october 2006 securitisation in russia and cis the broad strokes and fine lines of securitisation...

TRANSCRIPT

October 2006

Securitisation in Russia and CIS

The broad strokes and fine lines of securitisation

landscape

2

Table of Contents

1 CIS Market Update 3

2 Future development of securitisation in Russia and Kazakhstan 8

3 Kazakhstan case study 16

4 Panel discussion 26

1 CIS Market Update

4

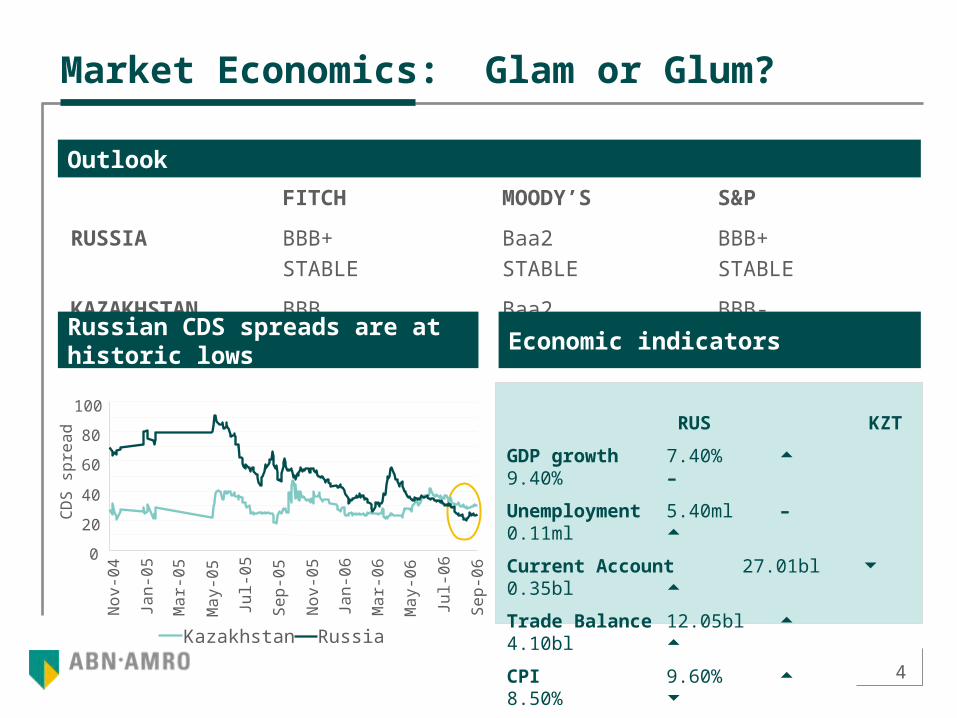

Market Economics: Glam or Glum?

Outlook

FITCH MOODY’S S&P

RUSSIA BBB+ STABLE Baa2 STABLE BBB+ STABLE

KAZAKHSTAN BBB STABLE Baa2 STABLE BBB- POSITIVE

Russian CDS spreads are at historic lows

Economic indicators

RUS KZT

GDP growth 7.40% 9.40% –

Unemployment 5.40ml – 0.11ml

Current Account 27.01bl 0.35bl

Trade Balance 12.05bl 4.10bl

CPI 9.60% 8.50%

0

20

40

60

80

100

No

v-0

4

Jan

-05

Ma

r-0

5

Ma

y-0

5

Jul-0

5

Se

p-0

5

No

v-0

5

Jan

-06

Ma

r-0

6

Ma

y-0

6

Jul-0

6

Se

p-0

6

CD

S s

pre

ad

Kazakhstan Russia

5

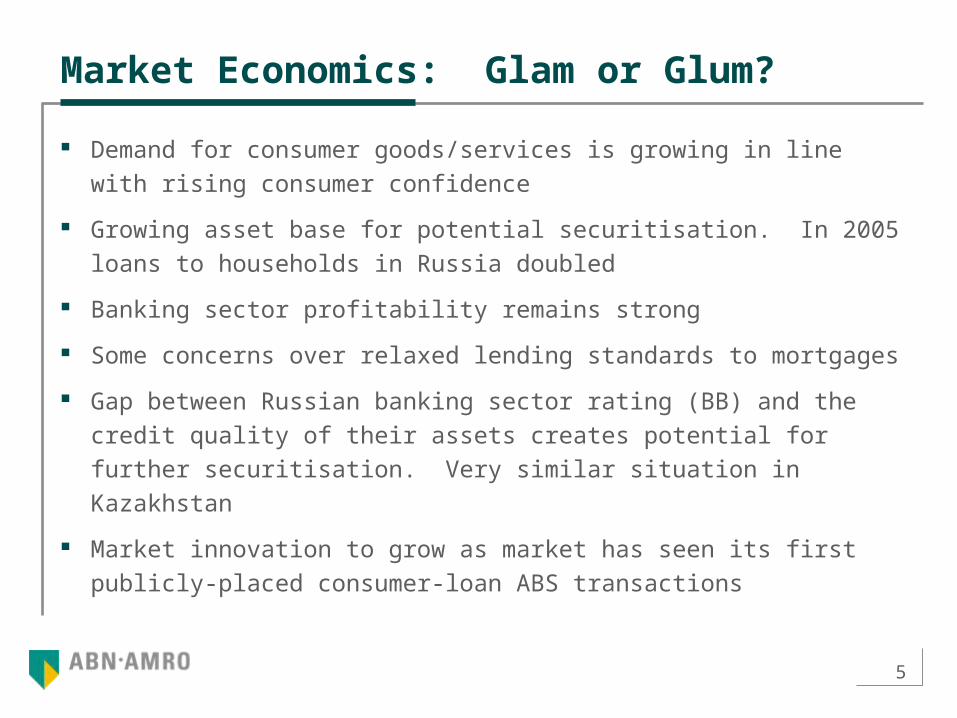

Market Economics: Glam or Glum?

Demand for consumer goods/services is growing in line with rising consumer

confidence

Growing asset base for potential securitisation. In 2005 loans to households

in Russia doubled

Banking sector profitability remains strong

Some concerns over relaxed lending standards to mortgages

Gap between Russian banking sector rating (BB) and the credit quality of

their assets creates potential for further securitisation. Very similar situation

in Kazakhstan

Market innovation to grow as market has seen its first publicly-placed

consumer-loan ABS transactions

6

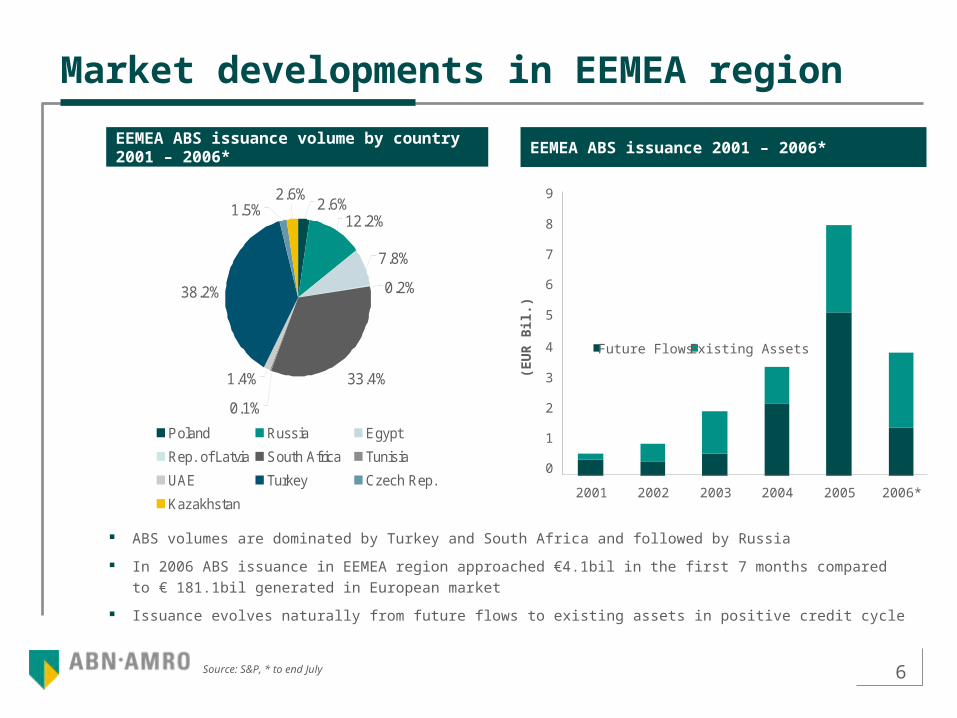

Market developments in EEMEA region

ABS volumes are dominated by Turkey and South Africa and followed by Russia

In 2006 ABS issuance in EEMEA region approached €4.1bil in the first 7 months compared to €

