office of student financial management - sturm … service...but include: need, merit, interest in a...

TRANSCRIPT

Office of Student Financial Management Kasia Palm, Director of Student Financial Management

We advise prospective, current, and former Denver Law students on: General financial aid questions

▪ We do not process student loans, that’s the Office of Financial Aid in University Hall

Denver Law scholarship opportunities

▪ We manage the Named and Endowed Scholarship Process

Financial literacy and debt management including:

▪ Budgeting ▪ Loan repayment & consolidation ▪ Loan forgiveness ▪ Loan Repayment Assistance Program (LRAP)

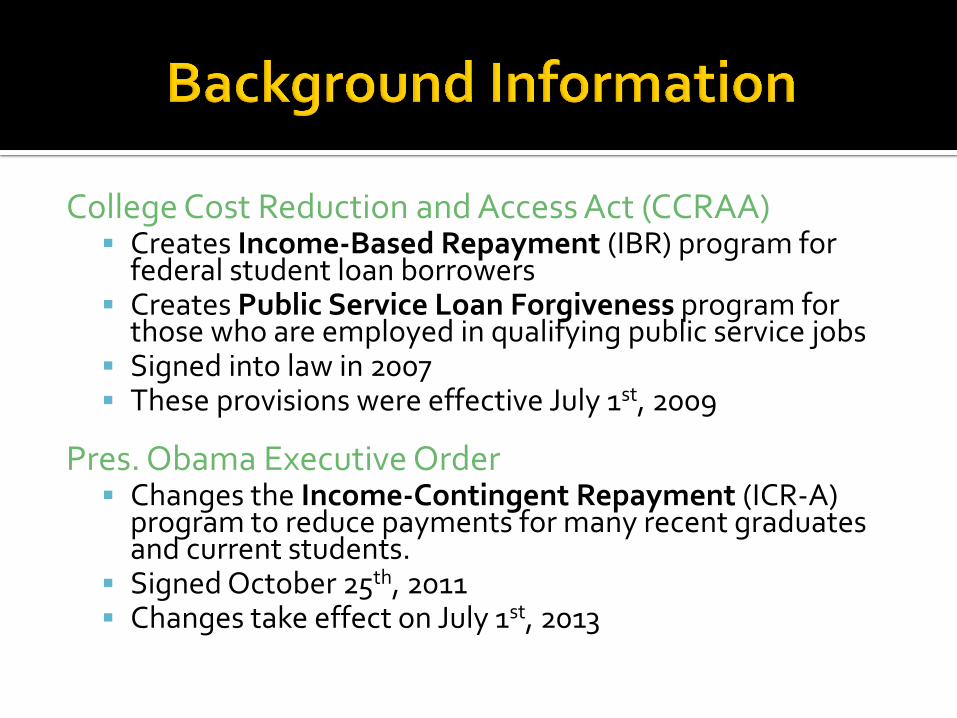

College Cost Reduction and Access Act (CCRAA) Creates Income-Based Repayment (IBR) program for

federal student loan borrowers Creates Public Service Loan Forgiveness program for

those who are employed in qualifying public service jobs Signed into law in 2007 These provisions were effective July 1st, 2009

Pres. Obama Executive Order

Changes the Income-Contingent Repayment (ICR-A) program to reduce payments for many recent graduates and current students.

