november 2017 - indigrid · information purposes only without regards to specific objectives, ......

TRANSCRIPT

I n v e s t o r P resentat ion

November 2017

1

Th is presentation is prepared and issued by Sterlite Investment Managers Limited (the “Investment Manager”) on behalf of and in its capacity as the investment manager of India Grid Trust (“IndiGrid”) for general

information purposes only without regards to specific objectives, financial situations or needs of any particular person and should not be construed as legal, tax, investment or other advice.

This presentation is not a prospectus, a statement in lieu of a prospectus, an offering circular, an offering memorandum, an advertisement, an offer or an offer document under the Companies Act, 2013, the Securities

and Exchange Board of India (Infrastructure Investment Trusts) Regulations, 2014, as amended, or any other applicable law in India. Th is presentation does not constitute or form part of and should not be construed

as, directly or indirectly, any offer or invitation or inducement to sell or issue or an offer, or any solicitation of any offer, to purchase or sell any securities.

Th is presentation should not be considered as a recommendation that any person should subscribe for or purchase any securities of: (i) IndiGrid or its portfolio assets (being, Sterlite Grid 1 Limited, Bhopal Dhule

Transmission Company Limited and Jabalpur Transmission Company Limited) (collectively, the “IndiGrid Group”), or (ii) its Sponsor (being Sterlite Power Grid Ventures Limited) or subsidiaries of the Sponsor

(collectively, the “Sponsor Entities”), and should not be used as a basis for any investment decision.

Unless otherwise stated in this presentation, the information contained herein is based on management information and estimates. The information contained in this presentation is only current as of its date, unless

specified otherwise, and has not been independently verified. Please note that, you will not be updated in the event the information in the presentation becomes stale. Th is presentation comprises information given in

summary form and does not purport to be complete and it cannot be guaranteed that such information is true and accurate. You must make your own assessment of the relevance, accuracy and adequacy of the

information contained in this presentation and must make such independent investigation as you may consider necessary or appropriate for such purpose. Moreover, no express or implied representation or warranty is

made as to, and no reliance should be placed on, the accuracy, fairness or completeness of the information presented or contained in this presentation. Further, past performance is not necessarily indicative of future

results. Any opinions expressed in this presentation or the contents of this presentation are subject to change without notice.

None of the IndiGrid Group or the Sponsor Entities or the Investment Manager or the Axis Trustee Company Limited or any of their respective affiliates, advisers or representatives accept any liability whatsoever for

any loss howsoever arising from any information presented or contained in this presentation. Furthermore, no person is authorized to give any information or make any representation which is not contained in, or is

inconsistent with, this presentation. Any such extraneous or inconsistent information or representation, if given or made, should not be relied upon as having been authorized by or on behalf of the IndiGrid Group or

the Sponsor Entities.

The distribution of this presentation in certain jurisdictions may be restricted by law. Accordingly, any persons in possession of this presentation should inform themselves about and observe any such restrictions. Th is

presentation contains certain statements of future expectations and other forward-looking statements, including those relating to IndiGrid Group’s general business plans and strategy, its future financial condition and

growth prospects, and future developments in its sectors and its competitive and regulatory environment. In addition to statements which are forward looking by reason of context, the words ‘may’, ‘will’, ‘should’,

‘expects’, ‘plans’, ‘intends’, ‘anticipates’, ‘believes’, ‘estimates’, ‘predicts’, ‘potential’ or ‘continue’ and similar expressions identify forward- looking statements.

By their nature, forward-looking statements involve risks and uncertainties because they relate to events and depend on circumstances that may or may not occur in the future. Forward-looking statements are not

guarantees of future performance including those relating to general business plans and strategy, future outlook and growth prospects, and future developments in its businesses and its competitive and regulatory

environment. No representation, warranty or undertaking, express or implied, is made or assurance given that such statements, views, projections or forecasts, if any, are correct or that the any objectives specified

herein will be achieved. All forward-looking statements are subject to risks, uncertainties and assumptions that could cause actual results, performances or events to differ materially from the results contemplated by

the relevant forward looking statement. The factors which may affect the results contemplated by the forward-looking statements could include, among others, future changes or developments in (i) the IndiGrid

Group’s business, (ii) the IndiGrid Group’s regulatory and competitive environment, (iii) the power transmission sector, and (iv) political, economic, legal and social conditions. Given the risks, uncertainties and other

factors, viewers of this presentation are cautioned not to place undue reliance on these forward-looking statements.

