oil, gas, and ngl market overview - latest energy, metals

TRANSCRIPT

© 2013 Platts, McGraw Hill Financial. All rights reserved.

Oil, Gas, and NGL Market Overview Charles Nevle, Manager Energy Analysis September 18, 2013

Premier Energy Data and Analytics

Who We Are • Ground-up approach to Energy Data

and Analytics

• 400+ Customers

• Division of Platts (McGraw-Hill) 40%

22%

33%

5%

Majors, Producers, Mktrs, Industrials

Pipelines, Utilities, Midstream

Financial and Hedge

Government, Associations, Consultants

What We Do • Reports and Consulting Services

• Collect, Analyze, Interpret and

Distribute Data, Information and

Knowledge to the Energy Industry

10/+3

181/+14

45/+4

53/+4

14/+0

2/-5

33/+2

22/+5

25/-2

115/+17

3/+0

2/-3

218/+0

30/+4

5/+0

49/+13

16/-4

4/-1

Active rig count: July 12, 2013 / Change in rig count from January 4, 2013

Rig Increases Dry Gas Focused Areas Rig Increases Liquids-Rich/Oil Focused Areas Rig Declines Source: BENTEK, July 2013

3/-1

98/+1

66/+9

41/+8

62/+5

15/+0 207/+2

459/+16

32/-9

15/+3 PICEANCE

CALIFORNIA

MICHIGAN

POWDER RIVER

GREEN RIVER

WIND RIVER

OTHER ROCKIES WILLISTON

SAN JUAN

UINTA OTHER

APPALACHIAN

D-J

MARCELLUS WET

MARCELLUS DRY

UTICA

ILLINOIS

ARK FAYETTEVILLE

ARK WOODFORD

OFFSHORE

TX GULF EAGLE FORD

PERMIAN

ANADARKO

FT WORTH

AL-MS-FL

LA GULF

EAST TX

ARKLA

OTHER MIDCONTINENT

TX GULF

30/+4

RATON 0/+0

Crude and Gas Prices Higher Since Beginning of Year Continuing to Prompt Drilling Investment Across Country

TOTAL

1857

CHANGE

+89

HH ($/MMBtu) WTI ($/Barrel) Mt. Belvieu ($/Gal)

Jan. 2013 $3.34 $94.57 $0.95

Jul. 2013 $3.62 $104.78 $0.88

Rig Count Does Not Reflect Improving Drilling Efficiencies

-

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

-

50

100

150

200

250

300

350

400

Wel

l per

Rig

per

Mon

th

No.

Wel

ls D

rille

d/Ac

tive

Rigs

Eagle Ford Wells Drilled vs. Active Rigs

Wells per Month per Rig Horizontal Rigs Horizontal Wells DrilledSource: Bentek, RIGDATA

U.S. Oil Plays Generate Very Attractive Returns Even at $80 Crude, at $100 Crude Producers Should Continue to Accelerate Development

0%

10%

20%

30%

40%

50%

60%

IRR

$80 $60Note: NG at $3/MMbtu and NGLs 30% of Crude, No Basis Differentials

5

Gas, Oil and NGL Price Comparison: MMBTU Equivalent

6

$0.00

$5.00

$10.00

$15.00

$20.00

$25.00

$30.00

$0.00

$5.00

$10.00

$15.00

$20.00

$25.00

$30.00

$/M

MB

tu E

quiv

alen

t

CAPP WTI HH MB NGL Brent

Value Gap

Crude Oil

• North American Production Growth Continues to Shape Market; Breaking Traditional Flow Patterns and Pricing Relationships

• Pipeline, Rail, and Waterborne Options Critical to Balancing Regional Markets and Bringing Light Crude to Coastal Markets

• U.S. Light Crudes Will Be Discounted to World Prices Until the Development of New Refining and Export Options Occur

