oil and gas industry trends ektinteractive

TRANSCRIPT

Industry Trends

INDUSTRY TRENDS

2

Introduction to Oil & Gas

Industry Trends

Copyright © 2013 EKT Interactive, Inc.

All Rights Reserved

Feel free to email, tweet, blog, and pass this eBook around the web… but please

don’t alter any of its contents when you do. Thanks.

EKTInteractive.com

INDUSTRY TRENDS

3

Learning Objectives

We have put these e-books together to give basic background on oil & gas to

professionals who are new to the industry or those interested in pursuing a

career in oil & gas. They have been developed by senior industry

professionals with decades of experience.

Upon completing the Industry Trends Lesson, participants will be able to:

Explain why OPEC has limited ability to dampen price spikes by producing

more.

Define Reserves-to-Production Ratio, and contrast the value of this metric in

the Middle East with the U.S.

Explain why the oil and gas industry may need to be renamed the Gas and

Oil industry in the future.

Explain why the oil and gas industry needs to invest massive amounts of capital in the coming years.

Explain why upstream and downstream construction costs have begun to rise dramatically.

List some of the key challenges facing the oil and gas industry in hiring staff to replace retiring employees.

Describe the two leading approaches for limiting CO2 emissions.

Contrast the concepts of independence with interdependence.

INDUSTRY TRENDS

4

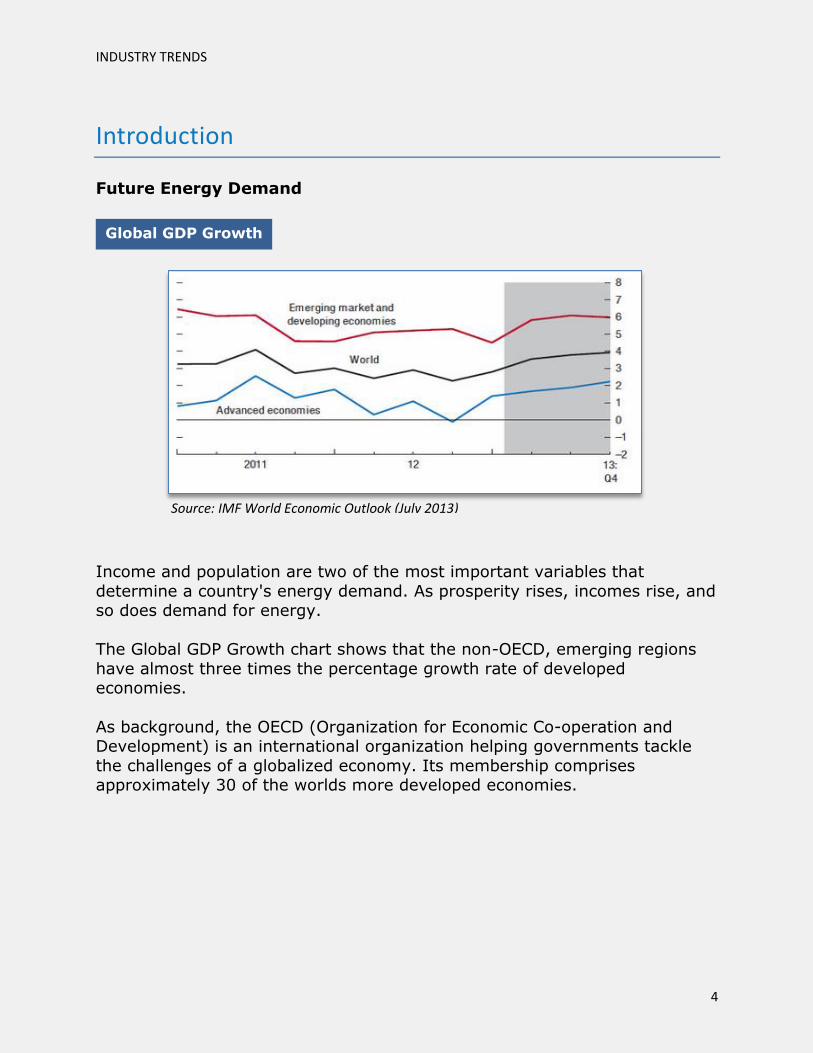

Introduction

Future Energy Demand

Income and population are two of the most important variables that

determine a country's energy demand. As prosperity rises, incomes rise, and so does demand for energy.

The Global GDP Growth chart shows that the non-OECD, emerging regions

have almost three times the percentage growth rate of developed economies.

As background, the OECD (Organization for Economic Co-operation and Development) is an international organization helping governments tackle

the challenges of a globalized economy. Its membership comprises approximately 30 of the worlds more developed economies.

GlobalGDPGrowth

Source:IMFWorldEconomicOutlook(July2013)

Global GDP Growth

Source: IMF World Economic Outlook (July 2013)

INDUSTRY TRENDS

5

“In 2005, Non-OECD and OECD energy demand was about equal, but by 2040, Non OECD demand will be nearly double that of the OECD.”

This projection has numerous geopolitical implications, as well as oil and gas

supply demand implications.

For example, while China garners most headline attention, the Middle East as a whole has a similar demand size and growth pattern. These economies

continue to invest recent oil revenue windfalls in massive infrastructure projects.

