notice of the annual general meeting - medipos

TRANSCRIPT

Summarised Financial Statements as at 31 December 2017

Notice of the Annual General Meeting to be held on 26 June 2018

MEDiPOS MEDICAL SCHEME

Notice to all membersNOTICE IS HEREBY GIVEN THAT THE ANNUAL GENERAL MEETING OF MEDiPOS MEDICAL SCHEME WILL BE HELD AT THE NATIONAL POST CENTRE, NCC, GROUND FLOOR, 497 SCHUBART STREET, PRETORIA ON TUESDAY, 26 JUNE 2018 AT 11:00.

AGENDA

1. Welcome and apologies

2. ConfirmationofminutesTo confirm the minutes of the MEDiPOS Medical Scheme Annual General Meeting (AGM) held on 27 June 2017.

3. AdoptionofreportandaccountsTo receive and adopt the report of the Board of Trustees, as well as the auditor`s report and summarised financial statements for the year ended 31 December 2017.

4. AppointmentofauditorsTo appoint the auditors for the 2018 financial year.

5. AnyotherbusinessTo transact other business as may, in terms of the rules, be transacted at an AGM.

Pleasenote: Notice of any motion to be placed before the AGM must reach the Principal Officer not later than seven days prior to the date of the meeting.

By order of the Board of Trustees

FRANCINA MOSOEUPRINCIPAL OFFICER

Notice to all members

2 3

MEDiPOS MEDICAL SCHEME MEDiPOS MEDICAL SCHEME Minutes of the Annual General Meeting

The Chairperson commented on the following:

ff The Scheme continues with its commitment to providing its members with appropriate healthcare funding without compromising on the quality of care or services in the current circumstances. The Board of Trustees continues to steer the Scheme through sound ethical governance processes to ensure the pursuit of service excellence in the provision of medical cover for members of the Scheme.

ff There are various sub-committees that add further impetus to the Scheme’s best practice governance principles.

These include:ff ffAudit and Risk Committee;ff ffInvestment Committee;ff ffClinical Committee; andff ffMarketing Committee.ffff The individuals participating in these committees provide expert insight and guidance on

the activities of the Scheme, while maintaining the best interests of the members.ff The Scheme employs the services of independent experts for independent advice and

review of the Scheme’s performance.ff MEDiPOS ended the 2016 financial year in a sound financial position despite ongoing

industry challenges affecting most medical schemes. However, as at 31 December 2016, all three options were in a net healthcare deficit position with the total healthcare deficit amounting to R47 103 875 compared to R29 816 625 in 2015. This represents 9.9% (2016: 6.63%) of the aggregated contributions of the Scheme. The Trustees have noted the net healthcare deficit and will continue to monitor the performance of the Scheme, while making appropriate interventions during the annual benefit review process.

ff The Scheme’s solvency ratio as at 31 December 2016 was 111.9% compared with the statutory minimum requirement of 25%, despite the fact that the Scheme has been reflecting an operational deficit since 2014.

ff Trustees are keeping abreast of external market developments and the pending National Health Insurance, allowing us to proactively plan for any impact on the Scheme.

ff Membership on the Scheme increased by 5.5% over the period January to December 2016. The total number of members as at the end of December 2016 was 13 056 compared to 12 370 at the end of December 2015. The average age of beneficiaries remained constant at 36 years, while the pensioner ratio decreased from 12% to 11%.

ff The Board of Trustees approved contribution increases for 2016 at 11.95% across all three options. This was necessary in order to continue providing members with better value for money and ensuring that the Scheme remains sustainable in the long term. No changes were made to the benefit sub-limits, however the Scheme introduced a pharmacy network and an in-lieu-of-hospitalisation benefit.

Minutes of the Annual General Meeting

Minutes of the Annual General Meeting MINUTES OF THE ANNUAL GENERAL MEETING HELD ON TUESDAY, 27 JUNE 2017 AT 10:00 AT THE NCC, BLOCK C, GROUND FLOOR, 350 WITCH HAZEL AVENUE, ECO POINT, CENTURION, PRETORIA

PRESENT:

191 members represented in person, 1 034 valid proxies received, Trustees and representatives from MMI Health and Willis Towers Watson

APOLOGIES:

None

1. WELCOME AND APOLOGIES

The Chairperson opened the meeting and welcomed those present. A special word of welcome was directed to the members of the Board of Trustees and representatives from MMI Health and Willis Towers Watson. There being a quorum present, the Chairperson confirmed that the meeting was duly constituted.

The Chairperson advised members that the Principal Officer received a total of 1 034 valid proxies from members who were not able to attend in person, and who will be recorded as being represented by proxy.

2. MINUTES OF THE PREVIOUS ANNUAL GENERAL MEETING (AGM) HELD ON 23 JUNE 2016

The minutes of the previous Annual General Meeting held on 23 June 2016, having been circulated, was taken as read and unanimously adopted.

3. ADOPTION OF REPORT AND ACCOUNTS

The report of the Board of Trustees, the report of the external auditors and summarised annual financial statements for the year ending 31 December 2016, having been circulated, was taken as read and adopted.

3. ADOPTION OF REPORT AND ACCOUNTS (continued)

4 5

MEDiPOS MEDICAL SCHEME MEDiPOS MEDICAL SCHEME

6. REMUNERATION OF TRUSTEES

The Board of Trustees proposed the remuneration of member-elected and employer-appointed Trustees effective 1 July 2017. The proposal was made during the Board’s annual review of Trustee remuneration and an increase equal to the consumer price index (CPI) (6%) as at the end of March 2017, was recommended.

The proposal to increase the Trustee remuneration fee by 6% was approved by the members of the Scheme.

7. GENERAL

The Chairperson allowed members the opportunity to raise any general issues, as well as any wish-list benefit enhancements for 2018 they wished the Board to consider:

7.1 A member requested that the Scheme consider reinstating the post-medical retirement benefit, which was offered to staff on retirement from SAPO. The Chairperson informed members that this benefit was discontinued in 2005, as it formed part of the Sunset clause to cover the retirees from the previous regime. This was a subsidised benefit offered by SAPO and does not form part of the Scheme’s benefits. The Board of Trustees undertook to raise this matter with the employer and to provide its members with feedback.

7.2 Following a request made at the 2016 AGM, a member enquired whether the Scheme would consider allowing day-to-day benefits to be carried over on a year-to-year basis. The Chairperson explained to the members the essence of how a medical scheme works and how cross-subsidisation ensures the sustainability of the Scheme. It was agreed that this request would be added to the 2018 benefit wish-list and considered by the Benefit Review Committee.

7.3 A member raised an enquiry as to the reasons why the Scheme does not want to cover the patented chronic medication prescribed for her dependant. Her son had a severe reaction to the generic medication and the member ended up having to cover the cost of the required medication. In addition, the member enquired why the Scheme does not cover malaria medication, as there is currently an outbreak in the greater Pretoria area. The Board advised the member that there is an exception management process, whereby the treating doctor could provide a clinical motivation to the Scheme for consideration of the patent medication. The member was advised that individual enquiries may be raised with the Principal Officer.

4. APPOINTMENT OF THE EXTERNAL AUDITORS

The Chairperson advised that the Board of Trustees recommended the appointment of KPMG Inc. as the external auditors to the Scheme for the financial year ending 31 December 2017. The proposal was adopted by the members of the Scheme.

In addition, the Board would be undertaking a formal procurement process prior to the appointment of an external auditor for the 2018 financial year.

5. ELECTION OF MEMBERS OF THE BOARD OF TRUSTEES

The election of five (5) member-elected Trustees was duly conducted as per the rules of the Scheme. The five (5) member-elected members of the Board of Trustees are to be elected at every third AGM of the Scheme from amongst duly nominated members.

Valid nominations were received in respect of the following members:ff Mr Bernard Blume;ff Mr Jurie Swart;ff Mr Jurie Kemp;ff Mr David Galloway;ff Mr Mohandas Naidoo;ff Mr Vincent Nair;ff Mr Robert Serage;

ff Mr Kgabo Mokgohloa;ff Mr Bongani Masondo;ff Mr Poobalan Thaver;ff Mr Mlungisi Nkunzi; ff Ms Nombulelo Ngubane;ff Ms Babueledi Thabane; andff Dr Maureen Mpata.

The Chairperson informed members that in future, election ballot forms would be accompanied by a picture, brief biography and manifesto of the candidates. A member of the South African Post Office’s (SAPO) Internal Audit Department explained and facilitated the voting process. Each member received a valid ballot paper listing the nominees and was requested to vote for five (5) Trustee members. As the voting process was quite extensive and time-consuming, the Chairperson proposed that the meeting continue and that the results of the voting were circulated to all members once finalised.

The Chairperson took the opportunity on behalf of the Scheme to thank the outgoing Trustees for their contribution to the Board of Trustees over the past three (3) years and wished them well in their future endeavours. In addition, the Chairperson thanked the members of the various sub-committees for assisting Trustees in carrying out their duties. The Board of Trustees thanked the Principal Officer and the Scheme’s investment consultants, administrator, auditors and actuaries for their diligent work during the past year.

Minutes of the Annual General Meeting Minutes of the Annual General Meeting

6 7

MEDiPOS MEDICAL SCHEME MEDiPOS MEDICAL SCHEME

8. OTHER BUSINESS

The Chairperson noted that the Principal Officer had not been notified of any other formal business, as is required by the rules of the Scheme.

9. CLOSING

There being no further questions from the floor and no further business for discussion, the Chairperson thanked the members for their continued support to the Scheme and attendance and declared the meeting closed.

Approvedandsignedonthis___________dayof___________________________________

CHAIRPERSON

7. GENERAL (continued)

7.4 A member requested feedback from the Board on the request raised at the 2016 AGM and captured under item 6.6 of the minutes. The Chairperson informed the member that the request for coverage of hearing aid batteries were considered and debated as part of the 2017 benefit review. It was decided that the longevity of the battery should be of a length that the replacement cost should not be that onerous. It was also determined that some practitioners are taking advantage of members by offering services that is not required, and in order to protect the interest of members, the Scheme decided not to cover this benefit.

The member also raised the question as to why glucose strips are not covered under chronic medication for diabetes. The Chairperson advised that the Board would investigate and provide the member with feedback.

