odeon & uci cinemas group - amazon s3 · issue of £300m 9% senior secured notes and €200m...

TRANSCRIPT

Q1 2011 Investor Presentation

21 June 2011

Odeon & UCI Finco plc

ODEON & UCI Cinemas Group

Disclaimer

DISCLAIMER

THIS DOCUMENT HAS BEEN PREPARED BY ODEON & UCI FINCO PLC (“ODEON”). BY REVIEWING THIS

DOCUMENT OR PARTICIPATING IN THE CONFERENCE CALL THAT PRESENTS IT, YOU AGREE TO BE

BOUND BY THE FOLLOWING CONDITIONS.

THIS DOCUMENT IS FOR INFORMATION PURPOSES ONLY AND DOES NOT CONSTITUTE AN OFFER TO

SELL OR THE SOLICITATION OF AN OFFER TO BUY SECURITIES IN ODEON. FURTHERMORE, IT DOES

NOT CONSTITUTE A RECOMMENDATION BY ODEON OR ANY OTHER PARTY TO SELL OR BUY

SECURITIES IN ODEON OR ANY OTHER SECURITIES. ALL WRITTEN OR ORAL FORWARD-LOOKING

STATEMENTS ATTRIBUTABLE TO ODEON OR PERSONS ACTING ON THEIR BEHALF ARE QUALIFIED

IN THEIR ENTIRETY BY THESE CAUTIONARY STATEMENTS.

Unaudited Information

This document contains financial information regarding ODEON and its fellow subsidiaries (the “Group”). Such

financial information may not have been audited, reviewed or verified by any independent accounting firm. The

inclusion of such financial information in this document or any related presentation should not be regarded as a

representation or warranty by ODEON, any of its respective affiliates, advisors or representatives or any other

person as to the accuracy or completeness of such information‟s portrayal of the financial condition or results of

operations by the Group.

Non-GAAP information

We have presented certain non-GAAP information in this document. As used in this document, this information

includes „„EBITDA‟‟, which represents earnings before interest, tax, depreciation, amortisation, exceptional

items and strategic costs. Our management believes that EBITDA is meaningful for investors because it

provides an analysis of our operating results, profitability and ability to service debt and because EBITDA is

used by our chief operating decision makers to track our business evolution, establish operational and strategic

targets and make important business decisions. In addition, we believe that EBITDA is a measure commonly

used by investors and other interested parties in our industry.

2

Forward-Looking Statements

Forward-Looking Statements

This document includes forward-looking statements. When used in this document, the words

"anticipate," "believe," "estimate," "forecast," "expect," "intend," "plan" and "project" and similar

expressions, as they relate to ODEON, its management or third parties, identify forward-looking

statements. Forward-looking statements include statements regarding ODEON‟s business strategy,

financial condition, results of operations, and market data, as well as any other statements that are not

historical facts. These statements reflect beliefs of ODEON‟s management, as well as assumptions

made by its management and information currently available to ODEON. Although ODEON believes that

these beliefs and assumptions are reasonable, the statements are subject to numerous factors, risks

and uncertainties that could cause actual outcomes and results to be materially different from those

projected. These factors, risks and uncertainties expressly qualify all subsequent oral and written

forward-looking statements attributable to ODEON or persons acting on its behalf.

3

Q1 2011 Highlights

Results are as reported in the Offering Memorandum (the “OM”) dated 13 May 2011.

EBITDA of £23.7m in Q1 was ahead of management expectations but 25% behind 2010, which was

unusually phased. However Q1 2011 was ahead of 2009 by 29% and 2008 by 77%

Strong local product in Q1 led to good attendance especially:

– The King‟s Speech (mainly in the UK)

– Che Bella Giornata (Italy)

Nevertheless attendance was lower than the unusual Q1 2010 (-9%) but higher than 2009 (5%) and

2008 (7%).

Lower 3D content than in 2010 which was driven by Avatar and Alice in Wonderland. Therefore ATP

was down 2% on 2010 but up on 2009 by 10% and 2008 by 19%

Q1 featured a high proportion of local and older-skewing product that is typically less retail-friendly and

therefore RPH was down 2% on 2010 but up on 2009 by 4% and 2008 by 6%

For these reasons, revenue of £169.0m was 10% lower than 2010 but higher on 2009 by 11% and

2008 by 18%

Gross profit margin improved because of lower film hire costs on less blockbuster product

Operating costs were controlled to an increase of less than 1% on constant estate on prior year

despite inflationary pressures, but EBITDA margin deteriorated because of the impact of fixed costs in

a lower volume quarter

4

2011 Activity Highlights to date

1,262 digital screens being rolled out to reach 59% of the total estate by the end of June 2011

(including completed acquisitions to date)

New site at La Coruna opened on 15 April 2011 with 12 screens including our first proprietary big-

screen format branded as iSens

Four acquisitions have been completed adding 27 cinemas and 294 screens in Spain, Italy and Ireland

Including the Pathe acquisition from December 2010 we have invested £102m over six months and

increased the number of screens by 15%

Issue of £300m 9% senior secured notes and €200m senior secured floating rate notes both due in

2018 on 13 May 2011

Launch of IMAX and proprietary big-screen format called iSens cinemas in our Continental Europe

estate with three and two cinemas to date respectively

Three cinemas in Continental Europe have been fully refurbished

Several cinemas in both the UK and Continental Europe have benefited from retail and seating-led

