nursery management understanding and managing finance. session 4

TRANSCRIPT

Nursery ManagementUnderstanding and Managing Finance

.

Session 4

Financial Terms

Income – An amount of money which comes in to, or is earned by, the business during an accounting period - sometimes called Revenue.

Expenditure – An amount of money which has been spent by, or goes out from, the business during an accounting period.

Creditors - suppliers of goods and services whose invoices are still outstanding for payment(someone to whom you owe money)

Debtors - customers who owe the organisation money

Assets and Claims

We have already established previously that: Assets are items which the organisations OWNS Claims or Liabilities are items which the

organisation OWES

We now look at these in more detail

Examples of Assets

1. Money in the bank.

2. Debts owed to the business by its customers

3. Land and property-if the business owns them

4. Machinery, mechanical and electrical equipment

5. Stock

6. Computers

7. Goodwill, patents and other ‘intangibles’ which can have a monetary value attached to them.

Activity 1

Which of the following do you think are assets?

Money in a supermarket till. Property deeds held by a nursery. Scrap paper in an office recycling bin. A computer expert hired by the nursery to

update their computer software.

Activity 1- Solution

Which of the following do you think are assets?

Money in a supermarket till. Asset (cash)Property deeds held by a nursery) Asset (or at least the property it represents is an asset)Scrap paper in an office recycling bin. Asset (until it is thrown away)A computer expert hired by the nursery. Not an Asset (difficult to assess in monetary terms, and

the business does not have exclusive rights.)

Claims (or Liabilities)

Claims are what a business ‘owes’.There are two forms of claims:

1. Capital: This is the owner’s (or in the case of a limited company shareholders’) investment in the business.

2. Liabilities: These are claims on the business made by external individuals and organisations, and include: Trade Creditors Bank and other Loans Unpaid Tax

Examples of Claims

1. Bank Overdrafts.

2. Debts owed by the business to its suppliers.

3. Bank Loans

4. Tax

5. Shareholder’s Capital (if there are any)

6. Profit

7. Dividends(if the business is a limited company).

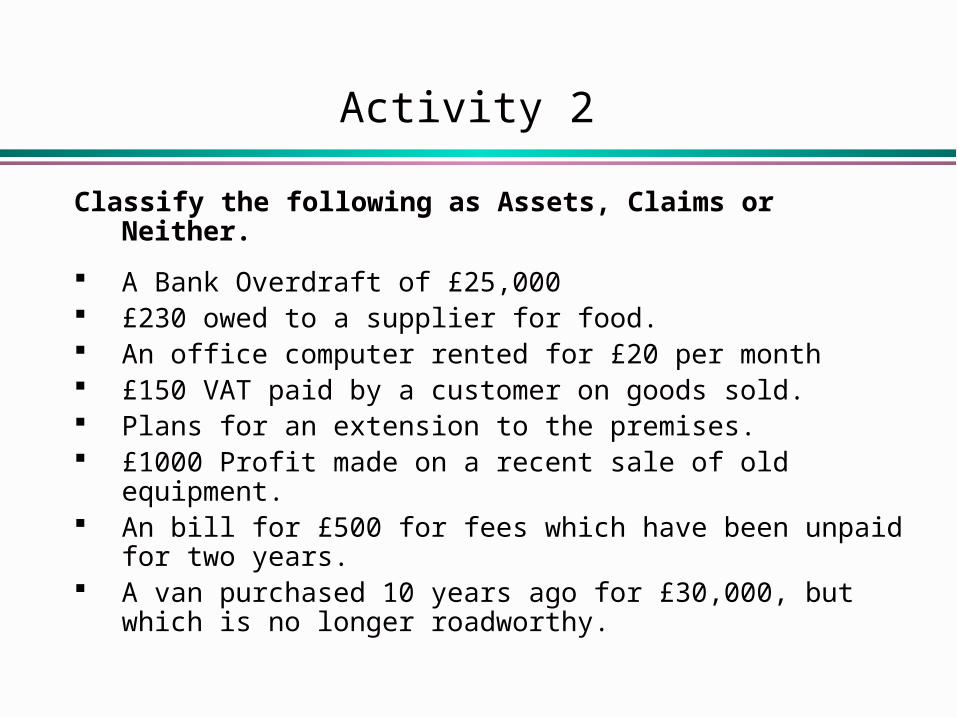

Activity 2

Classify the following as Assets, Claims or Neither.

A Bank Overdraft of £25,000 £230 owed to a supplier for food. An office computer rented for £20 per month £150 VAT paid by a customer on goods sold. Plans for an extension to the premises. £1000 Profit made on a recent sale of old equipment. An bill for £500 for fees which have been unpaid for

two years. A van purchased 10 years ago for £30,000, but which

is no longer roadworthy.

