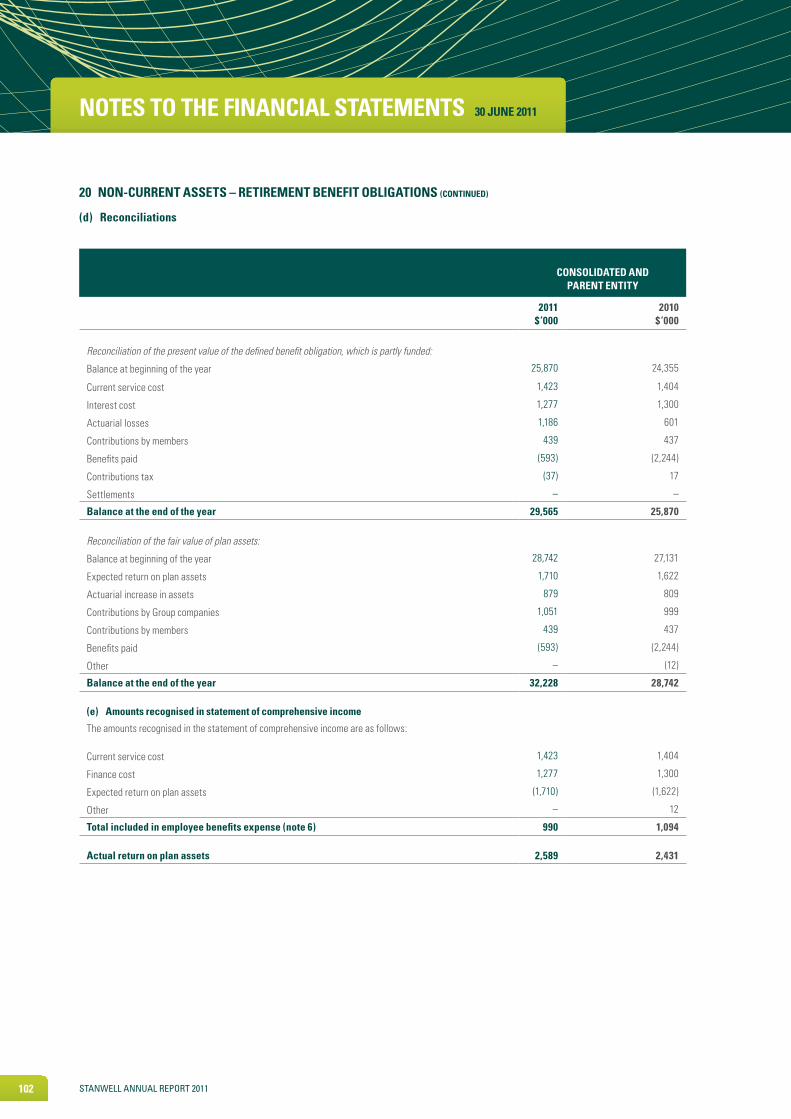

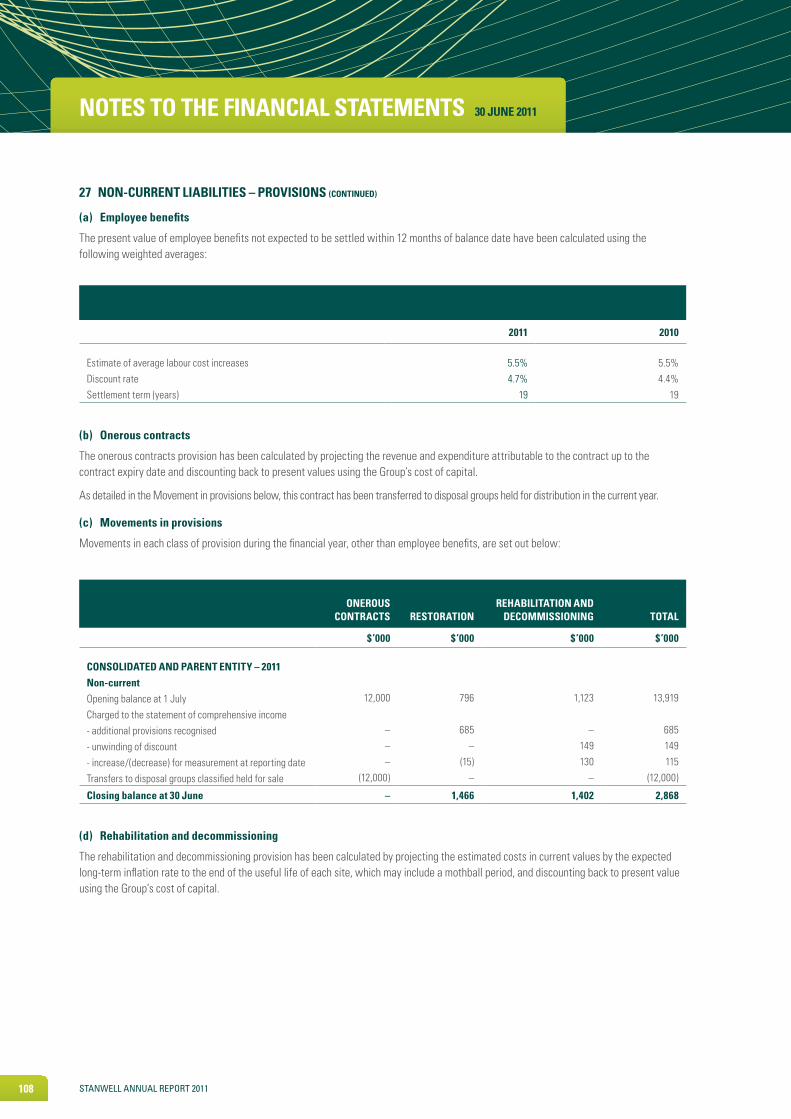

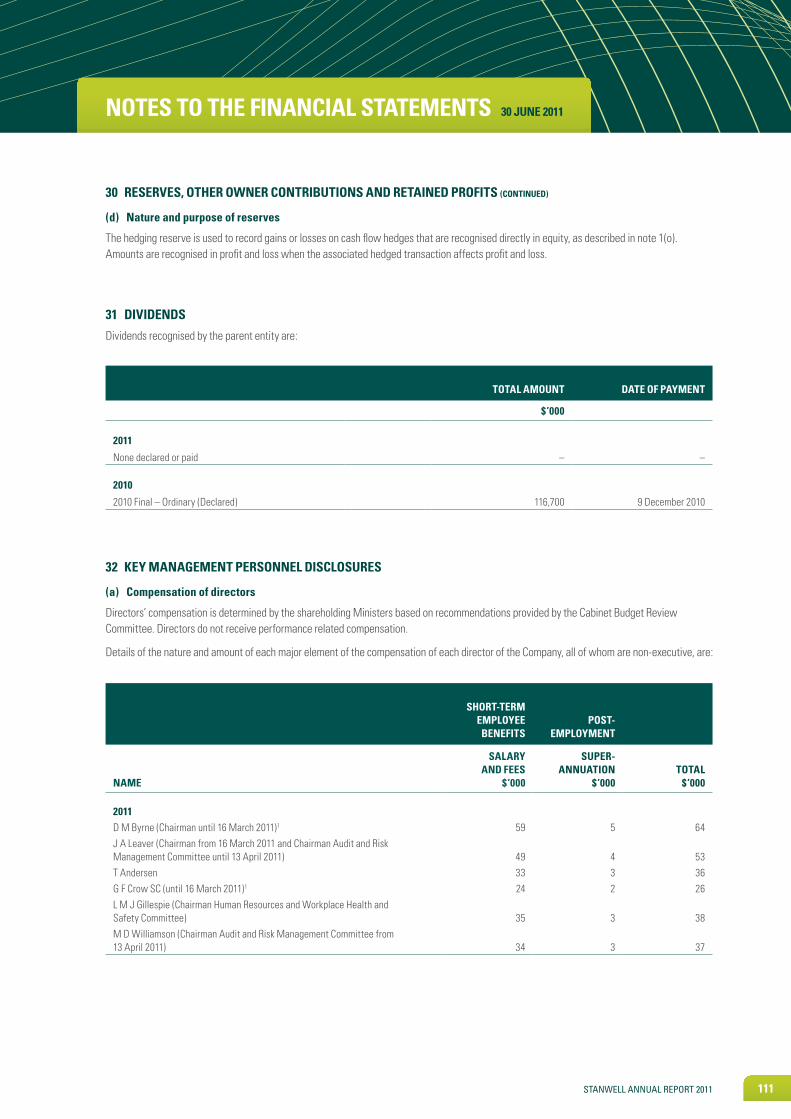

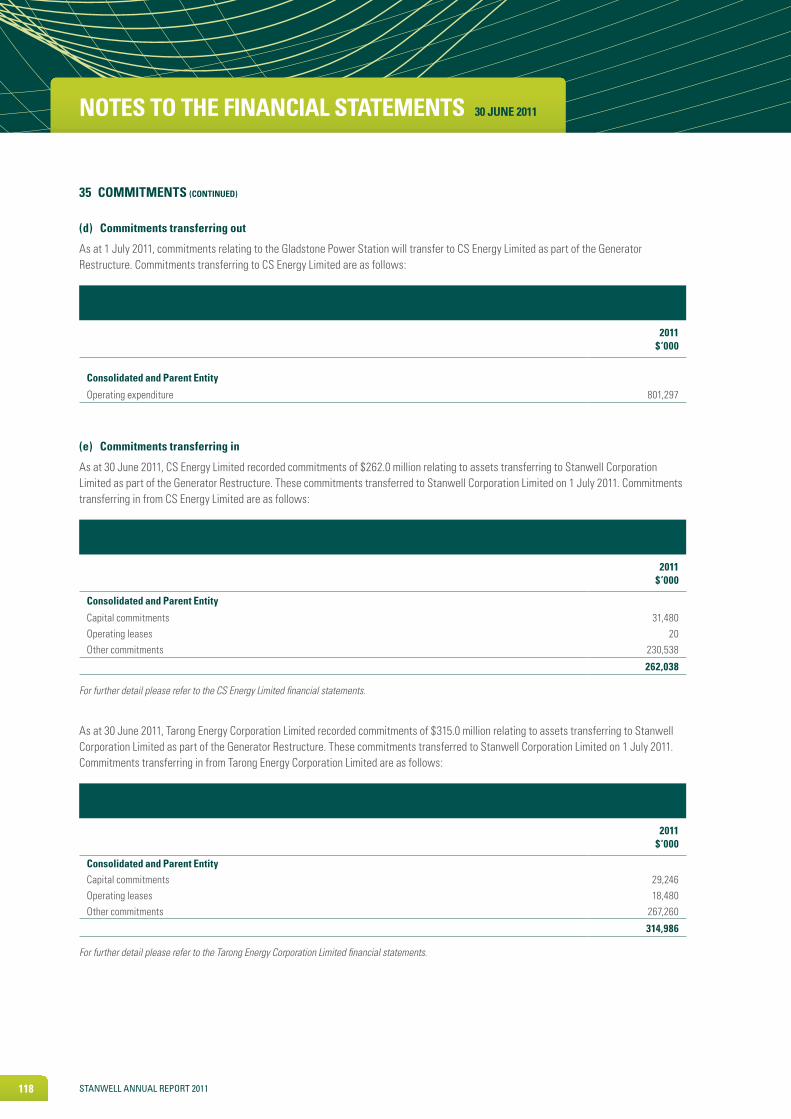

notes to the financial statements 30 june 2011

TRANSCRIPT

AnnuAl RepoRt 2011

ABout tHIS RepoRt

This report provides an accurate and detailed review of the company’s financial and non-financial performance in the 2010–11 financial year against our strategy, objectives and targets detailed in our Statement of Corporate Intent (SCI).

Our strategy, which we report against, is categorised into six key areas:

• Right people

• Right markets

• Right fuels

• Right plant

• Right organisation

• Right locations.

For each of the reporting sections, we have summarised our performance against both SCI and divisional indicators.

This report does not include our objectives for 2011–12.

Following the outcome of the Shareholder Review of Queensland Government Owned Corporation Generators (Genco Review), announced on 25 November 2010, the Queensland Government owned generating sector has been restructured from three Queensland Government owned generating companies (Stanwell

Corporation Limited, Tarong Energy Corporation Limited and CS Energy Limited) to two (Stanwell and CS Energy), with effect from 1 July 2011.

As this affects Stanwell’s business moving forward, the objectives of the restructured company will be a priority for the new Board and Executive Leadership Team.

This report also provides information on other important business processes, such as our approach to corporate governance and risk management.

We are responsibly managing our business to deliver value to our shareholders and, ultimately, to the people of Queensland. Our stakeholders include, but are not limited to, shareholders, employees, contractors, customers, local communities, suppliers, business partners, special interest groups and relevant authorities.

To assist in reading our Annual Report, we have included a glossary of terms and an index at the back of the report. Electronic versions of this and previous years’ annual reports are available online at www.stanwell.com

Stanwell Power Station in Central Queensland

i STanwell annual RepoRT 2011

ABout tHIS RepoRt _________________________________________________________________________________________ i

HIgHlIgHtS ______________________________________________________________________________________________________ 2

FInAncIAl HIgHlIgHtS ____________________________________________________________________________________ 2

WHo We ARe _____________________________________________________________________________________________________ 3

StRAtegIc dIRectIon ______________________________________________________________________________________ 5

YeAR In RevIeW ________________________________________________________________________________________________ 5

peRFoRmAnce oveRvIeW 2010–11 ___________________________________________________________________ 7

YeAR AHeAd 2011–12 _______________________________________________________________________________________ 10

cHAIRmAn’S StAtement _______________________________________________________________________________ 11

meSSAge FRom IncomIng cHAIRmAn __________________________________________________________ 12

ActIng cHIeF executIve oFFIceR’S RevIeW __________________________________________________ 13

BoARd oF dIRectoRS _____________________________________________________________________________________ 15

executIve mAnAgement teAm ___________________________________________________________________ 16

SocIAl peRFoRmAnce ___________________________________________________________________________________ 19

Health and safety _____________________________________________________________________________________________ 19

Employee relations __________________________________________________________________________________________ 21

Community relations _________________________________________________________________________________________ 24

BuSIneSS peRFoRmAnce_______________________________________________________________________________ 27

Operations _____________________________________________________________________________________________________ 27

Market trading _________________________________________________________________________________________________ 31

Project development ________________________________________________________________________________________ 33

envIRonmentAl peRFoRmAnce ___________________________________________________________________ 35

economIc peRFoRmAnce______________________________________________________________________________ 38

coRpoRAte goveRnAnce ______________________________________________________________________________ 40

FInAncIAl ReSultS ________________________________________________________________________________________ 48

gloSSARY _____________________________________________________________________________________________________ 127

ABBRevIAtIonS ___________________________________________________________________________________________ 128