Global Energy Demand Growth

Non OCED energy demand

Quadrillion BTUs

GlobalEnergyDemandGrowth

Source:ExxonMobilEnergyDataCenter

OCED energy demand

Quadrillion BTUs

GlobalEnergyDemandGrowth

Source:ExxonMobilEnergyDataCenter

Non OCED energy demand

Quadrillion BTUs

Source: ExxonMobil Energy Data Center

INDUSTRY TRENDS

6

The Peak Oil Debate

The Peak Oil Debate includes these topics:

Current peak oil definition

Crude oil spare capacity Oil reserves-to-production ratio

Natural gas reserves-to-production ratios Abundance of natural gas

Even with recent growth in renewable energy sources, the demand growth

for oil seems to be inevitable. At the same time, experts estimate that oilfield decline rates are somewhere around 4.5% per year for conventional

production.

This fact has led to one the most widely debated topics in the oil and gas industry today, the concept of Peak Oil. At its core, Peak Oil concerns the

decline rate of producing existing (conventional) oil fields.

It is worth noting that 80% of the world’s oil production comes from fields

discovered before 1970, the vast majority of which now have steep decline curves.

In 1956, nobody believed M. King Hubbert, a Shell Oil Company geologist,

when he predicted that the U.S. oil production would peak by 1970. At that time the U.S. was the king of oil, producing more oil than any other country

in the world. Right on Mr. Hubbert’s schedule, in 1970, the U.S. peaked in oil production.

If Peak Oil proves to be true, future global oil production could be much less

than it is today. Prior to the boom in domestic shale production, the U.S. production had peaked in the lower 48 states in 1970. Within 20 years, U.S.

production had fallen by over 40%.

INDUSTRY TRENDS

7

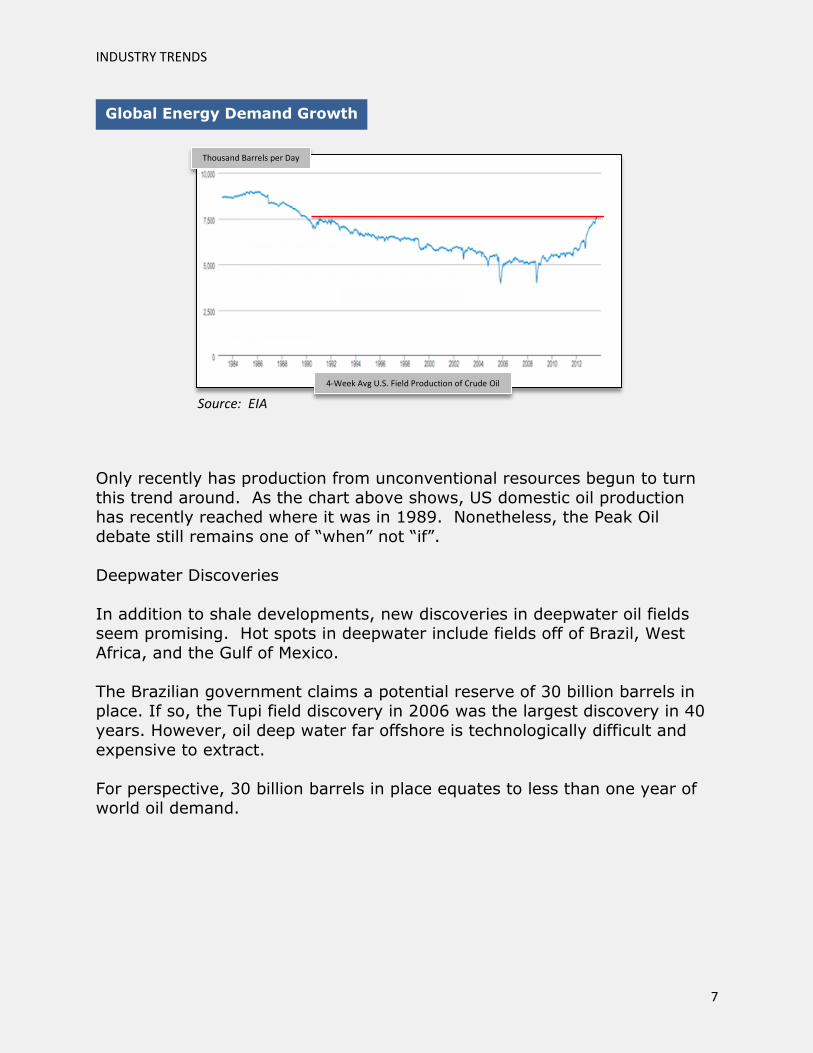

Only recently has production from unconventional resources begun to turn

this trend around. As the chart above shows, US domestic oil production has recently reached where it was in 1989. Nonetheless, the Peak Oil

debate still remains one of “when” not “if”.

Deepwater Discoveries

In addition to shale developments, new discoveries in deepwater oil fields seem promising. Hot spots in deepwater include fields off of Brazil, West

Africa, and the Gulf of Mexico.

The Brazilian government claims a potential reserve of 30 billion barrels in place. If so, the Tupi field discovery in 2006 was the largest discovery in 40

years. However, oil deep water far offshore is technologically difficult and

expensive to extract.

For perspective, 30 billion barrels in place equates to less than one year of world oil demand.

Global Energy Demand Growth

USOilfieldProduc on

Source:IMFWorldEconomicOutlook(July2013)

Source:EIA

4-Week Avg U.S. Field Production of Crude Oil

Thousand Barrels per Day

Source: EIA

INDUSTRY TRENDS

8

Source: EIA

Global Crude Oil Spare Capacity

One key barometer causing price spikes and supply turbulence in oil markets

is the OPEC’s spare crude oil production capacity. OPEC has continuous crude oil output capacity of around 30 million barrels per day, approximately

40% of the world’s demand for oil.