refurbishments and several more are in the pipeline for the rest of 2011

5

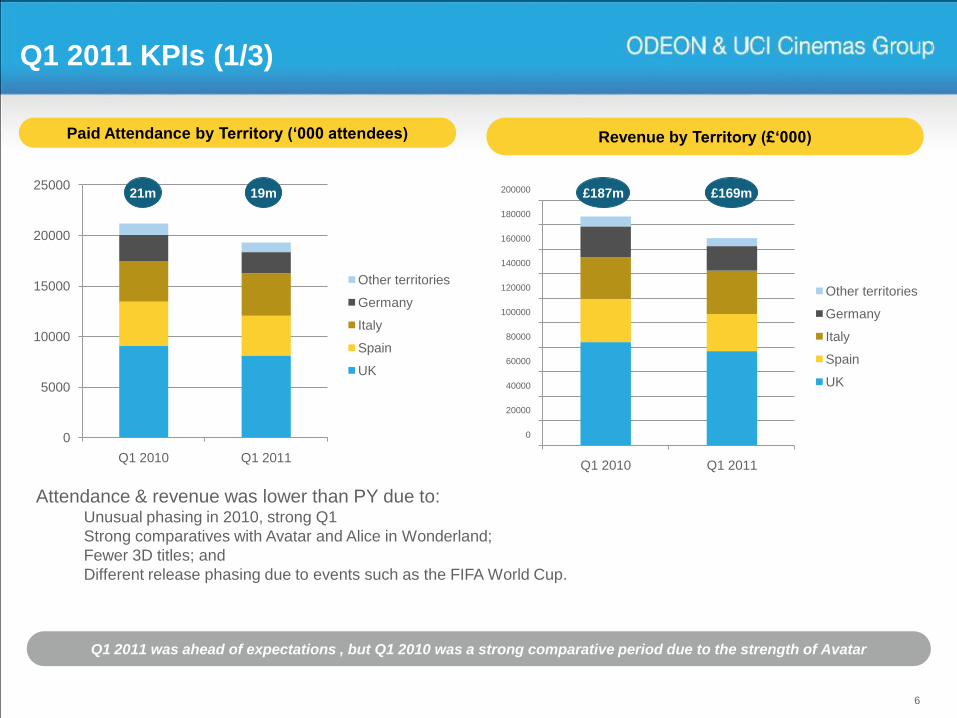

Q1 2011 KPIs (1/3)

6

0

5000

10000

15000

20000

25000

Q1 2010 Q1 2011

Other territories

Germany

Italy

Spain

UK

0

20000

40000

60000

80000

100000

120000

140000

160000

180000

200000

Q1 2010 Q1 2011

Other territories

Germany

Italy

Spain

UK

Paid Attendance by Territory („000 attendees) Revenue by Territory (£„000)

Q1 2011 was ahead of expectations , but Q1 2010 was a strong comparative period due to the strength of Avatar

Attendance & revenue was lower than PY due to:Unusual phasing in 2010, strong Q1

Strong comparatives with Avatar and Alice in Wonderland;

Fewer 3D titles; and

Different release phasing due to events such as the FIFA World Cup.

21m 19m £169m£187m

UK Top films Q1

7

Top 5 in the UK was 23% lower than 2010 but 41% higher than 2009

2011 2010 2009

Title (GBOR

„000s)

Title (GBOR

„000s)

Title (GBOR

„000s)

The King‟s Speech 44,525 Avatar 63,915 Slumdog Millionaire 30,960

Tangled 20,156 Alice in Wonderland 36,647 Bolt 17,695

Black Swan 16,047 Sherlock Holmes 17,384 Marley and Me 11,165

Gnomeo & Juliet 15,324 Alvin & The

Chipmunks

13,383 He‟s Just Not That

Into You

9,449

Paul 14,081 The Princess and

the Frog

11,028 The Curious Case

of Benjamin Button

9,048

Total 110,133 Total 142,357 Total 78,317

Variance to 2010 (23%)

Variance to 2009 41%

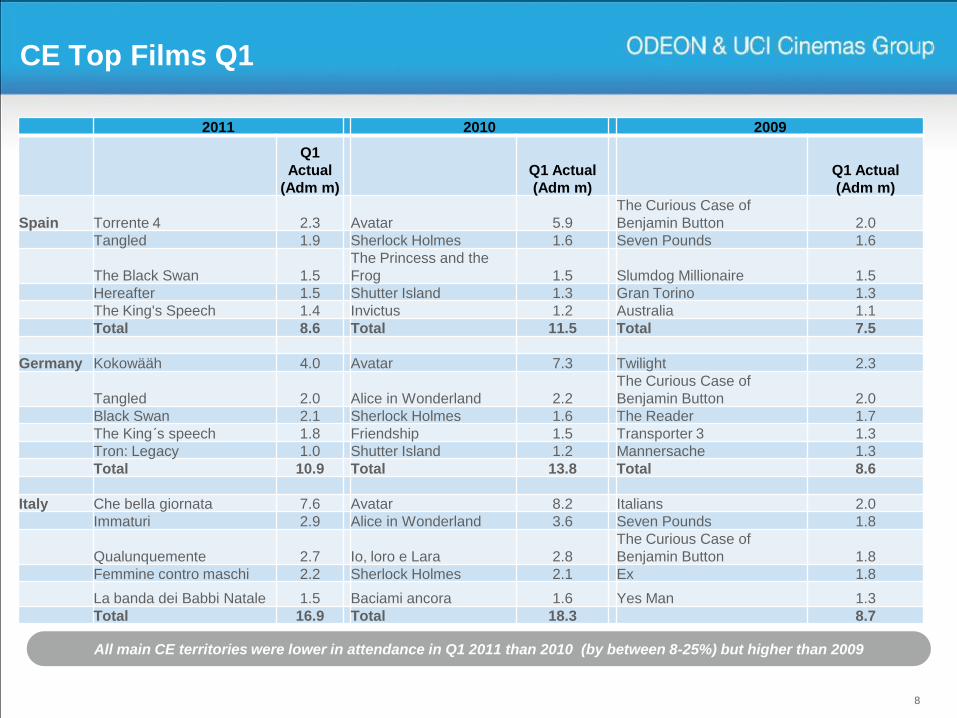

CE Top Films Q1

8

2011 2010 2009

Q1

Actual

(Adm m)

Q1 Actual

(Adm m)

Q1 Actual

(Adm m)

Spain Torrente 4 2.3 Avatar 5.9

The Curious Case of

Benjamin Button 2.0

Tangled 1.9 Sherlock Holmes 1.6 Seven Pounds 1.6

The Black Swan 1.5

The Princess and the

Frog 1.5 Slumdog Millionaire 1.5

Hereafter 1.5 Shutter Island 1.3 Gran Torino 1.3

The King's Speech 1.4 Invictus 1.2 Australia 1.1

Total 8.6 Total 11.5 Total 7.5

Germany Kokowääh 4.0 Avatar 7.3 Twilight 2.3

Tangled 2.0 Alice in Wonderland 2.2

The Curious Case of

Benjamin Button 2.0

Black Swan 2.1 Sherlock Holmes 1.6 The Reader 1.7

The King´s speech 1.8 Friendship 1.5 Transporter 3 1.3

Tron: Legacy 1.0 Shutter Island 1.2 Mannersache 1.3

Total 10.9 Total 13.8 Total 8.6

Italy Che bella giornata 7.6 Avatar 8.2 Italians 2.0

Immaturi 2.9 Alice in Wonderland 3.6 Seven Pounds 1.8

Qualunquemente 2.7 Io, loro e Lara 2.8

The Curious Case of

Benjamin Button 1.8

Femmine contro maschi 2.2 Sherlock Holmes 2.1 Ex 1.8

La banda dei Babbi Natale 1.5 Baciami ancora 1.6 Yes Man 1.3

Total 16.9 Total 18.3 8.7

All main CE territories were lower in attendance in Q1 2011 than 2010 (by between 8-25%) but higher than 2009

