office of the auditor-general - documents...

TRANSCRIPT

REPUBLIC OF KENYA

OFFICE OF THE AUDITOR-GENERALREPORT

OF

THE AUDITOR-GENERAL

ON

THE FINANCIAL STATEMENTS OFKENYA NATIONAL SAFETY NET

PROGRAM

FOR THE YEAR ENDED P.30 JUNE 2015

MINISTRY OF LABOUR, SOCIALSECURITY AND SERVICES

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

象-う

REPUBLIC OF KENYA

Telephone: +254-20-342330 P.O. Box 30084-00100Fax: +254-20-311482 NAIROBIE-mail: [email protected]: www.kenao.go.ke

OFFICE OF THE AUDITOR-GENERALREPORT OF THE AUDITOR-GENERAL ON KENYA NATIONAL SAFETY NETPROGRAM FOR THE YEAR ENDED 30 JUNE 2015

REPORT ON THE FINANCIAL STATEMENTS

I have audited the accompanying financial statements of Kenya National Safety NetProgram set out on pages 9 to 18, which comprise the statement of assets as at30 June 2015, and the statement of consolidated receipts and payments and statementof comparative budget and actual amounts for the year then ended, and a summary ofsignificant accounting policies and other explanatory information in accordance with theprovisions of Article 229 of the Constitution of Kenya, Section 8 of the Public Audit Act,2003 and Financing Agreements Number 5287-KE between the InternationalDevelopment Association and the Government of Kenya dated 9 September, 2013. 1have obtained all the information and explanations which, to the best of my knowledgeand belief, were necessary for the purpose of the audit.

Management's Responsibility for the Financial Statements

The Principal Secretary for the Ministry of Labour, Social Security and Services isresponsible for the preparation and fair presentation of these financial statements inaccordance with International Public Sector Accounting Standards (Cash Basis) and forsuch internal control as man agement determines is necessary to enable the preparationof financial statements that are free from material misstatement, whether due to fraud orerror.

The management is also responsible for the submission of the financial statements tothe Auditor-General in accordance with the provisions of Section 7 of the Public AuditAct, 2003.

Auditor-General's Responsibility

My responsibility is to express an opinion on these financial statements based on theaudit and report in accordance with the provisions of Section 9 of the Public Audit Act,2003 and submit the audit report in compliance with Article 229 (7) of the Constitution.The audit was conducted in accordance with International Standards of Supreme AuditInstitutions (ISSAls). Those standards require compliance with ethical requirements andthat the audit be planned and performed to obtain reasonable assurance about whetherthe financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amountsand disclosures in the financial statements. The procedures selected depend on theauditor's judgement, including the assessment of the risks of material misstatement ofthe financial statements, whether due to fraud or error.

In making those risk assessments, the auditor considers internal control relevant to theentity's preparation and fair presentation of the financial statements in order to design

Kenya National Safety Net Program - Annual Report and Financial Statementsfor the year ended 30 June 2015

Promoting Accountability in the Public Sector

audit procedures that are appropriate in the circumstances, but not for the purpose ofexpressing an opinion on the effectiveness of the Program's internal control. An auditalso includes evaluating the appropriateness of accounting policies used and thereasonableness of accounting estimates made by the management, as well asevaluating the overall presentation of the financial statements.

I believe that the audit evidence obtained is sufficient and appropriate to provide a basisfor my qualified audit opinion.