Index ____________________________________________________________________________________________________________ 129

STanwell annual RepoRT 2011 1

Pictured on front cover: Mechanical engineer Scott Coxon outside Stanwell Power Station in Central Queensland

contentS

2 STanwell annual RepoRT 2011

HIgHlIgHtS

• Positive progress towards Zero Harm with a 19.9% reduction in our All Injury Frequency Rate (Health and safety page 19).

• A reduction in Lost Time Injuries from nine last year to two this year (Health and safety page 19).

• No Level 4 or Level 5 environmental incidents. This is the fifth year that this outcome has been achieved (Environmental performance page 35).

• Completed the sale of the Mineral Development Licence 162 coal resource, delivering a profit after tax of $189.7 million (Project development page 33).

• Finalised a Rail Transport Agreement with QR National Coal, providing long-term certainty for the delivery of coal from Central Queensland to Stanwell Power Station (Project development page 33).

• Completed a number of transactions aimed at securing gas supply for future power generation (Project development page 33).

• Undertook a major overhaul of Stanwell Power Station’s Unit 4, which included a low pressure turbine upgrade and generator rewind, delivering a 2.38% improvement in efficiency (Operations page 27).

• Installed low NOx burners on Stanwell Power Station’s Unit 4. This follows the installation of low NOx burners on Unit 3 in 2009. The station has two units, producing 40% less NOx emissions than before (Environmental performance page 35).

• Completed the sale of two wind assets—the Emu Downs Wind Farm and the Badgingarra Wind Development Project, both in Western Australia, completing the divestment of our wind portfolio (Operations page 27).

FInAncIAl HIgHlIgHtS

IndIcAtoRActuAl AnnuAl

cHAnge (%) 2010–11 2009–10 2008–09 2007–08 2006–07

Total revenue ($’000) (15.1) 562,619 662,995 670,367 540,949 515,357

Operating (loss)/profit before income tax equivalent ($’000)

(112.0) (24,579) 205,527 265,903 167,621 222,926

Operating (loss)/profit after income tax equivalent ($’000)

(108.0) (11,992) 149,462 195,605 135,590 155,762

Dividends declared ($’000) (100.0) – 116,700 148,944 92,105 122,301

Total assets ($’000) 5.0 1,814,749 1,981,966 1,930,734 1,916,386 2,626,402

Total liabilities ($’000) (7.5) 1,204,328 1,302,045 973,779 1,183,414 2,291,046

Total shareholders’ equity ($’000) (10.2) 610,421 679,921 956,955 732,972 335,356

Return on total assets* (%) (99.1) 0.0 11.7 14.5 7.5 10.7

Return on total equity** (%) (110.2) (1.9) 18.3 23.1 25.4 22.9

Earnings per share (cents) (108.0) (1.3) 16.2 21.7 13.8 15.9 *Earnings before interest and tax/average total assets

** Operating profit after tax/average total equity.

STanwell annual RepoRT 2011 3

WHo We ARe

we are a Queensland Government owned Corporation, with an energy portfolio comprising gas and coal resources, and thermal and hydro power generation facilities across Queensland.

We have the capacity to trade more than 30% of Queensland’s electricity requirements. Our plant portfolio includes:

• Stanwell Power Station, Central Queensland – 1,434 MW

• Kareeya Hydro, Far North Queensland – 86.4 MW

• Barron Gorge Hydro, Far North Queensland – 60 MW

• Mackay Gas Turbine, North Queensland – 34 MW

• Koombooloomba Hydro, Far North Queensland – 7.3 MW

• Wivenhoe Small Hydro, South East Queensland – 4.3 MW.

In addition to our own generating plant, Stanwell trades the output of Gladstone Power Station (1,680 MW) in the National Electricity Market (NEM).

coRe BuSIneSS

Stanwell bids its available generating capacity into the NEM, a wholesale market for the supply and purchase of electricity managed by the Australian Energy Market Operator (AEMO).

Within the NEM, electricity generators compete for the right to generate electricity into a central pool by submitting competitive price bids to supply nominated quantities of generation in certain timeslots throughout the day. Stanwell sells the electricity from our power stations into this market pool and is paid according to the spot price.

We also make financial transactions in the electricity derivative market to manage the price risk that Stanwell is exposed to in the NEM. These transactions are made with counterparties, which are generally electricity retailers.

ouR cuStomeRS

As an electricity wholesaler, Stanwell has a limited number of wholesale customers (referred to as counterparties).

ouR SHAReHoldeRS

Stanwell was formed on 1 July 1997 under the Government Owned Corporations Act 1993 (Qld) and registered under the Corporations Act 2001 (Cth). All shares are held by the State of Queensland.

HIgHlY SkIlled WoRkFoRce

Stanwell’s highly skilled, experienced and dedicated people are crucial to achieving our business goals and objectives. We employ 371 people directly, and approximately 250 contractors, across a range of professional, technical, trade, and administrative roles, and we value their extensive skills and experience.

