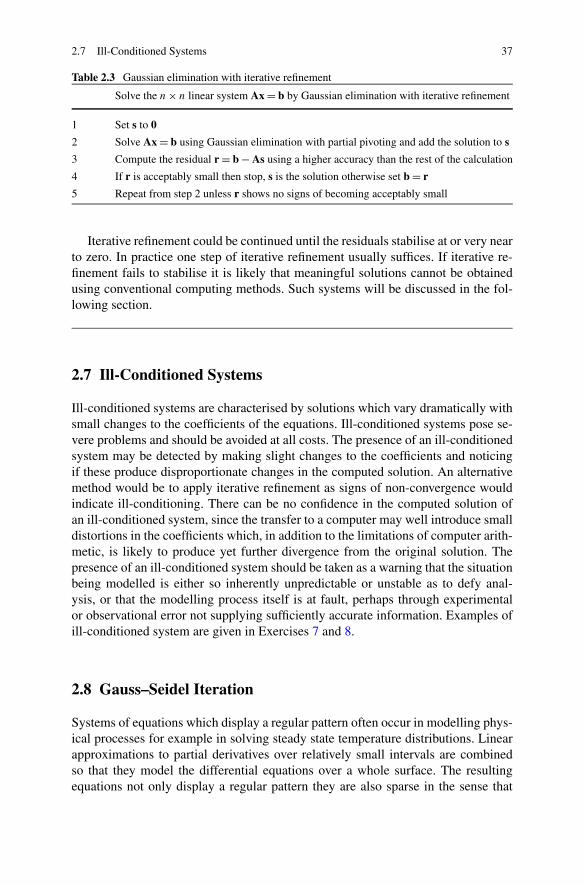

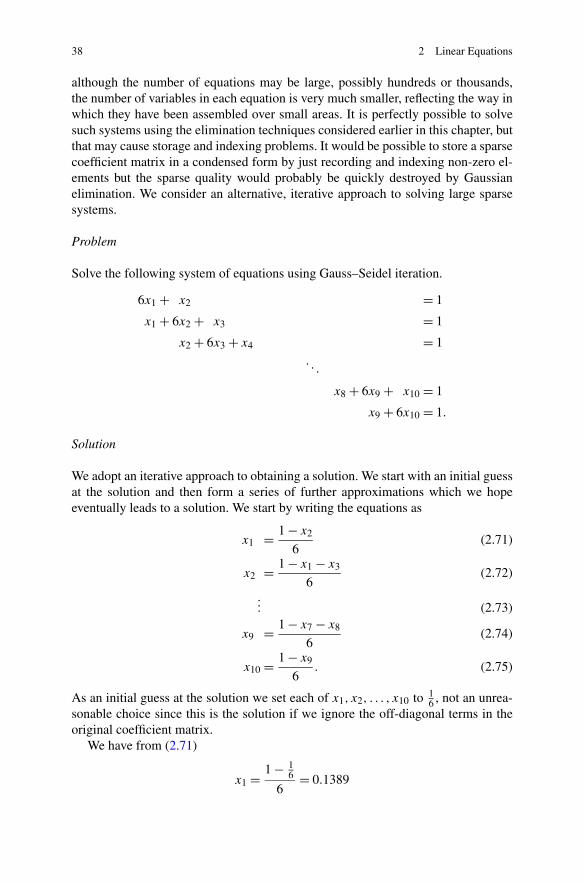

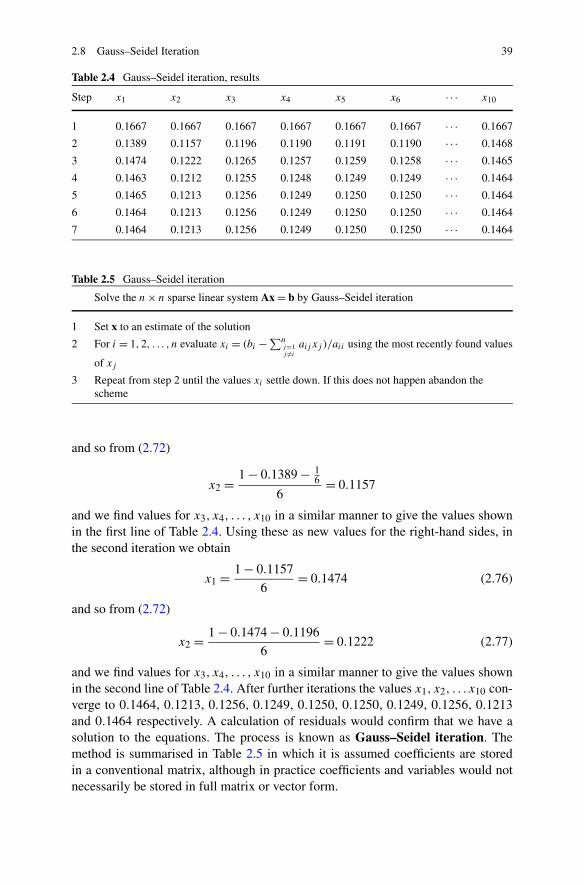

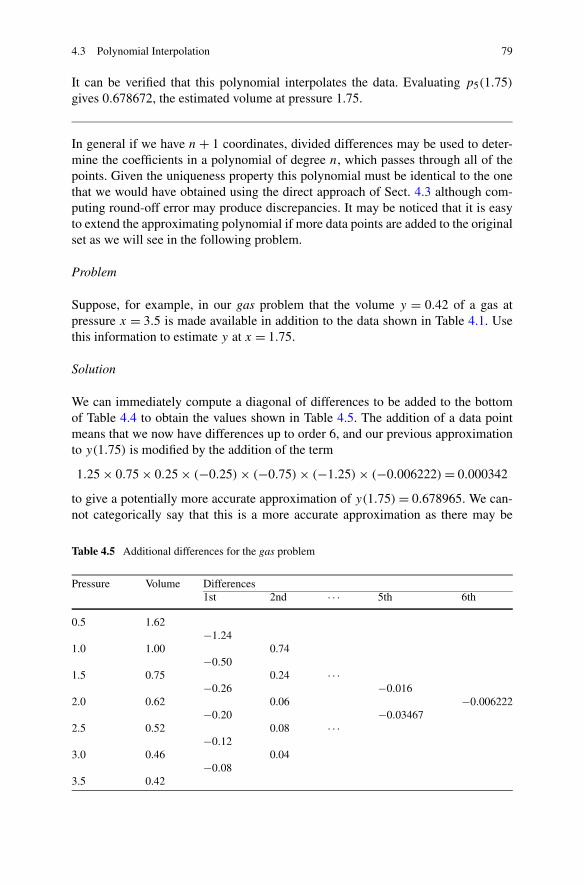

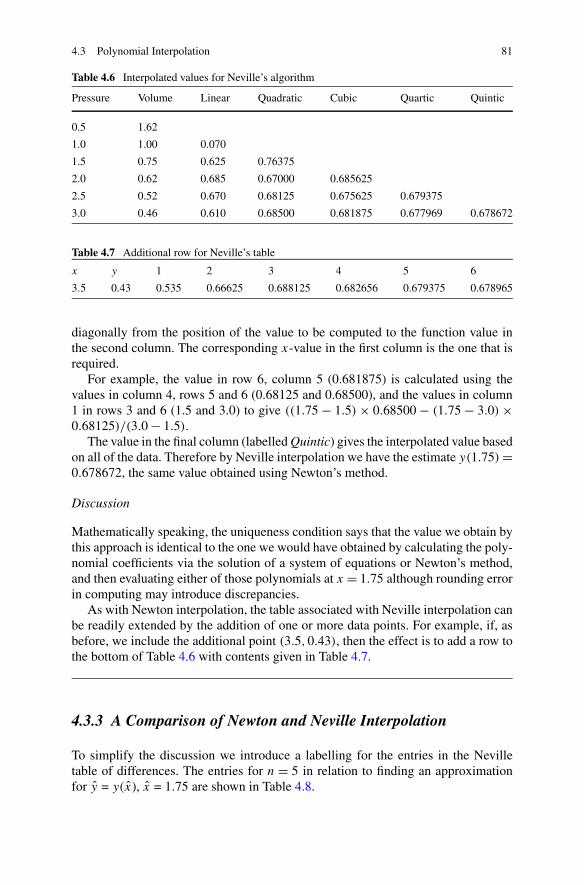

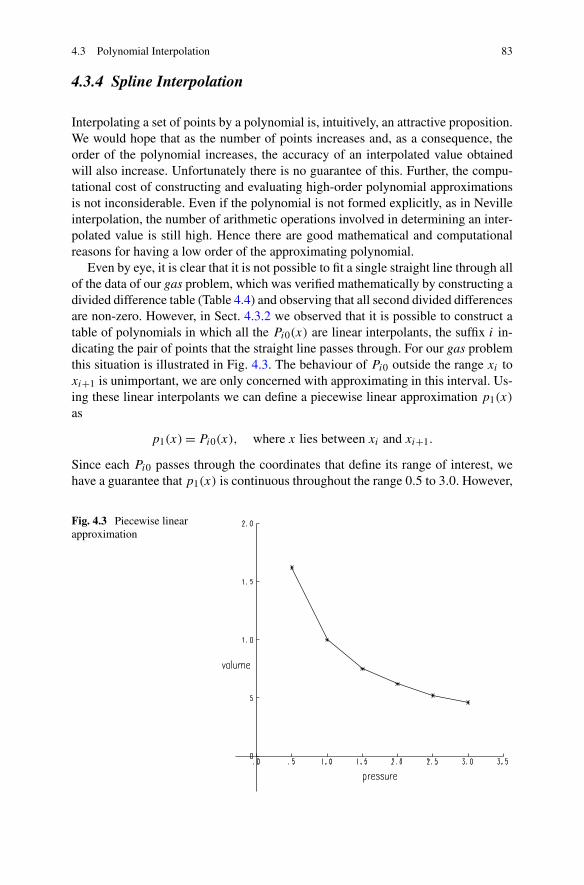

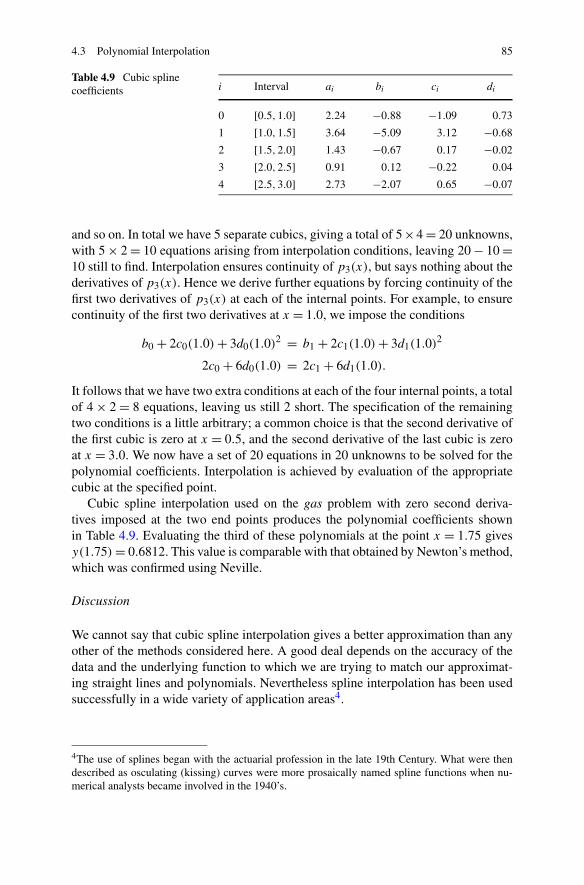

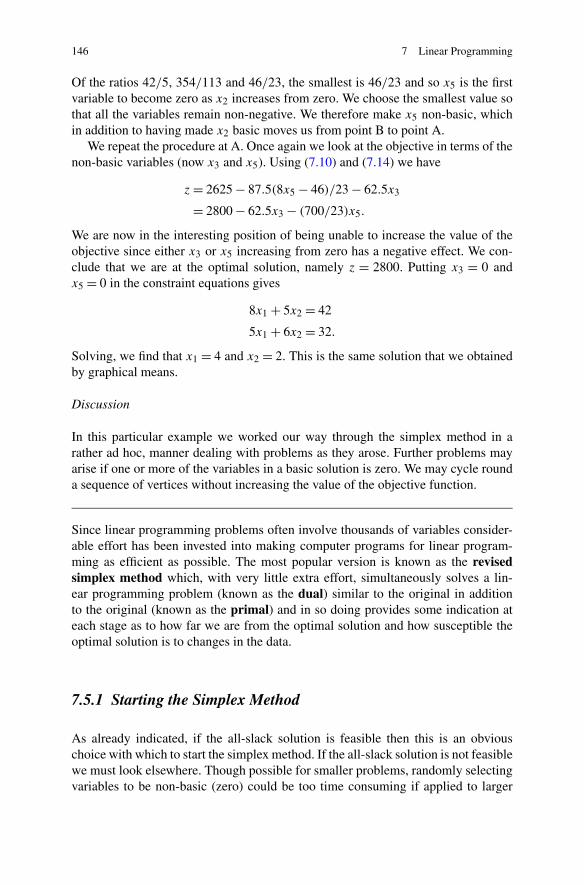

numerical methods with worked examples: matlab …vplab/downloads/opt/( ) c. woodford...numerical...

TRANSCRIPT

Numerical Methods with Worked Examples:Matlab Edition

C. Woodford � C. Phillips

Numerical Methodswith WorkedExamples:Matlab Edition

Second Edition

C. WoodfordDepartment of Computing ServiceNewcastle UniversityNewcastle upon Tyne, NE1 [email protected]

Prof. C. PhillipsSchool of Computing ScienceNewcastle UniversityNewcastle upon Tyne, NE1 7RUUK

Additional material to this book can be downloaded from http://extras.springer.com.

ISBN 978-94-007-1365-9 e-ISBN 978-94-007-1366-6DOI 10.1007/978-94-007-1366-6Springer Dordrecht Heidelberg London New York

Library of Congress Control Number: 2011937948

1st edition: © Chapman & Hall (as part of Springer SBM) 1997© Springer Science+Business Media B.V. 2012No part of this work may be reproduced, stored in a retrieval system, or transmitted in any form or byany means, electronic, mechanical, photocopying, microfilming, recording or otherwise, without writtenpermission from the Publisher, with the exception of any material supplied specifically for the purposeof being entered and executed on a computer system, for exclusive use by the purchaser of the work.

Cover design: deblik

Printed on acid-free paper

Springer is part of Springer Science+Business Media (www.springer.com)

Preface

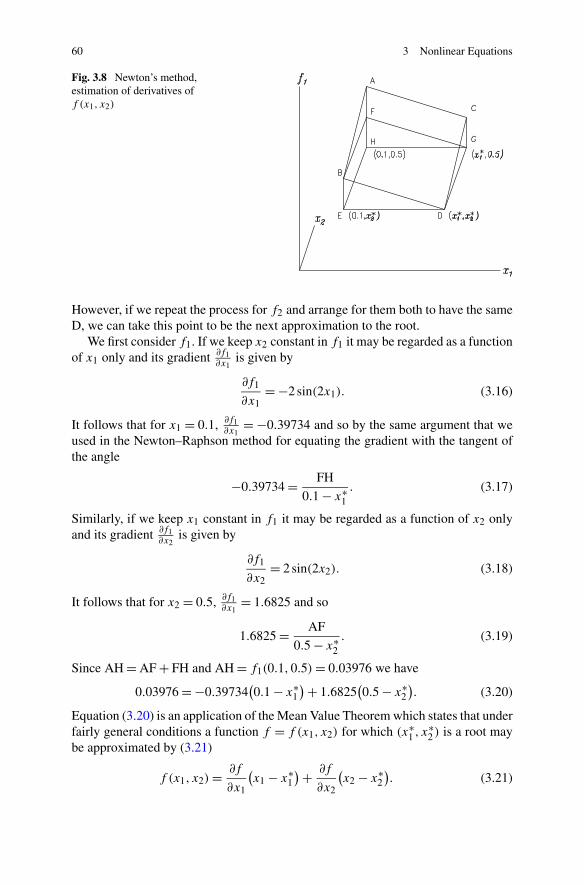

This book is a survey of the numerical methods that are common to undergraduatecourses in Science, Computing, Engineering and Technology. The aim is to presentsufficient methods to facilitate the numerical analysis of mathematical models likelyto be encountered in practice. Examples of such models include the linear equationsdescribing the stress on girders, bridges and other civil engineering structures, thedifferential equations of chemical and thermal reactions, and the inferences to bedrawn from observed data.

The book is written primarily for the student, experimental scientist and designengineer for whom it should provide a range of basic tools. The presentation isnovel in that mathematical justification follows rather than precedes the descriptionof any method. We encourage the reader first to gain a familiarity with a particularmethod through experiment. This is the approach we use when teaching this mate-rial in university courses. We feel it is a necessary precursor to understanding theunderlying mathematics. The aim at all times is to use the experience of numericalexperiment and a feel for the mathematics to apply numerical methods efficientlyand effectively.

Methods are presented in a problem–solution–discussion order. The solution maynot be the most elegant but it represents the one most likely to suggest itself on thebasis of preceding material. The ensuing discussion may well point the way to betterthings. Dwelling on practical issues we have avoided traditional problems havingneat, analytical solutions in favour of those drawn from more realistic modellingsituations which generally have no analytic solution.