2

Disclaimer

2

I nves to r

P resentation

November 2017

3

Index

1. Introduction

2. Vision & Strategy

3. Regulatory Framework and Corporate Governance

4. Growth Strategy

5. Proposed acquisition and transaction structure

6. Q2 FY18 performance

7. Appendix

I n t roduct ion

4

IndiGrid - India’s Fi rs t Power Sector InvIT

5

•Owns inter-state high voltage power transmission assets

•Ful ly operational and revenue generating portfolio

•Focused on stable & sustainable distribution

•Strong growth pipeline with ROFO on Sponsor assets

~ INR 37.4 BN*Asset under Management

1,936 circuit KM

6 , 0 0 0 MVA

AAA Rated

Perpetual Ownership

Two Project SPVs 8 Lines and 2 substations 33 years of residual contract life#

Notes: *Based on EV in the independent valuation report as of 30 Sep 2017#Remaining TSA contractual life of 33 years. However, the projects are built on BOOM model and have perpetual ownership for the owner

IndiGrid – High Quality Assets

6

IndiGrid – Key Stakeholders

7

~20.7% ~79.3%

I nd iGr id V i s ion

8

To become the most admired yield vehicle in Asia which is built

upon solid fundamentals of transparency, governance & providing

superior risk-adjusted returns to unitholders

INR 3 0 0 B N

AUM b y 2 0 2 2

Deliver

predictable

D P U and

growth

B e st-in-class

corporate

governance

IndiGrid Strategy

9

Focused Business

Model

Value Accretive

Growth

Optimal Capital

Structure

Maximize

Distribution

Focus on owning power transmission assets with

• long termcontracts

• low operatingrisks

• stable cash flows

• Minimum 90% net

cash to be

distributed

• Quarterly

distribution to the

unitholders

• 3-5% DPU growth

YoY

• Acquire assets from

Sponsor under ROFO

• Acquire third party

assets

• Cap of 49%

consolidated leverage

of total asset value

• Appropriate risk

policies in place

Regulatory Framework and Strong Governance

10

Distribution and borrowings

At least 90% of net distributable cash flows of the InvIT

to be distributed

Net consolidated borrowing capped at 49% of the

value of InvIT assets

Independent Board

At least 50% of the board of directors of Investment

Manager to be independent and should not be

directors or members of the governing board of

another InvIT

Governance

100% Independent Directors on Investment Committee

Independent Valuers and Advisors

Sponsor to own minimum 15% units of Indigrid for a

minimum period of three years

Sponsor can not vote in Related party Transactions

(RPTs)

Unitholder Rights

Majority vote is essential for all RPTs and exceeding 5%

of asset value

Any debt raising beyond 25% of asset value also require

unitholder vote

Growth

S t ra tegy

1112

Growth

S t ra tegy

1213

Growth

S t ra tegy

13

Strong pipeline of existing Sponsor Assets

© INDIGRID 14

2 x 400 kV D/C lines

Commissioned

909 ckms

INR 1,420 Mn

East North Interconnecti

on Ltd(ENICL)

NRSS XXIX Transmission

Ltd (NTL)

Odisha Generation

PhaseTransmission Ltd (OGPTL)

3x400 kV D/C lines,

1x400/220 kV D/C GIS sub-

station

Oct 2018

887 ckms

INR 5,030 Mn

1x765 kV D/C line, 1x400 kV

D/C line

Aug 2019

715 ckms

INR 1,590 Mn

Overview

Scheduled COD

Length

Revenues (5 yr. avg.)

