notice of meeting · notice of meeting you are hereby summoned to attend a meeting of the sheffield...

TRANSCRIPT

Sheffield City Region Combined AuthorityRegistered Address: 18 Regent Street, Barnsley, S70 2HG

19 April 2017

To: Members of the Sheffield City Region Combined Authority Audit CommitteeAppropriate Officers

NOTICE OF MEETING

You are hereby summoned to attend a meeting of the Sheffield City Region Combined Authority Audit Committee, to be held at at 11.00 am on Thursday 27 April 2017 for the purpose of transacting the business set out in the agenda.

Diana TerrisClerk to the Combined Authority

WEBCASTING NOTICE

This meeting is being filmed for live or subsequent broadcast via the Combined Authority’s website. At the start of the meeting the Chair will confirm if all or part of the meeting is being filmed.

You should be aware that the Combined Authority is a Data Controller under the Data Protection Act. Data collected during this webcast will be retained in accordance with the Combined Authority’s published policy.

Therefore by entering the meeting room, you are consenting to being filmed and to the possible use of those images and sound recordings for webcasting and/or training purposes.

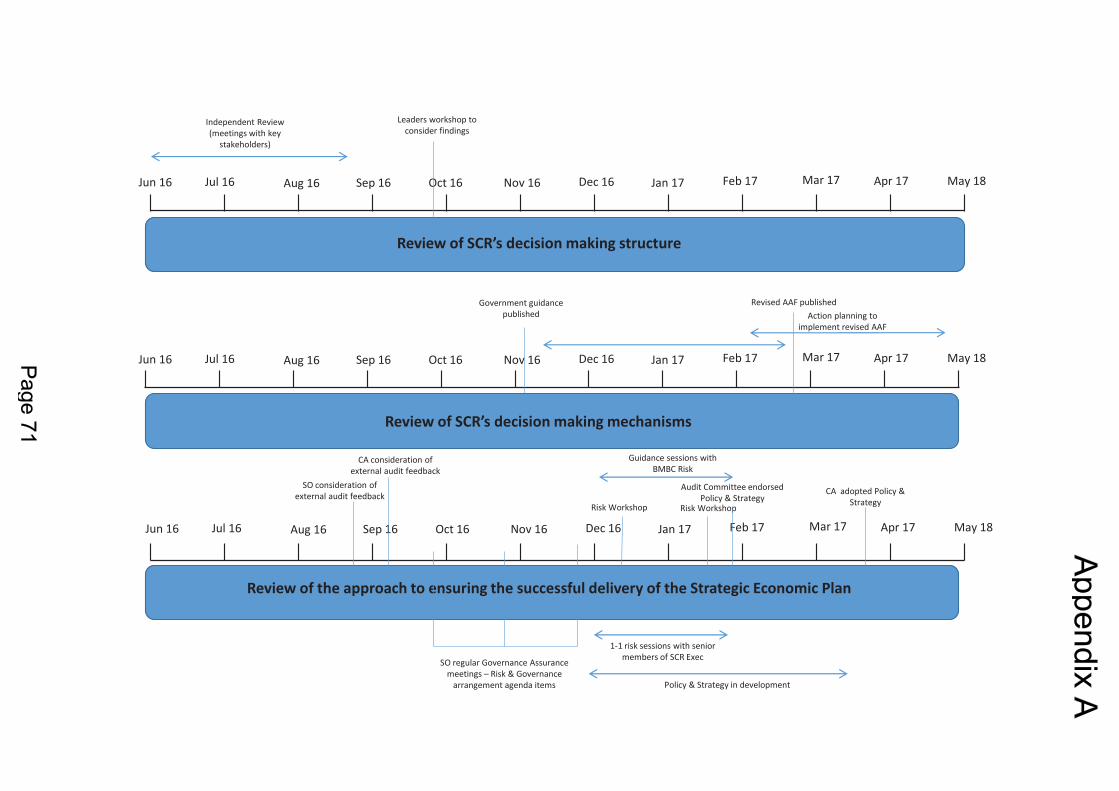

This matter is being dealt with by:Craig Tyler [email protected] 01226 772824

Gill Richards [email protected] 01226 772806

Contact Details

For further information or assistance please contact

Craig TylerSCR Combined Authority18 Regent StreetBarnsleySouth YorkshireS70 2HG

Tel: 01226 [email protected]

Gill RichardsSCR Combined Authority18 Regent StreetBarnsleySouth YorkshireS70 2HG

Tel: 01226 [email protected]

AUDIT COMMITTEE

11.00 AM, THURSDAY 27 APRIL 2017

18 Regent StreetBarnsleyS70 2HG

AGENDA

Item Page

1 Welcome and Apologies

2 Urgent Items / Announcements

3 Items to be considered in the Absence of the Public and Press

4 Declarations of Interest by Members

5 Reports from and Questions by Members

6 Questions from Members of the Public

7 Minutes of the Previous Meeting held on 26th January 2017 1 - 8

8 Internal Audit Charter 2017/18 9 - 24

9 Internal Audit Plan 2017/18 25 - 30

10 Internal Audit Progress Report 31 - 44

11 KPMG - SCR External Audit Plan Final 2016/17 45 - 64

12 SCR CA Governance Review Activity 2016/17 65 - 72

13 SCR Draft Code of Corporate Governance 73 - 84

AUDIT COMMITTEE

18 REGENT STREET, BARNSLEY, S70 2HG

MINUTES OF THE MEETING HELD ON 26 JANUARY 2017

PRESENT:

Councillor Mark Rayner, Chesterfield BC (Vice Chair, in the Chair)

Councillor Jeff Ennis, Barnsley MBCCouncillor Chris Furness, Derbyshire DalesCouncillor Allan Jones, Doncaster MBCCouncillor George Lindars-Hammond, Sheffield CCCouncillor Ian Saunders, Sheffield City CouncilCouncillor Austen White, Doncaster MBC

Ruth Adams, SCR Executive TeamTim Cutler, KPMGClaire James, SCR Executive TeamMartin McCarthy, South Yorkshire Joint AuthoritiesAndrew Shirt, South Yorkshire Joint AuthoritiesEugene Walker, S151 OfficerRob Winter, Internal Audit

Apologies for absence were received from Councillors K Reid, N Gibson, S Mohammed, J Shephard, P Short and K Wyatt

SCR Combined AuthorityAudit Committee

26/01/17

1 WELCOME AND APOLOGIES

The Chair welcomed everyone to the January meeting of the Sheffield City Region Combined Authority Audit Committee.

Apologies for absence were noted as above.

2 URGENT ITEMS / ANNOUNCEMENTS

No urgent items were requested.

3 ITEMS TO BE CONSIDERED IN THE ABSENCE OF THE PUBLIC AND PRESS

None.

4 DECLARATIONS OF INTEREST BY MEMBERS

None received.

5 REPORTS FROM AND QUESTIONS BY MEMBERS

Councillor Furness asked if he could be provided with an update in relation to the legal action taken by Derbyshire County Council against Sheffield City Region Combined Authority, noting that this had delayed the election of a City Region Mayor.

R Adams confirmed that Leaders of the CA had considered the High Court judgement and its implications on the Sheffield City Region’s Devolution Deal at the beginning of January.

CA Leaders had agreed that it was not possible to hold a Mayoral election in May 2017, due to the time required to carry out the additional consultation required and independent legal advice being sought before the period of Purdah commencing at the beginning of March.

CA Leaders had agreed that work on preparing the necessary additional consultation would not take place until after the May 2017 local elections.

6 QUESTIONS FROM MEMBERS OF THE PUBLIC

None received.

7 MINUTES OF THE PREVIOUS MEETING HELD ON 21ST JULY 2016

RESOLVED – That the minutes of the Committee held on 21 July 2016 be agreed as an accurate record.

SCR Combined AuthorityAudit Committee

26/01/17

8 SCR UPDATED RISK MANAGEMENT STRATEGY AND RISK REGISTER

A report was received to provide an update to the Audit Committee regarding the status of the strategic risks presented at the meeting held in July 2016 and, in addition, updates on the progress made in developing and embedding the SCR’s risk management process.

R Adams provided Members with an update on several matters arising in relation to risk following the Audit Committee held on 21 July 2016.

It was reported that Oxford Economics had been commissioned by the CA to carry out a piece of work on the implications of ‘Brexit’. This work would cover a number of areas, including the implications for trade and investment; business support; regulations; investment on university research funding; any sectorial impacts; labour market concerns, and any other areas of uncertainty.

The work on fully understanding the implications of ‘Brexit’ was underway; an update would be made at a future meeting.

It had been determined that the HS2 route change was not a particular risk for the CA, and was more appropriate for individual local authorities. It was noted that the CA had supported Councils where the blight would be most felt with the revised route. Additionally, the CA had agreed to carry out consultation to investigate how blight could be minimised from the routes.

Members were provided with an update on the current position in respect of the CA’s most significant Risks:-

The concern rating for Risk 001‘Failure of Partnership working to deliver the expected outcome for the Combined Authority’ had been minimised to concern rating 3, due to the control measures in place.

The concern rating for Risk 002 ‘Lack of robust internal control frameworks’ had been minimised to concern rating 3, due to the CA continually reviewing its governance arrangements and reviewing its Governance and Accountability Framework which would be presented at the next Scrutiny Committee. Additionally, the CA’s Financial Regulations had been updated, along with the CA’s Constitution being reviewed.

The concern rating for Risk 003 ‘Failure to ensure that the CA benefits from an appropriate level of staffing, resource and capacity’ had reduced to concern rating 3. Members were informed that the SCR Leaders had agreed that the SCR Executive Team be restructured around three key focuses. It was confirmed that the restructure was currently taking and that progress would be made during the forthcoming quarter.

The concern rating for Risk 11 ‘Failure to ensure that the CA considers wider implications and outcome that relate to non-essential impacts such as social value and growth’ had reduced to a concern rating of 5.

SCR Combined AuthorityAudit Committee

26/01/17

Risk 009 ‘Failure to ensure that significant changes and associated opportunities to the structure of the CA in terms of an Elected Mayor and the Devolution Deal are maximised to provide a strengthened approach to governance arrangements’, continued to be a high risk and a high concern rating; this risk continued to be monitored by the CA.

Linked to Risk 009 was Risk 012 ‘Unstable finance base: income and expenditure’ which continued to be a high risk, due to the CA having a large capital programme and a far smaller revenue programme.

It was reported that the revenue which supports the infrastructure was built on a variety of funding; the bulk of which, from income that derived from Enterprise Zone Business Rates. It was confirmed that Enterprise Zone Business Rates would not be known until the end of January, which, dependent upon the outcome, made it very difficult for long term planning in the SCR Executive for the next financial year, due to it being an unstable income base.

The anticipation was that, with the Devolution Deal, the SCR would be in receipt of Gainshare, which would have provided a more stable base and enable longer term planning.

Councillor Jones asked for confirmation when the SCR would likely receive confirmation that the Gainshare would be available.

