northwestern university - european central bank · northwestern university 9th ecb workshop on...

TRANSCRIPT

Priorsforthelongrun

Giannone,Lenza,Prim iceri Priors for the long run

Domenico GiannoneNewYorkFed

MicheleLenzaEuropeanCentralBank

GiorgioPrimiceriNorthwesternUniversity

9th ECB Workshop on Forecasting TechniquesJune3,2016

Giannone,Lenza,Prim iceri Priors for the long run

Whatwedo

n ProposeaclassofpriordistributionsforVARsthatdisciplinethelong-runimplicationsofthemodel

Priorsforthelongrun

Giannone,Lenza,Prim iceri Priors for the long run

Whatwedo

n ProposeaclassofpriordistributionsforVARsthatdisciplinethelong-runimplicationsofthemodel

Priorsforthelongrun

n PropertiesØ BasedonmacroeconomictheoryØ Conjugateà Easy toimplement andcombinewithexistingpriors

n Performwell inapplicationsØ Good(long-run)forecastingperformance

Giannone,Lenza,Prim iceri Priors for the long run

Outline

n Aspecificpathologyof(flat-prior)VARsØ Toomuchexplanatorypowerofinitialconditionsanddeterministic trendsØ Sims(1996and2000)

n PriorsforthelongrunØ IntuitionØ Specificationandimplementation

n Alternativeinterpretationsandrelationwiththeliterature

n Application:macroeconomicforecasting

Giannone,Lenza,Prim iceri Priors for the long run

Simpleexample

n AR(1):

€

yt = c + ρyt−1 +ε t

Giannone,Lenza,Prim iceri Priors for the long run

Simpleexample

n AR(1):

n Iteratebackwards:

€

yt = c + ρyt−1 +ε t

€

yt = ρ t y0 + ρ jcj=0

t−1∑ + ρ jε t− jj=0

t−1∑

Giannone,Lenza,Prim iceri Priors for the long run

Simpleexample

n AR(1):

n Iteratebackwards:

➠ModelseparatesobservedvariationofthedataintoØ DC:deterministic component,predictablefromdataattime0Ø SC:unpredictable/stochastic component

€

yt = c + ρyt−1 +ε t

€

yt = ρ t y0 + ρ jcj=0

t−1∑ + ρ jε t− jj=0

t−1∑

SCDC

Giannone,Lenza,Prim iceri Priors for the long run

Simpleexample

n AR(1):

n Iteratebackwards:

➠ModelseparatesobservedvariationofthedataintoØ DC:deterministic component,predictablefromdataattime0Ø SC:unpredictable/stochastic component

n Ifρ =1,DCisasimplelineartrend:

€

yt = c + ρyt−1 +ε t

€

yt = ρ t y0 + ρ jcj=0

t−1∑ + ρ jε t− jj=0

t−1∑

€

DC = y0 + c⋅ t

SCDC

Giannone,Lenza,Prim iceri Priors for the long run

Simpleexample

n AR(1):

n Iteratebackwards:

➠ModelseparatesobservedvariationofthedataintoØ DC:deterministic component,predictablefromdataattime0Ø SC:unpredictable/stochastic component

n Ifρ =1,DCisasimplelineartrend:

n Otherwisemorecomplex:

€

yt = c + ρyt−1 +ε t

€

yt = ρ t y0 + ρ jcj=0

t−1∑ + ρ jε t− jj=0

t−1∑

€

DC = y0 + c⋅ t

€

DC =c

1− ρ+ ρ t y0 −

c1− ρ

$

% &

'

( )

SCDC

Giannone,Lenza,Prim iceri Priors for the long run

Pathologyof(flat-prior)VARs(Sims,1996and2000)

n OLS/MLEhasatendencyto“use”thecomplexityofdeterministiccomponentstofitthelowfrequencyvariationinthedata

n Possiblebecauseinferenceistypicallyconditionalony0Ø Nopenalizationforparameterestimates ofimplyingsteadystates ortrendsfar

awayfrominitialconditions

Giannone,Lenza,Prim iceri Priors for the long run

DeterministiccomponentsinVARs

n ProblemmoreseverewithVARsØ implieddeterministic component ismuchmorecomplexthaninAR(1)case

Giannone,Lenza,Prim iceri Priors for the long run

DeterministiccomponentsinVARs

n ProblemmoreseverewithVARsØ implieddeterministic component ismuchmorecomplexthaninAR(1)case

n Example:7-variableVAR(5)withquarterlydataonØ GDPØ ConsumptionØ InvestmentØ RealWagesØ HoursØ InflationØ Federalfundsrate

n Sample:1955:I– 1994:IV

n FlatorMinnesotaprior

Giannone,Lenza,Prim iceri Priors for the long run

“Over-fitting”ofdeterministiccomponentsinVARs

1960 1980 2000

5.55.65.75.85.9

66.16.26.36.4

GDP

1960 1980 20003.9

44.14.24.34.44.54.64.7

Investment

1960 1980 2000

-0.65

-0.6

-0.55

-0.5

Hours

1960 1980 2000

-1.7-1.65

-1.6-1.55

-1.5-1.45

-1.4-1.35

-1.3-1.25

Investment-to-GDP ratio

1960 1980 2000-0.015

-0.01-0.005

00.005

0.010.015

0.020.025

Inflation

1960 1980 2000

-0.01

0

0.01

0.02

0.03

0.04

Interest rate

Data Flat MN PLR

Giannone,Lenza,Prim iceri Priors for the long run

“Over-fitting”ofdeterministiccomponentsinVARs

1960 1980 2000

5.55.65.75.85.9

66.16.26.36.4

GDP

1960 1980 20003.9

44.14.24.34.44.54.64.7

Investment

1960 1980 2000

-0.65

-0.6

-0.55

-0.5

Hours

1960 1980 2000

-1.7-1.65

-1.6-1.55

-1.5-1.45

-1.4-1.35

-1.3-1.25

Investment-to-GDP ratio

1960 1980 2000-0.015

-0.01-0.005

00.005

0.010.015

0.020.025

Inflation

1960 1980 2000

-0.01

0

0.01

0.02

0.03

0.04

Interest rate

Data Flat MN PLR

Giannone,Lenza,Prim iceri Priors for the long run

Pathologyof(flat-prior)VARs(Sims,1996and2000)