As the Spare Production Capacity chart shows, OPEC spare capacity and prices are inversely related, and current spare capacity is around 4-5 million

barrels per day. In the mid-1980s, OPEC had approximately 10 to 15 million

barrels per day of spare capacity which allowed them, especially Saudi Arabia, to dampen price spikes by bringing more oil to the market.

Although spare capacity is at its lower boundary, it is on the rise. OPEC

members have substantial investments underway to ensure secure oil supplies. Production capacity of natural gas liquids (NGL) and other liquids

available for transportation fuels also will be expanded significantly in the future.

Neither the Peak Oil discussion nor OPEC spare capacity calculations consider

increased availability of NGLs.

Spare Production Capacity and Prices SpareProcuc onCapacityandPrices

Source:EIA

INDUSTRY TRENDS

9

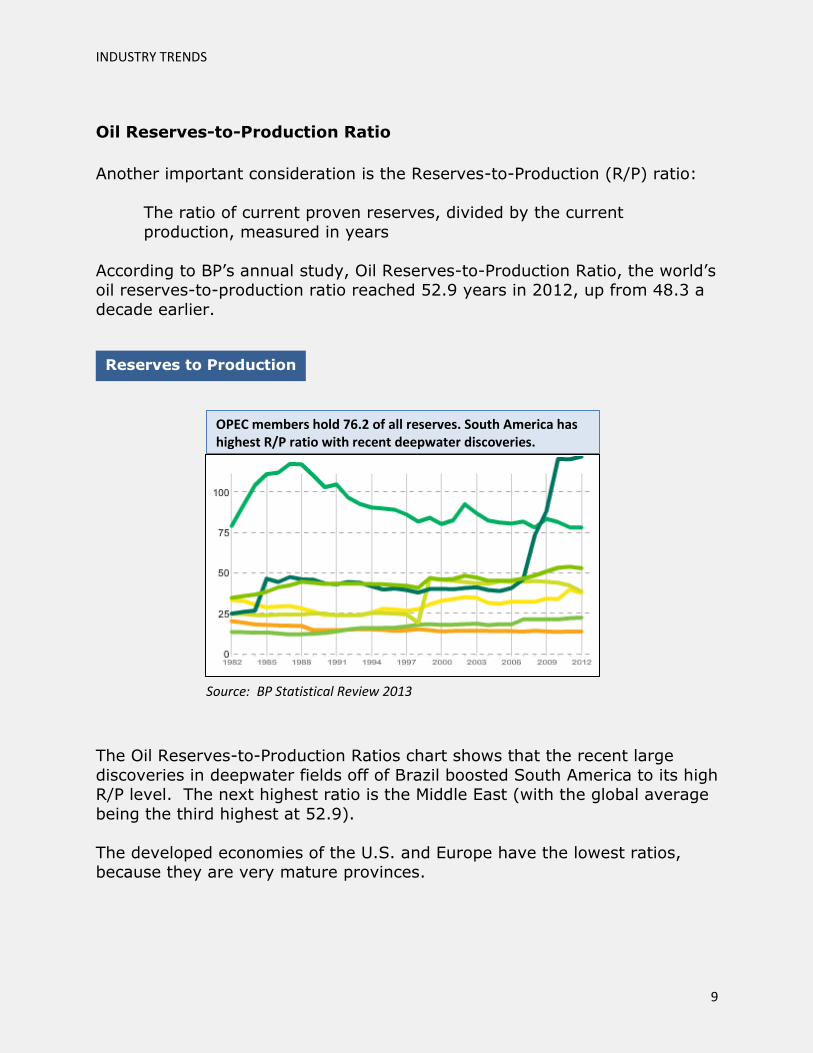

Source: BP Statistical Review 2013

Oil Reserves-to-Production Ratio

Another important consideration is the Reserves-to-Production (R/P) ratio:

The ratio of current proven reserves, divided by the current

production, measured in years

According to BP’s annual study, Oil Reserves-to-Production Ratio, the world’s oil reserves-to-production ratio reached 52.9 years in 2012, up from 48.3 a

decade earlier.

The Oil Reserves-to-Production Ratios chart shows that the recent large

discoveries in deepwater fields off of Brazil boosted South America to its high R/P level. The next highest ratio is the Middle East (with the global average

being the third highest at 52.9).

The developed economies of the U.S. and Europe have the lowest ratios, because they are very mature provinces.

Reserves to Production

OPEC members hold 76.2 of all reserves. South America has highest R/P ratio with recent deepwater discoveries.

INDUSTRY TRENDS

10

Source: Watts, P.: “Building Bridges – Fulfilling the Potential for Gas in the 21st Century,” speech – World Gas Conference, Tokyo, Japan, 060303.

Natural Gas Reserves-to-Production Ratios

The world’s natural gas R/P ratio is 55.7 (BP, 2012) years with global

reserves standing at 187.3 trillion cubic meters.

Europe/Eurasia and the Middle East combine to hold over 75% of the worlds proven natural gas reserves.

Recent developments in unconventional drilling have led the oil R/P Ratio to

gain ground on the natural gas R/P.

Industry Future – More Gas Than Oil

Energy experts agree that the fuel of choice in the 21st century will be natural gas, primarily because it is the cleanest burning of all the fossil fuels.