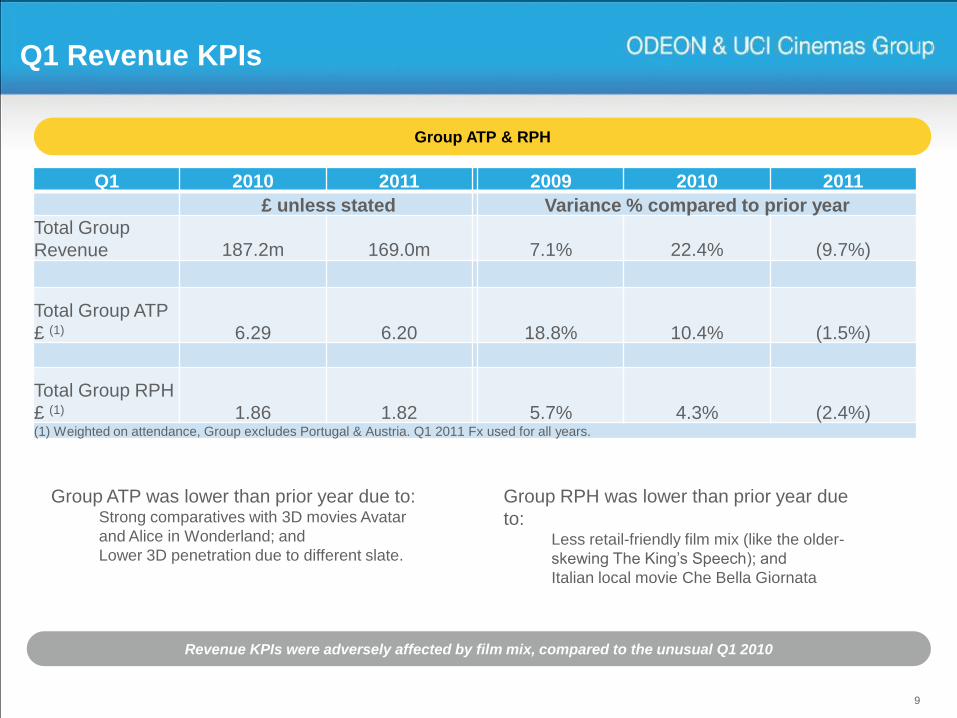

Q1 Revenue KPIs

9

Group ATP & RPH

Revenue KPIs were adversely affected by film mix, compared to the unusual Q1 2010

Group ATP was lower than prior year due to:Strong comparatives with 3D movies Avatar

and Alice in Wonderland; and

Lower 3D penetration due to different slate.

Group RPH was lower than prior year due

to:Less retail-friendly film mix (like the older-

skewing The King‟s Speech); and

Italian local movie Che Bella Giornata

Q1 2010 2011 2009 2010 2011

£ unless stated Variance % compared to prior year

Total Group

Revenue 187.2m 169.0m 7.1% 22.4% (9.7%)

Total Group ATP

£ (1) 6.29 6.20 18.8% 10.4% (1.5%)

Total Group RPH

£ (1) 1.86 1.82 5.7% 4.3% (2.4%)(1) Weighted on attendance, Group excludes Portugal & Austria. Q1 2011 Fx used for all years.

Q1 2011 Margins and Costs

10

Gross Profit Margin and EBITDA Margin analysis

Strong cost performance in the quarter, benefiting from lower film costs and good control on operating costs

Gross Profit Margin was higher than in the

prior year due to lower film hire costs due to

fewer blockbusters

EBITDA margin was lower than prior year

due to the impact of fixed costs on lower

group revenue

£m unless otherwise stated Q1 2010 Q1 2011 Variance from Q1

2010

Group revenue 187.2 169.0 (9.7%)

Cost of sales (70.2) (58.6) 16.5%

Gross Profit 117.0 110.4 5.6%

Gross Profit Margin 62.5% 65.3% 280 bps

Operating costs 85.4 86.7 1.5%

EBITDA 31.5 23.7 (25.0%)

EBITDA Margin 16.8% 14.0% (280 bps)