181.1bil generated in European market

Issuance evolves naturally from future flows to existing assets in positive credit cycle

Source: S&P, * to end July

EEMEA ABS issuance volume by country 2001 – 2006*

EEMEA ABS issuance 2001 – 2006*

Future Flows Existing Assets

0

1

2

3

4

5

6

7

8

9

2001 2002 2003 2004 2005 2006*

(EU

R B

il.)

7.8%

0.2%

33.4%

0.1%

1.4%

38.2%

12.2%2.6%

2.6%1.5%

Poland Russia Egypt

Rep. of Latvia South Africa Tunisia

UAE Turkey Czech Rep.

Kazakhstan

7

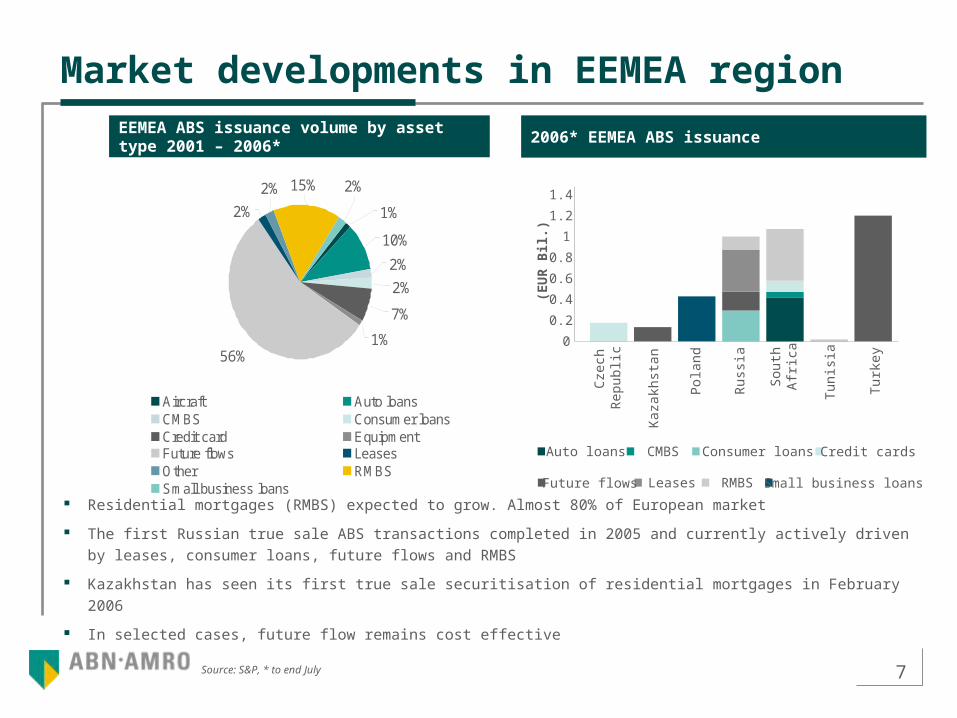

Market developments in EEMEA region

Residential mortgages (RMBS) expected to grow. Almost 80% of European market

The first Russian true sale ABS transactions completed in 2005 and currently actively driven by leases,

consumer loans, future flows and RMBS

Kazakhstan has seen its first true sale securitisation of residential mortgages in February 2006

In selected cases, future flow remains cost effective

Source: S&P, * to end July

EEMEA ABS issuance volume by asset type 2001 – 2006*

2006* EEMEA ABS issuance

Small business loansRMBSLeasesFuture flows

Credit cardsConsumer loansCMBSAuto loans

0

0.2

0.4

0.6

0.8

1

1.2

1.4

Cze

chR

epub

lic

Kaz

akhs

tan

Pol

and

Rus

sia

Sou

thA

fric

a

Tun

isia

Tur

key

(EU

R B

il.)

56%

2%

1%

7%

2%

2%

2%

10%

1%

15%2%

Aircraft Auto loansCMBS Consumer loansCredit card EquipmentFuture flows LeasesOther RMBSSmall business loans

8

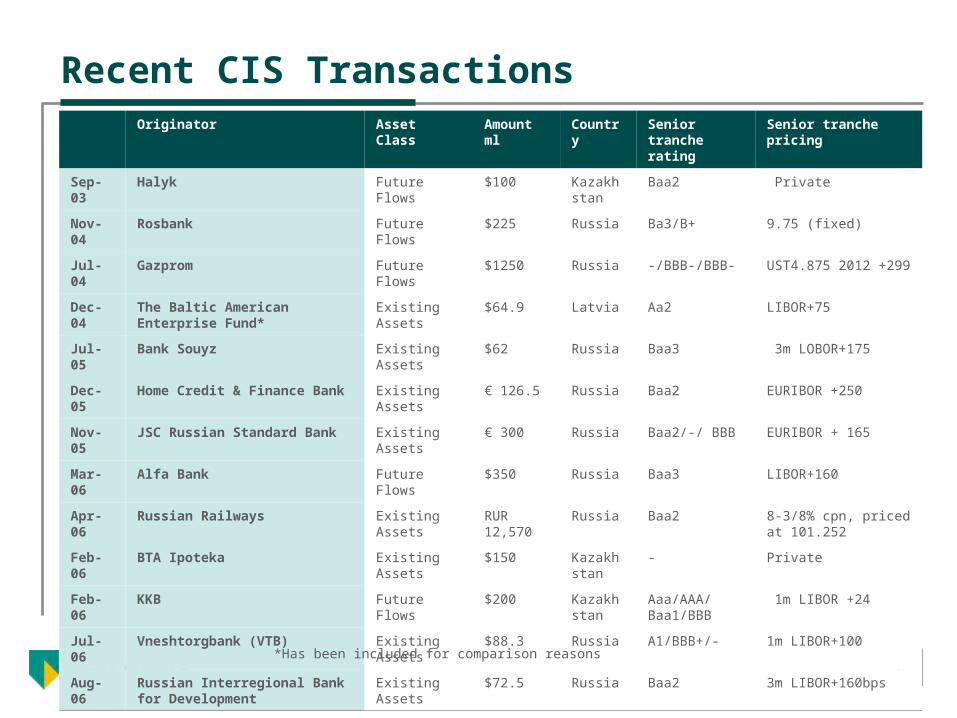

Recent CIS Transactions Originator Asset Class Amount

mlCountry Senior tranche

ratingSenior tranche pricing

Sep-03 Halyk Future Flows $100 Kazakhstan

Baa2 Private

Nov-04 Rosbank Future Flows $225 Russia Ba3/B+ 9.75 (fixed)