Stanwell is committed to providing opportunities for professional development and leadership training (Employee relations page 21).

commItment to HeAltH And SAFetY

The health and safety of our people is our number one priority. Stanwell’s safety vision, “we will manage health and safety risks with a goal that no one gets hurt”, is being embedded in Stanwell’s safety culture through the Safety Improvement Project (SIP) (Health and safety page 19).

commItment to tHe envIRonment

Stanwell’s business strategy is focused on creating options to reduce our carbon intensity from a mixture of coal, gas and renewable energy resources.

Stanwell’s commitment to upgrade its existing plant to improve environmental performance and ongoing research into clean, renewable forms of energy are integral to our future business viability.

With three of our hydro facilities located in the most northern parts of Australia, our management systems recognise the differing sensitivities of the ecosystems which surround our power stations.

ReSponSIBIlItY to ouR communItIeS

Stanwell prides itself on being an active participant in the communities in which we operate, supporting community-driven development including education, environment, and health and safety. Our sponsorship program provides opportunities for financial support and community engagement on both a regional and Queensland-wide level. The diverse nature of our operations enables us to deliver a range of socio-economic benefits, including direct local employment and training, and the procurement of local goods and services.

4 STanwell annual RepoRT 2011

A neW eRA

In November 2010, the Queensland Government announced plans to restructure the three Queensland Government owned generating companies (Stanwell, Tarong Energy Corporation Limited and CS Energy Limited) into two (Stanwell and CS Energy Limited), effective 1 July 2011.

As part of the restructure, from 1 July 2011, Stanwell’s existing assets were combined with the Tarong, Tarong North, Mica Creek and Swanbank power stations, and the trading of the output of the Collinsville Power Station. The trading of the output of the Gladstone Power Station was divested to CS Energy Limited from 1 July 2011.

On 20 June 2011, the shareholding Ministers announced the following appointments to the Stanwell Board with effect from 1 July 2011:

• Graham Carpenter, Chairman, 1 July 2011 to 30 September 2014

• Kym Collins, Director, 1 July 2011 to 30 September 2014

• Graeme Crow SC, Director, 1 October 2008 to 30 September 2013

• Ann Fitzpatrick, Director, 1 July 2011 to 30 September 2014

• Russell Kempnich, Director, 1 July 2011 to 30 September 2013

• Julie Leaver, Director, 1 October 2009 to 30 September 2013

• Stephen Rochester, Director, 1 July 2011 to 30 September 2014

• Rodney Welford, Director, 1 July 2011 to 30 September 2013.

The newly appointed Board convened on 1 July 2011. At that meeting, the Board established two Board committees, and confirmed the members and chairs of those committees as follows:

Audit and Risk committee

• Julie Leaver, Chair

• Graham Carpenter, Member

• Stephen Rochester, Member

• Rodney Welford, Member

people and Safety committee

• Russell Kempnich, Chair

• Graham Carpenter, Member

• Kym Collins, Member

• Graeme Crow SC, Member

• Ann Fitzpatrick, Member.

On 1 July 2011, the Stanwell Board confirmed Helen Gluer’s appointment as Chief Executive Officer (CEO) of the restructured Stanwell entity. The Board also confirmed that the Executive Leadership Team reporting to the CEO, with effect from 1 July 2011, was as follows:

• Jackie Barber, Executive General Manager Marketing and Trading

• Wayne Collins, Chief Operating Officer

• Jenny Gregg, Executive General Manager Human Resources and Stakeholder Engagement

• Michael O’Rourke, Executive General Manger Governance and Corporate Strategy

• Richard Van Breda, Chief Financial Officer

• John Williamson, Executive General Manager Integration.

STanwell annual RepoRT 2011 5

RIgHt people

We recorded two Lost Time Injuries and a 19.9% reduction in our All Injury Frequency Rate (Health and safety page 19)—a substantial improvement on the previous year.

Behavioural-based safety tools were introduced as part of the Safety Improvement Project, along with a substantial investment in safety leadership across the business (Health and safety page 19).

In 2010, seven employees completed Stanwell’s Leadership Development Program, which encourages the leadership and management capabilities of participants. Another seven enrolled in the program in 2011 (Employee relations page 21).

A range of initiatives was offered to all employees to improve their health, wellbeing and fitness. These initiatives included flu vaccinations, health assessments, first aid courses, cancer screenings, and ergonomic assessments (Employee relations page 21).

RIgHt mARketS

We developed robust commercial relationships and enhanced our reputation as a dependable, professional and market-focused trading team, evidenced by the completion of significant new structured contract arrangements with important customers (Market trading page 31).

A new Deal Capture and Settlements System was developed and implemented, enabling us to more effectively and comprehensively measure and manage our financial risks (Market trading page 31).

RIgHt FuelS

We completed a pre-feasibility study into a carbon capture and storage project, which would use integrated gasification combined cycle technology (Project development page 33).

The feasibility study into a proposed hydro power station on the Burdekin Falls Dam in North Queensland made substantial progress (Project development page 33).

The completion of a new Rail Transport Agreement provides long-term certainty for the delivery of coal to Stanwell Power Station (Project development page 33).

Completion of a transaction with Tri-Star has secured access to gas for future gas-fired power projects (Project development page 33).

RIgHt plAnt

An upgrade of the low pressure turbine and a generator rewind on Stanwell Power Station’s Unit 4 delivered a 2.38% improvement in efficiency (Operations page 27).

The installation of low NOx burners on Stanwell Power Station’s Unit 4 has lowered Nitrous Oxide emissions (Operations page 27).

Reliability of the hydro fleet was enhanced with the completion of a stator core rebuild and generator rewind on Unit 1 at Barron Gorge Hydro (Operations page 27).

RIgHt oRgAnISAtIon

We maintained key stakeholder relationships in the areas in which we operate by communicating regularly and supporting regional events and community organisations (Community relations page 24).

RIgHt locAtIonS

We managed our impact on the environment and maintained our right to operate, with no Level 4 or 5 environmental incidents for the fifth consecutive year (Environmental performance page 35).

StRAtegIc dIRectIon

as the outcomes of the Shareholder Review of Queensland Government owned Corporation Generators, announced by the State Government in november 2010, affect Stanwell’s business moving forward, the strategic direction of the company will be a priority for the new Board and executive leadership Team.

YeAR In RevIeW

6 STanwell annual RepoRT 2011

peRFoRmAnce IndIcAtoRS

2010–11 2009–10

target ActualActual annual

change (%) target Actual

FInAncIAl

Total revenue ($m) 522.5 562.6 (15.13) 574.7 663.0

Earnings before interest and tax ($m) 102.9 0.5 (99.8) 242.0 237.4

Profit/(loss) after tax ($m) 44.0 (12.0) (108.0) 95.2 149.5

Net assets ($m) 531.9 610.4 (10.2) 328.9 679.9

Return on total assets (%) 6.3 0.0 (99.2) 8.3 11.7

Return on equity (after interest and tax) (%) 6.4 (1.9) (110.2) 17.3 18.3

Debt/debt + equity (%) 55.3 51.1 5.57 66.0 48.4

Interest cover (times) 2.6 0.0 (99.7) 5.4 5.8

Current ratio (times) 0.5 2.1 4.78 0.6 1.9

opeRAtIonAl

Annual availability (Stanwell Power Station) (%) 91.00 88.32 (3.61) 92.20 91.63

Forced outage factor (Stanwell Power Station) (%) 2.60 1.61 (18.27) 2.40 1.97

HeAltH And SAFetY

lost time Injury Frequency Rates

Employees only 0 1.43 (86.14) 0 10.32

Contractors and employees 0 1.71 (78.08) 0 7.80

envIRonment

environmental incidents

Level 4 or 5 0 0 0 0 0

Kareeya Hydro Power Station in Far North Queensland

STanwell annual RepoRT 2011 7

peRFoRmAnce oveRvIeW 2010–11

each year, we document the nature and scope of our strategies, objectives and actions in our Statement of Corporate Intent (SCI).

As a Queensland Government Owned Corporation, this document is part of our performance agreement with our shareholding Ministers. The SCI is consistent with and complements our five-year Corporate Plan. Our performance against our 2010–11 SCI is summarised below. A full copy of the SCI will be tabled in the Legislative Assembly in accordance with Section 121 of the Government Owned Corporations Act 1993.

StRAtegIc oBjectIve: RIgHt people – SkIlled people, StRong leAdeRSHIp

Initiative Actions desired outcomes Results

Drive to Zero Harm by providing a safe workplace through demonstrated leadership, safe practices, safe behaviours and improvements to the work environment.

Implement initiatives that continue to improve our safety performance and eliminate hazards for the benefit of our employees and contractors.

Equal to or greater than 15% improvement on the All Injury Frequency Rate (AIFR) for 2009–10.

Achieved

A 19.9% reduction in our AIFR was achieved (Health and safety page 19).

Occupational Health and Safety Management System Audits – zero major non-compliances.

Achieved

(Health and safety page 19).

Ensure our skills meet our business needs.

Implement actions arising from the skills capability review undertaken to assess current organisational capability in relation to the delivery of Stanwell’s strategic objectives.

Identified action plans implemented.

Achieved

(Employee relations page 21).

Optimise Stanwell’s recruitment and retention strategies to ensure competitiveness.

Review Stanwell’s key employee processes to ensure alignment with our future needs.

Staff turnover rate to be comparable to industry rates.

Achieved

A 9.29% turnover rate was achieved.

StRAtegIc oBjectIve: RIgHt mARketS – pRoFItABle mARket gRoWtH

Initiative Actions desired outcomes Results

Engage our customers to develop positive, long-term, commercial relationships.

Pursue revenue opportunities with both existing and new customers with the aim to improve gross margin.

One or more significant large structured value adding transaction completed.