When it is burned, natural gas emits a great deal of energy. Natural gas is also abundant, easy to transport, and ideal for home and industrial heat

applications and generating electricity.

Industry Future – More Gas than Oil

Pace of moving to gas will increase as oil gets harder to find and produce…

INDUSTRY TRENDS

11

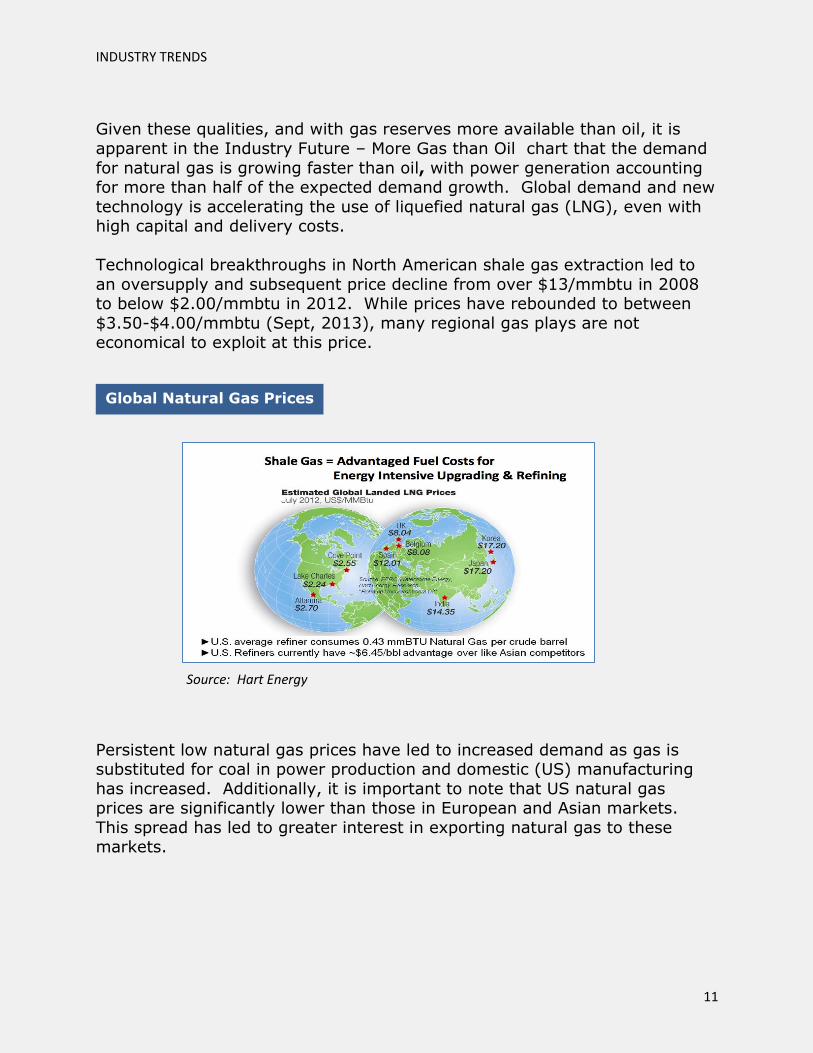

GlobalNaturalGasPrices

Source:HartEnergySource: Hart Energy

Given these qualities, and with gas reserves more available than oil, it is

apparent in the Industry Future – More Gas than Oil chart that the demand

for natural gas is growing faster than oil, with power generation accounting for more than half of the expected demand growth. Global demand and new

technology is accelerating the use of liquefied natural gas (LNG), even with high capital and delivery costs.

Technological breakthroughs in North American shale gas extraction led to

an oversupply and subsequent price decline from over $13/mmbtu in 2008 to below $2.00/mmbtu in 2012. While prices have rebounded to between

$3.50-$4.00/mmbtu (Sept, 2013), many regional gas plays are not economical to exploit at this price.

Persistent low natural gas prices have led to increased demand as gas is substituted for coal in power production and domestic (US) manufacturing

has increased. Additionally, it is important to note that US natural gas prices are significantly lower than those in European and Asian markets.

This spread has led to greater interest in exporting natural gas to these markets.