Signed October 25th, 2011 Changes take effect on July 1st, 2013

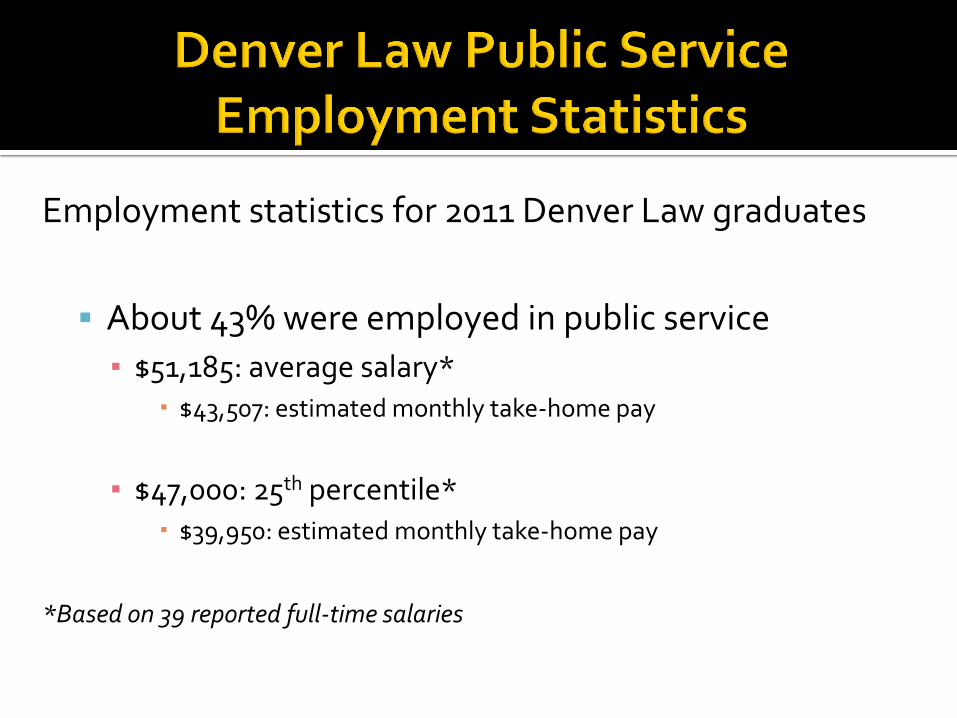

Employment statistics for 2011 Denver Law graduates

About 43% were employed in public service

▪ $51,185: average salary* $43,507: estimated monthly take-home pay

▪ $47,000: 25th percentile* $39,950: estimated monthly take-home pay

*Based on 39 reported full-time salaries

Monthly loan payments can be reduced significantly for borrowers selecting the IBR option ▪ Payments can be as low as $0

▪ Payments don’t have to cover accruing interest

Pay until balance is repaid OR until 300 payments have been made (25 years) ▪ Remaining balance is cancelled

▪ For those working in Public Service jobs, debt can be forgiven after 120 payments (10 years)

Early Implementation of a more beneficial IBR plan ▪ Plan was scheduled to go into affect for students who first

borrowed loans after 7/1/2014

▪ This EO moves up the implementation date to July 2013

To qualify for this plan, you must: ▪ Have no federal loans prior to October 2007

▪ Have at least one loan disbursement made after October 2011

Main differences between ICR-A and IBR: ▪ Monthly payments reduced by 1/3rd

▪ Provides for loan cancellation after 20 years

Payments are determined by: Adjusted Gross Income & family size, not loan balance

▪ Monthly Payment =

* 10% is for ICR-A and 15% for IBR

^ For 2012, 150% of the federal poverty level for a family of 1 in the 48 contiguous states is: $16,755

To qualify for IBR and ICR-A, a borrower must have a partial financial hardship, meaning: IBR/ICR-A Monthly Pymt < Monthly Pymt on Standard 10-yr Repayment Plan

▪ Generally speaking, a single borrower qualifies for IBR if their AGI is less than their loan debt upon entering repayment

▪ Borrowers qualify for ICR-A at higher incomes – if their AGI less than 150-160% of their loan debt

