nsaa it conference outsourcing audit services: virginia’s privatization study...

TRANSCRIPT

NSAA IT Conference

http://www.apa.virginia.gov

Outsourcing Audit Services: Virginia’s Privatization Study

_____________________________________

October 2, 2013

Staci Henshaw, CPA

Deputy Auditor of Public Accounts

NSAA IT Conference

Presentation Goals

• Provide study background • Discuss study methodology• Summarize study results• Share lessons learned

http://www.apa.virginia.gov Page 2

NSAA IT Conference

Why did we perform this study?

http://www.apa.virginia.gov Page 3

NSAA IT Conference

Proposed Statutory Changes

A. The Auditor of Public Accounts shall audit all the accounts of every state department, officer, board, commission, institution or other agency handling any state funds. In the performance of such duties and the exercise of such powers he may employ shall procure the professional services of certified public accountants and auditing firms in accordance with the Virginia Public Procurement Act (§ 2.2-4300 et seq.), provided the cost thereof shall not exceed such sums as may be available out of the appropriation provided by law for the conduct of his office.

http://www.apa.virginia.gov Page 4

NSAA IT Conference

Where did the idea for this bill originate?

http://www.apa.virginia.gov Page 5

NSAA IT Conference

Why is privatization popular?

http://www.youtube.com/watch?v=Fcu_fnXoc_I

http://www.apa.virginia.gov Page 6

NSAA IT Conference

What did we do in response to this bill?

• Met with Chairman of General Government Subcommittee– Was about to become chair of our oversight entity

• Requested that if this moved forward that the effective date be changed– Would have become effective on July 1– Needed more time to contract for larger audits (CAFR /

Single Audit)

• Offered to perform a study surrounding moving forward with this proposal– Received formal request from both the patron and chairman

http://www.apa.virginia.gov Page 7

NSAA IT Conference

Why did we offer to perform a study?

• This is not the first time this has been proposed

• Legislation from previous year had resulted in some audits being outsourcing

• Provided a good opportunity to highlight ALL the services the APA provides

http://www.apa.virginia.gov Page 8

NSAA IT Conference

Independence Implications?

• Goal was to provide information to the General Assembly to use to make decision on the proposal

• Asked for input from our state society of CPAs (VSCPA) throughout the process

http://www.apa.virginia.gov Page 9

NSAA IT Conference

Items we were requested to cover in our study

http://www.apa.virginia.gov Page 10

NSAA IT Conference

Study Methodology and Sources of Information

• Developed a comprehensive list of all the audit and non-audit services we provide– Reviewed the Code of Virginia– Surveyed management team– Utilized our work plan reports– Analyzed hours by audit type

http://www.apa.virginia.gov Page 11

NSAA IT Conference

What are APA Products and Services

http://www.apa.virginia.gov Page 12

NSAA IT Conference

Other Activities

• Code mandated calculations– Rainy day and local fines & fees reversion

• Comparative Report of Local Government • Commonwealth Data Point• Oversight of firms auditing local governments• Fraud investigations• Provide information to General Assembly

members and staff

http://www.apa.virginia.gov Page 13

NSAA IT Conference

Study Methodology and Sources of Information

• Gathered data on our operations– Expenses, staff, and number of reports

issued for five year period• Requested information from VSCPA

– Number of firms in Virginia in applicable practice areas based on their peer review program

http://www.apa.virginia.gov Page 14

NSAA IT Conference

APA Operational Data

http://www.apa.virginia.gov Page 15

NSAA IT Conference

130 Active Firms Practiced in Virginia in Related Practice Areas

http://www.apa.virginia.gov Page 16

NSAA IT Conference

Study Methodology and Sources of Information

• Utilized procurement data from recently outsourced audits– Primarily to determine rates