It is accepted that the best way to learn is to teach. But even more so, the bestway to understand a mathematical procedure is to implement the method on a to-tally unforgiving computer. Matlab enables mathematics as it is written on paperto be transferred to a computer with unrivalled ease and so offers every encourage-ment. The book will show how programs for a wide range of problems from solvingequations to finding optimum solutions may be developed. However we are not rec-ommending re-inventing the wheel. Matlab provides an enormous range of ready touse programs. Our aim is to give insight into which programs to use, what may beexpected and how results are to be interpreted. To this end we will include details ofthe Matlab versions of the programs we develop and how they are to be employed.

v

vi Preface

We hope that readers will enjoy our book. It has been a refreshing experience toreverse the usual form of presentation. We have tried to simplify the mathematicsas far as possible, and to use inference and experience rather than formal proof as afirst step towards a deeper understanding. Numerical analysis is as much an art as ascience and like its best practitioners we should be prepared to pick and choose fromthe methods at our disposal to solve the problem at hand. Experience, a readiness toexperiment and not least a healthy scepticism when examining computer output arequalities to be encouraged.

Chris WoodfordChris Phillips

Newcastle University, Newcastle upon Tyne, UK

Contents

1 Basic Matlab . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11.1 Matlab—The History and the Product . . . . . . . . . . . . . . . . 11.2 Creating Variables and Using Basic Arithmetic . . . . . . . . . . . 21.3 Standard Functions . . . . . . . . . . . . . . . . . . . . . . . . . 21.4 Vectors and Matrices . . . . . . . . . . . . . . . . . . . . . . . . . 31.5 M-Files . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51.6 The colon Notation and the for Loop . . . . . . . . . . . . . . . . 61.7 The if Construct . . . . . . . . . . . . . . . . . . . . . . . . . . . 71.8 The while Loop . . . . . . . . . . . . . . . . . . . . . . . . . . . 81.9 Simple Screen Output . . . . . . . . . . . . . . . . . . . . . . . . 91.10 Keyboard Input . . . . . . . . . . . . . . . . . . . . . . . . . . . 91.11 User Defined Functions . . . . . . . . . . . . . . . . . . . . . . . 101.12 Basic Statistics . . . . . . . . . . . . . . . . . . . . . . . . . . . . 111.13 Plotting . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 111.14 Formatted Screen Output . . . . . . . . . . . . . . . . . . . . . . 121.15 File Input and Output . . . . . . . . . . . . . . . . . . . . . . . . 14

1.15.1 Formatted Output to a File . . . . . . . . . . . . . . . . . . 141.15.2 Formatted Input from a File . . . . . . . . . . . . . . . . . 141.15.3 Unformatted Input and Output (Saving and Retrieving Data) 15

2 Linear Equations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 172.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 182.2 Linear Systems . . . . . . . . . . . . . . . . . . . . . . . . . . . . 192.3 Gaussian Elimination . . . . . . . . . . . . . . . . . . . . . . . . 22

2.3.1 Row Interchanges . . . . . . . . . . . . . . . . . . . . . . 242.3.2 Partial Pivoting . . . . . . . . . . . . . . . . . . . . . . . . 262.3.3 Multiple Right-Hand Sides . . . . . . . . . . . . . . . . . 30

2.4 Singular Systems . . . . . . . . . . . . . . . . . . . . . . . . . . . 322.5 Symmetric Positive Definite Systems . . . . . . . . . . . . . . . . 332.6 Iterative Refinement . . . . . . . . . . . . . . . . . . . . . . . . . 352.7 Ill-Conditioned Systems . . . . . . . . . . . . . . . . . . . . . . . 372.8 Gauss–Seidel Iteration . . . . . . . . . . . . . . . . . . . . . . . . 37

vii

viii Contents

3 Nonlinear Equations . . . . . . . . . . . . . . . . . . . . . . . . . . . 473.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 483.2 Bisection Method . . . . . . . . . . . . . . . . . . . . . . . . . . 49

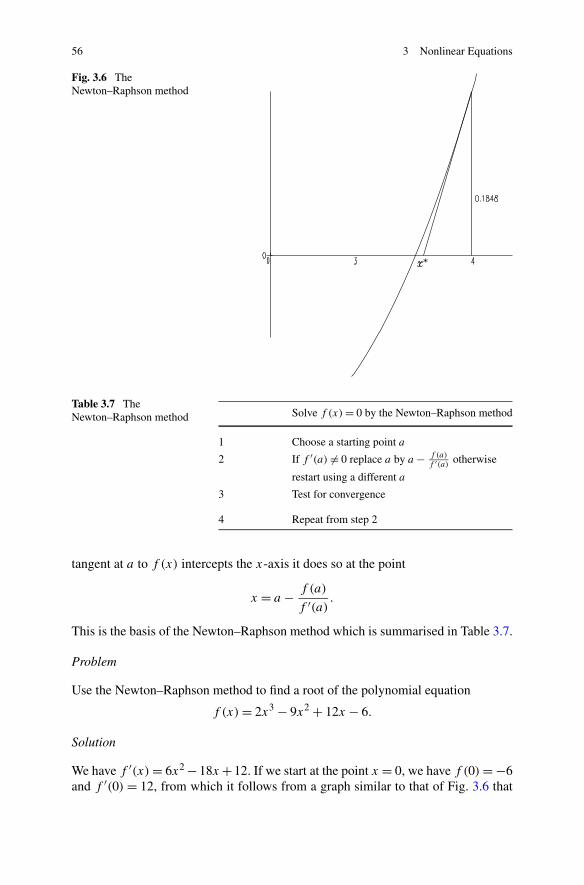

3.2.1 Finding an Interval Containing a Root . . . . . . . . . . . 503.3 Rule of False Position . . . . . . . . . . . . . . . . . . . . . . . . 513.4 The Secant Method . . . . . . . . . . . . . . . . . . . . . . . . . 523.5 Newton–Raphson Method . . . . . . . . . . . . . . . . . . . . . . 553.6 Comparison of Methods for a Single Equation . . . . . . . . . . . 583.7 Newton’s Method for Systems of Nonlinear Equations . . . . . . . 59

3.7.1 Higher Order Systems . . . . . . . . . . . . . . . . . . . . 63

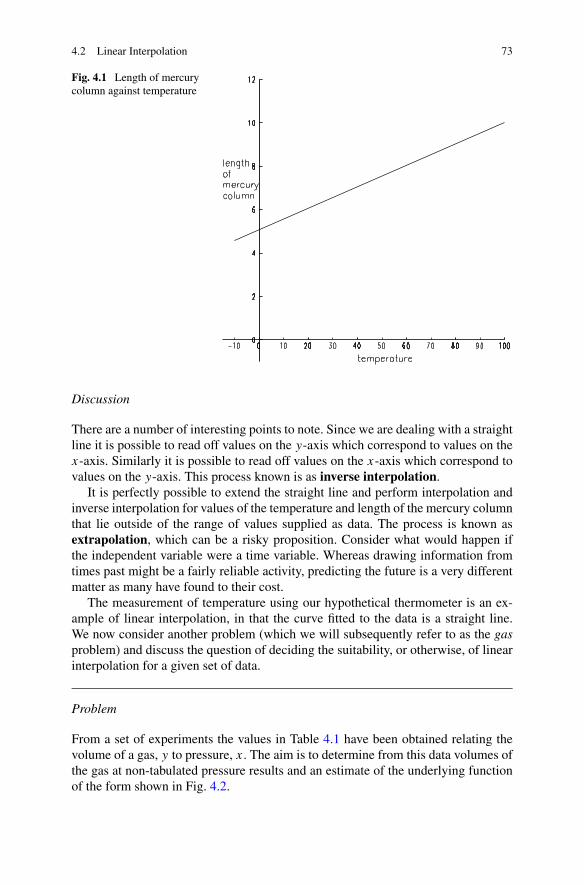

4 Curve Fitting . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 714.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 714.2 Linear Interpolation . . . . . . . . . . . . . . . . . . . . . . . . . 72

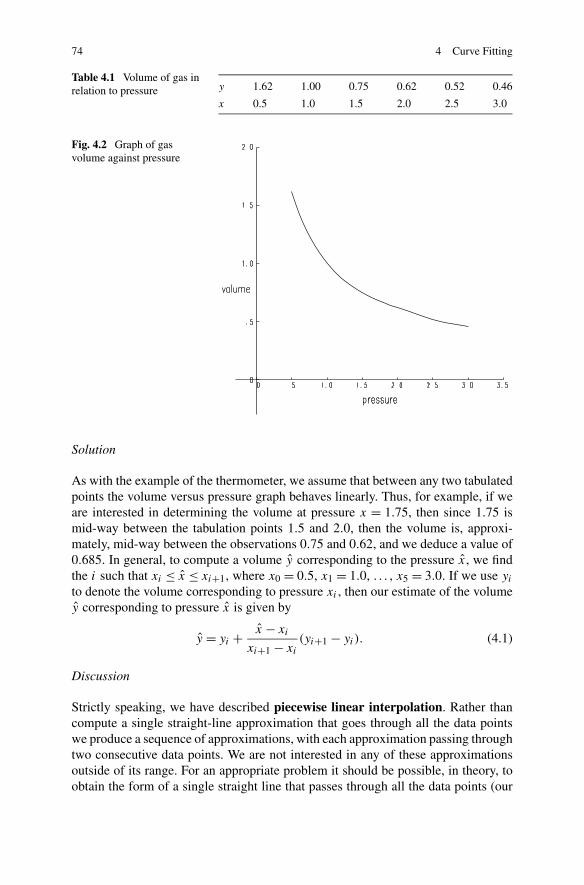

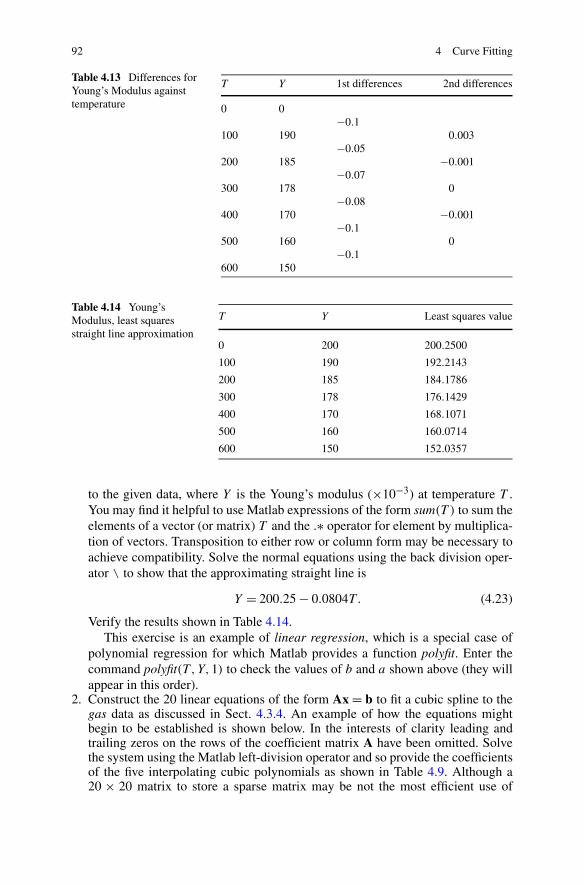

4.2.1 Differences . . . . . . . . . . . . . . . . . . . . . . . . . . 754.3 Polynomial Interpolation . . . . . . . . . . . . . . . . . . . . . . 77

4.3.1 Newton Interpolation . . . . . . . . . . . . . . . . . . . . 774.3.2 Neville Interpolation . . . . . . . . . . . . . . . . . . . . . 804.3.3 A Comparison of Newton and Neville Interpolation . . . . 814.3.4 Spline Interpolation . . . . . . . . . . . . . . . . . . . . . 83

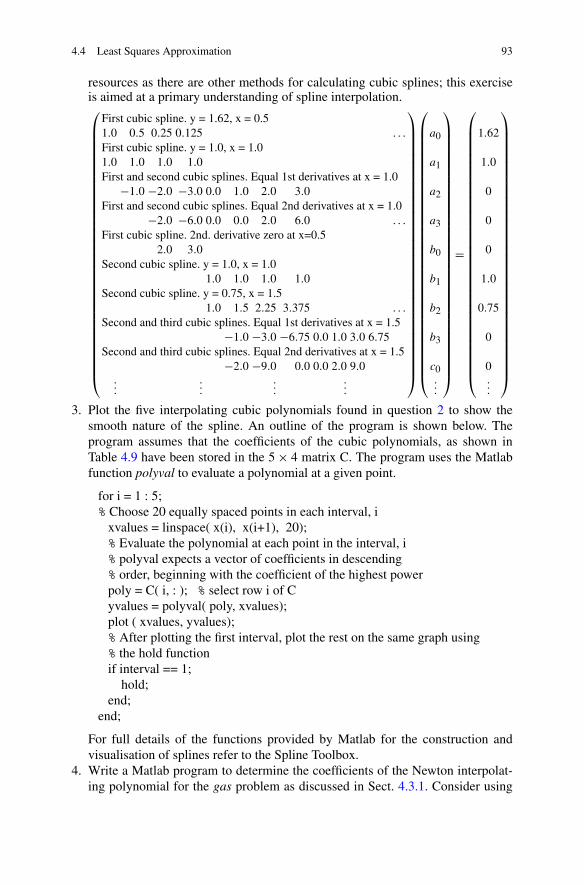

4.4 Least Squares Approximation . . . . . . . . . . . . . . . . . . . . 864.4.1 Least Squares Straight Line Approximation . . . . . . . . . 864.4.2 Least Squares Polynomial Approximation . . . . . . . . . 89

5 Numerical Integration . . . . . . . . . . . . . . . . . . . . . . . . . . 975.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 985.2 Integration of Tabulated Functions . . . . . . . . . . . . . . . . . 98

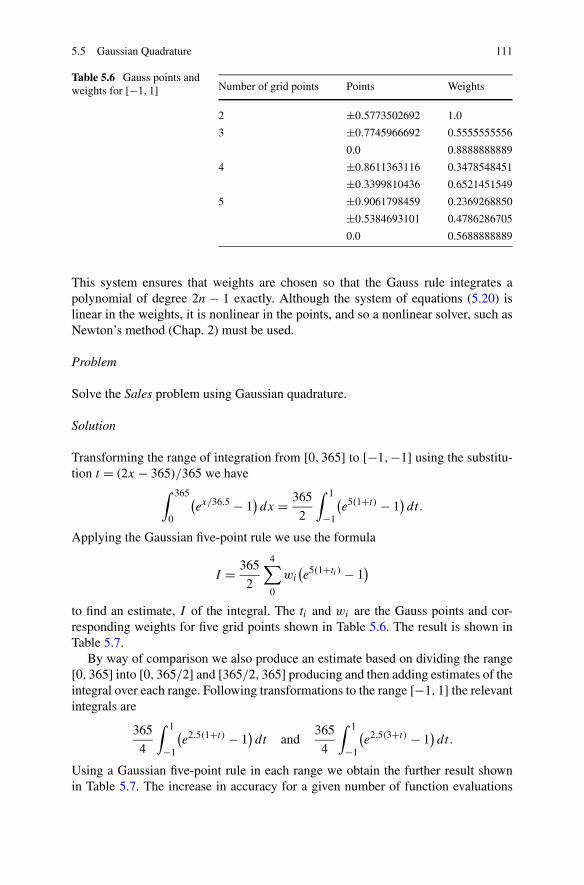

5.2.1 The Trapezium Rule . . . . . . . . . . . . . . . . . . . . . 995.2.2 Quadrature Rules . . . . . . . . . . . . . . . . . . . . . . 1015.2.3 Simpson’s Rule . . . . . . . . . . . . . . . . . . . . . . . 1015.2.4 Integration from Irregularly-Spaced Data . . . . . . . . . . 102

5.3 Integration of Functions . . . . . . . . . . . . . . . . . . . . . . . 1045.3.1 Analytic vs. Numerical Integration . . . . . . . . . . . . . 1045.3.2 The Trapezium Rule (Again) . . . . . . . . . . . . . . . . 1045.3.3 Simpson’s Rule (Again) . . . . . . . . . . . . . . . . . . . 106

5.4 Higher Order Rules . . . . . . . . . . . . . . . . . . . . . . . . . 1095.5 Gaussian Quadrature . . . . . . . . . . . . . . . . . . . . . . . . . 1105.6 Adaptive Quadrature . . . . . . . . . . . . . . . . . . . . . . . . . 112

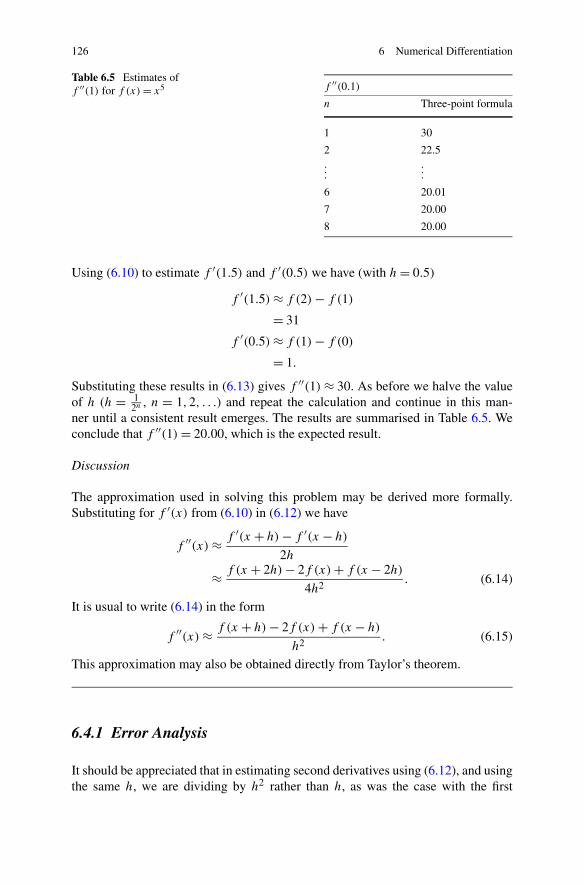

6 Numerical Differentiation . . . . . . . . . . . . . . . . . . . . . . . . 1196.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1206.2 Two-Point Formula . . . . . . . . . . . . . . . . . . . . . . . . . 1206.3 Three- and Five-Point Formulae . . . . . . . . . . . . . . . . . . . 1226.4 Higher Order Derivatives . . . . . . . . . . . . . . . . . . . . . . 125