(10% or 15%)* of (AGI – 150% of federal poverty level^) 12

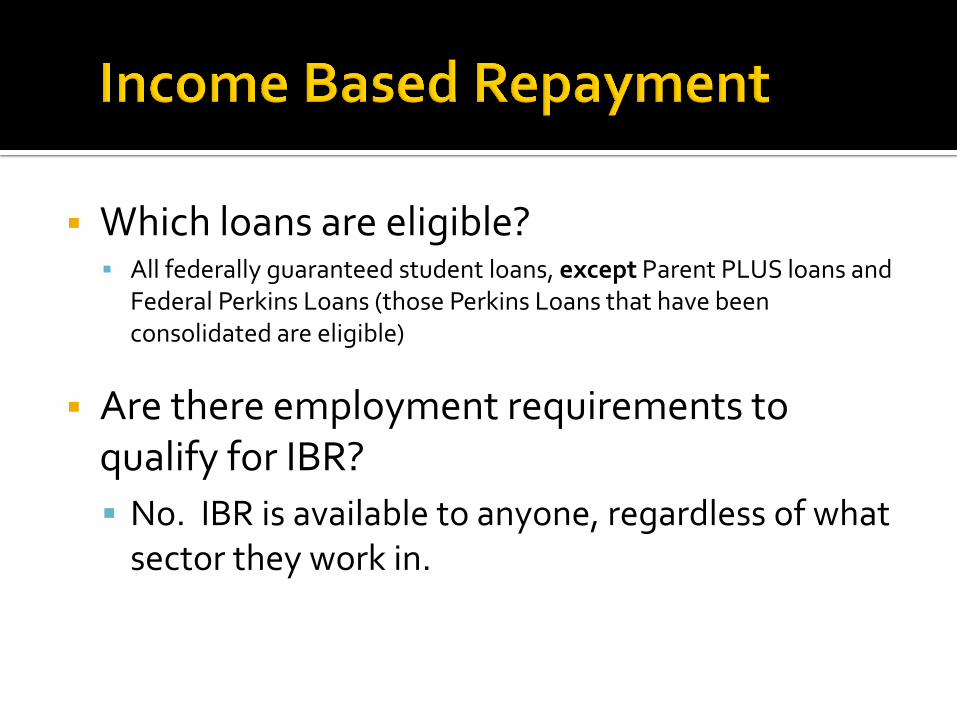

Which loans are eligible? All federally guaranteed student loans, except Parent PLUS loans and

Federal Perkins Loans (those Perkins Loans that have been consolidated are eligible)

Are there employment requirements to qualify for IBR?

No. IBR is available to anyone, regardless of what sector they work in.

AGI

IBR

Monthly Payment

(family size = 1)

ICR-A** Monthly Payment

(family size = 1)

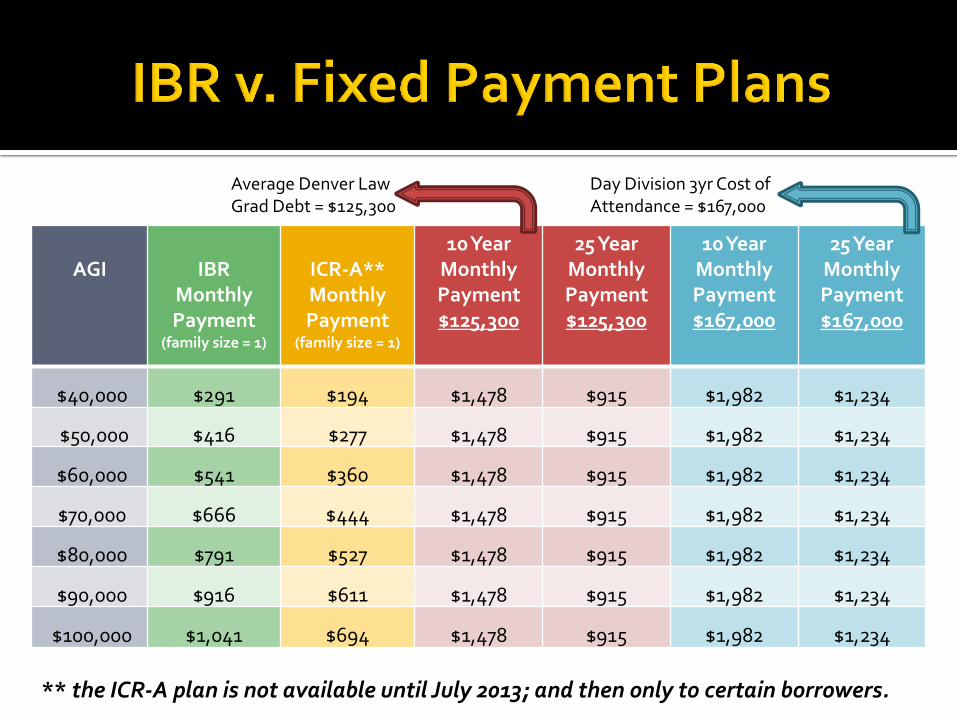

10 Year Monthly Payment $125,300

25 Year Monthly Payment $125,300

10 Year Monthly Payment $167,000

25 Year Monthly Payment $167,000

$40,000 $291 $194 $1,478 $915 $1,982 $1,234

$50,000 $416 $277 $1,478 $915 $1,982 $1,234

$60,000 $541 $360 $1,478 $915 $1,982 $1,234

$70,000 $666 $444 $1,478 $915 $1,982 $1,234

$80,000 $791 $527 $1,478 $915 $1,982 $1,234

$90,000 $916 $611 $1,478 $915 $1,982 $1,234

$100,000 $1,041 $694 $1,478 $915 $1,982 $1,234

Day Division 3yr Cost of Attendance = $167,000

Average Denver Law Grad Debt = $125,300

** the ICR-A plan is not available until July 2013; and then only to certain borrowers.

Borrowers paying under IBR may repay more, in the long run, because of accumulated interest Interest that accumulates on the loans is not capitalized,

unless a borrower exits the IBR plan If income increases significantly, IBR payment will too.