7.5 A member enquired what the contribution increases are based on annually and how the Board arrives at the percentage. The Chairperson informed the member that the Board considered a number of factors when determining contribution increases for the following financial year. Medical inflation is generally 5% higher than the normal CPI and it is unknown what the Schemes claims would be over the coming year. A substantial amount of fraud is also taking place within the medical scheme industry, which is depleting the Scheme’s reserves and affects the annual increase in member contributions. Members were also encouraged to actively engage with their doctors on the necessity of services rendered, tests done and hospital admissions.

7.6 A member enquired on how the Scheme determines chronic conditions, as she has an ongoing problem obtaining chronic authorisation for her medication. The Principal Officer informed the member that the Scheme contracts with a managed care organisation that ensures that the Scheme complies with the legislated requirements specific to prescribed minimum benefits (PMBs) and the chronic disease list (CDL). The member was encouraged to raise her individual matter with the Principal Officer.

7.7 A member enquired if healthcare service providers have access to the Scheme’s website in order to determine if medication is covered by the Scheme. The Chairperson encouraged members to request their pharmacists to recommend alternative medication should a particular medication be excluded.

Minutes of the Annual General MeetingMinutes of the Annual General Meeting

9

MEDiPOS MEDICAL SCHEME

8

MEDiPOS MEDICAL SCHEME

As Chairperson of the Board of Trustees of MEDiPOS Medical Scheme, I have pleasure in presenting the Board’s report for the year ended 31 December 2017.

The Scheme continued with its commitment to providing its members with appropriate healthcare funding, without compromising on the quality of care or services. The Board continued to steer the Scheme through sound, ethical governance processes to ensure the pursuit of service excellence in the provision of medical cover for members of the Scheme.

There are various sub-committees that add further impetus to the Scheme’s best practice governance principles. These include the Audit and Risk Committee, the Investment Committee, the Clinical Risk Committee, the Marketing Committee, the Operations Committee and the Ex Gratia Committee. The individuals participating in these committees provide expert insight and guidance on the activities of the Scheme, while upholding the best interests of the members.

The Scheme also employs the services of independent experts for independent advice and review of the Scheme’s performance.

Financial performanceMEDiPOS ended the 2017 financial year in a sound financial position, despite ongoing industry challenges affecting most medical schemes.

Due to the financial position of the South African Post Office (SAPO), contributions have not always been received after three days of it becoming due. The Board of Trustees (BOT) has prioritised this matter and informed the employer of its fiduciary responsibilities to act and to request a payment plan for the receipt of future contributions in terms of the Act.

The Trustees agreed that disinvestments would be made from the Scheme’s investments as and when necessary, in order to bridge any cash flow shortfall that may arise so that members and service providers are not unduly negatively impacted. The Trustees continue to proactively engage with SAPO regarding the payment of contributions.

As at 31 December 2017, all three options reflected a net healthcare deficit. The total healthcare deficit amounted to R43 502 640, representing 7.93% of the aggregated contributions of the Scheme. The Trustees have noted the net healthcare deficits and will continue to monitor the performance of the Scheme while making appropriate interventions during the annual benefit review process.

The Scheme’s solvency ratio (i.e. accumulated funds as a percentage of total contributions) as at 31 December 2017 was 95.70% compared with the statutory minimum of 25%.

Chairperson’s Report

Chairperson’s Report

Financial performance (continued)The Trustees are also keeping abreast of external market developments and the pending National Health Insurance scheme, allowing us to proactively plan for any impact on the Scheme.

MembershipMembership increased by 4.8% during the period under review from 13 056 at the end ofDecember 2016 to 13 683 at the end of December 2017. The average age of beneficiaries remains at 36 and the pensioner ratio at 11% over the same period.

Contribution increases and benefit changesThe Board approved contribution increases for 2017 at a rate that is close to inflation, combined with conservative benefit improvements. This was done to continue providing members with better value for money and to ensure that the Scheme remains sustainable in the long term.

The contribution increase for 2017 was 11.95% across all three options (Option A, Option B and Option C). No changes were made to the benefit sub-limits but the Scheme introduced a pharmacy network and an in-lieu-of-hospitalisation benefit.

Personal Medical Spending Accounts (PMSAs)The Board of Trustees approved the discontinuation of the PMSA with effect from 1 January 2013.

Any amounts owing to members due to unsuccessful savings payouts were invested in a separate call account with Standard Bank at a rate of 6.25% per annum.

Following the Constitutional Court ruling in favour of the Genesis Medical Scheme, the Council for Medical Schemes issued Circular 56 of 2017, confirming that savings account liabilities do not need to be treated separately or differently from any other liabilities of a medical scheme, and that the medical scheme is the holder of the funds. At a meeting of the Board of Trustees held on 23 November 2017, the Trustees resolved to apply the prescription rule and the unpaid balances were subsequently written back to income. Vote of appreciationI would like to express my thanks to my fellow Trustees, the members of the various sub-committees of the Board of Trustees, the Principal Officer, Ms Mosoeu, her assistant, Ms Masilela, the Scheme`s investment managers and consultants, the actuaries, the auditors, the Administrator, managed care organisations, the other Scheme`s service providers and you, our members, for your support during the past year.

Chairperson’s Report (continued)

Chairperson’s Report

10 11

MEDiPOS MEDICAL SCHEME MEDiPOS MEDICAL SCHEME

ConclusionThe Board is confident that the Scheme will continue to provide its members with excellent and affordable healthcare cover and encourages you and your dependants to continue to manage your benefits responsibly.

The Board expresses its appreciation to all members for their contribution and ongoing active participation in the Scheme. We look forward to yet another successful year for the Scheme in which our members and their dependants will enjoy good health.

ANDREW NONGOGOCHAIRPERSON

Chairperson’s Report (continued)

Chairperson’s Report

Contents

Report of the Board of Trustees 12-30Independent auditor’s report 31-32Summarised statement of financial position 33Summarised statement of comprehensive income 34Summarised statement of changes in funds and reserves 35Summarised statement of cash flows 36Notes to the summarised financial statements 37-62

Summarised financial statements

for the year ended 31 December 2017

Registration number: 01548

The reports and statements set out below comprise the summarised financial statements presented to the members:

12 13

Report of the Board of Trustees Report of the Board of TrusteesMEDiPOS MEDICAL SCHEME MEDiPOS MEDICAL SCHEME

Report of the Board of TrusteesThe Board of Trustees hereby presents its report for the year ended 31 December 2017.

The summarised financial statements have been extracted from the audited financial statements approved by the Board of Trustees on 19 April 2018.

Registrationnumber:01548

1. MANAGEMENT

1.1 BoardofTrustees(BOT)

The names of the Trustees in office during the year under review and up to the date of signing this report are:

Employerappointed M Mpata Chairperson (resigned 30 April 2017) A Nongogo Acting Chairperson (effective from 1 May 2017) K Rapoo M Mlauzi (resigned 15 February 2017) C Mofokeng (resigned 25 January 2017)

Memberelected M Mpata (elected 27 June 2017) B Blume (term of office expired 27 June 2017) J Swart (term of office expired 27 June 2017) R Serage (re-elected 27 June 2017) D Galloway (re-elected 27 June 2017) V Nair (term of office expired 27 June 2017) K Mokgohloa (elected 27 June 2017) B Thabane (elected 27 June 2017)

1.2 PrincipalOfficer

MFMosoeu South African Post Office State-owned Company Ltd Block A PO Box 2087 Eco Point Building Corporate Shop 350 Witch Hazel Avenue 0074Eco Park Centurion0157

1.3 Registeredofficeaddressandpostaladdress

SouthAfricanPostOfficeState-ownedCompanyLimitedBlock A PO Box 2087Eco Point Building Corporate Shop350 Witch Hazel Avenue 0074Eco ParkCenturion0157

1.4 Medicalschemeadministrator

MMIHealth(Pty)Ltd268 West Avenue P O Box 7400

Centurion Centurion Gauteng 0046 0157 Accreditation no. 13 1.5 Investmentmanagers

CoronationFundManagers(Proprietary)Limited7th Floor PO Box 44684MontClare Place ClaremontCnr Campground and Main Road 7735Claremont7735

Financial service provider number: 548

PrescientInvestmentManagement(Proprietary)LimitedPrescient House PO Box 31142The Terraces TokaiSteenberg Boulevard 7966Steenberg Office Park7966

Financial service provider number: 612

1. MANAGEMENT (continued)

14 15

Report of the Board of Trustees Report of the Board of TrusteesMEDiPOS MEDICAL SCHEME MEDiPOS MEDICAL SCHEME

1.5 Investmentmanagers(continued)

NedgroupInvestments(Proprietary)Limited Nedbank Clocktower PO Box 1510Clocktower Precinct Cape TownV&A Waterfront 8000Cape Town 8001

1.6 Auditor

KPMG Inc KPMG Crescent Private Bag 985 Empire Road ParkviewParktown 21222193

1.7 Actuarialconsultants

WillisTowersWatson(Proprietary)LimitedMontclare Place Private Bag X3023 Main Road Rondebosch Level 4 7700 Cape Town 7701

1.8 Managedcareservicesprovider

MetropolitanHealthRiskManagement(Proprietary)LimitedParc du Cap PO Box 4313Mispel Road Cape TownBellville 80007530

1.9 OncologyNetwork

IndependentClinicalOncologyNetwork(Proprietary)Limited(ICON)14 Mispel Road PO Box 15811Bellville Panorama7530 7500

1. MANAGEMENT (continued) 2. DESCRIPTION OF THE MEDICAL SCHEME

The Scheme is a not-for-profit, closed medical scheme, registered in terms of the Medical Schemes Act 131 of 1998, as amended (the Act).

2.1 Benefits

The Scheme offers three benefit options to employees and retirees of the participating employer in the Scheme. These are:

ff MEDiPOS Option A;ff MEDiPOS Option B; andff MEDiPOS Option C.

2.2 Savingsplan

The Board of Trustees approved the discontinuation of personal medical savings accounts effective 1 January 2013. The unpaid balance of R2 379 369 (2016: R2 296 727) in respect of stale cheques for savings payouts was invested in a separate call account with Standard Bank at a rate of 6.25% (2016: 6.5%) per annum.