6.4.1 Error Analysis . . . . . . . . . . . . . . . . . . . . . . . . 1266.5 Cauchy’s Theorem . . . . . . . . . . . . . . . . . . . . . . . . . . 128

Contents ix

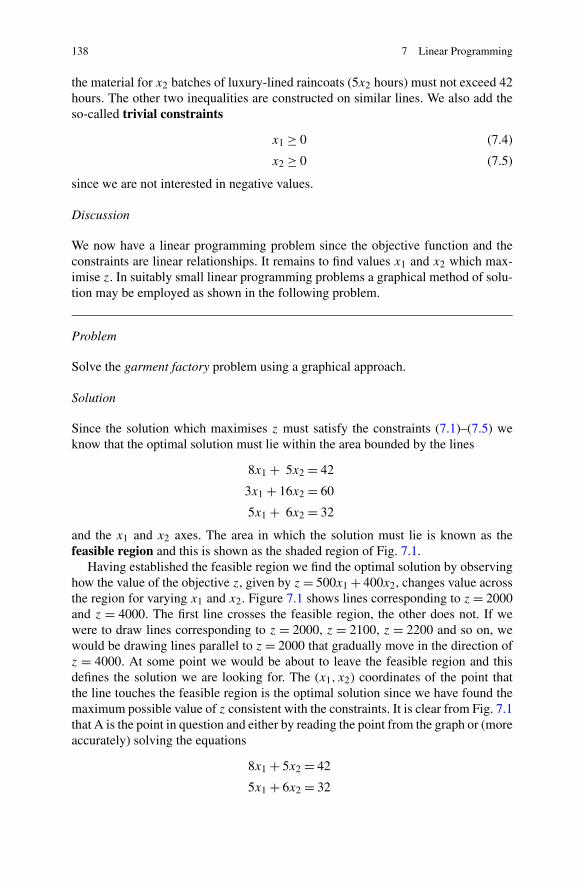

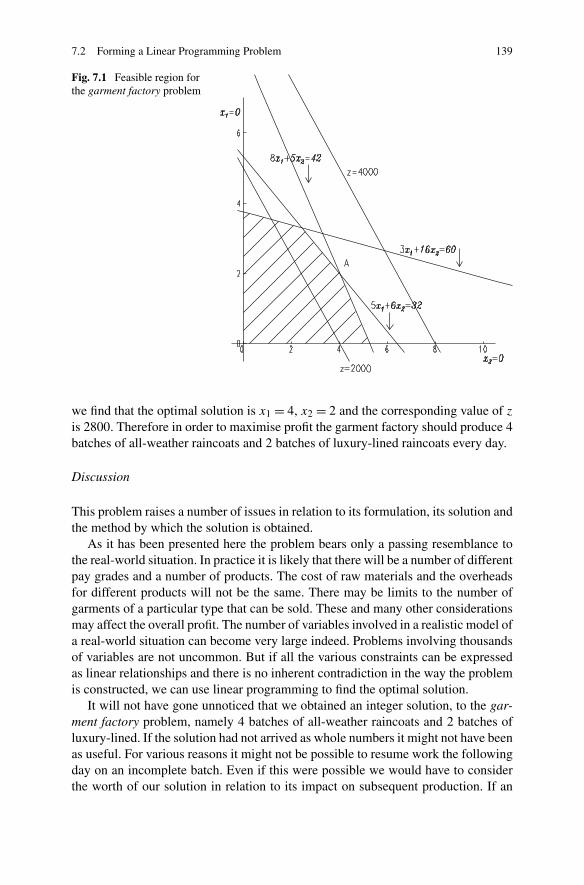

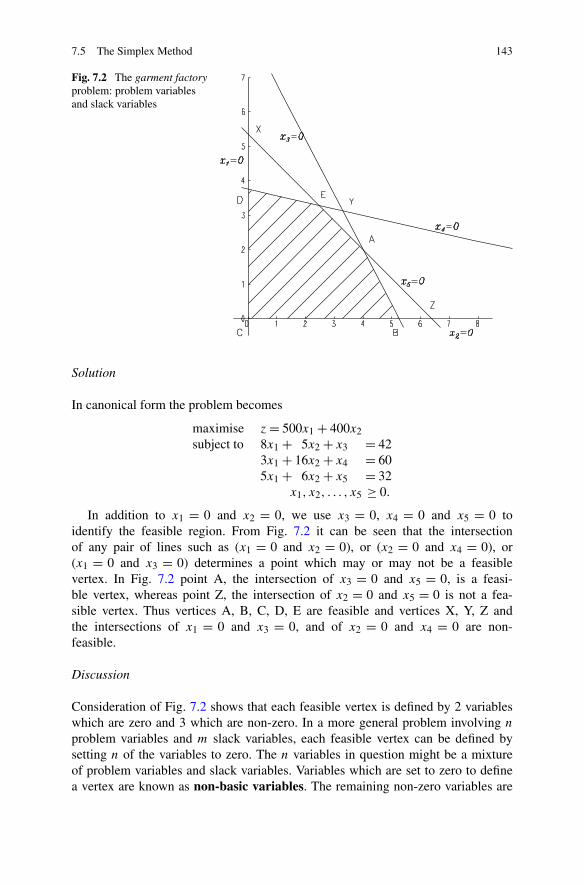

7 Linear Programming . . . . . . . . . . . . . . . . . . . . . . . . . . . 1357.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1367.2 Forming a Linear Programming Problem . . . . . . . . . . . . . . 1367.3 Standard Form . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1407.4 Canonical Form . . . . . . . . . . . . . . . . . . . . . . . . . . . 1417.5 The Simplex Method . . . . . . . . . . . . . . . . . . . . . . . . . 142

7.5.1 Starting the Simplex Method . . . . . . . . . . . . . . . . 1467.6 Integer Programming . . . . . . . . . . . . . . . . . . . . . . . . 149

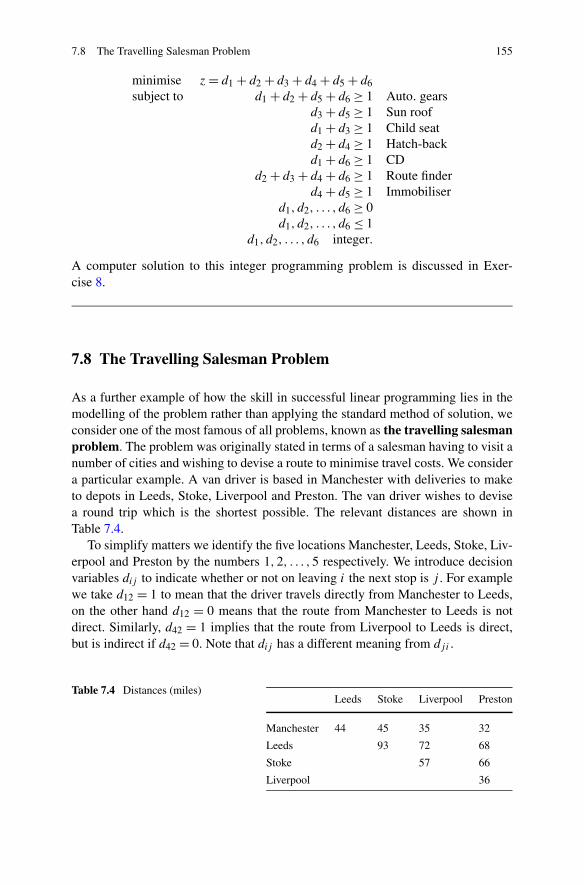

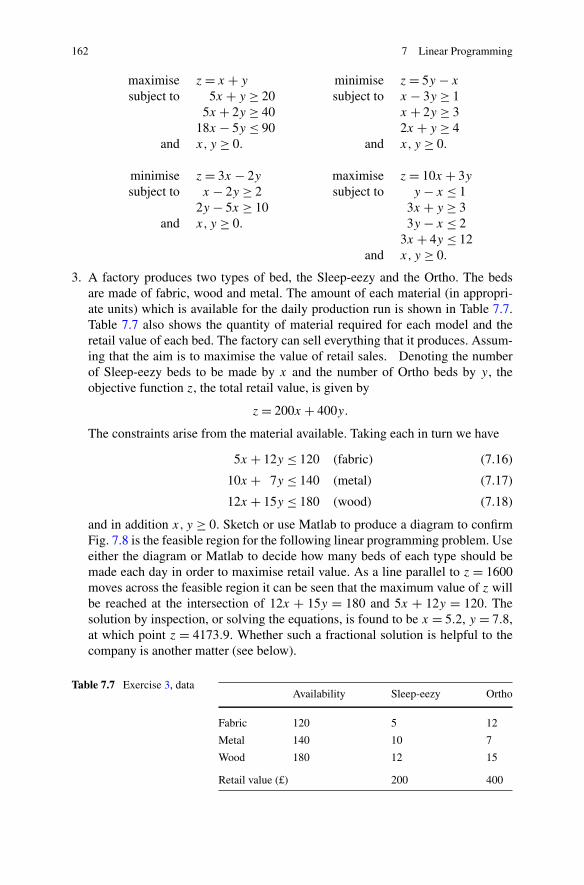

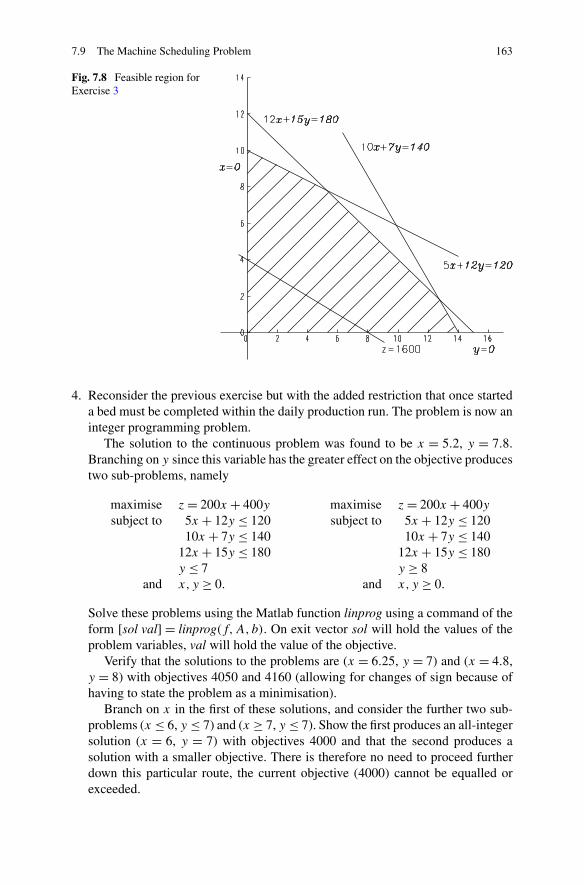

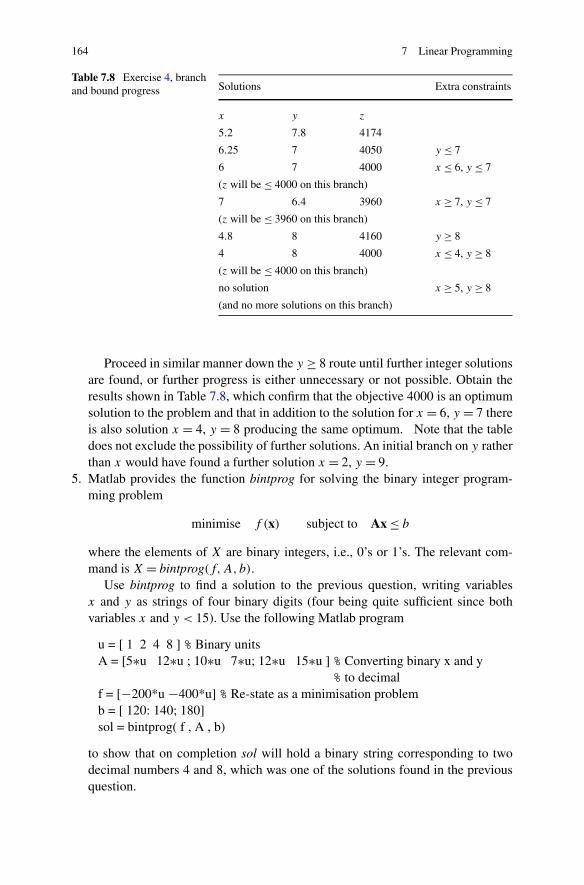

7.6.1 The Branch and Bound Method . . . . . . . . . . . . . . . 1517.7 Decision Problems . . . . . . . . . . . . . . . . . . . . . . . . . . 1537.8 The Travelling Salesman Problem . . . . . . . . . . . . . . . . . . 1557.9 The Machine Scheduling Problem . . . . . . . . . . . . . . . . . . 156

8 Optimisation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1698.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1708.2 Grid Searching Methods . . . . . . . . . . . . . . . . . . . . . . . 171

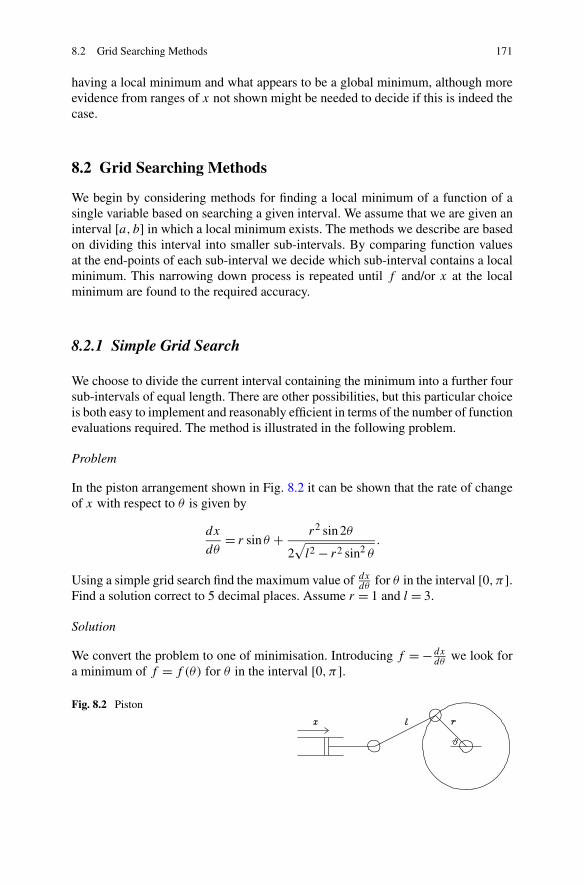

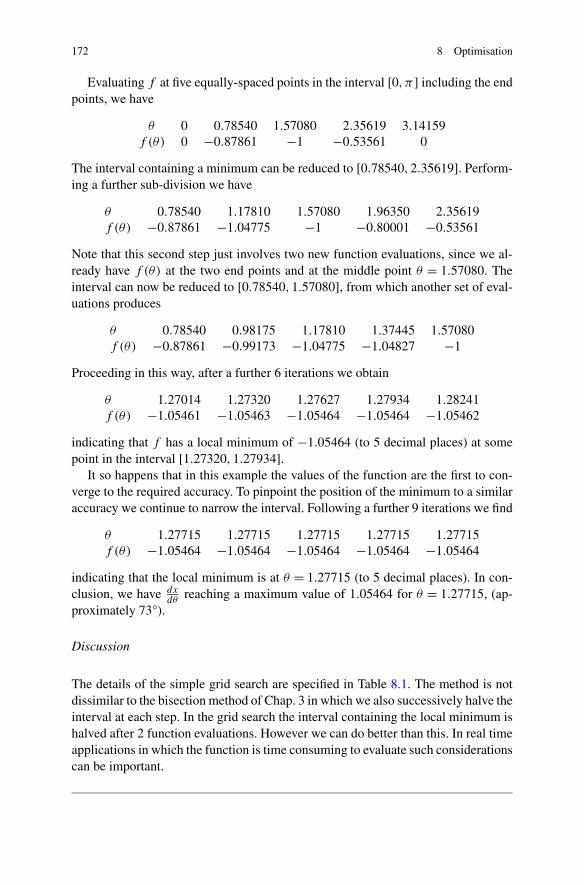

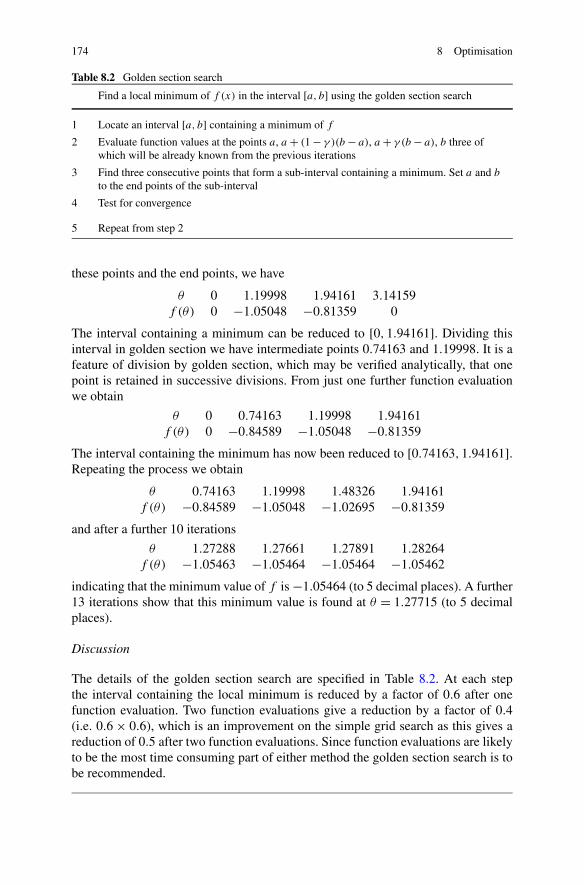

8.2.1 Simple Grid Search . . . . . . . . . . . . . . . . . . . . . 1718.2.2 Golden Section Search . . . . . . . . . . . . . . . . . . . . 173