n OLS/MLEhasatendencyto“use”thecomplexityofdeterministiccomponentstofitthelowfrequencyvariationinthedata

n Possiblebecauseinferenceistypicallyconditionalony0Ø Nopenalizationforparameterestimates ofimplyingsteadystates ortrendsfar

awayfrominitialconditions

➠Flat-priorVARsattributean(implausibly) largeshareofthelowfrequencyvariationinthedatatodeterministiccomponents

Giannone,Lenza,Prim iceri Priors for the long run

Pathologyof(flat-prior)VARs(Sims,1996and2000)

n OLS/MLEhasatendencyto“use”thecomplexityofdeterministiccomponentstofitthelowfrequencyvariationinthedata

n Possiblebecauseinferenceistypicallyconditionalony0Ø Nopenalizationforparameterestimates ofimplyingsteadystates ortrendsfar

awayfrominitialconditions

➠Flat-priorVARsattributean(implausibly) largeshareofthelowfrequencyvariationinthedatatodeterministiccomponents

n Needapriorthatdownplaysexcessiveexplanatorypowerofinitialconditionsanddeterministiccomponent

n Onesolution:centerprioron“non-stationarity”

Giannone,Lenza,Prim iceri Priors for the long run

Outline

n Aspecificpathologyof(flat-prior)VARsØ Toomuchexplanatorypowerofinitialconditionsanddeterministic trendsØ Sims(1996and2000)

n PriorsforthelongrunØ IntuitionØ Specificationandimplementation

n Alternativeinterpretationsandrelationwiththeliterature

n Application:macroeconomicforecasting

Giannone,Lenza,Prim iceri Priors for the long run

Priorforthelongrun

€

VAR(1) : yt = c + Byt−1 +ε t , ε t ~ N 0,Σ( )

Giannone,Lenza,Prim iceri Priors for the long run

Priorforthelongrun

n RewritetheVARintermsoflevelsanddifferences:

€

VAR(1) : yt = c + Byt−1 +ε t , ε t ~ N 0,Σ( )

€

Δyt = c +Πyt−1 +ε tΠ = B − I

Giannone,Lenza,Prim iceri Priors for the long run

Priorforthelongrun

n RewritetheVARintermsoflevelsanddifferences:

n Priorforthelongrun prioroncenteredat0

€

VAR(1) : yt = c + Byt−1 +ε t , ε t ~ N 0,Σ( )

€

Δyt = c +Πyt−1 +ε tΠ = B − I

€

Π

Giannone,Lenza,Prim iceri Priors for the long run

Priorforthelongrun

n RewritetheVARintermsoflevelsanddifferences:

n Priorforthelongrun prioroncenteredat0

n Standardapproach(DLS,SZ,andmanyfollowers)Ø Pushcoefficientstowardsallvariablesbeingindependentrandomwalks

€

VAR(1) : yt = c + Byt−1 +ε t , ε t ~ N 0,Σ( )

€

Δyt = c +Πyt−1 +ε tΠ = B − I

€

Π

Giannone,Lenza,Prim iceri Priors for the long run

Priorforthelongrun

n Rewriteas

€

Δyt = c +Πyt−1 +ε t

€

Δyt = c +Π H −1

Λ! " # Hyt−1

˜ y t−1

! " # +ε t

Giannone,Lenza,Prim iceri Priors for the long run

Priorforthelongrun

n Rewriteas

n ChooseH andputprioronΛ conditionalonH

€

Δyt = c +Πyt−1 +ε t

€

Δyt = c +Π H −1

Λ! " # Hyt−1

˜ y t−1

! " # +ε t

Giannone,Lenza,Prim iceri Priors for the long run

Priorforthelongrun

n Rewriteas

n ChooseH andputprioronΛ conditionalonH

n Economictheorysuggeststhatsomelinearcombinationsofy areless(more)likelytoexhibitlong-runtrends

€

Δyt = c +Πyt−1 +ε t

€

Δyt = c +Π H −1

Λ! " # Hyt−1

˜ y t−1

! " # +ε t

Giannone,Lenza,Prim iceri Priors for the long run

Priorforthelongrun

n Rewriteas

n ChooseH andputprioronΛ conditionalonH

n Economictheorysuggeststhatsomelinearcombinationsofy areless(more)likelytoexhibitlong-runtrends

n Loadingsassociatedwiththesecombinationsareless(more)likelytobe0

€

Δyt = c +Πyt−1 +ε t

€

Δyt = c +Π H −1

Λ! " # Hyt−1

˜ y t−1

! " # +ε t

Giannone,Lenza,Prim iceri Priors for the long run

Example:3-variableVARofKPSW

OutputConsumptionInvestment

€

Δyt = c +Π H −1

Λ! " # Hyt−1

˜ y t−1

! " # +ε t

€

1 1 1−1 1 0−1 0 1

#

$

% % %

&

'

( ( (

Giannone,Lenza,Prim iceri Priors for the long run

Example:3-variableVARofKPSW

OutputConsumptionInvestment

€

ΔxtΔctΔit

#

$

% % %

&

'

( ( (

= c +

Λ11 Λ12 Λ13

Λ21 Λ22 Λ23

Λ31 Λ32 Λ33

#

$

% % %

&

'

( ( (

xt−1 + ct−1 + it−1

ct−1 − xt−1

it−1 − xt−1

#

$

% % %

&

'

