nuts and bolts of foreign "in-country" operations ….an hr focus marjorie forster –...

TRANSCRIPT

Nuts and Bolts of Foreign "In-Country" Operations

….an HR focus

Marjorie Forster – University of Maryland BaltimoreBill Ferreira – Hogan Lovells

Bob Lammey – High Street PartnersNovember 6, 2012

2

Who are these guys?

Bob Lammey – Sr. Director of Higher Education

Leads higher education practice at HSP Prior to joining HSP, Bob was Director of Global Business

Compliance at Harvard University CPA, began his career at Ernst & Young

Bill Ferreira – Attorney at Hogan Lovells, Washington, DC

Hogan Lovells is a law firm that advises colleges, universities, and nonprofits organizations

Specializes in federal grants and contracts Has worked on dozens of international projects

3

What do we want to get out of today??

HR International Risks…….

• Legal risk

• Financial risk

• Reputational risk

• Human capital risk

4

……are hiding in many places

5

Why do we need to think differently ?

• Outside the “safe haven” of home campus….– No legal structure already established for HR framework

– Minimal hiring and employee oversight controls

– Unfamiliar labor and tax laws

– Changing HR landscapes

– Health and Safety considerations different

– Comp and benefits may be very different from US/Canadian standards

6

Trends with International Research in Higher Education

7

Overall Spending on Global Health Research

8

Ranking of countries benefitting from grant awards2004 to 2009

1. India2. Nigeria3. Tanzania4. Ethiopia5. Kenya6. Uganda7. South Africa8. Mozambique9. Zambia10.China

Detect a trend????

9

Why should we be worried?

The War Stories

• Independent contractors come forward claiming to be employees– Settlements in excess of $500,000– 3 cases in last few months - all “once friendly” contractors

• Foreign partner non-compliance– Not registered as employer– No taxes paid or year end filings made– Illegally hired employees as contractors

• Employee detained in India– Stopped at border flying home– Prevented from leaving country until visa/tax situation was

resolved by U.S. university

10

10

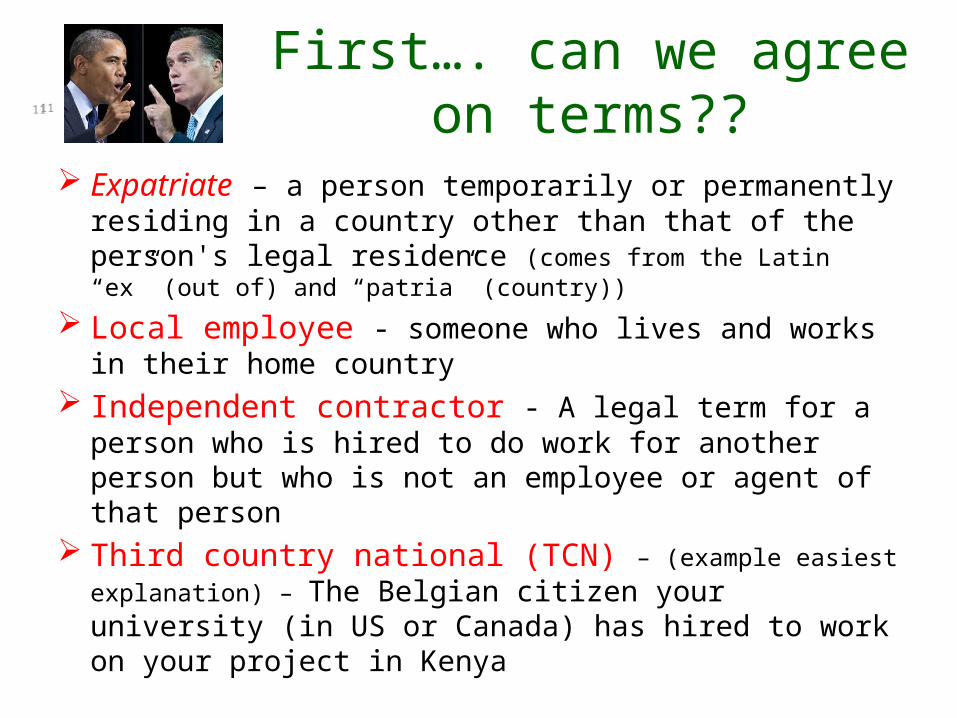

First…. can we agree on terms??