• Growing Supply Will Lead to Downward Pressure on North American Oil Prices

8

Market Conclusions

0

2

4

6

8

10

12

14

16

18

20

MM

b/d

U.S. & Canadian Production and Refinery Demand Forecast

PADD I PADD II PADD III PADD IV

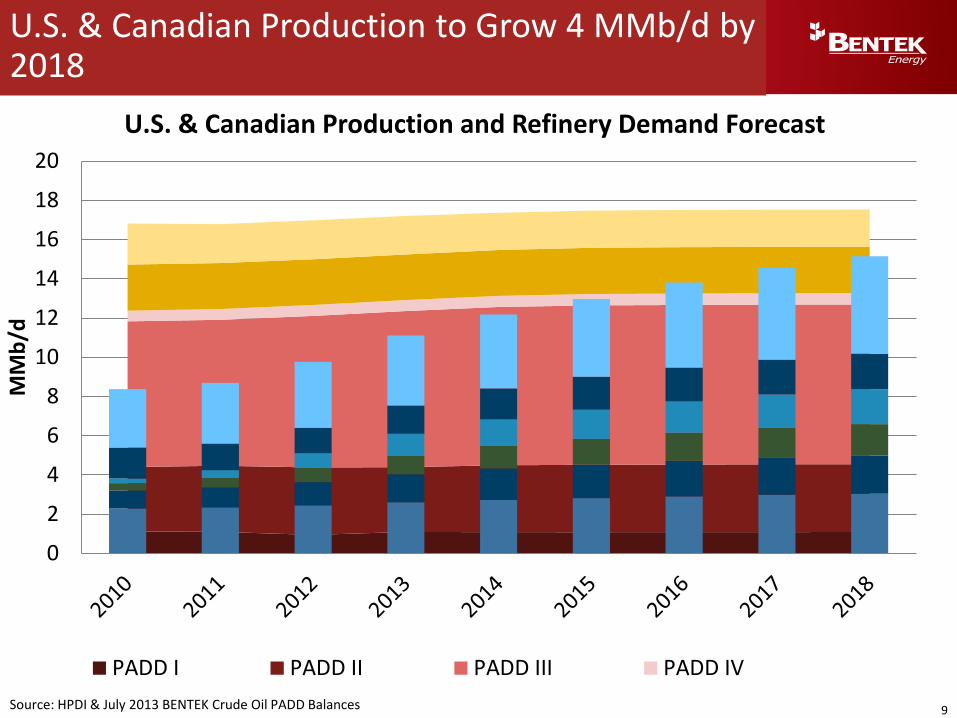

U.S. & Canadian Production to Grow 4 MMb/d by 2018

Source: HPDI & July 2013 BENTEK Crude Oil PADD Balances 9

5 10 15 20 25 30 35 40 45 50 55 60 65

Eagle FordBarnett Combo

Cana woodford / SCOOPUtica

DuvernayAvalon / Bone Spring

BakkenCline

Marmaton / HogshooterWolfcampMiss Lime

Alberta BakkenNiobraraCardium

Uinta Black WaxViking

SpearfishAlaska North Slope

Offshore/MarsSyncrude

ShaunavonHeavy Diluted Bitumen

Non-Upgraded Bitumen

API Gravity

U.S. Onshore Plays Predominantly Light Sweet Crude & Condensate, While Canadian Crudes Heavy