Achieved

(Market trading page 31).

Updating our trading systems to flexibly manage our future trading needs.

Achieved

A new Deal Capture and Settlement system was implemented to better manage and measure our financial risk.

Develop and implement emissions trading processes and systems.1

Implement systems and processes that will allow Stanwell to comply with the Carbon Pollution Reduction Scheme (CPRS) and associated emissions trading scheme.

Systems and processes implemented to ensure compliance to legislation prior to commencement.

on track

Awaiting carbon tax legislation.

Monitor and review alternative carbon reduction schemes or variations to CPRS that may emerge.

Plans adjusted to accommodate any change of timing or approach.

on track

Awaiting carbon tax legislation.

1 The need for emissions trading processes and systems is dependent upon the finalisation of legislation.

8 STanwell annual RepoRT 2011

StRAtegIc oBjectIve: RIgHt mARketS – pRoFItABle mARket gRoWtH (ConTInued)

Initiative Actions desired outcomes Results

Match plant performance to portfolio and market needs.

Operate our existing portfolio plant to a regime that best meets the needs of the market.

Portfolio average availability >91%.

Further action required

Conscious commercial decisions based on market price expectations impacted availability, which was 87.62%.

Portfolio average forced outage factor ≤2.6%.

Achieved

Portfolio average forced outage factor was 1.9%.

Stanwell Power Station summer availability >96%.

Further action required

Conscious commercial decisions based on market price expectations impacted summer availability, which was 90.46%.

Stanwell Power Station 2015 and beyond project to review asset life plans and refurbishment requirements substantially progressed.

Achieved

Manage costs to improve profitability.

Reduce controllable costs across the organisation to improve the return to shareholders.

Provide an efficiency dividend to shareholders each year in the form of cost savings of $5 million for the years 2010–11 to 2013–14.

Further action required

The Stanwell directors have recommended that no dividend be provided in 2010–11.

StRAtegIc oBjectIve: RIgHt FuelS – dIveRSIFY ouR Fuel mIx

Initiative Actions desired outcomes Results

Create options to reduce Stanwell’s carbon footprint and carbon dioxide (CO2) intensity with a mixture of coal, gas and renewable energy resources.

Identify and secure access to potential energy resources.

Additional gas resource opportunities identified and progressed after the current gas positions are resolved.

Achieved

Commenced exploration activities with Icon and completed Tri-Star gas transaction (Project development page 33).

Solar data monitoring program under way at a number of locations.

Achieved

Under way at two locations.

Ensure long-term certainty of supply and fuel cost for Stanwell Power Station.

Review Stanwell Power Station’s key fuel arrangements to achieve a better match between supply chain flexibility and forecast market conditions.

Stanwell Power Station rail agreement revised to provide long-term flexibility by June 2011.

Achieved

Stanwell finalised a new Rail Transport Agreement with QR National Coal on 22 June 2011 (Project development page 33).

Complete sale of Mineral Development License 162.

Achieved

Completed the sale of MDL 162 in September 2010, delivering a substantial profit (Project development page 33).

STanwell annual RepoRT 2011 9

StRAtegIc oBjectIve: RIgHt plAnt – loWeR ouR cARBon IntenSItY

Initiative Actions desired outcomes Results

Develop a pipeline of new projects with varying life spans that will deliver a sustainable long-term portfolio of lower CO2 intensive plant and secure cost effective electricity supply.

Investigate a range of project opportunities that will lead to future low emission plant.

Gas plant prefeasibility study complete.

Achieved

Prefeasibility study into the development of a 300 MW gas peaking plant completed (Project development page 33).

Gas plant feasibility study initiated.

Further action required

Deferred, pending the restructure implementation (Project development page 33).

One South East Queensland gas generating site permitting in progress.

Achieved

Site secured and environmental studies have commenced (Project development page 33).

Burdekin Hydro feasibility study complete.

Further action required

The Burdekin Hydro feasibility study is expected to be completed by the end of the 2011 calendar year (Project development page 33).

Electric Power Research Institute carbon capture technology trials completed.

on track

Of the two sponsored sites, one has completed and the other has commenced operations.

Accelerated the pre-feasibility study to complete the Wandoan Power Project.

Achieved

Study completed in February 2011 (Project development page 33).

Solar thermal concept study initiated.

on track

Study to be completed by September 2011.

Business positioned to learn and participate in a large-scale solar initiative.

Further action required

Deferred, pending the restructure implementation.

Improve performance of Stanwell’s existing plant.

Continue to develop and implement performance improvements that have a positive impact on portfolio emission intensity.

Stanwell Power Station Unit 4 low pressure turbine upgrade and generator rewind completed by December 2010.

Achieved

Completed in November 2010 (Operations page 27).

StRAtegIc oBjectIve: RIgHt oRgAnISAtIon – ImpRove oRgAnISAtIonAl cApABIlItY And ReSponSIveneSS

Initiative Actions desired outcomes Results

Create an agile and responsive organisation.

Ensure we have the right systems and processes to deliver our strategic plan.

Plant Information Management System (PIMS) commitment decision reached.

Achieved

PIMS implementation largely completed.

Engage stakeholders to ensure a clear understanding of Stanwell’s business.

Improve and maintain key stakeholder perceptions in areas where Stanwell has, or intends to have, operations.

Key stakeholders have a clear understanding of Stanwell’s business.

Achieved

10 STanwell annual RepoRT 2011

StRAtegIc oBjectIve: RIgHt locAtIonS – QueenSlAnd BASed, RegIonAllY FocuSed

Initiative Actions desired outcomes Results

Maintain our Right to Operate. Manage our impact on the environment to meet legislative and permit conditions.

Stanwell Power Station Unit 4 low NOx burners complete by December 2010.

Achieved

Completed in November 2010 (Operations page 27).

Zero Level 4 and 5 environmental incidents.

Achieved

(Environmental performance page 35).

No material external environmental audit non-conformances.

Achieved

(Environmental performance page 35).

YeAR AHeAd 2011–12

as a result of the restructure of the Queensland Government owned generation sector, announced on 25 november 2010 and with effect from 1 July 2011, Stanwell’s plans for the year ahead are subject to consideration by the restructured company’s Board and executive leadership Team.

Barron Gorge Hydro Administration and Visitors Centre in Far North Queensland

STanwell annual RepoRT 2011 11

The financial year ended 30 June 2011 marks the end of the initial phase of Stanwell since its formation in July 1997. From 1 July 2011, Stanwell is operating under a new structure in line with the Shareholder Review of Queensland Government Owned Corporation Generators (Genco Review), issued in november 2010.

Stanwell has incurred a net loss after tax of $12.0 million for the 2010–11 year. This loss would have been significantly higher without the contribution of:

• profit on the sale of assets surplus to ongoing requirements

• continuing revenue from our coal rebate arrangements.

Further information on the company’s performance is contained in the Directors’ Report.

The 2010–11 year has been a year of change and challenge particularly in the following areas:

SAFetY

Action to improve the safety of our employees and their workplaces has continued with the Safety Improvement Project and Zero Harm initiatives. The results have been encouraging to date and safety continues to remain our number one priority.

nAtuRAl dISASteRS

Our operations and staff experienced the impact of the floods in Brisbane and Central Queensland, and Cyclone Yasi in Far North Queensland during the year. These have been very difficult times for many, and Stanwell has been working to assist people and communities in the recovery effort. Our Business Continuity Plans were successfully enacted on each occasion and, while continued wet weather has delayed the rebuild of coal stockpile levels at both the Gladstone and Stanwell power stations, we have adjusted our generation to take this into account. The resilience of our people and the affected communities has been the outstanding trait exhibited during these times.

ReStRuctuRe

The Genco Review had been foreshadowed for some time and once announced, Stanwell’s directors, Acting Chief Executive Officer (CEO) and Executive Management Team focused on its successful implementation. This was a challenging time for Stanwell and its employees. It is a tribute to the calibre of our staff that ‘business as usual’ was able to continue while, at the same time, planning and involvement in the implementation teams for the restructure was taking place.

Wayne Collins, as Acting CEO, and his Executive Management Team have impressively steered the company and its activities during the year and I thank them most sincerely for their dedication and leadership. I also give my special thanks to my fellow directors Denis Byrne (former Chairman), Tony Andersen, Graeme Crow SC, Laurie Gillespie and Mark Williamson for their commitment and support.

On behalf of the Board, I thank our two shareholding Ministers for their support during the year: Minister for Finance, Natural Resources and The Arts, The Honourable Rachel Nolan MP, and Minister for Energy and Water Utilities, The Honourable Stephen Robertson MP.

I welcome the incoming Chairman and directors, and the new Chief Executive Officer and Executive Leadership Team appointed to the new Stanwell that is effective from 1 July 2011. It is a challenging environment in which we operate and I am sure that the new business will be invigorated by the changes and the challenges ahead.

julie leaver Chairman (17 March 2011 to 30 June 2011)

cHAIRmAn’S StAtement (StAnWell cHAIRmAn AS At 30 june 2011)

12 STanwell annual RepoRT 2011

meSSAge FRom IncomIng cHAIRmAn

as the incoming Chairman of the new Stanwell Board, I would like to pass on my thanks to former Stanwell directors for their stewardship during the past 14 years.

In particular, I would like to thank former chairmen Denis Byrne and Julie Leaver for their leadership in recent years. The 2010–11 financial year presented a unique set of challenges as Stanwell prepared for the restructure following the Genco Review.

The Stanwell Board’s commitment and support during this time ensured that Stanwell’s people, systems and assets were well-positioned for a smooth and effective restructure.

My immediate focus, and that of my fellow directors, will be to define the corporate values and strategy for the new organisation, while ensuring that we maintain our focus on safety, performance and profitability.