( ( ( +ε t

€

Δyt = c +Π H −1

Λ! " # Hyt−1

˜ y t−1

! " # +ε t

€

1 1 1−1 1 0−1 0 1

#

$

% % %

&

'

( ( (

Giannone,Lenza,Prim iceri Priors for the long run

Example:3-variableVARofKPSW

OutputConsumptionInvestment

€

ΔxtΔctΔit

#

$

% % %

&

'

( ( (

= c +

Λ11 Λ12 Λ13

Λ21 Λ22 Λ23

Λ31 Λ32 Λ33

#

$

% % %

&

'

( ( (

xt−1 + ct−1 + it−1

ct−1 − xt−1

it−1 − xt−1

#

$

% % %

&

'

( ( ( +ε t

€

Δyt = c +Π H −1

Λ! " # Hyt−1

˜ y t−1

! " # +ε t

Possibly stationary linear combinations

€

1 1 1−1 1 0−1 0 1

#

$

% % %

&

'

( ( (

Giannone,Lenza,Prim iceri Priors for the long run

Example:3-variableVARofKPSW

OutputConsumptionInvestment

€

ΔxtΔctΔit

#

$

% % %

&

'

( ( (

= c +

Λ11 Λ12 Λ13

Λ21 Λ22 Λ23

Λ31 Λ32 Λ33

#

$

% % %

&

'

( ( (

xt−1 + ct−1 + it−1

ct−1 − xt−1

it−1 − xt−1

#

$

% % %

&

'

( ( ( +ε t

€

Δyt = c +Π H −1

Λ! " # Hyt−1

˜ y t−1

! " # +ε t

Common trend

Possibly stationary linear combinations

€

1 1 1−1 1 0−1 0 1

#

$

% % %

&

'

( ( (

Giannone,Lenza,Prim iceri Priors for the long run

Example:3-variableVARofKPSW

OutputConsumptionInvestment

€

ΔxtΔctΔit

#

$

% % %

&

'

( ( (

= c +

Λ11 Λ12 Λ13

Λ21 Λ22 Λ23

Λ31 Λ32 Λ33

#

$

% % %

&

'

( ( (

xt−1 + ct−1 + it−1

ct−1 − xt−1

it−1 − xt−1

#

$

% % %

&

'

( ( ( +ε t

€

Δyt = c +Π H −1

Λ! " # Hyt−1

˜ y t−1

! " # +ε t

Common trend

Possibly stationary linear combinations

€

1 1 1−1 1 0−1 0 1

#

$

% % %

&

'

( ( (

Giannone,Lenza,Prim iceri Priors for the long run

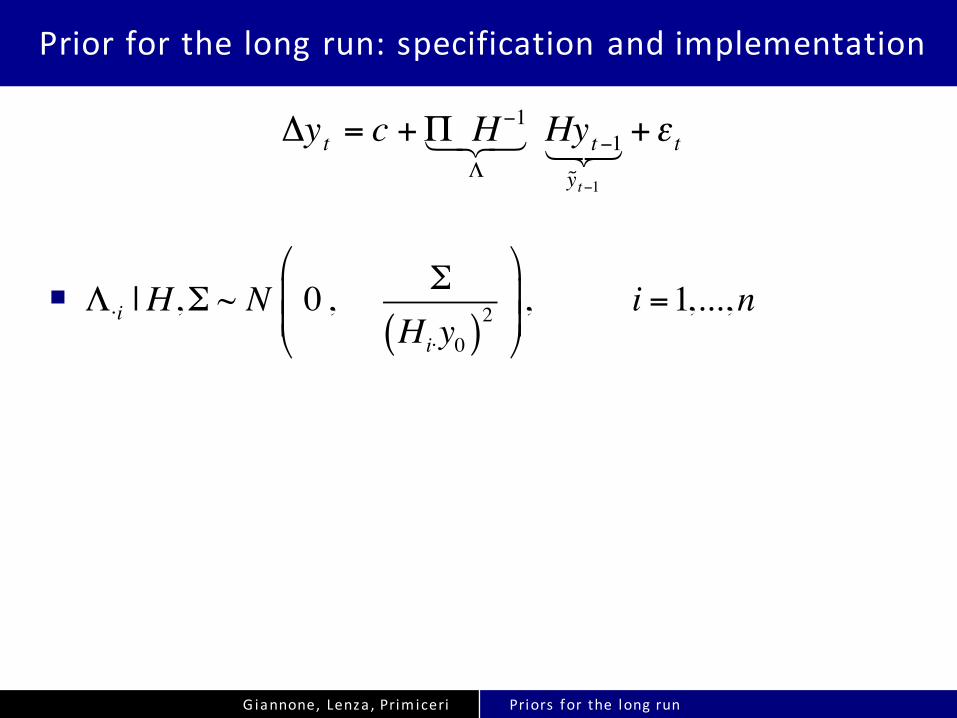

Priorforthelongrun:specificationandimplementation

n

€

Δyt = c +Π H −1

Λ! " # Hyt−1

˜ y t−1

! " # +ε t

Λ⋅i |H,Σ ~ N 0 , φi2 Σ

Hi⋅y0( )2 $

%&&

'

()), i =1,...,n

Giannone,Lenza,Prim iceri Priors for the long run

Priorforthelongrun:specificationandimplementation

n

€

Δyt = c +Π H −1

Λ! " # Hyt−1

˜ y t−1

! " # +ε t

Λ⋅i |H,Σ ~ N 0 , φi2 Σ

Hi⋅y0( )2 $

%&&

'

()), i =1,...,n

Giannone,Lenza,Prim iceri Priors for the long run

Priorforthelongrun:specificationandimplementation

n

n ConjugateØ Canimplement itwithTheilmixedestimation intheVARinlevels

€

Δyt = c +Π H −1

Λ! " # Hyt−1

˜ y t−1

! " # +ε t

Λ⋅i |H,Σ ~ N 0 , φi2 Σ

Hi⋅y0( )2 $

%&&

'