Canadian Play U.S. Play

Light Crude

10

Condensate

Bakken

Niobrara Anadarko

Permian

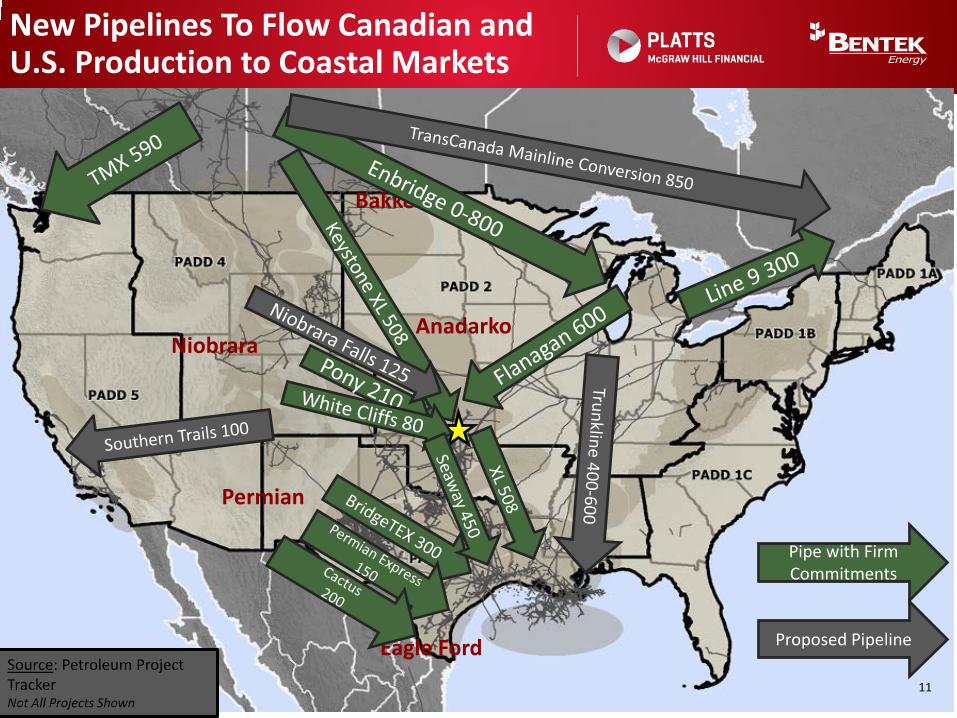

Eagle Ford Source: Petroleum Project Tracker Not All Projects Shown

New Pipelines To Flow Canadian and U.S. Production to Coastal Markets

Pipe with Firm Commitments

Proposed Pipeline

11

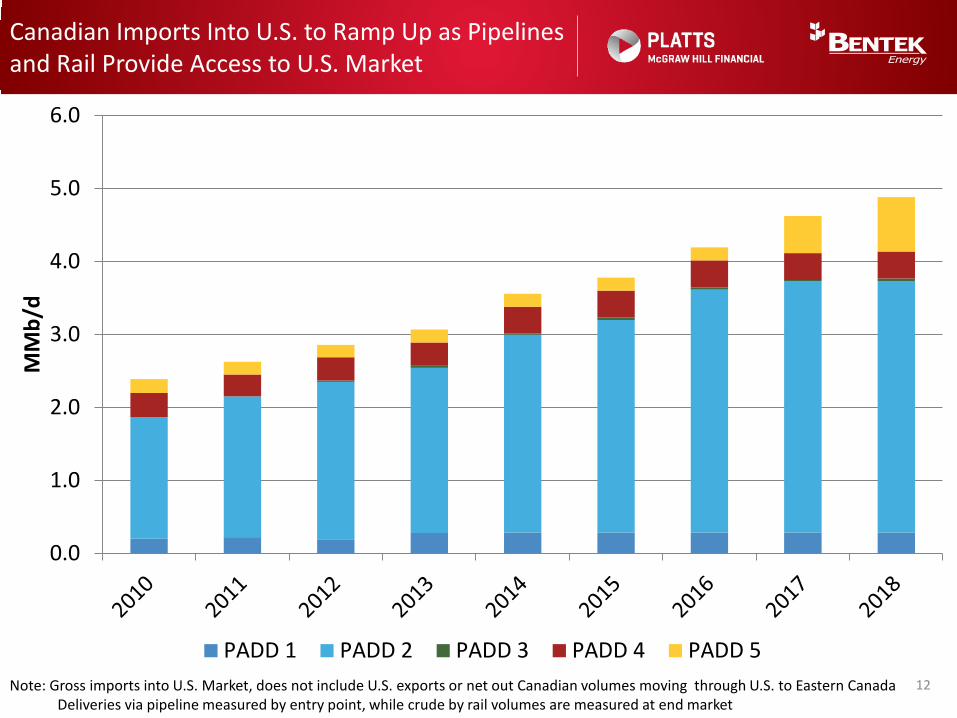

Canadian Imports Into U.S. to Ramp Up as Pipelines and Rail Provide Access to U.S. Market

0.0

1.0

2.0

3.0

4.0

5.0

6.0

MM

b/d

PADD 1 PADD 2 PADD 3 PADD 4 PADD 512 Note: Gross imports into U.S. Market, does not include U.S. exports or net out Canadian volumes moving through U.S. to Eastern Canada

Deliveries via pipeline measured by entry point, while crude by rail volumes are measured at end market

Crude by Rail Volumes Exceeding 1 MMb/d in 2013 as New CBR Loading and Unloading Stations Pop Up Everywhere Relieving Constraints

Bakken to East Can – 15 Mb/d

PADD IV to PADD I – 11 Mb/d

13

Long Haul Crude by Rail Volumes Expected to Continue to Grow Exceeding 1 MMb/d in 2014

-

200

400

600

800

1,000

1,200

1,400

2010 2011 2012 2013 2014 2015 2016 2017 2018

Mb/

d

PADD 1 PADD 2 PADD 3 PADD 5 EC

14

Note: Does Not Include Intra PADD Rail Shipments such as movements from Permian or Eagle to PADD 3 Unloading Terminals