Basis for Qualified Opinion

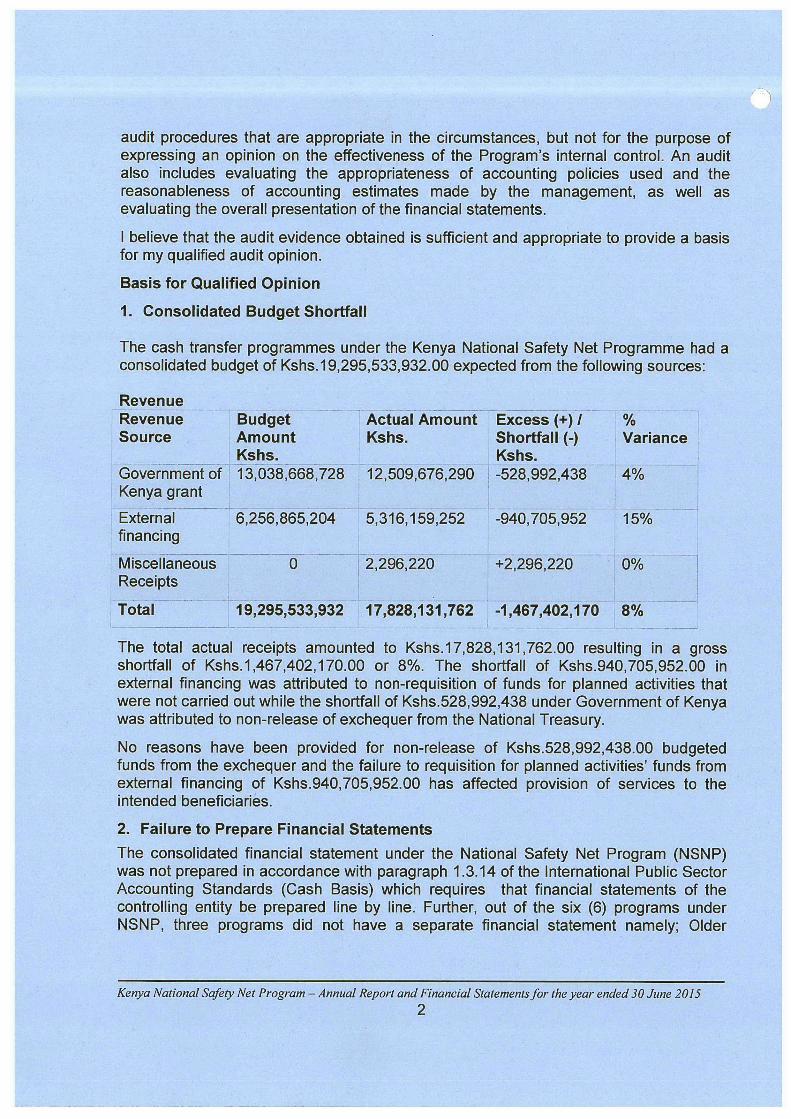

1. Consolidated Budget Shortfall

The cash transfer programmes under the Kenya National Safety Net Programme had aconsolidated budget of Kshs.19,295,533,932.00 expected from the following sources:

RevenueRevenue Budget Actual Amount Excess (+)I %Source Amount Kshs. Shortfall (-) Variance

Kshs. Kshs.Government of 13,038,668,728 12,509,676,290 -528,992,438 4%Kenya grant

External 6,256,865,204 5,316,159,252 -940,705,952 15%financing

Miscellaneous 0 2,296,220 +2,296,220 0%Receipts

Total 19,295,533,932 17,828,131,762 -1,467,402,170 i8%

The total actual receipts amounted to Kshs.17,828,131,762.00 resulting in a grossshortfall of Kshs.1,467,402,170.00 or 8%. The shortfall of Kshs.940,705,952.00 inexternal financing was attributed to non-requisition of funds for planned activities thatwere not carried out while the shortfall of Kshs.528,992,438 under Government of Kenyawas attributed to non-release of exchequer from the National Treasury.

No reasons have been provided for non-release of Kshs.528,992,438.00 budgetedfunds from the exchequer and the failure to requisition for planned activities' funds fromexternal financing of Kshs.940,705,952.00 has affected provision of services to theintended beneficiaries.

2. Failure to Prepare Financial Statements

The consolidated financial statement under the National Safety Net Program (NSNP)was not prepared in accordance with paragraph 1.3.14 of the International Public SectorAccounting Standards (Cash Basis) which requires that financial statements of thecontrolling entity be prepared line by line. Further, out of the six (6) programs underNSNP, three programs did not have a separate financial statement namely; Older

Kenya National Safety Net Program - Annual Report and Financial Statements for the year ended 30 June 20152

Persons Cash Transfer Program, Hunger Safety Net Program and the Social ProtectionSecretariat as is required under paragraph 1.4.23 of IPSAS (Cash Basis).