However, borrowers will never be required to pay more than the amount calculated on a Standard 10 year repayment plan, even if their IBR payment is calculated to be higher

This is not the best plan for everyone. Borrowers with higher incomes or lower debt levels may

benefit more from an extended repayment plan, especially if they are not pursuing public service employment

For married borrowers, the AGI used to calculate the monthly payment is whatever is reported to the IRS This could be significantly higher than the borrower’s income

alone A borrower can file “married filing separately” to use only

his/her income ▪ However, this may have other tax implications (increased tax rate,

limited deductions, etc.)

Under current tax laws, any amount forgiven at the end of 300 IBR payments is considered taxable income

▪ The first borrowers won’t be eligible for forgiveness until 2029, so this could change!

You have to submit documentation (typically your tax forms) to your servicer every year, to qualify for IBR

Established by the CCRAA in 2007

Individuals working full-time in public service, and repaying their eligible loans under specific repayment plans can qualify to have their remaining debt (interest and principal) forgiven after 120 payments (10 years).

What does that mean…?

What does that mean…? Working full-time

▪ The greater of: ▪ 30 or more hours per week, or ▪ whatever your employer considers full-time

▪ Can work in more than one job to meet 30 hr requirement

in public service ▪ Government (local, state, federal) ▪ Government contractors DO NOT QUALIFY

▪ Organization that is tax exempt under 501(c)(3) of the tax code

What does that mean…?

Repaying eligible loans ▪ Federal Direct Stafford loans (subsidized and unsubsidized)

▪ Federal Direct PLUS loans

▪ Federal Direct Consolidation loans

▪ Loans may be from undergrad or grad/ law school

Students who borrowed Perkins loans or loans through the bank-based FFEL program (ended in 09-10), must consolidate those loans to make them eligible for PSLF.

What does that mean…?

under specific repayment plans ▪ Standard 10-Year Plan

▪ Income Contingent Repayment Plan (ICR)

▪ Income Based Repayment Plan (IBR)

after 120 payments ▪ 120 payments do not need to be consecutive

▪ Each payment must be made while meeting all the above requirements

▪ Payments must be separate, monthly payments (i.e. paying double one month would not count as 2 payments, only 1)

You must be able to prove that you qualify for forgiveness

▪ The Dept of Ed has created an Employment Certification Form that borrowers can use to track their eligible payments:

Available at www.studentaid.ed.gov/publicservice

Can be filed annually

It is not mandatory – but we strongly recommend you use it!

▪ When you fill out the Certification Form for the first time, your eligible loans will be transferred to FedLoan Servicing (if they are currently with another servicer).

▪ FedLoan Servicing will inform you of how many qualifying payments you have made during the last year

Be sure to keep copies of everything you send in!

To qualify for forgiveness, you must also be working full-time in public service when:

▪ You apply for forgiveness ▪ Your forgiveness is granted

Amounts forgiven under PSLF do not count as taxable income

Forgiveness is only granted after 10 years of working in Public Service

▪ No partial cancellations ▪ The 10 years of service doesn’t have to be consecutive, you can take

breaks but any payments made while not employed full-time in public service sector don’t count toward 120 required for forgiveness