()), i =1,...,n

Giannone,Lenza,Prim iceri Priors for the long run

Priorforthelongrun:specificationandimplementation

n

n ConjugateØ Canimplement itwithTheilmixedestimation intheVARinlevelsØ Canbeeasilycombinedwithexistingpriors

€

Δyt = c +Π H −1

Λ! " # Hyt−1

˜ y t−1

! " # +ε t

Λ⋅i |H,Σ ~ N 0 , φi2 Σ

Hi⋅y0( )2 $

%&&

'

()), i =1,...,n

Giannone,Lenza,Prim iceri Priors for the long run

Priorforthelongrun:specificationandimplementation

n

n ConjugateØ Canimplement itwithTheilmixedestimation intheVARinlevelsØ CanbeeasilycombinedwithexistingpriorsØ CancomputetheMLinclosedform

n Usefulforhierarchicalmodelingandsettingofhyperparameters ϕ (GLP,2013)

€

Δyt = c +Π H −1

Λ! " # Hyt−1

˜ y t−1

! " # +ε t

Λ⋅i |H,Σ ~ N 0 , φi2 Σ

Hi⋅y0( )2 $

%&&

'

()), i =1,...,n

Giannone,Lenza,Prim iceri Priors for the long run

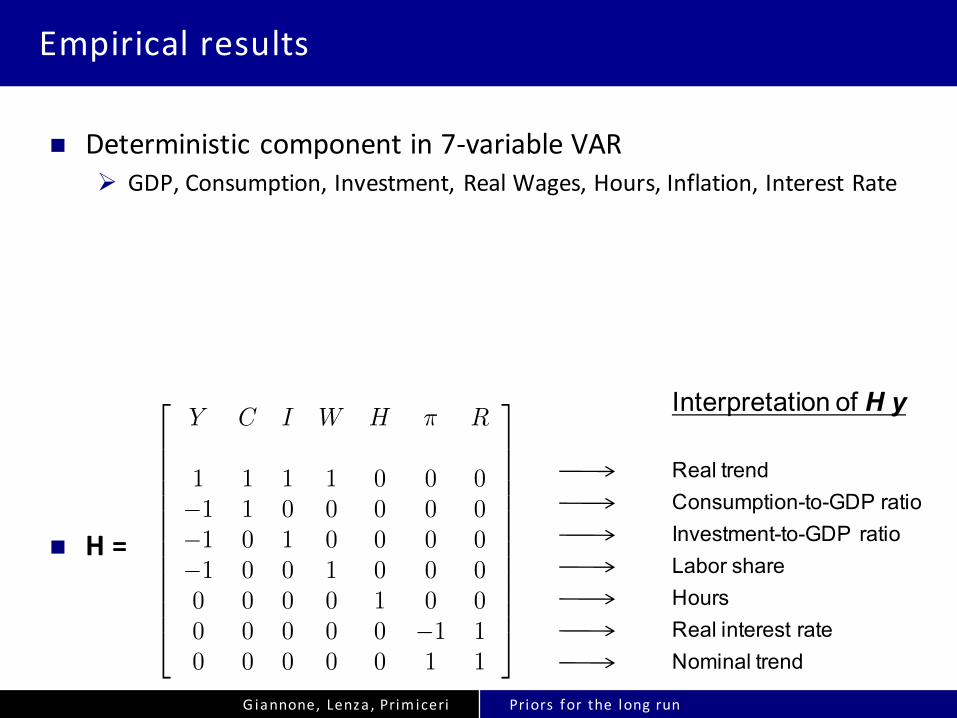

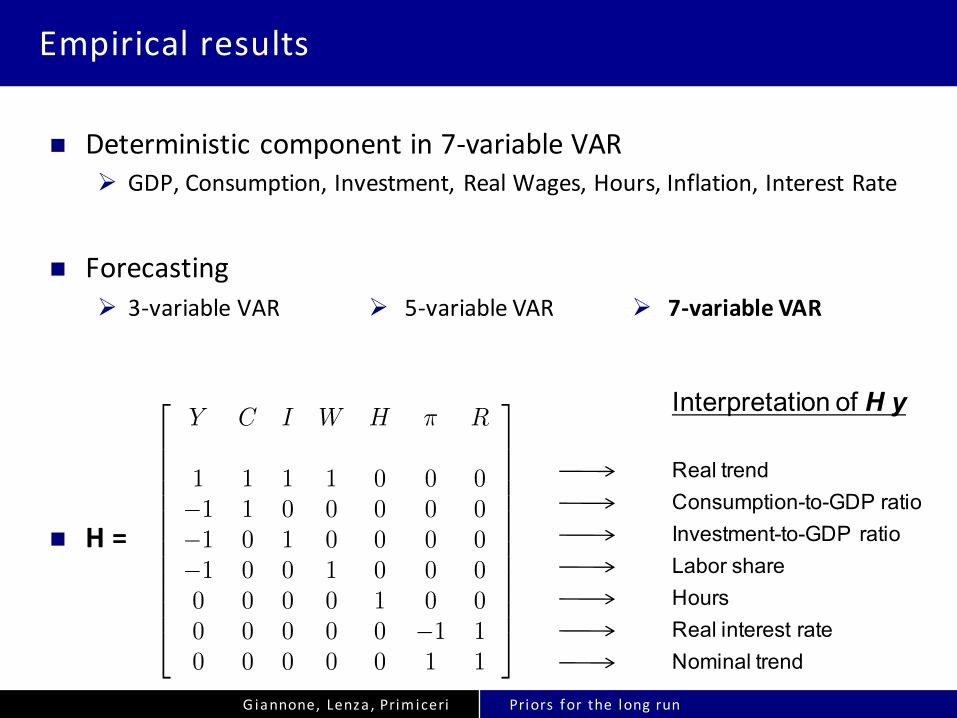

Empiricalresults

n Deterministiccomponentin7-variableVAR

n ForecastingØ 3-variableVARØ 5-variableVARØ 7-variableVAR

Giannone,Lenza,Prim iceri Priors for the long run

Empiricalresults

n Deterministiccomponentin7-variableVAR

Giannone,Lenza,Prim iceri Priors for the long run

Empiricalresults

n Deterministiccomponentin7-variableVARØ GDP,Consumption,Investment,RealWages,Hours,Inflation,InterestRate