The new business brings with it new challenges and new opportunities, which I am sure we will greet with the enthusiasm, professionalism and dedication that has ensured Stanwell’s success in the past.

graham carpenter Incoming Chairman

Stanwell Power Station in Central Queensland

STanwell annual RepoRT 2011 13

This year, we delivered significant financial and operational achievements, while maintaining our focus on safety. This was done despite the challenges we faced when natural disasters affected our corporate office in Brisbane and three of our main operational sites.

Adding to the challenges we faced this year was the announcement of the outcome of the review into the Queensland Government owned generating sector (Genco Review) and the transition period that followed.

Prior to the announcement of the carbon tax, the business was on track to deliver a record profit. Asset impairment and onerous contract provisions associated with the announcements will turn this into a loss of $12.0 million.

In addition to carrying out major planned maintenance activities and completing substantial plant upgrades, we have also made significant progress towards our Zero Harm goal. Almost 20% fewer people were hurt in this past year and this has provided great encouragement to continue the investment in our leadership group, our workforce, our plant and our systems, in pursuit of this goal.

ReSpondIng to cHAnge

In November 2010, following the announcement of the Genco Review, we began preparing our business for the transition. General managers Brad Neven and Michael O’Rourke took on important leadership roles for the transition and employees from all levels across the business were seconded to the two implementation teams at various times. As a consequence of their work, the foundations for a smooth and effective transition to the new business were laid.

As a result of the movement of people into the transition teams, many of our remaining staff willingly took on additional responsibility to ensure the existing business continued to perform. My thanks go to all who kept the business on track during this period. I particularly wish to thank Ian Gilbar, Jason Mahoney, Michelle Forrest, Trevor Hooper and Chris Walker, who very capably stepped in to the executive team for varying periods, for their sound leadership under difficult conditions.

opeRAtIng In A cHAllengIng envIRonment

Flooding in Central Queensland during December 2010 and January 2011 affected employee access and coal supplies to Stanwell and Gladstone power stations. It also affected access to our Rockhampton office for some employees. Prudent risk management and business continuity planning meant that we had enough coal in our stockpile at Stanwell Power Station to allow the station to continue to generate. Essential employees were flown in via helicopter to Stanwell Power Station while others used technology to continue to work remotely.

The rain continued south and, on 11 January 2011, our Brisbane corporate office was evacuated in preparation for flooding in Brisbane. We were unable to return to the office for a fortnight. Again, our business continuity planning and the distribution of our key systems allowed us to continue trading remotely for the 14 days that the office was out of commission. Mercifully, only a small number of our staff suffered property damage from the flooding.

Less than one month later, Barron Gorge and Kareeya hydro power stations were evacuated in preparation for Cyclone Yasi, which crossed the North Queensland coast on the night of Wednesday 2 February 2011. Almost all employees at Kareeya Hydro suffered some form of damage to their personal properties. Both hydros suffered minor damage and returned to service within a few days of the cyclone passing.

conSolIdAtIng ouR BuSIneSS

The effects of flooding on coal supplies and coal rebates, combined with a very soft electricity market, resulted in total revenue of $562.6 million for the 2010–11 year, which is $100 million less than the previous year.

The outstanding result achieved with the sale of Mineral Development Licence 162 saw the culmination of a long-term strategy to most profitably utilise and monetise our coal reserves.

Further, in June 2011, we completed the sale of two wind assets— the Emu Downs Wind Farm and the Badgingarra Wind Development Project, both in Western Australia. This sale will allow the business to focus on optimisation of our Queensland based portfolio of fuel and generation assets.

ActIng cHIeF executIve oFFIceR’S RevIeW

14 STanwell annual RepoRT 2011

A new Rail Transport Agreement with QR National Coal was signed, providing long-term certainty for the delivery of coal from Central Queensland to Stanwell Power Station. It also has the potential to facilitate coal deliveries to the Port of Gladstone.

upgRAdIng ouR ASSetS

The major overhaul of Stanwell Power Station’s Unit 4 included a low pressure turbine upgrade and generator rewind, delivering a 2.38% improvement in efficiency. As part of the outage, we also installed low NOx burners, which will reduce NOx emissions by about 40% when all units are modified.

At Barron Gorge, Unit 1 returned to service in August 2010 following a generator stator rebuild and rewind, and refurbishment of other key components. The same project commenced on Unit 2 in April 2011.

commIttIng to ZeRo HARm

We continued to make positive progress towards our target of Zero Harm to all employees and contractors. We have hurt less people this year, compared with the same time last year.

There were two Lost Time Injuries in 2010–11, which is significantly less than the nine recorded in 2009–10. The All Injury Frequency Rate reduced by 19.9%. However, even with the reduced number of injuries, there is still more to be done and we will continue to focus on keeping our people safer.

InveStIng In ouR communItIeS

In response to the December–January floods and Cyclone Yasi, Stanwell contributed more than $190,000 to recovery initiatives. A substantial portion of this support was directed to heavily impacted community organisations, schools and sporting clubs in the vicinity of our affected operations. Stanwell employees and contractors donated almost $20,000 to the Premier’s Disaster Relief Appeal and Rockhampton Wildlife Rescue. Stanwell matched these donations dollar-for-dollar.

RecognISIng ouR people

I would like to pay tribute to our Board, Executive Management Team and staff for their dedication and professionalism. I would particularly like to acknowledge the contribution of Denis Byrne and Julie Leaver, the two chairs of Stanwell during this past year. I have greatly appreciated their sage counsel and their unwavering support for staff throughout this period of uncertainty.

I must also recognise the efforts of our shareholders’ representatives: the Office of Government Owned Corporations and the Department of Employment, Economic Development and Innovation – Mines and Energy.

The past 18 months as Acting Chief Executive Officer have been extremely rewarding and I have been proud to see everyone step up and meet the challenges that we have encountered, while remaining positive and focused on the job at hand. Our achievements, as always, are a direct reflection of the high quality of the people we have working in the business.

Wayne collins Acting Chief Executive Officer

STanwell annual RepoRT 2011 15

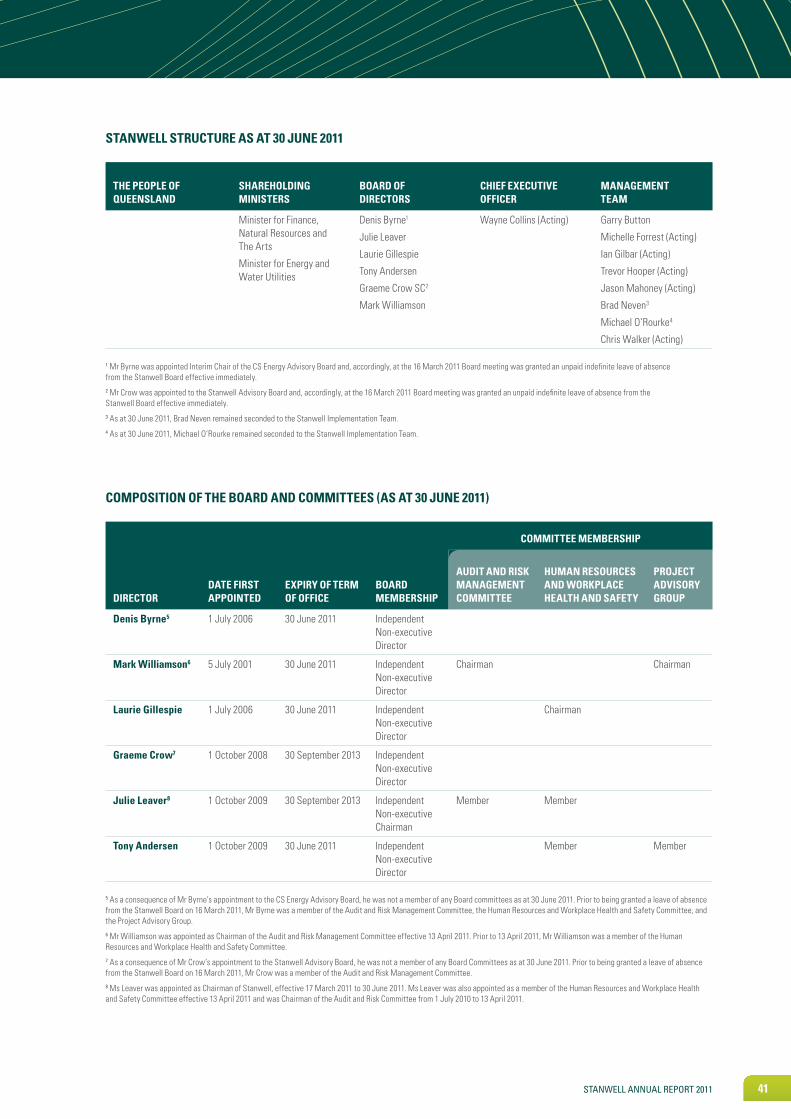

BoARd oF dIRectoRS (AS At 30 june 2011)

denIS BYRnechairman*(July 2006–March 2011)

Independent non-executive directorTerm of appointment: July 2006–June 2011

tonY AndeRSenIndependent non-executive directorTerm of appointment: October 2009–June 2011

julIe leAveRchairman (March 2011–June 2011)

chairman Audit and Risk management committee (October 2009–April 2011)

Independent non-executive directorTerm of appointment: October 2009–present

gRAeme cRoW ScIndependent non-executive directorTerm of appointment: October 2008–present

lAuRIe gIlleSpIechairman Human Resources and Workplace Health and Safety committee(August 2007–June 2011)

Independent non-executive directorTerm of appointment: July 2006–June 2011

mARk WIllIAmSonchairman Audit and Risk management committee(April 2011–June 2011)

chairman of the project Advisory group(October 2009–June 2011)

Independent non-executive directorTerm of appointment: July 2001–June 2011

For full biographies, please refer to page 51 of the Directors’ Report.

*Mr Byrne was appointed Interim Chairman of the CS Energy Advisory Board and, accordingly, at the 16 March 2011 Board meeting was granted an unpaid indefinite leave of absence from the Stanwell Board.