Global Natural Gas Prices

INDUSTRY TRENDS

12

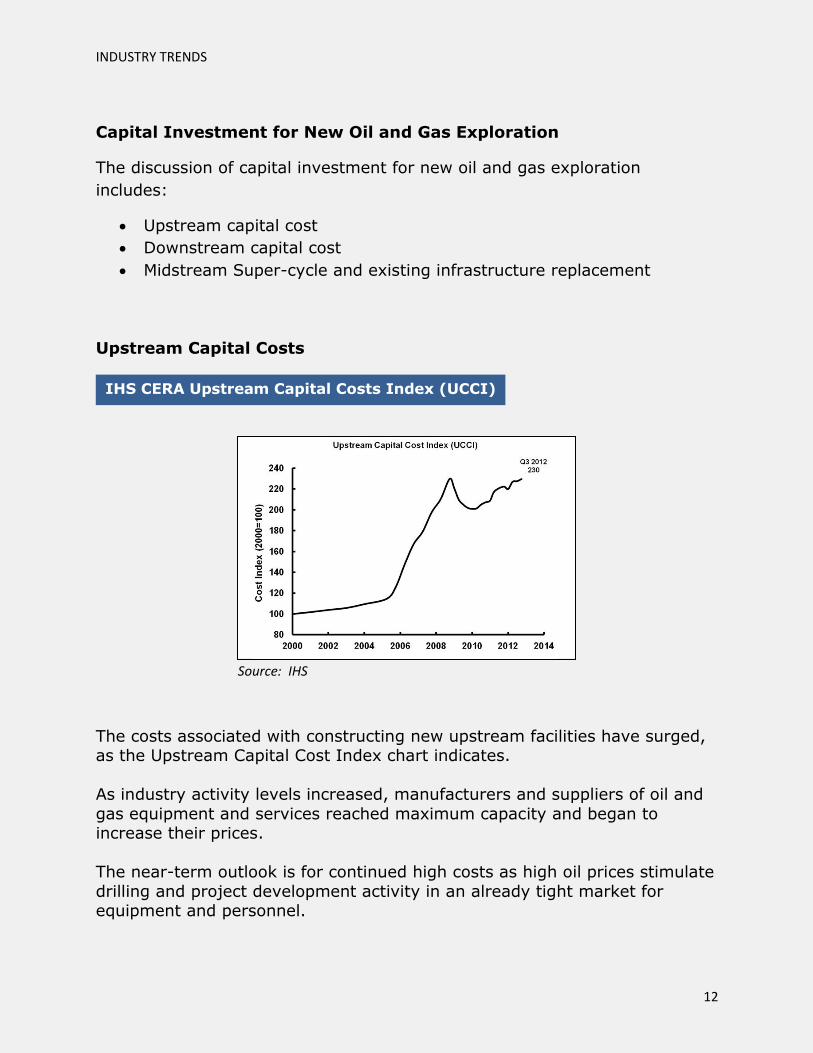

IHSCERAUpstreamCapitalCostsIndex(UCCI)

Source:IHS

Capital Investment for New Oil and Gas Exploration

The discussion of capital investment for new oil and gas exploration

includes:

Upstream capital cost

Downstream capital cost

Midstream Super-cycle and existing infrastructure replacement

Upstream Capital Costs

The costs associated with constructing new upstream facilities have surged, as the Upstream Capital Cost Index chart indicates.

As industry activity levels increased, manufacturers and suppliers of oil and

gas equipment and services reached maximum capacity and began to increase their prices.

The near-term outlook is for continued high costs as high oil prices stimulate

drilling and project development activity in an already tight market for equipment and personnel.

IHS CERA Upstream Capital Costs Index (UCCI)

Source: IHS

INDUSTRY TRENDS

13

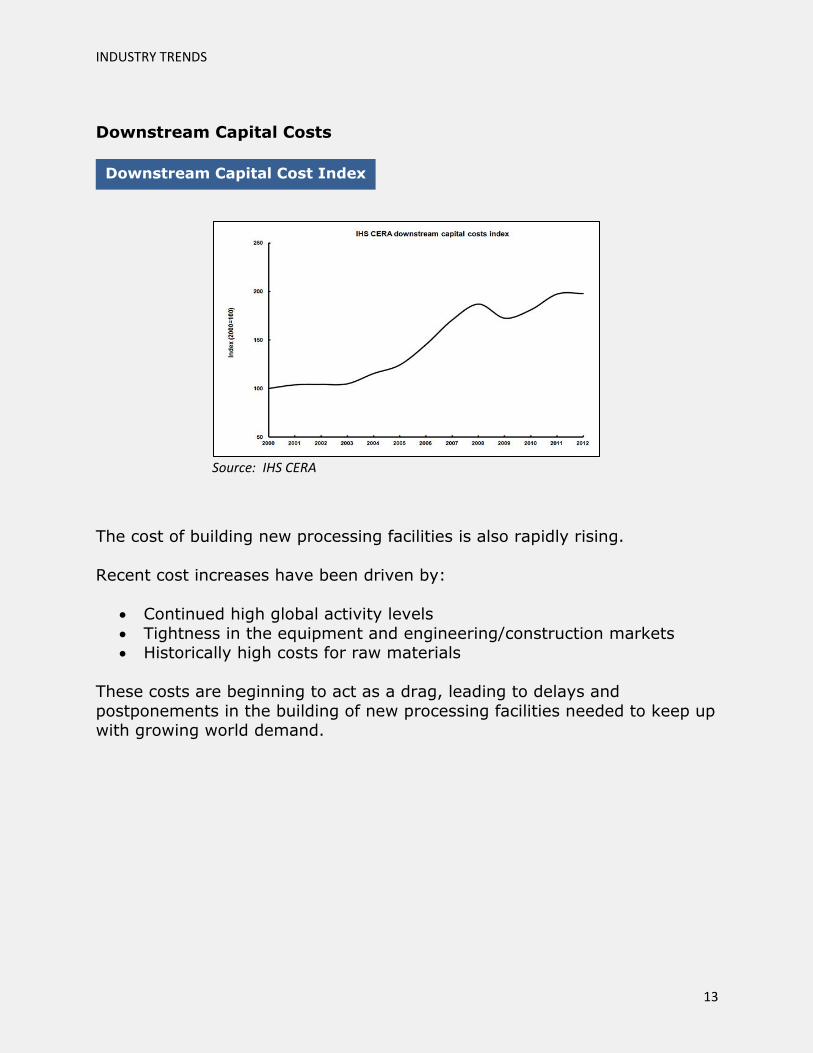

DownstreamCapitalCostIndex

Source:IHSCERA

Downstream Capital Costs

The cost of building new processing facilities is also rapidly rising.