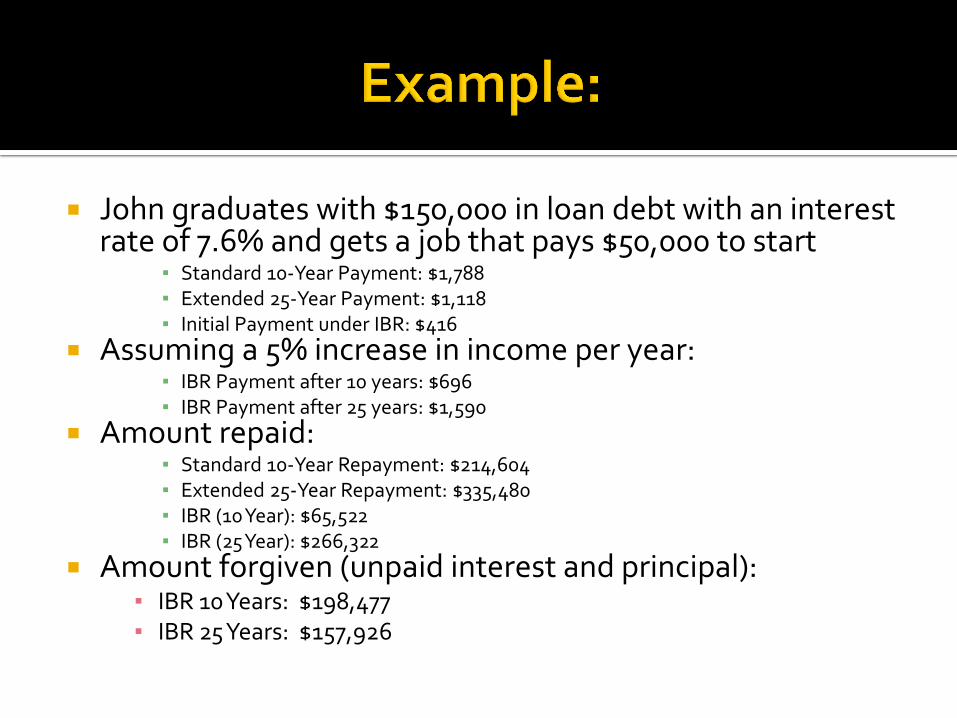

John graduates with $150,000 in loan debt with an interest rate of 7.6% and gets a job that pays $50,000 to start

▪ Standard 10-Year Payment: $1,788 ▪ Extended 25-Year Payment: $1,118 ▪ Initial Payment under IBR: $416

Assuming a 5% increase in income per year: ▪ IBR Payment after 10 years: $696 ▪ IBR Payment after 25 years: $1,590

Amount repaid: ▪ Standard 10-Year Repayment: $214,604 ▪ Extended 25-Year Repayment: $335,480 ▪ IBR (10 Year): $65,522 ▪ IBR (25 Year): $266,322

Amount forgiven (unpaid interest and principal): ▪ IBR 10 Years: $198,477 ▪ IBR 25 Years: $157,926

Make sure you have the “right” loans

Go to www.NSLDS.ed.gov

▪ Any loans labeled as “Direct…” qualify for PSLF

▪ Any loans labeled not labeled as Direct, need to be consolidated before they will qualify

▪ All loans borrowed after July 1st, 2010 are Direct loans

▪ Because many loans were sold to the Department of Education by private lenders, it is quite possible that you have eligible and non-eligible loans serviced by the same loan servicer.

Consolidate, if necessary

You can consolidate after you finish school

Go to www.LoanConsolidation.ed.gov to consolidate

Consolidation takes at least 6-8 weeks to process ▪ Once you consolidate, your grace period ends and repayment

begins ▪ May graduates should consolidate in September/October

▪ December graduates should consolidate in April/May

Sign up for Income Based Repayment Change to ICR-A, if eligible, when that plan becomes

available in July

Keep documentation of your qualifying employment

Submit the Employment Certification Form annually

You don’t sign up for PSLF, you apply for it once you have met all the requirements

Purpose: To enable and encourage committed students to accept

lower paying public interest legal positions by providing forgivable loans to help repay those students’ law school debt.