Following the Constitutional Court ruling in favour of the Genesis Medical Scheme, the Council for Medical Schemes issued Circular 56 of 2017 confirming that savings account liabilities do not need to be treated separately or differently from any other liabilities of a scheme, and that the Scheme is the holder of the funds.

At a meeting of the Board of Trustees held on 23 November 2017, the Trustees resolved to apply the prescription rule and the unpaid balances were subsequently written back to income.

3. INVESTMENT STRATEGY OF THE MEDICAL SCHEME

The Scheme’s investment strategy is to maximise the return on its investments on a long- term basis at minimum risk. The investment strategy takes into consideration constraints both imposed by legislation and by the BOT. The strategy is reviewed annually, taking into consideration compliance with the Act, the risk returns of the various investment instruments and surplus funds available.

16 17

Report of the Board of Trustees Report of the Board of TrusteesMEDiPOS MEDICAL SCHEME MEDiPOS MEDICAL SCHEME

The Scheme’s Investment Committee, which comprises Trustees and independent members, meet regularly to consider the Scheme’s investment strategy and to monitor investment performance and compliance. The committee’s recommendations are considered and approved by the BOT.

The Investment Committee is responsible for all the investment decisions and part of its strategy is to ensure that:ff the Scheme remains liquid;ff investments are placed at minimum risk at the best possible rate of return;ff investments are made in compliance with the Regulations of the Act;ff a risk assessment is performed with feedback to the BOT with recommendations on the

risks identified; and ff investing activities are only conducted with approved financial institutions.

The Scheme invested in bonds, equities, and cash instruments during 2017. This policy is reviewed annually, taking into consideration compliance with the Act, the risk and returns of the various investment instruments and surplus funds available. Realised gains are reflected in the summarised statement of comprehensive income.

4. MANAGEMENT OF INSURANCE RISK

The primary insurance activity carried out by the Scheme assumes the risk of loss from members and their dependants that are directly subject to the risk. These risks relate to the health of Scheme members. As such, the Scheme is exposed to the uncertainty surrounding the timing and severity of claims under the contract. The Scheme also has exposure to market risk through its insurance and investment activities.

The Scheme manages its insurance risk through benefit limits and sub-limits, approval procedures for transactions that involve pricing guidelines, pre-authorisation, case management and service provider profiling. These methods for mitigating insurance risk are reviewed annually and amended for changes in the Act, as amended and/or changes in the Scheme’s ability to accept insurance risk.

Experience shows that the larger the portfolio of similar insurance contracts, the smaller the relative variability about the expected outcome will be. In addition, a more diversified portfolio is less likely to be affected across the board by a change in any subset of the portfolio. The Scheme has developed its insurance underwriting strategy to diversify the type of insurance risks accepted and within each of these categories of risk to achieve a sufficiently large population of risks to reduce the variability of the expected outcome.

3. INVESTMENT STRATEGY OF THE MEDICAL SCHEME (continued)

Factors that aggravate insurance risk include lack of risk diversification in terms of type and amount of risk, geographical location and demographics of members covered.

In addition, further uncertainty is introduced via the Scheme's exposure to the risk of adverse member movements. Different plans are priced according to an assumed membership profile per option. Adverse membership movement will invalidate this assumption. The Scheme has partly mitigated this risk by allowing for some adverse membership movement in the pricing of the lower options.

The BOT frequently assesses the necessity to enter into risk transfer arrangements with the assistance of the Scheme's actuarial consultants.

The Scheme uses several methods to assess and monitor insurance risk exposures both for individual types of risks insured and overall risks. The principal risk is that the frequency and severity of claims is greater than expected.

Insurance events are by their nature random and the actual number and size of events during any one year may vary from those estimated using established statistical techniques.

5. REVIEW OF THE ACCOUNTING PERIOD’S ACTIVITIES

5.1 ResultsoftheScheme

The results of the Scheme’s operations for the year under review at 31 December 2017 are set out in the summarised financial statements and the Trustees believe no further clarification is required.

Option A, which consists of pensioner members, Option B, which is the mid-range option and largest by membership, and Option C, which consists mainly of entry-level and low-income members, were all costed to incur net healthcare deficits in 2017. These deficits would be funded from the favourable reserve position of the Scheme, as the contribution increases required to achieve net healthcare surpluses on these options were considered to be too onerous for members.

In 2017, Option A’s results were ahead of budget, whilst Option B and Option C results were worse than budgeted. As a result, the Scheme’s overall results were worse than budget. The driver of this adverse experience is as a result of a different member mix on the different options compared to budget, which resulted in lower than expected members and consequently contribution income on Option A, and higher than expected members and claims on Option B and Option C. The adverse claiming experience on Option B and Option C may also have been exacerbated by the fact that new members joining these options would not have been subject to any underwriting.

4. MANAGEMENT OF INSURANCE RISK (continued)

18 19

Report of the Board of Trustees Report of the Board of TrusteesMEDiPOS MEDICAL SCHEME MEDiPOS MEDICAL SCHEME

5.2 Reviewofoperations

Operationalactivities-2017 2017 2017 2017 2017 2016OptionA OptionB OptionC Total Total

Number of members at year end 1 734 9 134 2 815 13 683 13 056Average number of members for the year 1 779 9 066 2 668 13 513 12 436Number of beneficiaries at year end 2 285 19 258 5 612 27 155 26 161Average number of beneficiaries for the year 2 358 19 188 5 352 26 898 25 161Dependant ratio 0.3 1.1 1.0 1.0 1.0Average age of beneficiaries 71 33 31 36 36Pensioner ratio 76% 5% 2% 11% 11%Average contributions per member per month R 6 385 R 3 288 R 1 710 R 3 384 R 3 184 Average contributions per beneficiary per month R 4 817 R 1 554 R 852 R 1 700 R 1 574 Relevant healthcare expenditure per member per month R 6 249 R 3 442 R 1 705 R 3 468 R 3 327 Relevant healthcare expenditure per beneficiary per month R 4 715 R 1 626 R 850 R 1 742 R 1 644 Non-healthcare expenditure per member per month R 184 R 184 R 184 R 184 R 173 Non-healthcare expenditure per beneficiary per month R 139 R 87 R 92 R 92 R 85 Average managed care: Managed services per member per month R 46 R 46 R 46 R 46 R 44 Average members’ funds per member at year end N/A N/A N/A R 40 500 R 42 184 Relevant healthcare expenditure as a percentage of net contributions 97.9% 104.7% 99.7% 102.5% 104.5%Managed care: Management services as a percentage of contributions 0.7% 1.4% 2.7% 1.4% 1.4%Non-health expenses as a percentage of contributions 2.9% 5.6% 10.8% 5.4% 5.4%Amount paid to Administrator N/A N/A N/A R 33 517 891 R 29 086 520 ff Administration fees (MMI

Health (Pty) Ltd) N/A N/A N/A R 26 037 210 R 22 594 874 ff Managed care fees

(Metropolitan Health Risk Management (Pty) Ltd) 984 814 5 018 966 1 476 901 R 7 480 681 R 6 491 646

Return on investments N/A N/A N/A 7.3% 7.3%

5. REVIEW OF THE ACCOUNTING PERIOD’S ACTIVITIES (continued)

5.2 Reviewofoperations(continued)

Operationalactivities-2016 2016 2016 2016 2016OptionA OptionB OptionC Total

Number of members at year end 1 831 8 795 2 430 13 056Average number of members for the year 1 883 8 532 2 021 12 436Number of beneficiaries at year end 2 440 18 740 4 981 26 161Average number of beneficiaries for the year 2 537 18 360 4 264 25 161Dependant ratio 0.3 1.1 1.0 1.0Average age of beneficiaries 70 33 31 36Pensioner ratio 75% 6% 2% 11%Average contributions per member per month R 5 767 R 2 990 R 1 598 R 3 184 Average contributions per beneficiary per month R 4 280 R 1 389 R 757 R 1 574 Relevant healthcare expenditure per member per month R 6 079 R 3 134 R 1 580 R 3 327 Relevant healthcare expenditure per beneficiary per month R 4 512 R 1 456 R 749 R 1 644 Non-healthcare expenditure per member per month R 173 R 173 R 173 R 173 Non-healthcare expenditure per beneficiary per month R 128 R 80 R 82 R 85 Average managed care: Managed services per member per month R 43 R 44 R 44 R 44 Average members’ funds per member at year end N/A N/A N/A R 42 184 Relevant healthcare expenditure as a percentage of contributions 105.4% 104.8% 98.8% 104.5%Managed care: Management services as a percentage of contributions 0.8% 1.5% 2.7% 1.4%Non-health expenses as a percentage of contributions 3.0% 5.8% 10.8% 5.4%Amount paid to Administrator N/A N/A N/A R 29 086 520 ff Administration fees (MMI Health

(Pty) Ltd) N/A N/A N/A R 22 594 874 ff Managed care fees (Metropolitan

Health Risk Management (Pty) Ltd) 982 806 4 453 776 1 055 064 R 6 491 646 Return on investments N/A N/A N/A 7.3%

5. REVIEW OF THE ACCOUNTING PERIOD’S ACTIVITIES (continued)

20 21

Report of the Board of Trustees Report of the Board of TrusteesMEDiPOS MEDICAL SCHEME MEDiPOS MEDICAL SCHEME

5.3 Accumulatedfundsratio 2017R

2016R

The accumulated funds ratio is calculated on the following basis:

Total members’ funds per statement of financial position 554 157 382 550 752 824Less: Revaluation reserve (28 958 640) (18 972 595)

Accumulated funds per Regulation 29 of the Act 525 198 742 531 780 229

Gross contributions 548 775 999 475 169 844Accumulated funds ratio: (Reserve ratio) 95.70% 111.91%

The above calculation has been performed in terms of the formulae recommended by the Council for Medical Schemes (CMS). In terms of Regulation 29(2) of the Act, the Scheme must maintain accumulated funds expressed as a percentage of gross annual contributions for the accounting period under review, which may not be less than 25%.

5.4 Revaluationreserve-Available-for-saleinvestments

The revaluation reserve in the summarised statement of financial position reflects the net unrealised gains on the Scheme’s investment portfolios with Coronation Fund Managers (Pty) Ltd, Prescient Investment Management (Pty) Ltd and Nedgroup Investments (Pty) Ltd.

