised for projects in construction

160%

continuing $1.08 per share dividend as top priority for h h ld

NPI Merger Acquisition

120%

140%

shareholders

Growth, primarily projects under Full year

Reducing due to projects

coming online

Costs

80%

100%

p jconstruction, have caused Payout Ratio to rise above 100%

Full yearAll projectson‐line

40%

60%

Expected to be a temporary condition until projects

20%

40%

25

until projects completed

This chart has been complied by Northland management for illustrative purposes only* Payout is net of DRIP impact

0%2008 2009 2010 2011 2012F 2013F 2014F 2015F

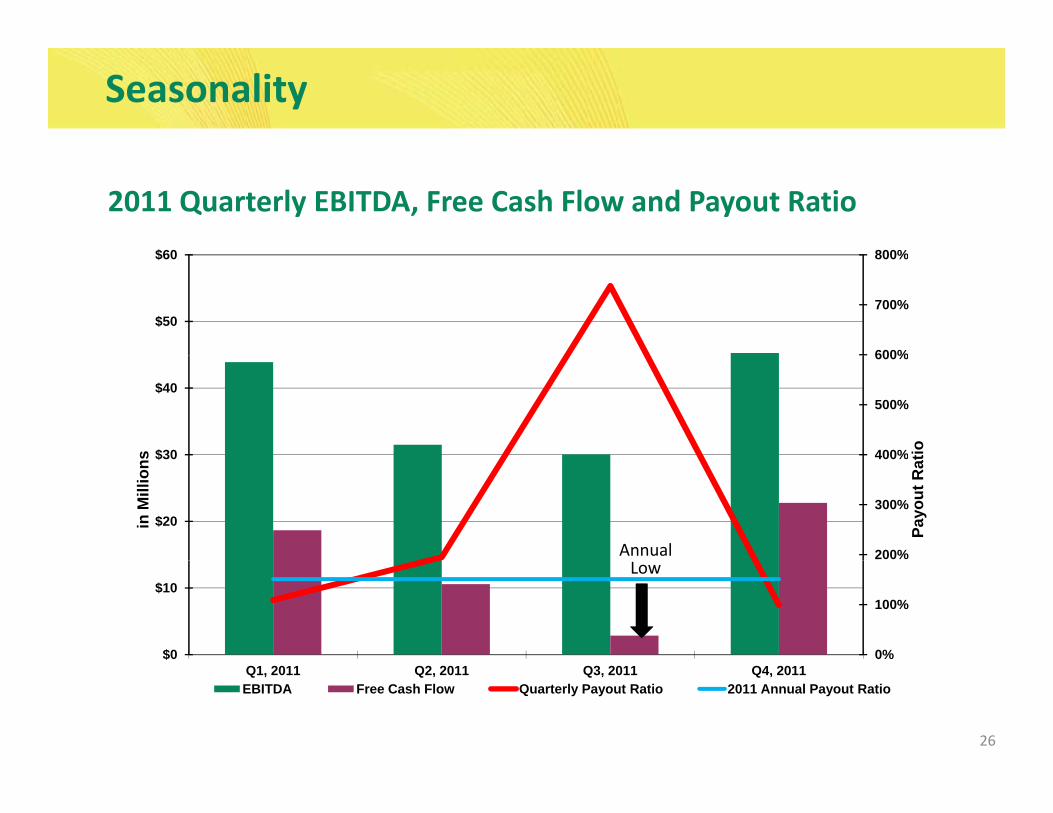

Seasonality

800%$60

2011 Quarterly EBITDA, Free Cash Flow and Payout Ratio

600%

700%

800%

$50

$60

400%

500%

600%

$30

$40

tios

200%

300%

400%

$20

$30

Payo

ut R

at

in M

illio

ns

Annual

0%

100%

$0

$10Low

26

Q1, 2011 Q2, 2011 Q3, 2011 Q4, 2011EBITDA Free Cash Flow Quarterly Payout Ratio 2011 Annual Payout Ratio