• Interviewed other states• NSAA

– Auditing in the States– Contacts in other states

http://www.apa.virginia.gov Page 17

NSAA IT Conference

Interviews with other states

• Developed interview template with 20 questions– Extent of outsourcing– Contracting process– Contract monitoring / quality control– Costs– Availability of firms– Pros and cons

http://www.apa.virginia.gov Page 18

NSAA IT Conference

Extent of Privatization in Other States

http://www.apa.virginia.gov Page 19

NSAA IT Conference

Models Used by States Interviewed

http://www.apa.virginia.gov Page 20

NSAA IT Conference

VSCPA Input

• Had several meetings– Planning Phase– Report Phase

• They did not provide a formal response since we made changes to the report to address their comments - we noted this in our report

http://www.apa.virginia.gov Page 21

NSAA IT Conference

Study Results

• Report provided information from the original request

• Provided decision considerations and related decision points for the General Assembly to address when evaluating the different options associated with outsourcing– Decision considerations included information that

was pertinent to the corresponding decision point and also included some “recommendations”

http://www.apa.virginia.gov Page 22

NSAA IT Conference

Key Points

• Recommended prior to moving forward the General Assembly first determine its overall objective for outsourcing

• Would help to provide a context for considering the various decision points, as some may not be relevant, depending on the objective

• Noted there were interdependencies between the various decisions points; therefore, they should not be addressed singularly

http://www.apa.virginia.gov Page 23

NSAA IT Conference

Key Points – Other Services

• Outsourcing could result in APA losing the depth of knowledge needed to advise the General Assembly– High risk areas– Impact of new accounting and auditing requirements

Information Technology projects

• Would be more difficult for us to maintain Commonwealth Data Point – We obtain and validate data as part of audit process– Responding to inquiries

http://www.apa.virginia.gov Page 24

NSAA IT Conference

Key Points – Legislative Oversight

• Recommended that the legislature retain responsibility for audit oversight– Helps to mitigate some of the risks – Provides separation of hiring function from

management (most agencies do not have oversight boards)

http://www.apa.virginia.gov Page 25

NSAA IT Conference

Key Points – Legislative Oversight

• Recommended Model 2 as the governance structure– State Auditor would oversee the contracting

process - hiring and quality assurance monitoring– Model allows for economies of scale relating to the

contracting function– Model best promotes accountability and

independence– Model helps ensure audit quality

http://www.apa.virginia.gov Page 26

NSAA IT Conference

Key Points – Outsourcing Alternatives

• Pointed out challenges in performing CAFR and Single Audits– Coordination required among different agencies

and auditing firms – Decentralized operating environment and internal

control structure in the Commonwealth – 80% of states either fully or partially perform these

audits – We provide a separate report for each agency or

Secretarial (included budget to actual data)

http://www.apa.virginia.gov Page 27

NSAA IT Conference

Key Points - Risks Identified

• State auditors focus on accountability (vs. profit motive of firms)

• Substantive vs. Internal Control Approaches

• We have extensive knowledge on Government

• Audit quality issues (National Single Audit Sampling Project)

http://www.apa.virginia.gov Page 28

NSAA IT Conference

Key Points - Benefits Identified

• Easier to manage staffing shortages and geographic challenges

• Large firms benefit from technical support /expertise from national offices

• May provide a “fresh” look at the entity• Outsourcing gives State auditors more

time to focus on special projects

http://www.apa.virginia.gov Page 29

NSAA IT Conference

Key Points - Transition

• Pointed out benefits of a phased-in approach– Firms may need to increase staffing and obtain

training related to government auditing– APA needs sufficient staff and processes in place

to perform the contracting and monitoring functions

http://www.apa.virginia.gov Page 30

NSAA IT Conference

Key Points – Audit Costs and Fiscal Impact

• Would need 25 staff if APA maintained oversight and some responsibilities

• Leaves approximately $8.2 million of $10.5 million budget

• Based on average rates from recent outsourcing, cost for entire work plan could be as high as $18.5 million

