oil capital conference - ascent resources

TRANSCRIPT

Oil Capital Conference

Colin Hutchinson, Chief Executive Officer

1 February 2018

Disclaimer

The information contained in these slides and this presentation is being supplied to you by Ascent Resources plc on behalf of itself and its subsidiaries (together “the Company”)

solely for your information and may not be reproduced or redistributed in whole or in part to any other person. This document has not been approved by a person authorised

under the Financial Services and Markets Act 2000 (as amended) ("FSMA") for the purposes of section 21 FSMA and therefore these slides and this presentation is being

delivered and made only to a limited number of persons and companies who are persons who have professional experience in matters relating to investments and who fall within

the category of person set out in Article 19 of the FSMA (Financial Promotion) Order 2005 (the “Order”) or are high net worth persons within the meaning set out in Article 49 of

the Order or are otherwise permitted to receive it. By accepting the slides and attending this presentation and not immediately returning the slides, the recipient represents and

warrants that they are a person who falls within the above description of persons entitled to receive the slides and attend the presentation.

These slides and this presentation do not constitute, or form part of, a prospectus relating to the Company nor do they constitute or contain any invitation or offer to any person to

underwrite, subscribe for, otherwise acquire, or dispose of any shares in the Company or advise persons to do so in any jurisdiction, nor shall they, or any part of them, form the

basis of or be relied on in any connection with any contract or commitment whatsoever. Recipients of these slides and/or persons attending this presentation who are considering

a purchase of ordinary shares in the Company are reminded that any such purchase must be made solely on the basis of the information that the Company has officially released

into the public domain.

Whilst all reasonable care has been taken to ensure that the facts stated in these slides and this presentation are accurate and the forecasts, opinions and expectations

contained in these slides and this presentation are fair and reasonable, the information contained in this document has not been independently verified and accordingly no

representation or warranty, express or implied, is made as to the accuracy, fairness or completeness of the information or opinions contained in these slides or this presentation

and no reliance should be placed on the accuracy, fairness or completeness of the information contained in these slides and this presentation. Some of the statements are the

opinions of the directors of the Company. None of the Company, its shareholders or any of their respective advisers, parents or subsidiaries nor any of their respective directors,

officers or employees or agents (including those of their parents or subsidiaries) accepts any liability or responsibility for any loss howsoever arising, directly or indirectly, from any

use of these slides or this presentation or their contents.

These slides and this presentation do not constitute a recommendation regarding the shares of the Company nor should the slides or the presentation be considered as the

giving of investment advice by the Company or any of its shareholders, directors, officers, agents, employees or advisers. Recipients of these slides and this presentation should

conduct their own investigation, evaluation and analysis of the business, data and property described therein. If you are in any doubt about the information contained in these

slides or this presentation, you should contact a person authorised by the Financial Services Authority who specialises in advising on securities of the kind described in these

slides and presentation.

Certain statements within this presentation constitute forward looking statements. Such forward looking statements involve risks and other factors which may cause the actual

results, achievements or performance expressed or implied by such forward looking statements. Such risks and other factors include, but are not limited to, general economic and

business conditions, changes in government regulations, currency fluctuations, the oil price, the Company's ability to recover its reserves or develop new reserves, competition,

changes in development plans and other risks.

There can be no assurance that the results and events contemplated by the forward looking statements contained in this presentation will, in fact, occur. These forward-looking

statements are correct or represent honestly held views only as at the date of delivery of this presentation.

The Company will not undertake any obligation to release publicly any revisions to these forward looking statements to reflect events, circumstances and unanticipated events

occurring after the date of this presentation except as required by law or by regulatory authority.

By accepting these slides and/or attending this presentation, you agree to be bound by the provisions and the limitations set out in this disclaimer. You agree to keep

permanently confidential the information contained in these slides or this presentation or made available in connection with further enquiries to the extent such information is not

made publicly available (otherwise through a breach by you of this provision).

Neither the slides nor any copy of it may be (a) taken or transmitted into Australia, Canada, Japan, the Republic of Ireland, the Republic of South Africa or the United States of

America (each a “Restricted Territory”), their territories or possessions; (b) distributed to any U.S. person (as defined in Regulation S under the United States Securities Act of

1933 (as amended)) or (c) distributed to any individual outside a Restricted Territory who is a resident thereof in any such case for the purpose of offer for sale or solicitation or

invitation to buy or subscribe any securities or in the context where its distribution may be construed as such offer, solicitation or invitation, in any such case except in compliance

with any applicable exemption. The distribution of this document in or to persons subject to other jurisdictions may be restricted by law and persons into whose possession this

document comes should inform themselves about, and observe, any such restrictions. Any failure to comply with these restrictions may constitute a violation of the laws of the

relevant jurisdiction.