Recent cost increases have been driven by:

Continued high global activity levels

Tightness in the equipment and engineering/construction markets Historically high costs for raw materials

These costs are beginning to act as a drag, leading to delays and

postponements in the building of new processing facilities needed to keep up with growing world demand.

Downstream Capital Cost Index

Source: IHS CERA

INDUSTRY TRENDS

14

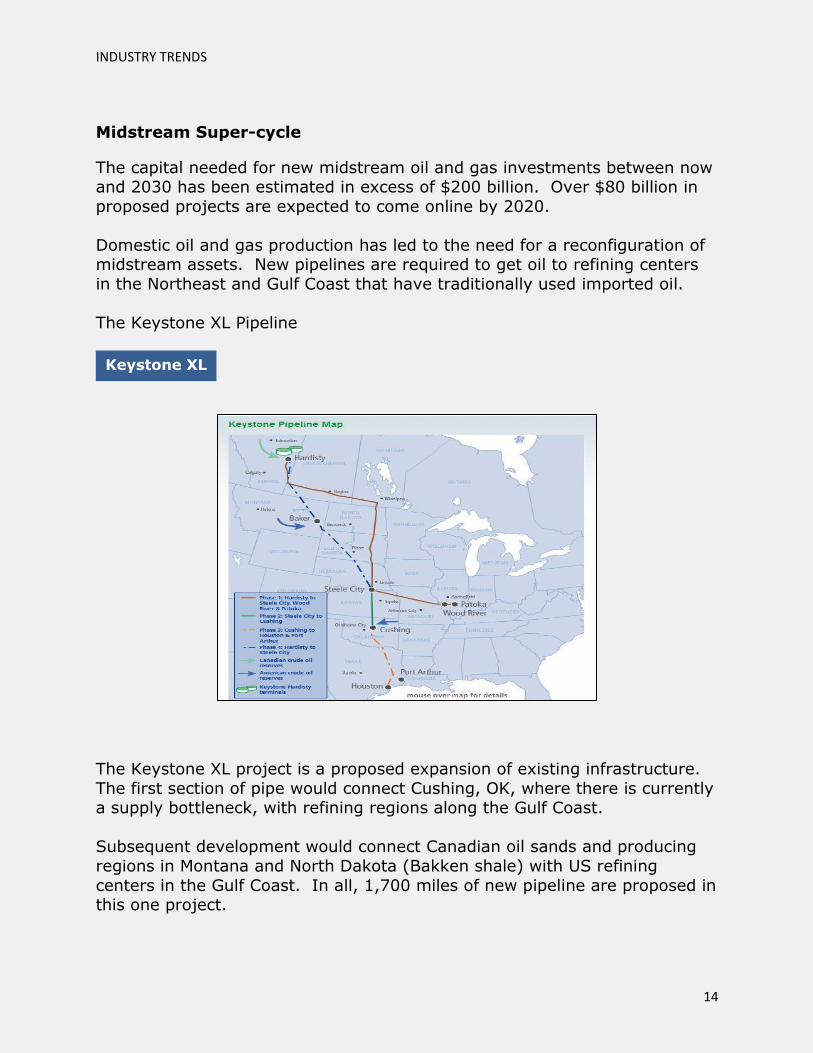

Midstream Super-cycle

The capital needed for new midstream oil and gas investments between now and 2030 has been estimated in excess of $200 billion. Over $80 billion in

proposed projects are expected to come online by 2020.

Domestic oil and gas production has led to the need for a reconfiguration of midstream assets. New pipelines are required to get oil to refining centers

in the Northeast and Gulf Coast that have traditionally used imported oil.

The Keystone XL Pipeline

The Keystone XL project is a proposed expansion of existing infrastructure.

The first section of pipe would connect Cushing, OK, where there is currently a supply bottleneck, with refining regions along the Gulf Coast.

Subsequent development would connect Canadian oil sands and producing

regions in Montana and North Dakota (Bakken shale) with US refining

centers in the Gulf Coast. In all, 1,700 miles of new pipeline are proposed in this one project.