16 STanwell annual RepoRT 2011

WAYne collInSBEng (Electrical), BBus, CPEng, GAICD

Acting chief executive officer(January 2010–June 2011)

gARRY ButtonBCom (UNSW), FCPA, FFTP, MAICD

Acting general manager corporate Services (April 2011–June 2011)

Acting general manager trading (April 2011–May 2011)

chief Financial officer(February 2008–April 2011)

mIcHelle FoRReStBCom, Adv Dip Fin Services (Financial Markets), AFMA Accredited

Acting general manager trading (May 2011–June 2011)

Wayne has worked in the electricity industry for almost 30 years, in a variety of engineering, managerial and business development roles, principally associated with power generation.

In January 2010, Wayne was appointed Acting Chief Executive Officer of Stanwell.

He has been a senior executive with Stanwell for 13 years, with previous management roles in business services, asset management and technical services, and business development.

As Acting General Manager Corporate Services, Garry is responsible for the internal departments of secretariat, legal, internal audit, insurance and quality.

Prior to this, Garry held the position of Stanwell Chief Financial Officer (from February 2008–April 2011). He has also held several senior financial and corporate roles within Queensland Rail, Fairfax and Unilever Australia.

Garry resigned as a non-executive director of Blue Energy Limited on 30 June 2011.

As Acting General Manager Trading, Michelle is responsible for managing the operations of the Trading division to maximise profitability through an integrated trading strategy within the risk management framework.

This includes the contract trading, spot trading, regulatory, strategy and analytical functions.

Prior to acting in the General Manager Trading role, Michelle held the positions of Trading Manager and Spot Trading Manager within Stanwell.

executIve mAnAgement teAm (AS At 30 june 2011)

STanwell annual RepoRT 2011 17

IAn gIlBARBEng (Electrical)

Acting chief operating officer(April 2010–June 2011)

tRevoR HoopeRAD Elect Eng, MBA

Acting general manager Business Services (January 2011–June 2011)

jASon mAHoneYBCompt (UNISA), Chartered Accountant

Acting chief Financial officer (April 2011–June 2011)

As Acting Chief Operating Officer, Ian is responsible for managing the organisation’s plant operations.

Ian has worked for Stanwell for 14 years and has almost 30 years’ experience in the electricity industry in various engineering and technical management roles.

During the past three years at Stanwell, Ian has been heavily involved in the renegotiation of the Gladstone Interconnection and Power Pooling Agreement.

As Acting General Manager Business Services, Trevor is responsible for managing health and safety, environment, information and communication technology, risk, facilities, quality, information resources and human resources.

Trevor has broad and extensive experience in the electricity industry in Queensland. He has performed various managerial roles across production, maintenance, commercial and more recently in the services areas. Trevor has been heavily involved in the implementation of the safety improvement initiatives across all Stanwell sites in recent times.

Jason is responsible for Stanwell’s finance, business improvement, energy and financial risk management, and procurement functions. Prior to being appointed the Acting Chief Financial Officer, Jason held the position of Financial Controller.

Jason has held a General Manager Finance role in an ASX 200 company and was a senior manager at Ernst & Young.

18 STanwell annual RepoRT 2011

BRAd nevenMBA (HRM), ComDec, MAHRI, MIRSQ

Seconded to the Implementation team for the restructured Stanwell(January 2011–June 2011)

general manager Business Services(May 2008–January 2011)

mIcHAel o’RouRkeBLaw, BCom, GDip Applied Finance and Management, GDip Company Secretarial Practice

Seconded to the Implementation team for the restructured Stanwell (April 2011–June 2011)

general manager corporate Services (September 2007–April 2011)

Acting general manager trading(March 2010–April 2011)

cHRIS WAlkeRBA, MBA (UQ)

Acting general manager Business development(April 2011–June 2011)

Brad Neven has worked for Stanwell for more than 10 years in a variety of human resource and managerial roles, including Employee Relations Manager.

In 2008, Brad was appointed the General Manager Business Services, responsible for managing health and safety, environment, information and communication technology, risk, land and property, and human resource management.

From January to June 2011, Brad was seconded to the Stanwell Implementation Team to assist with the smooth and effective transition to the new business.

Michael joined Stanwell in 1998 as Legal Counsel and was responsible for the strategic direction and operational performance of Stanwell’s legal team. In 2002, Michael was appointed Stanwell’s Company Secretary/Legal Counsel. As Company Secretary, Michael reported to the Stanwell Board on all secretariat related matters.

In 2008 Michael was appointed General Manager Corporate Services, responsible for the internal departments of secretariat, legal, internal audit, corporate communications, stakeholder relations, insurance and quality.

In March 2010, Michael was appointed Acting General Manager Trading and was responsible for the physical and financial trading of electricity and market forecasting.

From April to June 2011, Michael was seconded to the Stanwell Implementation Team to assist with the smooth and effective transition to the new business.

Chris Walker has more than 30 years of experience in the electricity industry in a variety of roles, including finance, power station operations and procurement.

For the past 13 years, Chris has worked for Stanwell in business development.

He is responsible for facilitating the development of corporate strategy, the operational and strategic fuel and water needs of existing assets, and investigating and securing investment opportunities in gas, clean coal, and renewable energy. He is also responsible for Corporate Communications.

STanwell annual RepoRT 2011 19

HeAltH And SAFetY

WHAt We Set out to AcHIeve tHIS YeAR HoW We peRFoRmed

Maintain the Zero Incident Process (ZIP). Achieved

The Health and Safety teams/site representatives have been trained as ZIP coaches, ensuring that the processes are maintained.

Maintain the Fitness for Duty (FFD) program. Achieved

Fatigue monitoring and alcohol and other drugs testing of employees and contractors continued.

Undertake compliance/improvement audits against health and safety corporate standards.

Achieved

Audits performed and non-compliances dealt with according to policy requirements.

Continue implementation of the Safety Performance Action Plan (Safety Improvement Project).

Achieved

The Safety Improvement Project is progressing according to project plan. Employees have received Zero Harm training and have been provided with tools to assist with personal risk assessment and performance of safety observations.

Retain AS/NZS 4801:2001 certification. Achieved

Undertake ongoing work environment improvements.

Achieved

Site safety committees continued to identify and implement safety improvement initiatives across all sites, with more than 20 site driven improvements noted by the Board.

Target Zero Harm. on track

All Stanwell performance indicators show a steady trend towards Zero Harm. However, there is still more to be done.

Continue to lower our All Injury Frequency Rate (AIFR).

on track

A 19.9% reduction was recorded this year.

SAFe people

Stanwell’s safety vision, “we will manage health and safety risks with a goal that no one gets hurt”, is being embedded in Stanwell’s safety culture through the Safety Improvement Project (SIP).

SAFe pRActIceS

Stanwell’s safe work systems (including Authority to Work) have been fully implemented, with a major upgrade of the computer software supporting this system successfully completed during the year.

Supporting these systems of work are new behavioural-based safety tools: Safety Observation Guides and TAKE 1 (a personal risk management process).

Underpinning these practices is an established network of health and safety meetings, including the Central Safety Committee and onsite safety meetings, which encourage teams to identify health and safety improvement initiatives.

SAFe WoRk envIRonment

During the year, Stanwell continued to identify and implement safety initiatives to improve the standard of safety in our working environments.

At Stanwell Power Station, traffic management improvements in the main workshop, new protocols for security gates and line marking for pedestrian access separated vehicle and pedestrian traffic across the site.

We developed a hydraulic system at Barron Gorge Hydro to eliminate the difficulties of working in a confined space and the risk of entrapment when replacing turbine runners.

We also endeavoured to assist our staff to be safe outside of work, by issuing high visibility vests, personal safety glasses and first aid kits to corporate staff.

SocIAl peRFoRmAnce

SAFetY ReSultS

Stanwell’s safety performance continues to show an improvement in line with our target of Zero Harm to all employees and contractors.

During the year, there were two Lost Time Injuries, which is significantly less than the nine recorded in 2009–10.

Stanwell recorded a Lost Time Injury Frequency Rate (LTIFR) of 1.43 for employees and 2.12 for contractors, resulting in a combined LTIFR of 1.71 (compared with 7.80 in 2009–10).

Most pleasing was the 19.9% reduction in the All Injury Frequency Rate.

20 STanwell annual RepoRT 2011

cASe StudYAudItIng And ImpRovIng ouR SYStemS

Stanwell’s Occupational Health and Safety Management System has retained certification to AS/NZS 4801:2001.

Selected occupational health and safety corporate standards were audited by an external auditor for compliance and to identify improvements. No major non-conformances were reported.

SAFe SpIne pRogRAm

In response to a number of strain injuries reported in office-based work environments, a safe spine program was implemented to prevent/reduce musculoskeletal strain injuries.

The safe spine program provided staff with tools and assistance to prevent back injuries, focusing on posture, workstation set-up, exercise and stress management. The program sought to protect people’s backs in their everyday working environments, as well as at home, on a plane and in the garden.

The safe spine program was delivered to the corporate offices during April and May 2011 with great success.

On a daily basis, corporate office workers complete a series of short exercises and stretches in their work groups to help mobilise and stretch their bodies, in order to help prevent future harm and increase health and wellbeing. These exercises are led by Stanwell employees who volunteered to attend the Safe Spine Leader training session.

“Leading the stretches has proven a great way to refresh not just the body, but the mind to ensure I am focused on the next job.”

– Safe Spine Leader

loSt tIme InjuRY FReQuencY RAte

4.29

5.79

3.08 3.57

1.52

9.73 10

.32

1.43

7.80

1.71

2006

–07

Employees Employees and contractors

2007

–08

2008

–09

2009

–10

2010

–11

This year we had a decrease in Lost Time Injuries, particularly during the Stanwell Power Station outage.

