oecd policy work on green investments nelly petkova oecd, environment directorate second...

TRANSCRIPT

OECD POLICY WORK ON GREEN INVESTMENTS

Nelly PetkovaOECD, Environment Directorate

Second international forum for sustainable business development 17 October 2013, Kiev, Ukraine

0

0.5

1

1.5

2

2.5

3

3.5

4

2

Closing the investment gap to 2030

Source: Compilation based on OECD, IEA, ITF, Mc Kinsey, WEF, Kennedy,C.,Corfee-Morlot,J.Energy Policy(2013)Note: Infrastructure sectors including roads, rail, ports, airports, power, water and telecoms

1: Annual average based on global investments over the period 1996-20122. Annual average needs for the period 2012-2030

US

D t

n/ y

ear

+60%

0

0.5

1

1.5

2

2.5

3

3.5

4

Global infrastructure investments - current

Global infrastructure investments needs - BAU

Global infrastructure investments needs - 2°C

scenario

0

0.5

1

1.5

2

2.5

3

3.5

4

Global infrastructure investments - current

Global infrastructure investments needs - BAU

Global infrastructure investments needs - 2°C

scenario

0

0.5

1

1.5

2

2.5

3

3.5

4

Global infrastructure investments - current

Global infrastructure investments needs - BAU

Global infrastructure investments needs - 2°C

scenario

1 2

?

+10% to -16%

?

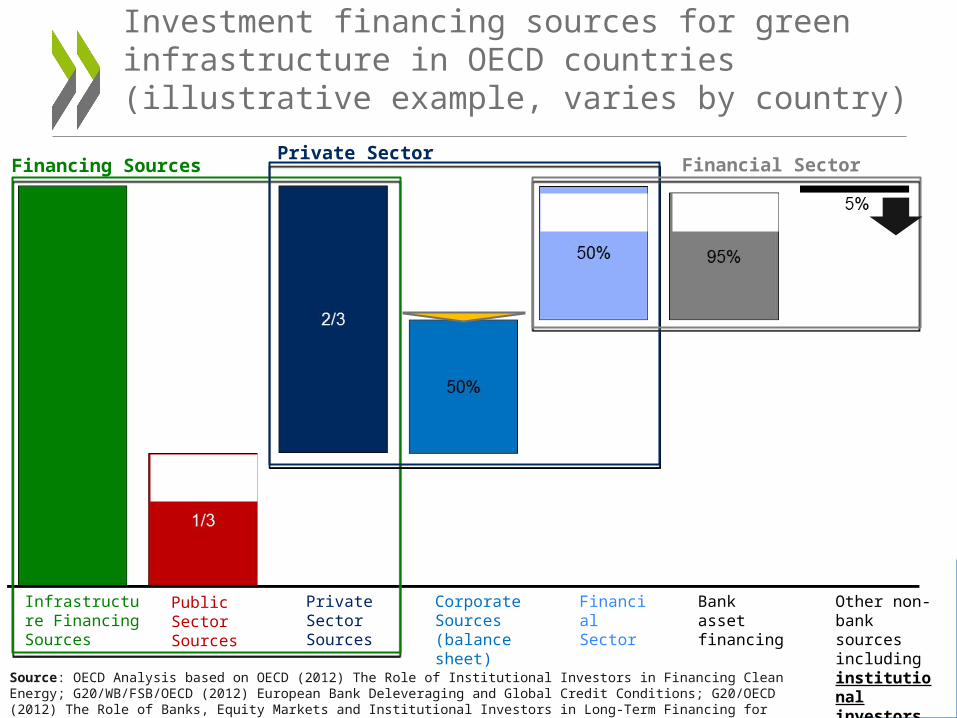

Investment financing sources for green infrastructure in OECD countries (illustrative example, varies by country)

Source: OECD Analysis based on OECD (2012) The Role of Institutional Investors in Financing Clean Energy; G20/WB/FSB/OECD (2012) European Bank Deleveraging and Global Credit Conditions; G20/OECD (2012) The Role of Banks, Equity Markets and Institutional Investors in Long-Term Financing for Growth and Development

Infrastructure Financing Sources

Private Sector Sources

Corporate Sources (balance sheet)

Financial Sector

Bank asset financing

Other non-bank sources including institutional investors

Public Sector Sources

Financing SourcesPrivate Sector

Financial Sector

Average annual ODA to climate-relevant sectors 2010-2011: USD 54 billion

Average annual total ODA 2010-2011: USD 129.3 billion

• ODA to climate-relevant sectors (eg emitting ones) comprises 42% of total ODA from DAC donors in 2010-11.

• Of the total ODA to climate-relevant sectors, 16% of this is to support climate action (i.e. mitigation and/or adaptation is a principal or significant objective).

ODA to climate action, annual average 2010-2011: USD 21 billion

Green vs. brown: Climate-focused ODA as a proportion of total ODA to climate-relevant sectors

* Illustrative chart : represents sectors considered most mitigation and/or adaptation relevant.

New investment in clean energy, 2004 - 2012

Source: Bloomberg New Energy Finance.

Note: Total values include estimates for undisclosed deals. Includes corporate and government R&D. Includes digital energy & energy storage asset investment.

Top 10 countries in clean investments, billion USD

Source: Bloomberg New Energy Finance.

Scale of energy subsidiesEstimated energy subsidies, 2010, USD billion (fossil fuels - USD 409 billion; renewables - USD 66 billion), non-OECD countries

Source: IEA, World Energy Outlook 2011.

Subsidies to fossil fuels Subsidies to renewables

Carbon intensity measured in kilogrammes of CO2 per 2005 USD of GDP

EECCA countries – among the most carbon intensive economies in the world

Source: IEA..

Access to private finance for green investments in EECCA – Objectives of the project

Access to private finance for green investments in EECCA

OECD-Ukraine Co-ordination Council

Agribusiness:Access to Finance

Machinery/Aircraft Manufacturing

Working Group 1 Working Group 3

Civil society and private sector representatives

Relevant ministries and government agencies

Chaired by First Deputy Prime Minister of Ukraine

OECD + donors(including relevant WG members)

The project Sector Competitiveness Strategy for Ukraine was launched in 2009The OECD Eurasia Competitiveness Programme

Energy-efficiency/ Renewable Energy

Working Group 4

Agribusiness:Human Capital

Working Group 2

Facilitate access to finance for SMEs

Improve investment policy and promotion

Strengthen the industry cluster

Ensure appropriate skills provision to the industry

Public-Private dialogue through Working Groups