Giannone,Lenza,Prim iceri Priors for the long run

Empiricalresults

n Deterministiccomponentin7-variableVARØ GDP,Consumption,Investment,RealWages,Hours,Inflation,InterestRate

n H=

Real trendConsumption-to-GDP ratioInvestment-to-GDP ratioLabor shareHoursReal interest rateNominal trend

Interpretation of H y2

6666666666664

Y C I W H ⇡ R

1 1 1 1 0 0 0�1 1 0 0 0 0 0�1 0 1 0 0 0 0�1 0 0 1 0 0 00 0 0 0 1 0 00 0 0 0 0 �1 10 0 0 0 0 1 1

3

7777777777775

1

Giannone,Lenza,Prim iceri Priors for the long run

Empiricalresults

n Deterministiccomponentin7-variableVARØ GDP,Consumption,Investment,RealWages,Hours,Inflation,InterestRate

n ForecastingØ 3-variableVAR

n H=

Real trendConsumption-to-GDP ratioInvestment-to-GDP ratioLabor shareHoursReal interest rateNominal trend

Interpretation of H y2

6666666666664

Y C I W H ⇡ R

1 1 1 1 0 0 0�1 1 0 0 0 0 0�1 0 1 0 0 0 0�1 0 0 1 0 0 00 0 0 0 1 0 00 0 0 0 0 �1 10 0 0 0 0 1 1

3

7777777777775

1

Ø 5-variableVAR Ø 7-variableVAR

Giannone,Lenza,Prim iceri Priors for the long run

Empiricalresults

n Deterministiccomponentin7-variableVARØ GDP,Consumption,Investment,RealWages,Hours,Inflation,InterestRate

n ForecastingØ 3-variableVAR

n H=

Real trendConsumption-to-GDP ratioInvestment-to-GDP ratioLabor shareHoursReal interest rateNominal trend

Interpretation of H y2

6666666666664

Y C I W H ⇡ R

1 1 1 1 0 0 0�1 1 0 0 0 0 0�1 0 1 0 0 0 0�1 0 0 1 0 0 00 0 0 0 1 0 00 0 0 0 0 �1 10 0 0 0 0 1 1

3

7777777777775

1

Ø 5-variableVAR Ø 7-variableVAR

Giannone,Lenza,Prim iceri Priors for the long run

Empiricalresults

n Deterministiccomponentin7-variableVARØ GDP,Consumption,Investment,RealWages,Hours,Inflation,InterestRate

n ForecastingØ 3-variableVAR

n H=

Real trendConsumption-to-GDP ratioInvestment-to-GDP ratioLabor shareHoursReal interest rateNominal trend

Interpretation of H y2

6666666666664

Y C I W H ⇡ R

1 1 1 1 0 0 0�1 1 0 0 0 0 0�1 0 1 0 0 0 0�1 0 0 1 0 0 00 0 0 0 1 0 00 0 0 0 0 �1 10 0 0 0 0 1 1

3

7777777777775

1

Ø 5-variableVAR Ø 7-variableVAR

Giannone,Lenza,Prim iceri Priors for the long run

DeterministiccomponentsinVARs

1960 1980 2000

5.55.65.75.85.9

66.16.26.36.4

GDP

1960 1980 20003.9

44.14.24.34.44.54.64.7

Investment

1960 1980 2000

-0.65

-0.6

-0.55

-0.5

Hours

1960 1980 2000

-1.7-1.65

-1.6-1.55

-1.5-1.45

-1.4-1.35

-1.3-1.25

Investment-to-GDP ratio

1960 1980 2000-0.015

-0.01-0.005

00.005

0.010.015

0.020.025

Inflation

1960 1980 2000

-0.01

0

0.01

0.02

0.03

0.04

Interest rate

Data Flat MN PLR

Giannone,Lenza,Prim iceri Priors for the long run

DeterministiccomponentsinVARswithPriorfortheLongRun

1960 1980 2000

5.5

6

6.5GDP

1960 1980 2000

4

4.2

4.4

4.6

4.8

5Investment

1960 1980 2000

-0.65

-0.6

-0.55

-0.5

Hours

1960 1980 2000

-1.7-1.65

-1.6-1.55

-1.5-1.45

-1.4-1.35

-1.3-1.25

Investment-to-GDP ratio

1960 1980 2000-0.015

-0.01-0.005

00.005

0.010.015

0.020.025

Inflation

1960 1980 2000

-0.01

0

0.01

0.02

0.03

0.04

Interest rate

Data Flat MN PLR

Giannone,Lenza,Prim iceri Priors for the long run

Forecastingresultswith3-,5- and7-variableVARs

n Recursiveestimationstartsin1955:I

n Forecast-evaluationsample:1985:I– 2013:I

Giannone,Lenza,Prim iceri Priors for the long run

3-variableVAR:MSFE(1985-2013)