Jul-04 Gazprom Future Flows $1250 Russia -/BBB-/BBB- UST4.875 2012 +299

Dec-04 The Baltic American Enterprise Fund*

Existing Assets

$64.9 Latvia Aa2 LIBOR+75

Jul-05 Bank Souyz Existing Assets

$62 Russia Baa3 3m LOBOR+175

Dec-05 Home Credit & Finance Bank Existing Assets

€ 126.5 Russia Baa2 EURIBOR +250

Nov-05 JSC Russian Standard Bank Existing Assets

€ 300 Russia Baa2/-/ BBB EURIBOR + 165

Mar-06 Alfa Bank Future Flows $350 Russia Baa3 LIBOR+160

Apr-06 Russian Railways Existing Assets

RUR 12,570

Russia Baa2 8-3/8% cpn, priced at 101.252

Feb-06 BTA Ipoteka Existing Assets

$150 Kazakhstan

- Private

Feb-06 KKB Future Flows $200 Kazakhstan

Aaa/AAA/Baa1/BBB

1m LIBOR +24

Jul-06 Vneshtorgbank (VTB) Existing Assets

$88.3 Russia A1/BBB+/- 1m LIBOR+100

Aug-06 Russian Interregional Bank for Development

Existing Assets

$72.5 Russia Baa2 3m LIBOR+160bps

*Has been included for comparison reasons

9

Market Developments in CIS

Rapid expansion in consumer asset pool

Legal, tax and regulatory environment is better understood

ABS transactions are becoming an increasingly popular tool of funding in CIS

and Kazakhstan

Diversified funding source and improve cost of lending

Rating agencies are becoming more familiar with the legal framework,

macroeconomic situation, and the underlying assets to be securitised

2 Future development of securitisation in Russia and Kazakhstan

11

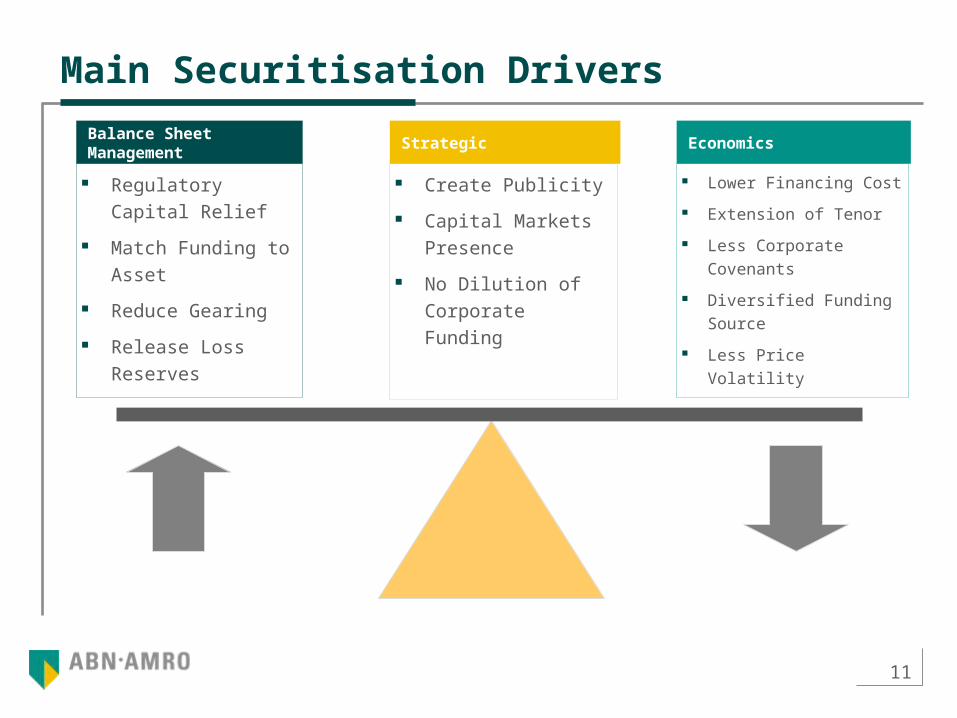

Lower Financing Cost

Extension of Tenor

Less Corporate

Covenants

Diversified Funding

Source

Less Price Volatility

Economics

Create Publicity

Capital Markets

Presence

No Dilution of

Corporate Funding

Strategic

Regulatory Capital

Relief

Match Funding to

Asset

Reduce Gearing

Release Loss

Reserves

Balance Sheet Management

Main Securitisation Drivers

12

Challenges for Market Expansion

Establishment of clear underwriting standards and collection procedures

Build up of loan portfolios with consistency … and credit quality

Proven track record for specific loan types

Set-up IT systems to accommodate securitisation requirements

Major Challenges for Originators

Major Market Challenges Development or refinement of the legal framework to facilitate true sale securitisations:

– Achieving an insolvency remote transfer of assets/loans– Proper protection of creditors and investors;– Efficient transfer of underlying securities (e.g. residential mortgage loans)

Clarification or ascertaining of tax positions

– Withholding taxes;– VAT– Stamp duties

Regulatory treatment for the portfolio sale

Development of a local SPV infrastructure and issuance of ABS notes in local currencies

13

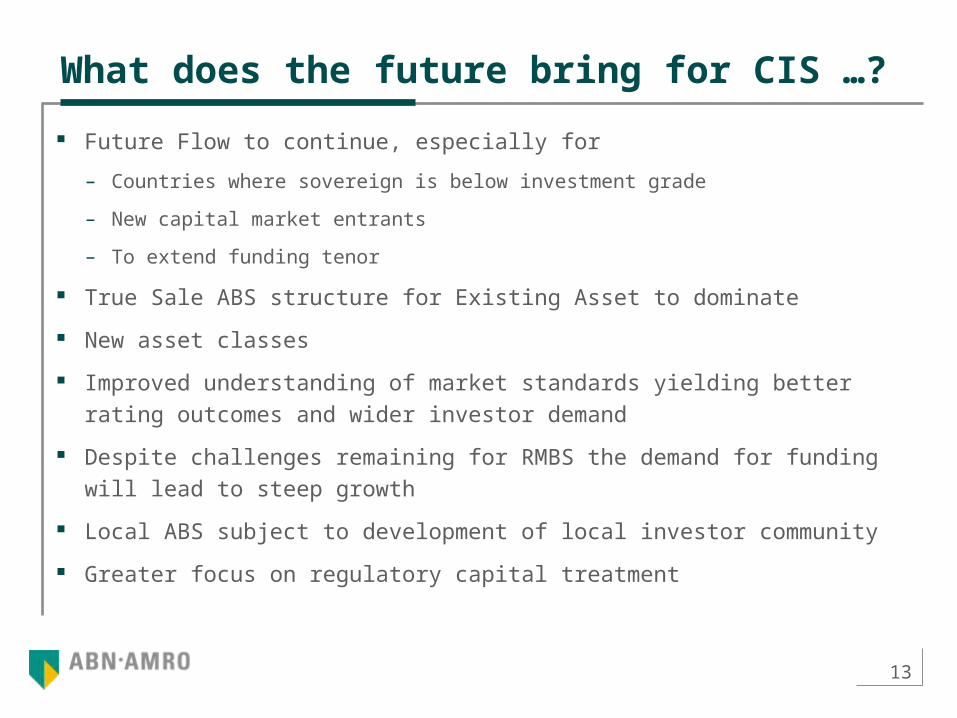

What does the future bring for CIS …?