Gurgaon-Palwal

TransmissionLtd (GPTL)

5x400kV D/C lines and

3x400/220 kV substations

Sep 2019

271 ckms

INR 1,440 Mn

KhargoneTransmission

Ltd (KTL)

2x765 kV D/C lines, 1x400 kV

D/C lineand 1x765/400 kV substation

Jul 2019

624 ckms

INR 1,860 Mn

NER-II Transmission

Limited

2x400 kV D/C lines, 2x132 kV

D/C linesand 2x400/132 kV substations

Nov 2020

900 ckms

INR 4,520 Mn

2 x 400 kV D/C lines

Commissioned

546 ckms

INR 750 Mn

Purulia & Kharagpur

Transmission Company Ltd (PKTCL)

RAPP Transmission Company Ltd (RTCL)

MaheshwaramTransmission

Ltd (MTL)

1x400/220 kV D/C line

Commissioned

403 ckms

INR 460 Mn

2 x 400 kV D/C lines

477 ckms

INR 580 Mn

Proposed Acquisition

* Actual COD Q3 FY18

June 2018*

© INDIGRID 15

Revenue 5 yr. average (INR billion)

4.4

22.1

FY18 FY22

BDTCL

JTCL

RTCL

PKTCL

MTL

ENICL

NTL

OGPTL

GPTL

KTL

NER-II

Visibi l i ty of 4x revenue growth in next 5 years from sponsor

assets

Further growth potential from near term bids…

16

Name of Tender Stage of Tender Location Estimated Cost (INR billion)

WR-NR Interconnection RFP UP, MP 9.1

GTTPL Goa Bids Results Awaited Goa, Karnataka, Chhattisgarh 11.0

Ultra Mega Solar Park in Fatehgarh RFQ Rajasthan 5.4

Connectivity and LTA to HPPCL RFQ Himachal Pradesh 3.2

Strengthening in Jharkhand (Package 1) RFQ Jharkhand 9.8

Strengthening in Jharkhand (Package 2) RFQ Jharkhand 10.8

Strengthening in Jharkhand (Package 3) RFQ Jharkhand 9.5

Strengthening in Jharkhand (Package 4) RFQ Jharkhand 10.3

Strengthening in Jharkhand (Package 5) RFQ Jharkhand 11.4

Connectivity System for LVTPPL + S.S. RFQ Maharashtra, MP 7.4

ISTS Feed to Navi Mumbai Pipeline Maharashtra 5.4

New Substation near Vapi area Pipeline Gujarat 3.6

Additional 400 kV outlets from Banaskantha Pipeline Gujarat 0.6

Total 97.5

Current Inter-State and Intra-state TBCB tenders

55,350

91,250

FY16 FY 22

Inter regional transmission capacity to increase significantly

Supported by structural growth in the sector

(MW)

61%38%

20%33%

19% 29%

FY 2012–16 FY 2017–21

Generation Transmission Distribution

US$149bn US$134-142bn

Share of transmission sector to grow 1.7x of total power sector investment

17

Key Drivers for growth:• Significant past under investment in transmission as

compared to generation

• Widening gap between load centers & generation centers

across regions

• Improving financial health of DISCOMs through UDAY and

other such scheme

• Staggering growth in renewable energy: 175 GW capacity

by 2022

• Strong govt. focus though initiatives such as “Power for All”

Increased Private Participation:

• All bids to be routed through TBCB process

• In the 13th year plan (2017-21), share of private player

investments in the new bids of transmission lines is expectedto be over 50%.

~US$ 46 billion investment in power transmission sector over next five years

P roposed

acqu i s i t ion and

t ransact ion

s t ruc tu re

18

Acquisition of sponsor assets

19

Acquisition of 3 ROFO assets in FY 18, subjectto customary regulatory and unitholders’approval

3,361 circuit kms

(+75%)

Presence in 8 states

across India (+ 4 states)

1,936 circuit kms

Presence in 4 states

across India

AUM: ~INR 52 billion

(+40%)

AUM: INR 37.4 billion

Proposed acquisition to result in a diversified transmission portfolio

RTCL

MTL

PKTCL

Purlia

Kota

Shujalpur

Yeddumailaram

Mehboobnagar

Kharagpur

Mehesshwaram

Nizamabad

Ranchi

Chaibasa

BDTCL

JTCL

IPO assets

ROFO Assets to be injected

Today Post acquisition

Indicative valuation and proposed acquisit ion consideration

© INDIGRID 20

Source: independent valuation report from Haribhakti & Co. LLP., a member firm of Baker Tilly International

Independent valuation and acquisition consideration

Asset

Enterprise Value as per

independent valuation

(INR mn)

Acquisition consideration

(INR mn)