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

2010 2011 2012 2013 2014 2015 2016 2017 2018

Mb/

d

PADD I PADD III PADD V Eastern Canada

Eastern Canada, U.S. East Coast and West Coast Light Imports to Be Fully Displaced by 2018 Due Increased Access to North American Crude Slates from Rail, Pipeline, and Water

Waterborne Imports

Source: BENTEK May 2013 Crude Oil PADD Balances 15

North American Production Putting Downward Pressure on Prices

16

($0)

($9)

$18

$18

Avg. 2012

Avg. 2018

($9)

$8

$3

($7)

Brent Premium

$17 $5

$94 $80

Source: BENTEK July 2013 Market Call: North American Crude Oil

$11 $17

($15) ($16)

16

Natural Gas

Net Change in Lower 48 U.S. Natural Gas Fundamentals from 2007 to 2012

18

7.4

12.5

(3.3) (1.7)

6.5

(1.7)

0.8 0.8 0.2

6.6

-6.0-4.0-2.00.02.04.06.08.0

10.012.014.0

Tota

l Sup

ply

Prod

uctio

n

Impo

rts f

rom

Can

ada

LNG

Dem

and

from

Pow

er

ResC

omm

Dem

and

Indu

stria

l Dem

and

Expo

rts t

o M

exic

o

Pipe

Los

s

Tota

l Dem

and

Bcf/

d

2007-2012 Fundamentals (Henry Hub Avg. - $5.14)

Net Long 0.8 Bcf/d

Source: BENTEK Cell Model

Net Change in Lower 48 U.S. Natural Gas Fundamentals from 2013 to 2018

19

12.3

14.3

(1.9) (0.0)

5.1

0.7 2.3 1.9 2.8

0.2

13.0

-4.0-2.00.02.04.06.08.0

10.012.014.016.0

Tota

l Sup

ply

Prod

uctio

n

Impo

rts f

rom

Can

ada

LNG

Dem

and

from

Pow

er

ResC

omm

Dem

and

Indu

stria

l Dem

and

Expo

rts t

o M

exic

o

LNG

Exp

orts

Pipe

Los

s

Tota

l Dem

and

Bcf/

d

Source: BENTEK Cell Model

North American Production Growth Focused in Northeast and Texas

+0.7 Bcf/d

2.6 Bcf/d

-0.2 Bcf/d

+5.6 Bcf/d +2.0

Bcf/d

+3.3 Bcf/d

-0.1 Bcf/d

+0.2 Bcf/d

Note: Forecasts Compare 2013 to 2018 (Bcf/d)

+0.2 Bcf/d

Total Increase: 14.2 Bcf/d

20 Source: Bentek Cell Model

Northeast Adds 5.2 Bcf/d by 2018

0.02.04.06.08.0

10.012.014.016.018.020.0

Bcf/

d

Total Northeast Production Forecast

N. PA Dry Marcellus SW Wet & WV Marcellus and LegacySW PA Dry Ohio Utica and Legacy

21

12.5 Bcf/d

17.7 Bcf/d

45

50

55

60

65

70

75

80

85

90

95

Bcf/

d

U.S. Supply/Demand Balance

Dry Production US Production ForecastUS Domestic Demand US Domestic Demand Forecast