2

Summary

▪ AIM listed, exploration & production company focused on onshore European gas.

▪ Operator of the Petišovci concession in Slovenia.

▪ De-risked asset over the past 12 months on financial, operational and regulatory level.

▪ Debt free & cash generative.

▪ Potential for material increases in production and pricing over the next 24 months.

3

PLC Board of Directors

Clive Carver, Non-executive Chairman• Clive Carver has worked in the City since 1986 and focused exclusively on the small cap sector since 1994.• Chairman of Caspian Sunrise plc, an AIM listed oil and gas exploration and production company operating in

Kazakhstan. • Also Non-executive Chairman of Tax Systems plc, appScatter Group plc, 365 Agile plc and Non-executive Director of

Darwin Strategic Limited & Primary Bid Limited• Fellow of the Institute of Chartered Accountants in England and Wales and is a qualified Corporate Treasurer.

Colin Hutchinson, Chief Executive Officer• Fellow of the Institute of Chartered Accountants in Ireland, law graduate with an MBA from Warwick Business

School.• Previously served as the Company's Finance Director.• Prior to joining Ascent, he was Group Financial Controller at Lochard Energy plc.• CEO since September 2015, has overseen the rebalancing of the financial structure, positioning for growth and first

gas sales

Nigel Moore, Non-executive Director• Chartered Accountant and previously a partner at Ernst & Young for 30 years where he specialised in the oil and gas

sector, advising a wide range of client companies. • Chairman of the audit committee

Cameron Davies, Non-executive Director• Cameron Davies is an international energy sector specialist and the former Chief Executive of Alkane Energy plc.• Also Non-executive Chairman of PowerHouse Energy plc.• A geologist, Dr Davies has over thirty-five years’ experience in the oil and gas sectors.• PhD from Imperial College, is a Fellow of the Geological Society of London and a member of the European

Petroleum Negotiators Group and the PESGB.• Chairman of the Remuneration Committee.

4

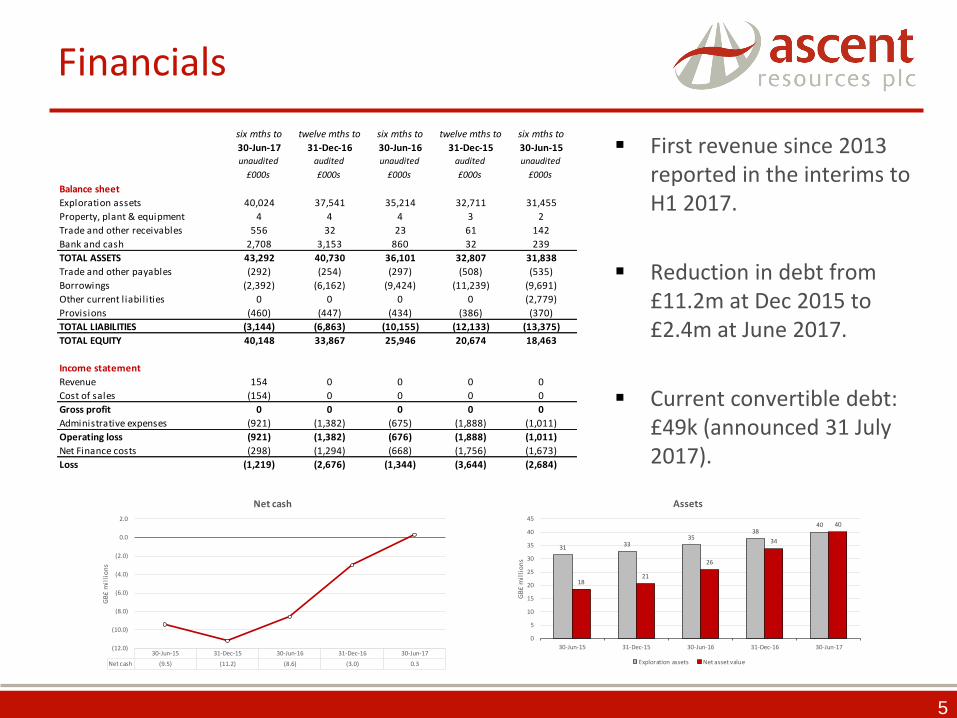

Financials

▪ First revenue since 2013 reported in the interims to H1 2017.

▪ Reduction in debt from £11.2m at Dec 2015 to £2.4m at June 2017.

▪ Current convertible debt: £49k (announced 31 July 2017).