Premium / (Discount) to

Independent valuation

RTCL 3,935 3,738 (5.0%)

PKTCL 6,512 6,186 (5.0%)

MTL* 5,218 4,957 (5.0%)

Total 15,666 14,881 (5.0%)

IndiGrid will acquire the three ROFO assets at 5% discount to independent valuation

Value accretive acquisition

21

9.2 11 11 11

FY18* FY18 FY19 FY20

11.44

Full year

11.44

0.44 0.44

* For 10 months (excluding ROFO)

Indicative DPU (INR/unit)

11.00

• First acquisition by IndiGrid of ROFO assets worth INR 14.9billion

• Assets to be acquired at a discount of 5% to enterprisevaluation calculated by an Independent Valuer,Haribhakti & Co. LLP., a member firm of Baker TillyInternational

• Acquisition to be funded entirely by raising debt atIndiGrid or SPV level; debt tenure to be 10-15 years

• Acquisition leads to IndiGrid annualised DPU increasefrom INR 11/unit to INR 11.44/unit that is in line with the

guidance (3-5% DPU increase p.a.)

Acquisition in line with IndiGrid Strategy

22

Focused Business

Model

Value Accretive

Growth

Optimal Capital

Structure

Maximize

Distribution

~34 years of residual

tenure

Interstate

transmission assets

under PoC

mechanism

Avg. availability

since COD: 99.83%*

Distribution from the

assets to be

consistent with

existing distribution

policy

Annualized DPU to

increase by 4% in

line with the

guidance of 3-5%

annualized DPU

growth

Investment to be

financed through

debt by utilizing the

available

headroom up to

49% cap

* Average availability for RTCL and PKTCL since COD

.

Sterlite Grid 1 Limited (“SGL1”)

RTCL PKTCL

Sponsor

(through SGL3)*

49%

51%

100%100%

100%100%

IndiGrid’s structure post acquisit ion

© INDIGRID 23

IndiGrid structure post acquisition

Assets to be acquired directly under IndiGrid

Assets

proposed for

acquisition

IPO Assets

Note: Acquisition of 49% due to equity lock in restrictions as per the TSA (IndiGrid will have option to acquire remaining 51% post expiry of the lock in restriction –

(i)24% to be released post 2 years from COD and (ii)26% after another 3 years)

* SGL3 is the immediate holding company of MTL

JTCLBDTCL

MTL

Overview of the f inancing structure

© INDIGRID 24

Proposed funding mechanism Key terms of debt

Rated, Senior, Secured Non

Convertible debentures* /

other debt

Long tenure (10-15 years)

In line with current interest rate

of existing assets

Acquisition to be funded entirely by debt at IndiGrid or SPV level

Debt to be secured against the cash flows of the underlying assets

Possibility of issuing NCDs subject to SEBI notification* on issuance of debt security at InvIT level before the transaction closure timeline

Alternatively, IndiGrid to evaluate mix of NCDs and bank loan

* SEBI has recently allowed InvITs /REITs to issue debt securities (notification yet to come)