R Adams explained that, Government had confirmed that Gainshare would only be made available to the CA, if SCR Leaders consent to the SCR Devolution Order.

Councillor Furness asked when Members would receive details of the re-convened Scrutiny Committee. It was confirmed that Members would be canvassed for their availability shortly.

Members were provided with further information regarding the SCR Executive Team’s revised method of managing risk for the CA.

Members were asked for their opinion in relation to the provision of assurance as set out in section 7 of the CA’s Risk Management Strategy.

Section 7 set out how the CA would manage risk, with the aim of providing Members with greater assurance of the Risk Framework. Members noted section 8 of the Strategy set out the longer term objectives for the Governance and Compliance function in relation to Risk Management.

In parallel with the Strategic Risk Register, the SCR’s Single Assurance Framework ensured that appropriate processes and protocols were in place for investment decisions. The framework also set out the mechanisms used to make decisions to deliver the SCR’s Regional Growth Deal allocations and its Strategic Economic Plan (SEP) and included a comprehensive approach to the identification, assessment and management of risk at Programme and Project level.

SCR Combined AuthorityAudit Committee

26/01/17

It was noted that, following Audit Committee feedback and in line with the SCR’s evolving governance and control procedures, the SCR Executive Team had reviewed its approach to monitoring and managing risk against relevant governance themes that underpin the successful delivery of the SEP. Moving forward, the strategic risk management approach would focus on the effectiveness of, and compliance with, the components of the governance and control framework.

Members were informed that, further to endorsement by the Audit Committee, the Risk Policy and Risk Management Strategy would be presented to the Combined Authority for approval.

Further work was currently underway with the SCR Executive Team to embed Risk Management processes at a strategic, operational and project level.

Councillor Jones commented that there were no operational risks which appeared on the Risk Register; he queried why this was the case. He felt that Audit Committee Members should have a full oversight of both strategic and operational risks.

R Winter explained that, the responsibility of the Audit Committee was to seek assurances that there were good and effective Risk Management processes in place which would give Members the assurance that, whatever the risks are, these were being identified, assessed and managed. If an operational risk became unmanageable and its risk score escalated, it would be on the radar of the statutory officers and reflected in Audit Committee reporting.

R Adams confirmed that, if a risk became out of tolerance, it would be escalated and appear on the Strategic Risk Register.

In addition, following the conclusion of the organisational restructure, the senior leadership group would work with their teams to identify risks and embed risk management processes at an operational level, focussing on high risk programmes.

Risk Management training would be rolled-out to relevant team members over the coming weeks.

RESOLVED – That the Audit Committee:-

1. Reviewed the status of risks recorded on the current Risk Register.

2. Reviewed the progress made in developing the SCR’s Risk Management processes and the proposed approach to Risk Management going forward.

3. Endorsed the Risk Policy and Risk Management Strategy for recommendation to the Combined Authority.

SCR Combined AuthorityAudit Committee

26/01/17

9 INTERNAL AUDIT PLAN CONSULTATION 2017/18

The Committee considered a report which set out the annual audit planning process and requested nominations for projects for potential inclusion in the draft Internal Audit Plan 2017/18.

Members were requested to provide the Chair with any nominations for collation and notification to the Head of Internal Audit.

It was noted that the proposed plan for 2017/18 would be presented at the next meeting.

RESOLVED – That the Audit Committee noted the following recommendations detailed in the report:-

1. Members’ views were sought regarding projects for potential inclusion in the Internal Audit Plan 2017/18.

2. Members should pass nominations for the 2017/18 Internal Audit Plan through the Chair for notification to Internal Audit.

3. Members considered the proposed planning process and were satisfied that it is sufficiently robust that it will determine a value-adding audit plan, informed by risk and through consultation with appropriate senior management.

10 INTERNAL AUDIT PROGRESS REPORT

A report was received to inform the Committee of the Internal Audit work completed and in progress from 1st July 2016 to 6th January 2017, the position with regard to the implementation of recommendations, about planned audit work and the performance of the Team.

It was reported that to date, a total of 75 days had been delivered (of the 110 days planned). Due to the continued work in developing and implementing aspects of the SCRCA’s control and governance framework, much of the planned Internal Audit work was scheduled towards the end of the financial year. In addition, two compliance reviews had been undertaken, both being concluded during 2016/17.

Members noted that there were no longstanding recommendations to report at this time.

There was one change to the Audit Plan at this time; the review of IT arrangements had been deferred to 2017-18, due to management currently undertaking a fundamental review of this business area. A review of procurement arrangements would be undertaken in 2016-17.

RESOLVED – That the Audit Committee noted the contents of the report.

SCR Combined AuthorityAudit Committee

26/01/17

11 EXTERNAL AUDIT UPDATE

T Cutler informed the Committee that detailed planning conversations continued with the SCR Executive Team with regard to producing the 2016/17 Audit Plan. It was anticipated that the 2016/17 Audit Plan would be presented at the April meeting of the Committee.

Members were informed that there would be no planned changes to the scope of KPMG’s audit for this year. KPMG would be providing an audit on the Financial Statements Opinion and a Value for Money Conclusion. In relation to the Value for Money Conclusion it was confirmed that, one of the areas of focus for KPMG would be to obtain an updated understanding of progress in implementing the CA’s governance arrangements, given those exceptions around the Value for Money Conclusion given last year.

RESOLVED – That the Audit Committee noted the verbal update.

CHAIR

.

Purpose of Report

To inform the Committee of the Internal Audit Charter for 2017/18.

Freedom of Information and Schedule 12A of the Local Government Act 1972

Under the Freedom of Information Act this paper and any appendices will be made available under the Combined Authority Publication Scheme. This scheme commits the Authority to make information about how decisions are made available to the public as part of its normal business activities.

In this section it must be clear if:

A – the paper will be available under the Combined Authority Publication Scheme

B – the paper is exempt under section 1 to 7 of Schedule 12A to the Local Government Act 1972 (report author to specify which exemption applies and why)

C – the paper is exempt under Part II of the Freedom of Information Act 2000 (report author to specify which exemption applies and why)

Recommendation

That the Audit Committee consider the Internal Audit Charter and be satisfied that it meets the requirements of the Public Sector Internal Audit Standards and adequately represents and describes the required function to provide the Audit Committee and senior management with a professional service.

27th APRIL 2017

AUDIT COMMITTEE: INTERNAL AUDIT CHARTER 2017/18

1. Introduction

1.1 The update of the Charter has considered the requirements of the revised Public Sector Internal Audit Standards which became effective from the 1st April 2017.

The Charter, prepared by the Head of Internal Audit (HoIA) and complemented by regular reports and an annual report, are intended to give the Audit Committee assurances regarding how the Internal Audit function is resourced, managed, organised and delivers its responsibilities.

1.2 The Audit Committee considers the Charter annually as required by the Public Sector Internal Audit Standards (PSIAS).

This latest review has ensured that the Charter reflects the current working arrangements of the function but also the aspirations and developments necessary to ensure continuous improvement. The Charter will be made available to all employees through the Service’s Intranet site.

The Charter has been revised to also reflect the changes within the broad client base and the revised structure of the Service that became effective from 1st April 2017 following a fundamental review through the Council’s Future Council programme.

As well as to the SCRCA, the Internal Audit Team provides services to Barnsley MBC, Berneslai Homes, the South Yorkshire Police and Crime Commissioner, South Yorkshire Police Chief Constable, South Yorkshire Fire and Rescue Authority, South Yorkshire Pensions Authority and the South Yorkshire Passenger Transport Executive. Core Internal Audit coverage is now a 40:60 split between the Council and non-Council clients.

The Charter will undergo an annual review to ensure it remains reflective of current working arrangements and professional standards.

2. Implications

2.1 Financial

The charge for the Internal Audit service is estimated to be as planned and budgeted for and consequently there are no specific financial implications to consider.

2.2 Legal

There are no legal implications.

2.3 Risk Management

Management engagement and responses remain positive which helps support a positive assurance that where opportunities for control, risk or governance improvements are highlighted, these are embraced by management.

2.4 Equality, Diversity and Social Inclusion

There are no implications.

3. Appendices/Annexes

3.1 The Internal Audit Charter is attached at Appendix A

REPORT AUTHOR Rob Winter CPFAPOST Head of Internal Audit and Corporate Anti-Fraud

Officer responsible Sharon Bradley CMIIAOrganisation Audit Manager (SCRCA)

Email [email protected] 01226 773187

Background papers used in the preparation of this report are available for inspection at: Barnsley MBC Westgate Plaza One office, Barnsley.

Other sources and references: Public Sector Internal Audit Standards 2013 and revised global internal audit standards 2017.

1

BARNSLEY M.B.C.

INTERNAL AUDIT SERVICES

INTERNAL AUDIT CHARTER

2017 / 2018

The Barnsley MBC Internal Audit Service also provides services to a broad range of external organisations. The term 'organisation' is therefore used in the Charter to cover all clients both individually and collectively. Unless specifically referred to all aspects of the Charter apply to all client organisations.

For the purposes of Internal Audit activity, the term ‘board’ refers to the appropriate Audit Committee. The term ‘senior management’ refers to the Chief Executive and most senior directors or equivalent e.g. the Chief Constable and Senior Leadership Group; the Chief Fire Officer and Executive Team; or the Chief Executive and Senior Management Team.

Other senior posts such as the statutory Section 151 Officer / Director of Finance / Chief Finance Officer are used synonymously.

The Public Sector Internal Audit Standards (PSIAS) refer to the officer responsible for the Internal Audit function as the Chief Audit Executive. This role is undertaken by the Head of Internal Audit (HoIA).

2

INTERNAL AUDIT CHARTER

1. Introduction

The Internal Audit function is a key component of an organisation's governance framework. As such it aims to provide a professional and high quality objective and independent management support function in order to influence and contribute to the achievement of strategic and operational objectives. A key component of this support is the development and maintenance of excellent client relationships and adopting an innovative and flexible approach to the delivery of the function.

This Charter provides the framework for the conduct of the Internal Audit function and is applicable to all client organisations. This Charter will be reviewed annually by the relevant Audit Committee, or their equivalent to ensure it remains relevant to the demands and responsibilities of the client service and supports the relevant organisation's corporate objectives.

Each client organisation is responsible for establishing and maintaining appropriate risk management processes, internal control systems, accounting records and governance arrangements. Internal Audit plays a vital part in advising whether effective and efficient arrangements exist. The annual HoIA opinion, which informs the annual governance statement, both emphasises and reflects upon the importance of this aspect of Internal Audit work. The response to Internal Audit activity should, where deemed necessary, lead to the strengthening of the control environment and therefore contribute to the achievement of the corporate objectives, improvement, support innovation and change and enhance public accountability and transparency.

Vital components of a successful internal audit service include effective working relationships, maintaining professional independence and objectivity and working in partnership with management to assist in ensuring that an effective organisation-wide control environment exists. The Internal Audit service embraces this approach by effective communication and regular contact with its clients in order to help the organisation achieve its objectives.

