october 2016 digital technology through the supply chain · digital technology through the supply...

TRANSCRIPT

Digital Technology Through The Supply Chain

Michael Whitehead

October 2016

2

• ANZ And Agri

• Real Time Financing

• Cattle As An Example

• Trust – New Market Entrants

• The Alibaba Effect

AGENDA

2

ANZ AND AGRICULTURE

3

OUR SUPER REGIONAL NETWORK

Note: *GCC - Gulf Cooperation of Council countries **Pacific Islands comprises of Guam, Solomon Islands, Fiji, Kiribati, Samoa, American Samoa, Cook Islands, Timor Leste, Tonga, Vanuatu and New Caledonia. Fiji operations comprises of Commercial/International Banking, Large Corporate & Institutional Banking, and Retail Banking & Wealth Management

KEY: Commercial/ International Banking

Large Corporate & Institutional Banking Private Banking

Retail Banking & Wealth Management

Partner Bank Representative Office

ANZ has an established regional network across 33 markets which include 15 Asian markets and representation in Europe, America and Middle East. ANZ is a leading bank in Australia and the largest bank in New Zealand & the Pacific Islands (12 markets)

GERMANY Frankfurt

LAOS

VIETNAM

THAILAND

MYANMAR

UNITED KINGDOM

London

CHINA

UAE (GCC*)

INDIA

CAMBODIA

SINGAPORE

MALAYSIA

SOUTH KOREA

JAPAN

HONG KONG

TAIWAN

UNITED STATES OF AMERICA New York

PHILIPPINES

INDONESIA

PAPUA NEW GUINEA

AUSTRALIA

PACIFIC ISLANDS**

NEW ZEALAND

4

4

ANZ AGRIBUSINESS

Regional Business Banking Agribusiness Specialists

Corporate Agribusiness

Institutional Banking

Family Farms Agri Value Chain Sub-industry

expertise Lending up to

$10M

Large primary producers, 1st stage processors and services to agri. Industry specialisation Turnover < $500m

Multi-nationals and Listed Australian companies Turnover > $500m

We understand the flow of your

produce through the entire supply chain, from paddock to

plate. Our regional network offers you

access to local industry expertise, valuable connections

and growth opportunities to help take your agribusiness into

the future.

5

6

AND TECHNOLOGY IS CHANGING THE COURSE – EXPONENTIALLY!