Growth in Demand Not Enough: Exports Needed

9.3 Bcf/d

10.2 Bcf/d

24.7 Bcf/d

17.1 Bcf/d

22 Source: BENTEK Cell Model

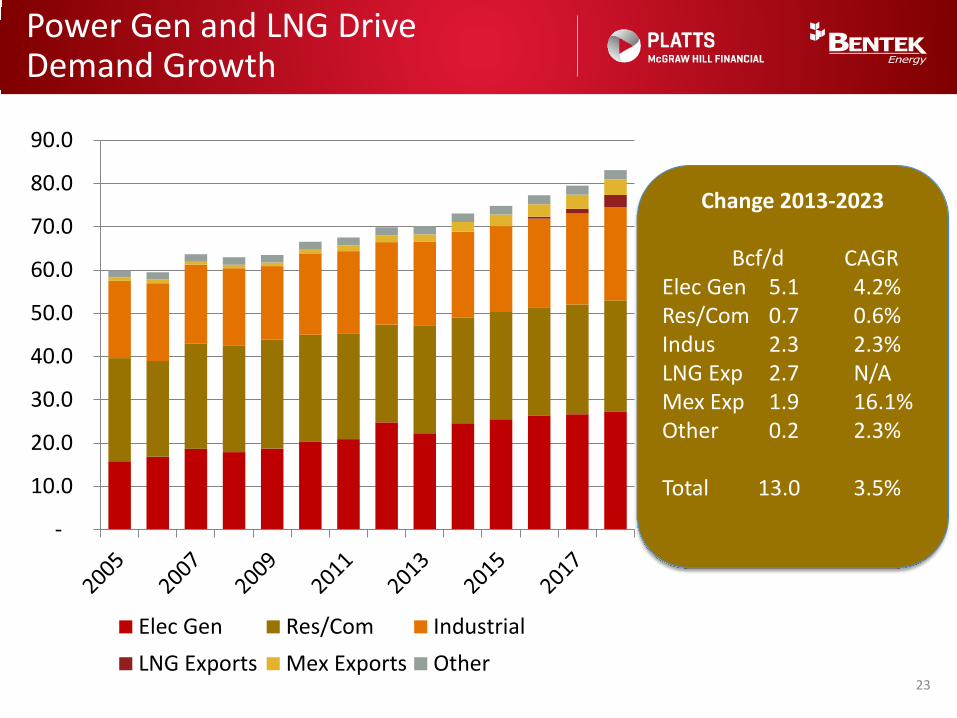

Power Gen and LNG Drive Demand Growth

-

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

Elec Gen Res/Com IndustrialLNG Exports Mex Exports Other

23

Change 2013-2023

Bcf/d CAGR Elec Gen 5.1 4.2% Res/Com 0.7 0.6% Indus 2.3 2.3% LNG Exp 2.7 N/A Mex Exp 1.9 16.1% Other 0.2 2.3% Total 13.0 3.5%

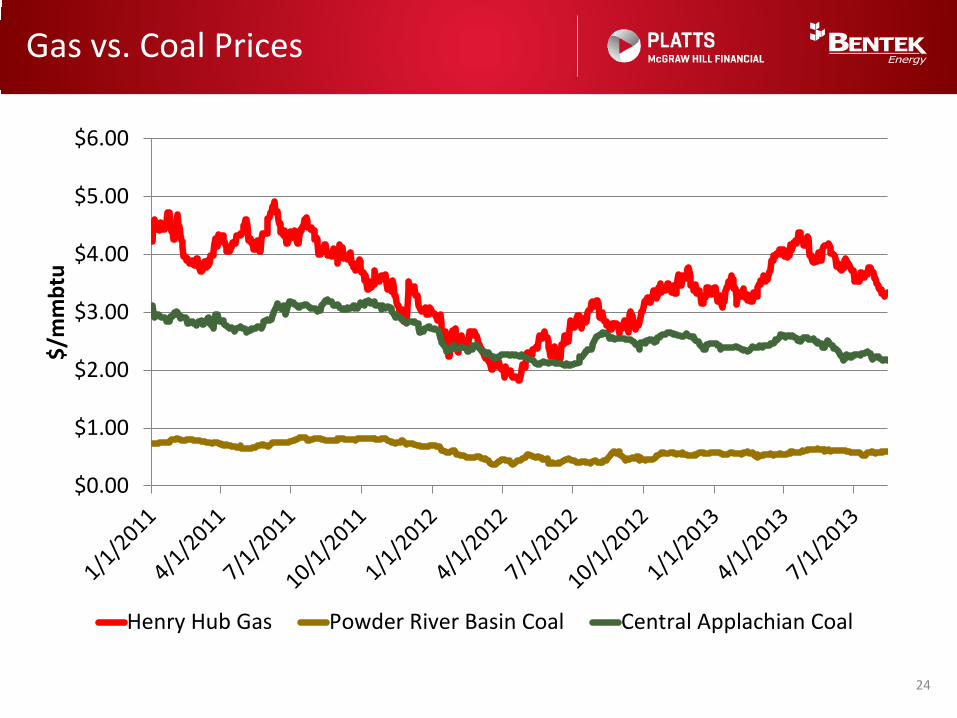

Gas vs. Coal Prices

24

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

$/m

mbt

u

Henry Hub Gas Powder River Basin Coal Central Applachian Coal

Southeast and Texas Dominate Industrial Demand Growth

0

5

10

15

20

25

NE SE TX MCP MCM ROX SW NW25

Change 2013-2023

Bcf/d CAGR NE 0.3 2.1% SE 1.0 3.7% TX 0.3 1.4% MCP 0.0 0.9% MCM 0.6 2.8% ROX 0.1 2.8% SW 0.1 0.8% NW 0.0 0.1% Total 2.3 2.3%