In the circumstances, it has not been possible to confirm the accuracy of the figuresconsolidated in the Kenya National Safety Net Program as at 30 June 2015.

3. Cash Disbursements

i) Payments to Beneficiaries through Kenya Commercial Bank

Reconciliations received from the service provider - Kenya Commercial Bank withregard to cash disbursements to beneficiaries reflect amounts totallingKshs.462,268,000.00 as refunds due to the Ministry of Labour from undisbursed cashfor Orphans and Vulnerable Children(OVC), Older Persons Cash Transfer (OPCT), andPersons with Severe Disability ( PWSD ) for the period January 2015 to April 2015. Theamount of Kshs.462,268,000.00 was refunded on 9 July 2015, two months after thestipulated due date set for refunds.

However, no interest was shown as having accrued from Kshs.462,268,000.00 held fortwo months by the bank.

ii) Payments to Beneficiaries through Postal Corporation of Kenya

During the financial year ended 30 June 2015 the Ministry of Labour remitted a total ofKshs.1,968,000,000.00 to Postal Corporation of Kenya for onward payment tobeneficiaries under the Older Persons Cash Transfer Programme. However, noreconciliation was done showing the total payments to the beneficiaries and the refundsmade to the Ministry as required in the mutual agreement between the Ministry andPostal Corporation of Kenya.

In the absence of the required reconciliations, the status of Kshs.1,968,000,000 remittedto Postal Corporation of Kenya and the payments therein could not be established.