REAL TIME FINANCING

7

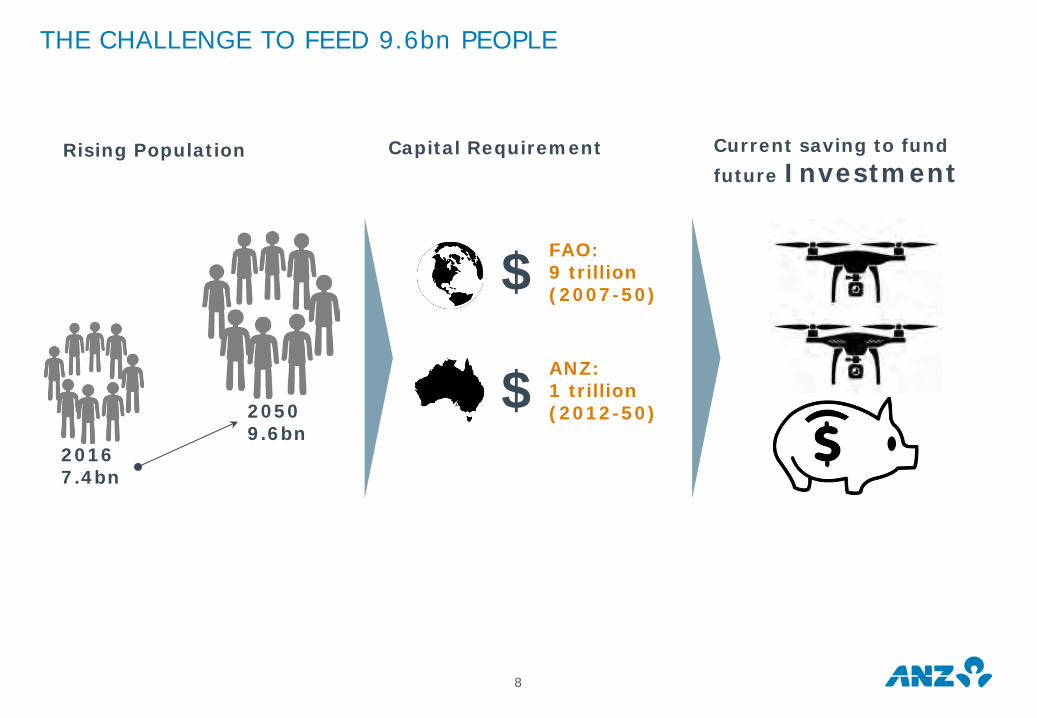

THE CHALLENGE TO FEED 9.6bn PEOPLE

8

2016 7.4bn

2050 9.6bn

FAO: 9 trillion (2007-50) $ ANZ: 1 trillion (2012-50) $

Rising Population Capital Requirement Current saving to fund future Investment

BANKS REMAIN INTEGRAL PART OF SUPPLY CHAIN

9

10

AUSTRALIAN BEEF INDUSTRY

47%

22%

19%

5%4%

3%

QLDNSWVICSAWATAS

29.1 Million

7%

8%

4%

44%

20%

14%

3%

Bee

f

2.7mt cwt

1 m

28 mGrass Fed

Feedlot

Feed

ing

Sys

tem

2.0

1.1Kg/Day

Kg/Day

Grass Fed

Feedlot W

eig

ht

Gai

n

CATTLE AS AN EXAMPLE…

11

12

TRADITIONAL VS REAL TIME FINANCING

Real Time Financing

300 Kg 400 Kg 500 Kg

Day 0 Day 50 Day 100

$ $$$ $$$$$

$ Gained $ Gained

300 Kg 400 Kg 500 Kg

Day 0 Day 50 Day 100

$ $$$ $$$$$

$ Lost $ Lost

Traditional Financing

Funding Against Land

Failure to tap the working capital finance opportunity

Works well with operators with long operation history

Technology provide opportunity to unlock working capital

300

450

600

750

900

1,050

1,200

1.5

2.0

2.5

3.0

3.5

4.0

Jan 15 Feb 15 Mar 15 Apr 15 May 15

AUD

Mill

ion

AUD

Per

Kg

Cattle Price Market Value (RHS) Real Time Model (RHS)

13

An Inventory that Grows: Feedlot

Tap the Market Value: Feedlot1

300

350

400

450

500

550

1.5

2.0

2.5

3.0

3.5

4.0

4.5

Jan 15 Feb 15 Mar 15 Apr 15 May 15

Kg

AUD

Per

Kg

Australia Eastern Young Cattle Indicator Ave Weight (RHS)

Note1: Dressing %=52%, 85% of market value for feed lot with 100 day cycle

DIGITAL FINANCING LEVERAGES ALL AVAILABLE INFORMATION

ABILITY TO ATTRACT NEW CAPITAL IN THE INDUSTRY BY UNLOCKING WORKING CAPITAL

14

20151 20161

0

200

400

600

800

1,000

1,200

Jan 15 Feb 15 Mar 15 Apr 15 May 15

AUD

Mill

ion

Traditional Model Real Time Model

0

200

400

600

800

1,000

1,200

Jan 16 Feb 16 Mar 16 Apr 16 May 16

AUD

Mill

ion

Traditional Model Real Time Model

Works well with operators with long operation history

Note1: Dressing %=52%, 85% of market value for feed lot with 100 day cycle

15 TRADITIONAL VS DIGITAL FINANCING

Additional Capital 0-50 Days (In AUD m) Additional Capital 50-100 Days (In AUD m)

-50

0

50

100

150

200

250

300

0 Day 10 Day 20 Day 30 Day 40 Day

2010 2011 2012 20132014 2015 2016

-50

0

50

100

150

200

250

300

50 Day 60 Day 70 Day 80 Day 90 Day

2010 2011 2012 2013

2014 2015 2016

15

THE WAY AHEAD

16

WHY BLOCKCHAIN?