2. The Purpose of the Charter

The Public Sector Internal Audit Standards (PSIAS) are mandatory guidance and constitute principles of the fundamental requirements for the professional practice of internal auditing and for evaluating the effectiveness of Internal Audit’s performance. An important element of these standards is the requirement to have a formal Charter.

The purpose of this Charter is to set out the purpose, authority and responsibility of the Internal Audit Service. In addition it also sets out the nature, objectives, outcomes and the scope of its activities within its client organisations. This therefore forms the basis of the terms of reference for the function.

3

3. Definition of Internal Audit

The PSIAS provides the following definition of Internal Audit:

“Internal auditing is an independent, objective assurance and consulting activity designed to add value and improve an organisation’s operations. It helps an organisation accomplish its objectives by bringing a systematic, disciplined approach to evaluate and improve the effectiveness of risk management, control and governance processes”.

This definition encourages a collaborative style of audit review which focuses on evaluating and improving the effectiveness of risk, control and governance and therefore goes significantly beyond basic compliance.

Allied to this definition are the 10 Core Principles for internal audit as defined in the International Standards for the Professional Practice of Internal Auditing (IPPF). These are:

Demonstrates integrity – through adherence to the code of ethics for internal auditors

Demonstrates competence and due professional care – having a comprehensive performance and professional development framework

Is objective and free from undue influence (independent) – through its organisational position, access rights and the status of the HoIA

Aligns with the strategies, objectives and risks of the organisation – adopting a risk-based approach to all work

Is appropriately positioned and adequately resourced – through access to senior management and the audit committee and having an appropriate level of resources / budget

Demonstrates quality and continuous improvement – meeting the requirements of the PSIAS in maintaining an appropriate quality assurance and improvement programme (QAIP)

Communicates effectively – through appropriate liaison and reporting channels with senior management and audit committees

Provides risk-based assurance – through a robust audit planning process and the consideration of risk and strategic and operational objectives

Is insightful, proactive and future-focussed – through effective and proportionate deployment of resources for research, adopting a ‘single point of contact/subject matter expert’ approach and undertaking appropriate consultancy services

Promotes organisational improvement – maximising the wider consultancy capacity of internal audit and ensuring a clear understanding of the operational and strategic context of each client organisation

How the Internal Audit service is structured, managed and operates aims to demonstrate how these core principles are met. The performance management

4

and accountability framework developed by the Service is how this will be demonstrated.

The IPPF has also provided a ‘mission statement’ for internal audit that sets out what it aspires to accomplish within an organisation through the definition and core principles. The mission is:

“To enhance and protect organisational value by providing risk-based and objective advice and insight”

4. Operational Context

The Barnsley Internal Audit Service operates within a challenging and diverse environment across a variety of client organisations to deliver the services each requires and to ensure it does so to high professional standards and demonstrating added value. The Service needs to be able to react and adapt to the rapid pace of change which is taking place both locally, regionally and nationally within each client organisation. Accordingly, the Charter includes the aspirations of the Internal Audit Service, which are to:

further develop and enhance working relationships particularly where a client organisation is undergoing significant change to ensure that the service is aware of and understands its needs and objectives

promote and support clients with regards to an increase in collaborative working

understand its position with respect to the organisation’s other sources of assurance and plan our work accordingly

be seen as a catalyst and support for change at the heart of the organisation

be the internal auditor of choice, delivering exceptional client service add value and assist the organisation in achieving its objectives be forward looking – knowing where the organisation wishes to be and

being aware of the relevant national agenda and its impact be innovative, insightful and challenging help to shape the ethics and standards of the organisation, reducing

bureaucracy whilst maintaining high standards of public accountability, transparency and governance

ensure the right resources are available, recognising that the skills mix, capacity, specialisms, qualifications and experience requirements all change constantly

ensure all staff are supported in undertaking relevant professional qualifications and continuous professional development to increase standards, efficiency and effectiveness

share best practice with other internal auditors, clients and other professional services (e.g. financial services) and

seek opportunities for joint working with other organisations’ auditors.

5

5. Scope of Internal Audit

The scope of internal auditing encompasses the examination and evaluation of any aspect of an organisation’s activities in order to assess the adequacy and effectiveness of the framework of governance, risk management, and internal control processes such that the HoIA can provide an annual opinion on the extent to which the organisation can rely on it.

6. Responsibilities and Objectives of Internal Audit

The responsibilities and objectives of Internal Audit are as follows:

i. To be a valuable asset to the organisation by supporting senior management in meeting their corporate responsibilities.

ii. To contribute to the assurances sought by those charged with governance in relation to the robustness and reliability of internal controls, risk management and governance to support the Annual Governance Statement (AGS).

iii. To support the Statutory Chief Finance Officer in discharging their duties.iv. To review, appraise and report on the extent to which the assets and

interests of the organisation are accounted for and safeguarded from loss and the suitability and reliability of financial and other management data and information.

v. To support the requirement to seek efficiency including the arrangements for achieving value for money and effective change management.

vi. To provide soundly based assurances to management on the adequacy and effectiveness of their internal control, risk and governance arrangements, with such assurances including information technology governance and ethical behaviour.

vii. To assess the adequacy and effectiveness of the organisation's contracts, procurement, commissioning and associated governance arrangements.

viii. To assess effectiveness of the corporate risk management process and make recommendations to improve and embed the process where required whilst ensuring that Internal Audit does not adopt management responsibilities for managing risks.

ix. To evaluate the risk of fraud, bribery and corruption and the manner and effectiveness of how it is managed by the organisation. In addition, to reduce the incidence of fraud, loss and irregularity by publicising the findings of fraud investigations to act as a deterrent and provide a quality corporate fraud and irregularity prevention, detection and investigation service.

x. To disseminate examples of best practice in the application of an effective control, risk and governance framework.

xi. To provide an Internal Audit advisory service intended to add wider organisational value and improve the effectiveness and efficiency of governance, risk management and control processes.

xii. To provide advice and an objective and supportive consulting service in respect of the development of new programmes and processes and / or significant changes to existing programmes and processes including the design of appropriate controls. This is usually achieved through

6

membership of Officer Groups, Governance and other Boards or working parties as well as direct contact with officers within services / functions / departments. Such advice and consultation work forms an increasingly important part of the audit plan.

xiii. To prepare timely, concise and informative reports to management to facilitate the improvement of the control environment.

xiv. To undertake Audit support activities in respect of assisting the Audit Committee (or equivalent) to discharge its responsibilities; monitoring the implementation of agreed recommendations; disseminating across the entity best practice and lessons learnt arising from its audit activities, and having oversight of the audit function.

7. Organisational Independence of Internal Audit

An independent approach and mindset is essential to the effectiveness of the Internal Audit function. To ensure this, Internal Audit will operate within a framework that allows:-

Unrestricted access to the 'Chief Executive'; the 'Chief Finance Officer'; the Chair of the Audit Committee and Audit Committee Members; individual Senior Management Officers; employees and the responsible External Auditor.

The HoIA reporting in his own name. Segregation from line operations.

The Internal Audit function has no sole or direct responsibility for developing or implementing procedures or systems and does not prepare records or engage in original line processing functions or activities.

Internal Auditors are generally not involved in undertaking non-audit activities and an Auditor will not be involved in the audit of any system or process for which they had previous operational responsibility for a period of two years. This principle will equally apply to any consultancy type assignments.

Audit responsibilities are periodically rotated to avoid over-familiarity and complacency but balanced to provide reasonable service continuity and resilience.

8. Code of Ethics

The IPPF advocates that internal auditors conform to a code of ethics to promote an ethical culture in the profession of internal auditing. This is an important concept given that the nature of internal auditing is one built on trust and respect under-pinning its independent and objective approach.

The four components of the Code of Ethics are:

Integrity:

In the conduct of audit work, Internal Audit staff will:

7

i. Perform their work with honesty, diligence and responsibility;ii. Observe the law and make disclosures expected by the law and the

profession;iii. Not knowingly be party to any illegal activity, or engage in acts that are

discreditable to the profession of internal auditing or the organisation;iv. Respect and contribute to the legitimate and ethical objectives of the

organisation.

Objectivity:

Internal Auditors must exhibit the highest level of professional objectivity in gathering, evaluating, and communicating information about the activity or process being examined. Internal Auditors must make a balanced assessment of all the relevant circumstances and not be unduly influenced by their own interests or by others in forming judgements.

In the conduct of audit work internal auditors shall:

i. Not take part in any activity or relationship that may impair or be perceived to impair their unbiased assessment;

ii. Not accept anything that may impair or be perceived to impair their professional judgement

iii. Disclose all material facts known to them that if not disclosed may distort the reporting of activities under review

In addition, internal auditors will;

iv. Declare any real or perceived interests on an annual basis. A prompt is included at the assignment planning phase of each audit;

v. Comply with the Bribery Act 2010.

Confidentiality:

Internal auditors must respect the value and ownership of information they receive and do not disclose information without appropriate authority unless there is a legal or professional obligation to do so.

Internal Auditors are expected to display confidentiality by:

i. Acting prudently when using information acquired in the course of their duties and protecting that information and;

ii. Not using information for any personal gain or in any manner that would be contrary to the law or detrimental to the legitimate and ethical objectives of the organisation.

Competency:

Internal Auditors are expected to apply the knowledge, skills and experience needed in the performance of internal audit activities.

Internal auditors will demonstrate their competency by:

8

i. Only engaging in services for which they have the necessary knowledge, skills and experience;

ii. Performing internal audit services in accordance with the IPPF iii. Continually seeking to improve their proficiency, effectiveness and quality

of their services

In addition, internal auditors will:

iv. Be skilled in dealing with people at all levels and communicating audit, risk management and related issues effectively;

v. Exercise due professional care in performing their duties and;vi. Conform with the PSIAS. NB: Any non-conformance with the PSIAS will

be disclosed within the engagement results / output including the reasons for the non-conformance and the impact.

8. Accountability, Reporting Lines and Relationships of the Head of Internal Audit

Accountability:

In relation to organisations governed by public sector legislation, (e.g. the Accounts and Audit Regulations 2015, Regulation 5 and Police Reform and the Social Responsibility Act 2011), such organisations are responsible for maintaining an adequate and effective Internal Audit function. In practical terms this means that the HoIA is accountable to the ‘Chief Executive’ and Audit Committee.

Reporting Lines and Relationships:

Within Barnsley MBC as the direct employing organisation, the HoIA reports administratively to the Service Director – Finance and has strategic and operational responsibility for the Internal Audit function and fulfils the specific designated role of the HoIA for the Council.

This specific designated role and its responsibilities are replicated for each client organisation with the HoIA being responsible to a designated senior manager (usually the chief financial officer or chief executive) and accountable to the Audit Committee or other relevant executive body.

While audit plans are considered by a range of senior managers and the Audit Committees of each client organisation, the professional responsibility for Internal Audit coverage rests with the HoIA who may determine and change the Internal Audit Service’s own priorities as appropriate. The HoIA has a functional reporting line to each client Audit Committee Chairman, the 'Chief Executive' and SMT Members, or equivalent.