http://www.apa.virginia.gov Page 31

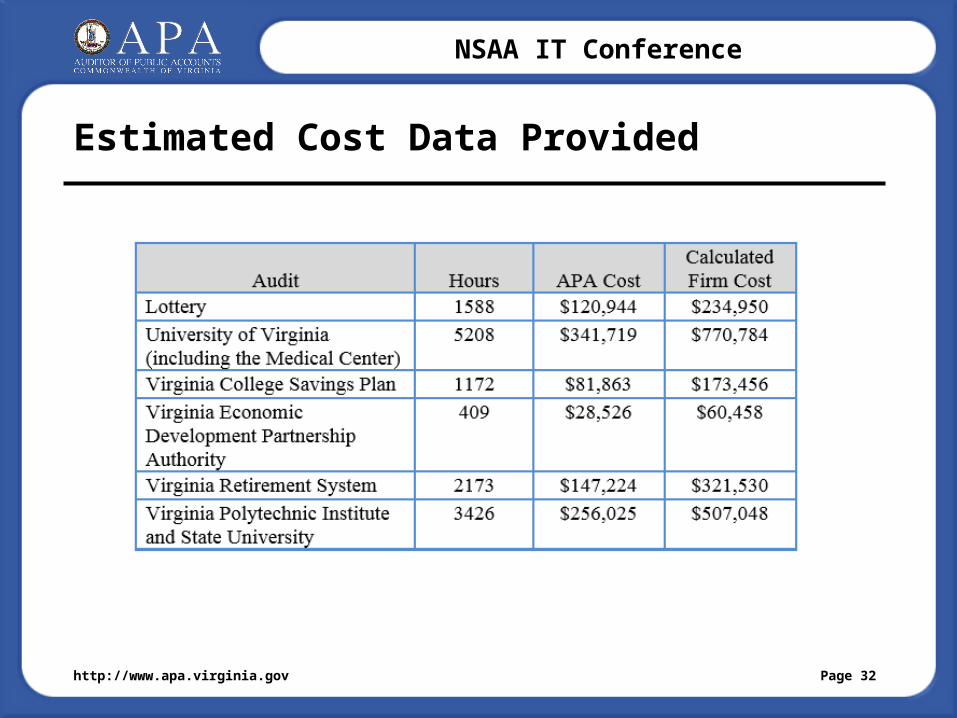

NSAA IT Conference

Estimated Cost Data Provided

http://www.apa.virginia.gov Page 32

NSAA IT Conference

Report Response – Patron of Original Bill

• Felt we should continue to perform the CAFR and Single Audit work

• Requested that we develop a list of other audits that could be outsourced and report back to him

• Communicated objective was to reduce costs

http://www.apa.virginia.gov Page 33

NSAA IT Conference

Report Response – Our Oversight Entity

• While presenting our annual work plan to our oversight entity we communicated the patron’s request

• Oversight entity felt there was already the opportunity for firms to propose to perform this work through our Public-Private Partnership process

http://www.apa.virginia.gov Page 34

NSAA IT Conference

Lessons Learned

• Be Competitive!– Innovation is important in being competitive

(reduces costs and helps to identify issues)– Keep track of the extras for comparison

purposes– Know how your staff spend their time and

set goals• Chargeable vs. non-chargeable

http://www.apa.virginia.gov Page 35

NSAA IT Conference

Lessons Learned

• Don’t turn down work!– But be careful to maintain independence

• Communicate all the services you provide!– We are now using our quarterly and annual

reports to better communicate this information

http://www.apa.virginia.gov Page 36

NSAA IT Conference

Lessons Learned

• Maintain relationships!– With State CPA Societies– With legislative members and staff– With NASACT / NSAA

http://www.apa.virginia.gov Page 37

NSAA IT Conference

Report Link and Hours

• www.apa.virginia.gov/reports/CPAFeasibilityRpt12-12.pdf

• Study actual hours = 175

http://www.apa.virginia.gov Page 38