Requirements:

▪ 501(c) (3); government

▪ Must be position that utilizes grad’s legal skills

▪ AGI of $75,000 or less

▪ Graduated after May 2003

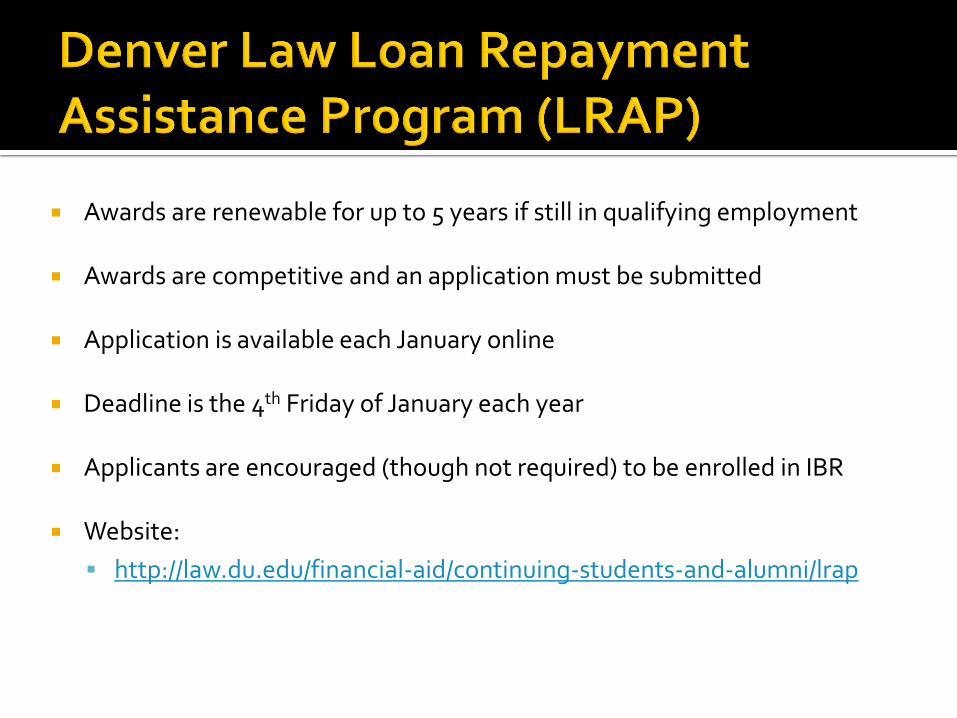

Awards are renewable for up to 5 years if still in qualifying employment

Awards are competitive and an application must be submitted

Application is available each January online

Deadline is the 4th Friday of January each year

Applicants are encouraged (though not required) to be enrolled in IBR

Website:

http://law.du.edu/financial-aid/continuing-students-and-alumni/lrap

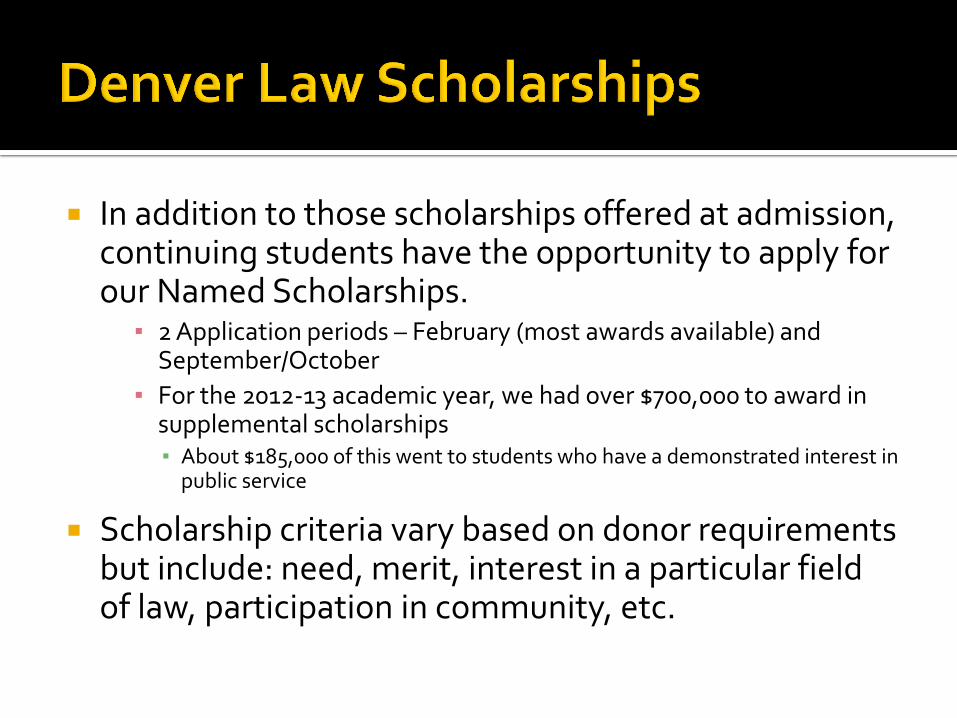

In addition to those scholarships offered at admission, continuing students have the opportunity to apply for our Named Scholarships.