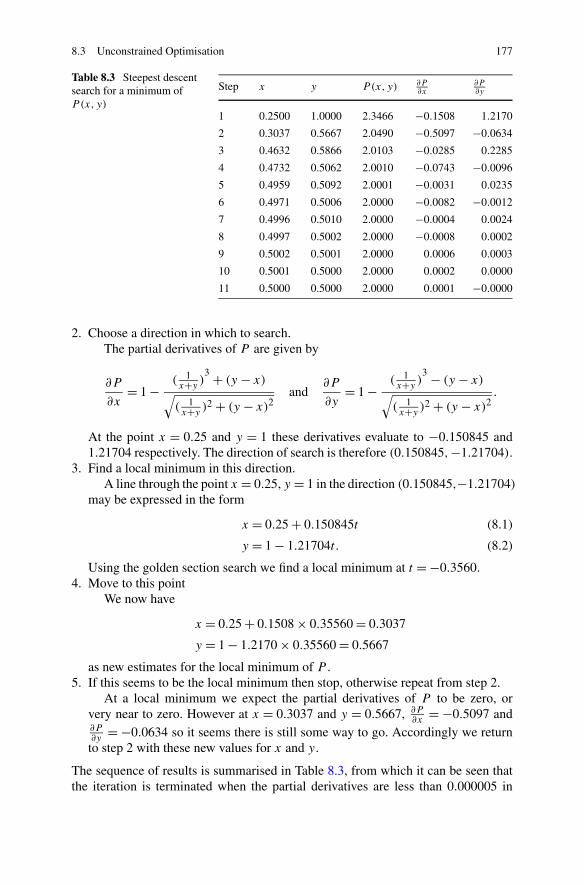

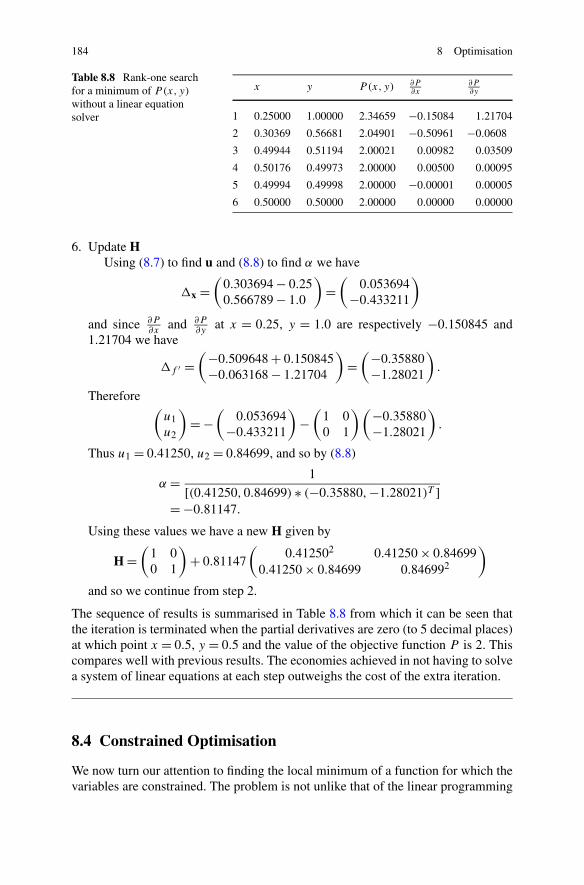

8.3 Unconstrained Optimisation . . . . . . . . . . . . . . . . . . . . . 1758.3.1 The Method of Steepest Descent . . . . . . . . . . . . . . 1768.3.2 A Rank-One Method . . . . . . . . . . . . . . . . . . . . . 1788.3.3 Generalised Rank-One Method . . . . . . . . . . . . . . . 181

8.4 Constrained Optimisation . . . . . . . . . . . . . . . . . . . . . . 1848.4.1 Minimisation by Use of a Simple Penalty Function . . . . . 1858.4.2 Minimisation Using the Lagrangian . . . . . . . . . . . . . 1878.4.3 The Multiplier Function Method . . . . . . . . . . . . . . 188

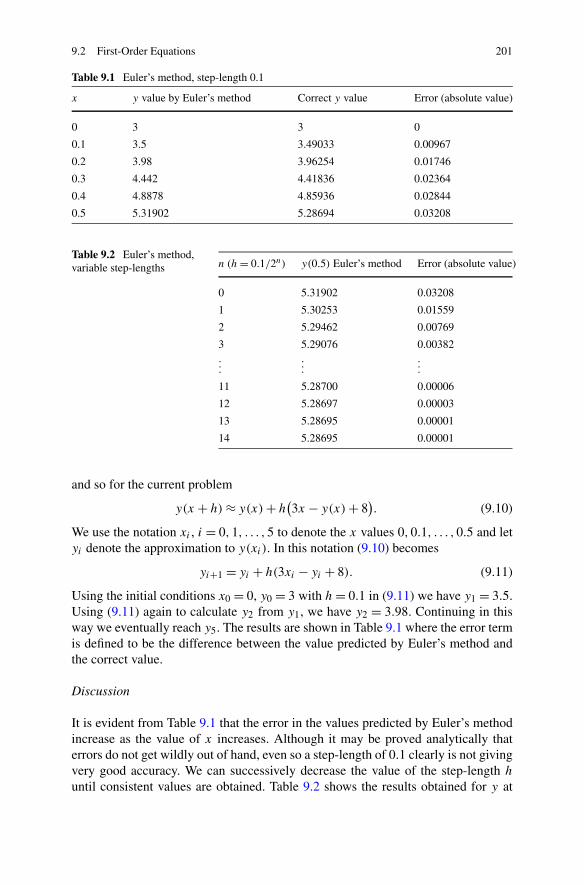

9 Ordinary Differential Equations . . . . . . . . . . . . . . . . . . . . 1979.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1989.2 First-Order Equations . . . . . . . . . . . . . . . . . . . . . . . . 200

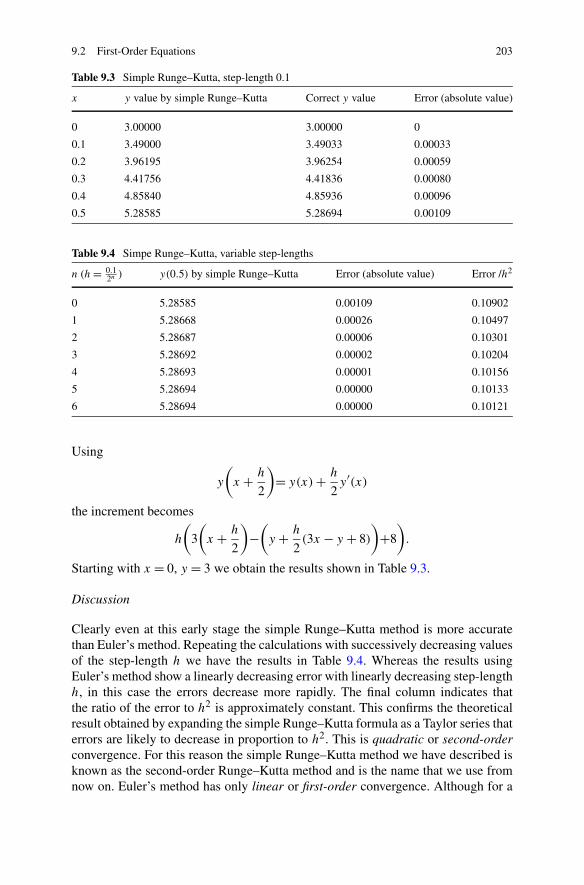

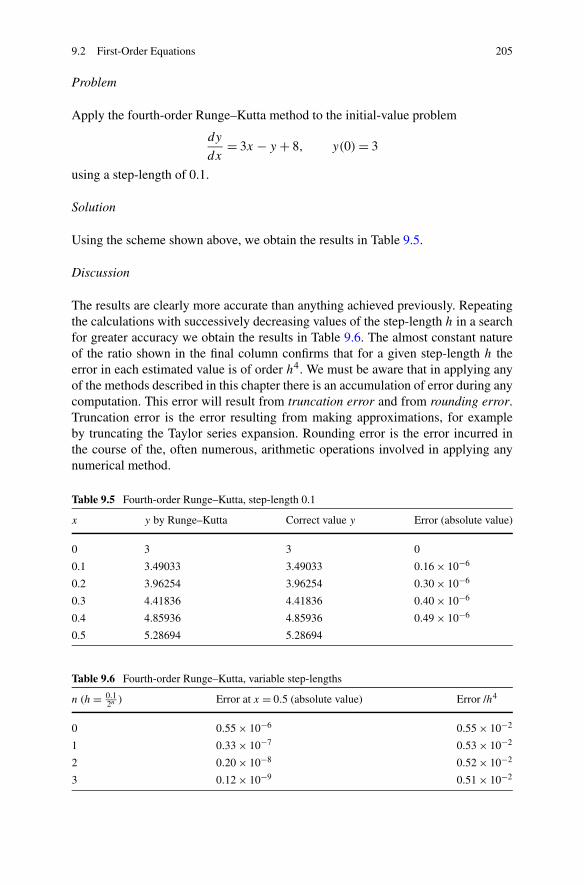

9.2.1 Euler’s Method . . . . . . . . . . . . . . . . . . . . . . . . 2009.2.2 Runge–Kutta Methods . . . . . . . . . . . . . . . . . . . . 2029.2.3 Fourth-Order Runge–Kutta . . . . . . . . . . . . . . . . . 2049.2.4 Systems of First-Order Equations . . . . . . . . . . . . . . 2069.2.5 Higher Order Equations . . . . . . . . . . . . . . . . . . . 207

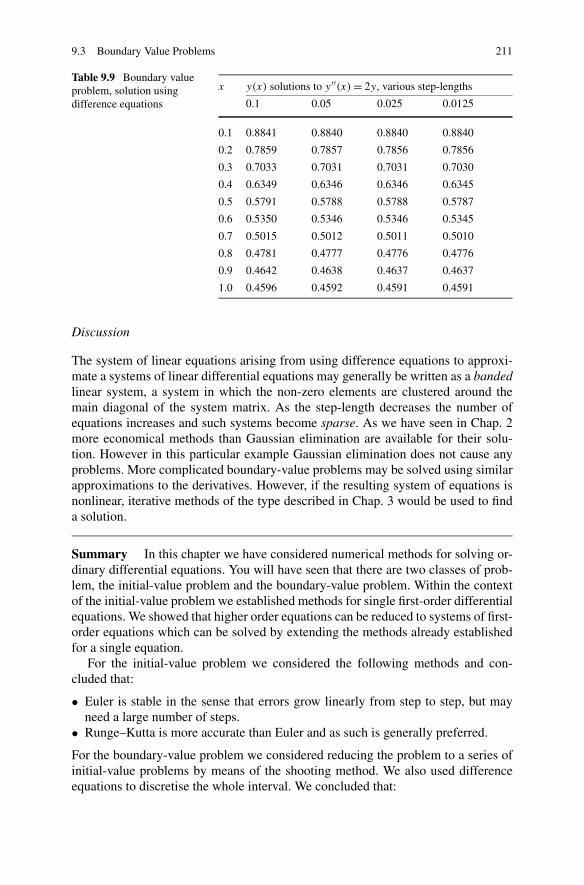

9.3 Boundary Value Problems . . . . . . . . . . . . . . . . . . . . . . 2089.3.1 Shooting Method . . . . . . . . . . . . . . . . . . . . . . 2089.3.2 Difference Equations . . . . . . . . . . . . . . . . . . . . 209

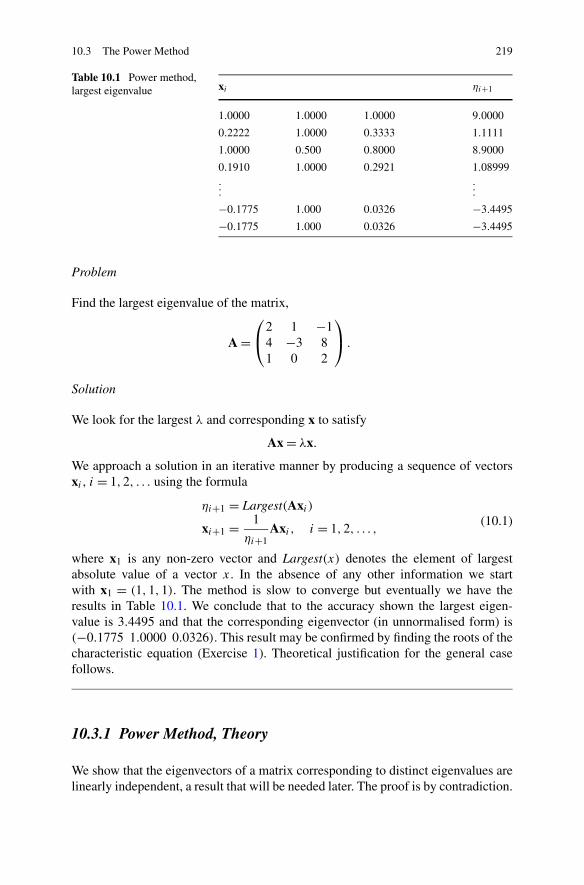

10 Eigenvalues and Eigenvectors . . . . . . . . . . . . . . . . . . . . . . 21510.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21510.2 The Characteristic Polynomial . . . . . . . . . . . . . . . . . . . 21710.3 The Power Method . . . . . . . . . . . . . . . . . . . . . . . . . . 218

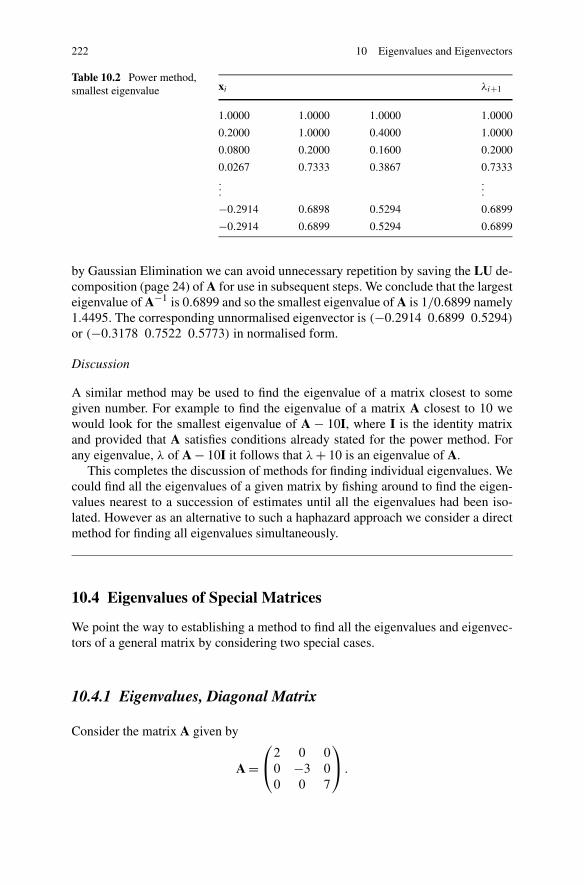

10.3.1 Power Method, Theory . . . . . . . . . . . . . . . . . . . 21910.4 Eigenvalues of Special Matrices . . . . . . . . . . . . . . . . . . . 222

10.4.1 Eigenvalues, Diagonal Matrix . . . . . . . . . . . . . . . . 22210.4.2 Eigenvalues, Upper Triangular Matrix . . . . . . . . . . . 223

x Contents

10.5 A Simple QR Method . . . . . . . . . . . . . . . . . . . . . . . . 223

11 Statistics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23111.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 23211.2 Statistical Terms . . . . . . . . . . . . . . . . . . . . . . . . . . . 232

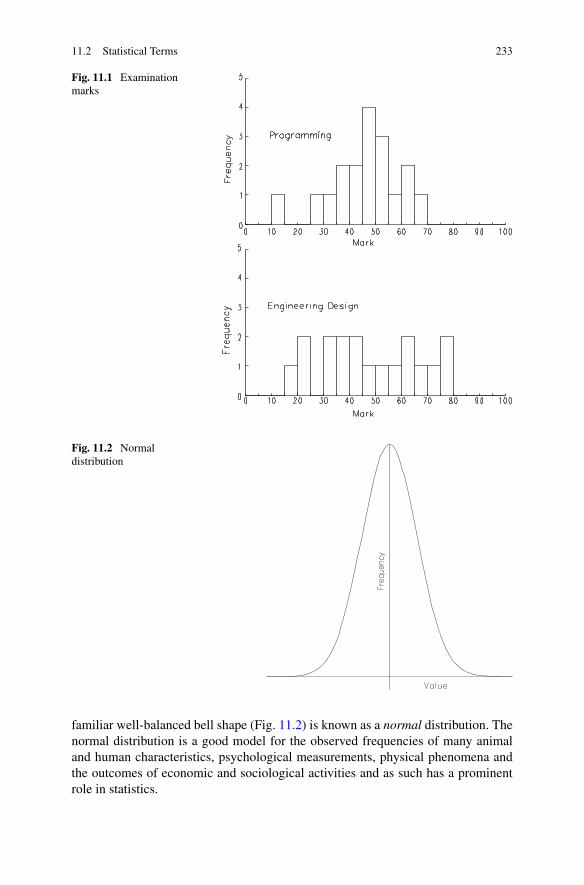

11.2.1 Random Variable . . . . . . . . . . . . . . . . . . . . . . 23211.2.2 Frequency Distribution . . . . . . . . . . . . . . . . . . . 23211.2.3 Expected Value, Average and Mean . . . . . . . . . . . . . 23411.2.4 Variance and Standard Deviation . . . . . . . . . . . . . . 23411.2.5 Covariance and Correlation . . . . . . . . . . . . . . . . . 236

11.3 Least Squares Analysis . . . . . . . . . . . . . . . . . . . . . . . 23911.4 Random Numbers . . . . . . . . . . . . . . . . . . . . . . . . . . 241

11.4.1 Generating Random Numbers . . . . . . . . . . . . . . . . 24211.5 Random Number Generators . . . . . . . . . . . . . . . . . . . . 243

11.5.1 Customising Random Numbers . . . . . . . . . . . . . . . 24311.6 Monte Carlo Integration . . . . . . . . . . . . . . . . . . . . . . . 244

Matlab Index . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 249

Index . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 253

Chapter 1Basic Matlab

Aims This introductory chapter aims to encourage the immediate use of Mat-lab through examples and exercises of basic procedures. Sufficient techniques andskills will be illustrated and practised to prepare for the end of chapter exercises inthe main text and indeed for any numerical calculation. Presentation of results andreading and writing data from files will also be considered. Overall it is hoped thatthe beauty, simplicity and power of Matlab will begin to appear.