5.5 Outstandingclaimsprovision

Movements in the outstanding risk claims provision are set out in Note 3 to the summarised financial statements. The accuracy of the provision was tested against subsequent settlements.

6. INVESTMENTS IN AND LOANS TO PARTICIPATING EMPLOYERS OF MEMBERS OF THE SCHEME AND TO OTHER RELATED PARTIES

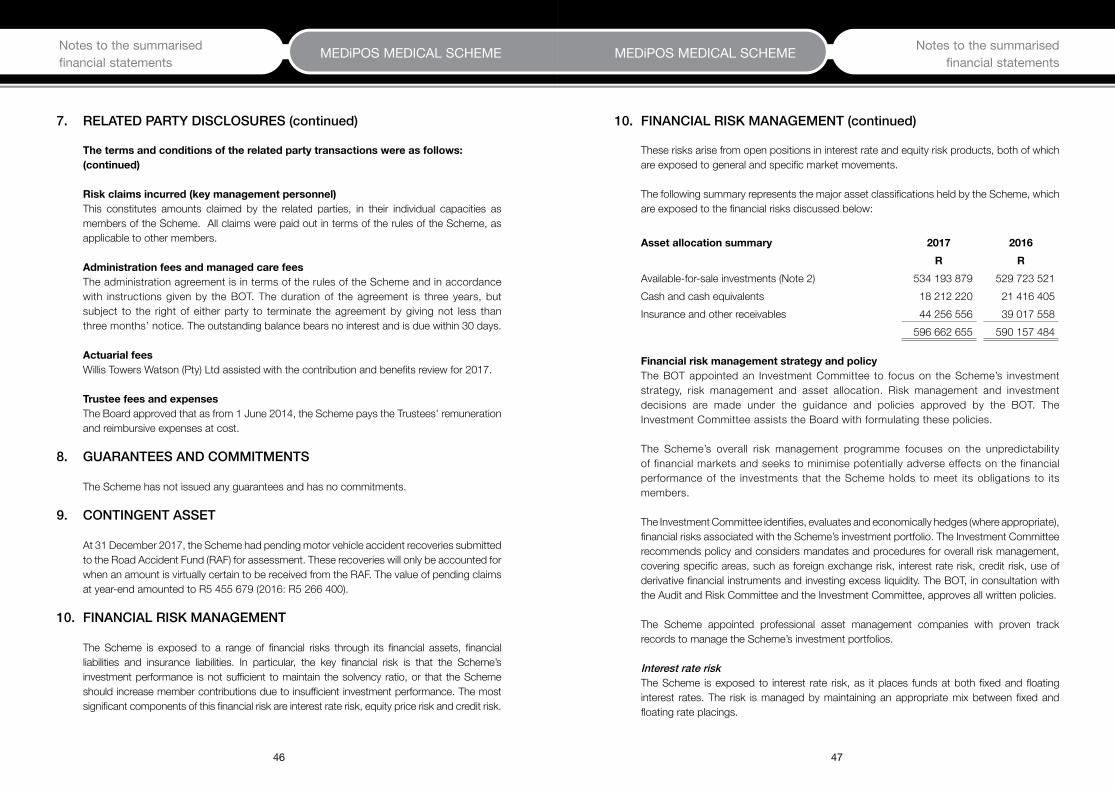

The Scheme holds no direct investments in and has granted no loans to the participating employers of the Scheme or any other related parties. Refer to Note 7 to the summarised financial statements for related party disclosures. The investments in administrators form part of a pooled vehicle and the Scheme has been granted an exemption in this respect. Refer to Note 14.1 to the summarised financial statements for non-compliance disclosure.

7. FIDELITY COVER

The Scheme has a fidelity policy underwritten by Carmargue Underwriting Managers (Pty) Ltd. The sum insured is R75 million (2016: R75 million) and extends to the Trustees, Principal Officer and members of sub-committees of the BOT.

5. REVIEW OF THE ACCOUNTING PERIOD’S ACTIVITIES (continued) 8. ACTUARIAL SERVICES

Willis Towers Watson (Pty) Ltd was consulted in the determination of the contribution and benefit levels, as well as the calculation of the incurred-but-not-reported (IBNR) provision.

9. COMMITTEES OF THE BOT

The BOT conducts the Scheme’s business with integrity by applying appropriate corporate governance policies and practices.

The Scheme has an independent BOT, which has established its own governance practices and committees that comply with the applicable governance and regulatory requirements. These committees fulfil key roles in ensuring good corporate governance.

The following committees are mandated by the BOT by means of written terms of reference as to their membership, authority and duties. These committees meet on a regular basis and when the need arises.

9.1 AuditandRiskCommittee

The committee met on the following four occasions during the course of the year: 6 April 2017 13 June 2017 6 September 2017 12 October 2017.

The Principal Officer, the Administrator, internal auditors and the Scheme’s external auditor attend committee meetings and have unrestricted access to the Chairperson of the Audit and Risk Committee. In accordance with the provisions of the Act, the primary responsibility of the committee is to assist the BOT in carrying out its duties relating to the Scheme’s accounting policies, internal control systems and financial reporting practices. Further objectives include ensuring that all material risks to which the Scheme is exposed, as identified by the BOT, are adequately managed. The external auditors and internal auditors report formally to the committee on critical findings arising from the audit.

22 23

Report of the Board of Trustees Report of the Board of TrusteesMEDiPOS MEDICAL SCHEME MEDiPOS MEDICAL SCHEME

9.1 AuditandRiskCommittee(continued)

The members of the committee are:

M Brown Chairperson and independent memberD Galloway TrusteeK Rapoo TrusteeC Phillips IndependentM Mncwabe Independent. The Audit and Risk Committee has reported that:

ff it has carried out its duties in terms of the Act, as amended and the BOT’s written Audit Committee charter;

ff the external auditors have confirmed their independence; ff the assurance provided by the Administrator has satisfied the Audit Committee that

associated risks have been considered and addressed; ff the assurances provided by the Administrator, the external auditors and the internal

auditors have satisfied the committee that internal controls are adequate and effective; and

ff it has reviewed the Scheme’s financial statements, reviewed the accounting policies, obtained assurances from the external auditors and recommended the adoption of the financial statements by the BOT for presentation to members.

9.2 InvestmentCommittee

The primary responsibility of the committee is to assist the BOT in carrying out its duties relating to the review, formulation and implementation of the investment strategy of the Scheme.

The committee met once during the course of the year:

6 April 2017.

9. COMMITTEES OF THE BOT (continued)

9.2 InvestmentCommittee(continued) The members of the committee are:

D Galloway Chairman and Trustee B Blume Trustee (term of office expired 27 June 2017)M Mlauzi Trustee (resigned 15 February 2017)J Erasmus Member M Faasen Member.

9.3 ClinicalCommittee

The primary responsibility of the committee is to assist the BOT in its responsibility for oversight of the Scheme’s various managed care programmes and to ensure that all clinical risks to which the Scheme is exposed, are identified and adequately managed.

The committee met on the following six occasions during the course of the year:

9 February 2017 (Clinical strategic workshop)10 February 2017 18 May 2017 (Clinical strategic workshop)19 May 2017 28 July 2017 27 October 2017. The members of the committee are:

Dr M Mpata Chairman and Trustee K Rapoo Trustee J Swart Trustee (term of office expired 27 June 2017)D Galloway Trustee (appointed to Committee 27 June 2017)MF Mosoeu Principal Officer.

9.4 BenefitReviewCommittee(SpecialBOTMeeting)

The primary responsibility of the committee is to advise on new benefit and contribution structures.

The committee met on the following four occasions during the course of the year: 7 June 2017 23 August 2017 6 July 2017 7 September 2017.

9. COMMITTEES OF THE BOT (continued)

24 25

Report of the Board of Trustees Report of the Board of TrusteesMEDiPOS MEDICAL SCHEME MEDiPOS MEDICAL SCHEME

9.4 BenefitReviewCommittee(SpecialBOTMeeting)(continued)

The members of the committee are: M Mpata Employer-appointed Trustee (resigned 30 April 2017)A Nongogo Acting Chairperson and employer-appointed TrusteeB Blume Member-elected Trustee (term of office expired 27 June 2017)J Swart Member-elected Trustee (term of office expired 27 June 2017)R Serage Member-elected Trustee (re-elected 27 June 2017)D Galloway Member-elected Trustee (re-elected 27 June 2017)V Nair Member-elected Trustee (term of office expired 27 June 2017)K Rapoo Employer-appointed TrusteeM Mpata Member-elected Trustee (elected 27 June 2017)K Mokgohloa Member-elected Trustee (elected 27 June 2017)B Thabane Member-elected Trustee (elected 27 June 2017)MF Mosoeu Principal Officer.

9.5 MarketingCommittee

The primary responsibility of the committee is to assist the BOT to develop a marketing strategy for the Scheme in order to market the Scheme to the employees of the South African Post Office (SAPO).

The committee met on the following four occasions during the course of the year:

15 March 2017 14 June 2017 6 September 2017 11 October 2017. The members of the committee are:

R Serage Chairperson and Trustee (re-elected 27 June 2017)V Nair Trustee (term of office expired 27 June 2017)B Thabane Member (resigned 26 June 2017)B Thabane Trustee (appointed 27 June 2017)S Khumalo MemberM Fikizolo Member MF Mosoeu Principal Officer.

9. COMMITTEES OF THE BOT (continued)

9.6 OperationsCommittee

The primary responsibility of the committee is to assist the BOT on operational matters of the Scheme.

The committee met on the following two occasions during the course of the year:

15 March 2017 11 October 2017. The members of the committee are:

R Serage Chairperson and Trustee (re-elected 27 June 2017)J Swart Trustee (term of office expired 27 June 2017)A Nongogo Trustee K Mokgohloa Trustee (appointed 24 August 2017)O Godlo MemberJ Mokone MemberM Swart MemberG Moore MemberD Troskie Member.

9. COMMITTEES OF THE BOT (continued)

26 27

Report of the Board of Trustees Report of the Board of TrusteesMEDiPOS MEDICAL SCHEME MEDiPOS MEDICAL SCHEME

10. MEETING ATTENDANCES

The following schedule sets out BOT meeting attendances and attendances by members of Board Sub-Committees.