The HoIA reports periodically to each Audit Committee. The reports provide information in respect of:

9

i. Periodic reports detailing: the audits completed; an assurance opinion on the overall state of internal controls for that particular period along with any fundamental issues requiring management attention based on the work of internal audit; progress in implementing the audit work plan; the status of the implementation of agreed internal audit recommendations;

ii. An annual opinion on the internal control, risk management and governance arrangements in each client organisation highlighting any fundamental issues requiring management attention based on the work of internal audit as reported within the periodic reports and;

iii. An annual report summarising the outcome of the review of the effectiveness of the internal audit function which is required under the PSIAS.

Internal and External Audit activities will be coordinated to help ensure the adequacy of overall audit coverage and to minimise any duplication of effort. Periodic meetings and contact between Internal and External Audit will be held to discuss matters of mutual interest. External Audit will have full and free access to all Internal Audit plans, working papers and reports. Similarly the function will coordinate its activities with other regulatory / inspection bodies where relevant.

Where it is appropriate Internal Audit will liaise with other internal functions or inspectorates, to ensure work is co-ordinated, mutually beneficial and where applicable utilised for assurance purposes (e.g. HMIC).

It is important to stress the existence of Internal Audit does not diminish the responsibility of management to establish and maintain systems of internal control, effective risk management and governance arrangements to ensure that activities are conducted in a secure, efficient and well-ordered manner.

9. Arrangements for Anti Fraud, Corruption and Bribery

Arrangements for combatting fraud, bribery and corruption will be set out by management in each organisation's anti-fraud and corruption policies and other supporting guidance. The HoIA should be notified of all suspected or detected fraud, corruption, impropriety or other irregularity, in order to inform the annual Internal Audit opinion and the risk-based plan.

Internal Audit’s role in respect of fraud-related work is as follows:

i. In support of the organisation's anti-fraud, Whistleblowing, Money Laundering, bribery and corruption policies, Internal Audit prepares periodic guidance for managers and the Board;

ii. To undertake proactive fraud detection work in high risk areas as defined by the fraud risk assessment and management process;

iii. To co-ordinate Barnsley MBC's, SY Fire and Rescue Authority, SY Police, SYPCC and SY Pensions Authority response to the mandatory National Fraud Initiative (NFI) exercise;

iv. To contribute to corporate counter fraud arrangements and;v. In certain circumstances and where discussed and agreed with

management, Internal Audit (through the Corporate Anti-Fraud Team) assume a lead role in the investigation of alleged irregularities. Internal

10

Audit will provide guidance and support to management throughout the investigatory process. The balance of work between that undertaken by Internal Audit and management will be kept under review to ensure the most appropriate use of specialist resources. With this in mind it is anticipated that Internal Audit will spend increasingly less time undertaking routine investigations.

10. Consultancy Work

The definition of internal audit makes reference to it being a “consulting activity” and therefore such work needs to be carefully scoped and managed to ensure the core purpose and responsibilities of internal audit are not compromised.

The scoping of audit work will make it clear in what guise it will be performed, the methodology to be used and the format and nature of the reported outcomes.

Due regard of the requirements of the client will be considered to preserve and demonstrate internal audit objectivity and independence in any consultancy engagement.

This nature of work is however increasingly important and valued by clients and provides an additional way in which Internal Audit can provide and demonstrate wider value beyond basic controls assurance. Providing this support also clearly links to a number of the core principles about being insightful, forward-focussed, proactive, and being able to promote organisational improvement.

11. Authority of Internal Audit

In accordance with the PSIAS, the scope of Internal Audit allows that in fulfilment of audit responsibilities unrestricted coverage of all the organisation’s activities and unrestricted access to all functions, records, data, personnel, premises and assets of the organisation and its partner organisations, is granted in the course of audit work and as set out in relevant partnership agreements and contracts.

Internal Audit has the authority to obtain such information and explanations as it considers necessary to fulfil its responsibilities.

All records, documentation and information accessed in the course of undertaking internal audit activities are to be used solely for the conduct of these activities. The HoIA and staff are responsible and accountable for maintaining the confidentiality of the information they receive during the course of their work.

12. Appropriate Resourcing of Internal Audit

At least annually, the HoIA will submit to the 'Chief Executive' and the Audit Committee an Internal Audit plan for review and approval. The plan will consist of a work schedule and resource requirements for the next financial year. The plan will include the impact of any resource limitations and significant actual or planned changes.

11

The Internal Audit plan is developed utilising a risk-based methodology to determine the prioritisation of the audit work, including the input of senior management and the Audit Committee. Any material deviations from the approved Internal Audit plan will be communicated to the Audit Committee through periodic activity reports.

Should the HoIA have concerns regarding the resources of the Internal Audit function, he will raise these with the appropriate client Chief Executive and Chief Finance Officer. The inadequate resourcing of the internal audit function may result in the HoIA being unable to provide an annual opinion on a client’s internal control, risk and governance environment.

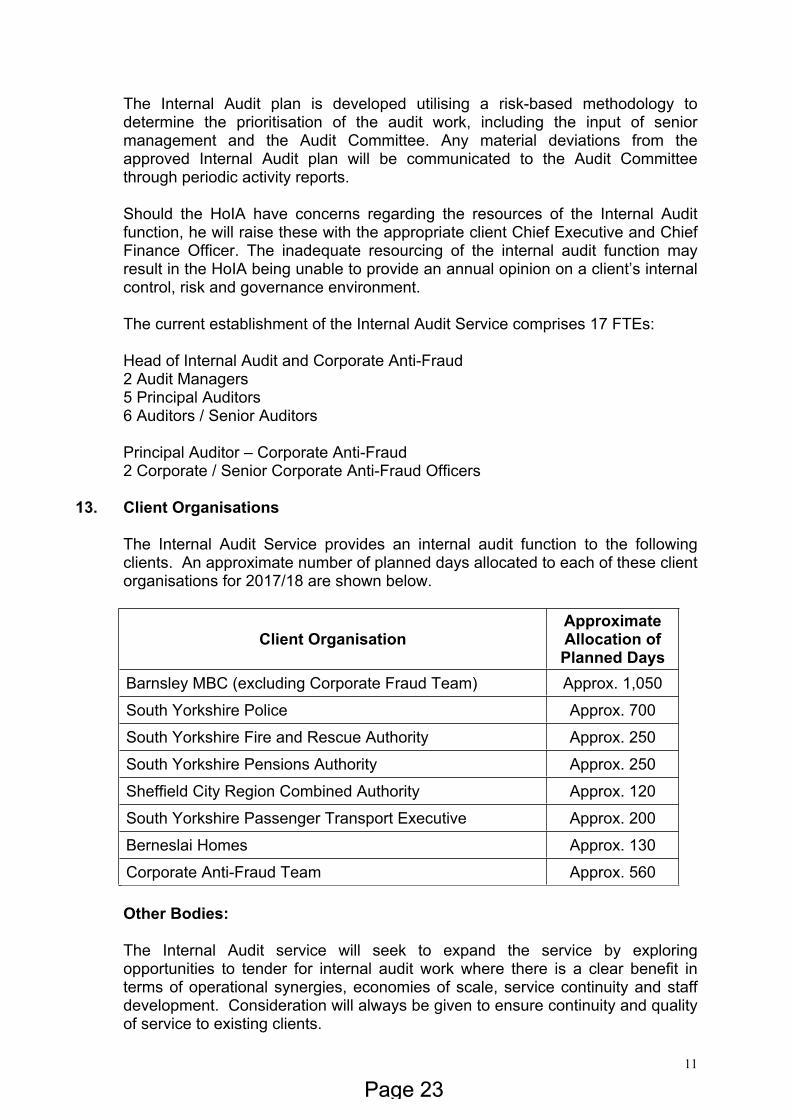

The current establishment of the Internal Audit Service comprises 17 FTEs:

Head of Internal Audit and Corporate Anti-Fraud2 Audit Managers5 Principal Auditors6 Auditors / Senior Auditors

Principal Auditor – Corporate Anti-Fraud2 Corporate / Senior Corporate Anti-Fraud Officers

13. Client Organisations

The Internal Audit Service provides an internal audit function to the following clients. An approximate number of planned days allocated to each of these client organisations for 2017/18 are shown below.

Client OrganisationApproximate Allocation of Planned Days

Barnsley MBC (excluding Corporate Fraud Team) Approx. 1,050

South Yorkshire Police Approx. 700

South Yorkshire Fire and Rescue Authority Approx. 250

South Yorkshire Pensions Authority Approx. 250

Sheffield City Region Combined Authority Approx. 120

South Yorkshire Passenger Transport Executive Approx. 200

Berneslai Homes Approx. 130

Corporate Anti-Fraud Team Approx. 560

Other Bodies:

The Internal Audit service will seek to expand the service by exploring opportunities to tender for internal audit work where there is a clear benefit in terms of operational synergies, economies of scale, service continuity and staff development. Consideration will always be given to ensure continuity and quality of service to existing clients.

12

14. Internal Audit Strategy

Whilst not a specific requirement of the PSIAS the Internal Audit Service also prepares a Strategy. This strategy has previously been an over-arching one covering all client organisations. Due to the increasing differences between clients, their operational contexts, pressures, priorities and requirements from Internal Audit, a specific strategy document has been prepared for each client organisation.

The audit strategy documents reflect closely the audit planning process and the context of the annual operational audit plans.

April 2017

.

Purpose of ReportThis report informs the Audit Committee of the Internal Audit plan for 2017/18 (Appendix A). The report includes a summary of audit activity in relation to the Authority.

This report briefly describes the rationale and process for setting the plan, that it is based on a risk assessment process, historical data and consultation.

The proposed Plan has been considered by the Statutory Officers Group on 10th April 2017.

The consideration and approval of the audit plan is one of the key responsibilities of the Audit Committee.

Freedom of Information and Schedule 12A of the Local Government Act 1972Under the Freedom of Information Act this paper and any appendices will be made available under the Combined Authority Publication Scheme. This scheme commits the Authority to make information about how decisions are made available to the public as part of its normal business activities.In this section it must be clear if: A – the paper will be available under the Combined Authority Publication Scheme

B – the paper is exempt under section 1 to 7 of Schedule 12A to the Local Government Act 1972 (report author to specify which exemption applies and why)C – the paper is exempt under Part II of the Freedom of Information Act 2000 (report author to specify which exemption applies and why)

RecommendationsIt is recommended that:-

i. the Internal Audit plan 2017/18 (Appendix A) is approved, acknowledging the need for the Head of Internal Audit to exercise his professional judgement during the year to apply the Plan flexibly according to priority, risk and resources available; and

ii. the Committee receives monitoring reports from the Head of Internal Audit to

demonstrate progress against the plan including information where the Plan has materially varied from the original Plan.