Black Hole of Demand Appears

0.0

10.0

20.0

30.0 Southeast Demand Poised to Explode

LNG EXPORTS POWER RES/COM INDUSTRIAL PIPE LOSS

Southeast and Southeast Texas demand cause a demand pull attracting supply from Texas, Midcontinent and Northeast to supply new demand

Source: BENTEK Cell Model

North American LNG Export Facilities

Sabine Pass

Freeport

Lake Charles

Cameron

Cove Pt.

Existing Import + Proposed Export

Source: BENTEK

North East Exports: Cove Point – 0.75 Bcf/d (5.6 mtpa)

Gulf Coast Export Terminals: Freeport LNG– 1.76 Bcf/d (13.2 mtpa) Lake Charles – 2 Bcf/d (15 mtpa) Sabine Pass – 2.4 Bcf/d (18 mtpa) Cameron – 1.6 Bcf/d (12 mtpa)

Kitimat LNG HN DC LNG

LNG Canada

Proposed Export

Canadian Exports: DC LNG – 0.25 Bcf/d (1.8 mtpa) Kitimat LNG – 1.4 Bcf/d (10 mtpa) LNG Canada (Phase 1 ) - 1.6 Bcf/d (12 mpta)

South East Exports: Elba Island FLNG – 0.5 Bcf/d ( 4mtpa)

Elba Island

27

New Demand Projects Double Exports

28

Project Name Capacity City StateIn-Service

Date

El Paso Willcox Lateral 2013 Expansion 185 Douglas Arizona 4/1/2013El Paso Norte Crossing* 366 Clint Texas 8/1/2013El Paso Samalayuca Lateral* 237 Clint Texas 8/1/2013Kinder Morgan Mier Monterrey Expansion 275 Salineno Texas 4/1/2014TETCO South Texas Expansion 300 Reynosa Texas 6/1/2014El Paso Sierrita Pipeline** 812 Sasbe Arizona 10/1/2014Net Midstream/PEMEX -- Agua Dulce - Frontera 2,100 Reynosa Texas 11/1/2014Total Export Capacity Additions 4,275 Total U.S. Export Capacity with Expansions 9,648 * Samalayuca and Norte Crossing exports are limited to a total of 545 MMcf/d by current Samalayuca lateral capacity. **Sierrita is expected to have an initial capacity of 0.2 Bcf/d, expanding to 0.8 Bcf/d by 2016. Samalayuca presidential permit for exports is 545

Mexican Border Crossing Expansions

0.00.51.01.52.02.53.03.54.04.5

Bcf/

d

US Exports to Mexico

SW TO MEX SW TO MEX Forecast TX TO MEX TX TO MEX Forecast

East Gets Long/West Gets Short

-15-10

-505

Northeast Balance (Bcf/d)

-10

-5

0

5 Southeast Balance (Bcf/d)

02468 MCP Balance (Bcf/d)

0

5

10

15 Texas Balance (Bcf/d)

-8-6-4-20 Southwest Balance (Bcf/d)

0

5

10

15 W. Canada Balance (Bcf/d)

Natural Gas Price Forecast

30

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

$7.00

$8.00

$9.00

$10.00

$/M

mbt

u (R

eal)

NYMEX BentekNote: Price forecast as of Aug 12, 2013

Vast increases in gas supply potential combined with ‘subsidizing’ impact of NGL production keeps gas prices low

throughout the forecast period.

Natural Gas Liquids

NGL Conclusions

• U.S. NGL production capacity to increase by 1.5 MMb/d (52%) 2013 – 2018

• Ethane will remain long 2013-2017 until new steam crackers are built with length increasing again after this period.

• Ethane production from the Williston Basin is a wild card due to demand, transportation constraints, and costs.