Future Flow to continue, especially for

– Countries where sovereign is below investment grade

– New capital market entrants

– To extend funding tenor

True Sale ABS structure for Existing Asset to dominate

New asset classes

Improved understanding of market standards yielding better rating outcomes and

wider investor demand

Despite challenges remaining for RMBS the demand for funding will lead to

steep growth

Local ABS subject to development of local investor community

Greater focus on regulatory capital treatment

14

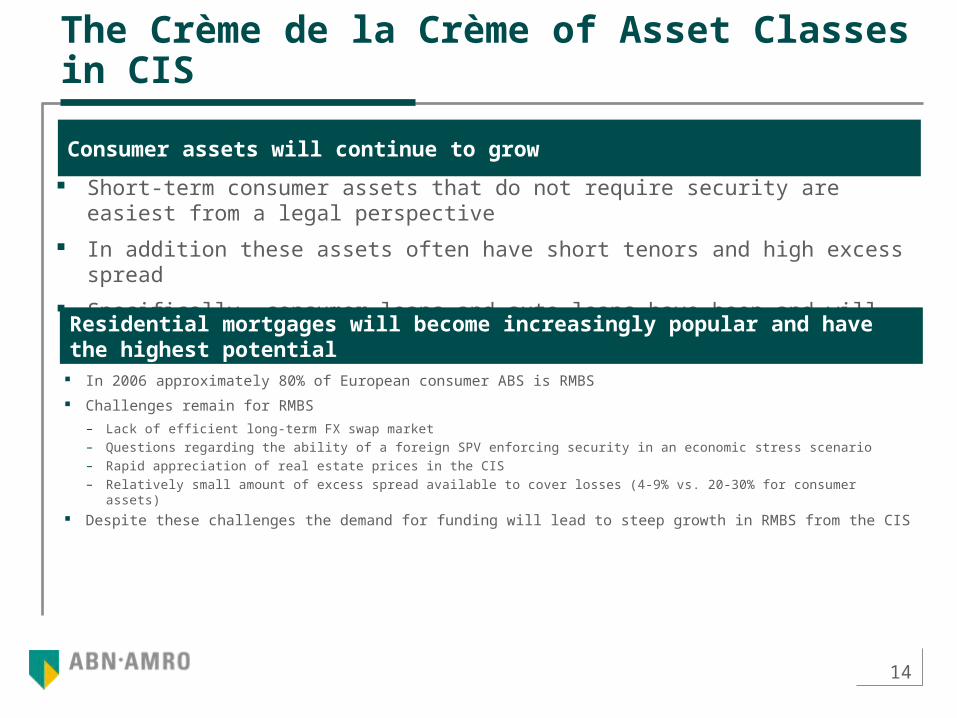

The Crème de la Crème of Asset Classes in CIS

Short-term consumer assets that do not require security are easiest from a legal perspective

In addition these assets often have short tenors and high excess spread

Specifically, consumer loans and auto loans have been and will continue to be positive

Consumer assets will continue to grow

Residential mortgages will become increasingly popular and have the highest potential

In 2006 approximately 80% of European consumer ABS is RMBS

Challenges remain for RMBS

– Lack of efficient long-term FX swap market

– Questions regarding the ability of a foreign SPV enforcing security in an economic stress scenario

– Rapid appreciation of real estate prices in the CIS

– Relatively small amount of excess spread available to cover losses (4-9% vs. 20-30% for consumer assets) Despite these challenges the demand for funding will lead to steep growth in RMBS from the CIS

15

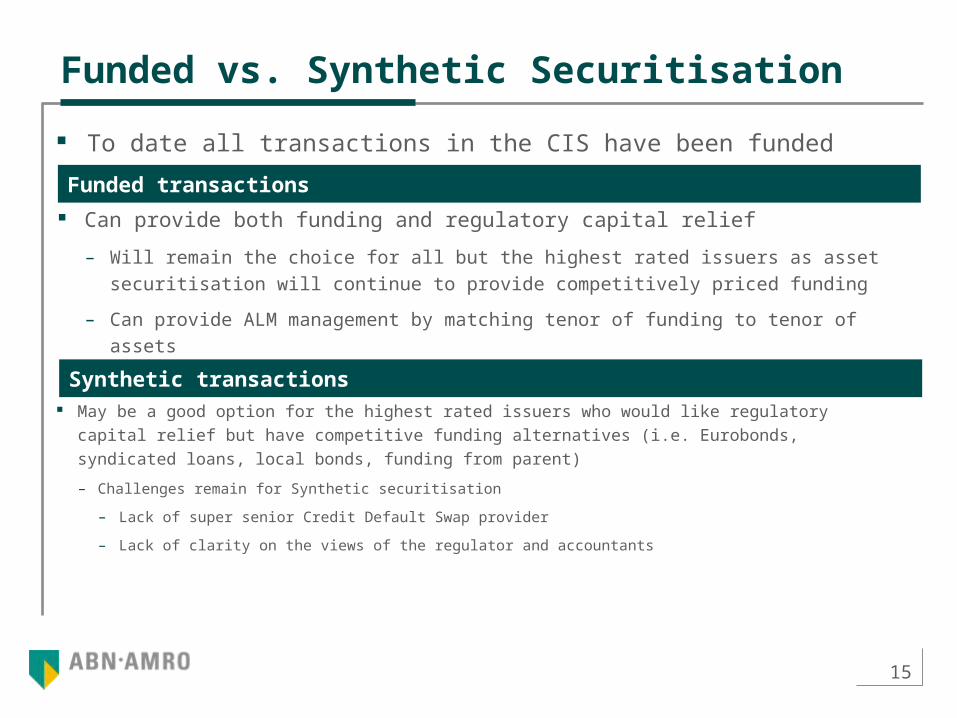

Funded vs. Synthetic Securitisation

To date all transactions in the CIS have been funded transactions

Funded transactions

Synthetic transactions

Can provide both funding and regulatory capital relief

– Will remain the choice for all but the highest rated issuers as asset securitisation will

continue to provide competitively priced funding

– Can provide ALM management by matching tenor of funding to tenor of assets

May be a good option for the highest rated issuers who would like regulatory capital relief but have

competitive funding alternatives (i.e. Eurobonds, syndicated loans, local bonds, funding from parent)

– Challenges remain for Synthetic securitisation

– Lack of super senior Credit Default Swap provider

– Lack of clarity on the views of the regulator and accountants

16

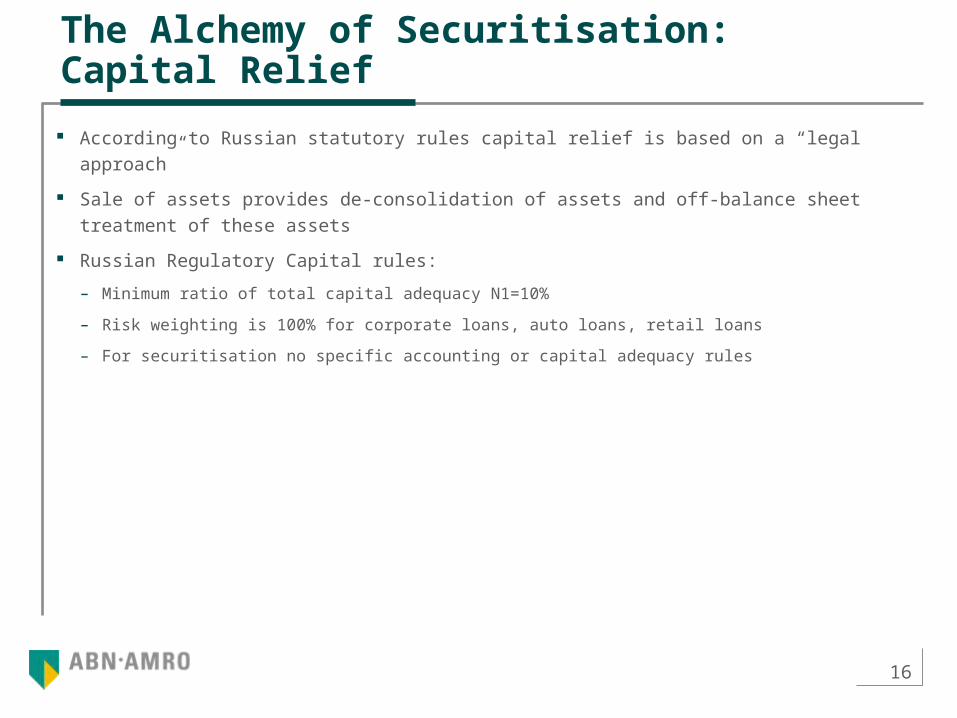

The Alchemy of Securitisation: Capital Relief

According to Russian statutory rules capital relief is based on a “legal approach”