5

six mths to twelve mths to six mths to twelve mths to six mths to

30-Jun-17 31-Dec-16 30-Jun-16 31-Dec-15 30-Jun-15unaudited audited unaudited audited unaudited

£000s £000s £000s £000s £000s

Balance sheet

Exploration assets 40,024 37,541 35,214 32,711 31,455

Property, plant & equipment 4 4 4 3 2

Trade and other receivables 556 32 23 61 142

Bank and cash 2,708 3,153 860 32 239

TOTAL ASSETS 43,292 40,730 36,101 32,807 31,838

Trade and other payables (292) (254) (297) (508) (535)

Borrowings (2,392) (6,162) (9,424) (11,239) (9,691)

Other current l iabilities 0 0 0 0 (2,779)

Provisions (460) (447) (434) (386) (370)

TOTAL LIABILITIES (3,144) (6,863) (10,155) (12,133) (13,375)

TOTAL EQUITY 40,148 33,867 25,946 20,674 18,463

Income statement

Revenue 154 0 0 0 0

Cost of sales (154) 0 0 0 0

Gross profit 0 0 0 0 0

Administrative expenses (921) (1,382) (675) (1,888) (1,011)

Operating loss (921) (1,382) (676) (1,888) (1,011)

Net Finance costs (298) (1,294) (668) (1,756) (1,673)

Loss (1,219) (2,676) (1,344) (3,644) (2,684)

30-Jun-15 31-Dec-15 30-Jun-16 31-Dec-16 30-Jun-17

Net cash (9.5) (11.2) (8.6) (3.0) 0.3

(12.0)

(10.0)

(8.0)

(6.0)

(4.0)

(2.0)

0.0

2.0

GB

£ m

illi

on

s

Net cash

31 3335

3840

1821

26

34

40

0

5

10

15

20

25

30

35

40

45

30-Jun-15 31-Dec-15 30-Jun-16 31-Dec-16 30-Jun-17

GB

£ m

illi

on

s

Assets

Exploration assets Net asset value

Slovenia

EU Member Since 2004

Schengen Member Since 2007

Currency Euro

Capital Ljubljana

Government Parliamentary representative democratic republic. Last elections were 2014; next should be 2018.

Population 2 million

Language Slovenian

Religion 58% Catholic

GDP Composition as of 2016

Services 65%, Industry 33%, Agriculture 2%

Annual gas consumption as of 2016

761m cubic metres / 27 Bcf (99.9% imported)

6

Shares & shareholders

▪ 52 week range 1.0p to 3.74p.

▪ Average volume 34.6m.

▪ 2,268m shares in issue.

▪ £49k of convertible debt outstanding at 1p – potentially 5m shares.

▪ 50 million shares potentially due under the Trameta SPA.

▪ 152 million options outstanding at an average price of 2.4p.

Share price significantly below analysts target of 3p+.

7

Source: yahoo.com 24 January 2018

Source: Computershare 12 January 2018

0

50

100

150

200

250

300

350

400

0

0.5

1

1.5

2

2.5

3

3.5

Vo

lum

e tr

ad

ed (

Mil

lio

ns)

Sha

re P

rice

(PEN

CE)

Share Price

Hargreaves Lansdown (Nominees) Limited (15942) 258,213,766 11.38%

Interactive Investor Services Nominees Limited (SMKTNOMS) 220,889,767 9.74%

Barclays Direct Investing Nominees Limited (Client1) 187,862,391 8.28%

Hargreaves Lansdown (Nominees) Limited (HLNOM) 157,760,068 6.95%

Hargreaves Lansdown (Nominees) Limited (VRA) 149,448,768 6.59%

HSDL Nominees Limited 137,920,379 6.08%

Interactive Investor Services Nominees Limited (SMKTISA) 92,597,603 4.08%

HSDL Nominees Limited (Maxi) 80,865,307 3.56%

JIM Nominees Limited (Jarvis Investment Management) 76,085,311 3.35%

Other shareholders 907,106,960 39.98%

Shares in issue 2,268,750,320 100.00%

Achievements in 2017

▪ Revenues for the year of close to €1 million.

▪ Debt reduced from £8.7 million to £49k.

▪ Commenced production locally in April & export in November.

▪ Executed the work programme:

✓ Recompleted two wells.

✓ Constructed flow lines.

✓ Refurbished existing processing equipment.

✓ Installed metering & pigging station.

✓ Recertified export pipeline.

8

Targets for 2018

▪ Increase production from Pg-10 and Pg-11A.

▪ Acquire permits to re-enter Pg-7, Pg-9, Pg-6 & Pg-8.

▪ Receive IPPC permit in full.

▪ Extend INA gas sales agreement.

▪ Develop other value enhancing opportunities:

▪ Petišovci

▪ Slovenia

▪ Wider Region

9

Production to date

▪ Production to local industrial company from April.

▪ Production suspended in October while export infrastructure put in place.

▪ Export production rate for November at 2.1 MMscfd rising to 2.6 MMscfdfor January.

▪ Revenues to Ascent for last three months of close to €1 million.

▪ Figures for January 2018 are estimates.