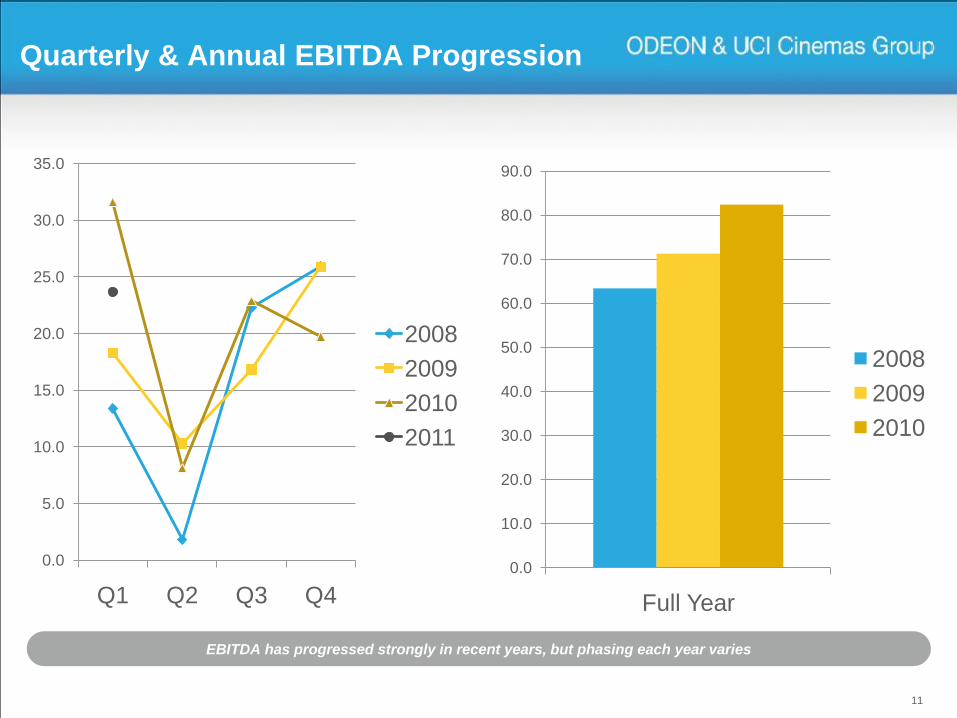

Quarterly & Annual EBITDA Progression

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

Q1 Q2 Q3 Q4

2008

2009

2010

2011

11

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

Full Year

2008

2009

2010

EBITDA has progressed strongly in recent years, but phasing each year varies

12

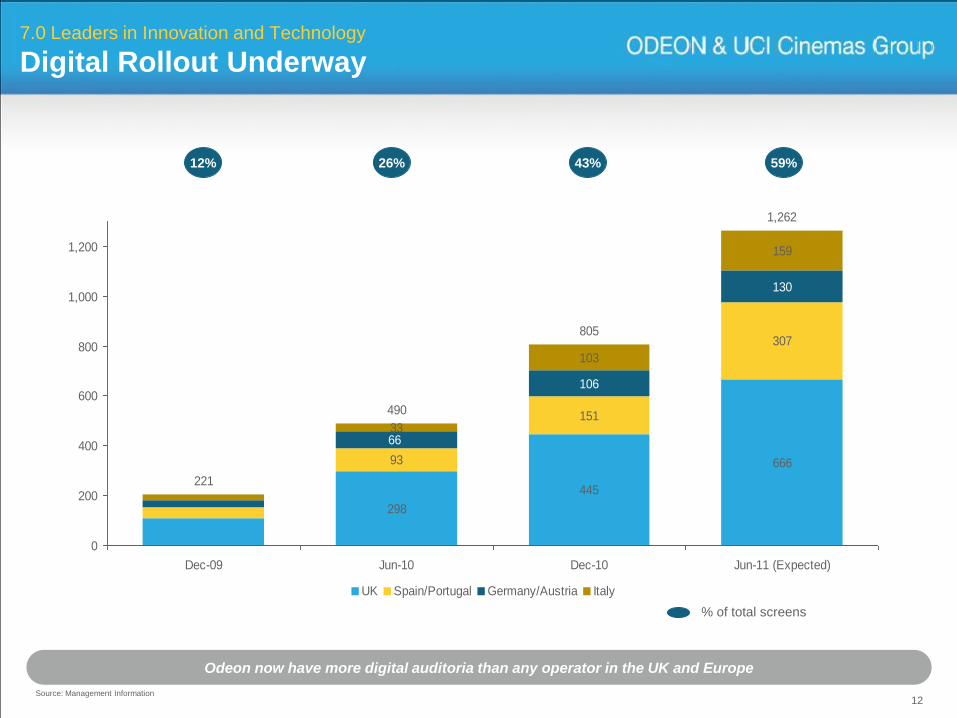

7.0 Leaders in Innovation and Technology

Digital Rollout Underway

Odeon now have more digital auditoria than any operator in the UK and Europe

% of total screens

Source: Management Information

298

445

66693

151

307

106

130

33

103

159

221

490

805

1,262

6629

0

200

400

600

800

1,000

1,200

Dec-09 Jun-10 Dec-10 Jun-11 (Expected)

UK Spain/Portugal Germany/Austria Italy

12% 26% 59%43%

13

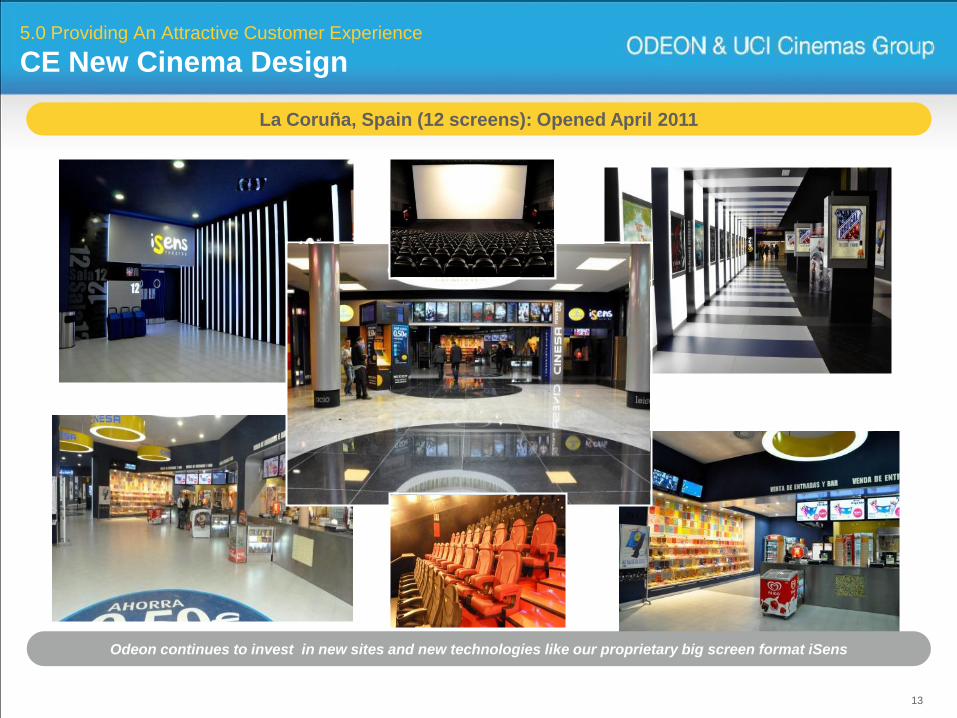

5.0 Providing An Attractive Customer Experience

CE New Cinema Design

La Coruña, Spain (12 screens): Opened April 2011

Odeon continues to invest in new sites and new technologies like our proprietary big screen format iSens

UK 2011 Initiatives

IMAX– A twelfth IMAX site at London Swiss Cottage is being installed. The entire Swiss Cottage site is

being refurbished with new screens. Anticipated relaunch date during Q3 2011.

Costa– We continue to find appropriate opportunities to expand our Costa franchise in the UK. Two new

sites have recently opened at Putney and Aylesbury bringing our total estate to 17 locations

Retail refurbishments were completed in May in Bracknell, Warrington and

Dudley

Retail Matters programme that targets increased perception of value for money

for our retail range has now been rolled out to all UK sites and is due to be

completed by the end of June 2011 in Ireland

Seating refurbishments are due to be completed at Guildford and Cardiff by the

end of June in time for the release of Harry Potter and the Deathly Hallows Part

II

14

CE 2011 Initiatives

IMAX– We have begun a series of trials of the format in CE – three sites opened in May in Madrid, Majorca

and Milan

iSens– We have also launched a trial of our own proprietary Big Screen format in CE called iSens – two

sites opened since April in La Coruna and Principe Pio (Madrid). We also plan an additional four

installations in Germany and Italy during 2011

Refurbishments– Since year-end we have fully refurbished Arrabida (Portugal), Las Rozas (Madrid) and Vienna SCS

(Austria) sites.