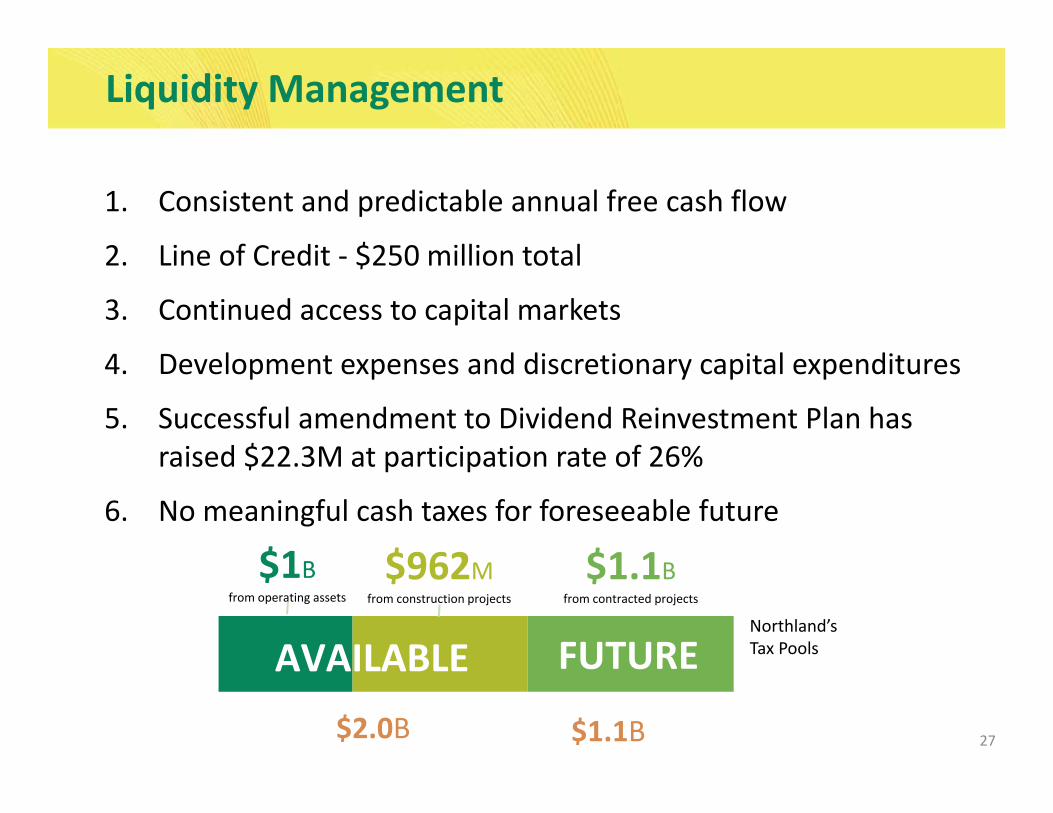

Liquidity Management

1. Consistent and predictable annual free cash flow

2 Line of Credit $250 million total2. Line of Credit ‐ $250 million total

3. Continued access to capital markets

4 D l t d di ti it l dit4. Development expenses and discretionary capital expenditures

5. Successful amendment to Dividend Reinvestment Plan has raised $22 3M at participation rate of 26%raised $22.3M at participation rate of 26%