Expatriate – a person temporarily or permanently residing in a country other than that of the person's legal residence (comes from the Latin “ex” (out of) and “patria” (country))

Local employee - someone who lives and works in their home country

Independent contractor - A legal term for a person who is hired to do work for another person but who is not an employee or agent of that person

Third country national (TCN) – (example easiest explanation) – The Belgian citizen your university (in US or Canada) has hired to work on your project in Kenya

1111

12

How do we know which HR practices may be of greatest risk?

13

Myth #1: “We don’t have HR compliance issues…We’re just doing research.”

• Most common HR compliance issues :

– “Partner” or subcontractor acts as employer/agent, but doesn’t have proper registration in-country

– Contractors are really employees of university

– Home country employees working in foreign country for more than “a few weeks”

– Home country employees entering country with incorrect visa

14

Myths #2-5

2. Non-profit status in U.S. means we don’t have to worry about employer obligations

3. Educational or research activities don’t require registration as an employer

4. Our foreign “contractors” would never turn on us

5. US/Canadian employees don’t need to worry because they’re paying taxes in home country already

15

Overview of HR issues

High

Risk

Lev

el

Hiring independent contractors (Admin burden – low)

Immigration – Home employees and TCNs (Admin burden – med)

Taxation – Home employees and TCNs (Admin burden – very high)

Locally hired employees (Admin burden – high)

16

Let’s go deep on some of these issues….

Immigration

Faculty and staff abroad

Independent contractors

Hiring local employees

17

Immigration Applies to expats and TCNs

Visas often require a local host to sponsor

Without correct visa, employee is non-compliant from day ONE

“Tourist” visas commonly not legally compliant form of documentation for employees working in a foreign country

Employees often in position of having to lie to passport control upon arrival at airport or border

University would be considered to blame since employee is working for university

Left to their own auspices and due to lack of understanding of immigration laws, employees will frequently not take steps to get correct visa

18

Faculty and staff working abroad

Compliance issues….

Visas and work permits

Individual taxation

• 183 day “rule of thumb”

• Advances and personal bank accounts

• Should be paying taxes somewhere

FBAR reporting (mentioned in finance section)

19

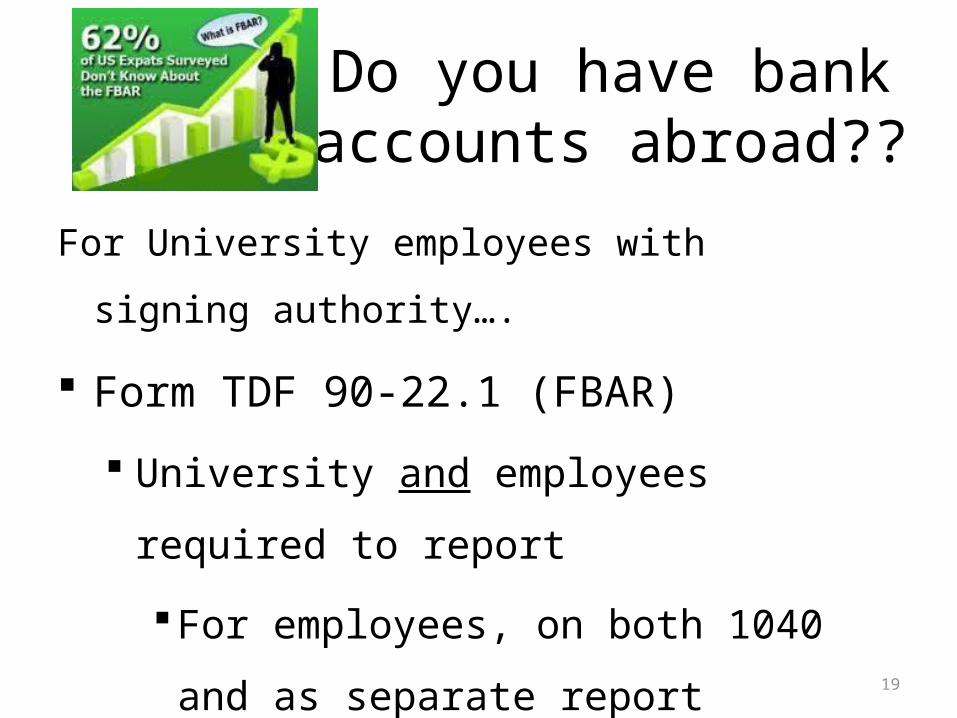

Do you have bank accounts abroad??