– We continue to invest in Loge and VIP seating in Germany where new products were rolled out at

Leipzig, Huerth, Othmarschen Hamburg

– The three Pathe sites acquired in Italy in December have been fully rebranded to UCI with new retail

offerings

– New Pick „n‟ Mix walls have been installed in Italy and Germany

– Completed refurbishment of retail areas at Vienna MEC cinema in Austria

15

16

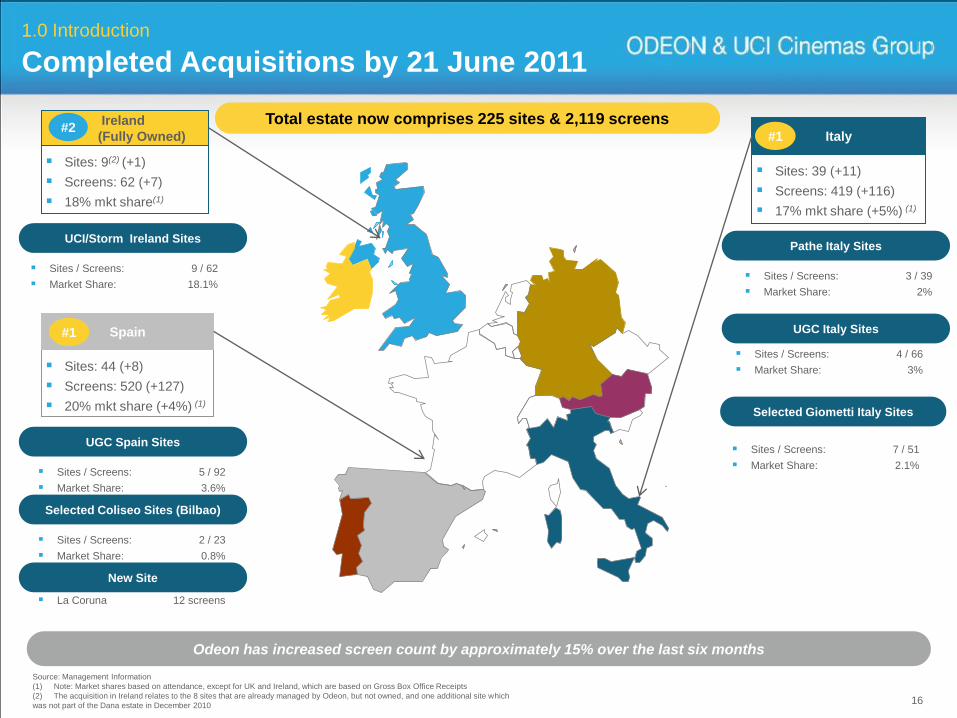

Total estate now comprises 225 sites & 2,119 screens

Source: Management Information

(1) Note: Market shares based on attendance, except for UK and Ireland, which are based on Gross Box Office Receipts

(2) The acquisition in Ireland relates to the 8 sites that are already managed by Odeon, but not owned, and one additional site which

was not part of the Dana estate in December 2010

Ireland

(Fully Owned)

Sites: 9(2) (+1)

Screens: 62 (+7)

18% mkt share(1)

#2

Sites: 44 (+8)

Screens: 520 (+127)

20% mkt share (+4%) (1)

Spain#1

Sites: 39 (+11)

Screens: 419 (+116)

17% mkt share (+5%) (1)

Italy#1

Odeon has increased screen count by approximately 15% over the last six months

1.0 Introduction

Completed Acquisitions by 21 June 2011

Sites / Screens: 9 / 62

Market Share: 18.1%

UCI/Storm Ireland Sites

Sites / Screens: 5 / 92

Market Share: 3.6%

UGC Spain Sites

Sites / Screens: 3 / 39

Market Share: 2%

Pathe Italy Sites

Sites / Screens: 4 / 66

Market Share: 3%

UGC Italy Sites

Sites / Screens: 2 / 23

Market Share: 0.8%

Selected Coliseo Sites (Bilbao)

La Coruna 12 screens

New Site

Selected Giometti Italy Sites

Sites / Screens: 7 / 51

Market Share: 2.1%

Acquisition Economics

Over £100m invested over the last six months

Acquisition EBITDA multiples in the range of 6 to 8 times, EBITDA acquired of c.£15m in total

Improvements to come from:

– Film hire costs

– Retail Cost

– Average ticket price

– Retail per head

– Operating cost reductions

– Digital conversion synergies

– New site pipeline

Typically we have doubled EBITDA over the past six acquisitions

Profit improvements usually delivered within 2 years

Post-acquisition EBITDA multiples expected to be in the range of 3 to 5 times on average

17

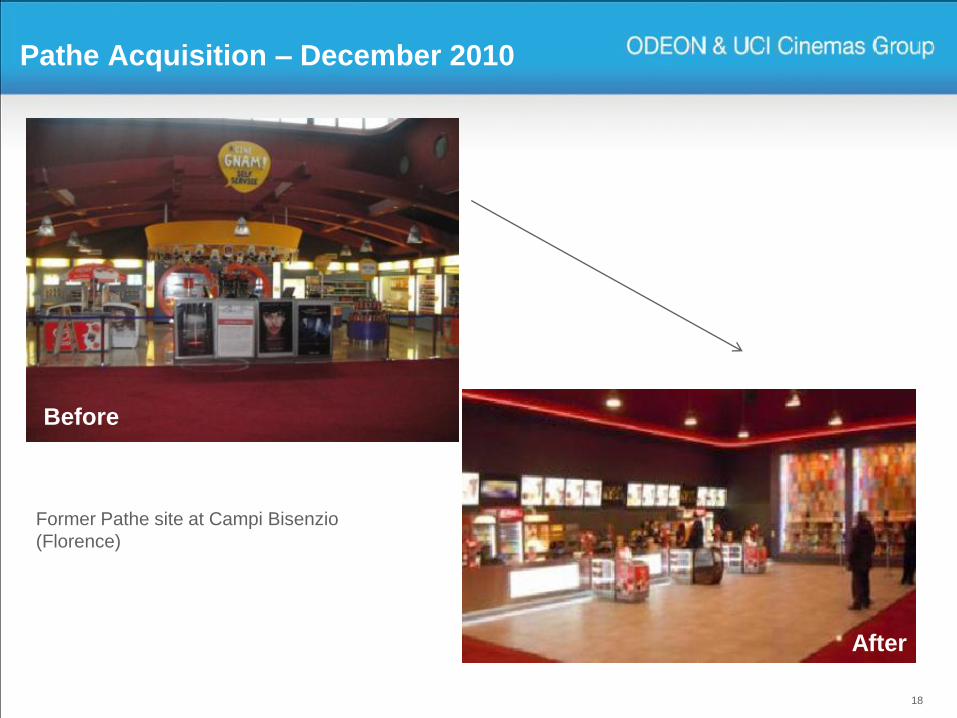

Pathe Acquisition – December 2010

18

Before

AfterAfter

Former Pathe site at Campi Bisenzio

(Florence)