• U.S. demand insufficient to absorb C3+ growth and market will rely on exports to balance the market

32

NGL Supply Growth

33 Source: Bentek

-

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0MMb/d US NGL Production from Gas Plants

PADD 1 PADD 2 PADD 3 PADD 4 PADD 5

US supply growth from gas plants expected to reach 4.9 MMb/d by 2023

PADD 1 PADD 2 PADD 3 PADD 4 PADD 5 TotalGrowth 429 492 495 32 2 1,450

% 345% 94% 29% 8% 10% 52%

Growth 2013 - 2018

Nearly 80% of U.S. NGL Production Coming from 6 Regions by 2018

Marcellus/Utica, 124

Eagle Ford, 464

Permian, 381

Anadarko, 356

Rockies, 411

Bakken, 84

Other, 1,031

2013 Production

Total Production 2.85 MMb/d

Marcellus/Utica, 552

Eagle Ford, 875

Permian, 453

Anadarko, 485

Rockies, 444

Bakken, 468

Other, 1,026

2018 Production

Total Production 4.3 MMb/d 34

Processing Plant Capacity

35

0.95

1.40

2013 2015

Bakken

SW Marcellus/Utica

Eagle Ford/Gulf Coast TX

9.94

11.8

2013 2015

3.80

8.56

2013 2015Current US gas processing capacity

~ 74 Bcf/d and set to potentially increase by 16 Bcf/d to 90 Bcf/d by end-2015

Source: Bentek NGL Facilities Databank

Fractionation Plant Capacity

36

0.03

0.06

2013 2015

Bakken

SW Marcellus/Utica

Eagle Ford/Gulf Coast TX

1.85 2.58

2013 2015

0.21

0.77

2013 2015Current US fractionation capacity

~ 2.7 MMb/d and set to nearly double to 5.3 MMb/d by end-2015

Source: Bentek NGL Facilities Databank

NGL Pipelines on the Horizon

37

By the end of 2015, could be as much as 1,178 MB/d of incremental NGL pipeline capacity into Mont Belvieu

Conway

Mont Belvieu

NGL Pipelines on the Horizon

38

Project Name Owner Capacity (MB/d)

In-Service Date

Region

Texas Express Anadarko / DCP / Enbridge / Enterprise 280 9/1/2013 Skellytown, TX to

Mont Belvieu, TX

TBD Kinder Morgan / MarkWest 200 9/1/2015 Ohio to Mont Belvieu

Bluegrass Williams & Boardwalk Joint Venture 200 9/1/2015 OH, PA to

Gulf Coast

Mariner South Lone Star NGL / Sunoco 200 3/1/2015 Mont Belvieu, TX to Nederland, TX

Sterling III ONEOK Partners 193 12/1/2013 Medford, OK to Mont Belvieu, TX

Front Range Anadarko / DCP / Enbridge 150 12/1/2013 DJ Basin, CO to Skellytown, TX

Eagle Ford Enterprise Products Partners 140 7/1/2013 La Salle County, TX to Yoakum Plant, TX

ATEX Express Enterprise Products Partners 125 3/31/2014 Houston, PA to Gulf Coast

Crosstex NGL Crosstex 77 TBA Permian, Eagle Ford, Barnett to Acadia/Ascension, LA

Mariner East MarkWest / Sunoco 70 9/1/2014 Houston, PA to Markus Hook, PA

MAPL - Rockies Segment Enterprise Products Partners 75 3/1/2014 Rockies to

Gaines County, TX

Bakken ONEOK Partners 75 9/1/2014 Williston, ND to Weld County, CO

Vantage Mistral Energy 40 12/1/2013 Williston, ND to AB, Canada

Arbuckle ONEOK Partners 15 12/1/2013 Velma, OK to Mont Belvieu, TX

Panola Expansion Enterprise Products Partners 15 11/1/2013 Cartage, TX to Mont Belvieu, TX

Source: Bentek research, company reports

NGL Demand Projects

39

Project Name/Location

Owner Ethane Capacity (MB/d)

In-Service Date

Status Region

Baytown, TX ExxonMobil 89 2017 Planned Gulf Coast Baytown, TX CP Chem 89 2017 Planned Gulf Coast Ingleside, TX OxyChem/Mexichem 36 2017 Planned Gulf Coast Westlake, LA Sasol 89 2017 Planned Gulf Coast Freeport, TX Dow Chemical 89 2018 Under Construction Gulf Coast

Point Comfort, TX Formosa 48 2018 Planned Gulf Coast Total Base Case 440

Various Others ? Speculative

Ethylene Facilities

Owner Capacity (MB/d) In-Service Date Status Region

C3 Petrochemicals 25 4Q2015 New Build TX Dow Chemical 32 2Q2015 New Build TX Enterprise Products 32 3Q2015 New Build TX Formosa Plastics 26 2Q2016 New Build TX Williams 21 2Q2016 New Build AB