Activity 2- solution

Classify the following as Assets, Claims or Neither.

A Bank Overdraft of £25,000. CLAIM £230 owed to a supplier for food. CLAIM An office computer rented for £20 per month. ASSET £150 VAT paid by a customer on goods sold. CLAIM Plans for an extension to the premises. ASSET £1000 Profit made on a recent sale of old equipment.

CLAIM An bill for £500 for nursery fees which have been unpaid for two

years. NEITHER

A Van purchased 10 years ago for £30,000, but which is no longer roadworthy. NEITHER

Balance Sheets

The purpose of a Balance Sheet is to measure the accumulated wealth at a specific point in time. This gives a “snapshot” of the financial position of the organisation, balancing Assets against Capital and Liabilities.

Balance Sheets often show the last 2 years to allow comparison

Balance Sheet Formats

Balance Sheet can be produced in two different ways:

Horizontal Format This is the easier format to understand, and the type you

have already seen.

Vertical Format This is used mainly to communicate to shareholders the

size of their investment in a company.

Balance Sheets In Horizontal Format

This method is the easiest to understand, as the ‘balance’ figure can be seen at once.

Balance Sheet Layout(Horizontal Format)

Fixed Assets Capital and

Reserves + + Current Assets Long-term

Liabilities+ Current Liabilities

Total Assets Total ClaimsBALANCE

Sample Balance Sheet (Horizontal format)

Fixed Assets Capital and ReservesLand £ 120,000 Share capital £ 100,000Buildings £ 150,000 Retained profit £ 120,000Fix and Fit £ 75,000 Total £ 220,000Total £ 345,000 L/T Liabilities

Loan £ 250,000Current Assets Total £ 250,000Stock £ 55,000 Current LiabilitiesDebtors £ 75,000 Creditors £ 22,000Bank £ 25,000 Tax and VAT £ 8,000Total £ 155,000 Total £ 30,000

________ ________£ 500,000 £ 500,000

The two bottom lines Balance

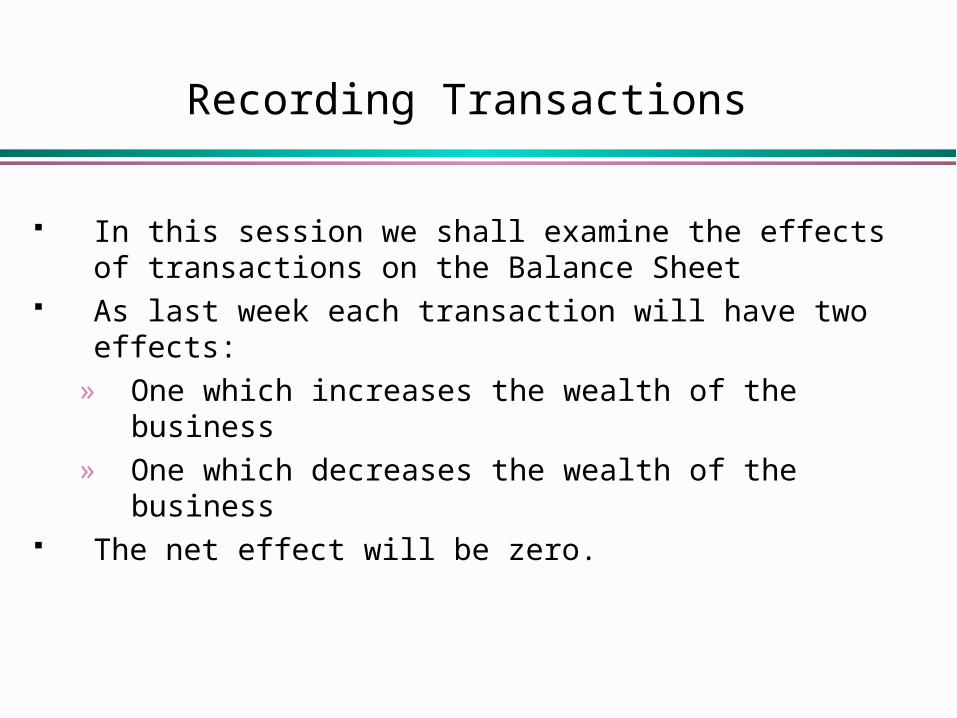

Recording Transactions

In this session we shall examine the effects of transactions on the Balance Sheet

As last week each transaction will have two effects:» One which increases the wealth of the business» One which decreases the wealth of the business

The net effect will be zero.