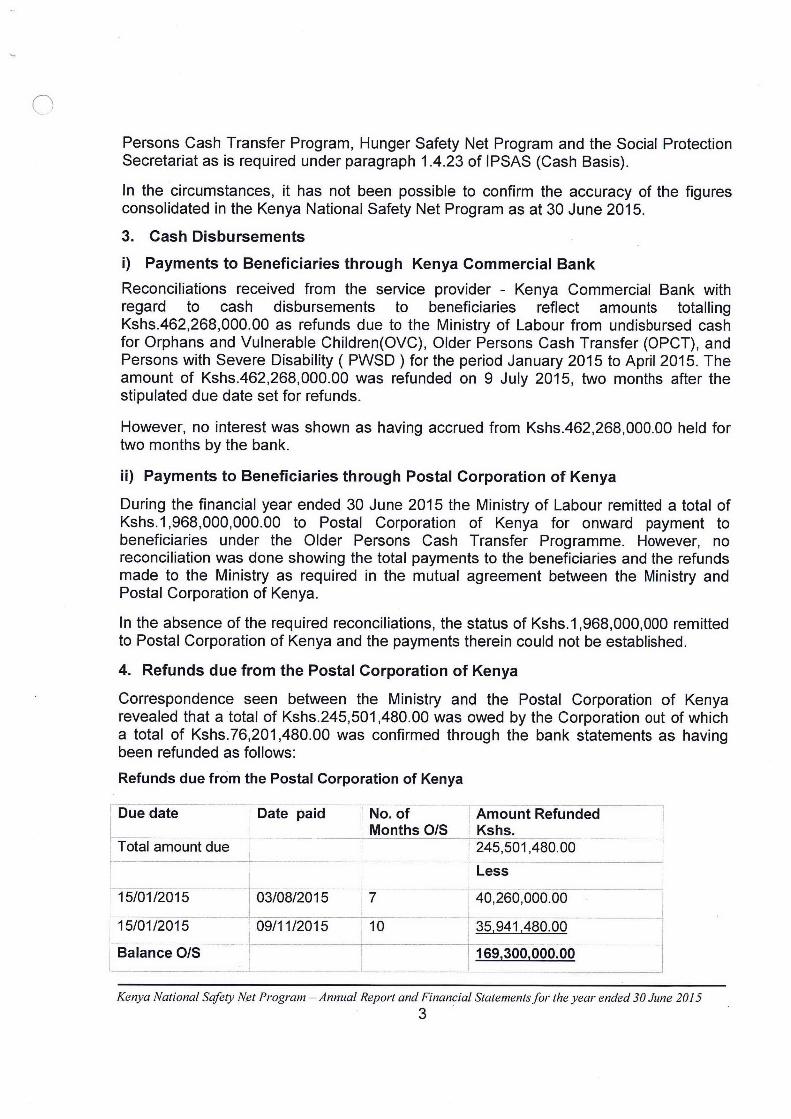

4. Refunds due from the Postal Corporation of Kenya

Correspondence seen between the Ministry and the Postal Corporation of Kenyarevealed that a total of Kshs.245,501,480.00 was owed by the Corporation out of whicha total of Kshs.76,201,480.00 was confirmed through the bank statements as havingbeen refunded as follows:

Refunds due from the Postal Corporation of Kenya

Due date Date paid No. of Amount RefundedMonths O/S Kshs.

Total amount due 245,501,480.00Less

15/01/2015 03/08/2015 7 40,260,000.00

15/01/2015 09/11/2015 10 35,941,480.00

Balance O/S 169,300,000.00

Kenya National Safety Net Program - Annual Report and Financial Statements for the year ended 30 June 20153

No explanation was given as to why the outstanding balance of Kshs.169,300,000.00had not been refunded by the stipulated due date of 15th day of the month following theclose of the pay period.

Further, no interest appears to have accrued on the amount of Kshs.40,260,000.00refunded six months after the September/December payment cycle as well as on theKshs.35,941,480.00 refunded ten months after the September/December payment cycleas tabulated above.