17

Prohibits digital copies of assets

Individual ownership of data

Ability to uniquely identify each asset

Lower cost of operation

Faster processing

Failure resilience

THE WAY AHEAD

18

Drivers Platform

Cattle in feedlot 2,000

Funding Based on Land AUD 1.0m

Working Capital Opportunity AUD 0.4m

Swipe Right to unlock AUD 400k

2.12.42.73.03.33.63.94.24.54.8

10 11 12 13 14 15 16Australia Eastern Young Cattle Indicator

AU

D /

Kg

ENHANCED TRUST = NEW MARKET ENTRANTS

19

20

LEVERAGE THE INFORMATION TO UNLOCK CAPITAL

Technology to support Real Time financing

THE “ALIBABA” EFFECT

21

CHINA’s “OUTSIZED” AGRI DEMAND – MEAT M

eat

Con

sum

pti

on

CA

GR

(2

01

5-2

0)

GDP (PPP) CAGR (2015-20)

Notes: 1. Meat includes Beef & Veal, Sheep meat, Poultry and Pork

Meat Consumption (million tonnes) vs GDP (PPP)

Bubble Size represent 2020 Meat Consumption

Source: BMI, IMF, ANZ

92.5mt

41.0mt

Brazil, 21.7mt

Russia, 11.0mt

Viet Nam, 6.9mt

Japan, 5.7mt

Korea, 3.5mt

Canada, 3.3mt

2020 Meat Consumption

China

USA

Philippines, 4.0mt

Saudi Arabia, 2.0mt

Thailand, 2.0mt

China

United States

Brazil

Russia

Japan

Korea

Viet Nam

Philippines

Canada

Saudi Arabia

Thailand

-

0.5%

1.0%

1.5%

2.0%

2.5%

1% 3% 5% 7% 9% 11%

22

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

1960 1964 1968 1972 1976 1980 1984 1988 1992 1996 2000 2004 2008 2012 2016

China United States

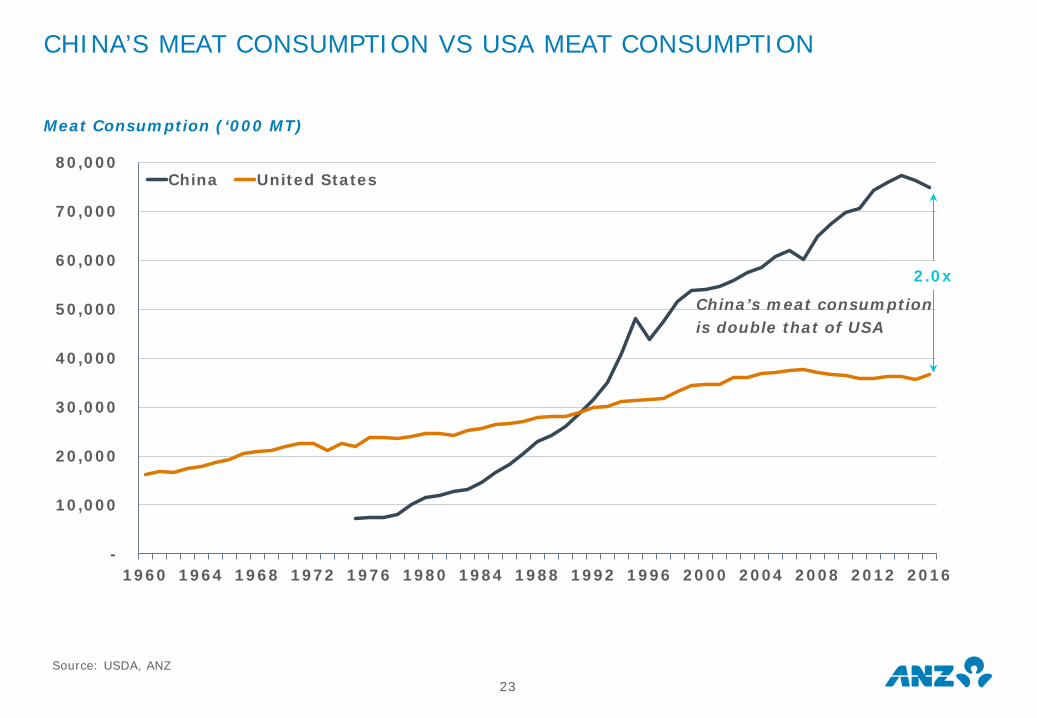

CHINA’S MEAT CONSUMPTION VS USA MEAT CONSUMPTION

China’s meat consumption is double that of USA

Meat Consumption (‘000 MT)

Source: USDA, ANZ

2.0x

23

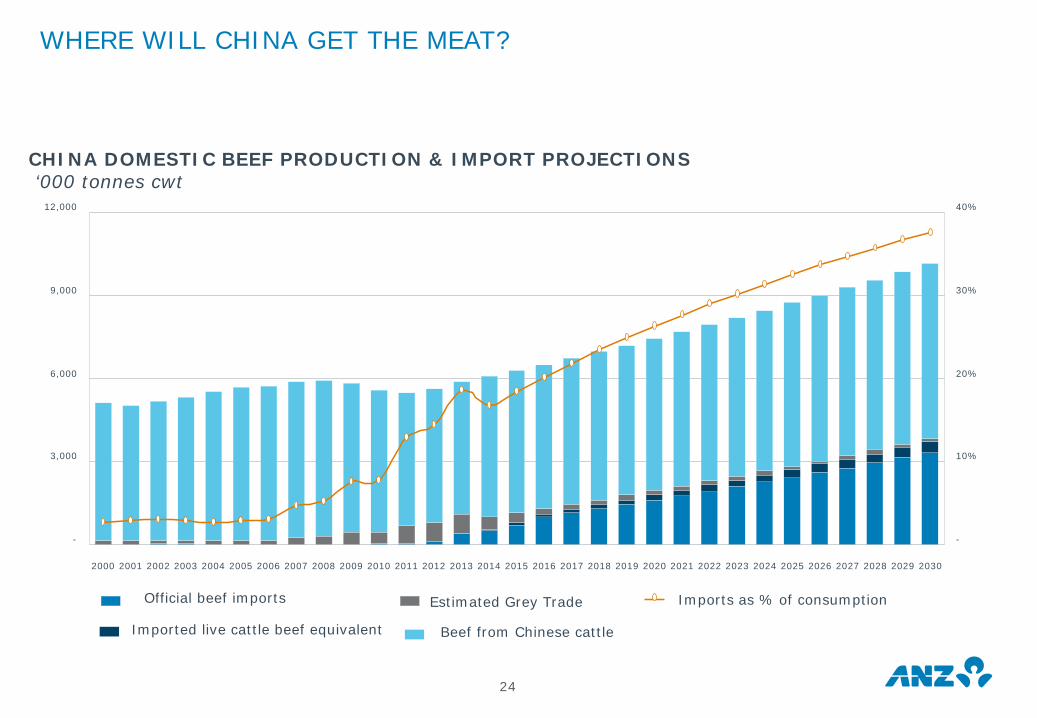

WHERE WILL CHINA GET THE MEAT?