6. No meaningful cash taxes for foreseeable future

$962 $1 1$1

AVAILABLE FUTURE

$962Mfrom construction projects

$1.1Bfrom contracted projects

Northland’s Tax Pools

$1Bfrom operating assets

27

AVAILABLE FUTURE

$2.0B $1.1B

Liquidity Management

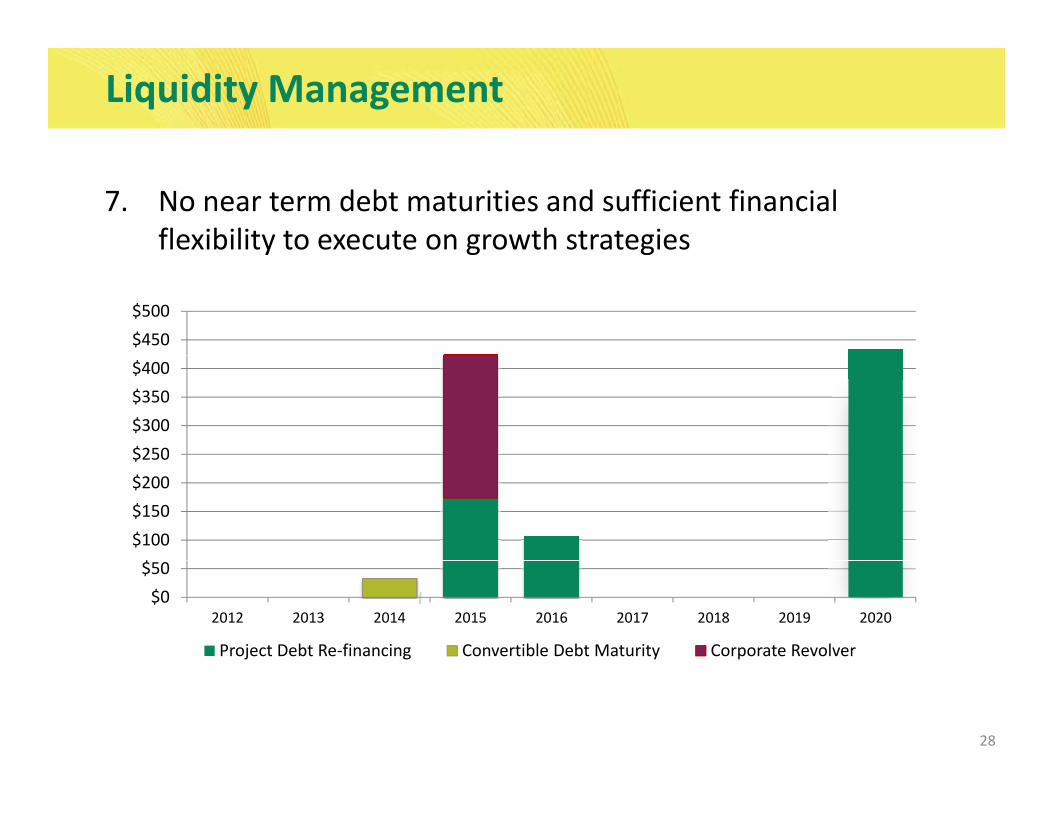

7. No near term debt maturities and sufficient financial flexibility to execute on growth strategiesy g g

$450$500

$250$300$350$400

$$100$150$200$250

$0$50

2012 2013 2014 2015 2016 2017 2018 2019 2020

Project Debt Re‐financing Convertible Debt Maturity Corporate Revolver

28

Why Invest in Northland?

Stability: The track record, commitment and ability to deliver shareholder value. Commitment to $1.08 $annual dividend.

Strong and Visible Growth Opportunities: AnStrong and Visible Growth Opportunities: An exciting portfolio of attractive, strategic development projects.

Experienced Team: Strong, seasoned people at every level.

Management’s ownership of more than 37% ensures alignment with shareholder interests