All InjuRY FReQuencY RAte

58.9

6

147.

67

120.

41*

173.

43

65.3

5 96.4

5

Employees Employees and contractors

2009

–10

2008

–09

2010

–11

A reduction in the AIFR can be attributed to fewer injuries throughout the year.* This figure has been changed following the submission of data for reporting. The figure provided in the 2009–10 Annual Report was 108.28.

loSt tIme InjuRY duRAtIon RAte

18.0

011

.60

3.00 3.50

16.0

03.

91

6.71

1.00

7.78

2.00

2006

–07

Employees Employees and contractors

2007

–08

2008

–09

2009

–10

2010

–11

The decrease in the LTIDR can be attributed to a decrease in the days lost per injury.

loSt tIme InjuRY SeveRItY RAte

Employees Employees and contractors

69.2

860

.64

1.43 3.41

2009

–10

24.3

6 40.7

020

08–0

9

2010

–11

A significant decrease in the LTISR was recorded due to fewer days lost for the two lost time injuries.

STanwell annual RepoRT 2011 21

emploYee RelAtIonS

WHAt We Set out to AcHIeve tHIS YeAR HoW We peRFoRmed

Finalise new workplace agreements for Stanwell Power Station, Barron Gorge Hydro and Kareeya Hydro.

on track

Negotiations with the unions regarding the new workplace agreements are continuing, with completion expected in the second half of 2011.

Implement e-Recruitment – a technology to improve efficiency in the recruitment process.

Further action required

Project placed on hold due to the Genco Review.

Implement a new performance management system.

Further action required

Project placed on hold due to the Genco Review.

Stanwell’s employee relations strategy recognises the importance of providing individual development opportunities to foster the potential of our people.

Stanwell’s strategies are also cognisant of our broader corporate obligations to ensure that a skilled and trained workforce exists to assure management, technical and operational resources in our industry, into the future.

Our current workforce includes 371 employees and approximately 250 Full Time Equivalent contractors.

BuIldIng A StRong RegIonAl WoRkFoRce

As many of our employees are located in regional areas, Stanwell has continued to focus its workforce development initiatives in these locations.

In 2010–11, Stanwell continued to review the location of Brisbane-based professional and administrative roles as vacancies occurred. Where sensible, these have been filled in Rockhampton.

AddReSSIng tHe SkIllS gAp

Stanwell supports an integrated approach to employee development, recognising that it is an essential part of planning, management and day-to-day operations. Stanwell’s capability review, completed in

2010, provided the basis for ensuring that gaps in identified key capabilities were addressed via a combination of targeted recruitment and individual development (via training plans).

To remain competitive, and to attract and retain skilled employees, Stanwell has in place a range of initiatives, including:

• training and development programs, including the Leadership Development Program, graduate programs, study support, and apprentice and trainee programs

• improvements to recruitment processes, including improved branding and a review of Stanwell’s Recruitment Guidelines

• the Power Generation Skills Development Program which, in conjunction with three Queensland universities, offers professional engineers and paraprofessionals the opportunity to accelerate their technical competency. There are currently 13 employees participating in this program

• hosting engineering students and lecturers from CQUniversity at Stanwell Power Station to demonstrate engineering career opportunities

• participating in career fairs and expos across Queensland

• providing part-time study support to 43 employees across the company.

SuppoRtIng gRAduAteS, AppRentIceS And tRAIneeS

Stanwell’s Apprentice and Trainee Program offers one-year Business Administration trainee positions, two-year Warehousing trainee positions, and four-year trade and five-year dual-trade apprentice placements. As of 30 June 2011, there were 16 apprentices and five trainees placed throughout Stanwell.

In February 2011, Stanwell welcomed two new apprentices in the electrical, and fitting and turning fields. This year, the apprentices undertook a portion of their training at Gladstone Area Group Apprenticeships Ltd’s state-of-the-art training centre in Gladstone.

Stanwell’s Graduate Development Program is a two-year or three-year structured program that includes extensive on-the-job training and development. At 30 June 2011, there were seven graduates enrolled in the program across disciplines such as electrical and mechanical engineering, industrial chemistry and land management.

InveStIng In ouR FutuRe leAdeRS

In 2011, seven employees completed Stanwell’s Leadership Development Program. The program is designed to harness the leadership and management capabilities of participants through initiatives such as:

• professionally accredited business courses

• coaching and mentoring programs

• leadership benchmark assessments, prior to and at the end of the program, to gauge leadership skill improvement

• involvement in special company projects and/or geographical and functional rotation within Stanwell

• exposure to guest speakers and networking opportunities

• technical skills training.

Many past participants have now moved onto more senior roles and special projects within the company, and provide ongoing support and encouragement to new program participants.

22 STanwell annual RepoRT 2011

WoRkFoRce numBeRS*

2006–07 2007–08 2008–09 2009–10 2010–11

360 368 395 383 371

Workforce numbers have reduced during the past three years. Last year’s reductions can be attributed to a freeze on recruitment of non-critical roles due to the Genco Review.*Workforce numbers do not include positions within the organisation that were vacant at the time of reporting and which are intended to be filled in the future.

SecuRIng condItIonS oF emploYment

There are four certified agreements that contain the conditions of employment for our employees: Stanwell Power Station, Barron Gorge Hydro, Kareeya Hydro and Stanwell Corporate Offices.

The renegotiation of the Stanwell Power Station, Barron Gorge Hydro and Kareeya Hydro certified agreements commenced in the second half of the 2010–11 financial year. Stanwell is working towards renegotiating these agreements by 30 September 2011.

HelpIng ouR people StAY HeAltHY And Well

Stanwell has a health and wellbeing initiative called Stanwellbeing. This initiative focuses on proactively improving the health, wellness and fitness of all employees. It includes health assessments and cancer screenings; a free, confidential and voluntary counselling service; flu vaccinations; first aid training; access to a child care referral service; ergonomic assessments; and a range of educational newsletters and fact sheets addressing key health and wellbeing topics.

In 2010–11:

• 77 employees took up Stanwell’s offer of a flu vaccination

• 135 employees received a health assessment

• Stanwell nominated first aiders received annual training

• 14 employees volunteered to undertake cancer screenings

• 141 corporate staff participated in safe spine training

• 200 Stanwell employees and contractors participated in the Global Corporate Challenge (a pedometer-based challenge to ‘virtually’ walk around the world)

• 100 people received an ergonomic assessment

• three employees utilised Stanwell’s childcare referral service.

SuppoRtIng eQuAl emploYment oppoRtunItY And dIveRSItY

Stanwell provides all employees with easy access to Equity Referral Officers (EROs) who are specially trained to engage with employees who require information or support relating to discrimination or harassment issues. These officers are situated at each site.

Stanwell regularly monitors Equal Employment Opportunity (EEO) statistics and focuses on both its EEO provisions and promotion of EEO within the workplace. Stanwell provides the Public Service Commissioner with an annual report on the outcomes of any actions, as required under section 30 of the Public Service Act 2008.

Initiatives to further improve the diversity of the corporation’s workforce are currently being developed.

EEO discrimination and harassment training is provided as part of our induction process for all new employees, with all employees undergoing EEO refresher training every two years.

cASe StudY

WoRkplAce mentoRIng FoR Women

Stanwell introduced a workplace mentoring program to develop our future female leaders and to assist us to achieve genuine diversity within the organisation.

The program provides participants with the tools, skills and awareness to enhance business productivity and align with Stanwell’s ongoing commitment to best practice. The program runs for 12 weeks, with 12 modules to be completed during that time.

The modules provide information on, and practical strategies for, planning and managing a career; understanding gender differences in leadership styles; personal branding and adding value; and negotiation and communication skills required for leadership.

STanwell annual RepoRT 2011 23

eeo numBeRS

eeo*

numBeR oF emploYeeS AS At 30 june 2011 poSItIon cAtegoRY

Female 97 Managerial, professional and clerical

Male 274 Managerial, professional, trade or related, clerical

Non-English speaking background

19 Managerial, professional, clerical

Aboriginal and Torres Strait Islander (ATSI)

3 Professional, clerical

People with a disability 17 Managerial, professional, trade or related, clerical

The number of Aboriginal and Torres Strait Islander employees remained consistent with last year. * Employees have the option not to respond to our EEO questionnaire. As at 30 June 2011, 32 employees had not responded. The number of respondents that chose not to respond to each of the EEO categories is:

• Non-English speaking background: 32

• ATSI: 32

• People with a disability: 32

cAReeR development pRogRAmS

poSItIonS numBeR oF poSItIonS AS At 30 june 2011

Trainees 7

Apprentices 16

Graduate development 6

Paraprofessional 0

Co-op engineers 2

Total 31

Approximately 9% of the workforce is involved in a formal career development program.

emploYee tuRnoveR

2006

–07

70

60

50

40

30

20

10

0

Number of departures

Annual turnover rate

2007

–08

2008

–09

2009

–10

2010

–11

There has been a significant reduction in the turnover rate during the past five years. However, there was a slight increase from last year to this year.

24 STanwell annual RepoRT 2011

communItY RelAtIonS

WHAt We Set out to AcHIeve tHIS YeAR HoW We peRFoRmed

Apply agreed social investment protocols to ensure support remains regionally focused and relevant to the communities in which we operate, and to achieve mutually beneficial outcomes from sponsor partnerships.

Achieved

Adhered to approved processes and procedures with regard to consideration of sponsorship proposals, support agreed to during the period and ongoing partnerships. Delivered positive outcomes for Stanwell and sponsored organisations.