CHINA DOMESTIC BEEF PRODUCTION & IMPORT PROJECTIONS ‘000 tonnes cwt

-

3,000

6,000

9,000

12,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

-

10%

20%

30%

40%

Official beef imports

Imported live cattle beef equivalent

Estimated Grey Trade

Beef from Chinese cattle

Imports as % of consumption

24

CHINA DEMOGRAPHICS – INCREASING AGEING

Population by Age Group

CHINA JAPAN GERMANY Male Female

Source: US Bureau, International Database

10% - 10%

0-45-9

10-1415-1920-2425-2930-3435-3940-4445-4950-5455-5960-6465-6970-7475-7980-8485-8990-9495-99100+

10% - 10% 10% - 10%

25

CHINA CONSUMES AS MANY CALORIES PER CAPITA AS JAPAN DID IN 1990

China Calorie consumption by Source

Source: FAO Statistics, ANZ

-

500

1,000

1,500

2,000

2,500

3,000

3,500

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

Dairy and Eggs Grain Meat Produce Sugar and Fat Other

26

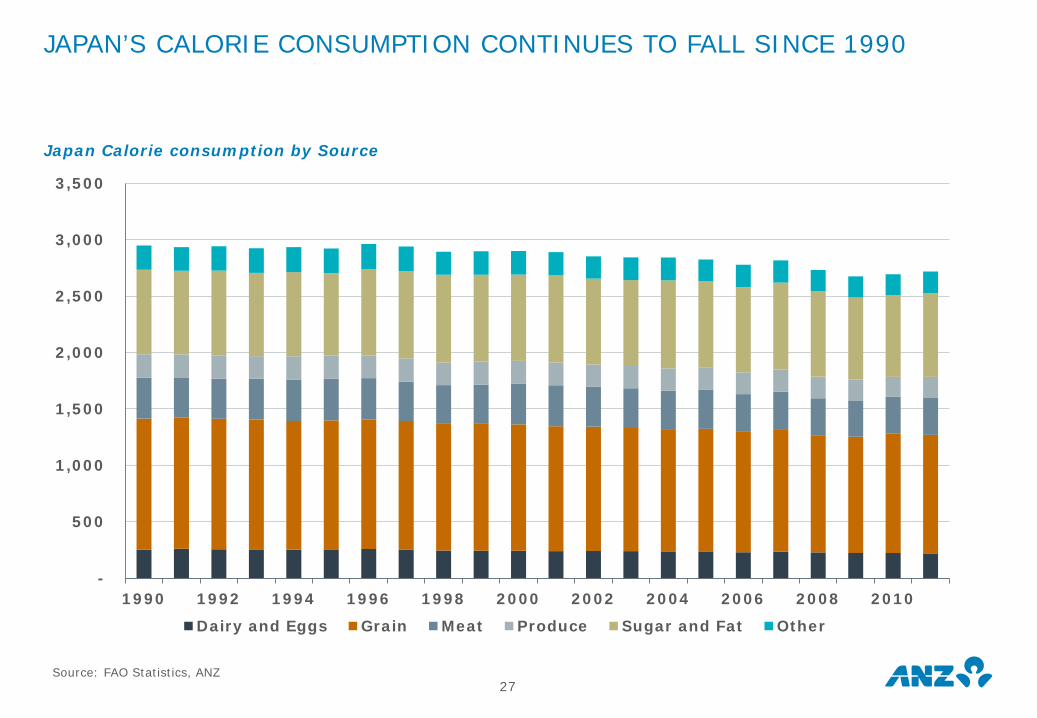

JAPAN’S CALORIE CONSUMPTION CONTINUES TO FALL SINCE 1990

Japan Calorie consumption by Source

Source: FAO Statistics, ANZ

-

500

1,000

1,500

2,000

2,500

3,000

3,500

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

Dairy and Eggs Grain Meat Produce Sugar and Fat Other

27

GERMANY CALORIE CONSUMPTION HAD INCREASED BUT STAGNATED IN RECENT PAST

Germany Calorie consumption by Source

Source: FAO Statistics, ANZ

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

Dairy and Eggs Grain Meat Produce Sugar and Fat Other

28

EVEN WITH LOW GROWTH SCENARIO, CHINA REMAINS IMPORTANT

Nominal Private Consumption Estimate – 20201 (USD trillions)