27th APRIL 2017AUDIT COMMITTEE: INTERNAL AUDIT PLAN 2017/18 REPORT

1. Introduction

1.1 One of the key aspects of the organisation and operation of Internal Audit is the preparation and delivery of an operational plan. The plan seeks to ensure an appropriate deployment of the allocated resources across the Authority taking into account known risks, organisational developments, projects and initiatives all supporting the fundamental need to assess the adequacy and effectiveness of the internal control, risk and governance environment and ultimately inform the Head of Internal Audit’s opinion for inclusion in the Annual Governance Statement (AGS).

1.2 Key to a sound risk based plan is to ensure it is developed in collaboration with management. The culture of a modern Internal Audit service is not about keeping its work secret - successful audit services are characterised by operating ‘with’ and ‘for’ management rather than doing it ‘to’ them. This Plan has therefore been prepared following consultation with a range of senior officers and as audit planning is a continuous process it has included the following:

Consideration of issues included in the risk register(s) together with mitigating controls.

Consideration of historical and topical issues as well as horizon scanning to attempt to identify any major issues that might affect the controls, risks or governance of the Authority.

Consideration of issues to assist the Section 151 Officer to fulfil his responsibilities and to meet other legal requirements.

Consultation with senior managers responsible for the delivery of services. Consultation with the Audit Committee with responsibility for overseeing

delivery of the work of the Internal Audit Team and with the responsibility for overseeing good governance within the Authority.

1.3 It is important to acknowledge at the outset that whilst great care and consideration is given to establish the operational plan each year, it is designed to be flexible. Good audit practice encourages the flexible use of limited resources reflecting the need to respond to emerging risk issues, requests for advice and assistance, and the need to investigate any irregularities should they arise.

1.4 As well as providing management with an overview of Internal Audit coverage in support of their risk concerns, the plan sets a framework to manage Internal Audit resources within the function. The plan gives Internal Audit staff a focus and a degree of certainty regarding what they will be doing. This lends itself to establish a robust training and development framework where Internal Audit staff can be allocated to jobs based on their skills, experience and emerging abilities. Internal Audit has a policy of regularly reviewing the skills needs of the Service and identifying the training and development necessary to meet these needs.

1.5 Further information is contained within the Audit Charter which sets out the nature, objectives, outcomes, responsibilities and scope of its activities within its client organisations. The Audit Charter is compiled in accordance with the Public Sector Internal Audit Standards (PSIAS) which contains mandatory guidance and principles behind the professional practice of internal auditing and for evaluating the effectiveness of Internal Audit’s performance. The Audit Charter for 2017/18

is included on the Audit Committee’s agenda.

1.6 Delivery of the service will be by Barnsley MBC who deliver services to the following ‘clients’:

Sheffield City Region Combined Authority; South Yorkshire Passenger Transport Executive; South Yorkshire Fire and Rescue Authority; South Yorkshire Police & Crime Commissioner South Yorkshire Police Chief Constable; South Yorkshire Pensions Authority; Barnsley MBC; and Berneslai Homes.

2. Internal Audit Plan 2017/18

2.1 The Audit Plan (Appendix A) has been prepared to ensure adequate coverage across a broad basis of Internal Audit work to support the assurances that management and the corresponding Audit Committee require and provides a total planned allocation of 120 days assigned to the Authority for 2017/18 whic will be monitored during the year.

2.2 Whilst the principle of the audit plan is one based on risk, there are a number of areas of work and therefore a proportion of the plan that are undertaken annually. The precise deployment of Audit resources may within these areas be risk based but the initial identification of these areas is somewhat pre-determined. These are:-

Audit Activity RationaleCore financial systems

This work is also required by the S151 officer and also considered by External Audit.

Corporate Governance

Annual provision for undertaking review work on the Annual Governance Statement process and risk management.

Advice, audit planning, management, follow up & feedback

Standard annual provisions for each client for general advice, annual and periodic planning, obtaining and dealing with feedback from audits along with the follow up of audit recommendations (as per the follow up protocol), preparation of Audit Committee reports, attendance at Audit Committee and other meetings

Contingency Days set aside for unplanned work or increases in the scope of planned work, including provision for undertaking special investigations and follow-up work.

2.3 In addition to the annual areas of work referred to in 2.2, consultation with the Management Team and Statutory Officers has identified key priority areas of work for Internal Audit, to provide the required assurances that the control framework is operating robustly within their particular business areas. A full list of planned work is attached to the report. The key areas of activity are:

Information governance assurance

Compliance with transparency requirements Programme / Performance Management Business Innovation Fund (BIF)

2.4 At the point of preparing the Plan it is not always easy or appropriate to specifiy a number of days against certain pieces of work. Given the flexibility underpinning the Plan approach and the need for Internal Audit to be able to respond to unforeseen events, the total number of indicative days are agreed with senior management relevant to budget provision and risk assessment with the understanding that during the year as and when individual pieces of work are scoped in detail, the precise number of days for each piece of work will be determined. Most pieces of work are likely to be between 10 and 20 days in duration to allow sufficient depth of coverage and therefore provide the greatest benefit and value. Equally, the flexibility within the Plan also extends to when work will be undertaken during the year, including the possibility of deferring work to the following financial year. All proposed changes to the Plan or when work will be undertaken will be discussed and agreed with management and reported within the Progress reports to the Audit Committee.

2.5 Themes have also been developed and applied to each auditable area. These have been based on the key areas of assurance as reflected in the annual governance statement process and therefore in support of those officers charged with lead responsibilities. The same themes are set up within the audit management system and linked to all findings and recommendations. Functionality within the system enables reports covering the defined themes to be produced on audit work completed during a given period. This serves as a source of assurance information for Internal Audit and the senior officers with lead responsibilities for compliance and monitoring e.g. having an information technology or systems theme enables the appropriate responsible officer to be provided with issues extracted from across all audits regarding the levels of compliance with IT/IS related controls and procedures.

2.6 As part of the delivery of the 2017/18 Audit Plan emphasis will continue on enhanced customer focus and liaison, which will include periodic attendance at relevant senior management team meetings to report on progress against planned work. Quarterly plan monitoring/progress reports will continue to be presented to the Audit Committee.

3. Appendices/Annexes

3.1 The report attached at Appendix A includes a detailed draft 2017/18 plan.

REPORT AUTHOR Rob Winter CPFAPOST Head of Internal Audit and Corporate Anti-Fraud

Officer responsible Sharon Bradley CMIIAOrganisation Audit Manager (SCRCA)

Email [email protected] 01226 773187

Background papers used in the preparation of this report are available for inspection at: Barnsley MBC Westgate Plaza One office, Barnsley.

Sheffield City Region Combined Authority – Internal Audit Plan 2017/18

Client Business Unit / Service Assignment Title Outline Scope / Purpose Risk / Gov. Area

SCRCA Finance C/fwd Procurement Review To complete the 2016/17 review Fin. Mgt; Int. Controls; DQ; Legal

SCRCA Finance C/fwd Payroll Review To complete the 2016/17 review. Fin. Mgt; Int. Controls; DQ

SCRCA Service Wide Advice, Planning & Feedback, Follow Up of Recommendations & Client Liaison

Provision of advice, as and when requested. Day to day management of annual audit plan, including scheduling of resources and incorporating any revisions. Follow up and update of the status of recommendations from individual audit assignments. Attendance at Stat Officers Meeting, client rep meetings etc.

All

SCRCA Service Wide Annual Audit Planning 2018-19 To discuss and develop an agreed annual audit plan for 2018-19. All

SCRCA Service Wide Audit Committee Preparation of reports and attendance at the Audit Committee meetings. Liaison with the Chair of the Audit Committee.

All

SCRCA Service Wide AGS process To provide advice, support and guidance on the AGS process and arrangements. HoIA statement.

Ethical; Safeguarding; Fin. Mgt; Int. Controls;

DQSCRCA Service Wide Risk Management To provide assurance on the Risk Management Framework and process. To include

compliance testing.Fin. Mgt; Int. Controls;

DQ

SCRCA Finance Core Financial Systems To provide assurance that systems and controls are robust and operating effectively and efficiently. Risk based strategy, systems to be determined.

Fin. Mgt; Int. Controls; DQ

SCRCA TBD Information Governance To provide assurance that the information handled by the SCRCA is effectively and efficiently managed, adherence to legislation. To include the retention of documentation and data quality.

Ethical; Safeguarding; Fin. Mgt; Int. Controls;

DQSCRCA TBD Compliance with Transparency To provide assurance that the SCRCA is complying with the AAF guidelines.

Reduced scope - this will not extend to the compliance with the wider government transparency agenda compliance (e.g. publishing of procurement data, salaries etc).

Fin. Mgt; Int. Controls; DQ

SCRCA TBD BIF To provide assurance that the programme/project management arrangements are robust and operating effectively & efficiently. BIF delegations are set out and decisions reported to the CA.

Fin. Mgt; Int. Controls; DQ

SCRCA TBD Programme / Performance Management

To provide assurance that the capital programme (incl. Growth Hub) is being effectively and efficiently managed, with clearly defined roles & responsibilities assigned to Officers. To include performance management arrangements of projects.

Fin. Mgt; Int. Controls; DQ

SCRCA Service Wide Contingency General provision of days to accommodate changes in the scope of work, ad hoc requests beyond advisory and general unplanned work.

All

.

Purpose of Report

To inform the Committee of the Internal Audit work completed and in progress from 7th January 2017 to 31st March 2017, the position with regard to the implementation of recommendations, about planned audit work and the performance of the Team.

Freedom of Information and Schedule 12A of the Local Government Act 1972

Under the Freedom of Information Act this paper and any appendices will be made available under the Combined Authority Publication Scheme. This scheme commits the Authority to make information about how decisions are made available to the public as part of its normal business activities.

In this section it must be clear if:

A – the paper will be available under the Combined Authority Publication Scheme

B – the paper is exempt under section 1 to 7 of Schedule 12A to the Local Government Act 1972 (report author to specify which exemption applies and why)

C – the paper is exempt under Part II of the Freedom of Information Act 2000 (report author to specify which exemption applies and why)

Recommendations

It is recommended that Members consider the report and as necessary request further information and/or explanations from Internal Audit or Management.