Instrument

Issue amount

Tenure

Coupon

Up to the acquisition amount

Expected timeline

25

Completed Future actions

September 2017

October 2017

1st week -November

2017

3rd week -November

2017

November 2017 /

January 2018

Due diligence of assets

Independent valuation

Financing arrangement

Unitholder and other regulatory

approvals for the

transaction

Transaction Closure

Board approval for the transactions

Finalization of definitive

agreements

Q2 FY18

per fo rmance

26

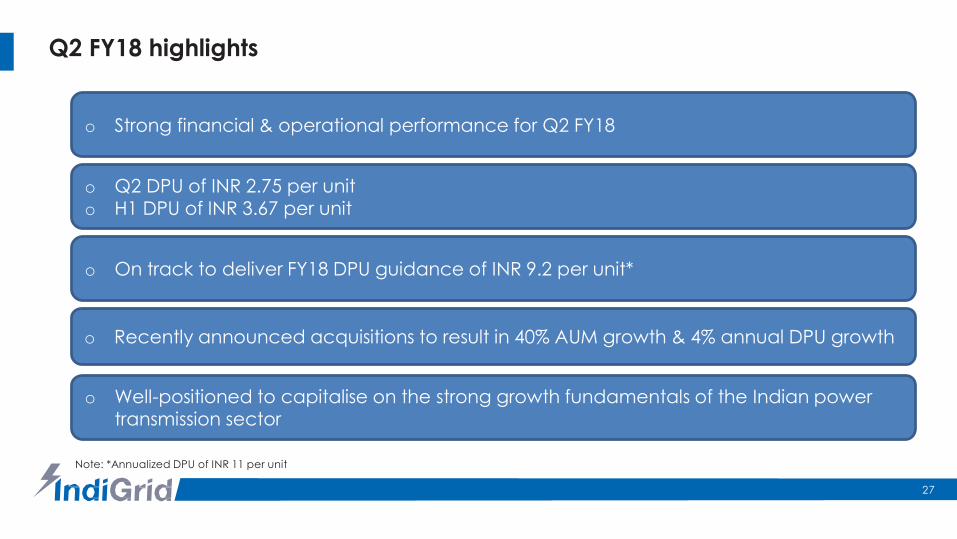

Q2 FY18 highlights

o Strong financial & operational performance for Q2 FY18

o Q2 DPU of INR 2.75 per unito H1 DPU of INR 3.67 per unit

o Recently announced acquisitions to result in 40% AUM growth & 4% annual DPU growth

o Well-positioned to capitalise on the strong growth fundamentals of the Indian power transmission sector

27

o On track to deliver FY18 DPU guidance of INR 9.2 per unit*

Note: *Annualized DPU of INR 11 per unit

Operational performance

© INDIGRID 28

Avg. availability (since COD) : 99.7% Avg. availability (YTD FY 18) : 99.9%

* Estimates for month of September’17

BDTCL JTCL

Continue to deliver robust operational efficiency

98% 98% 98% 98%

1.6% 1.8% 1.8% 1.9%

99.6% 99.8% 99.8% 99.9%

FY 16 FY 17 Q1 FY18 Q2 FY18*

98% 98% 98% 98%

1.8% 1.9% 1.7% 1.8%

99.8% 99.9% 99.7% 99.8%

FY 16 FY 17 Q1 FY18 Q2 FY18*

Avg. availability (since COD) : 99.8% Avg. availability (YTD FY 18) : 99.7%

Financial performance

Financial performance in line with IndiGrid’s strategy of stable cash flows while maintaining optimal capital structure

29

Consolidated

Financials -

IndiGrid (INR Mn)

Q1 FY18One month of operations

Q2 FY18Full Quarter of operations

H1 FY18Four months of operations

Revenue 406 1,323 1,729

EBITDA 369 1,223 1,592

NDCF 258 1,014 1,272

Net debt to AUM: ~23%

NDCF

Q2 FY18 Net Distributable Cash Flow (at IndiGrid in INR million)

30

H1 FY18 Net Distributable Cash Flow (at IndiGrid in INR million)

Appendix

31

Overv iew of

the

acquis i t ion

assets

32

R A P P Transmission Company Limited ( R T C L )

RAPP Transmission Company Limited

Overview

• Project was set up to transfer power from the atomic power

plant near Kota in Rajasthan to Shujalpur in Madhya Pradesh to

provide the path for the evacuation of electricity generated at

RAPP-7 and8

• The network will act as an interregional link between the Northern

and the Western region

• RAPP would help in evacuation of power even in case of any grid

constraints in the Northern region

Description• Project scope involves establishment and operation of one

400kV Double Circuit transmission line

Key dates

and tenure

• Initial tenure period of 35 years (residual tenure of 33.5 years)

• TSA signed on: July 24, 2013

• Scheduled COD: March 1, 2016

• Actual COD: February 26, 2016

• Injection into POC: March 1, 2016

Lead LTTC • UP Power Corporation Limited

Lines Route Length Specifications Location Status

RAPP- Shujalpur 403 cKms 4 0 0 kVD/C Rajasthan,

MadhyaPradesh

Operational

© INDIGRID 33

Purulia & Kharagpur Transmission Company Limited ( P K T C L )

Purulia & Kharagpur Transmission Company Limited

Overview

• Connecting link further strengthening the interconnection

between the West Bengal state grid and ISTS to strengthen

the transmission system in the Indian states of West Bengal and

Jharkhand

Description

• 4 0 0 kV substation at Kharagpur of West Bengal State

Electricity Transmission Company Limited (WBSETCL) has been

commissioned with LILO of Kolaghat-Baripada line.