19

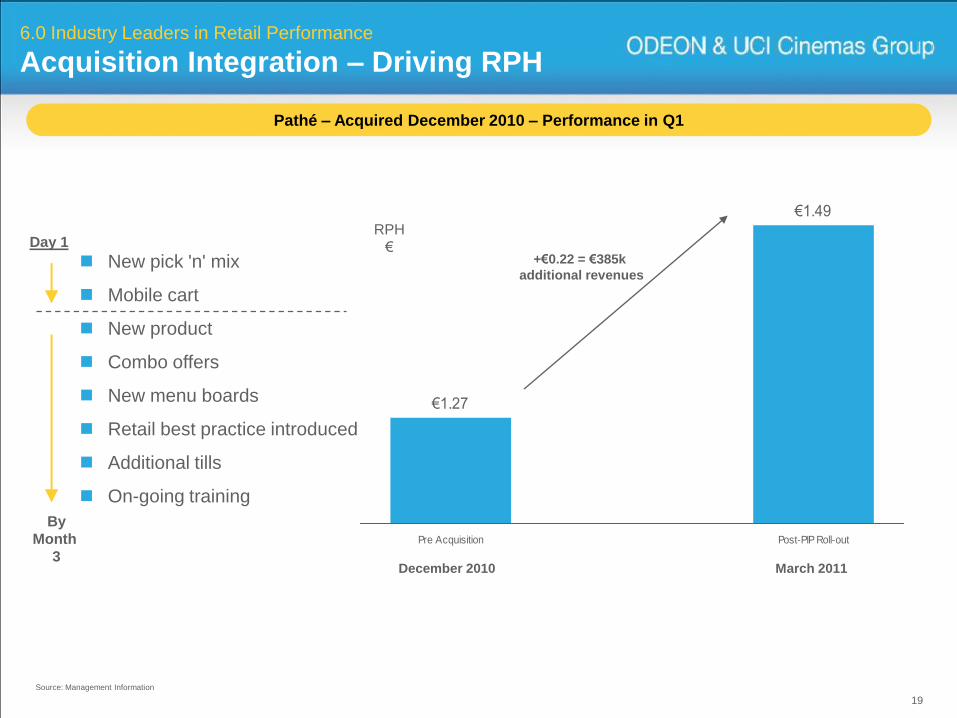

€1.27

€1.49

Pre Acquisition Post-PIP Roll-out

6.0 Industry Leaders in Retail Performance

Acquisition Integration – Driving RPH

+€0.22 = €385k

additional revenues

Pathé – Acquired December 2010 – Performance in Q1

New pick 'n' mix

Mobile cart

New product

Combo offers

New menu boards

Retail best practice introduced

Additional tills

On-going training

Day 1

December 2010 March 2011

By

Month

3

RPH

€

Source: Management Information

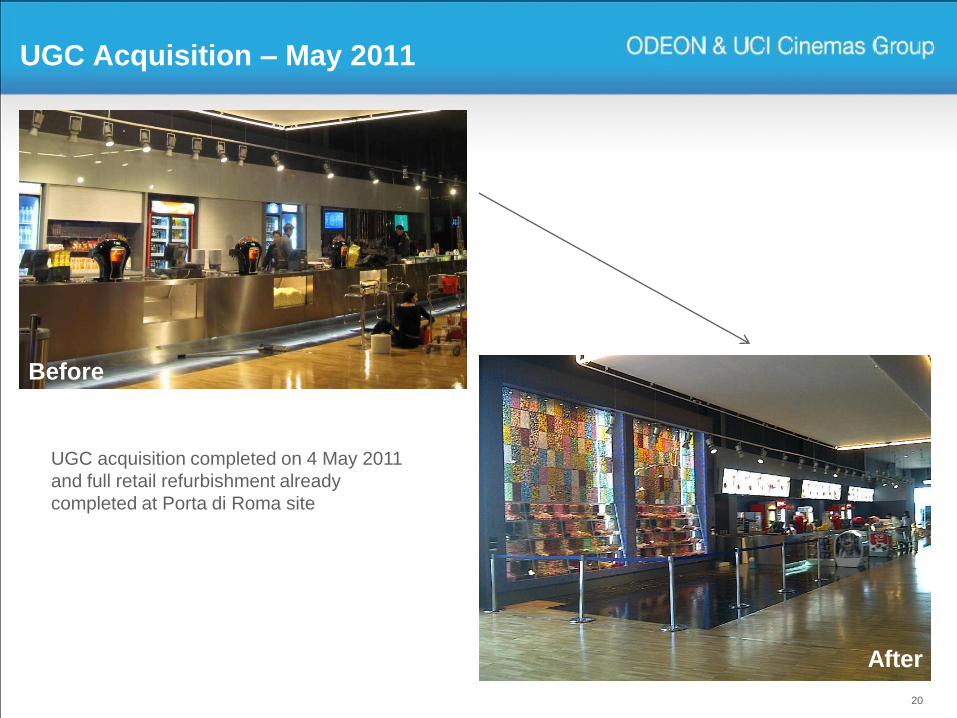

UGC Acquisition – May 2011

20

Before

AfterAfter

Before

After

UGC acquisition completed on 4 May 2011

and full retail refurbishment already

completed at Porta di Roma site

21

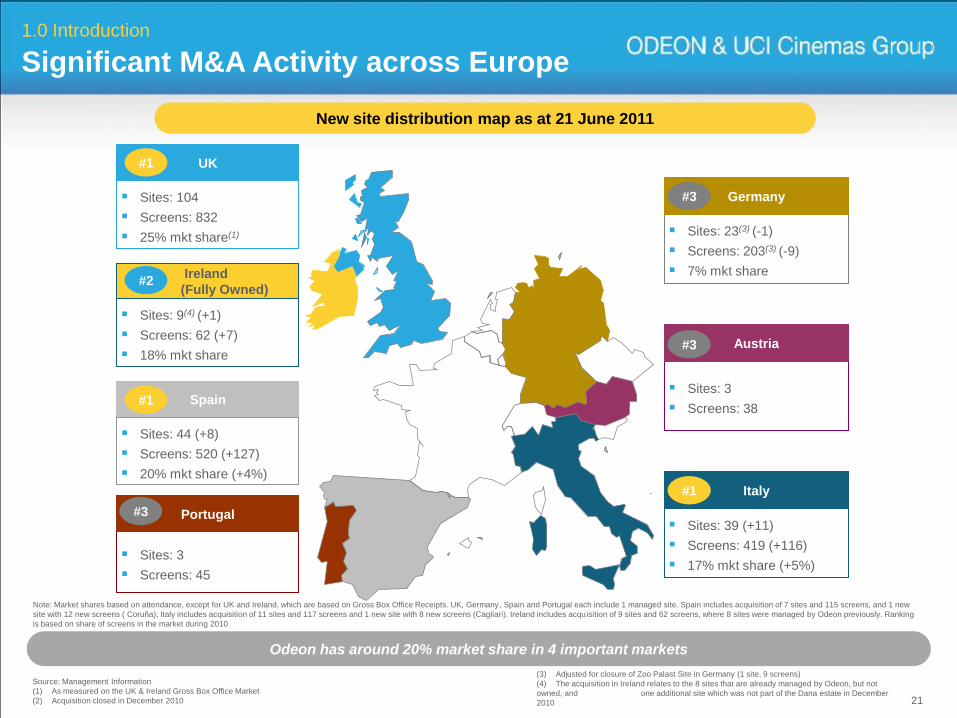

New site distribution map as at 21 June 2011

Source: Management Information

(1) As measured on the UK & Ireland Gross Box Office Market

(2) Acquisition closed in December 2010

Note: Market shares based on attendance, except for UK and Ireland, which are based on Gross Box Office Receipts. UK, Germany, Spain and Portugal each include 1 managed site. Spain includes acquisition of 7 sites and 115 screens, and 1 new

site with 12 new screens ( Coruña); Italy includes acquisition of 11 sites and 117 screens and 1 new site with 8 new screens (Cagliari). Ireland includes acquisition of 9 sites and 62 screens, where 8 sites were managed by Odeon previously. Ranking