27th APRIL 2017

AUDIT COMMITTEE: INTERNAL AUDIT PROGRESS REPORT

1. Introduction

1.1 As part of its core functions the Audit Committee oversees the work of the Internal Audit Team and receives various reports. The following have been provided to date:-

April 2016

IA Progress ReportIA Annual Plan Report 2016-17IA Charter & Strategy 2016-17

July 2016

IA Annual ReportIA Effectiveness ReportIA Progress Report

January 2017

IA Plan Consultation ReportIA Progress Report

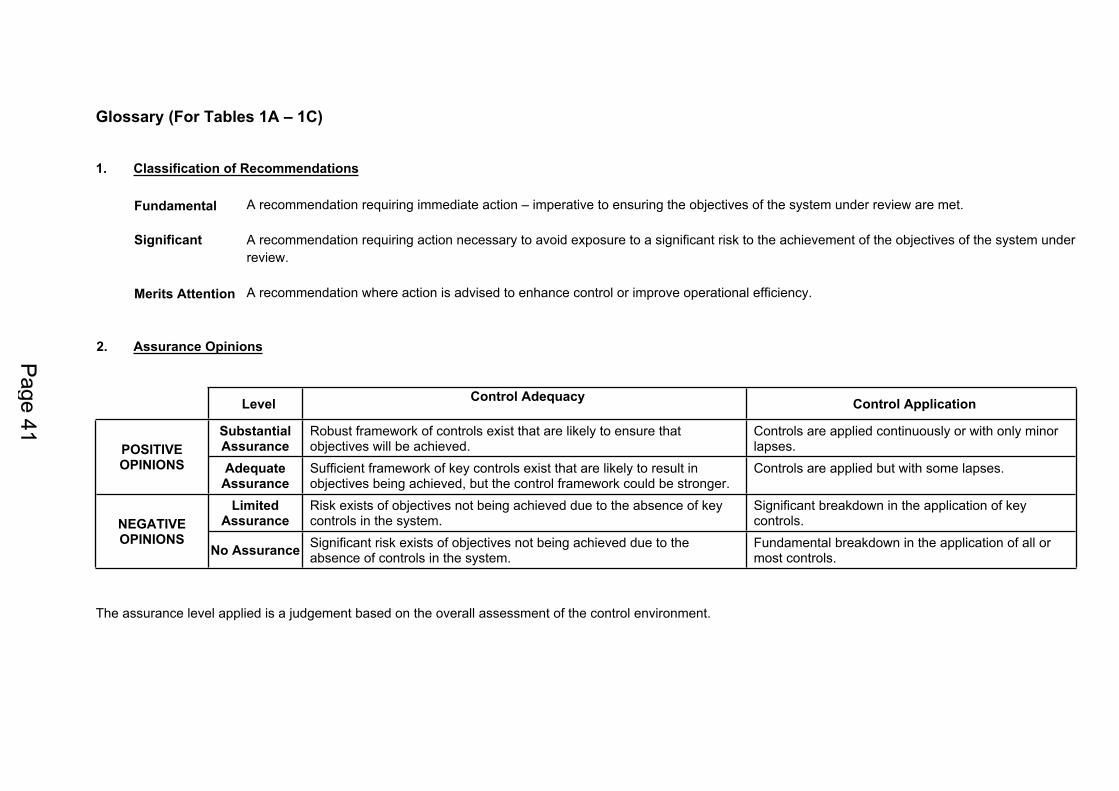

1.2 Assurance Opinion

The Assurance Opinion applied for each piece of work is selected from the following range:-

Substantial; } Positive assurance Adequate; } Positive assurance

Limited; } Negative assurance No Assurance. } Negative assurance

The Assurance Opinion is primarily driven by the number and priority level of the recommendations made / agreed. The priority level of recommendations is described either as Fundamental, Significant or Merits Attention.

The Assurance Opinion is also influenced by whether the recommendations are in respect of the adequacy (or existence) of controls or the application of existing controls.

The final factor influencing the overall opinion is in relation to the controls assessed and whether the result of that assessment regards the effectiveness of the control as Good, Adequate, Limited or Poor.

2. Implications

2.1 Financial

The charge for the Internal Audit service is estimated to be as planned and consequently there are no financial implications to consider.

2.2 Legal

There are no legal implications.

2.3 Risk Management

Management engagement and responses remain positive which helps support a positive assurance that where opportunities for control, risk or governance improvements are highlighted, these are embraced by management.

2.4 Equality, Diversity and Social Inclusion (Equality Act - Public Sector Equality Duty)

There are no implications.

3. Appendices/Annexes

3.1 The report attached at Appendix A includes:-

significant control or compliance issues; longstanding recommendations; a summary of the work completed and also work in progress since the previous

progress report; assurance opinions given and total recommendations made; recommendations followed-up by Internal Audit since the previous progress report; Internal Audit performance information.

REPORT AUTHOR Rob Winter CPFAPOST Head of Internal Audit and Corporate Anti-Fraud

Officer responsible Sharon Bradley CMIIAOrganisation Audit Manager (SCRCA)

Email [email protected] 01226 773187

Background papers used in the preparation of this report are available for inspection at: Barnsley MBC Westgate Plaza One office, Barnsley.

Other sources and references: Internal Audit Charter & Strategy 2016-17, Annual Plan 2016-17, Internal Audit Reports, MK Insight (audit management system), Public Sector Internal Audit Standards 2013.

APPENDIX AINTERNAL AUDIT PROGRESS REPORT

1. Annual Plan and Actual Comparison

The annual audit plan for 2016-17 was discussed and agreed in principle with the Executive Director, Section 151 Officer and Monitoring Officer. It was also reported to this Committee at the April 2016 meeting. The plan included a brief description of the work Internal Audit would undertake to support the SCRCA as it evolved during the year to design and embed its control, risk and governance framework arrangements. Each piece of work was to be more clearly defined and scoped as it commenced. In addition, the plan included compliance work to be undertaken by Internal Audit to provide Management and the Committee with assurances that the financial processes were operating effectively and efficiently. It was acknowledged by all parties that a higher number of days was required for 2016-17 (potentially circa. 120 days), to enable Internal Audit to support the SCRCA in establishing its governance framework.

At 31st March 2017, a total of 98 days have been delivered in relation to the planned work. This is time supporting management to develop and embed the governance framework and also the completion of six compliance reviews (fundamental financial systems 2015-16, skills capital grants, programme management and Sales Ledger 2016-17, Main Accounting 2016-17, Purchase Ledger 2016-17). Reviews of the SCRCA’s procurement arrangements and Payroll 2016-17 are currently being completed.

Due to the continued work in developing and implementing aspects of the SCRCA’s control and governance framework, much of the planned Internal Audit work was scheduled towards the end of the financial year. A further 17 days will actually be delivered early in the new audit year to complete the 2016/17 plan. The results of all the 2016/17 work will therefore be taken into account in the Annual Assurance Report to be considered by the Audit Committee in July.

2. Significant Control or Compliance issues to bring to the Audit Committee's Attention

No fundamental recommendations have been made within the completed pieces of work and therefore there are no specific control or compliance issues to bring to the Committee’s attention.

Of note for the Committee is the progress that management have made in the development and implementation of a range of governance related policies and procedures. Whilst not yet fully complete and embedded this is a marked improvement from the beginning of the year.

3. Longstanding Recommendations and Management Reponses

This section highlights to Members any recommendations that remain outstanding for 6 months or more following the original recommendation/agreed action target completion date and/or where the recommendation/agreed action target completion date has been subject to 3 revisions.

There are no longstanding recommendations to report at this time.

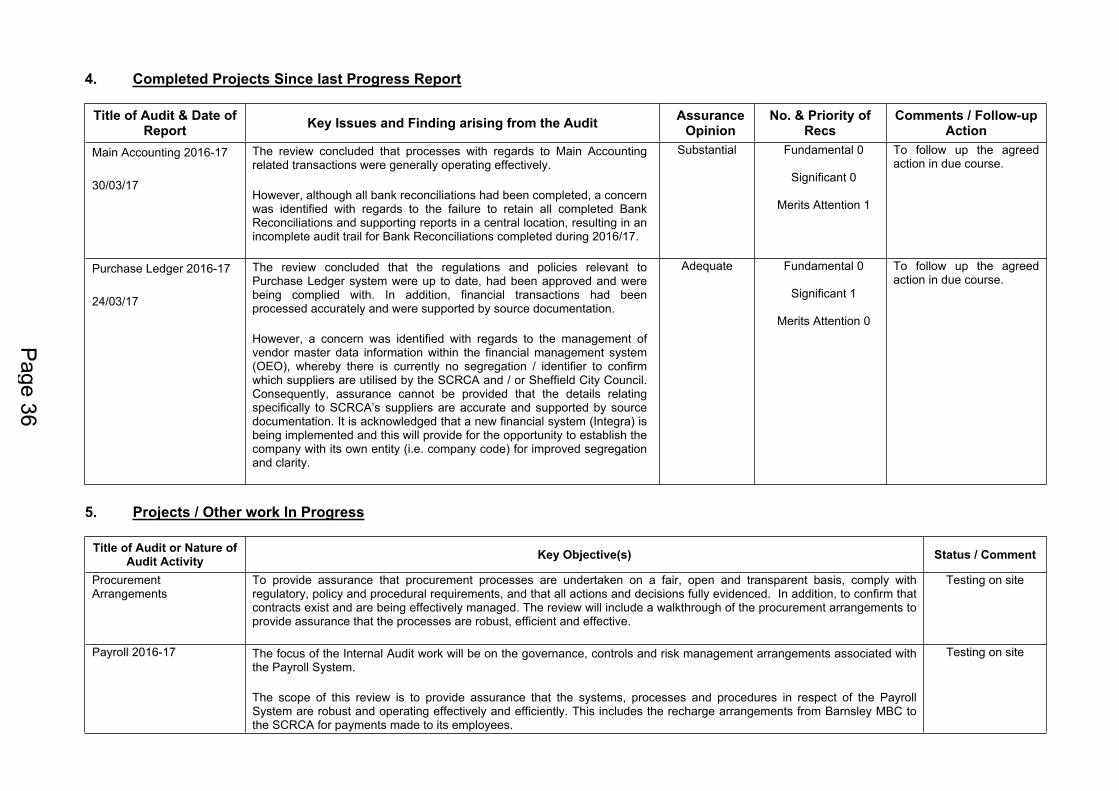

4. Completed Projects Since last Progress Report

Title of Audit & Date of Report Key Issues and Finding arising from the Audit Assurance

OpinionNo. & Priority of

RecsComments / Follow-up

ActionMain Accounting 2016-17

30/03/17

The review concluded that processes with regards to Main Accounting related transactions were generally operating effectively.

However, although all bank reconciliations had been completed, a concern was identified with regards to the failure to retain all completed Bank Reconciliations and supporting reports in a central location, resulting in an incomplete audit trail for Bank Reconciliations completed during 2016/17.

Substantial Fundamental 0

Significant 0

Merits Attention 1

To follow up the agreed action in due course.

Purchase Ledger 2016-17

24/03/17

The review concluded that the regulations and policies relevant to Purchase Ledger system were up to date, had been approved and were being complied with. In addition, financial transactions had been processed accurately and were supported by source documentation.

However, a concern was identified with regards to the management of vendor master data information within the financial management system (OEO), whereby there is currently no segregation / identifier to confirm which suppliers are utilised by the SCRCA and / or Sheffield City Council. Consequently, assurance cannot be provided that the details relating specifically to SCRCA’s suppliers are accurate and supported by source documentation. It is acknowledged that a new financial system (Integra) is being implemented and this will provide for the opportunity to establish the company with its own entity (i.e. company code) for improved segregation and clarity.

Adequate Fundamental 0

Significant 1

Merits Attention 0

To follow up the agreed action in due course.