1.1 Matlab—The History and the Product

Matlab was devised by Cleve Moler in the late 1970’s to make numerical computingeasier for students at the University of New Mexico. Many of the obstacles to usinga computer for mathematics were removed. In a Matlab program variables, whetherreal or complex numbers, vectors or matrices may be named and used as and whenrequired without prior notification or declaration and may be manipulated accordingto the rules of mathematics. Matlab spread to other Universities and in 1984 Clevewent into partnership with a colleague to set up a company called Mathworks tomarket Matlab. Mathworks is now a multi-national corporation specialising in tech-nical computing software. Matlab and products built on Matlab are used all overthe world by innovative technology companies, government research labs, financialinstitutions, and more than 3,500 universities.

Matlab is a high-level user friendly technical computing language and interactiveenvironment for algorithm development, data visualisation, data analysis, and nu-meric computation. Matlab applications include signal and image processing, com-munications, control design, test and measurement, financial modelling and analy-sis, and computational biology. Matlab provides specialised collections of programsapplicable to particular problem areas in what are known as Toolboxes and whichrepresent the collaborative efforts of top researchers from all over the world. Mat-lab can interface with other languages and applications and is the foundation for allMathWorks products. Matlab has an active user community that contributes freely

C. Woodford, C. Phillips, Numerical Methods with Worked Examples: Matlab Edition,DOI 10.1007/978-94-007-1366-6_1, © Springer Science+Business Media B.V. 2012

1

2 1 Basic Matlab

available Matlab programs to a supported web site1 for distribution and appraisal.Help, advice and discussion of matters of common interest are always available ininternet user forums. Whatever the question, someone somewhere in the world willhave the answer.

1.2 Creating Variables and Using Basic Arithmetic

To create a single variable just use it on the left hand side of an equal sign. Enter thename of the variable to see its current value.

The ordinary rules of arithmetic apply using the symbols +, −, ∗ and \ for ad-dition, subtraction, multiplication and division and ∧ raising to a power. Use roundbrackets ( and ) to avoid any ambiguities.

In the interests of clarity when illustrating Matlab commands the ∧ symbol willbe used throughout the book to denote the caret (or circumflex) entered from mostkeyboards by the combination SHIFT-6.

Exercises

1. Enter the following commands2 on separate lines in the command window.

(i) r = 4 (ii) ab1 = 7.1 + 3.2 (iii) r(iv) A = r∧2 (v) sol = ab1∗(1 + 1/r) (vi) ab1 = sol∧ (1/2)(vii) CV2 = 10/3 (viiii) x = 1.5e-2

2. Enter one or more of the previous commands on the same line using a semi-colon ; to terminate each command. Notice how the semi-colon may be used tosuppress output.

3. If £1000 is owed on a credit card and the APR is 17.5% how much interest wouldbe due? Divide the APR by 12 to get the monthly rate.

1.3 Standard Functions

Matlab provides a large number of commonly used functions including abs, sqrt,exp, log and sin, cos and tan and inverses asin, acos, atan. Functions are calledusing brackets to hold the argument, for example

x = sqrt(2); A = sin(1.5); a = sqrt(a∧2 + b∧2); y = exp(1/x);

For a full list of Matlab provided functions with definitions and examples, follow thelinks Help → Product Help from the command window and choose either FunctionsBy Category or Functions Alphabetical List from the ensuing window.

1www.mathworks.com/matlabcentral/fileexchange/2We may also terms such as statement, expression and code within the context of Matlab com-mands.

1.4 Vectors and Matrices 3

Exercises

1. Find the longest side of a right angled triangle whose other sides have lengths 12and 5. Use Pythagoras: (a2 + b2 = c2).

2. Find the roots of the quadratic equation 3x2 − 13x + 4 using the formulax = (−b ± √

b2 − 4ac)/2a. Calculate each root separately. Note that arithmeticexpressions with an implied multiplication such as 2a are entered as 2∗a in Mat-lab.

3. Given a triangle with angle π/6 between two sides of lengths 5 and 7, use thecosine rule (c2 = a2 + b2 − 2ab cosC) to find the third side.

Note that π is available in Matlab as pi.

1.4 Vectors and Matrices

Vectors and matrices are defined using square brackets. The semi-colon ; is usedwithin the square brackets to separate row values.

For example the matrix

A =⎛⎝

2 3 −14 8 −3

−2 3 1

⎞⎠

may be created using

A = [ 2 3 −1; 4 8 −3; −2 3 1 ]

A row vector v = (2 3 −1 ) may be created using v = [ 2 3 −1 ].The transpose of a vector (or matrix) may be formed using the ' notation. It fol-

lows that the column vector

w =⎛⎝

532

⎞⎠

may be created using either w = [ 5; 3; 2 ] or w = [ 5 3 2 ]'.

Exercises

1. Create the row vector x = (4 10 −1 0 ).2. Create the column vector y = (−5.3 −2 0.9 1 ).3. Create the matrix

B =⎛⎝

1 7.3 −5.6 21.4 8 −3 0−2 6.3 1 −2

⎞⎠ .

4. The roots of a polynomial may be found by using the function roots. For ex-ample the command roots(p) will return the roots of a polynomial, where p

4 1 Basic Matlab

specifies the vector of coefficients of the polynomial beginning with the coef-ficient of the highest power and descending to the constant term. For exampleroots([ 1 2 −3 ]) would find the roots of x2 + 2x − 3. Use roots to check thesolution of question (2), Sect. 1.3.

Individual elements of a vector or matrix may be selected using row-columnindices, for example by commands such as A( 1, 2 ) or z = w(3).

Whole rows (or columns) may be selected. For example, A( : , 1 ) selects the1st column and A( 3 , : ) selects the 3rd row of a matrix A. More generally, havingassigned values to variables i and j, use expressions such as abc = A( : , j ) to assignthe j th column of A to a variable, abc and xyz = A ( i , : ) to assign the ith row ofA to a variable, xyz.

Exercises

1. Using B (as above) assign the values held at B(1, 2) to a variable, a and B(3, 4)to variable, b.

2. Form a vector, v1 from the 2nd column of B and the vector, v2 from the 1st rowof B.

Note that Matlab enforces the rules regarding the multiplication of matrices andvectors. A command of the form A∗B is only executed if A has the same number ofcolumns as B has rows.

Exercises

1. Using the previous A and w form the product A∗w. See what happens if the orderof multiplication is reversed.

2. The norm (or size) of a vector, v where v = (v1, . . . , vn) is defined to be√v2

1 + · · · + v2n. Find the norm of the vector (3 4 5 −1) either by adding indi-

vidual terms and taking the square root or by using the formula√

v.vT , where v

is a row vector. Check the result using the Matlab function norm and a commandof the form norm(v).

In general inserting spaces in Matlab commands does not affect the outcome.However care has to be taken when forming a list of numbers as is the case whenspecifying the elements of a vector or an array. The notation for numbers takespriority over the notation for expressions connecting numbers with operators. Inpractice this means that the command, V = [ 1 2 −1 ] produces the 3-elementvector, [1 2 −1]. On the other hand, V = [ 1 2 − 1 ] produces the 2-element vector,[1 1].

In addition to the usual operations for adding, subtracting and multiplication ofcompatible matrices and vectors Matlab provides a large number of other matrix–vector operations. Use the Matlab help system and follow the links Help → ProductHelp → Functions: By Category → Mathematics → Arrays and Matrices (and also→ Linear Algebra) for details. As example we consider the left-division \ operator.

1.5 M-Files 5

A system of linear equations such as

3x1 + 5x2 + 7x3 = 25,

x1 − 4x2 + 2x3 = 10,

4x1 − x2 − 3x3 = −1

may be written in the form Ax = b, where

A =⎛⎝

3 5 71 −4 24 −1 −3

⎞⎠ , x =

⎛⎝

x1x2x3

⎞⎠ , b =

⎛⎝

2510−1

⎞⎠ .

If A is an n × n matrix and b is a column vector having n rows then the solution(if it exists) to the linear system of equations written in the form Ax = b is given inMatlab by using the command

x = A\b

A warning is given if the solution does not exist or is unreliable due to roundingerror.

Exercises

1. Solve the following systems of equations.

(i) 2 a + c = 5 (ii) 3 a + 2 c − d = 33 a − 2 c = 4 2 a − 2 c + 3 d = 9

a − c − d = 2.

1.5 M-Files

On the whole entering Matlab commands and statements line by line is too errorprone for anything but very short, transitory programs. Programs under developmentand programs which are going to be used repeatedly are better stored as a sequenceof commands in a file. Such files are called M-files. A single command, filenameif that is the name of the M-file stored in the working directory, causes Matlab toexecute the commands stored in filename. An M-file is created by opening the Filemenu in the command window and following the link New → M-File. At this pointa new window titled Untitled opens into which Matlab commands may be entered.Use the Save As option to save the M-file and allocate a name. A suffix .m will beadded automatically. The file may be re-opened for editing using the open optionfrom the File menu.

Exercises

1. Use the file menu to create an M-file. Enter a sequence of commands. Save thefile using a name of your choice. Execute the newly created M-file. Edit the fileif necessary to obtain successful execution, then close the file.

2. Re-open the M-file, make changes to the program and re-execute.

6 1 Basic Matlab

1.6 The colon Notation and the for Loop

The colon operator, which has already been used in specifying rows and columnsof matrices (page 4), may be used to specify a range of values. In general the colonoperator uses variable names or actual numbers. For example:

1 : n is equivalent to 1, 2, 3, 4, . . . , n. (incrementing by 1)1 : m : n is equivalent to 1, 1+m, 1+2m, 1+3m, . . . , n. (incrementing by m)

The colon notation is particularly useful in the for construct, which repeats a se-quence of commands a number of times. For example, the following code adds thefirst 10 integers: 1, 2, . . . , 10, one by one. The running total is held in the variableaddnumbers.

addnumbers = 0; % initial totalfor i = 1 : 10;

addnumbers = addnumbers + i; % running totalend

Note the use of the % symbol to document the program. Matlab ignores anything onthe line following the % sign.

Exercises

1. By making a small change to the program above, use Matlab to find the sum ofthe even numbers 2, . . . , 10.

2. Create the vector b = (2.5 5 9 −11). Add the elements of b by indexing theelements of b within a for loop, in which a statement of the form

eltsum = eltsum + b(i)

holds the running total in the variable, eltsum.3. The following series may be used to calculate an approximation to

√2

xn+1 = xn

2+ 1

xn

, n = 1,2, . . . , x1 = 1.

Calculate x1, x2, . . . , x7 and show convergence to√

2. The following code wouldbe sufficient

x(1) = 1 % first approximationfor n = 1 : 6

x(n+1) = x(n)/2 + 1/x(n) % successive approximationsend

Devise an alternative, more economical version which does not save intermediateresults but simply displays and then overwrites the current estimate of

√2 by the

next estimate.4. The Fibonacci numbers: 0,1,1,2,3,5,8,13, . . . (each number is the sum of the

two preceding numbers) relate to several natural phenomena. Use a for loop toprint the ratio of successive Fibonacci numbers Fn+1/Fn for n = 2, . . . ,20 andso illustrate convergence of this ratio to (1 + √

5)/2 (The Golden ratio).

1.7 The if Construct 7

Note By default Matlab continues printing until a program is completed. To viewoutput page by page enter the command more on. To restore the default enter more.

1.7 The if Construct

In addition to the loop structure program flow may be controlled using if, else andelseif. The basic constructs are shown below:

if expression; if expression; if expression;statements; statements; statements;

end; else elseif expression;statements; statements;

end; elsestatements;

end;

where expression is a logical statement which evaluates to either true or false andwhere statements is any set of Matlab statements. Logical statements include vari-able relationships such as:

== (equals) > (greater than) >= (greater than or equal to)< (less than) <= (less than or equal to) ∼ (not) && (and) || (or)

Use brackets for compound expressions to ensure that Matlab interprets the logic asintended.

Exercises

1. Predict the values of the variables following execution of the fragments of code.Enter the code in a Matlab program to verify the outcome.

(i) x = 2;y = 1;if x > 2; y = x; end;

(ii) a = 1;b = 2;if a == 1; b = a + 1; end;

(iii) u = 1; v = 2; w = −2;if (u ∼= 0 && u < abs(w) ) || u < 0;

u = u + w;else

u = u − w;end;

2. In using the formula for the solution of a quadratic equation the discriminant(b2 − 4ac) may be positive (indicating two real roots), zero (a double root) ornegative (complex roots). Write Matlab code to set a variable roots to 2, 1 or 0

8 1 Basic Matlab

depending on the value of the discriminant. Test the program using various val-ues of a, b and c.

3. Given a vector (or matrix) of dimension (m, n) use a for loop within a for loop tocount the number of non-zero elements. Test your code on simple examples.

Note the function size may be used to determine the dimensions of an array. Forexample [ n m ] = size(A) returns the number of rows, n and the number ofcolumns, m.

1.8 The while Loop

The while loop repeats a sequence of instructions until a specified condition is met.It is used as an alternative to the for loop in cases where the number of requiredrepeats is not known in advance. The basic construct is:

while expressionMatlab commands

end;

If expression evaluates to true the Matlab commands are executed and the programreturns to re-evaluating expression. If expression evaluates to false the commandfollowing end; (if any) is executed.

Exercises

1. Although a for loop would be more appropriate, enter the following code whichuses a while loop to find the sum of the numbers 1, . . . , 10.

addnumbers = 0; % set running total to 0n = 1; % first numberwhile n <= 10

addnumbers = addnumbers + n; % add current number to running totaln = n + 1; % next number

end;addnumbers % show the result

2. Create a vector of numbers which includes one or more zeros. Construct a whileloop to find the sum of the numbers up to the first zero.

3. Use a while loop and the previously quoted series to calculate an approximationto

√2 accurate to 4 decimal places by terminating the loop when the difference

between successive estimates is less than 0.00005.

Note Enter Ctrl C from the keyboard to terminate execution prematurely (useful ifa program runs out of control).

1.9 Simple Screen Output 9

1.9 Simple Screen Output

As an alternative to entering the name of a variable the function disp may be usedto output a value or a string. The standard forms are disp(x) and disp('s ') where x

is a variable and s is a string of alphanumeric and other characters.

Exercises

1. Assign a value to the single variable root and enter the command

disp('Root of the equation:'); disp(root);

to show how more meaningful output may be produced.2. Repeat the previous question with a vector rather than a single variable.

1.10 Keyboard Input

The function input may be used to request user input. The standard form isx = input('request'). The user sees the character string request on the screen andenters number(s) from the keyboard to be allocated to the program variable x. Ifan answer in the form of a character string is required the command has the formx = input('request','s'). The command is useful for constructing programs that inter-act with the user.

Note The character string, \n may be inserted into the request string to move thecursor to a new line.

Exercises

1. As part of an interactive program, use the following code to obtain the value ofm and echo the input to the screen. The program asks for confirmation (Y or N)that the number is correct and if necessary repeats the original request.

m=input('Enter the number of data values \n');reply=input('Is that correct, answer Y or N\n','s');while ∼ strcmp(reply,'Y')

input('Enter the number of data values\n');reply=input('Is that correct, answer Y or N\n','s');

end;disp('Thank you');

2. Modify the program by allowing a maximum of 3 corrections to the first entry.3. Write a program to request a password from the user. Compare the reply with a

stored string. If necessary repeat the request at most twice until there is agree-ment.

10 1 Basic Matlab

Note the function strcmp may be used to compare two strings. strcmp(a, b) evaluatesto true if a and b are identical and false otherwise. If two strings have equal leadingcharacters but one has trailing blanks they are not considered equal. The functionstrncmp for comparing the leading n characters of two strings is also provided byMatlab. Enter the command help strncmp for details.