is based on share of screens in the market during 2010

UK

Sites: 104

Screens: 832

25% mkt share(1)

#1

Ireland

(Fully Owned)

Sites: 9(4) (+1)

Screens: 62 (+7)

18% mkt share

#2

Sites: 44 (+8)

Screens: 520 (+127)

20% mkt share (+4%)

Spain#1

Sites: 3

Screens: 45

Portugal#3 Sites: 39 (+11)

Screens: 419 (+116)

17% mkt share (+5%)

Italy#1

Sites: 3

Screens: 38

Austria#3

Sites: 23(3) (-1)

Screens: 203(3) (-9)

7% mkt share

Germany#3

Odeon has around 20% market share in 4 important markets

1.0 Introduction

Significant M&A Activity across Europe

(3) Adjusted for closure of Zoo Palast Site in Germany (1 site, 9 screens)

(4) The acquisition in Ireland relates to the 8 sites that are already managed by Odeon, but not

owned, and one additional site which was not part of the Dana estate in December

2010

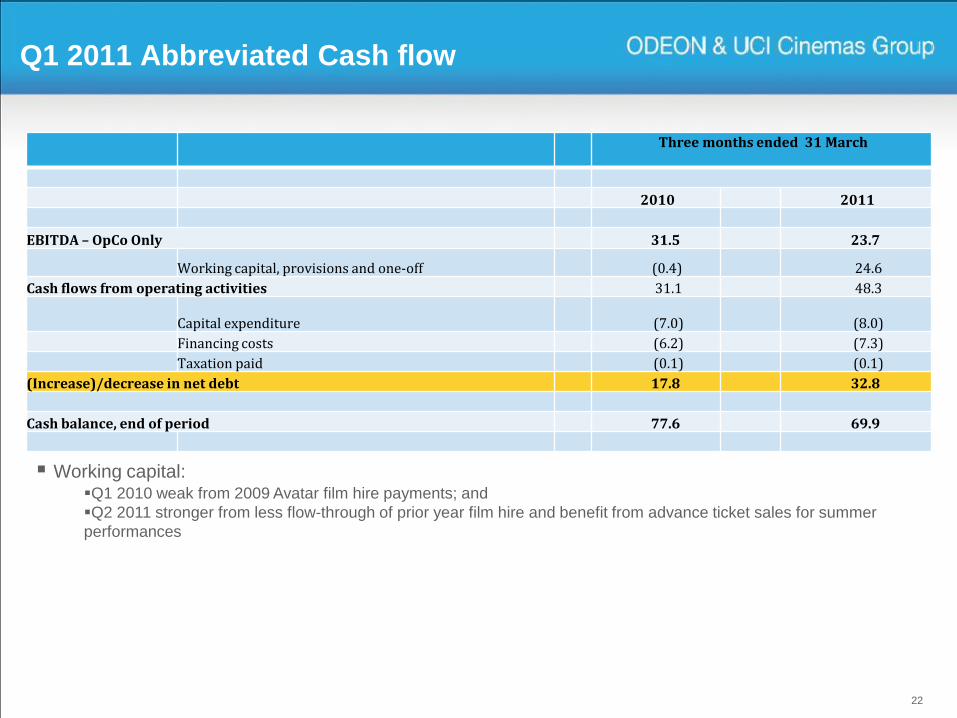

Q1 2011 Abbreviated Cash flow

Three months ended 31 March

2010 2011

EBITDA – OpCo Only 31.5 23.7

Working capital, provisions and one-off (0.4) 24.6

Cash flows from operating activities 31.1 48.3

Capital expenditure (7.0) (8.0)

Financing costs (6.2) (7.3)

Taxation paid (0.1) (0.1)

(Increase)/decrease in net debt 17.8 32.8

Cash balance, end of period 77.6 69.9

22

Working capital:Q1 2010 weak from 2009 Avatar film hire payments; and

Q2 2011 stronger from less flow-through of prior year film hire and benefit from advance ticket sales for summer