Trustee/Sub-Committeemember BoardofTrustees

AuditandRiskCommittee

InvestmentCommittee

Clinical Committee

A B A B A B A BM Mpata (resigned as employer-appointed Trustee 30 April 2017) 2 2 2 2

M Mpata (elected as member Trustee 27 June 2017) 2 2 2 2K Rapoo 5 4 4 3 6 6B Blume (term of office expired 27 June 2017) 3 2 1 1D Galloway 5 5 4 4 1 1 2 2V Nair (term of office expired 27 June 2017) 3 3R Serage 5 5J Swart (term of office expired 27 June 2017) 3 3 4 4A Nongogo 5 5M Mlauzi (resigned 15 February 2017) 0 0C Mofokeng (resigned 25 January 2017) 0 0B Thabane (elected 27 June 2017) 2 2K Mokgohloa (elected 27 June 2017) 2 2MF Mosoeu (Principal Officer) 5 5 4 4 1 1 6 6M Brown 1 1 4 4C Phillips 4 4M Mncwabe 4 3M Faasen 1 1J Erasmus 1 1O GodloM SwartG MooreB Thabane (resigned as non-Trustee 26 June 2017)J MokoneD TroskieM FikizoloS Khumalo

A - Total possible number of meetings could have attendedB - Actual number of meetings attended

10. MEETING ATTENDANCES (continued)

The following schedule sets out BOT meeting attendances and attendances by members of Board Sub-Committees.

Trustee/Sub-Committeemember BenefitReview

Committee

OperationsCommittee

MarketingCommittee

A B A B A BM Mpata (resigned as employer-appointed Trustee 30 April 2017)

0 0

M Mpata (elected as member Trustee 27 June 2017) 3 3K Rapoo 4 3B Blume (term of office expired 27 June 2017) 1 1D Galloway 4 3V Nair (term of office expired 27 June 2017) 1 1 2 2R Serage 4 4 2 2 4 4J Swart (term of office expired 27 June 2017) 1 1 1 1A Nongogo 4 4 2 2M Mlauzi (resigned 15 February 2017) 0 0C Mofokeng (resigned 25 January 2017) 0 0B Thabane (elected 27 June 2017) 3 3 2 2K Mokgohloa (elected 27 June 2017) 3 3MF Mosoeu (Principal Officer) 4 4 2 2 4 4M BrownC PhillipsM MncwabeM FaasenJ ErasmusO Godlo 2 2M Swart 2 2G Moore 2 2B Thabane (resigned as non-Trustee 26 June 2017) 2 2J Mokone 2 1D Troskie 2 2M Fikizolo 4 3S Khumalo 4 2

A - Total possible number of meetings could have attendedB - Actual number of meetings attended

28 29

Report of the Board of Trustees Report of the Board of TrusteesMEDiPOS MEDICAL SCHEME MEDiPOS MEDICAL SCHEME

11. EVENTS AFTER THE REPORTING DATE

No material facts or circumstances have arisen between the date of the statement of financial position and the date of this report, which affect the financial position or financial performance of the Scheme, as reflected in these summarised financial statements.

12. NON-COMPLIANCE WITH THE MEDICAL SCHEMES ACT 131 OF 1998

The CMS stipulated, via Circular 11 of 2006, that all cases of non-compliance with the Act should be disclosed in the financial statements. The following stipulations were not complied with during the year:

12.1 ContraventionofSection35(8)(c)oftheMedicalSchemesAct131of1998,asamended

Nature and impactThe Scheme holds shares in MMI Holdings Ltd, Sanlam Ltd and Discovery Holdings Ltd. This is in contravention of Section 35(8) of the Act, as the Scheme is not allowed to hold shares in the holding company of its administrator and other administrators.

Causes of the non-complianceThe Scheme invests in a pooled product and does not have control over the underlying assets.

Corrective course of actionThe Scheme received an exemption from the CMS on 7 April 2017, valid for a period of 12 months, from complying with Section 35(8)(c) insofar as it relates to investments placed with asset managers who invest on behalf of the Scheme and where such investment choices are not influenced by the Scheme.

12.2Non-compliancewithSection26(7)oftheAct-contributionsreceivedafter threedaysofbecomingdue Nature and impact

In terms of Section 26(7) of the Act, all contributions shall be paid to a medical scheme not later than three days after payment thereof becoming due. This may pose a financial risk to the Scheme due to non-payment, as well as a loss of interest on these amounts to the Scheme.

Causes of the non-complianceDue to the financial position of SAPO, contributions have been received after three days of it becoming due. Certain pensioners also paid late due to unsuccessful debit order deductions. As a result, the Scheme is in contravention of Section 26(7).

12.2Non-compliancewithSection26(7)oftheAct-contributionsreceivedafter threedaysofbecomingdue(continued)

Corrective course of actionThe BOT has prioritised this matter and there are continuous engagements with the Post Office to ensure that contributions are received timeously. The Board will continue monitoring the payments until the issue is resolved. The Board resolved that disinvestments will be made as and when necessary from the Scheme’s investments in order to bridge any cash flow shortfall that may arise, and that members as well as service providers, will not be prejudiced in any way.

12.3Non-compliancewithSection33(2)oftheAct-optionsnotfinanciallysound

Nature and impactIn terms of Section 33(2) of the Act, each benefit option shall be self-supporting in terms of membership and financial performance and will be financially sound. As at 31 December 2017, all three options were in a net healthcare deficit position, thereby contravening Section 33(2) of the Act. The total healthcare deficit amounted to R43 502 640 (2016: R47 103 875) representing 7.93% (2016: 9.91%) of the aggregated contributions of the Scheme. As at 31 December 2017, Option A as well as Option C is in a net surplus position of R3 798 741 and R1 624 062 respectively (2016: Option A net deficit R5 347 651 and Option C net surplus R1 984 418), and Option B is in a net deficit position of R12 004 291 (2016: R7 285 183).

Causes of the non-complianceOption A, which consists of pensioner members, Option B, which is the mid-range option and largest by membership, and Option C, which consists mainly of entry-level and low-income members, were all costed to incur net healthcare deficits in 2017. These deficits would be funded from the favourable reserve position of the Scheme as the contribution increases required to achieve net healthcare surpluses on these options were considered to be too onerous for members. In 2017, Option A’s results were ahead of budget whilst Option B and Option C results were worse than budgeted. As a result, the Scheme’s overall results were worse than budget. The driver of this adverse experience is a different member mix on the different options compared to budget, which resulted in lower than expected members and consequently contribution income on Option A, and higher than expected members and claims on Option B and Option C. The adverse claiming experience on Option B and Option C may also have been exacerbated by the fact that new members joining these options would not have been subject to any underwriting.

12. NON-COMPLIANCE WITH THE MEDICAL SCHEMES ACT 131 OF 1998 (continued)

Summarised financial statementsMEDiPOS MEDICAL SCHEME

3130

Report of the Board of Trustees MEDiPOS MEDICAL SCHEME

Corrective course of actionThe Trustees have noted the net healthcare deficits and will continue to monitor the performance of the Scheme and they will make appropriate interventions during the annual benefit review process together with corrective action to be taken to correct the performance in the ensuing three to five years.

12. NON-COMPLIANCE WITH THE MEDICAL SCHEMES ACT 131 OF 1998 (continued)

12.3 Non-compliancewithSection33(2)of theAct -optionsnot financially sound(continued)

Independent Auditor’s report on Summary Financial Statements TO THE MEMBERS OF MEDiPOS MEDICAL SCHEME

Opinion

The summary financial statements, as set out on pages 33 to 62 which comprise the summary statement of financial position as at 31 December 2017, and the summary statement of comprehensive income, summary statement of changes in funds and reserves and summary statement of cash flows for the period then ended, and related notes, are derived from the audited financial statements of MEDiPOS Medical Scheme (the Scheme) for the year ended 31 December 2017.

In our opinion, the accompanying summary financial statements are consistent, in all material respects, with the audited financial statements, in accordance with the content and disclosure requirements of Circular 6 of 2013 issued by the Council for Medical Schemes.

Summary Financial Statements

The summary financial statements do not contain all the disclosures required by International Financial Reporting Standards and the Medical Schemes Act of South Africa. Reading the summary financial statements and the auditor’s report thereon, therefore, is not a substitute for reading the audited financial statements and the auditor’s report thereon. The summary financial statements and audited financial statements do not reflect the effects of events that occurred subsequent to the date of our report on the audited financial statements.

The Audited Financial Statements and Our Report Thereon

We expressed an unmodified audit opinion on the audited financial statements in our report dated 20 April 2018. That report also includes:

- The communication of key audit matters.

Trustees’ Responsibility for the Summary Financial Statements

The Trustees are responsible for the preparation of the summary financial statements in accordance with the content and disclosure requirements of Circular 6 of 2013 issued by the Council for Medical Schemes.

Summarised financial statements Summarised financial statementsMEDiPOS MEDICAL SCHEME MEDiPOS MEDICAL SCHEME

32 33

Auditor’s Responsibility

Our responsibility is to express an opinion on whether the summary financial statements are consistent, in all material respects, with the audited financial statements based on our procedures, which were conducted in accordance with International Standards on Auditing (ISA) 810 (Revised), Engagements to Report on Summary Financial Statements.