1.11 User Defined Functions

Matlab provides a variety of built-in functions to cover a vast range of activities butit also allows user-defined functions. As we will see this can be a very useful facility.Each user-defined file must be stored in an M-file with the same name (apart fromthe .m suffix) as the function. The function heading has the form

function [out1,out2, . . .] = functionname (in1, in2, . . .)

where functionname is the chosen name of the function (and the M-file), in1, in2, . . .

are input parameters to the function and out1,out2, . . . are output parameters. Inpractice actual values or names of variables would be used as parameters.

As an example we consider a function for calculating the sum of the series

1 + x + x2 + · · · + xn.

We will call our function sumGP and allow for two input variables x and n and oneoutput parameter sum.

The following code (or similar) would be entered in an M-file with the namesumGP.m. The variable names we have used as parameters (and corresponding vari-ables within the function) are an arbitrary choice.

function [result] = sumGP( x, n )if x == 1; result = n+1 % Check for the exceptional case.else result = (x∧(n+1) − 1)/(x − 1)end

Assuming the M-file, sumGP.m is in the working directory a command of theform z = sumGP(p, q) or sumGP(p, q) would be used to apply the function wherep and q are either variable names or actual values. In this instance variables z, p andq would take the place of parameters result, x and n used in the formal definition ofSumGP.

Exercises

1. Create the aforementioned function sumGP and test it using the commandssumGP(1,4) (which should return the value 5) and sumGP(0.5,2) (to re-turn 1.75).

2. Write and test a function FtoC having one input and one output parameterto convert degrees Fahrenheit to degrees Centigrade. Use the formula C =(5/9)(F − 32). Establish the function in the M-file FtoC.m and test it from aprogram with calls such as FtoC(32) and centigrade = FtoC(212).

1.12 Basic Statistics 11

3. Write a function MaxElement to find the largest absolute value of all elements ofan array or vector. Test the function on simple examples. Note that for a given ma-trix or vector, A the Matlab function max applied to abs(A), as in max(abs(A))

would produce the same result.

1.12 Basic Statistics

A list of basic statistical functions, including mean and std (standard deviation), andplotting functions bar (bar charts) and pie (pie charts) may be found by followingthe links Help → Product Help → Functions: By Category → Data Analysis fromthe command window. Other statistical applications including Regression Analysis,Hypothesis Testing and Multivariate Methods may be found in the Statistics Tool-box. Follow the links Help → Product Help → Statistics Toolbox for details.

Exercises

1. As examples of some of the basic functions store a random selection of numbersin a vector v and enter each of the commands: mean(v), std(v), bar(v) and pie(v)

separately.2. Enter the command help pie for an explanation of the pie function and use the

information to add labels to the pie chart of variables v.

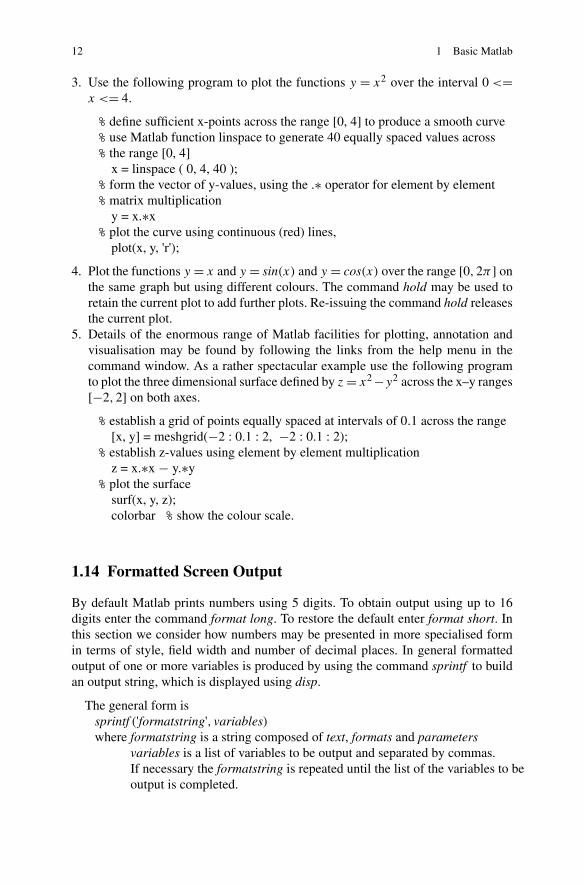

1.13 Plotting

For 2-D graphics, the basic commands are: plot(v), plot(u, v) and plot(u, v, 's ')where u and v are vectors and s is a combination of up to three character options,one from under each heading of Table 1.1.

The default option for plotting corresponds to '−b' (solid line, no data marks,blue).

Exercises

1. Store a random selection of (x, y) coordinates in the vectors x and y and enterthe command plot(x, y, ' − +r ').

2. Repeat the previous question with other character strings.

Table 1.1 Plotting options

Line style Data markers Colour

− solid line + plus sign y yellow r red

−. dash–dot line o circle m magenta g green

−− dashed line . dot c cyan b blue

: dotted line * asterisk k black g white

x cross

12 1 Basic Matlab

3. Use the following program to plot the functions y = x2 over the interval 0 <=x <= 4.

% define sufficient x-points across the range [0, 4] to produce a smooth curve% use Matlab function linspace to generate 40 equally spaced values across% the range [0, 4]

x = linspace ( 0, 4, 40 );% form the vector of y-values, using the .∗ operator for element by element% matrix multiplication

y = x.∗x% plot the curve using continuous (red) lines,

plot(x, y, 'r');

4. Plot the functions y = x and y = sin(x) and y = cos(x) over the range [0,2π] onthe same graph but using different colours. The command hold may be used toretain the current plot to add further plots. Re-issuing the command hold releasesthe current plot.

5. Details of the enormous range of Matlab facilities for plotting, annotation andvisualisation may be found by following the links from the help menu in thecommand window. As a rather spectacular example use the following programto plot the three dimensional surface defined by z = x2 −y2 across the x–y ranges[−2,2] on both axes.

% establish a grid of points equally spaced at intervals of 0.1 across the range[x, y] = meshgrid(−2 : 0.1 : 2, −2 : 0.1 : 2);

% establish z-values using element by element multiplicationz = x.∗x − y.∗y

% plot the surfacesurf(x, y, z);colorbar % show the colour scale.

1.14 Formatted Screen Output

By default Matlab prints numbers using 5 digits. To obtain output using up to 16digits enter the command format long. To restore the default enter format short. Inthis section we consider how numbers may be presented in more specialised formin terms of style, field width and number of decimal places. In general formattedoutput of one or more variables is produced by using the command sprintf to buildan output string, which is displayed using disp.

The general form issprintf ('formatstring', variables)where formatstring is a string composed of text, formats and parameters

variables is a list of variables to be output and separated by commas.If necessary the formatstring is repeated until the list of the variables to beoutput is completed.

1.14 Formatted Screen Output 13

Formats are preceded by % and are applied in the order of the variables. The moreused formats are illustrated below:

d for integer formatfor example %6d for a field width of 6 places.

f fixed point formatfor example %10.5f for a field width of 10 places and 5 decimal places.

e floating point (exponent) formatfor example %10.3e for a field width of 10 places and 3 decimal placeexponent.

We will use the parameter \n (newline) but there are others. For more details anddetails of other features of the format command, enter help format in the commandwindow.

Exercises

1. Enter the following code to compare π and its popular approximation 22/7.

ratio = 22/7;s1 = sprintf('pi to 6 decimal places is %8.6f ', pi);s2 = sprintf('22/7 to 6 decimal places is %8.6f ', ratio);disp(s1); disp(s2);

2. Repeat the previous question making use of the \n parameter to obtain the sameoutput using a single string. It may be necessary to use more that one line to enterthe format. Use the continuation mark as shown in the example below.

3. Allocate values to variables Node, ux and uy and use the following commandsto produce the output:

Node 27 ux 1.0934 uy 3.5e+005

s = sprintf( . . . % three dots indicate a continuation to the next line'Node %3d ux %6.4f uy %10.3e', Node, ux, uy);disp(s);

4. Display the matrix

A =⎛⎝

1 2 4.563 4 5.03 29 4.567

⎞⎠

noting that Matlab stores elements of a matrix in column order and so to obtainthe desired effect the transpose of A is used, for example:

s = sprintf('%6.3f %6.3f %6.3f \n ', A');disp(s);

5. Repeat the previous question but with a more detailed format so that the displayof matrix A bears a closer resemblance to the form shown above.

14 1 Basic Matlab

1.15 File Input and Output

In order to access a file it must be opened. A command of the form fid =fopen('filename', 'w+') opens a file for read, write and create access in M/S Win-dows systems (other operating systems may vary). Formats may be used for ap-pending output to an existing file. Enter the command help fopen for details. Thevariable, fid is known as a file identifier and is used by Matlab to identify the file insubsequent operations.

1.15.1 Formatted Output to a File

The command fprintf writes formatted data to a file. The structure of the commandis exactly the same as that of sprintf but with a file identifier as the first parameter.For example fprintf (fid, . . . ).

Exercises

1. Repeat any of the questions from (1.14) but print the results to a file. Display thefile after executing the formatting code using the command type filename.

Use the following code as an example which opens and writes to a Windowsfile myfile.txt. If the file already exists it is overwritten.

fid = fopen('myfile.txt','w+');fprintf(fid, 'pi to 6 decimal places is %8.6f ', pi);type myfile.txt

1.15.2 Formatted Input from a File

There are other commands for reading formatted input from a file but textscan is par-ticularly useful as it does not require the precise specification of incoming formats.For example to read a line of the form

Node 27 ux 1.0934 uy 3.5e+005textscan only requires the information

%s %d %s %f %s %fwhere %s denotes a character string, %d denotes an integer and %f denotes a fixed orfloating point number. Other formats are available.

Exercises

1. Create a file data.txt with first line:

Node 27 ux 1.0934 uy 3.5e+005

1.15 File Input and Output 15

Enter the code shown below to open the file, read the data and allocate thenumbers to program variables a, b and c. The function textscan produces out-put in a Matlab cell, which differs from an array in that elements of differentsizes and different types may be stored. In this example the name mydata hasbeen chosen for the cell, output corresponding to each item in the format stringis placed in successive positions of mydata. Whereas items from a matrix are re-trieved using enclosing ( and ) parentheses, items from a cell are retrieved usingthe pair { and }.

fid = fopen('data.txt');mydata = textscan(fid, ' %s %d %s %f %s %f ')% retrieve the numbers 27, 1.0934 and 3.5e+005% the strings Node, ux and uy will be held in mydata{1}, mydata{3} and% mydata{5}a = mydata{2}b = mydata{4}c = mydata{6}

The function textscan may be used to collect data from several consecutive linesof data provided the stated format applies. To limit the number of lines that textscanreads for a given format a third parameter is available. A command of the formtextscan(fid, format, n) would apply the format n times from the current position.A command frewind(fid) is available to re-set the internal pointer to start of the file.

A further feature of textscan allows unwanted data to be skipped by insertingan ∗ between the relevant % and the following s, d or f in the format string.

Exercises

1. Add a few more lines of similar data to the file mydata. Use a single textscancommand to read the whole file and notice how the data is retrieved as columnvectors.

2. Modify the format string of the previous question. Choose a selection of columnsof the data file to be retrieved.

1.15.3 Unformatted Input and Output (Saving and RetrievingData)

Workspace variables may be stored more economically as unformatted data (data inbinary form and as such impossible to read with the human eye) in a file having aname with a .mat suffix. Use the commands save to save and load to restore.

For example the command save('savedata.mat', 'x ', 'y ', 'z') would store variablesx, y, z in the file savedata.mat and load('savedata.mat', 'x ', 'y ', 'z') would re-loadthe variables. The commands save and load without parameters save and load allworkspace variables.

16 1 Basic Matlab

Exercises

1. Assign variables to matrices A and B. Save the matrices in unformatted form toa .mat file.

2. Clear A and B from the workspace using the command clear A B. Check thatthey no longer exist.

3. Retrieve the matrices A and B from the .mat file. Check that nothing has beenlost.

Chapter 2Linear Equations

Aims In this chapter we look at ways of solving systems of linear equations,sometimes known as simultaneous linear equations. We investigate

• Gaussian elimination and its variants, to obtain a solution to a system.• partial pivoting within Gaussian elimination, to improve the accuracy of the re-

sults.• iterative refinement after Gaussian elimination, to improve the accuracy of a first

solution.

In some circumstances the use of Gaussian elimination is not recommended andother techniques based on iteration are more appropriate including

• Gauss–Seidel iteration.

We look at the method in detail and compare this iterative technique with directsolvers based on elimination.

Overview We begin by examining what is meant by a linear relationship, beforeconsidering how to handle the (linear) equations which represent such relationships.We describe methods for finding a solution, which simultaneously satisfies severalsuch linear equations. In so doing we identify situations for which we can guaranteethe existence of one, and only one, solution; situations for which more than onesolution is possible; and situations for which there may be no solution at all.

As already indicated, the methods to be considered neatly fall into two categories;direct methods based on elimination; and iterative techniques. We look at each typeof method in detail. For direct methods we need to bear in mind the limitations ofcomputer arithmetic, and hence we consider how best to implement the methods sothat as the algorithm proceeds the accumulation of error may be kept to a minimum.For iterative methods the concern is more related to ensuring that convergence to aspecified accuracy is achieved in as few iterations as possible.

Acquired Skills After reading this chapter you will appreciate that solving lin-ear equations is not as straightforward a matter as might appear. No matter which

C. Woodford, C. Phillips, Numerical Methods with Worked Examples: Matlab Edition,DOI 10.1007/978-94-007-1366-6_2, © Springer Science+Business Media B.V. 2012

17

18 2 Linear Equations

method you use accumulated computer errors may make the true solution unattain-able. However you will be equipped with techniques to identify the presence ofsignificant errors and to take avoiding action. You will be aware of the differencesbetween a variety of direct and indirect methods and the circumstances in which theuse of a particular method is appropriate.

2.1 Introduction

One of the simplest ways in which a physical entity may be seen to behave is to varyin a linear manner with respect to some external influence. For example, the length(L) of the mercury column in a thermometer is accepted as being directly related toambient temperature (T ); an increase in temperature is shown by a correspondingincrease in the length of the column. This linear relationship may be expressed as

L = kT + c.

Here k and c are constants whose values depend on the units in which temperature(degrees Celsius, Fahrenheit, etc.) and length (millimetres, inches, etc.) are mea-sured, and on the bore of the tube. k represents the change in length relative to a risein temperature, whilst c corresponds to the length of the column at zero degrees.We refer to T as the independent variable and L as the dependent variable. If wewere to plot values of L against corresponding values of T we would have a straightline with slope k and intercept on the L axis equal to c.

A further example of a linear relationship is Hooke’s Law (2.1) which relates thetension in a spring to the length by which it has been extended. If T is the tension,x is the extension of the spring, a is the unextended length and λ is the modulus ofelasticity, then we have

T = λ

ax. (2.1)

Typical units are Newtons (for T and λ) and metres (for x and a). A plot of T

against x would reveal a straight line passing through the origin with slope λ/a.An example which involves more than two variables is supplied by Kirchoff’s

Law which states that the algebraic sum of currents meeting at a point must be zero.Hence, if i1, i2 and i3 represent three such currents, we must have

i1 + i2 + i3 = 0. (2.2)

An increase in the value of one of the variables (say i1) must result in a correspond-ing decrease (to the same combined value) in one or more of the other two variables(i2 and/or i3) and in this sense the relationship is linear. For a relationship to be lin-ear, the variables (or constant multiples of the variables) are combined by additionsand subtractions.

2.2 Linear Systems 19

2.2 Linear Systems

In more complicated modelling situations it may be that there are many linear re-lationships, each involving a large number of variables. For example, in the stressanalysis of a structure such as a bridge or an aeroplane, many hundreds (or indeedthousands) of linear relationships may be involved. Typically, we are interested indetermining values for the dependent variables using these relationships so that wecan answer the following questions:

• For a given extension of a spring, what is the tension?• If one current has a specific value, what values for the remaining currents ensure

that Kirchoff’s Law is preserved?• Is a bridge able to withstand a given level of traffic?

As an example of a linear system consider a sporting event where spectators werecharged for admission at the rate of £15.50 for adults and £5.00 for concessions. It isknown that the total takings for the event was £3312 and that a total of 234 spectatorswere admitted to the event. The problem is to determine how many adults watchedthe event.

If we let x represent the number of adults and y the number of concessions thenwe know that the sum of x and y must equal 234, the total number of spectators.Further, the sum of 15.5x and 5y must equal 3312, the total takings. Expressed inmathematical notation, we have

x + y = 234 (2.3)

15.5x + 5y = 3312. (2.4)

Sets of equations such as (2.3) and (2.4) are known as systems of linear equationsor linear systems. It is an important feature of this system, and other systems weconsider in this chapter, that the number of equations is equal to the number ofunknowns to be found.

When the number of equations (and consequently the number of variables inthose equations) becomes large it can be tedious to write the system out in full. Inany case, we need some notation which will allow us to specify an arbitrary linearsystem in compact form so that we may conveniently examine ways of solving sucha system. Hence we write linear systems using matrix and vector notation as

Ax = b (2.5)

where A is a matrix, known as the coefficient matrix (or matrix of coefficients),b is the vector of right-hand sides and x is the vector of unknowns to be determined.Assuming n (the length of x) unknowns to be determined, b must be an n-columnvector and A an m × n square matrix, although for the time being we only considersystems with the same number of equations as unknowns, (m = n).

Problem

Write (2.3), (2.4) in matrix–vector form.