Examples of Transactions

Examine the following Example Carefully:

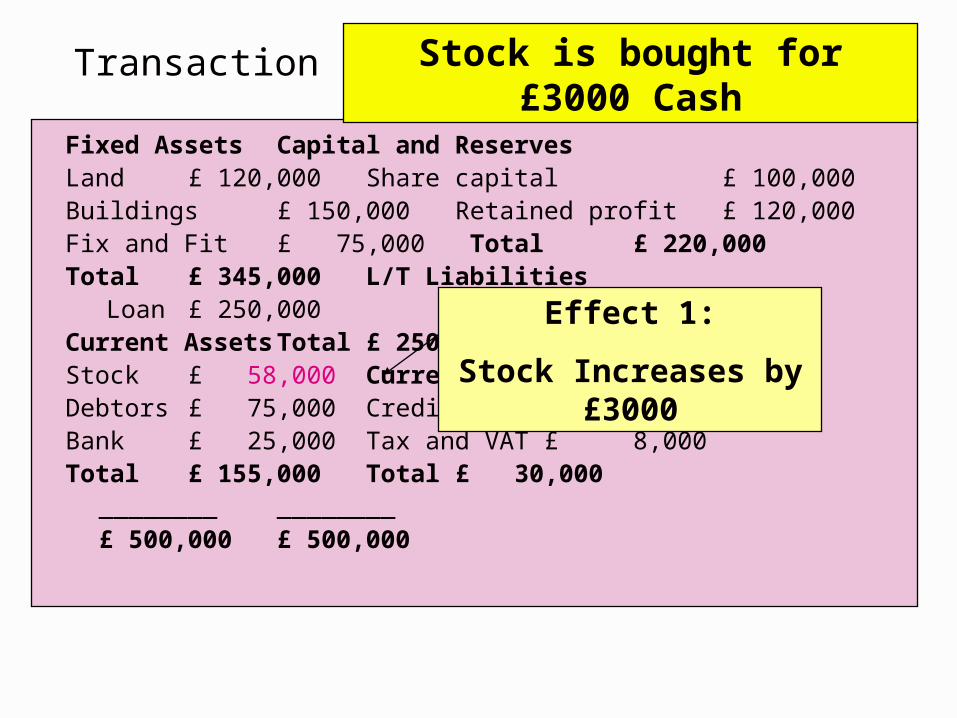

Transaction

Stock(food and art equipment for example)is bought for £3000 Cash

Transaction

Fixed Assets Capital and ReservesLand £ 120,000 Share capital £ 100,000Buildings £ 150,000 Retained profit £ 120,000Fix and Fit £ 75,000 Total £ 220,000Total £ 345,000 L/T Liabilities

Loan £ 250,000Current Assets Total £ 250,000Stock £ 55,000 Current LiabilitiesDebtors £ 75,000 Creditors £ 22,000Bank £ 25,000 Tax and VAT £ 8,000Total £ 155,000 Total £ 30,000

________ ________£ 500,000 £ 500,000

Stock is bought for £3000 Cash

Transaction

Fixed Assets Capital and ReservesLand £ 120,000 Share capital £ 100,000Buildings £ 150,000 Retained profit £ 120,000Fix and Fit £ 75,000 Total £ 220,000Total £ 345,000 L/T Liabilities

Loan £ 250,000Current Assets Total £ 250,000Stock £ 55,000 Current LiabilitiesDebtors £ 75,000 Creditors £ 22,000Bank £ 25,000 Tax and VAT £ 8,000Total £ 155,000 Total £ 30,000

________ ________£ 500,000 £ 500,000

Stock is bought for £3000 Cash

Effect 1:

Stock Increases by £3000

Transaction

Fixed Assets Capital and ReservesLand £ 120,000 Share capital £ 100,000Buildings £ 150,000 Retained profit £ 120,000Fix and Fit £ 75,000 Total £ 220,000Total £ 345,000 L/T Liabilities

Loan £ 250,000Current Assets Total £ 250,000Stock £ 58,000 Current LiabilitiesDebtors £ 75,000 Creditors £ 22,000Bank £ 25,000 Tax and VAT £ 8,000Total £ 155,000 Total £ 30,000

________ ________£ 500,000 £ 500,000

Stock is bought for £3000 Cash

Effect 1:

Stock Increases by £3000

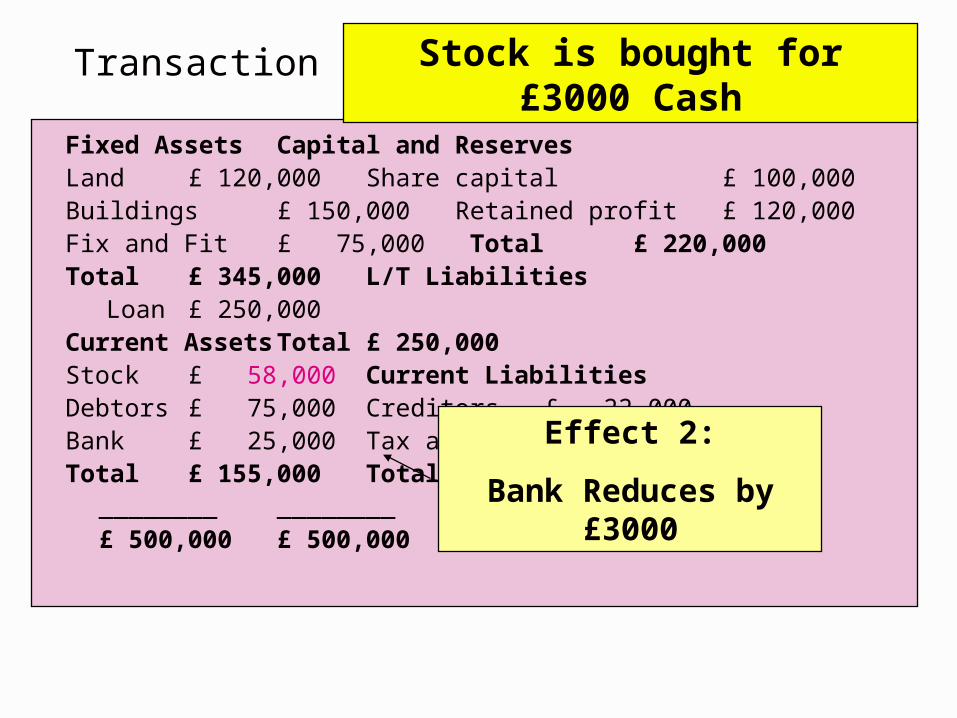

Transaction 1

Fixed Assets Capital and ReservesLand £ 120,000 Share capital £ 100,000Buildings £ 150,000 Retained profit £ 120,000Fix and Fit £ 75,000 Total £ 220,000Total £ 345,000 L/T Liabilities

Loan £ 250,000Current Assets Total £ 250,000Stock £ 58,000 Current LiabilitiesDebtors £ 75,000 Creditors £ 22,000Bank £ 25,000 Tax and VAT £ 8,000Total £ 155,000 Total £ 30,000

________ ________£ 500,000 £ 500,000

Stock is bought for £3000 Cash

Effect 2:

Bank Reduces by £3000

Transaction

Fixed Assets Capital and ReservesLand £ 120,000 Share capital £ 100,000Buildings £ 150,000 Retained profit £ 120,000Fix and Fit £ 75,000 Total £ 220,000Total £ 345,000 L/T Liabilities

Loan £ 250,000Current Assets Total £ 250,000Stock £ 58,000 Current LiabilitiesDebtors £ 75,000 Creditors £ 22,000Bank £ 22,000 Tax and VAT £ 8,000Total £ 155,000 Total £ 30,000

________ ________£ 500,000 £ 500,000

Stock is bought for £3000 Cash

Effect 2:

Bank Reduces by £3000

Transaction

Fixed Assets Capital and ReservesLand £ 120,000 Share capital £ 100,000Buildings £ 150,000 Retained profit £ 120,000Fix and Fit £ 75,000 Total £ 220,000Total £ 345,000 L/T Liabilities

Loan £ 250,000Current Assets Total £ 250,000Stock £ 58,000 Current LiabilitiesDebtors £ 75,000 Creditors £ 22,000Bank £ 22,000 Tax and VAT £ 8,000Total £ 155,000 Total £ 30,000

________ ________£ 500,000 £ 500,000

Stock is bought for £3000 Cash

Net Effect :

Stock Increases by £3000

Cash Reduces by £3000

No Change in Balances

Vertical Format Balance Sheets

Although the Horizontal Format for Balance Sheets is easy to understand, many companies prefer to use the Vertical Format.

This Balance sheet is divided into two parts:» The top part shows the Net Assets of the

Company, that is, what the company owns when all debts and loans and outstanding tax bills etc. have been paid off.

» The bottom part shows the Shareholders’ Claim; in other words, all the money that is invested in the company through share owning.

SAMPLE BALANCE SHEET (VERTICAL FORMAT)Fixed Assets Land £ 120,000

Buildings £ 150,000Fix and Fit £

75,000Total £ 345,000

Current Assets Stock £ 55,000Debtors £ 75,000Bank £ 25,000Total £ 155,000

Current LiabilitiesCreditors £ 22,000Tax and VAT £ 8,000Total £ (30,000)Net Current Assets £ 125,000Total Assets £ 470,000Less Long term liabilities (Loan) £(250,000)

£ 220,000Capital and ReservesShare capital £ 100,000Retained profit £ 120,000

£ 220,000