▪ 2 Application periods – February (most awards available) and September/October

▪ For the 2012-13 academic year, we had over $700,000 to award in supplemental scholarships ▪ About $185,000 of this went to students who have a demonstrated interest in

public service

Scholarship criteria vary based on donor requirements but include: need, merit, interest in a particular field of law, participation in community, etc.

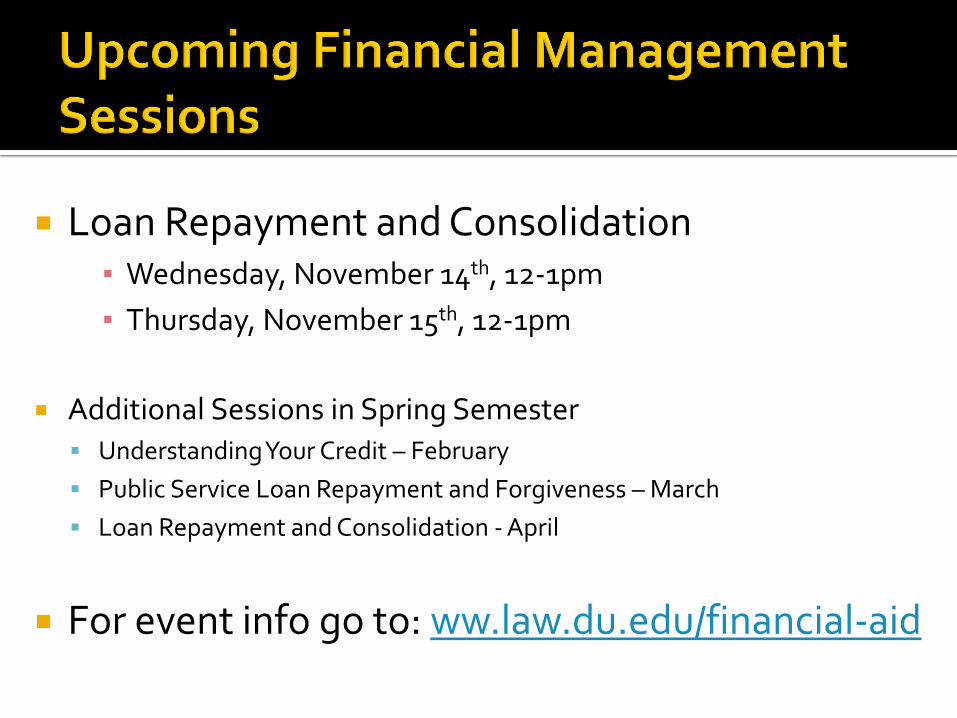

Loan Repayment and Consolidation ▪ Wednesday, November 14th, 12-1pm

▪ Thursday, November 15th, 12-1pm

Additional Sessions in Spring Semester

Understanding Your Credit – February

Public Service Loan Repayment and Forgiveness – March

Loan Repayment and Consolidation - April

For event info go to: ww.law.du.edu/financial-aid

Student Financial Management: www.law.du.edu/financial-aid Income-Based Repayment & Public Interest Forgiveness: www.ibrinfo.org www.equaljusticeworks.org www.askheatherjarvis.com www.studentaid.ed.gov/publicservice Loan Repayment Calculators: www.finaid.org/calculators www.edfund.org/loancalculator www.ibrinfo.org/calculator.php Loan Consolidation: www.loanconsolidation.ed.gov

Federal Student Loan History: www.nslds.ed.gov www.pin.ed.gov Other Websites: www.ombudsman.ed.gov/about/contactus.html http://askheatherjarvis.com/uploads/images/PSLF_QAs_final_02%2012%2010.pdf

Contact us: Email: [email protected]

Phone: 303.871.6557 Web: www.law.du.edu/financial-aid Location: Law 115

Hours: Monday – Friday, 8:00am – 4:30pm

Appointment Scheduling: Go to the “Law Student” tab in webCentral Look under the “Calendars and Announcements” section Click on “Schedule an Appointment with Law School Financial Management”