0 10 20 30 40

MSF

E

0

0.002

0.004

0.006

0.008

0.01Y

Quarters ahead0 10 20 30 40

MSF

E

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14Y + C + I

0 10 20 30 40 0

0.002

0.004

0.006

0.008

0.01

0.012

0.014C

Quarters ahead0 10 20 30 40

0

0.0002

0.0004

0.0006

0.0008

0.001

0.0012C - Y

0 10 20 30 40 0

0.01

0.02

0.03

0.04

0.05

0

0.01

0.02

0.03I

Quarters ahead0 10 20 30 40

0

0.005

0.01

0.015

0.02

0.025

0.03I - Y

MN SZ Naive PLR

Giannone,Lenza,Prim iceri Priors for the long run

3-variableVAR:MSFE(1985-2013)

0 10 20 30 40

MSF

E

0

0.002

0.004

0.006

0.008

0.01Y

Quarters ahead0 10 20 30 40

MSF

E

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14Y + C + I

0 10 20 30 40 0

0.002

0.004

0.006

0.008

0.01

0.012

0.014C

Quarters ahead0 10 20 30 40

0

0.0002

0.0004

0.0006

0.0008

0.001

0.0012C - Y

0 10 20 30 40 0

0.01

0.02

0.03

0.04

0.05I

Quarters ahead0 10 20 30 40

0

0.005

0.01

0.015

0.02

0.025

0.03I - Y

MN SZ Naive PLR

Giannone,Lenza,Prim iceri Priors for the long run

Consumption- andInvestment-to-GDPratios

1960 1970 1980 1990 2000 2010-0.65

-0.6

-0.55

-0.5

C - Y

1960 1970 1980 1990 2000 2010-1.7

-1.6

-1.5

-1.4

-1.3

I - Y

Actual Naive PLR

Giannone,Lenza,Prim iceri Priors for the long run

Forecasts(5yearsahead)

1960 1970 1980 1990 2000 2010-0.65

-0.6

-0.55

-0.5

C - Y

1960 1970 1980 1990 2000 2010-1.7

-1.6

-1.5

-1.4

-1.3

I - Y

Actual Naive PLR

Giannone,Lenza,Prim iceri Priors for the long run

Forecasts(5yearsahead)

1960 1970 1980 1990 2000 2010-0.65

-0.6

-0.55

-0.5

C - Y

1960 1970 1980 1990 2000 2010-1.7

-1.6

-1.5

-1.4

-1.3

I - Y

Actual Naive PLR

Giannone,Lenza,Prim iceri Priors for the long run

5-variableVAR:MSFE(1985-2013)

0 10 20 30 40

MSF

E

0

0.001

0.002

0.003

0.004

0.005

0.006

0.007

0.008Y

0 10 20 30 40M

SFE

0

0.002

0.004

0.006

0.008

0.01

0.012C

0 10 20 30 40

MSF

E

0

0.01

0.02

0.03

0.04

0.05

0.06

0.07

0.08I

Quarters Ahead0 10 20 30 40

MSF

E

0

0.001

0.002

0.003

0.004

0.005

0.006

0.007H

Quarters Ahead0 10 20 30 40

MSF

E

0

0.002

0.004

0.006

0.008

0.01

0.012W

MNSZNaivePLR

Giannone,Lenza,Prim iceri Priors for the long run

7-variableVAR:MSFE(1985-2013)

0 20 40

MSF

E

00.0010.0020.0030.0040.0050.0060.0070.0080.009 0.01

Y

0 20 40

MSF

E

0

0.002

0.004

0.006

0.008

0.01

0.012

0.014C

0 20 40

MSF

E

0

0.01

0.02

0.03

0.04

0.05

0.06

0.07

0.08I

0 20 40

MSF

E

0

0.001

0.002

0.003

0.004

0.005

0.006

0.007

0.008

0.009H

Quarters Ahead0 20 40

MSF

E

00.0020.0040.0060.008 0.01

0.0120.0140.0160.018 0.02

W

Quarters Ahead0 20 40

MSF

E

0

2e-05

4e-05

6e-05

8e-05

0.0001

0.00012:

Quarters Ahead0 20 40

MSF

E

0

5e-05

0.0001

0.00015

0.0002

0.00025

0.0003R

MNSZNaivePLR

𝝅

Giannone,Lenza,Prim iceri Priors for the long run

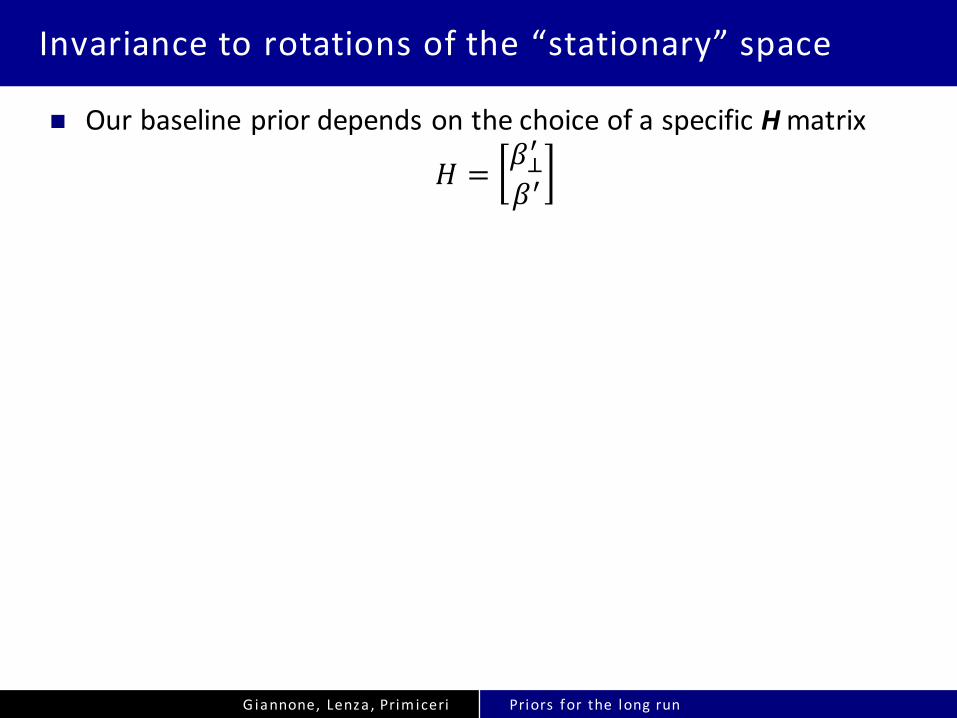

Invariancetorotationsofthe“stationary”space

n OurbaselinepriordependsonthechoiceofaspecificHmatrix

𝐻 = 𝛽%&

𝛽&

Giannone,Lenza,Prim iceri Priors for the long run

Invariancetorotationsofthe“stationary”space

n OurbaselinepriordependsonthechoiceofaspecificHmatrix

𝐻 = 𝛽%&

𝛽&

n Economictheoryisuseful,butnotsufficienttouniquelypindownHØ Macromodelsaretypically informativeabout𝜷%andsp(𝜷)

Giannone,Lenza,Prim iceri Priors for the long run

Invariancetorotationsofthe“stationary”space

n OurbaselinepriordependsonthechoiceofaspecificHmatrix

𝐻 = 𝛽%&

𝛽&

n Economictheoryisuseful,butnotsufficienttouniquelypindownHØ Macromodelsaretypically informativeabout𝜷%andsp(𝜷)

➠ ExtensionofourPLRthatisinvarianttorotationsof𝜷

Giannone,Lenza,Prim iceri Priors for the long run

Invariancetorotationsofthe“stationary”space

n OurbaselinepriordependsonthechoiceofaspecificHmatrix

𝐻 = 𝛽%&

𝛽&

n Economictheoryisuseful,butnotsufficienttouniquelypindownHØ Macromodelsaretypically informativeabout𝜷%andsp(𝜷)

➠ ExtensionofourPLRthatisinvarianttorotationsof𝜷

BaselinePLR: Λ*+ * 𝐻+*𝑦-. |𝐻, Σ~𝑁 0,𝜙+6Σ , 𝑖 = 1, … ,𝑛

Giannone,Lenza,Prim iceri Priors for the long run

Invariancetorotationsofthe“stationary”space

n OurbaselinepriordependsonthechoiceofaspecificHmatrix

𝐻 = 𝛽%&

𝛽&

n Economictheoryisuseful,butnotsufficienttouniquelypindownHØ Macromodelsaretypically informativeabout𝜷%andsp(𝜷)

➠ ExtensionofourPLRthatisinvarianttorotationsof𝜷

BaselinePLR: Λ*+ * 𝐻+*𝑦-. |𝐻, Σ~𝑁 0,𝜙+6Σ , 𝑖 = 1, … ,𝑛

InvariantPLR: ;Λ*+ * 𝐻+*𝑦-. |𝐻, Σ~𝑁 0,𝜙+6Σ , 𝑖 = 1, … ,𝑛 − 𝑟

∑ Λ*+ * 𝐻+*𝑦-. |𝐻, Σ~𝑁 0,𝜙?@ABC6 Σ?+D?@ABC

Giannone,Lenza,Prim iceri Priors for the long run

7-variableVAR:Forecasting resultswith“invariant”PLR

0 20 40

MS

FE

0

0.002

0.004

0.006

0.008

0.01Y

0 20 40M

SFE

0

0.002

0.004

0.006

0.008

0.01C

0 20 40

MS

FE

0

0.01

0.02

0.03

0.04

0.05I

0 20 40

MS

FE

0

0.002

0.004

0.006

0.008H

0 20 40

MS

FE

0

2e-05

4e-05

6e-05

8e-05

0.0001π

0 20 40M

SFE

0

2e-05

4e-05

6e-05

8e-05

0.0001

0.00012R

Quarters Ahead0 20 40

MS

FE

0

0.0005

0.001

0.0015

0.002

0.0025

0.003C - Y

Quarters Ahead0 20 40

MS

FE

0

0.005

0.01

0.015

0.02

0.025I - Y

Quarters Ahead0 20 40

MS

FE

0

0.0005

0.001

0.0015

0.002W - Y

PLR baseline PLR invariant PLR invariant (except C-Y)

Giannone,Lenza,Prim iceri Priors for the long run

Hy inthedata

1940 1960 1980 2000 2020-0.7

-0.65

-0.6

-0.55

-0.5

-0.45C-Y

1940 1960 1980 2000 2020-1.8

-1.7

-1.6

-1.5

-1.4

-1.3

-1.2I-Y

1940 1960 1980 2000 2020-0.72-0.7-0.68-0.66-0.64-0.62-0.6-0.58-0.56-0.54-0.52

H

1940 1960 1980 2000 2020-0.62

-0.6

-0.58

-0.56

-0.54

-0.52

-0.5W-Y

1940 1960 1980 2000 2020-0.01

0

0.01

0.02

0.03

0.04

0.05

0.06

0.07R+:

1940 1960 1980 2000 2020-0.01

-0.005

0

0.005

0.01

0.015

0.02

0.025

0.03R-:𝝅 𝝅

Giannone,Lenza,Prim iceri Priors for the long run

7-variableVAR:Forecasting resultswith“invariant”PLR

0 20 40

MS

FE

0

0.002

0.004

0.006

0.008

0.01Y

0 20 40M

SFE

0

0.002

0.004

0.006

0.008

0.01C

0 20 40

MS

FE

0

0.01

0.02

0.03

0.04

0.05I

0 20 40

MS

FE

0

0.002

0.004

0.006

0.008H

0 20 40

MS

FE

0

2e-05

4e-05

6e-05

8e-05

0.0001π

0 20 40M

SFE

0

2e-05

4e-05

6e-05

8e-05

0.0001

0.00012R

Quarters Ahead0 20 40

MS

FE

0

0.0005

0.001

0.0015

0.002

0.0025

0.003C - Y

Quarters Ahead0 20 40

MS

FE

0

0.005

0.01

0.015

0.02

0.025I - Y

Quarters Ahead0 20 40

MS

FE

0

0.0005

0.001

0.0015

0.002W - Y

PLR baseline PLR invariant PLR invariant (except C-Y)