For University employees with signing authority….

Form TDF 90-22.1 (FBAR)

University and employees required to report

For employees, on both 1040 and as

separate report

May not be applicable for public universities

Faculty and staff working abroad

Logistical and safety issues…

“Cash in a suitcase”

Advances and personal bank accounts

Safety in developing nations

20

Cash management – HR –related issuesIssues:• “Cash in a suitcase”• Personal bank accounts• Advances/safety concerns• Tax implications for employees

Solutions: Client trust accounts Prepaid and reloadable cards Third party or partner account Bank transfer

21

Overseas employment – income tax principles

General Principles• As a general principle, an institution that has employees

working overseas is required to withhold taxes for the host country.

• The U.S. is one of the few countries that tax its citizens on worldwide income; therefore, for U.S. citizens, the U.S. employer is obligated to withhold U.S. income taxes unless the country in which the services are performed has a tax code that requires local tax withholding for that country’s taxes.

• Normally, a U.S. citizen can credit any income taxes paid to the foreign country against his or her U.S. income tax liability. U.S. citizens also may be eligible for the “foreign earned income exclusion”.

23

Tax treaties• What’s great about them?

– Easy to find – just google “US tax treaties” or “Canadian tax treaties”– Definition for Permanent Establishment (which may be triggered by

employees)– Defines and often extends number of days US/Canadian citizen can work

in country without tax issue (immigration still an issue!)– Info about tax exemptions which may apply for teaching or research

• And……not so great…..– Not written for higher ed/NFP audience (lots of info not relevant)– Certainly doesn’t address all issues with registration or HR– 66 treaties for US……..90 for Canada

• US has only 3 treaties of 54 African countries (Canada has 14!)• But treaties exist with countries like….Kyrgyzstan (can I buy a vowel???) and Malta

(100k fewer people than smallest US state!)

24

Tax equalization for home employees paying taxes abroad

• What is it?– The offsetting of tax difference between a home country and a foreign country

so that working abroad is tax neutral for the worker• Who does it apply to?

– Employees working abroad who are on the home country payroll but subject to foreign country income tax

• Why you probably need it– You will either pay more in the end or expose the university and the employee

to significant risk• How is it calculated?

– Using employee’s personal tax situation to determine what net pay would have been in the home country in lieu of the assignment

• How would it be administered?– Not easily! Through home country payroll, as well as through local payroll

provider

A moment to consider other tax-related obligations of the university

• U.S. tax filings associated with foreign “boots on the ground” activity can be a minefield. – FBAR– Information filings associated with foreign funds transfer (Form 5471)– Form 990

• Schedule F of Form 990 requires the organization to provide information on activities conducted outside the U.S. at any time during the tax year.

• To the extent the institution establishes special purpose vehicles, such as separate legal entities, in the U.S. or elsewhere to facilitate foreign activity, Schedule R of Form 990 may require a report of such entities as “related organizations,” and a report of transactions between such entities and the institution.

• Playing “catch up” is dangerous territory.• Consult tax counsel.

26

Engaging Independent Contractors – Why so high risk?

• Employee vs contractor - #1 compliance issue today

• Do not assume that foreign employee vs contractor classification is foreign country is not as stringent as the U.S.

• An agreement that person is a contractor is not enough!