10

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Apr-17 May-17 Jun-17 Jul-17 Aug-17 Sep-17 Oct-17 Nov-17 Dec-17 Jan-18

Production rates - MMscfd

MMscfd

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

Apr-17 May-17 Jun-17 Jul-17 Aug-17 Sep-17 Oct-17 Nov-17 Dec-17 Jan-18

Ascent revenue - €

Revenue (€)

Petišovci Joint Venture

Petišovci Joint

Venture

Service provider to the Joint Venture.Owns infrastructure and drilling equipment.

Concession holder. Operator

11

100% 100%50% 50%

25% 75%

Asset

▪ Pannonian basin.

▪ Production of oil & gas from shallower zones since 1940’s – these are pressure depleted but there remains oil in place.

▪ Ascent and partners’ main focus has been the deep gas reservoirs.

▪ Two wells drilled in 2011 proved commercial production was viable.

▪ P50 reserves 88 BCF plus best estimate recoverable resources 76 BCF to Ascent. Valued by the Company at c£200m.

12

Structure

13

▪ Re-enter existing wells to boost production.

▪ Recomplete upwards as reservoirs deplete, getting multiple uses from each well structure.

44

103

50

8

29

73

24

17

106

10

2226

1915

0

20

40

60

80

100

120

A1 B3 C D1 D2 E1 E4 F K L M N O P Q

BC

F

P50 gas in place by reservoir (RPS data)

Subsurface map

14

Well locations

15

▪ Existing well locations to be re-completed during the five year field development plan.

▪ All wells are already connected to the CPP via intra-field pipelines.

▪ All wells drilled to 2,000+ metres.

Export production

▪ Significant technical and operational challenges have been overcome.

▪ Export agreement with INA for untreated gas.

▪ Initial 12 month agreement, scope to extend term and materially increased volumes.

▪ Initial revenues expected at around €300k per month based on 2.5 – 3 MMscfd.

16

Gas to grid

▪ Our plan remains to construct our own treatment facility and sell gas into the national grid, achieving highest possible price

▪ Acquiring IPPC Permit needed to construct our own gas treatment facility has been a lengthy process.

▪ Administrative court dismissed final appeal in November 2017, ruling in favour of Ascent and partners.

▪ Permit expected from Environment Agency in 2018.

▪ Debt & cash flow expected to fund new plant.

17

Petišovci development plan

▪ Increase gas sales to INA from current levels.

▪ Install our own gas treatment facility to increase pricing and capacity.

▪ Deepen 7 existing wells to increase production up to 35 MMscfd.

▪ First re-entries in early 2019 – Pg-7 & Pg-9.

▪ Drill 6 infill wells to maintain production at plateau of 35 MMscfd.

▪ Applied for water re-injection permit.

▪ Investigate enhanced oil recovery in shallow reservoirs – seismic review in progress.

New treatment facility ready

Existing wells deepened

Infill wells drilled

Source: internal management estimates.

18

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034

wel

ls p

rod

uci

ng

MM

scfd

Production

Average wellsproducingAverage daily MMscfd

Petišovci economics

Source: internal management estimates.

19

0.0

10.0

20.0

30.0

40.0

50.0

60.0

2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028

GB

£ m

illi

on

s

Revenues & operating cash flow

Revenues Operating cash flow

-20.0

-18.0

-16.0

-14.0

-12.0

-10.0

-8.0

-6.0

-4.0

-2.0

0.0

2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028

GB

£ m

illi

on

s

CAPEXSummary

NPV10 219 € £199 Millions

Gross cash flow

Revenue £730 Millions

Preferential recovery £44 Millions

CAPEX -£108 Millions

Other costs -£81 Millions

Tax -£85 Millions

Net Cash £500 Millions

Total Production 4,939 174 38%

MMm3 BCF Recovery

Total wells 15

Current 2

Old wells deepened 7

New wells drilled 6

18 years to 2035

2

4

6

910

12 1211

1314

13

1 4 2 3 2 4 2 2 3 3 50

2

4

6

8

10

12

14

16

2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

Wel

ls

Pro

du

ctio

n (M

Msc

fd)

Average MMscfd & average wells producing

Wells active (eop) Wells drilled or worked over

Average daily production (MMscfd)

Growth strategy

Within Petišovci

▪ Increase production from high value gas asset to 35 MMscfd over five year period.

▪ Investigate shallow oil reservoirs.

Within Slovenia

▪ Target other concession areas – seismic acquired in the past during a previous joint venture.

Within the region

▪ Actively reviewing three value-enhancing transactions.

20

Summary

▪ Producing from our high value gas asset.

▪ Profitable and cash generative.

▪ Virtually debt free.

▪ Potential to grow through acquisition.

▪ Supportive retail shareholder base.

▪ Share price significantly below analyst’s and company target.

21

Thank you