20 2 Linear Equations

Solution

We have

Ax = b, where A =(

1 115.5 5

), x =

⎧⎪⎪⎩x

y

⎫⎪⎪⎭ , b =⎧⎪⎪⎩ 234

3312

⎫⎪⎪⎭ .

A great number of electronic, mechanical, economic, manufacturing and naturalprocesses may be modelled using linear systems in which, as in the above simpleexample, the number of unknowns matches the number of equations. If, as some-times happens, the modelling process results in nonlinear equations (equations in-volving perhaps squares, exponentials or products of the unknowns) it is often thecase that the iterative techniques involved to solve these systems reduce to findingthe solution of a linear system at each iteration. Hence linear equation solvers havea wider applicability than might at first appear to be the case.

Since the modelling process either directly or indirectly yields a system of linearequations, the ability to solve such systems is fundamental. Our interest is in meth-ods which can be implemented in a computer program and so we must bear in mindthe limitations of computer arithmetic.

Problem

The structure shown in Fig. 2.1 shows a pitched portal frame. Using standard engi-neering analysis and assuming certain restrictions on the dimensions of the structure(the details of which need not concern us) it can be shown that the resulting displace-ments and rotations at the points A, B and C may be related to the acting forces andmoments by a set of nine linear equations in nine unknowns. The equations involveconstants reflecting the nature of the material of the structure.

Writing the displacements and rotations in the ascending sequence x1, x2, . . . , x9

and assigning values to the constants and the external loads (the forces and the

Fig. 2.1 Pitched portal frame

2.2 Linear Systems 21

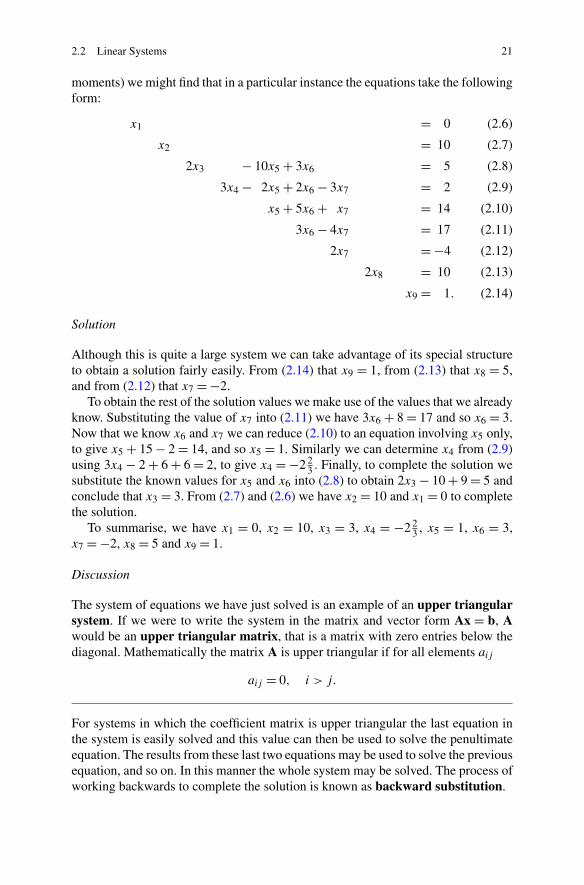

moments) we might find that in a particular instance the equations take the followingform:

x1 = 0 (2.6)

x2 = 10 (2.7)

2x3 − 10x5 + 3x6 = 5 (2.8)

3x4 − 2x5 + 2x6 − 3x7 = 2 (2.9)

x5 + 5x6 + x7 = 14 (2.10)

3x6 − 4x7 = 17 (2.11)

2x7 = −4 (2.12)

2x8 = 10 (2.13)

x9 = 1. (2.14)

Solution

Although this is quite a large system we can take advantage of its special structureto obtain a solution fairly easily. From (2.14) that x9 = 1, from (2.13) that x8 = 5,and from (2.12) that x7 = −2.

To obtain the rest of the solution values we make use of the values that we alreadyknow. Substituting the value of x7 into (2.11) we have 3x6 + 8 = 17 and so x6 = 3.Now that we know x6 and x7 we can reduce (2.10) to an equation involving x5 only,to give x5 + 15 − 2 = 14, and so x5 = 1. Similarly we can determine x4 from (2.9)using 3x4 − 2 + 6 + 6 = 2, to give x4 = −2 2

3 . Finally, to complete the solution wesubstitute the known values for x5 and x6 into (2.8) to obtain 2x3 − 10 + 9 = 5 andconclude that x3 = 3. From (2.7) and (2.6) we have x2 = 10 and x1 = 0 to completethe solution.

To summarise, we have x1 = 0, x2 = 10, x3 = 3, x4 = −2 23 , x5 = 1, x6 = 3,

x7 = −2, x8 = 5 and x9 = 1.

Discussion

The system of equations we have just solved is an example of an upper triangularsystem. If we were to write the system in the matrix and vector form Ax = b, Awould be an upper triangular matrix, that is a matrix with zero entries below thediagonal. Mathematically the matrix A is upper triangular if for all elements aij

aij = 0, i > j.

For systems in which the coefficient matrix is upper triangular the last equation inthe system is easily solved and this value can then be used to solve the penultimateequation. The results from these last two equations may be used to solve the previousequation, and so on. In this manner the whole system may be solved. The process ofworking backwards to complete the solution is known as backward substitution.

22 2 Linear Equations

2.3 Gaussian Elimination

As part of the process we consider how general linear systems may be solved byreduction to upper triangular form.

Problem

Find the numbers of adults and concessions at the sporting event (2.3), (2.4) bysolving the system of two equations in two unknowns.

Solution

In subtracting 15.5 times (2.3) from (2.4) we have 1.5y = 91.5, and combining thiswith the original first equation we have

x + y = 234 (2.15)

−10.5y = −315 (2.16)

which is in upper triangular form. Solving (2.16) gives y = 30 (concessions) andsubstituting this value into (2.15) gives x = 234 − 30 = 204 (adults).

Discussion

The example illustrates an important mechanism for determining the solution toa system of equations in two unknowns, which may readily be extended to largersystems. It has two components:

1. Transform the system of equations into an equivalent one (that is, the solution tothe transformed system is mathematically identical to the solution to the originalsystem) in which the coefficient matrix is upper triangular.

2. Solve the transformed problem using backward substitution.

A linear system may be reduced to upper triangular form by means of successivelysubtracting multiples of the first equation from the second, third, fourth and so on,then repeating the process using multiples of the newly-formed second equation,and again with the newly-formed third equation, and so on until the penultimateequation has been used in this way. Having reduced the system to upper triangularform backward substitution is used to find the solution. This systematic approach,known as Gaussian elimination, is illustrated further in the following example.

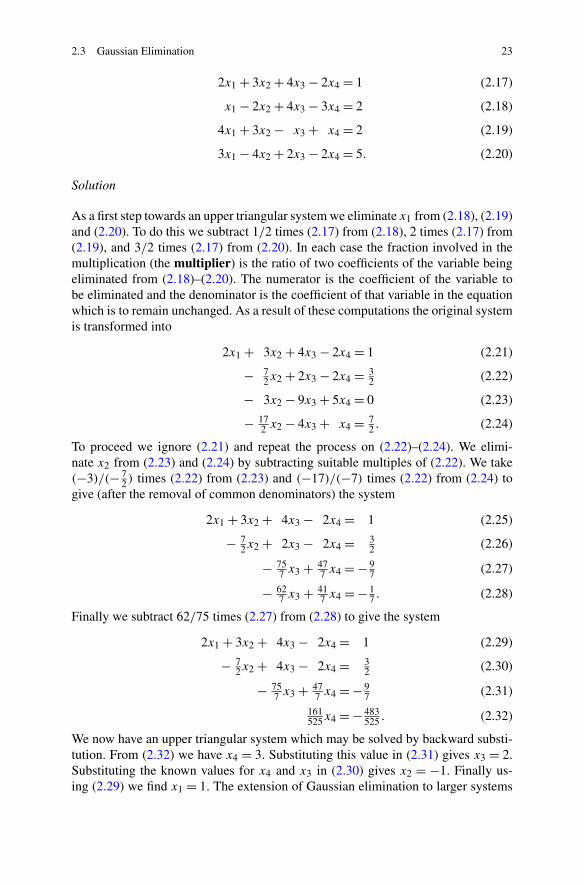

Problem

Solve the following system of four equations in four unknowns

2.3 Gaussian Elimination 23

2x1 + 3x2 + 4x3 − 2x4 = 1 (2.17)

x1 − 2x2 + 4x3 − 3x4 = 2 (2.18)

4x1 + 3x2 − x3 + x4 = 2 (2.19)

3x1 − 4x2 + 2x3 − 2x4 = 5. (2.20)

Solution

As a first step towards an upper triangular system we eliminate x1 from (2.18), (2.19)and (2.20). To do this we subtract 1/2 times (2.17) from (2.18), 2 times (2.17) from(2.19), and 3/2 times (2.17) from (2.20). In each case the fraction involved in themultiplication (the multiplier) is the ratio of two coefficients of the variable beingeliminated from (2.18)–(2.20). The numerator is the coefficient of the variable tobe eliminated and the denominator is the coefficient of that variable in the equationwhich is to remain unchanged. As a result of these computations the original systemis transformed into

2x1 + 3x2 + 4x3 − 2x4 = 1 (2.21)

− 72x2 + 2x3 − 2x4 = 3

2 (2.22)

− 3x2 − 9x3 + 5x4 = 0 (2.23)

− 172 x2 − 4x3 + x4 = 7

2 . (2.24)

To proceed we ignore (2.21) and repeat the process on (2.22)–(2.24). We elimi-nate x2 from (2.23) and (2.24) by subtracting suitable multiples of (2.22). We take(−3)/(− 7

2 ) times (2.22) from (2.23) and (−17)/(−7) times (2.22) from (2.24) togive (after the removal of common denominators) the system

2x1 + 3x2 + 4x3 − 2x4 = 1 (2.25)

− 72x2 + 2x3 − 2x4 = 3

2 (2.26)

− 757 x3 + 47

7 x4 = − 97 (2.27)

− 627 x3 + 41

7 x4 = − 17 . (2.28)

Finally we subtract 62/75 times (2.27) from (2.28) to give the system

2x1 + 3x2 + 4x3 − 2x4 = 1 (2.29)

− 72x2 + 4x3 − 2x4 = 3

2 (2.30)

− 757 x3 + 47

7 x4 = − 97 (2.31)

161525x4 = − 483

525 . (2.32)

We now have an upper triangular system which may be solved by backward substi-tution. From (2.32) we have x4 = 3. Substituting this value in (2.31) gives x3 = 2.Substituting the known values for x4 and x3 in (2.30) gives x2 = −1. Finally us-ing (2.29) we find x1 = 1. The extension of Gaussian elimination to larger systems

24 2 Linear Equations

is straightforward. The aim, as before, is to transform the original system to uppertriangular form which is solved by backward substitution.

Discussion

The process we have described may be summarised in matrix form as pre-multiplying the coefficient matrix A by a series of lower-triangular matrices to forman upper-triangular matrix.

We have⎛⎜⎜⎜⎜⎝

1 0 0 0

0 1 0 0

0 0 1 0

0 0 − 6275 1

⎞⎟⎟⎟⎟⎠

⎛⎜⎜⎜⎜⎝

1 0 0 0

0 1 0 0

0 −3/( 72 ) 1 0

0 − 177 0 1

⎞⎟⎟⎟⎟⎠

⎛⎜⎜⎜⎜⎝

1 0 0 0

− 12 1 0 0

−2 0 1 0

− 32 0 0 1

⎞⎟⎟⎟⎟⎠

⎛⎜⎜⎜⎜⎝

2 3 4 −2

1 −2 4 −3

4 3 −1 1

3 −4 2 −2

⎞⎟⎟⎟⎟⎠

=

⎛⎜⎜⎜⎜⎝

2 3 4 −2

− 72 4 −2

− 757

477

161525

⎞⎟⎟⎟⎟⎠

where it can be seen that sub-diagonal entries correspond to the multipliers in theelimination process. Since the product of lower triangular matrices is also lowertriangular we may write the above as LA = U where L is a lower triangular matrixand U is upper triangular. Since the inverse of a lower triangular matrix is also lowertriangular multiplying both sides by the inverse of L produces

A = LU

where L is another lower triangular matrix and U is upper triangular. This factori-sation is generally known as the LU decomposition. If the factorisation is known itmay be used repeatedly to solve the same set of equations for different right handsides, as will be shown in Sect. 2.3.3.

2.3.1 Row Interchanges

In certain circumstances, Gaussian elimination fails as we see in the following ex-ample.

Problem

Solve the system of 4 equations in 4 unknowns

2.3 Gaussian Elimination 25

2x1 − 6x2 + 4x3 − 2x4 = 8 (2.33)

x1 − 3x2 + 4x3 + 3x4 = 6 (2.34)

4x1 + 3x2 − 2x3 + 3x4 = 3 (2.35)

x1 − 4x2 + 3x3 + 3x4 = 9. (2.36)

Solution

To eliminate x1 from (2.34), (2.35) and (2.36) we take multiples 12 , 2 and 1

2 of(2.33) and subtract from (2.34), (2.35) and (2.36) respectively. We now have thelinear system

2x1 − 6x2 + 4x3 − 2x4 = 8

2x3 + 4x4 = 2 (2.37)

15x2 − 10x3 + 7x4 = −13 (2.38)

− x2 + x3 + 4x4 = 5. (2.39)

Since x2 does not appear in (2.37) we are unable to proceed as before. However asimple re-ordering of the equations enables x2 to appear in the second equation ofthe system and this permits further progress. Exchanging (2.37) and (2.38) we havethe system

2x1 − 6x2 + 4x3 − 2x4 = 8

15x2 − 10x3 + 7x4 = −13 (2.40)

2x3 + 4x4 = 2

− x2 + x3 + 4x4 = 5. (2.41)

Resuming the elimination procedure we eliminate x2 from (2.41) by taking a multi-ple (−1)/15 of (2.40) from (2.41) to give

2x1 − 6x2 + 4x3 − 2x4 = 8

15x2 − 10x3 + 7x4 = −13

2x3 + 4x4 = 2 (2.42)13x3 + 67

15x4 = 6215 . (2.43)

Finally, to eliminate x3 from (2.43) we take a multiple 1/6 of (2.42) from (2.43). Asa result we now have the linear system

2x1 − 6x2 + 4x3 − 2x4 = 8

15x2 − 10x3 + 7x4 = −13

2x3 + 4x4 = 25715x4 = 57

15 ,

which is an upper triangular system that can be solved by backward substitution togive the solution x4 = 1, x3 = −1, x2 = −2, and x1 = 1.

26 2 Linear Equations

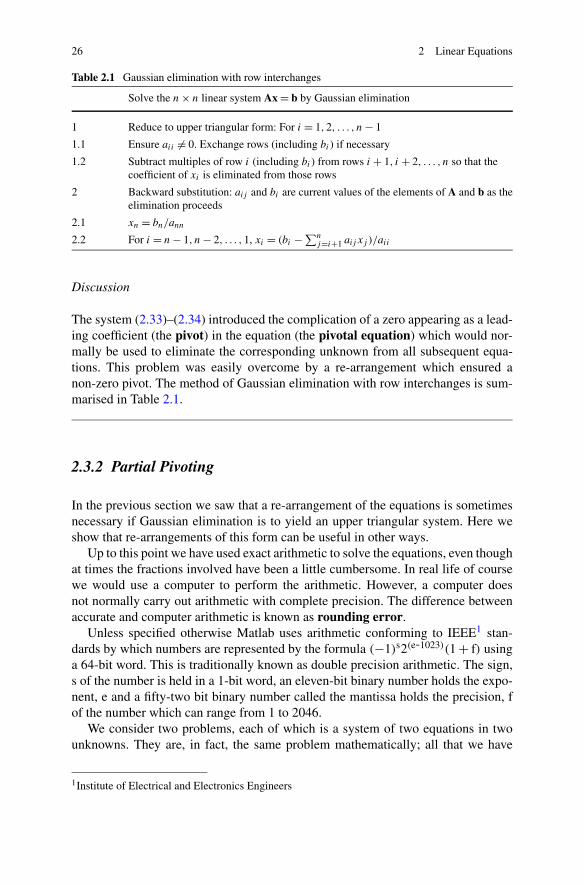

Table 2.1 Gaussian elimination with row interchanges

Solve the n × n linear system Ax = b by Gaussian elimination

1 Reduce to upper triangular form: For i = 1,2, . . . , n − 1

1.1 Ensure aii �= 0. Exchange rows (including bi ) if necessary

1.2 Subtract multiples of row i (including bi ) from rows i + 1, i + 2, . . . , n so that thecoefficient of xi is eliminated from those rows

2 Backward substitution: aij and bi are current values of the elements of A and b as theelimination proceeds

2.1 xn = bn/ann

2.2 For i = n − 1, n − 2, . . . ,1, xi = (bi − ∑nj=i+1 aij xj )/aii

Discussion

The system (2.33)–(2.34) introduced the complication of a zero appearing as a lead-ing coefficient (the pivot) in the equation (the pivotal equation) which would nor-mally be used to eliminate the corresponding unknown from all subsequent equa-tions. This problem was easily overcome by a re-arrangement which ensured anon-zero pivot. The method of Gaussian elimination with row interchanges is sum-marised in Table 2.1.

2.3.2 Partial Pivoting

In the previous section we saw that a re-arrangement of the equations is sometimesnecessary if Gaussian elimination is to yield an upper triangular system. Here weshow that re-arrangements of this form can be useful in other ways.