5. Projects / Other work In Progress

Title of Audit or Nature of Audit Activity Key Objective(s) Status / Comment

Procurement Arrangements

To provide assurance that procurement processes are undertaken on a fair, open and transparent basis, comply with regulatory, policy and procedural requirements, and that all actions and decisions fully evidenced. In addition, to confirm that contracts exist and are being effectively managed. The review will include a walkthrough of the procurement arrangements to provide assurance that the processes are robust, efficient and effective.

Testing on site

Payroll 2016-17 The focus of the Internal Audit work will be on the governance, controls and risk management arrangements associated with the Payroll System.

The scope of this review is to provide assurance that the systems, processes and procedures in respect of the Payroll System are robust and operating effectively and efficiently. This includes the recharge arrangements from Barnsley MBC to the SCRCA for payments made to its employees.

Testing on site

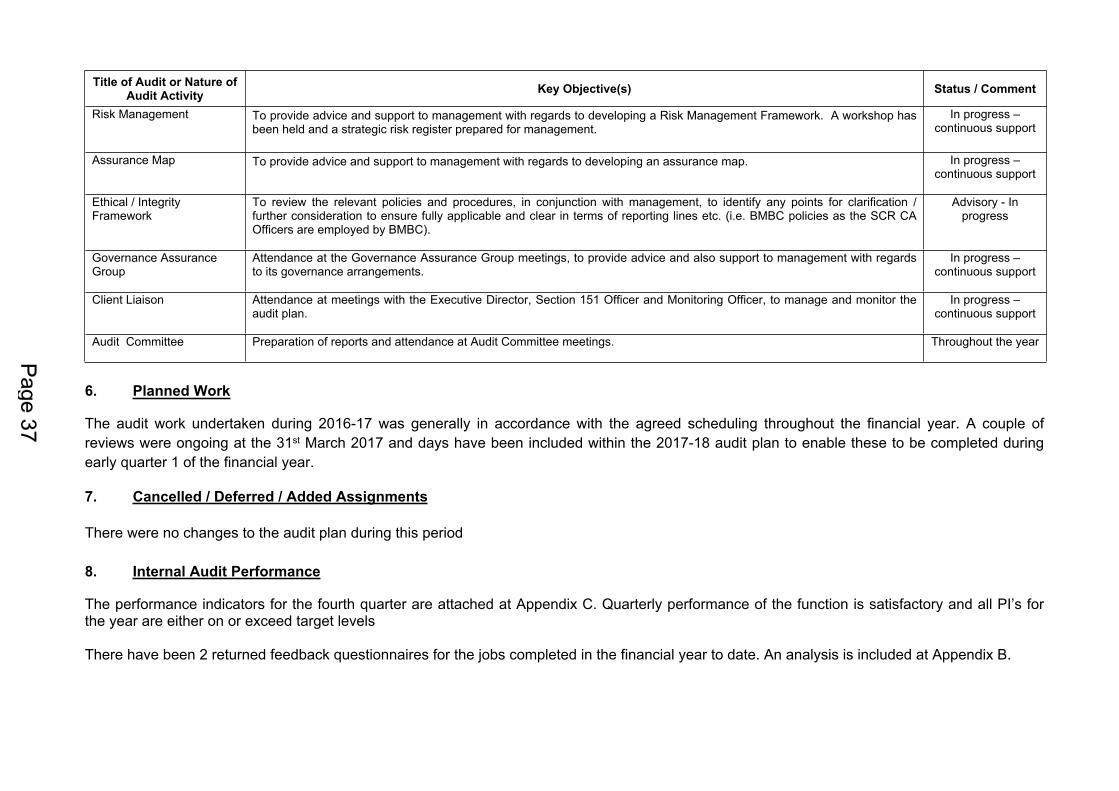

Title of Audit or Nature of Audit Activity Key Objective(s) Status / Comment

Risk Management To provide advice and support to management with regards to developing a Risk Management Framework. A workshop has been held and a strategic risk register prepared for management.

In progress – continuous support

Assurance Map To provide advice and support to management with regards to developing an assurance map. In progress – continuous support

Ethical / Integrity Framework

To review the relevant policies and procedures, in conjunction with management, to identify any points for clarification / further consideration to ensure fully applicable and clear in terms of reporting lines etc. (i.e. BMBC policies as the SCR CA Officers are employed by BMBC).

Advisory - In progress

Governance Assurance Group

Attendance at the Governance Assurance Group meetings, to provide advice and also support to management with regards to its governance arrangements.

In progress – continuous support

Client Liaison Attendance at meetings with the Executive Director, Section 151 Officer and Monitoring Officer, to manage and monitor the audit plan.

In progress – continuous support

Audit Committee Preparation of reports and attendance at Audit Committee meetings. Throughout the year

6. Planned Work

The audit work undertaken during 2016-17 was generally in accordance with the agreed scheduling throughout the financial year. A couple of reviews were ongoing at the 31st March 2017 and days have been included within the 2017-18 audit plan to enable these to be completed during early quarter 1 of the financial year.

7. Cancelled / Deferred / Added Assignments

There were no changes to the audit plan during this period

8. Internal Audit Performance

The performance indicators for the fourth quarter are attached at Appendix C. Quarterly performance of the function is satisfactory and all PI’s for the year are either on or exceed target levels

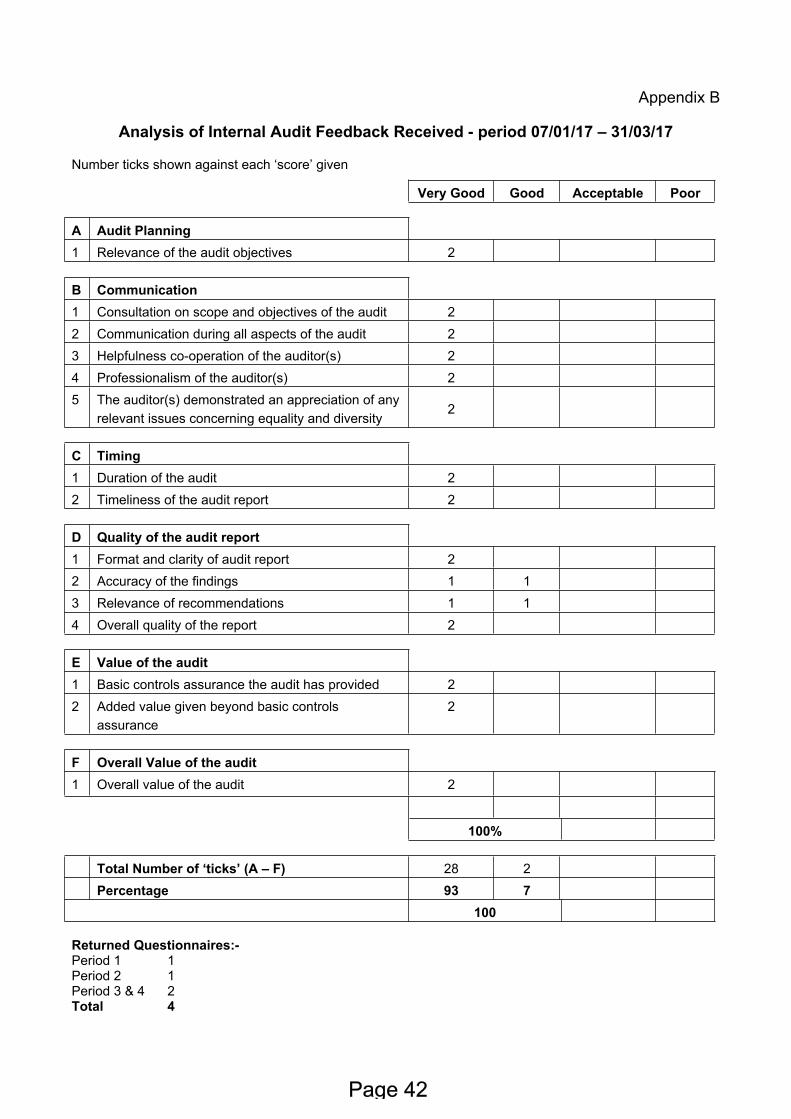

There have been 2 returned feedback questionnaires for the jobs completed in the financial year to date. An analysis is included at Appendix B.

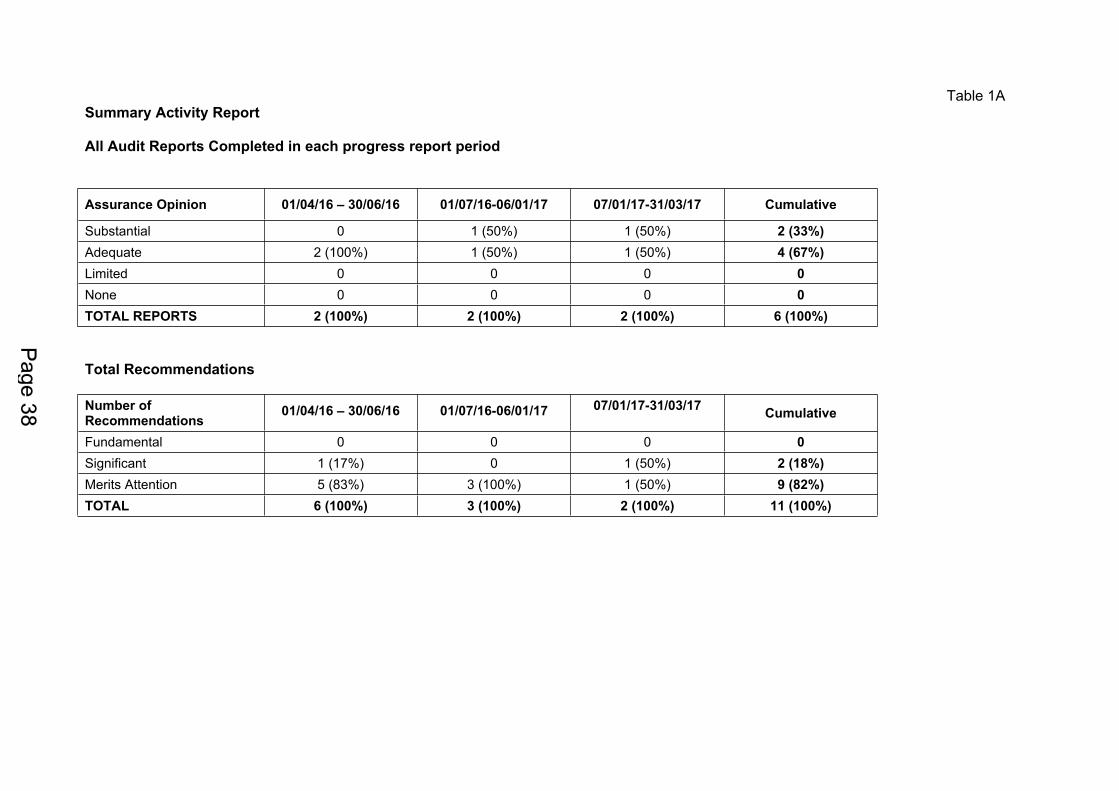

Table 1ASummary Activity Report

All Audit Reports Completed in each progress report period

Assurance Opinion 01/04/16 – 30/06/16 01/07/16-06/01/17 07/01/17-31/03/17 Cumulative