• Chaibasa substation of Powergrid is under implementation with

LILO of both circuits of Jamshedpur-Rourkela line

• Ranchi 4 0 0 kV substation is a sub-station in Eastern Region grid

and also one of the gateways for power exchange with Western

Region Grid

Key dates

and tenure

• Initial tenure period of 35 years (residual tenure of 34.5 years)

• TSA signed on: August 6, 2013

• Scheduled COD: April 2016

• Actual COD: June 18, 2016 (KC Line), Jan 7, 2017 (PR Line)

• Injection into POC: June 18, 2016 (KC Line), Jan 7, 2017 (PR Line)

Lead LTTC • Bihar State Electricity Board

Lines Route Length Specifications Location Status

Kharagpur – Chaibasa 322 cKms 4 0 0 kVD/C West Bengal,

Jharkhand

Operational

Purulia – Ranchi 223 cKms 4 0 0 kVD/C West Bengal,

Jharkhand

Operational

© INDIGRID 34

Maheshwaram Transmission Limited (MTL)

Maheshwaram Transmission Limited

Overview

• Maheshwaram Transmission Limited (MTL) will create a key

component to enable Southern region to draw more power from

North-East-West (NEW) Grid and address the issue of power

stability in Telangana region to a great extent

• The improved grid connectivity shall facilitate power procurement

from the I STS network to

the beneficiary states Telangana, Tamil Nadu, Seemandhra and

Karnataka to meet their electricity demands

Description• Project envisaged to provide grid connectivity for

Maheshwaram 765/400 kV Pooling Substation and Nizamabad

765/400 kV Substation

Key dates

and tenure

• Initial tenure period of 35 years (residual tenure of 35 years)

• TSA signed on: June 10, 2015

• Scheduled COD: June 2018

Lead LTTC • TANGEDCO

Lines Route Length Specifica

tions

Location Status

Maheshwaram (PG) – Mehboob Nagar 199 cKms 4 0 0 kV

D/C

Telangana Expected COD: Q3

FY 2018

Ni z a m a b a d – Yeddumailaram(Shankarpal l i )

278 cKms 4 0 0 kV

D/C

Telangana Commissioned in

September 2017

© INDIGRID 35

Annual tariffs

© INDIGRID 36

0

500

1,000

1,500

2,000

2,500

FY18

FY19

FY20

FY21

FY22

FY23

FY24

FY25

FY26

FY27

FY28

FY29

FY30

FY31

FY32

FY33

FY34

FY35

FY36

FY37

FY38

FY39

FY40

FY41

FY42

FY43

FY44

FY45

FY46

FY47

FY48

FY49

INR

Cro

re

Revenue (ROFO and Non ROFO)

Non ROFO ROFO IPAs

Glossary

© INDIGRID 37

Availability The percentage amount of time for which the asset i s available for power flow

BDTCL Bhopal Dhule Transmission Company Limited

DPU Distribution Per Unit (DPU) i s cash paid to the Unitholders in the form of interest/ capital repayment / dividend

IPA Initial Portfolio Assets (IPAs) refers to BDTCL and JTCL which were acquired by IndiGrid at the time of IPO

ISTS Inter-State Transmission System

JTCL Jabalpur Transmission Company Limited

MTL Maheshwaram Transmission Limited

NDCFNet Distributable Cash Flow (NDCF) i s the net cash flow that the trust has at it’s disposal for distribution to IndiGrid in

a particular year in accordance with the formula defined in the Offer Document

O&M Operations and Maintenance (O&M) cost

PKTCL Purulia Kharagpur Transmission Company Limited

ROFO Right Of F i r s t Offer

RTCL RAPP Transmission Company Limited

Tariff

Composed of Non-Escalable, Escalable and Incentive component. The incentive component i s based on the availability of

the asset = 2*(Annual Availability – 98%)*(Escalable + Non-escalable); incentive i s maximum 3.5% of (Escalable+Non-

escalable tariff)

TBCB Tariff Based Competitive Bidding

YoY Year on year

Thank You