Sale of assets provides de-consolidation of assets and off-balance sheet treatment of

these assets

Russian Regulatory Capital rules:

– Minimum ratio of total capital adequacy N1=10%

– Risk weighting is 100% for corporate loans, auto loans, retail loans

– For securitisation no specific accounting or capital adequacy rules

17

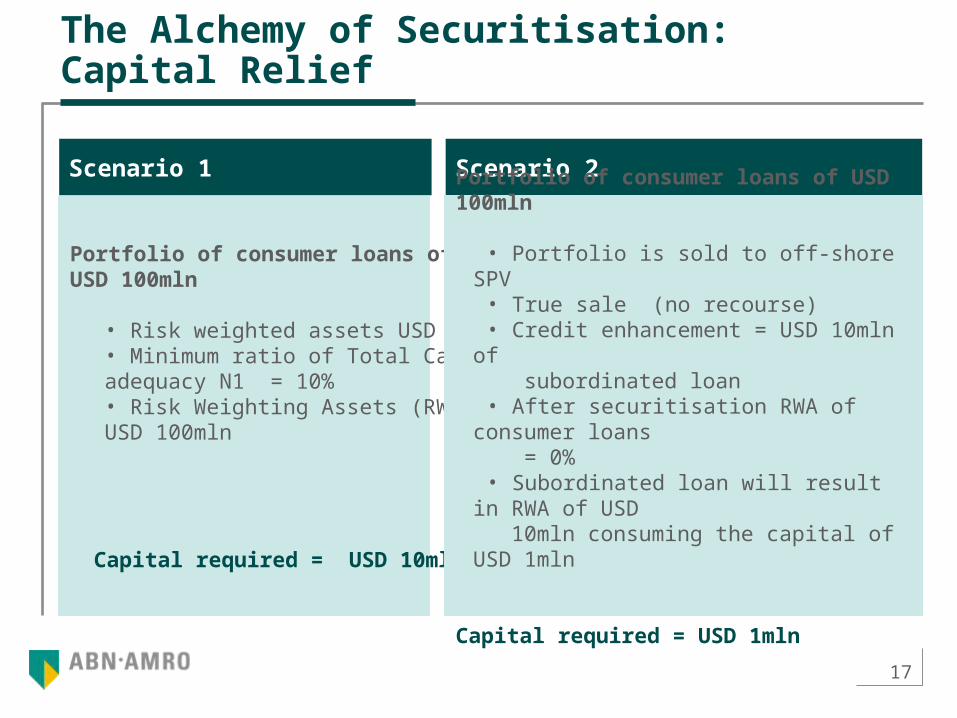

The Alchemy of Securitisation: Capital Relief

Scenario 1 Scenario 2

Portfolio of consumer loans of USD 100mln

• Risk weighted assets USD 100mln• Minimum ratio of Total Capital adequacy N1 = 10% • Risk Weighting Assets (RWA) = USD 100mln

Capital required = USD 10mln

Portfolio of consumer loans of USD 100mln

• Portfolio is sold to off-shore SPV • True sale (no recourse) • Credit enhancement = USD 10mln of

subordinated loan• After securitisation RWA of consumer loans

= 0%• Subordinated loan will result in RWA of

USD 10mln consuming the capital of USD 1mln

Capital required = USD 1mln

18

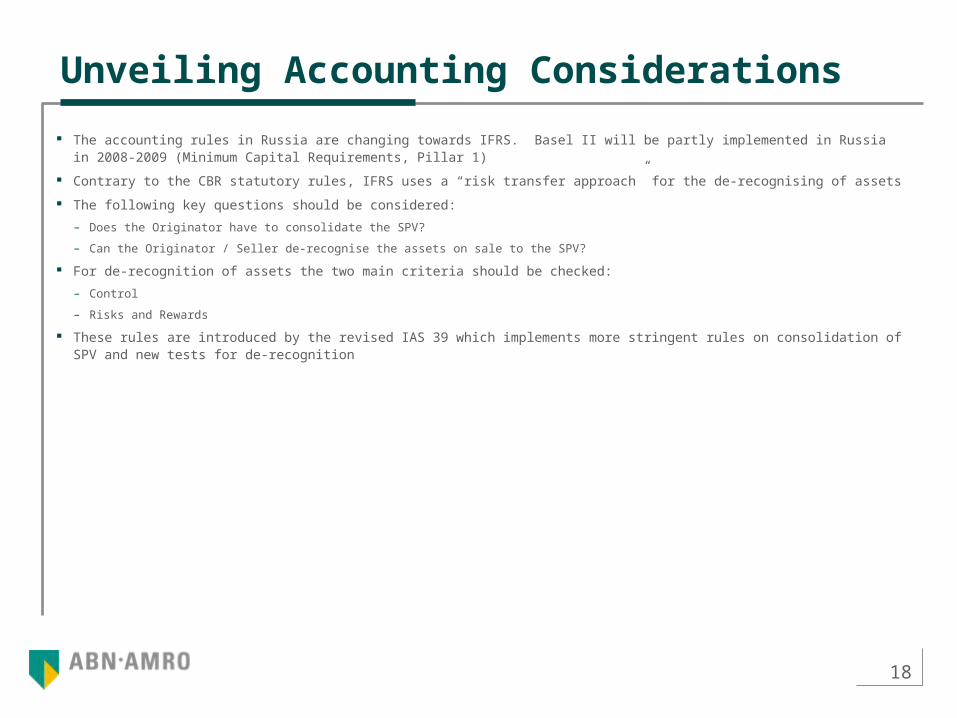

Unveiling Accounting Considerations

The accounting rules in Russia are changing towards IFRS. Basel II will be partly implemented in Russia in 2008-2009 (Minimum Capital Requirements, Pillar 1)

Contrary to the CBR statutory rules, IFRS uses a “risk transfer approach” for the de-recognising of assets

The following key questions should be considered:

– Does the Originator have to consolidate the SPV?

– Can the Originator / Seller de-recognise the assets on sale to the SPV?

For de-recognition of assets the two main criteria should be checked:

– Control

– Risks and Rewards

These rules are introduced by the revised IAS 39 which implements more stringent rules on consolidation of SPV and new tests for de-recognition

3 Case Study

First Kazakhstan RMBS Transaction

20

First one in Kazakhstan …

21

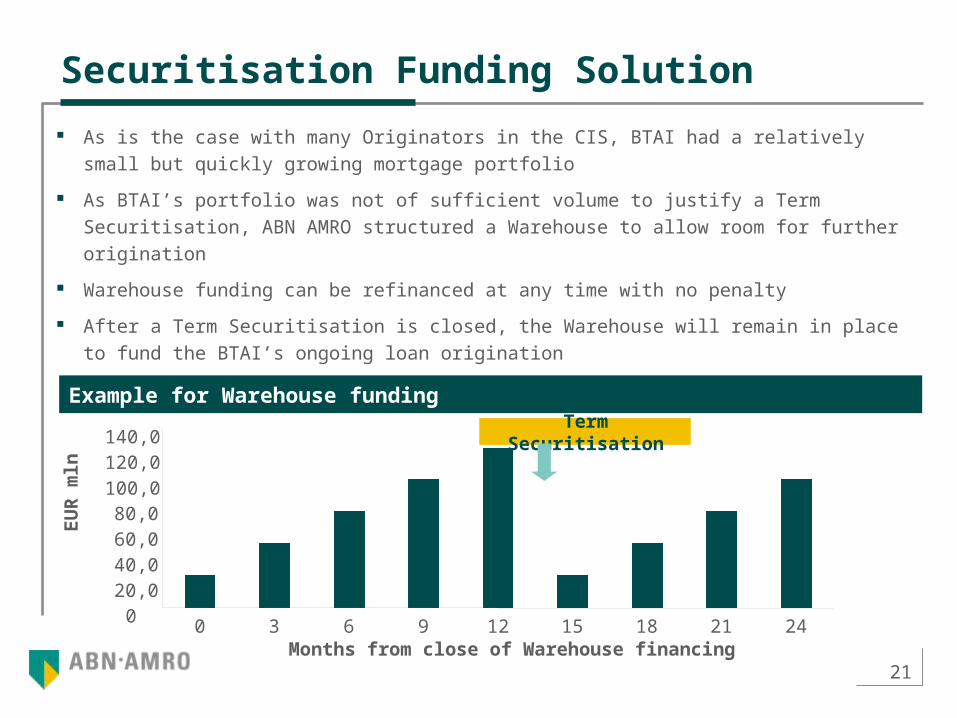

Securitisation Funding Solution

As is the case with many Originators in the CIS, BTAI had a relatively small but quickly

growing mortgage portfolio

As BTAI’s portfolio was not of sufficient volume to justify a Term Securitisation, ABN