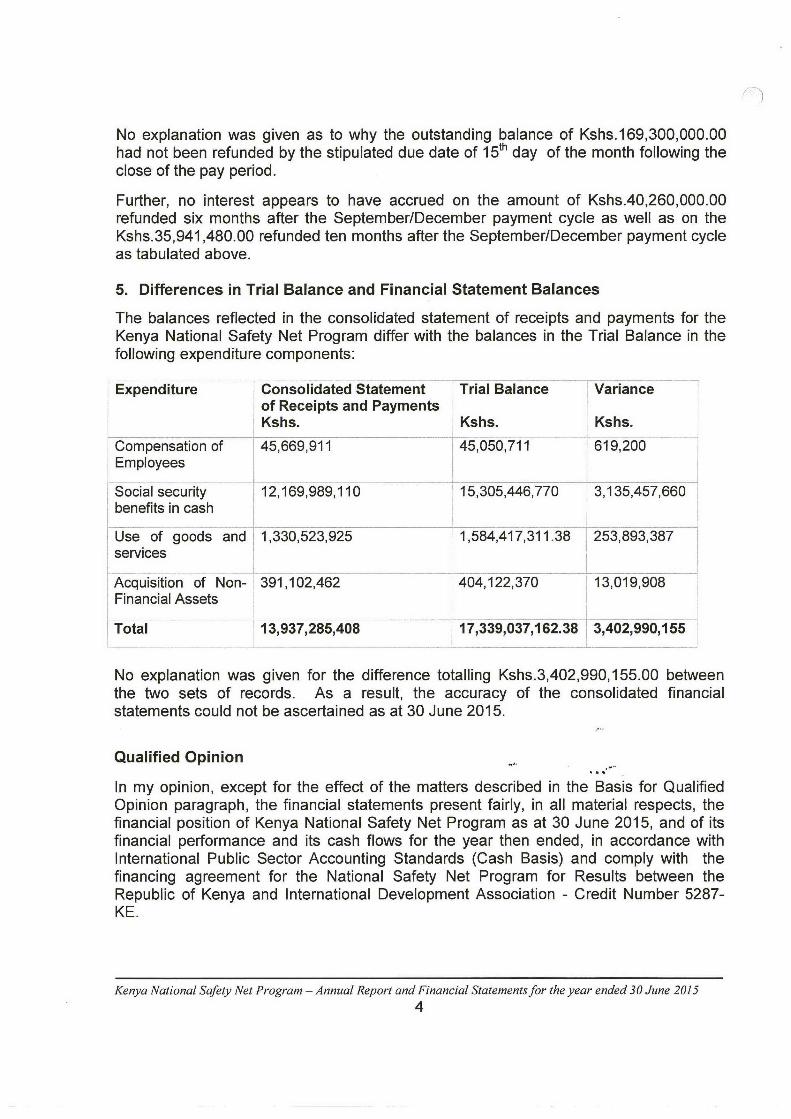

5. Differences in Trial Balance and Financial Statement Balances

The balances reflected in the consolidated statement of receipts and payments for theKenya National Safety Net Program differ with the balances in the Trial Balance in thefollowing expenditure components:

Expenditure Consolidated Statement Trial Balance Varianceof Receipts and PaymentsKshs. Kshs. Kshs.

Compensation of 45,669,911 45,050,711 619,200Employees

Social security 12,169,989,110 15,305,446,770 3,135,457,660benefits in cash

Use of goods and 1,330,523,925 1,584,417,311.38 253,893,387services

Acquisition of Non- 391,102,462 404,122,370 13,019,908Financial Assets

Total 13,937,285,408 17,339,037,162.38 3,402,990,155

No explanation was given for the difference totalling Kshs.3,402,990,155.00 betweenthe two sets of records. As a result, the accuracy of the consolidated financialstatements could not be ascertained as at 30 June 2015.

Qualified Opinion

In my opinion, except for the effect of the matters described in the Basis for QualifiedOpinion paragraph, the financial statements present fairly, in all material respects, thefinancial position of Kenya National Safety Net Program as at 30 June 2015, and of itsfinancial performance and its cash flows for the year then ended, in accordance withInternational Public Sector Accounting Standards (Cash Basis) and comply with thefinancing agreement for the National Safety Net Program for Results between theRepublic of Kenya and International Development Association - Credit Number 5287-KE.

Kenya National Safety Net Program - Annual Report and Financial Statements for the year ended 30 June 2015

4

Other Matter

1. Failure to Absorb Funds

The total budgeted transfer of funds to beneficiaries was Kshs.19,295,533,932.However, the actual cash transfer during the year was Kshs.13,945,805, 684 (72.3%) ofthe total project budget receipts. The Program was not able to absorbKshs.3,882,326,078 (32%) of the actual receipts.

No explanation has been provided for failure to utilize the funds received to meet theneed of the given number of beneficiaries in the country.

2. DFID Transfers to Beneficiaries

The consolidated statement of receipts and payments reflects Kshs.3,441,798,502.00 astransfers to the beneficiaries from DFID grant under the Hunger Safety Net Program forthe year ended 30 June 2015. However, records made available indicate thatKshs.3,637,558,730.00 was initially budgeted for transfer to the beneficiaries from DFIDresulting in a difference of Kshs.195,760,228.00.

The difference of Kshs.195,760,228.00 between the budgeted and the amount actuallytransferred was attributed to failure to reach the targeted number of beneficiaries thatwas set at the beginning of the financial year due to lack of National Identity Cards (IDs)to enable the potential beneficiaries open bank accounts. As a result, intendedbeneficiaries are left suffering while project funds remain unutilized.

3. Verification of Beneficiary Disbursements

The sampled audit reports for specific projects under the Program revealed that cashdisbursements to the enlisted beneficiaries were not utilized in accordance with theprogram objectives. Consequently, there is need for extensive in-depth verification of thebeneficiary cash disbursements.

My opinion is however not qualified in respect to these matters.

FCPA Edward R. 0. Ouko, CBSAUDITOR-GENERAL

Nairobi

23 February 2016

Kenya National Safety Net Program - Annual Report and Financial Statements for the year ended 30 June 20155