KeystoneXLKeystone XL

INDUSTRY TRENDS

15

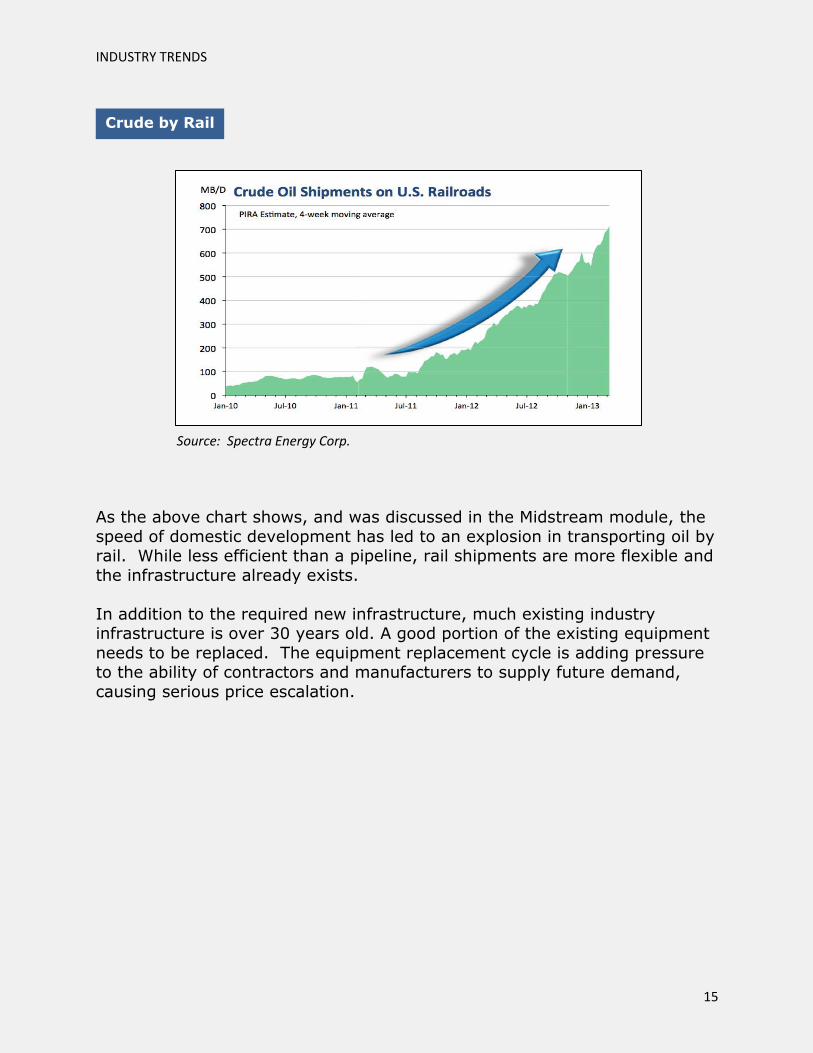

As the above chart shows, and was discussed in the Midstream module, the

speed of domestic development has led to an explosion in transporting oil by rail. While less efficient than a pipeline, rail shipments are more flexible and

the infrastructure already exists.

In addition to the required new infrastructure, much existing industry infrastructure is over 30 years old. A good portion of the existing equipment

needs to be replaced. The equipment replacement cycle is adding pressure to the ability of contractors and manufacturers to supply future demand,

causing serious price escalation.

CrudebyRailCrude by Rail

Source: Spectra Energy Corp.

INDUSTRY TRENDS

16

The Effect of Emissions Growth in the Developing World

The topic of emissions includes:

Increase in emissions in developed countries Efforts to control carbon growth

A call for interdependence

Energy demand growth is accelerating in the developing world, and CO2

emissions follow. In addition, the energy mix in these geographies includes a higher concentration of fossil fuels, especially coal.

The U.S. and China together account for approximately 40% of the world's

total CO2 emissions. This statistic points to a global issue, requiring global solutions.

The scale and complexity of the challenge to meaningfully reduce carbon

emissions is daunting.

In 2012, U.S. energy related carbon emissions declined to 5.3 billion tons of CO2., the lowest since 1994. The dominant reason for this was a decreased

use of coal in power generation due to persistently low natural gas prices.

Power generated from coal accounts for approximately 44% of all generation

capacity in the US. Yet coal plants account for 74% of CO2 emissions from domestic electricity generation activities.

GlobalCO2ChangeSince1990

Change in Global CO2 Emissions Relative to 1990

INDUSTRY TRENDS

17

Other factors included lower demand for transportation fuels and mild winter

temperatures.

Limiting Carbon Growth

Another challenge is the shifting political debate. No longer is the argument

about whether or not the world is warming, and whether or not it is a problem. The political arena is convinced that it is.

The global warming culprit is also considered to be carbon dioxide, although

there is still raging scientific debate on the topic. Be that as it may, two approaches have been considered to limit carbon:

When a carbon tax is considered, industrial sources of carbon dioxide are required to pay a tax for every ton of pollution they emit. The

challenge is to determine a standard for emissions that are taxable and how to guarantee payment of the tax. Then, the governing body

must figure out who pays the tax and what to do with the revenue. This solution proved to be politically unviable.

Under a cap-and-trade program, the government sets an overall

emissions cap and allows companies to buy and sell emission permits. The U.S. implemented a cap-and-trade system to control acid rain

pollution (The Acid Rain Program) and achieved greater reductions at lower costs than anyone anticipated.

The U.S. is behind the European Union (EU) in implementing carbon

mitigation systems. The EU has had a carbon cap-and-trade program in

place since 2005, with mixed (but improving) results.

Some cap-and-trade programs in effect in the US include:

The Clean Air Interstate Rule Clean Air Visibility Rule

The Acid Rain Program The NOX Budget Trading Program

RGGI – Northeast and Mid-Atlantic RECLAIM – South Coast Air Basin

Assembly Bill 32 - California HRVOC – Texas (Houston, Galveston, Brazoria)

Emissions Reduction Market System - Illinois

INDUSTRY TRENDS

18

Talent Storage Challenge

Interdependence as a Solution

Recent developments in domestic energy production have started the

rallying cries for energy independence. In reality, the complexity and global nature of our energy markets will always require a mindset of

interdependence. An independent attitude and policy environment implies self-sufficiency while interdependence is more dynamic, requiring mutual

responsibility to and a shared set of principles with others.

In global energy, consuming countries need the hydrocarbons to fuel their growing economies and populations. Producing countries need an outlet for

their hydrocarbon resources.

There are very few countries that are energy self-sufficient; therefore, the complex global energy system of facilities and people needs to work even

more closely to meet the future challenges.