KPMG Inc

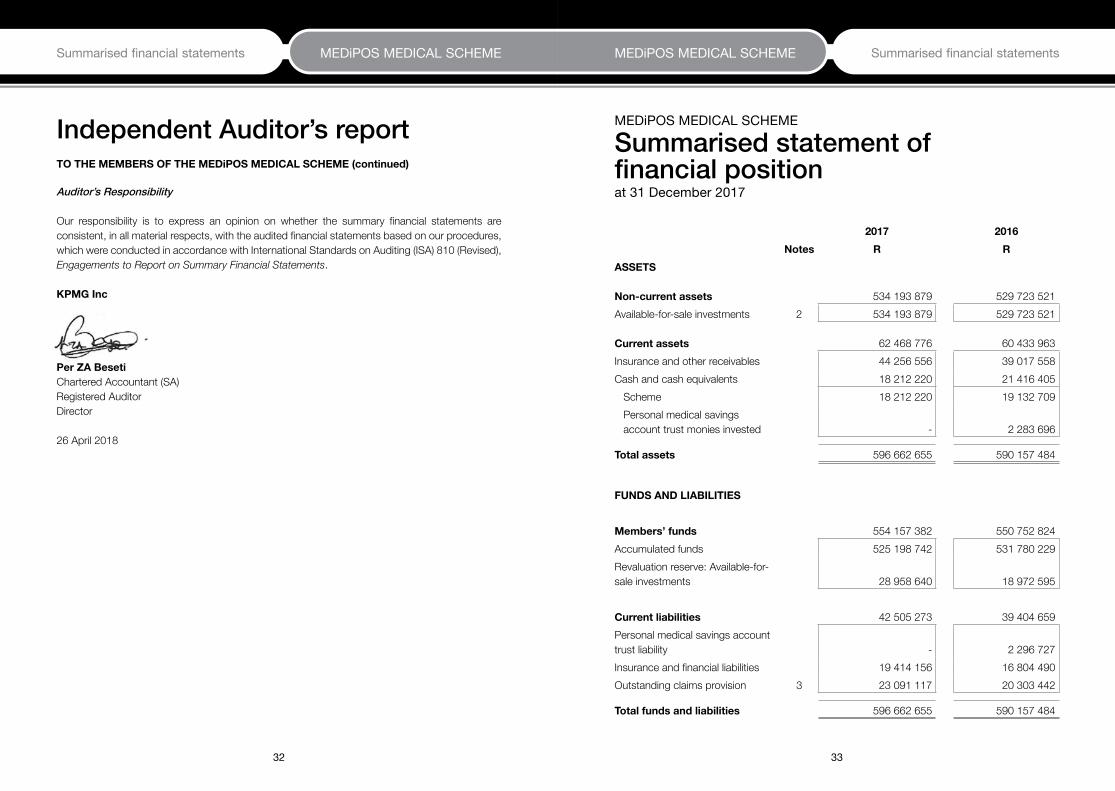

PerZABeseti Chartered Accountant (SA) Registered Auditor Director 26 April 2018

Independent Auditor’s report TOTHEMEMBERSOFTHEMEDiPOSMEDICALSCHEME(continued)

MEDiPOS MEDICAL SCHEME

Summarised statement of financial positionat 31 December 2017

2017 2016Notes R R

ASSETS

Non-currentassets 534 193 879 529 723 521 Available-for-sale investments 2 534 193 879 529 723 521

Currentassets 62 468 776 60 433 963 Insurance and other receivables 44 256 556 39 017 558 Cash and cash equivalents 18 212 220 21 416 405 Scheme 18 212 220 19 132 709 Personal medical savings

account trust monies invested - 2 283 696

Totalassets 596 662 655 590 157 484

FUNDS AND LIABILITIES

Members’funds 554 157 382 550 752 824 Accumulated funds 525 198 742 531 780 229 Revaluation reserve: Available-for-sale investments 28 958 640 18 972 595

Currentliabilities 42 505 273 39 404 659 Personal medical savings account trust liability - 2 296 727 Insurance and financial liabilities 19 414 156 16 804 490 Outstanding claims provision 3 23 091 117 20 303 442

Totalfundsandliabilities 596 662 655 590 157 484

Summarised financial statements Summarised financial statementsMEDiPOS MEDICAL SCHEME MEDiPOS MEDICAL SCHEME

34 35

MEDiPOS MEDICAL SCHEME

Summarised statement of comprehensive incomefor the year ended 31 December 2017

2017 2016Notes R R

Riskcontributionincome 4 548 775 999 475 169 844

RelevanthealthcareexpenditureNet claims incurred (562 428 829) (496 507 072) Risk claims incurred (555 702 243) (490 721 447) Managed care: Management services (7 480 681) (6 491 646) Third-party claim recoveries 754 095 706 021

Grosshealthcareresult (13 652 830) (21 337 228)

Administration expenses (29 666 941) (25 722 513)Net impairment losses on insurance receivables (182 869) (44 134)

Nethealthcareresult (43 502 640) (47 103 875)

Otherincome 40 347 565 39 742 765 Investment income 5 35 967 993 35 589 761 Realised gain on disposal of available-for-sale

investments 2 1 995 419 4 151 751 Sundry income 2 384 153 1 253

Otherexpenditure (3 426 413) (3 287 306) Asset management fees (3 309 017) (3 156 751) Interest allocated to savings accounts (117 396) (130 555)

Deficitfortheyear (6 581 488) (10 648 416)

Othercomprehensiveincome

Itemsthatmaybereclassifiedsubsequentlytoprofitandloss: Fair value adjustment on available-for-sale

investments 2 11 981 464 4 753 322 Less: Realised gain on disposal of available-for-

sale investments 2 (1 995 419) (4 151 751)

Totalcomprehensiveincome/(loss)fortheyear 3 404 557 (10 046 845)

MEDiPOS MEDICAL SCHEME

Summarised statement of changes in funds and reserves for the year ended 31 December 2017

2017 2016R R

Accumulatedfunds

Balance at the beginning of the year 531 780 229 542 428 645

Deficit for the year (6 581 488) (10 648 416)

Balance at the end of the year 525 198 742 531 780 229

Revaluationreserve:Available-for-saleinvestments

Balance at the beginning of the year 18 972 595 18 371 024

Movement in revaluation of available-for-sale investments 11 981 464 4 753 322

Realised gain on disposal of available-for-sale investments (1 995 419) (4 151 751)

Balance at the end of the year 28 958 640 18 972 595

Members’ funds 554 157 382 550 752 824

37

MEDiPOS MEDICAL SCHEME Notes to the summarised financial statements

Summarised financial statements MEDiPOS MEDICAL SCHEME

36

MEDiPOS MEDICAL SCHEME

Summarised statement of cash flowsfor the year ended 31 December 2017

2017 2016R R

CASH FLOWS FROM OPERATING ACTIVITIESCash flows from operations before working capital changes (6 464 092) (10 517 861)Deficit for the year (6 581 488) (10 648 416)Add back: Interest on savings accounts 117 396 130 555 Adjustments for:- Investment income (35 967 993) (35 589 761)- Realised gain on disposal of available-for-sale investments (1 995 419) (4 151 751)- Movement in accumulated impairment losses 134 478 51 845 - Interest accrued on savings accounts (117 396) (130 555)

Cash flows utilised in operations before working capital changes (44 410 422) (50 338 083)

Workingcapitalchanges (2 293 328) 11 878 797 - Increase in insurance and other receivables (5 393 942) (2 911 861)- Increase in insurance and financial liabilities 2 609 666 13 000 509 - (Decrease)/Increase in savings plan liability (2 296 727) 34 857 - Increase in outstanding claims provision 2 787 675 1 755 292

Netcashutilisedinoperatingactivities (46 703 750) (38 459 286)

CASH FLOWS FROM INVESTING ACTIVITIES 43 499 565 40 186 756 Purchase of available-for-sale investments (124 671 179) (676 305 677)Proceeds on disposal of available-for-sale investments 132 182 285 680 923 689 Interest received 29 065 725 29 631 039 Dividends received 6 922 734 5 937 705

NET(DECREASE)/INCREASEINCASHANDCASH EQUIVALENTS (3 204 185) 1 727 470

Cash and cash equivalents at the beginning of the year 21 416 405 19 688 935 CASH AND CASH EQUIVALENTS AT THE END OF THE YEAR 18 212 220 21 416 405 Scheme 18 212 220 19 132 709 Personal medical savings account trust monies invested - 2 283 696

MEDiPOS MEDICAL SCHEME

Notes to the summarisedfinancial statements for the year ended 31 December 2017

1. PRINCIPAL ACCOUNTING POLICIES

The accounting policies set out below have been applied consistently to all periods presented in these summarised financial statements. The same accounting policies and methods of computation are followed in the interim financial statements as compared with the most recent annual financial statements. StatementofcomplianceThe summarised financial statements are prepared in accordance with International Financial Reporting Standards (IFRS) and its interpretations adopted by the International Accounting Standard Board (IASB) and the requirements of the Medical Schemes Act of South Africa no 131 of 1998 (the Act).

1.1 BasisofpreparationThe summarised financial statements provide information about the financial position, results of operations and changes in financial position of the Scheme. These have been prepared under the historical cost convention, except for available-for-sale financial assets, which are carried at fair value. The Scheme’s functional and presentation currency is South African rands. Useofestimates The preparation of the summarised financial statements necessitates the use of estimates and assumptions. These estimates and assumptions affect the reported amount of assets, liabilities and contingent liabilities at the reporting date as well as affecting the reported income and expenditure for the year. The actual outcome may differ from these estimates. For further information on critical estimates and judgements refer to Note 3.

38 39

MEDiPOS MEDICAL SCHEME MEDiPOS MEDICAL SCHEME Notes to the summarised financial statements

Notes to the summarised financial statements

2. AVAILABLE-FOR-SALE INVESTMENTS 2017 2016R R

Fair value at the beginning of the year 529 723 521 529 588 211 Additions 124 671 179 676 305 677 Disposals (130 186 866) (676 771 938)Realised gain on disposal of available-for-sale investments (1 995 419) (4 151 751)Unrealised gain on revaluation of available-for-sale investments 11 981 464 4 753 322 Fair value at the end of the year 534 193 879 529 723 521

Non-current 534 193 879 529 723 521

The investments included above represent investments managed by:

Prescient Investment Management (Pty) Ltd 254 446 071 234 826 199 Coronation Fund Managers (Pty) Ltd 279 747 808 294 897 322

534 193 879 529 723 521

Investments are summarised as follows:

- Bonds and debentures 54 177 654 64 179 486 - Money-market (cash and outstanding) 67 425 276 67 090 336 - Equities 134 969 472 167 586 596 - Collective investment scheme 246 208 972 185 793 545 - Pooled fund 31 412 505 45 073 558

534 193 879 529 723 521

The maturity profile of the bonds vary and are as follows (percentage of total fair value):