29

Appendix

30

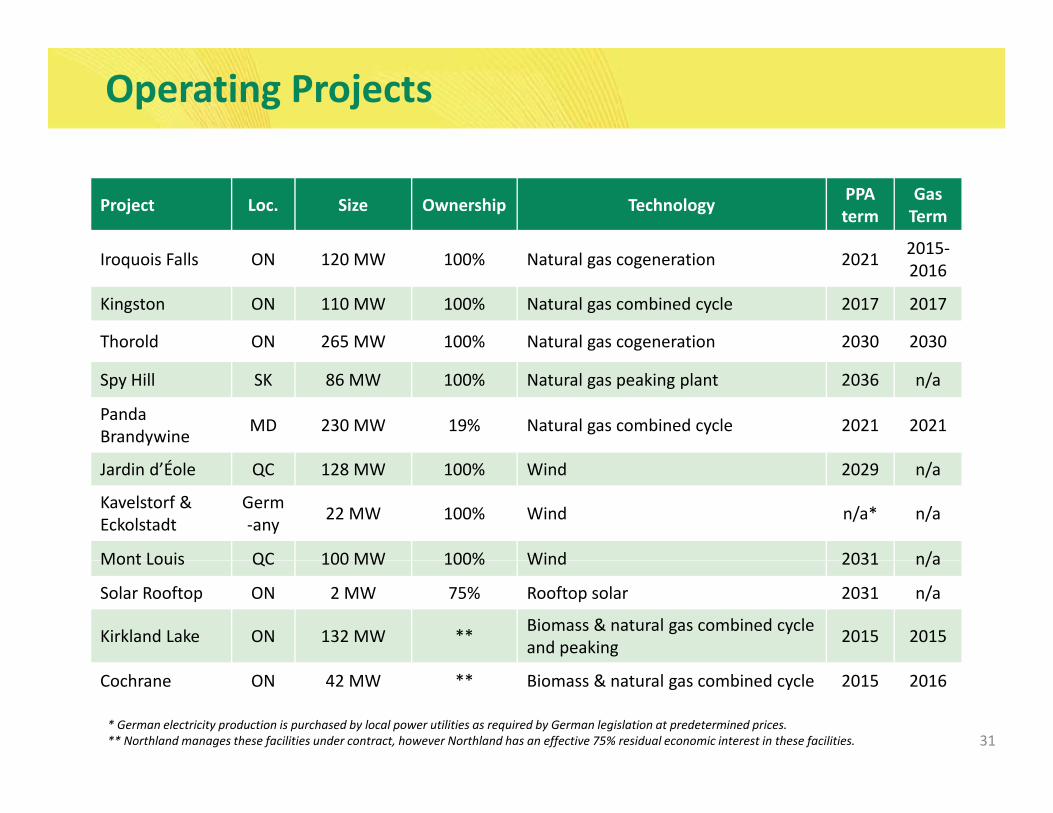

Operating Projects

Project Loc. Size Ownership Technology PPAterm

Gas Term

ll l 2015‐Iroquois Falls ON 120 MW 100% Natural gas cogeneration 2021 20152016

Kingston ON 110 MW 100% Natural gas combined cycle 2017 2017

Thorold ON 265 MW 100% Natural gas cogeneration 2030 2030

Spy Hill SK 86 MW 100% Natural gas peaking plant 2036 n/a

PandaBrandywine MD 230 MW 19% Natural gas combined cycle 2021 2021

Jardin d’Éole QC 128 MW 100% Wind 2029 n/a

Kavelstorf &Eckolstadt

Germ‐any 22 MW 100% Wind n/a* n/a

Mont Louis QC 100 MW 100% Wind 2031 n/aMont Louis QC 100 MW 100% Wind 2031 n/a

Solar Rooftop ON 2 MW 75% Rooftop solar 2031 n/a

Kirkland Lake ON 132 MW ** Biomass & natural gas combined cycleand peaking 2015 2015

31

Cochrane ON 42 MW ** Biomass & natural gas combined cycle 2015 2016

* German electricity production is purchased by local power utilities as required by German legislation at predetermined prices.** Northland manages these facilities under contract, however Northland has an effective 75% residual economic interest in these facilities.