Giannone,Lenza,Prim iceri Priors for the long run

Strengthsandweaknesses

n StrengthsØ Imposesdiscipline onlong-runbehaviorofthemodelØ BasedonrobustlessonsoftheoreticalmacromodelsØ Performswellinforecasting(especially atlongerhorizons)Ø Veryeasytoimplement

Giannone,Lenza,Prim iceri Priors for the long run

Strengthsandweaknesses

n StrengthsØ Imposesdiscipline onlong-runbehaviorofthemodelØ BasedonrobustlessonsoftheoreticalmacromodelsØ Performswellinforecasting(especially atlongerhorizons)Ø Veryeasytoimplement

n “Weak”pointsØ Non-automaticprocedureà needtothinkaboutitØ Mightprovedifficulttosetupinlarge-scalemodelsà mightrequiretoo

muchthinking

Giannone,Lenza,Prim iceri Priors for the long run

Connectionsandextremecases

n Rewriteas

€

Δyt = c +Π H −1

Λ! " # Hyt−1

˜ y t−1

! " # +ε t

Δyt = c+ Λ1 Λ2[ ] β⊥ 'β '$

%&

'

()yt−1 +εt

Giannone,Lenza,Prim iceri Priors for the long run

Connectionsandextremecases

n Rewriteas

€

Δyt = c +Π H −1

Λ! " # Hyt−1

˜ y t−1

! " # +ε t

Δyt = c+ Λ1 Λ2[ ] β⊥ 'β '$

%&

'

()yt−1 +εt

Δyt = c+Λ1β⊥ ' yt−1 +Λ2β ' yt−1 +εt

Giannone,Lenza,Prim iceri Priors for the long run

Connectionsandextremecases

€

Δyt = c +Λ1β⊥' yt−1 +Λ2β' yt−1 +ε t

Giannone,Lenza,Prim iceri Priors for the long run

Connectionsandextremecases

n ErrorCorrectionModel:dogmaticprioronΛ1=0

€

Δyt = c +Λ1β⊥' yt−1 +Λ2β' yt−1 +ε t

Giannone,Lenza,Prim iceri Priors for the long run

Connectionsandextremecases

n ErrorCorrectionModel:dogmaticprioronΛ1=0

€

Δyt = c +Λ1β⊥' yt−1 +Λ2β' yt−1 +ε t

Ø KPSW,CEEn fixβ basedontheoryn flatprioronΛ2

Giannone,Lenza,Prim iceri Priors for the long run

Connectionsandextremecases

n ErrorCorrectionModel:dogmaticprioronΛ1=0

€

Δyt = c +Λ1β⊥' yt−1 +Λ2β' yt−1 +ε t

Ø KPSW,CEEn fixβ basedontheoryn flatprioronΛ2

Ø Cointegrationn estimateβn flatprioronΛ2

n EG(1987)

Giannone,Lenza,Prim iceri Priors for the long run

Connectionsandextremecases

n ErrorCorrectionModel:dogmaticprioronΛ1=0

€

Δyt = c +Λ1β⊥' yt−1 +Λ2β' yt−1 +ε t

Ø Bayesiancointegrationn uniform prioronsp(β)n KSvDV (2006)

Ø Cointegrationn estimateβn flatprioronΛ2

n EG(1987)

Ø KPSW,CEEn fixβ basedontheoryn flatprioronΛ2

Giannone,Lenza,Prim iceri Priors for the long run

Connectionsandextremecases

n ErrorCorrectionModel:dogmaticprioronΛ1=0

n VARinfirstdifferences:dogmaticprioronΛ1=Λ2=0

€

Δyt = c +Λ1β⊥' yt−1 +Λ2β' yt−1 +ε t

Ø KPSW,CEEn fixβ basedontheoryn flatprioronΛ2

Ø Cointegrationn estimateβn flatprioronΛ2

n EG(1987)

Ø Bayesiancointegrationn uniform prioronsp(β)n KSvDV (2006)

Giannone,Lenza,Prim iceri Priors for the long run

Connectionsandextremecases

n ErrorCorrectionModel:dogmaticprioronΛ1=0

n VARinfirstdifferences:dogmaticprioronΛ1=Λ2=0

n Sum-of-coefficientsprior(DLS,SZ)Ø [β’ β’]’ =H=IØ shrinkΛ1 andΛ2 to0

€

Δyt = c +Λ1β⊥' yt−1 +Λ2β' yt−1 +ε t

Ø KPSW,CEEn fixβ basedontheoryn flatprioronΛ2

Ø Cointegrationn estimateβn flatprioronΛ2

n EG(1987)

Ø Bayesiancointegrationn uniform prioronsp(β)n KSvDV (2006)

Giannone,Lenza,Prim iceri Priors for the long run

3-varVAR:MeanSquaredForecastErrors(1985-2013)

0 10 20 30 40

MSF

E

0

0.002

0.004

0.006

0.008

0.01Y

Quarters ahead0 10 20 30 40

MSF

E

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14Y + C + I

0 10 20 30 40 0

0.002

0.004

0.006

0.008

0.01

0.012

0.014C

Quarters ahead0 10 20 30 40

0

0.0002

0.0004

0.0006

0.0008

0.001

0.0012C - Y

0 10 20 30 40 0

0.01

0.02

0.03

0.04

0.05I

Quarters ahead0 10 20 30 40

0

0.005

0.01

0.015

0.02

0.025

0.03I - Y

MN SZ Naive PLR