Up to this point we have used exact arithmetic to solve the equations, even thoughat times the fractions involved have been a little cumbersome. In real life of coursewe would use a computer to perform the arithmetic. However, a computer doesnot normally carry out arithmetic with complete precision. The difference betweenaccurate and computer arithmetic is known as rounding error.

Unless specified otherwise Matlab uses arithmetic conforming to IEEE1 stan-dards by which numbers are represented by the formula (−1)s2(e-1023)(1 + f) usinga 64-bit word. This is traditionally known as double precision arithmetic. The sign,s of the number is held in a 1-bit word, an eleven-bit binary number holds the expo-nent, e and a fifty-two bit binary number called the mantissa holds the precision, fof the number which can range from 1 to 2046.

We consider two problems, each of which is a system of two equations in twounknowns. They are, in fact, the same problem mathematically; all that we have

1Institute of Electrical and Electronics Engineers

2.3 Gaussian Elimination 27

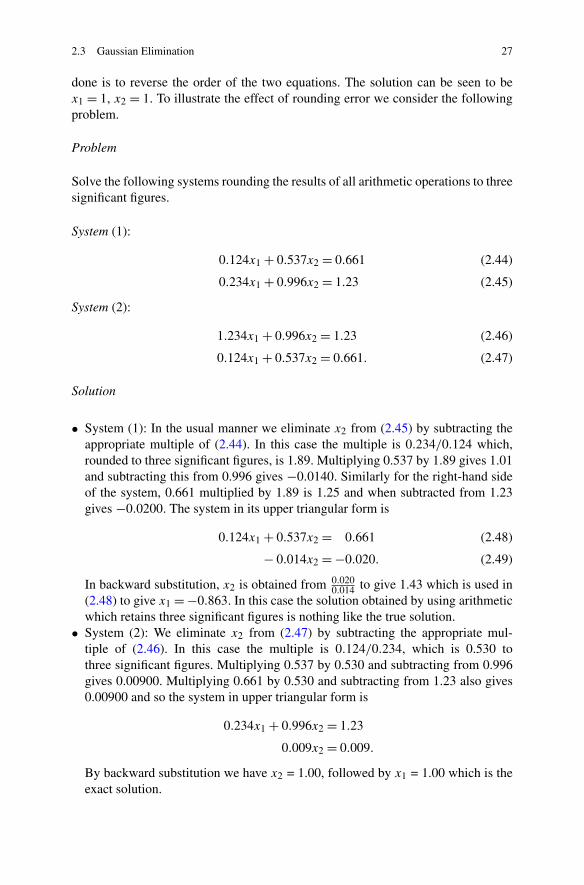

done is to reverse the order of the two equations. The solution can be seen to bex1 = 1, x2 = 1. To illustrate the effect of rounding error we consider the followingproblem.

Problem

Solve the following systems rounding the results of all arithmetic operations to threesignificant figures.

System (1):

0.124x1 + 0.537x2 = 0.661 (2.44)

0.234x1 + 0.996x2 = 1.23 (2.45)

System (2):

1.234x1 + 0.996x2 = 1.23 (2.46)

0.124x1 + 0.537x2 = 0.661. (2.47)

Solution

• System (1): In the usual manner we eliminate x2 from (2.45) by subtracting theappropriate multiple of (2.44). In this case the multiple is 0.234/0.124 which,rounded to three significant figures, is 1.89. Multiplying 0.537 by 1.89 gives 1.01and subtracting this from 0.996 gives −0.0140. Similarly for the right-hand sideof the system, 0.661 multiplied by 1.89 is 1.25 and when subtracted from 1.23gives −0.0200. The system in its upper triangular form is

0.124x1 + 0.537x2 = 0.661 (2.48)

− 0.014x2 = −0.020. (2.49)

In backward substitution, x2 is obtained from 0.0200.014 to give 1.43 which is used in

(2.48) to give x1 = −0.863. In this case the solution obtained by using arithmeticwhich retains three significant figures is nothing like the true solution.

• System (2): We eliminate x2 from (2.47) by subtracting the appropriate mul-tiple of (2.46). In this case the multiple is 0.124/0.234, which is 0.530 tothree significant figures. Multiplying 0.537 by 0.530 and subtracting from 0.996gives 0.00900. Multiplying 0.661 by 0.530 and subtracting from 1.23 also gives0.00900 and so the system in upper triangular form is

0.234x1 + 0.996x2 = 1.23

0.009x2 = 0.009.

By backward substitution we have x2 = 1.00, followed by x1 = 1.00 which is theexact solution.

28 2 Linear Equations

Discussion

We can infer from these two simple examples that the order in which equations arepresented can have a significant bearing on the accuracy of the computed solution.The example is a little artificial, given that a modern computer carries out its arith-metic to many more significant figures than the three we have used here, often asmany as sixteen or more. Nevertheless, for larger systems it may be verified that theorder in which the equations are presented has a bearing on the accuracy of a com-puter solution obtained using Gaussian elimination. The next example describes astrategy for rearranging the equations within Gaussian elimination with a view toreducing the effect of rounding errors on a computed solution. We note in passingthat an LU decomposition which takes account of partial pivoting of a non-singularmatrix A is available in the form PA = LU where L and U are lower and uppertriangular matrices and P is a permutation matrix, a matrix of zeros and ones that inpre-multiplying A performs the necessary row exchanges. For example exchangingrows 2 and 3 of a 3 × 3 matrix A may be achieved by pre-multiplying A by the

permutation matrix

(1 0 00 0 10 1 0

).

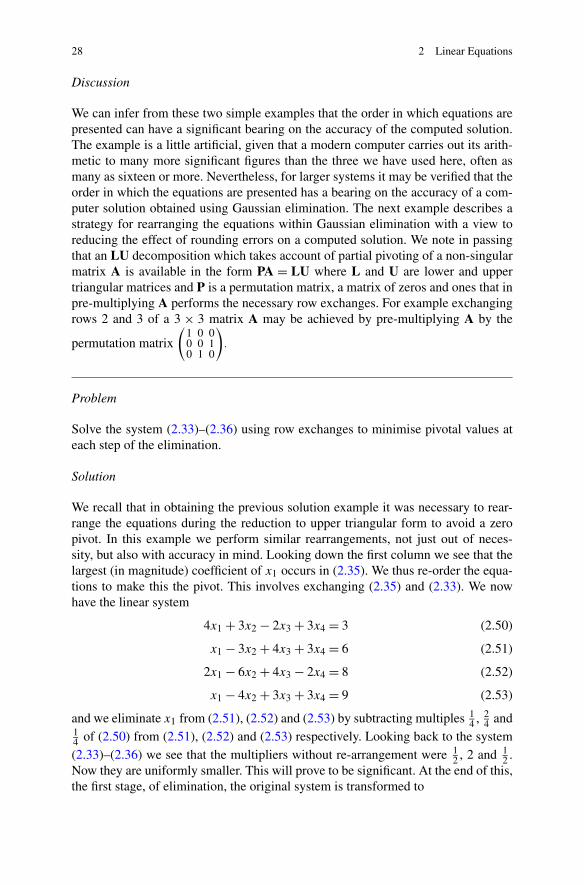

Problem

Solve the system (2.33)–(2.36) using row exchanges to minimise pivotal values ateach step of the elimination.

Solution

We recall that in obtaining the previous solution example it was necessary to rear-range the equations during the reduction to upper triangular form to avoid a zeropivot. In this example we perform similar rearrangements, not just out of neces-sity, but also with accuracy in mind. Looking down the first column we see that thelargest (in magnitude) coefficient of x1 occurs in (2.35). We thus re-order the equa-tions to make this the pivot. This involves exchanging (2.35) and (2.33). We nowhave the linear system

4x1 + 3x2 − 2x3 + 3x4 = 3 (2.50)

x1 − 3x2 + 4x3 + 3x4 = 6 (2.51)

2x1 − 6x2 + 4x3 − 2x4 = 8 (2.52)

x1 − 4x2 + 3x3 + 3x4 = 9 (2.53)

and we eliminate x1 from (2.51), (2.52) and (2.53) by subtracting multiples 14 , 2

4 and14 of (2.50) from (2.51), (2.52) and (2.53) respectively. Looking back to the system(2.33)–(2.36) we see that the multipliers without re-arrangement were 1

2 , 2 and 12 .

Now they are uniformly smaller. This will prove to be significant. At the end of this,the first stage, of elimination, the original system is transformed to

2.3 Gaussian Elimination 29

4x1 − 3x2 − 2x3 + 3x4 = 3

− 3 34x2 + 4 1

2x3 + 2 14x4 = 5 1

4 (2.54)

− 7 12x2 + 5x3 − 3 1

2x4 = 6 12 (2.55)

− 4 34x2 + 3 1

2x3 + 2 14x4 = 8 1

4 . (2.56)

Considering (2.54)–(2.56) we see that the largest coefficient of x2 occurs in (2.55).We exchange (2.55) and (2.54) to obtain

4x1 − 3x2 − 2x3 + 3x4 = 3

− 7 12x2 + 5x3 − 3 1

2x4 = 6 12 (2.57)

− 3 34x2 + 4 1

2x3 + 2 14x4 = 5 1

4 (2.58)

− 4 34x2 + 3 1

2x3 + 2 14x4 = 8 1

4 . (2.59)

To eliminate x2 from (2.58) and (2.59) we take multiples 12 and 19

30 of (2.57) andsubtract them from (2.58) and (2.59) respectively. As a result we have the linearsystem

4x1 − 3x2 − 2x3 + 3x4 = 3

− 7 12x2 + 5x3 − 3 1

2x4 = 6 12

2x3 + 4x4 = 213x3 + 4 7

15x4 = 4 215 . (2.60)

No further row interchanges are necessary since the coefficient of x3 having thelargest absolute value is already in its correct place. We eliminate x3 from (2.60)using the multiplier 1

6 and as a result we have the linear system

4x1 − 3x2 − 2x3 + 3x4 = 3

− 7 12x2 + 5x3 − 3 1

2x4 = 6 12

2x3 + 4x4 = 2

3 45x4 = 3 4

5 .

Solving by backward substitution we obtain x4 = 1.0, x3 = −1.0, x2 = −2.0, andx1 = 1.0.

Discussion

The point of this example is to illustrate the technique known as partial pivoting.At each stage of Gaussian elimination the pivotal equation is chosen to maximisethe absolute value of the pivot. Thus the multipliers in the subsequent subtractionprocess are reduced (a division by the pivot is involved) so that they are all at mostone in magnitude. Any rounding errors present are less likely to be magnified asthey permeate the rest of the calculation.

The 4 × 4 example of this section was solved on a computer using an imple-mentation of Gaussian elimination and computer arithmetic based on a 32-bit word

30 2 Linear Equations

Table 2.2 Gaussian elimination with partial pivoting

Solve the n × n linear system Ax = b by Gaussian elimination with partial pivoting

1 Reduce to upper triangular form: For i = 1,2, . . . , n − 1

1.1 Find the j from j = i, i + 1, . . . , n for which |aji | is a maximum

1.2 If i �= j exchange rows i and j (including bi and bj )

1.3 Subtract multiples of row i (including bi ) from rows i + 1, i + 2, . . . , n so that thecoefficient of xi is eliminated from those rows

2 Backward substitution: aij and bi are current values of the elements of A and b as theelimination proceeds

2.1 xn = bn/ann

2.2 For i = n − 1, n − 2, . . . ,1, xi = (bi − ∑nj=i+1 aij xj )/aii

(equivalent to retaining at least six significant figures). Without partial pivotingthe solution obtained was x1 = 1.00000, x2 = −2.00000, x3 = −0.999999, andx4 = 1.00000, whereas elimination with pivoting gave the same solution except forx3 = −1.00000. This may seem to be an insignificant improvement but the exampleillustrates how the method works. Even with 64-bit arithmetic it is confirmed byexperience that partial pivoting particularly when used in solving larger systems ofperhaps 10 or more equations is likely to be beneficial. As we will see, the form ofthe coefficient matrix can be crucial. For these reasons commercial implementationsof Gaussian elimination always employ partial pivoting. The method is summarisedin Table 2.2.

2.3.3 Multiple Right-Hand Sides

In a modelling process the right-hand side values often correspond to boundaryvalues which may, for example, be the external loads on a structure or the resourcesnecessary to fund various activities. As part of the process it is usual to experimentwith different boundary conditions in order to achieve an optimal design. Gaussianelimination may be used to solve systems having several right-hand sides with littlemore effort than that involved in solving for just one set of right-hand side values.

Problem

Find three separate solutions of the system of (2.33)–(2.36) corresponding to threedifferent right-hand sides.

Writing the system in the form Ax = b we have three different vectors b, namely⎧⎪⎪⎪⎪⎪⎪⎪⎪⎪⎩8639

⎫⎪⎪⎪⎪⎪⎪⎪⎪⎪⎭ ,

⎧⎪⎪⎪⎪⎪⎪⎪⎪⎪⎩23

−14

⎫⎪⎪⎪⎪⎪⎪⎪⎪⎪⎭ and

⎧⎪⎪⎪⎪⎪⎪⎪⎪⎪⎩1

−6−3

9

⎫⎪⎪⎪⎪⎪⎪⎪⎪⎪⎭ .

2.3 Gaussian Elimination 31

The three problems may be expressed in the following compact form

2x1 − 6x2 + 4x3 − 2x4 = 8, 2, 1

x1 − 3x2 + 4x3 + 3x4 = 6, 3,−6

4x1 + 3x2 − 2x3 + 3x4 = 3,−1,−3

x1 − 4x2 + 3x3 + 3x4 = 9, 4, 9.

Solution

We can solve all three equations at once by maintaining not one, but three columnson the right-hand side. The interchanges required by partial pivoting and the oper-ations on the coefficient matrix do not depend on the right-hand side values and soneed not be repeated unnecessarily. After the first exchange we have

4x1 + 3x2 − 2x3 + 3x4 = 3,−1,−3

x1 − 3x2 + 4x3 + 3x4 = 6, 3,−6

2x1 − 6x2 + 4x3 − 2x4 = 8, 2, 1

x1 − 4x2 + 3x3 + 3x4 = 9, 4, 9

followed by

4x1 − 3x2 − 2x3 + 3x4 = 3, −1, −3

− 3 34x2 + 4 1

2x3 + 2 14x4 = 5 1

4 , 3 14 , −5 1

4

− 7 12x2 + 5x3 − 3 1

2x4 = 6 12 , 2 1

2 , 2 12

− 4 34x2 + 3 1

2x3 + 2 14x4 = 8 1

4 , 4 14 , 9 3

4 .

Continuing the elimination we obtain

4x1 − 3x2 − 2x3 + 3x4 = 3, −1, −3

− 7 12x2 + 5x3 − 3 1

2x4 = 6 12 , 2 1

2 , 2 12

2x3 + 4x4 = 2, 2, −6 12

3 45x4 = 3 4

5 , 2 13 , 9 1

4 .

Backward substitution is applied to each of the right-hand sides in turn to yieldthe required solutions, which are (1,−2,−1,1)T , (−0.2456,−0.7719,−0.2281,

0.6190)T and (−1.4737,−6.8816,−8.1184,2.4342)T (to 4 decimal places).

Discussion

In solving a system of equations with several right-hand sides the reduction to uppertriangular form has been performed once only. This is significant since the compu-tation involved in the elimination process for larger systems is significantly greaterthan the computation involved in backward substitution and hence dominates theoverall effort of obtaining a solution. If the system Ax = b is to be repeatedly solvedfor the same A but for different b it makes sense to save and re-use the LU decom-position of A.

32 2 Linear Equations

2.4 Singular Systems

Not all systems of linear equations have a unique solution. In the case of two equa-tions in two unknowns we may have the situation whereby the equations may berepresented as parallel lines in which case there is no solution. On the other handthe representative lines may be coincident in which case every point on the linesis a solution and so we have an infinity of solutions. These ideas extend to largersystems. If there is no unique solution then there is either no solution at all or elsethere is an infinity of solutions and we would expect Gaussian elimination to breakdown at some stage.

Problem

Solve the system

2x1 − 6x2 + 4x3 − 2x4 = 8 (2.61)

x1 − 3x2 + 4x3 + 3x4 = 6 (2.62)

x1 − x2 + 2x3 − 5x4 = 3 (2.63)

x1 − 4x2 + 3x3 + 3x4 = 9. (2.64)

Solution

Applying Gaussian elimination with partial pivoting to the system we first eliminatex1 to obtain

2x1 − 6x2 + 4x3 − 2x4 = 8

2x3 + 4x4 = 2

2x2 − 4x4 = −1

− x2 + x3 + 4x4 = 5.

Partial pivoting and elimination of x2 gives

2x1 − 6x2 + 4x3 − 2x4 = 8

2x2 − 4x4 = −1

2x3 + 4x4 = 2

x3 + 2x4 = 4 12 .

Finally, elimination of x3 gives

2x1 − 6x2 + 4x3 − 2x4 = 8

2x2 − 4x4 = −1

2x3 + 4x4 = 2

0x4 = 3 12 .

2.5 Symmetric Positive Definite Systems 33

Clearly we have reached a nonsensical situation which suggests that 0 is equal to3 1

2 . This contradiction suggests that there is an error or a wrong assumption in themodelling process which has provided the equations.

Changing the right-hand side of (2.61)–(2.64) to (8,6,3,5.5)T and applyingelimination gives

2x1 − 6x2 + 4x3 − 2x4 = 8

2x2 − 4x4 = −1

2x3 + 4x4 = 2

0x4 = 0

which is more sensible than before, if a little odd. There is no longer any contra-diction. In effect we are free to choose any value we like for x4 and to employ thisvalue into the backward substitution process. In the first system we had no solution;now we have an infinity of solutions.

Discussion