AMRO structured a Warehouse to allow room for further origination

Warehouse funding can be refinanced at any time with no penalty

After a Term Securitisation is closed, the Warehouse will remain in place to fund the

BTAI’s ongoing loan origination

Example for Warehouse funding

Term Securitisation

020,040,060,080,0

100,0120,0140,0

0 3 6 9 12 15 18 21 24Months from close of Warehouse financing

EU

R m

ln

22

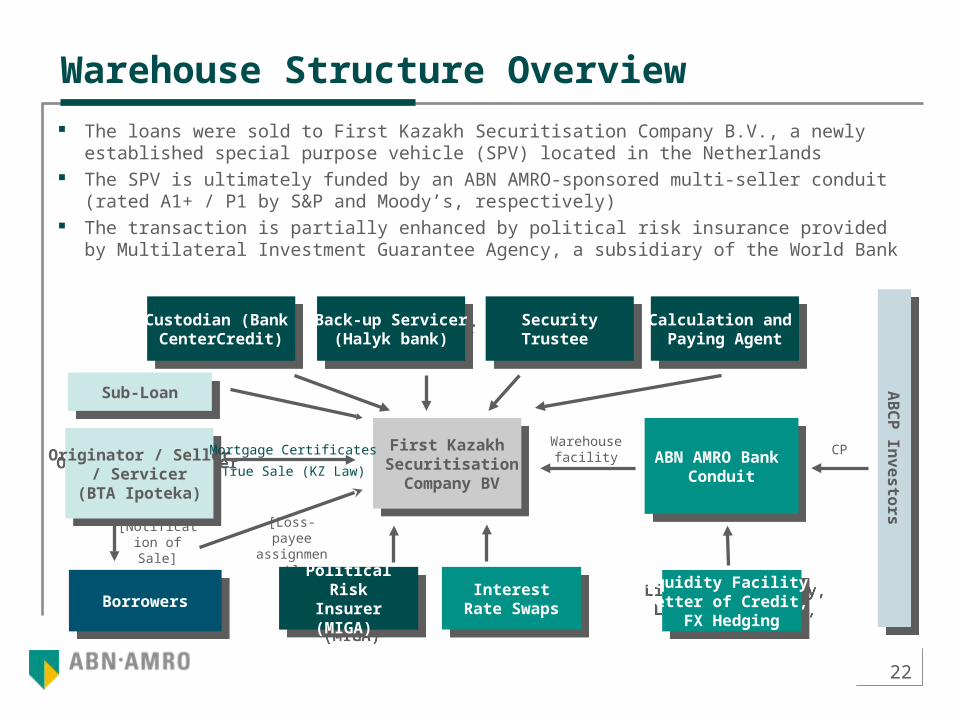

Warehouse Structure Overview The loans were sold to First Kazakh Securitisation Company B.V., a newly established

special purpose vehicle (SPV) located in the Netherlands The SPV is ultimately funded by an ABN AMRO-sponsored multi-seller conduit (rated

A1+ / P1 by S&P and Moody’s, respectively) The transaction is partially enhanced by political risk insurance provided by Multilateral

Investment Guarantee Agency, a subsidiary of the World Bank

First Kazakh Securitisation Company BV

First Kazakh Securitisation Company BV

ABN AMRO Bank Conduit

ABN AMRO Bank ConduitTrue Sale (KZ Law)Originator / Seller

/ Servicer(BTA Ipoteka)

Originator / Seller/ Servicer

(BTA Ipoteka)

Warehouse facility

BorrowersBorrowers Interest Rate Swaps

Interest Rate Swaps

Sub-LoanSub-Loan

Mortgage Certificates

[Notification of Sale]

SecurityTrustee

SecurityTrustee

Back-up Servicer(Halyk bank)

Back-up Servicer(Halyk bank)

[Loss-payee assignment]

AB

CP

Inv

es

tors

AB

CP

Inv

es

tors

Political RiskInsurer(MIGA)

Political RiskInsurer(MIGA)

CP

Calculation and Paying Agent

Calculation and Paying Agent

Liquidity Facility, Letter of Credit,

FX Hedging

Liquidity Facility, Letter of Credit,

FX Hedging

Custodian (Bank CenterCredit)

Custodian (Bank CenterCredit)

23

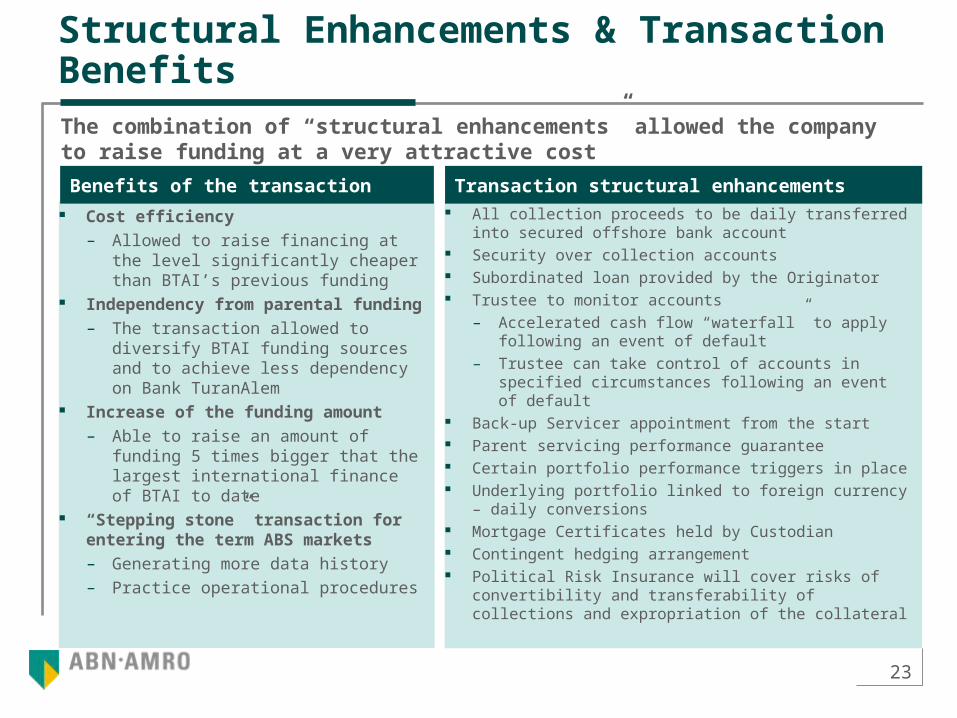

All collection proceeds to be daily transferred into secured offshore bank account

Security over collection accounts Subordinated loan provided by the Originator Trustee to monitor accounts

– Accelerated cash flow “waterfall” to apply following an event of default

– Trustee can take control of accounts in specified circumstances following an event of default

Back-up Servicer appointment from the start Parent servicing performance guarantee Certain portfolio performance triggers in place Underlying portfolio linked to foreign currency – daily

conversions Mortgage Certificates held by Custodian Contingent hedging arrangement Political Risk Insurance will cover risks of convertibility

and transferability of collections and expropriation of the collateral

Cost efficiency

– Allowed to raise financing at the level significantly cheaper than BTAI’s previous funding