• Fines would far exceed cost of hiring as employee

• Countries taking aggressive measures to encourage “whistleblowers”

• Both contractor and local tax authority can pursue claims/fines

27

Red flag characteristics• The worker is paid a fixed amount per month

• The worker has decision-making authority and/or can sign contracts on behalf of university

• Worker does not have discretion on how and when to complete tasks

• A high percentage of the worker’s income comes from the university

• The worker is not part of a separate organization of 3 or more people, and does not have a distinct separate identity (such as business cards)

• The worker works a set number of hours as specified by a contract

• The worker is entitled to overtime pay, bonuses or benefits (such as paid

leave)

• The worker is provided with equipment or tools of trade (such as a computer)

28

Steps to reduce risk (but won’t eliminate)

Agreement in writing

Policy for evaluating employee vs contractor in foreign country

Educate administrators and PI’s (see next slide)

Require contractor to obtain certificate from local tax authority

29

Tips on hiring a contractor

Don’t do this Pay for time worked Give them tools Worker self-employed Paid leave (vacation) Supervise and direct daily Nothing in writing Require contractor

to perform all work Executing contracts or making

decisions

Do this!

Pay for milestone or task

Worker provides own tools

Works for company (3 or more)

No “employee” benefits

Flexibility to set own hours

Contract stating terms

Work can be performed by others at worker’s discretion

No decision making on behalf of university!

30

What are requirements of an employer?

The university qualifies as an employer if……

Those being paid qualify as employee, not contractor You have control over those being engaged by partner You’re considered an employer in a country that your

home country employees are working in

What is often required: Tax withholdings Tax payments to local authority Statutory benefits (pension, medical, etc.)

Local employee considerations• Employment contracts (often required by law, and in local language)

• Understand termination regulations before hiring

• Compensation and Benefits

• Local laws and customs relate differently to local nationals, US expats, third-country nationals, and contractors

• There should be an understanding of what benefits are mandatory in-country, then what incrementally would be “market norm”

• Comparison with the US benefit plan can certainly be a factor in evaluating local benefits, but it shouldn’t be the only one

32

Summary of options to support employees abroad

(assuming individual does not qualify as independent contractor)

– Standard exemption period for working in country? (employees on US payroll only)

• Citizenship may impact period, and a filing may also apply

– Do teaching or research exemptions apply? (employees on US payroll only)

• Citizenship may determine, and a filing may also apply

– “Manage” days working in foreign country (employees on US payroll only)

– Special exemption granted by foreign gov’t? (rare – typically research in developing nations)

– Third party “partner” (a university or subcontractor)

– Professional employment organization (PEO)

– Non-resident employer registration (NRE), engaging payroll provider

– Entity registration, engaging payroll provider

• NOT A RECOMMENDED OPTION!– Telling the employee it is their responsibility to report

and pay their own taxes

33

Federally Sponsored Projects

Federal Research Considerations• Foreign bank accounts

– Funding to a university official’s personal foreign account for grant expenses is not ideal– How do we address pre-registration programming?

• Foreign taxes (including Value Added Tax) on equipment, supplies, vehicles, etc. purchased in host country– NIH GPS: “Value-added taxes and other related charges are unallowable on foreign

grants or the foreign component of a domestic grant”– Circular A-21: Local taxes are allowable if no tax exemption is available– The exemption process can be long and cumbersome– Customs duties present similar issues

• Currency fluctuation– Is any part of currency losses an allowable cost?

• Disposition of assets upon expiration/termination of project– Be aware of foreign law requirement to keep grant-funded assets in host country

Federal Research Considerations• Credentialing medical professionals

– Can U.S. clinicians freely practice abroad? In developing countries?

• Patient care issues– Licensing and credentialing of health care professionals– Treatment of patient records; privacy– Storing and dispensing medications– Disposal of biohazards and other waste

• Local procurement complications – USAID and other host country rules

• Foreign gift and contract reports

36

What should you do?

Raise issues when you see them…

37

“International project alert!” Engaging contractors

Having US employees or TCNs traveling to foreign country

37

Using subcontractor or local partner to “hire” on your behalf

If project will be…….

Who you gonna call?

38

General Counsel’s Office

External Professional help

38

Project team or PI

39

NACUBO Resources forInternational Activities

International Resource Center (IRC)

International Webcast Series (available on www.nacubo.org)

40

Questions?

41

Congratulations – you made it!