performances

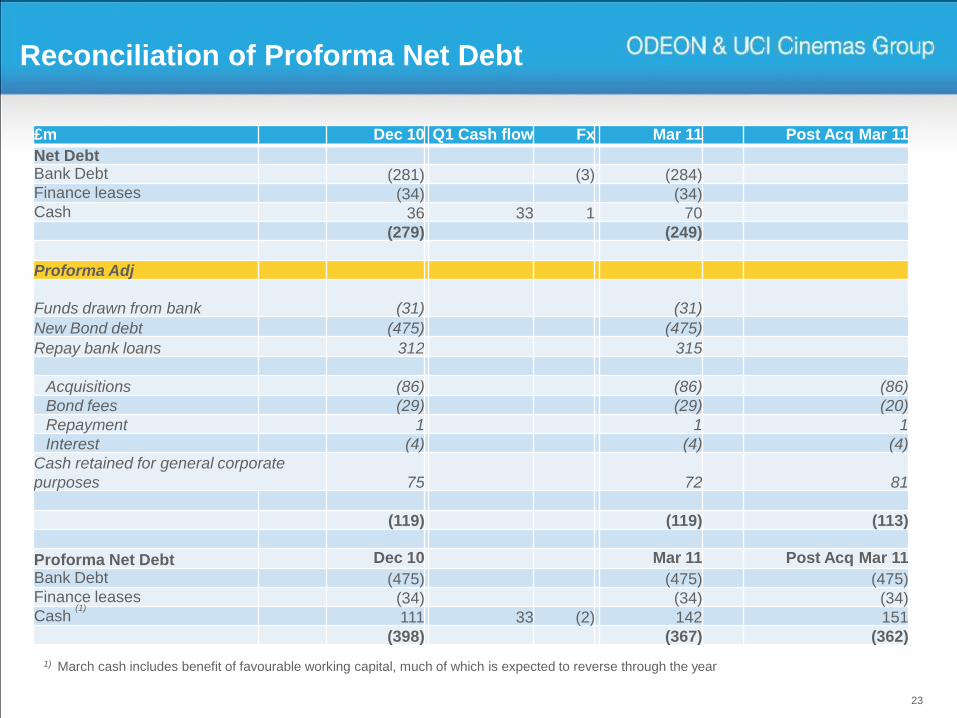

Reconciliation of Proforma Net Debt

23

£m Dec 10 Q1 Cash flow Fx Mar 11 Post Acq Mar 11

Net DebtBank Debt (281) (3) (284)Finance leases (34) (34)Cash 36 33 1 70

(279) (249)

Proforma Adj

Funds drawn from bank (31) (31)

New Bond debt (475) (475)

Repay bank loans 312 315

Acquisitions (86) (86) (86)

Bond fees (29) (29) (20)

Repayment 1 1 1

Interest (4) (4) (4)

Cash retained for general corporate

purposes 75 72 81

(119) (119) (113)

Proforma Net Debt Dec 10 Mar 11 Post Acq Mar 11

Bank Debt (475) (475) (475)Finance leases (34) (34) (34)Cash

(1)

111 33 (2) 142 151

(398) (367) (362)

1) March cash includes benefit of favourable working capital, much of which is expected to reverse through the year

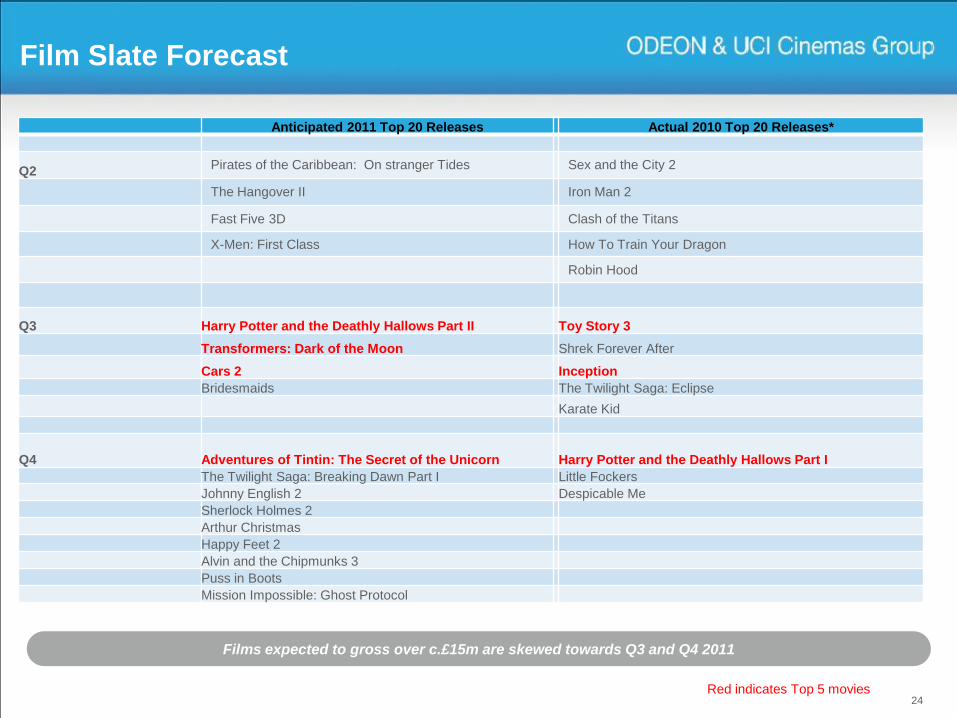

Film Slate Forecast

24

Anticipated 2011 Top 20 Releases Actual 2010 Top 20 Releases*

Q2Pirates of the Caribbean: On stranger Tides Sex and the City 2

The Hangover II Iron Man 2

Fast Five 3D Clash of the Titans

X-Men: First Class How To Train Your Dragon

Robin Hood

Q3 Harry Potter and the Deathly Hallows Part II Toy Story 3

Transformers: Dark of the Moon Shrek Forever After

Cars 2 Inception

Bridesmaids The Twilight Saga: Eclipse

Karate Kid

Q4 Adventures of Tintin: The Secret of the Unicorn Harry Potter and the Deathly Hallows Part I

The Twilight Saga: Breaking Dawn Part I Little Fockers

Johnny English 2 Despicable Me

Sherlock Holmes 2

Arthur Christmas

Happy Feet 2

Alvin and the Chipmunks 3

Puss in Boots

Mission Impossible: Ghost Protocol

Films expected to gross over c.£15m are skewed towards Q3 and Q4 2011

Red indicates Top 5 movies

Current trading & Outlook

Expect to be in line with management expectation YTD, Q2 ahead of last year, but YTD still below 2010

Slower start to the quarter due to the warm, dry weather in April and May in our territories

Stronger than Q2 2010 because of FIFA World Cup in South Africa

KPIs improved on Q1 because of better film mix (3D/blockbuster films) and ahead of prior year

Several potential Top 5 titles in Q3 namely Transformers: Dark of the Moon and Harry Potter and the

Deathly Hallows Part II, both in 3D

Q2 results and next trading/outlook update on 31 August 2011

25

Q&A & AOB

Any questions?

Further questions can be addressed below:– Email: [email protected]

– PR: [email protected]

– Financial PR: Andrew Dowler, Finsbury +44 (0) 20 7251 3801

– Telephone: Jonny Mason +44 (0) 20 7321 6221

26

27