Independency from parental funding

– The transaction allowed to diversify BTAI funding sources and to achieve less dependency on Bank TuranAlem

Increase of the funding amount

– Able to raise an amount of funding 5 times bigger that the largest international finance of BTAI to date

“Stepping stone” transaction for entering the term ABS markets

– Generating more data history

– Practice operational procedures

Structural Enhancements & Transaction BenefitsThe combination of “structural enhancements” allowed the company to raise funding at a very attractive cost

Benefits of the transaction Transaction structural enhancements

24

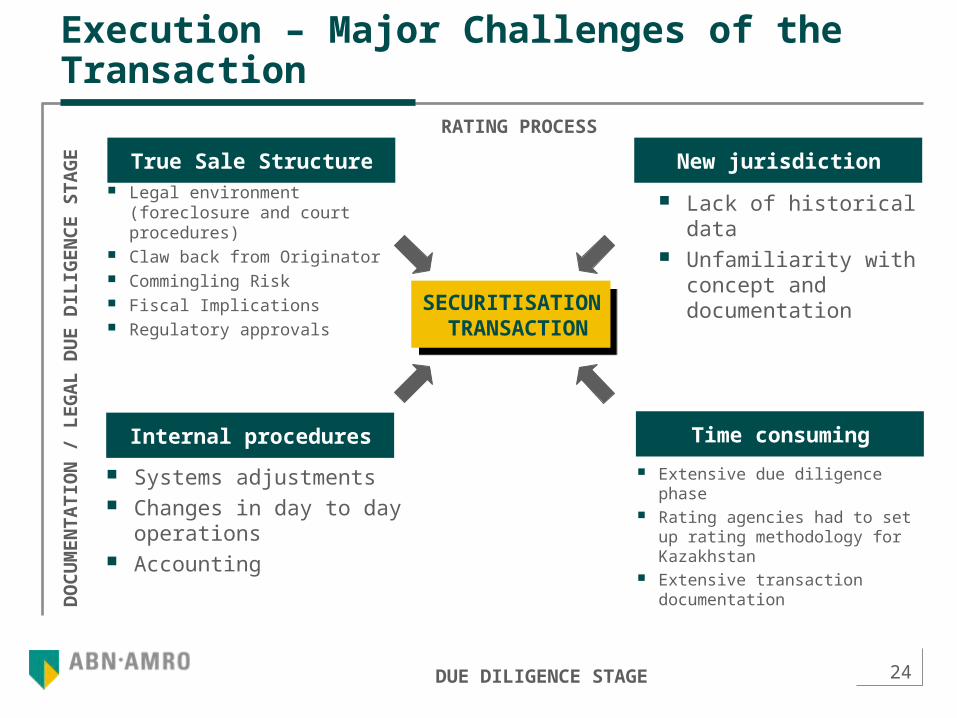

Execution – Major Challenges of the Transaction

SECURITISATION TRANSACTION

SECURITISATION TRANSACTION

Legal environment (foreclosure and court procedures)

Claw back from Originator Commingling Risk Fiscal Implications Regulatory approvals

True Sale Structure

Lack of historical data Unfamiliarity with

concept and documentation

New jurisdiction

Extensive due diligence phase Rating agencies had to set up

rating methodology for Kazakhstan

Extensive transaction documentation

Time consuming

Systems adjustments Changes in day to day

operations Accounting

Internal procedures

RATING PROCESS

DUE DILIGENCE STAGE

DO

CU

ME

NT

AT

ION

/ L

EG

AL

DU

E D

ILIG

EN

CE

ST

AG

E

25

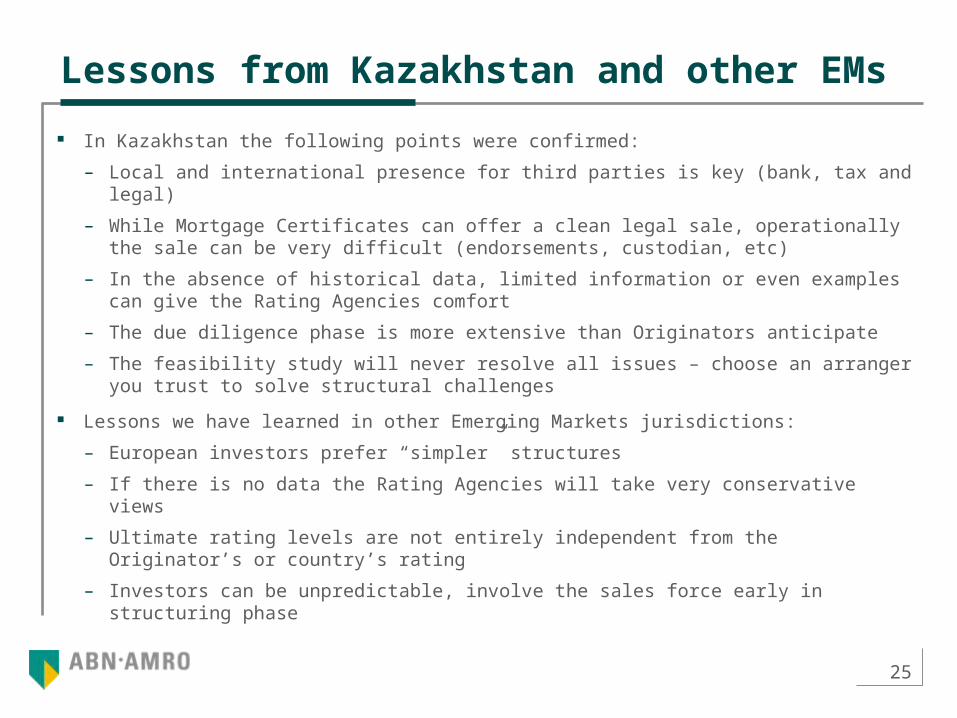

Lessons from Kazakhstan and other EMs

In Kazakhstan the following points were confirmed:

– Local and international presence for third parties is key (bank, tax and legal)

– While Mortgage Certificates can offer a clean legal sale, operationally the sale can be very difficult (endorsements, custodian, etc)

– In the absence of historical data, limited information or even examples can give the Rating Agencies comfort

– The due diligence phase is more extensive than Originators anticipate

– The feasibility study will never resolve all issues – choose an arranger you trust to solve structural challenges

Lessons we have learned in other Emerging Markets jurisdictions:

– European investors prefer “simpler” structures

– If there is no data the Rating Agencies will take very conservative views

– Ultimate rating levels are not entirely independent from the Originator’s or country’s rating

– Investors can be unpredictable, involve the sales force early in structuring phase