Substantial 0 1 (50%) 1 (50%) 2 (33%)Adequate 2 (100%) 1 (50%) 1 (50%) 4 (67%)Limited 0 0 0 0None 0 0 0 0TOTAL REPORTS 2 (100%) 2 (100%) 2 (100%) 6 (100%)

Total Recommendations

Number of Recommendations

01/04/16 – 30/06/16 01/07/16-06/01/17 07/01/17-31/03/17 Cumulative

Fundamental 0 0 0 0Significant 1 (17%) 0 1 (50%) 2 (18%)Merits Attention 5 (83%) 3 (100%) 1 (50%) 9 (82%)TOTAL 6 (100%) 3 (100%) 2 (100%) 11 (100%)

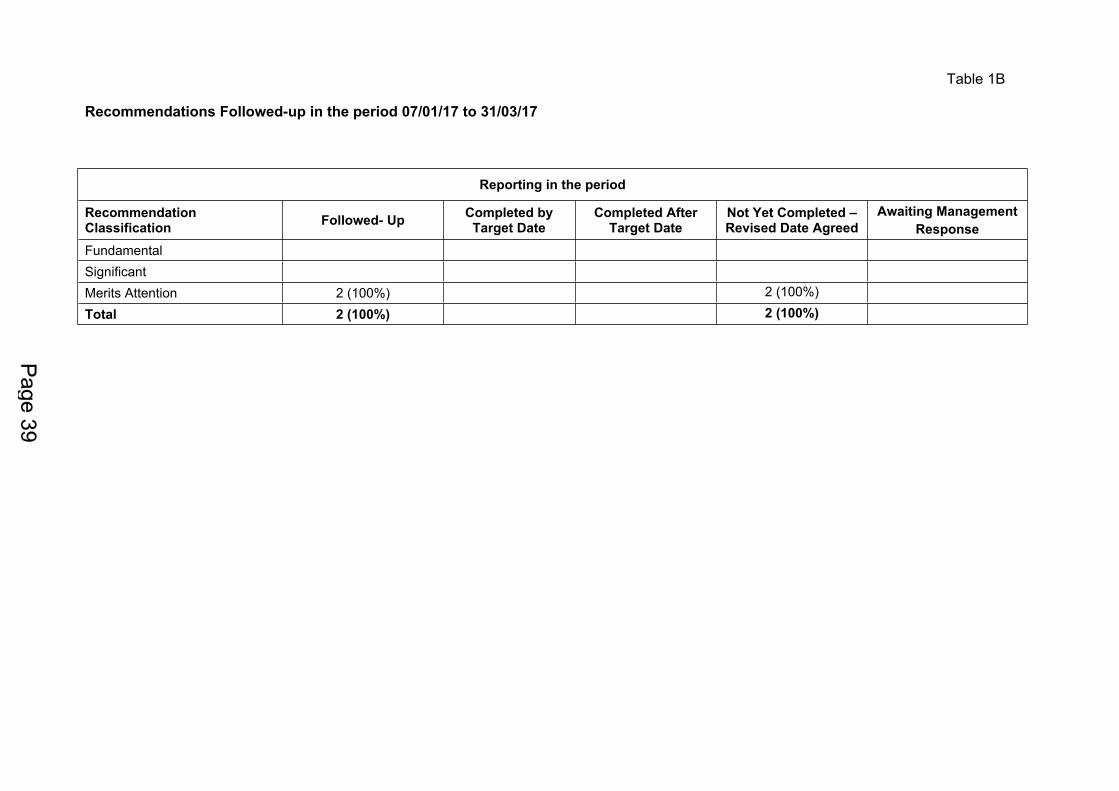

Table 1B

Recommendations Followed-up in the period 07/01/17 to 31/03/17

Reporting in the period

Recommendation Classification Followed- Up Completed by

Target DateCompleted After

Target DateNot Yet Completed – Revised Date Agreed

Awaiting ManagementResponse

FundamentalSignificantMerits Attention 2 (100%) 2 (100%)

Total 2 (100%) 2 (100%)

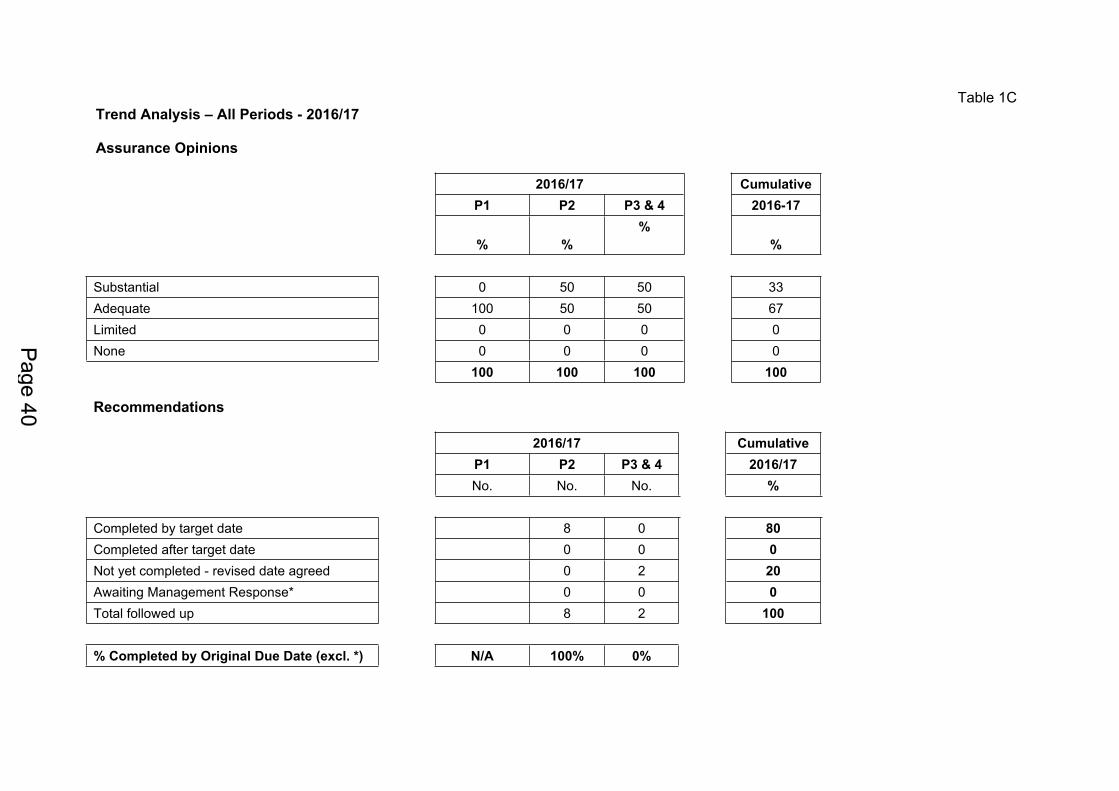

Table 1CTrend Analysis – All Periods - 2016/17

Assurance Opinions

2016/17 CumulativeP1 P2 P3 & 4 2016-17

% %%

%

Substantial 0 50 50 33Adequate 100 50 50 67Limited 0 0 0 0None 0 0 0 0

100 100 100 100

Recommendations

2016/17 CumulativeP1 P2 P3 & 4 2016/17No. No. No. %

Completed by target date 8 0 80Completed after target date 0 0 0Not yet completed - revised date agreed 0 2 20Awaiting Management Response* 0 0 0Total followed up 8 2 100

% Completed by Original Due Date (excl. *) N/A 100% 0%

Glossary (For Tables 1A – 1C)

1. Classification of Recommendations

Fundamental A recommendation requiring immediate action – imperative to ensuring the objectives of the system under review are met.

Significant A recommendation requiring action necessary to avoid exposure to a significant risk to the achievement of the objectives of the system under review.

Merits Attention A recommendation where action is advised to enhance control or improve operational efficiency.

2. Assurance Opinions

Level Control Adequacy Control Application

Substantial Assurance

Robust framework of controls exist that are likely to ensure that objectives will be achieved.

Controls are applied continuously or with only minor lapses.POSITIVE

OPINIONS Adequate Assurance

Sufficient framework of key controls exist that are likely to result in objectives being achieved, but the control framework could be stronger.

Controls are applied but with some lapses.

Limited Assurance

Risk exists of objectives not being achieved due to the absence of key controls in the system.

Significant breakdown in the application of key controls.NEGATIVE

OPINIONSNo Assurance Significant risk exists of objectives not being achieved due to the

absence of controls in the system.Fundamental breakdown in the application of all or most controls.

The assurance level applied is a judgement based on the overall assessment of the control environment.

Appendix B

Analysis of Internal Audit Feedback Received - period 07/01/17 – 31/03/17

Number ticks shown against each ‘score’ given

Very Good Good Acceptable Poor

A Audit Planning1 Relevance of the audit objectives 2

B Communication1 Consultation on scope and objectives of the audit 22 Communication during all aspects of the audit 23 Helpfulness co-operation of the auditor(s) 24 Professionalism of the auditor(s) 25 The auditor(s) demonstrated an appreciation of any

relevant issues concerning equality and diversity2

C Timing1 Duration of the audit 22 Timeliness of the audit report 2

D Quality of the audit report1 Format and clarity of audit report 22 Accuracy of the findings 1 13 Relevance of recommendations 1 14 Overall quality of the report 2

E Value of the audit1 Basic controls assurance the audit has provided 22 Added value given beyond basic controls

assurance2

F Overall Value of the audit1 Overall value of the audit 2

100%

Total Number of ‘ticks’ (A – F) 28 2Percentage 93 7

100

Returned Questionnaires:-Period 1 1Period 2 1Period 3 & 4 2Total 4

Appendix C

Ref. Indicator Frequency of Report

Target 2016/17

This Period

Year to Date

1.

1.1

2.

2.1

2.2

2.3

3.

3.1

Customer Perspective:

Percentage of questionnaire received noted “good” or “very good” relating to work concluding with an audit report. * Business Process Perspective:

Percentage of final audit reports issued within 10 working days of completion and agreement of the draft audit report. *

Percentage of chargeable time against total available.

Average number of days lost through sickness per FTE (Cumulative 45 days in total)

Continuous Improvement Perspective:

Personal development plans for staff completed within the prescribed timetable.

Quarterly

Quarterly

Quarterly

Quarterly

Annual

95%

80%

73%

6 days

100%

100%

100%

72%

1 day

100%

100%

100%

73%

<3 days

100%

* KPIs relate specifically to the SCRCA.

INTERNAL AUDIT PERFORMANCE INDICATORS FOR 2016/17 (QUARTER 4)

External Audit Plan 2016/2017

Sheffield City Region Combined Authority

April 2017

1

Document Classification: KPMG Confidential

© 2017 KPMG LLP, a UK limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a