Talent Gap

The oil industry experienced a hiring surge in the late 1970s and early 1980s, followed by an extended period of decline.

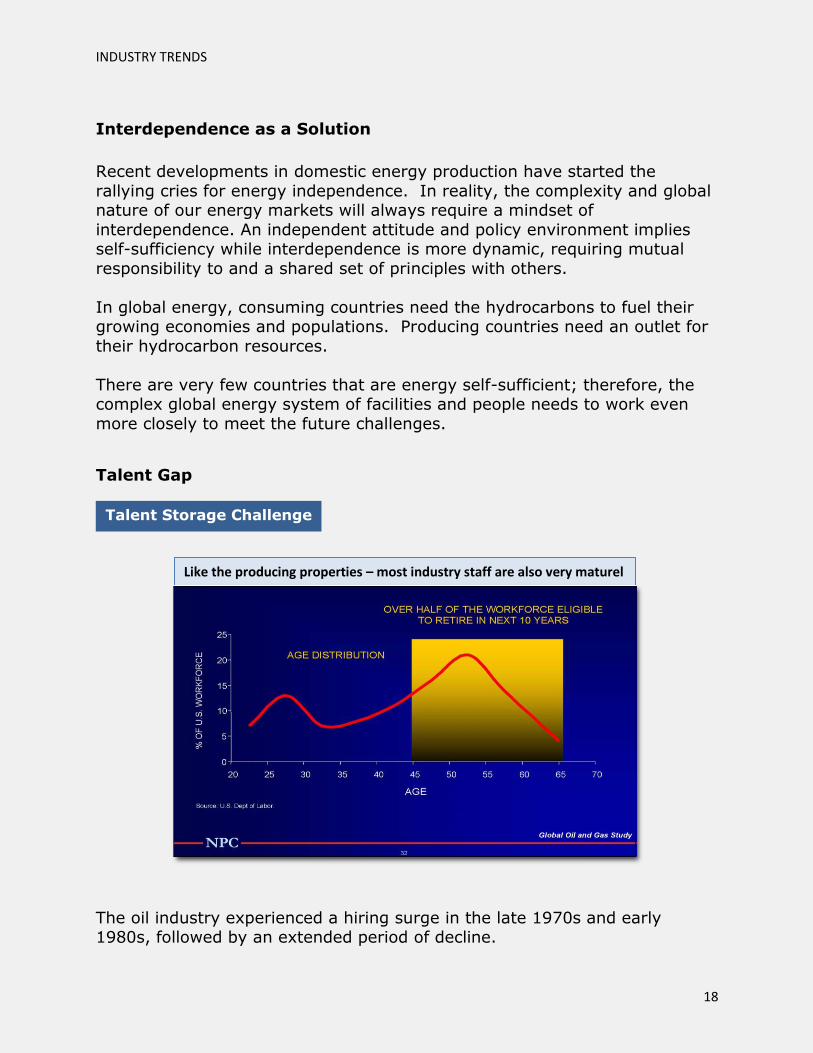

Like the producing properties – most industry staff are also very maturel

Talent Shortage Challenge

17

Like the producing properties – most industry staff are also very mature!

INDUSTRY TRENDS

19

New talent has not made up for decades of depressed hiring activity. As a

result, over half of today's U.S. workforce is eligible for retirement within the

next 10 years, often referred to as "the big crew change."

A 2008 survey by Ernst and Young and Rice University confirmed the extent of the struggle that oil and gas companies have in recruiting, training, and

developing a sufficient number of staff:

Nearly 90% of the senior executives interviewed at 22 top international oil and gas companies called the talent shortage one of

the top five issues facing their companies.

More than half the executives surveyed feel the talent void could hurt corporate growth as a result of an inability to staff projects.

Nearly three quarters agreed that the need for training has increased due to

changing workforce demographics.

More recently, a study performed by Schlumberger Business Consulting

(2011) highlighted a loss of 5,000 experienced petrotechnical professionals by 2014. Universities have succeeded in ramping up graduates in petroleum

engineering and geosciences. However, over 70% of these graduates come from Asia and Russia CIS which will require a global mindset in recruitment

of talent.

INDUSTRY TRENDS

20

Summary

For the first time in history, non-Organisation for Economic Co-operation and

Development (OECD) energy demand has exceeded OECD energy demand.

The concept of Peak Oil concerns the decline rate of producing existing

(conventional) oil fields.

Energy experts agree that the fuel of choice in the 21st century will be

natural gas, primarily because it is the cleanest burning of all the fossil fuels.

The discussion of capital investment for new oil and gas exploration

includes:

Upstream capital cost

Downstream capital cost

Midstream Super-cycle

Talent shortage

Even with recent developments in domestic oil and gas production, complex

global energy markets will always require a mindset of interdependence,

rather than independence.

INDUSTRY TRENDS

21

Are You Ready to Unlock the Opportunities Available in Oil & Gas?

The eBook you have just read is only one part of our Introduction to Oil &

Gas course.

EKT Interactive has been providing custom training solutions to the oil and

gas industry since 1986, and our Introduction to Oil & Gas courses have

been used by energy companies of all sizes and specialties including super-

majors, large independents, and niche players.

Beyond traditional industry players, we have worked with Big 6 accounting

firms and other financial services companies looking to increase industry

awareness in audit, analyst, sales, and support functions.

If you are looking to become a part of the global boom in oil and gas

opportunities or are committed to making the most of your current position

in the industry, sign up now and get started.

Click Here to Find Out More