26

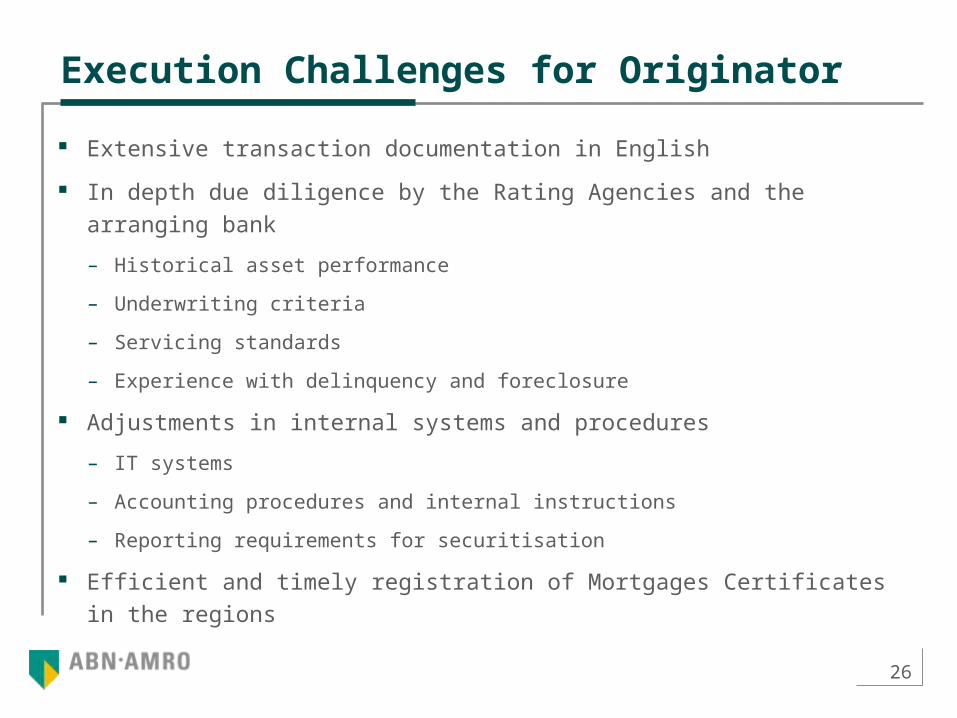

Execution Challenges for Originator

Extensive transaction documentation in English

In depth due diligence by the Rating Agencies and the arranging bank

– Historical asset performance

– Underwriting criteria

– Servicing standards

– Experience with delinquency and foreclosure

Adjustments in internal systems and procedures

– IT systems

– Accounting procedures and internal instructions

– Reporting requirements for securitisation

Efficient and timely registration of Mortgages Certificates in the regions

27

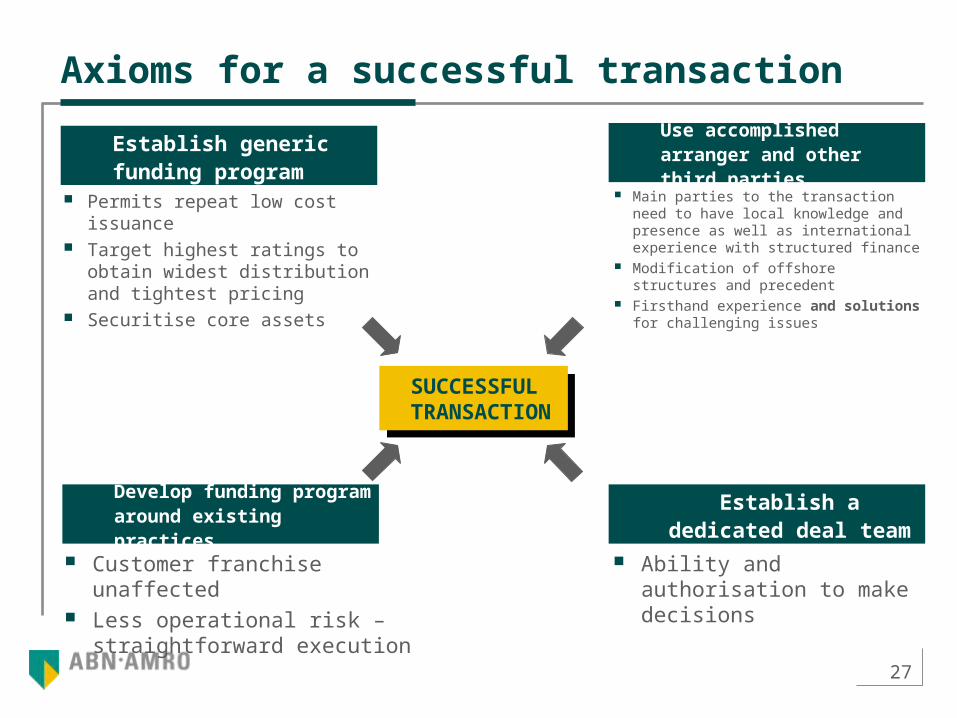

Main parties to the transaction need to have local knowledge and presence as well as international experience with structured finance

Modification of offshore structures and precedent

Firsthand experience and solutions for challenging issues

Axioms for a successful transaction

SUCCESSFUL TRANSACTION

SUCCESSFUL TRANSACTION

Permits repeat low cost issuance

Target highest ratings to obtain widest distribution and tightest pricing

Securitise core assets

Ability and authorisation to make decisions

Customer franchise unaffected Less operational risk –

straightforward execution

Develop funding program around existing practices

Establish generic funding program

Use accomplished arranger and other third parties

Establish a dedicated deal team

28

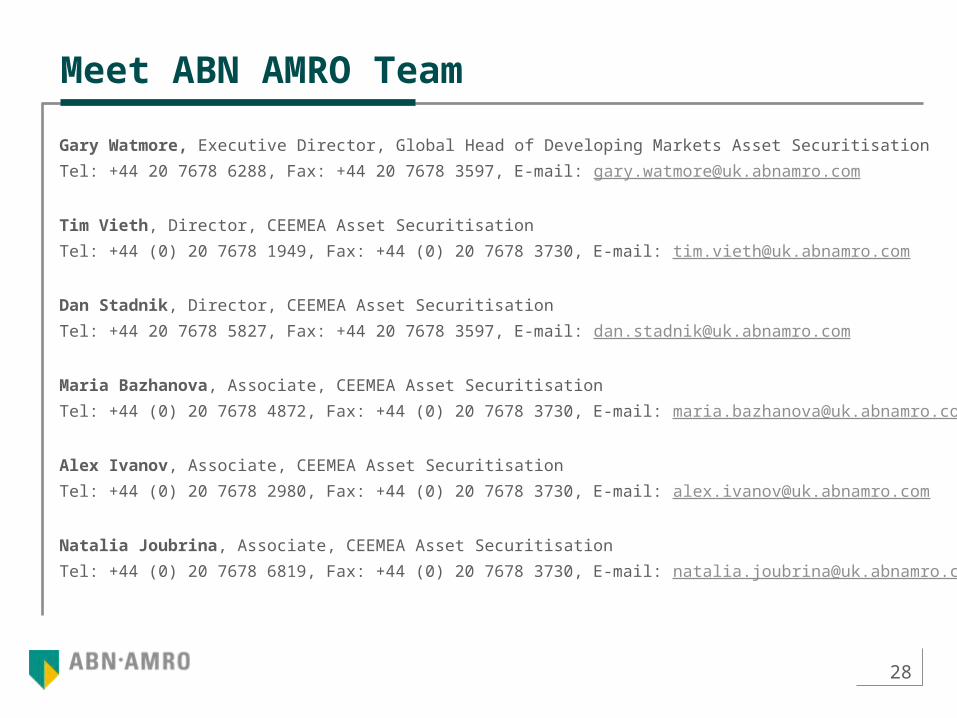

Meet ABN AMRO Team

Gary Watmore, Executive Director, Global Head of Developing Markets Asset Securitisation

Tel: +44 20 7678 6288, Fax: +44 20 7678 3597, E-mail: [email protected]

Tim Vieth, Director, CEEMEA Asset Securitisation

Tel: +44 (0) 20 7678 1949, Fax: +44 (0) 20 7678 3730, E-mail: [email protected]

Dan Stadnik, Director, CEEMEA Asset Securitisation

Tel: +44 20 7678 5827, Fax: +44 20 7678 3597, E-mail: [email protected]

Maria Bazhanova, Associate, CEEMEA Asset Securitisation

Tel: +44 (0) 20 7678 4872, Fax: +44 (0) 20 7678 3730, E-mail: [email protected]

Alex Ivanov, Associate, CEEMEA Asset Securitisation

Tel: +44 (0) 20 7678 2980, Fax: +44 (0) 20 7678 3730, E-mail: [email protected]

Natalia Joubrina, Associate, CEEMEA Asset Securitisation

Tel: +44 (0) 20 7678 6819, Fax: +44 (0) 20 7678 3730, E-mail: [email protected]

4 Panel discussion

30

Making more possible