0 - 3 years 1.30% 1.07%3 - 7 years 6.27% 5.98%7 years+ 2.57% 5.06%

10.14% 12.12%

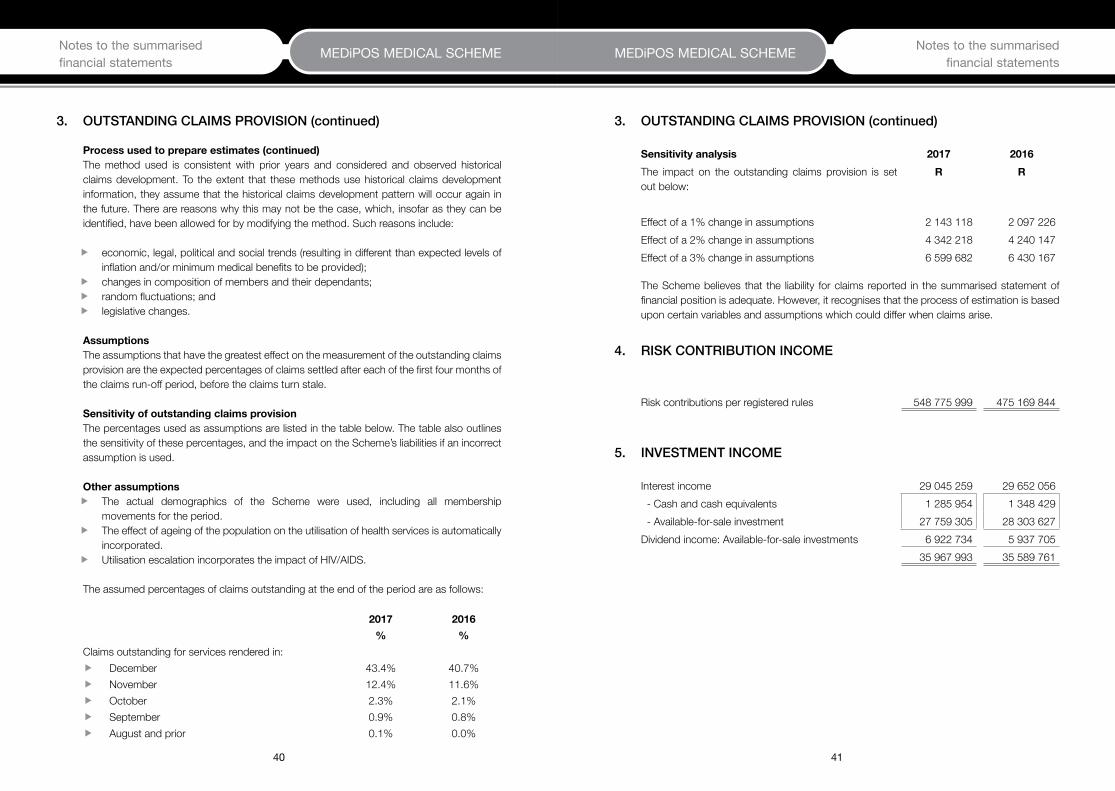

3. OUTSTANDING CLAIMS PROVISION 2017 2016R R

NotcoveredbyrisktransferarrangementsProvision for outstanding claims 23 091 117 20 303 442

AnalysisofmovementsinoutstandingclaimsBalance at beginning of year 20 303 442 18 548 150 Payments in respect of prior year (18 321 125) (18 704 066)Over/(Under) provision in the prior year 1 982 317 (155 916)(Over)/Under provision in respect of prior year written back (1 982 317) 155 916 Adjustment for current year 23 091 117 20 303 442 Balance at end of year 23 091 117 20 303 442

ProcessusedtoprepareestimatesThe process used to determine the assumptions is intended to result in neutral estimates of the most likely or expected outcome. The sources of data used as inputs for the assumptions are internal, using detailed studies that are carried out monthly. There is more emphasis on current trends, and where in early years there is insufficient information to make a reliable best estimate of claims development, prudent assumptions are used. Each notified claim is assessed on a separate, case-by-case basis with due regard to the claim circumstances, information available from managed care: management services and historical evidence of the size of similar claims. The provisions are based on information currently available. However, the ultimate liabilities may vary as a result of subsequent developments. The impact of many of the items affecting the ultimate costs of the loss is difficult to estimate. The provision estimation difficulties are further complicated by claims complexity, volume of claims, the severity of claims, determining the occurrence date of claim and reporting lags.

The cost of outstanding claims is estimated using run-off triangles. Such methods extrapolate the development of paid and incurred claims, average cost per claims and ultimate claim numbers for each year based upon observed development of earlier years and expected loss ratios. Run-off triangles are used in situations where it takes time after the treatment date until the full extent of the claims to be paid is known. It is assumed that payments will emerge in a similar way in each service month. The proportional increase in the known cumulative payments from one development month to the next can then be used to calculate payments for future development months.

40 41

MEDiPOS MEDICAL SCHEME MEDiPOS MEDICAL SCHEME Notes to the summarised financial statements

Notes to the summarised financial statements

Processusedtoprepareestimates(continued)The method used is consistent with prior years and considered and observed historical claims development. To the extent that these methods use historical claims development information, they assume that the historical claims development pattern will occur again in the future. There are reasons why this may not be the case, which, insofar as they can be identified, have been allowed for by modifying the method. Such reasons include:

ff economic, legal, political and social trends (resulting in different than expected levels of inflation and/or minimum medical benefits to be provided);

ff changes in composition of members and their dependants; ff random fluctuations; andff legislative changes.

AssumptionsThe assumptions that have the greatest effect on the measurement of the outstanding claims provision are the expected percentages of claims settled after each of the first four months of the claims run-off period, before the claims turn stale.

SensitivityofoutstandingclaimsprovisionThe percentages used as assumptions are listed in the table below. The table also outlines the sensitivity of these percentages, and the impact on the Scheme’s liabilities if an incorrect assumption is used. Otherassumptionsff The actual demographics of the Scheme were used, including all membership

movements for the period.ff The effect of ageing of the population on the utilisation of health services is automatically

incorporated.ff Utilisation escalation incorporates the impact of HIV/AIDS.

The assumed percentages of claims outstanding at the end of the period are as follows:

2017 2016% %

Claims outstanding for services rendered in:ff December 43.4% 40.7%ff November 12.4% 11.6%ff October 2.3% 2.1%ff September 0.9% 0.8%ff August and prior 0.1% 0.0%

3. OUTSTANDING CLAIMS PROVISION (continued)

Sensitivityanalysis 2017 2016The impact on the outstanding claims provision is set out below:

R R

Effect of a 1% change in assumptions 2 143 118 2 097 226 Effect of a 2% change in assumptions 4 342 218 4 240 147 Effect of a 3% change in assumptions 6 599 682 6 430 167

The Scheme believes that the liability for claims reported in the summarised statement of financial position is adequate. However, it recognises that the process of estimation is based upon certain variables and assumptions which could differ when claims arise.

4. RISK CONTRIBUTION INCOME

Risk contributions per registered rules 548 775 999 475 169 844

5. INVESTMENT INCOME

Interest income 29 045 259 29 652 056 - Cash and cash equivalents 1 285 954 1 348 429 - Available-for-sale investment 27 759 305 28 303 627 Dividend income: Available-for-sale investments 6 922 734 5 937 705

35 967 993 35 589 761

3. OUTSTANDING CLAIMS PROVISION (continued)

42 43

MEDiPOS MEDICAL SCHEME MEDiPOS MEDICAL SCHEME Notes to the summarised financial statements

Notes to the summarised financial statements6.

SU

RPLU

S/ (D

EFIC

IT) F

ROM

OPE

RATI

ON

S PE

R BE

NEF

IT O

PTIO

N

2017

OptionA

OptionB

OptionC

Total

R

R

R

R

Riskco

ntrib

utioninco

me

136

315

287

3

57 7

28 6

52

54

732

060

548

775

999

Relevan

thea

lthca

reexp

enditure

(133

404

053

) (3

74 4

44 6

91)

(54

580

085)

(562

428

829

)Ne

t clai

ms

incu

rred

(133

404

053

) (3

74 4

44 6

91)

(54

580

085)

(562

428

829

)Ri

sk c

laim

s in

curre

d9

(132

520

471

) (3

69 9

33 4

22)

(53

248

350)

(555

702

243

)M

anag

ed c

are:

Man

agem

ent s

ervic

es (9

84 8

14)

(5 0

18 9

66)

(1 4

76 9

01)

(7 4

80 6

81)

Third

-par

ty c

laim

reco

verie

s 1

01 2

32

507

697

1

45 1

66

754

095

Grosshea

lthca

rere

sult

2 9

11 2

34

(16716039)

151

975

(1

3652830)

Adm

inist

ratio

n ex

pens

es (3

905

165

) (1

9 90

4 12

3) (5

857

653

) (2

9 66

6 94

1)Ne

t im

pairm

ent g

ain o

n in

sura

nce

rece

ivabl

es (2

3 37

4) (1

22 0

43)

(37

452)

(182

869

)

Nethea

lthca

rere

sult

(1017305)

(36742205)

(5743130)

(43502640)

Otherin

come

5 2

51 3

09

27

047

361

8 0

48 8

95

40

347

565

Inve

stm

ent i

ncom

e 4

720

758

2

4 15

0 81

8 7

096

417

3

5 96

7 99

3 Re

alise

d ga

in o

n di

spos

al of

ava

ilabl

e-fo

r-sa

le in

vest

men

ts 2

27 0

05

1 3

06 0

03

462

411

1

995

419

Su

ndry

inco

me

303

546

1

590

540

4

90 0

67

2 3

84 1

53

Otherexp

enditure

(435

263

) (2

309

447

) (6

81 7

03)

(3 4

26 4

13)

Asse

t man

agem

ent f

ees

(435

263

) (2

219

708

) (6

54 0

46)

(3 3

09 0

17)

Inte

rest

paid

on

savin

gs a

ccou

nts

- (8

9 73

9) (2

7 65

7) (1

17 3

96)

Surplus/(defi

cit)forthe

yea

r 3

798

741

(1

2 00

4 29

1) 1

624

062

(6

581

488

)

Num

bero

fmem

bersaty

eare

nd 1

734

9

134

2

815

1

3 68

3

6.