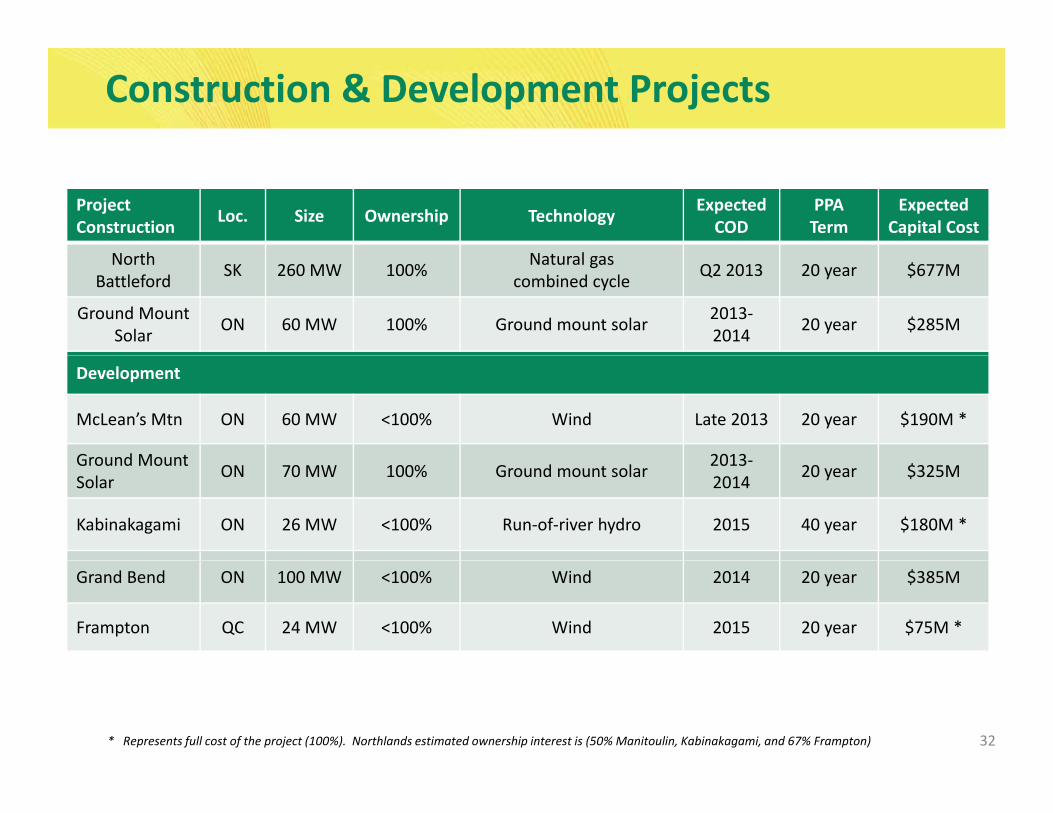

Construction & Development Projects

ProjectConstruction Loc. Size Ownership Technology Expected

CODPPATerm

Expected Capital Cost

h lNorth Battleford SK 260 MW 100% Natural gas

combined cycle Q2 2013 20 year $677M

Ground Mount Solar ON 60 MW 100% Ground mount solar 2013‐

2014 20 year $285M

Development

McLean’s Mtn ON 60 MW <100% Wind Late 2013 20 year $190M *

Ground Mount 2013Ground MountSolar ON 70 MW 100% Ground mount solar 2013‐

2014 20 year $325M

Kabinakagami ON 26 MW <100% Run‐of‐river hydro 2015 40 year $180M *

Grand Bend ON 100 MW <100% Wind 2014 20 year $385M

Frampton QC 24 MW <100% Wind 2015 20 year $75M *

32* Represents full cost of the project (100%). Northlands estimated ownership interest is (50% Manitoulin, Kabinakagami, and 67% Frampton)

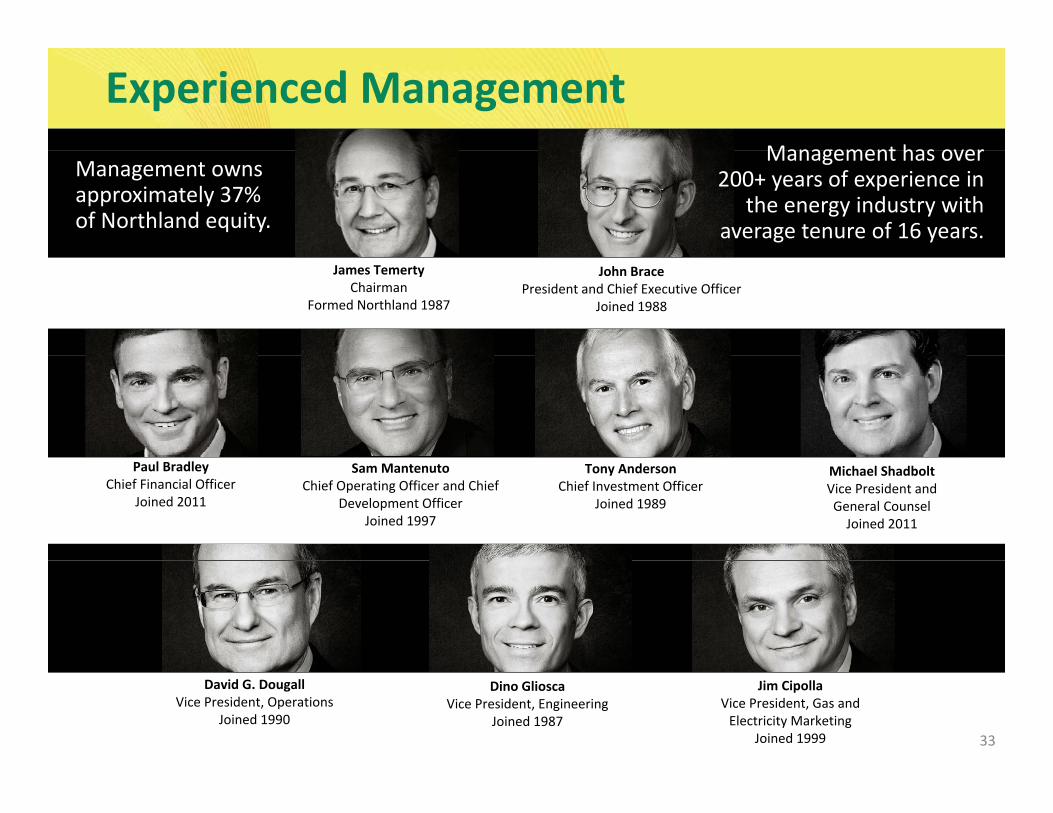

Experienced ManagementManagement has over

Management owns approximately 37% of Northland equity.

Management has over 200+ years of experience in

the energy industry with average tenure of 16 years.

John BracePresident and Chief Executive Officer

Joined 1988

. James Temerty

ChairmanFormed Northland 1987

Michael ShadboltVice President and General CounselJoined 2011

Sam MantenutoChief Operating Officer and Chief

Development OfficerJoined 1997

Tony AndersonChief Investment Officer

Joined 1989

Paul BradleyChief Financial Officer

Joined 2011

33

Jim CipollaVice President, Gas and Electricity Marketing

Joined 1999

Dino GlioscaVice President, Engineering

Joined 1987

David G. DougallVice President, Operations

Joined 1990

Investor Relations Contacts

Adam BeaumontDirector of Finance

647.288.1929

i t l ti @ thl [email protected]

www.northlandpower.ca

Barb BoklaManager, Investor RelationsManager, Investor Relations

647.288.1438

34