PDH Facilities

NGL Demand Projects

40

Project Name Owner Capacity (MB/d)

In-Service Date

Status Region

N/A Enterprise Products 225 N/A Current TX

N/A Targa 40 N/A Current TX Galena Park Targa 60 3Q2013 Expansion TX

Galena Park II Targa 67 3Q2014 Expansion TX Patriot Targa 40 3Q 2015 Expansion TX

N/A Coastal Caverns/Vitol 90 1Q2015 New Build TX

Ingleside Occidental Chemical 150 2Q2015 New Build TX N/A Enterprise 75 2Q 2015 Expansion TX N/A Crosstex 40 3Q 2015 New Build LA

Total Export Capacity 787

Mariner South Sunoco Logistics 200? 1Q 2015 New Build TX Mariner East Sunoco Logistics 70 (E/P mix) 2H 2014 New Build PA

LPG Export Facilities

Ethane Supply/Demand

41 Source: Bentek

Ethane demand will struggle to keep pace with supply growth

*Due to lack of demand **Due to lack of infrastructure

0.0

0.5

1.0

1.5

2.0

2011 2012 2013 2014 2015 2016 2017 2018

Mb/

d

Petchem Exports Rejection Total Supply

US Ethane Rejection

42 Source: Bentek

0

50

100

150

200

250

300

350

400

2011 2012 2013 2014 2015 2016 2017 2018

MMb/d US Ethane Rejection by Region

PADD 2 PADD 1 PADD 4

Ethane rejection will be primarily in Williston and Appalachia

US Ethane Rejection - 2018

43 Source: Bentek

Ethane Rejection by Region in 2018 (Mb/d)

Vantage 40 Mb/d

Bakken 66 Mb/d 81 rejected

187 Mb/d Supply

248 Mb/d Supply

ATEX 125 Mb/d

Mariner West 50 Mb/d

Mariner East 47 Mb/d

Bluegrass 90 Mb/d

Ethane rejected due to lack of pipeline takeaway capacity

Conway

Mont Belvieu

14 cpg

6.2 cpg

Region Total Ethane

Rejection (Mb/d)

Williston 147

SW Marc/Utica 21

PADD IV 50

Total US 218

Bakken

SW Marcellus/Utica

West Rockies

East Rockies

0 rejected

50 rejected

8.9 cpg

13.8 cpg

14.5 cpg

Propane Supply/Demand

44 Source: Bentek

Propane likely oversupplied in 2014, however, assuming sufficient demand from global markets, propane exports will help rebalance the market.

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8Mb/d US Propane Supply/Demand Balance

Res/Comm Petchem Mariner East Exports Gulf Coast Exports Total Supply

Normal Butane Supply/Demand

45 Source: Bentek

Normal butane likely oversupplied in 2014, however, assuming sufficient demand from global markets, exports will help rebalance the market.

0

100

200

300

400

500

600

700Mb/d US Normal Butane Supply/Demand Balance

Petchem Refinery Inputs Isomerization Product Supplied Exports Total Supply

Iso Butane Supply/Demand

46 Source: Bentek

Iso butane growth from gas plants to be offset by reduction in merchant isomerization supply

0

50

100

150

200

250

300

350

400

2011 2012 2013 2014 2015 2016 2017 2018

Mb/d US Iso Butane Supply/Demand Balance

Product Supplied

Octane Enhancement

Refinery Inputs

Petchem

Total Supply*

* Includes iso butane from merchant isomerization

Natural Gasoline Supply/Demand

47 Source: Bentek

Natural gasoline prices should remain strong as long as diluent demand remains healthy

-100

0

100

200

300

400

500

600

2011 2012 2013 2014 2015 2016 2017 2018

Mb/d US Natural Gasoline Supply/Demand Balance

Exports to Canada byRailExports to Canada byPipelineProduct Supplied

Refinery Inputs

Total Supply

NGL Price Forecast

48 Source: Bentek, ICE

$-

$0.50

$1.00

$1.50

$2.00

$2.50

2011 2012 2013 2014 2015 2016 2017 2018

$/gal Mont Belvieu Price Forecast

Ethane (Base Case) Propane Normal Butane Iso Butane Natural Gasoline

Q&A