Notes: 1. Sourced from World Economic Forum; China real GDP is assumed to

be 5.5% pa

0.1

0.6

1.6

2010 2015 2020

China e-commerce, Gross merchandise value (USD trillions)

Source: WEF, BCG Analysis

12.4

4.2

1.3 2.4 1.8 1.8 1.3

2.6

2.3

1.6 0.4

0.5 0.3 0.4

-

$2tr

$4tr

$6tr

$8tr

$10tr

$12tr

$14tr

$16tr

US China India Japan Germany UK France

Private Consumption, 2015 Consumption growth 2015-20

29

58% 23%

4% 3%

2% 11%

Tmall

JD

Suning

VIP.com

Gome.com

Other

30

EMPHASIS ON USER EXPERIENCE, LOGISTICS SERVICES AND NEW CATEGORY EXPANSION

China B2C Online Shopping Market Share by GMV - 2015

788

137

884

Same Day Next DayAlibaba Cainiao JD.Com

Number of Cities for Same Day Delivery/Next Day Delivery

19% 15%

7% 8%

36% 30%

11% 18%

6% 6% 5% 12% 16% 11%

2015 2020e

Others

Packaged Food &DrinkHome Furnishing

Maternal & Child

Apparel

B&PC

ConsumerElectronics

Alibaba's parcels delivered

42m/day 100m/day

Traceability

Premiumisation

Differentiation

34%

20% 21%

-

50

100

150

200

China Australia USA'15 '20F CAGR (15-20F)

-

8%

16%

24%

32%

40%

'14 '15E '16F '17F '18F '19FChina Australia USA

INCREASING ONLINE GROCERY RETAIL

GROWING SHARE OF ECOMMERCE SALES2,3 Proportion of Total Retail Sales

RISING DIGITAL BUYER PENETRATION1,3 % of population

32.7% 51.7%

63.1% 66.3%

62.8% 71.1%

2014 2019F

ONLINE GROCERY MARKET 2015-2020F

With rising internet penetration ecommerce sales is expected to grow; online grocery market, although smaller in size, is forecast to grow by over 20% per annum in China, Australia & USA from 2015-2020F

• Online penetration of grocery is low in China. One of the primary reasons is slow development of cold-chain delivery infrastructure and shipping standards, especially in fresh food category

• Investments in online grocery and food has been on the rise since 2015

• Major online grocery players:

• Online grocery sales accounted for only 2.5% of total grocery revenue in 2015-16

• Companies such as Woolworths and Coles have invested significantly in online shopping solutions to ensure fast and efficient delivery

• Major online grocery players:

• Online grocery market is only a small share of USA grocery market at 2%

• In USA, over 2016, online grocery penetration for fresh foods and packaged foods is expected to increase from 8% to 26% and 16% to 28%, respectively

• Major online grocery players:

Key Market Trends/Issues

Source: eMarketer Worldwide Retail Ecommerce Sales 2014-2019 report, IBISWorld, Morgan Stanley Global Ecommerce report (Jan 2016), EY – The Retailer report (Jul-Sep 2015), ANZ Analysis

Note 1: Ages 14+ internet users who have purchased at least one item/service via online in a calendar year through any digital channel Note 3: For USA, forecast from Aug 2015; China excludes Hong Kong 31

Demand Analytics

32

THE EVOLVING AUSTRALIA CHINA WINE SUPPLY CHAIN: ACTIVE CHANNEL

S1

S2

S3

S4

S5

+

+

Active Supply Chain Facilitation

Product Transfer

33

THE EVOLVING AUSTRALIA CHINA MEAT SUPPLY CHAIN

Current State: Passive Supply Chain Participation

Market Intelligence

Future State: Active Supply Chain Participation to Create Sustainable

Thank You Michael Whitehead

34