SURP

LUS/

(DEF

ICIT

) FRO

M O

PERA

TIO

NS

PER

BEN

EFIT

OPT

ION

(con

tinue

d)

2016

OptionA

OptionB

OptionC

Total

R

R

R

R

Riskco

ntrib

utioninco

me

130

300

254

3

06 1

10 1

66

38

759

424

475

169

844

Relevan

thea

lthca

reexp

enditure

(137

363

050

) (3

20 8

30 9

03)

(38

313

119)

(496

507

072

)Ne

t clai

ms

incu

rred

(137

363

050

) (3

20 8

30 9

03)

(38

313

119)

(496

507

072

)Ri

sk c

laim

s in

curre

d9

(136

489

900

) (3

16 8

64 1

01)

(37

367

446)

(490

721

447

)M

anag

ed c

are:

Man

agem

ent s

ervic

es (9

82 8

06)

(4 4

53 7

76)

(1 0

55 0

64)

(6 4

91 6

46)

Third

-par

ty c

laim

reco

verie

s 1

09 6

56

486

974

1

09 3

91

706

021

Grosshea

lthca

rere

sult

(7062796)

(14720737)

446

305

(2

1337228)

Adm

inist

ratio

n ex

pens

es (3

894

004

) (1

7 64

7 29

1) (4

181

218

) (2

5 72

2 51

3)Ne

t im

pairm

ent g

ain o

n in

sura

nce

rece

ivabl

es (7

540

) (3

0 87

4) (5

720

) (4

4 13

4)

Nethea

lthca

rere

sult

(10964340)

(32398902)

(3740633)

(47103875)

Otherin

come

6 0

95 3

51

27

382

566

6 2

64 8

48

39

742

765

Inve

stm

ent i

ncom

e 5

380

783

2

4 44

4 34

0 5

764

638

3

5 58

9 76

1 Re

alise

d ga

in o

n di

spos

al of

ava

ilabe

-for-

sale

inve

stm

ents

714

396

2

937

386

4

99 9

69

4 1

51 7

51

Sund

ry in

com

e17

284

024

1 1

253

Otherexp

enditure

(478

662

) (2

268

847

) (5

39 7

97)

(3 2

87 3

06)

Asse

t man

agem

ent f

ees

(478

662

) (2

166

555

) (5

11 5

34)

(3 1

56 7

51)

Reali

sed

loss

on

disp

osal

of a

vaila

ble-

for-

sale

inve

stm

ents

-

- -

- In

tere

st p

aid o

n sa

vings

acc

ount

s -

(102

292

) (2

8 26

3) (1

30 5

55)

Surplus/(defi

cit)forthe

yea

r (5

347

651

) (7

285

183

) 1

984

418

(1

0 64

8 41

6)

Num

bero

fmem

bersaty

eare

nd 1

831

8

795

2

430

1

3 05

6

44 45

MEDiPOS MEDICAL SCHEME MEDiPOS MEDICAL SCHEME Notes to the summarised financial statements

Notes to the summarised financial statements

6. SURPLUS/(DEFICIT) FROM OPERATIONS PER BENEFIT OPTION (continued)

BasisofallocationsExcept for contribution income and claims, all other income and expenses are allocated according to membership at year end.

7. RELATED PARTY DISCLOSURES

PartieswithsignificantinfluenceovertheSchemeMMI Health (Proprietary) Limited (MMI Health) has significant influence over the Scheme, as it provides financial and operational information on which policy decisions are based, but does not control the Scheme. MMI Health provides administration services.

South African Post Office (SAPO) State-owned Company Ltd is able to participate in operating and financial decisions, as they are able to appoint 50% of the Trustees. Managed care organisation, Metropolitan Health Risk Management (Pty) Ltd, a wholly-owned subsidiary of MMI Health, provides managed care services and has significant influence over the Scheme, but does not control the Scheme. Willis Towers Watson (Pty) Ltd has significant influence over the Scheme, as they provide operational information on which policy decisions are based, but does not control the Scheme. Willis Towers Watson (Pty) Ltd provides consulting and actuarial services and assisted with the contribution and benefits review for 2017. KeymanagementpersonnelandtheirclosefamilymembersKey management personnel are those persons having authority and responsibility for planning, directing and controlling the activities of the Scheme. Key management personnel include the Board of Trustees (BOT), the Principal Officer and members of committees.

Close family members include family members of the BOT, Principal Officer and members of the committees.

TransactionsandbalanceswithrelatedpartiesThe breakdown below provides the total amount of transactions that have been entered into with related parties for the relevant financial year.

2017R

2016RSummarisedstatementofcomprehensiveincome

Risk contributions received (key management personnel) 455 436 553 827 Risk claims incurred (key management personnel) 426 966 930 815 Administrator’s fees - MMI Health (Pty) Ltd 26 037 210 22 594 874 Managed care fees- Metropolitan Health Risk Management (Pty) Ltd 7 480 681 6 491 646 Actuarial fee (Willis Towers Watson (Pty) Ltd) 690 242 666 900 Contribution subsidies (SAPO) 445 884 461 336 189 702 Principal Officer’s office travelling, accommodation and conference expenses 48 337 61 738 Trustees' fees and expenses 774 443 714 447 Audit Committee fees 42 840 27 200

The Principal Officer is being remunerated by the South African Post Office State-owned Company Limited.

SummarisedstatementoffinancialpositionMMI Health (Pty) Ltd- Administrator's fees and cost recoveries payable 2 456 214 2 066 080Metropolitan Health Risk Management (Pty) Ltd- Managed care fees due 630 964 567 967The South African Post Office SOC - 19 806

Thetermsandconditionsoftherelatedpartytransactionswereasfollows:

Riskcontributionsreceived(keymanagementpersonnel) This constitutes the contributions paid by the related parties as members of the Scheme, in their individual capacities. All contributions were at the same terms as applicable to other members.

7. RELATED PARTY DISCLOSURES (continued)

46 47

MEDiPOS MEDICAL SCHEME MEDiPOS MEDICAL SCHEME Notes to the summarised financial statements

Notes to the summarised financial statements

Thetermsandconditionsoftherelatedpartytransactionswereasfollows:(continued)

Riskclaimsincurred(keymanagementpersonnel) This constitutes amounts claimed by the related parties, in their individual capacities as members of the Scheme. All claims were paid out in terms of the rules of the Scheme, as applicable to other members. AdministrationfeesandmanagedcarefeesThe administration agreement is in terms of the rules of the Scheme and in accordance with instructions given by the BOT. The duration of the agreement is three years, but subject to the right of either party to terminate the agreement by giving not less than three months’ notice. The outstanding balance bears no interest and is due within 30 days.

ActuarialfeesWillis Towers Watson (Pty) Ltd assisted with the contribution and benefits review for 2017.

TrusteefeesandexpensesThe Board approved that as from 1 June 2014, the Scheme pays the Trustees’ remuneration and reimbursive expenses at cost.

8. GUARANTEES AND COMMITMENTS

The Scheme has not issued any guarantees and has no commitments.

9. CONTINGENT ASSET

At 31 December 2017, the Scheme had pending motor vehicle accident recoveries submitted to the Road Accident Fund (RAF) for assessment. These recoveries will only be accounted for when an amount is virtually certain to be received from the RAF. The value of pending claims at year-end amounted to R5 455 679 (2016: R5 266 400).

10. FINANCIAL RISK MANAGEMENT

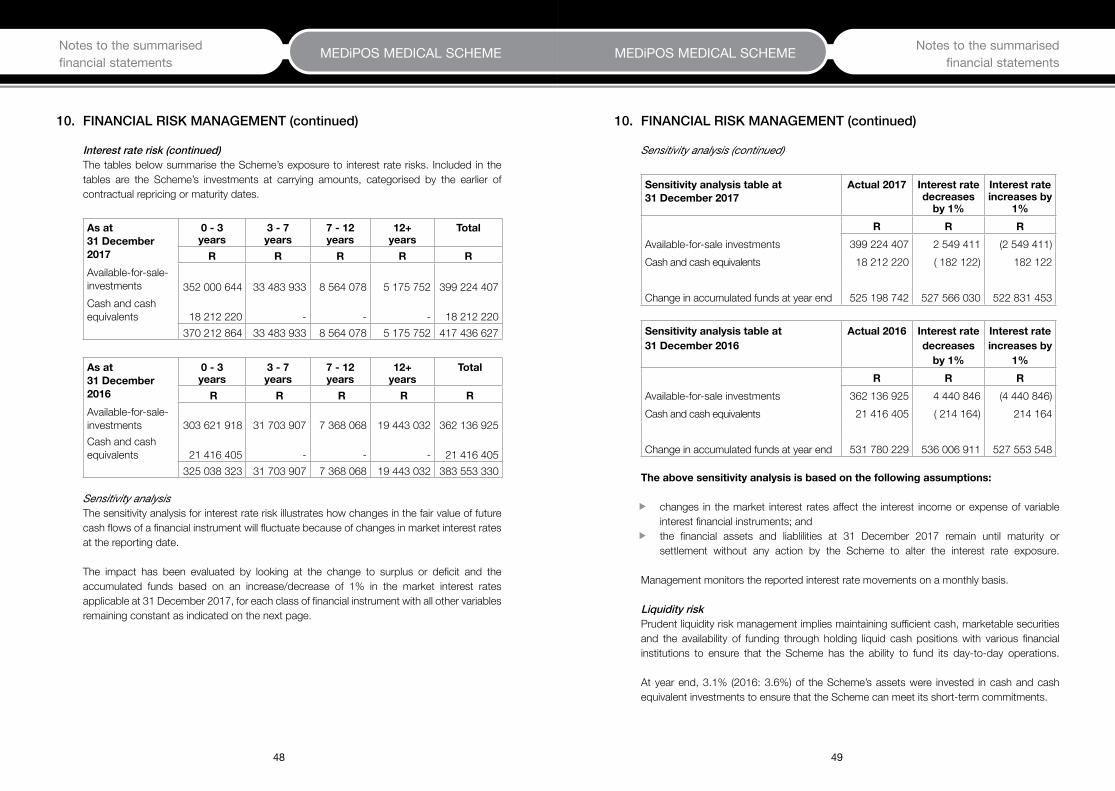

The Scheme is exposed to a range of financial risks through its financial assets, financial liabilities and insurance liabilities. In particular, the key financial risk is that the Scheme’s investment performance is not sufficient to maintain the solvency ratio, or that the Scheme should increase member contributions due to insufficient investment performance. The most significant components of this financial risk are interest rate risk, equity price risk and credit risk.

7. RELATED PARTY DISCLOSURES (continued)

These risks arise from open positions in interest rate and equity risk products, both of which are exposed to general and specific market movements.