Explore and continue to develop our stakeholder database system to improve reporting and the management and analysis of interactions with stakeholders.

on track

Used database effectively to record stakeholder interactions and outcomes, and for monitoring and reporting purposes. Continued to develop and make improvements to the system.

ouR SocIAl InveStment StRAtegY

Stanwell’s social investment strategy focuses support on three key areas to effectively address the company’s social interests:

• education – support for youth in areas of educational and self development, with particular focus on regional Queensland, and support for opportunities to improve the outlook for skilled engineering and other professions related to Stanwell’s core business

• environment – support for positive environmental initiatives, particularly those aligning with Stanwell’s business direction and/or those that are of benefit to our regional communities

• Health and Safety – support for initiatives that seek to promote a healthy, active and safe lifestyle and which demonstrate Stanwell’s commitment to a positive work-life balance and to the communities in which we operate.

InveStIng In ouR communItIeS

During 2010–11, we continued to focus our social investment activities in the regions where Stanwell operates, and to provide opportunities for local communities and employees to engage in positive ways through financial and non-financial support for these activities.

We maintained support for our existing major sponsorships, committing to another three years’ support for Beacon Foundation, Life Stream Foundation and the Central Queensland Comets. In addition, Stanwell committed to sponsor Capricorn Netball (to December 2013) and the Central Queensland NRL Bid’s Junior Development Program (to December 2011).

capricorn netball

In January 2011, Stanwell committed major sponsorship for Capricorn Netball’s new ‘Train Well…Play Well…Stanwell’ player and volunteer development strategy for the region’s netballing community. The program will help identify and nurture promising young players, and provide development pathways for talented juniors, and education and training opportunities for the sport’s volunteers.

the Beacon Foundation

As part of our support for Beacon, Stanwell Power Station hosted a ‘Lunch with the Girls’ program for 15 to 16 year-old Mount Morgan State High School girls, providing an opportunity for students to engage with professional women and increase their knowledge of work culture, employer expectations and potential career paths. Stanwell also worked with Beacon to progress development of a similar ‘BBQ with the Boys’ program, expected to be rolled out in 2011–12. In addition, we conducted student and teacher tours at our power stations and offices, provided

guest speakers at Beacon events, and attended No Dole program charter signing ceremonies.

life Stream Rockhampton

Stanwell continued to have a representative on Life Stream’s Board and to provide office space to Life Stream Rockhampton to assist with the expansion of services to people in Central Queensland who have an intellectual disability. During the year, Life Stream delivered weekly sporting programs to local schools and the Endeavour Club, catering for ages ranging from six to 60. Disability workshops and practical community programs were also organised, along with interschool athletics competitions.

central Queensland Rugby league development programs

In January 2011, Stanwell renewed its major sponsorship of the Central Queensland Comets Rugby League Under 16 and Under 18 Development Squads, and committed to sponsor the CQ NRL Bid’s new Junior Development Program for Under 13 players from Central Queensland. Stanwell’s support aims to provide opportunities for local youth to stay and play in the region longer, while offering a path for young players through to higher levels in the game.

otHeR SponSoRed InItIAtIveS• Rotary club of Rockhampton

Stanwell power Station Rocky River Run – Held on 12 June 2011, the annual community fun run has continued to grow, attracting approximately 500 registered entrants this year, including representatives from Stanwell and local Stanwell-sponsored organisations. Proceeds from the event were again directed to local charities working for the prevention of youth suicide.

• Southern cross Soloists SunWater and Stanwell music School – Held in Rockhampton in July 2010 and April 2011, the week-long annual educational event was attended by more than 90 talented young high school music students from around the State.

STanwell annual RepoRT 2011 25

• tennis Queensland Stanwell Far north Queensland Regional development program – This initiative encouraged physical activity by providing opportunities to play tennis at free Stanwell Community Fun Days, held by participating tennis clubs in and around Cairns. It also provided professional development for leading regional junior tennis players. Stanwell also supported the inaugural Cairns Tennis International.

• Yalari – The annual ‘Stanwell Classic’ lawn bowls fundraiser was hosted by Stanwell in Brisbane on 28 October 2010, raising more than $40,000 for youth charity Yalari to provide scholarships to indigenous students.

• cQ Zero Harm conference – Held in Rockhampton in October 2010, this has become an annual event aimed at increasing the profile of workplace health and safety in Central Queensland.

• Queensland natural disaster Recovery initiatives – In response to the December/January floods and Cyclone Yasi, Stanwell contributed more than $190,000 to recovery initiatives, including the Premier’s Disaster Relief Appeal, Rockhampton Wildlife Rescue, local schools and sporting clubs in Rockhampton and Tully, and essentials kits provided by Baked Relief.

emploYee SuppoRt Employee-driven support of charitable programs saw our staff commit their personal time to assist community fundraising initiatives:

• In Rockhampton in May 2011, Stanwell Power Station’s Live Wires team competed in the local annual Cancer Council’s Relay for Life for the eighth consecutive year, raising more than $5,000. Stanwell acknowledged the Live Wires’ support by matching this amount dollar-for-dollar.

• In Brisbane in November 2010, a team of Stanwell employees took part in the annual Cool Night Classic corporate run/walk in the CBD to raise funds for chosen beneficiaries The Pyjama Foundation and Street Swags.

• In Cairns in November 2010, Stanwell employees participated in the Cairns Crocs Triathlon Club time trial event to raise funds for the Movember male health initiatives, specifically prostate cancer and depression in men.

• In early 2011, Stanwell employees and contractors donated almost $20,000 to the Premier’s Disaster Relief Appeal and Rockhampton Wildlife Rescue. Stanwell matched these donations dollar-for-dollar.

engIneeRIng ouR FutuReAs an organisation that relies on the expertise of skilled engineers to conduct our core business, Stanwell recognises the importance of promoting engineering-related careers and fostering the development of the next generation of engineers.

To assist in ensuring the long-term capacity of the energy industry, we have continued our support of several educational initiatives, including:

• Australian Power Institute, which promotes power engineering in universities and assists undergraduate students in areas of engineering relevant to the energy sector

• Queensland Minerals and Energy Academy, a joint venture between the Queensland Resources Council and the Queensland Government, which aims to attract school leavers to careers in the resources sectorTalented young musicians participate in the Southern Cross Soloists SunWater and Stanwell Music

School in Rockhampton

26 STanwell annual RepoRT 2011

cASe StudY

RockHAmpton HoStS ecomAn

In April 2011, Stanwell sponsored the delivery of an Economics and Management (ECOMAN) program for Year 11 and 12 business students from Rockhampton State High School.

The ECOMAN course, which is designed to prepare young people for the business world, was held at Stanwell’s Rockhampton office from 27 to 29 April.

Stanwell supplied in-kind sponsorship by providing conference facilities to Queensland Private Enterprise Centre (QPEC), Griffith Business School, to run the program.

ECOMAN is a computerised business simulation program, used extensively in schools in Europe.

Participating students spend three working days in the premises of a sponsoring business. Under the guidance of experienced facilitators, the students simulate four years in the life of a company, negotiating business opportunities and presenting their outcomes to ‘annual general meetings’.

In addition to providing the venue for the three-day course, Stanwell representatives attended proceedings to act as ‘shareholders’ and ask questions of the student directors about their business reports.

QPEC was responsible for introducing the course to Queensland and has since expanded its delivery to more than 50 schools across the State.

Stanwell has been a sponsor of the ECOMAN Program for several years and has hosted a number of student groups in the Brisbane office. However, this was the first time ECOMAN had been offered in Rockhampton.

My experience of the ECOMAN program was highly enjoyable and worthwhile. The program was a great start to the term and taught me the key concepts of business management and economics, as well as valuable skills of teamwork, leadership and confidence. ECOMAN gave me the opportunity to apply these skills to a simulated manufacturing company, which is an experience that cannot be offered in the classroom. The facilitators of the program were friendly and engaging, and the venue where the program was held added to the realism of my business experience. The knowledge that I gained from ECOMAN will help me with my future endeavours in the business industry, and I cannot recommend highly enough the benefit of this program to students and schools.

– Taralee Cosstick, Student – Rockhampton State High School

• The Engineering Link Group, a not-for-profit organisation established to facilitate the introduction of secondary school students from regional Queensland to the discipline of engineering, through practical projects conducted in Rockhampton during school holidays

• Power Generation Skills Development Program, a collaboration by the three Queensland Government-owned generators and leading Queensland universities to offer innovative professional development for engineers and paraprofessionals.

SuppoRtIng locAl pRocuRement

This year, we remained committed to promoting local economic development and fostering relationships with our suppliers.

During the Stanwell Power Station Unit 4 planned maintenance outage, from September to November 2010, goods and services were purchased locally wherever possible, representing a significant injection into the region’s economy.

During the outage, more than 660 additional personnel were required. Providing local accommodation, transportation, catering and other goods and services for the increased workforce meant considerable additional business for local suppliers.

connectIng WItH ouR communItIeS

We are aware of the impact our activities can have on the communities located near our operational and project sites. As such, we focus considerable resources on developing proactive relationships with local communities.

During 2010–11, Stanwell Power Station hosted regular community meetings for neighbours and other local stakeholders, as well as educational tours for school students and community groups.

Both Kareeya and Barron Gorge hydros supported local commercial rafting activities on the Tully and Barron rivers through scheduled water releases.

Stanwell provided regular updates on the organisation’s regional activities through our Central Queensland, North Queensland and Far North Queensland community newsletters.

We continued to consult with key stakeholders associated with the proposed Burdekin Hydro Project, including the Birri people, the traditional owners of the land

surrounding the Burdekin Falls Dam and proposed transmission line.

Engagement with local indigenous groups in North Queensland was also progressed in relation to cultural heritage protocols for future property works and duty of care obligations for strategic land assets in the region.

STanwell annual RepoRT 2011 27

BuSIneSS peRFoRmAnce

opeRAtIonS

WHAt We Set out to AcHIeve tHIS YeAR HoW We peRFoRmed

Undertake a major overhaul on Stanwell Power Station Unit 4.

Achieved

Stanwell Power Station Unit 4 returned to service on 10 November 2010, following the completion of the major overhaul.

Implement low pressure turbine and generator upgrade on Unit 4.

Achieved