oil & gas market challenges: a trading house perspective€¦ · oil & gas market...

TRANSCRIPT

Unsa

ve

d D

ocu

me

nt

/ 0

1/0

5/2

01

2 /

08

:12

Oil & Gas Market Challenges: A Trading House Perspective

IEA Training Week,

Paris, 7-11 April 2014

Unsa

ve

d D

ocu

me

nt

/ 0

1/0

5/2

01

2 /

08

:12

1

Disclaimer

The information contained in this presentation (the “Presentation”) is being provided by Gunvor Group Ltd (the “Company”) and its subsidiaries (together with the Company, the “Group”). The Presentation is for information purposes only and any information made available orally or in writing at the Presentation is strictly confidential and may not be distributed, published, copied or reproduced (in whole or in part) or disclosed by its recipients to any other person for any purpose, at any time or in any form other than with the prior written consent of the Company.

This Presentation does not constitute or form part of and should not be construed as, any offer or invitation to sell or issue, or any solicitation of any offer to purchase or subscribe for, any securities to any person in any jurisdiction nor shall it (or any part of it), or the fact of its distribution, form the basis of, or be relied on in connection with or act as any recommendation or inducement to enter into, any contract, commitment or investment decision whatsoever relating to any securities. The information contained in this Presentation, unless otherwise specified, is only current as of the date of this Presentation and is subject to further verification and amendment in any way without liability or notice to any person. The information contained in this Presentation has not been independently verified. The Company, all members of the Group and their respective associates or directors, officers, employees, advisers or representatives expressly disclaim any duty, undertaking or obligation to update publicly or release any revisions to any of the information, opinions or forward looking statements contained in this Presentation to reflect any events or circumstances occurring after the date of this Presentation. No undertaking, representation or warranty or other assurance, express or implied, is made or given as to the accuracy, completeness, sufficiency or fairness of the information or opinions contained or expressed in the Presentation or any information made available orally or in writing at the Presentation (or whether any information has been omitted from the Presentation) and, save in the case of fraud, no responsibility or liability is accepted by any person for any loss, cost or damage suffered or incurred as a result of the reliance on such information or opinions or otherwise arising in connection with the Presentation. In addition, no duty of care or otherwise is owed by any person for any loss, cost or damage suffered or incurred as a result of the reliance on such information or opinions or otherwise arising in connection with the Presentation. Recipients of the Presentation should conduct their own investigation, evaluation and analysis of the business, data and property described in the Presentation. This Presentation contains unaudited financial information in relation to the Group.

This presentation includes statements that are, or may be deemed to be, ‘forward-looking statements’. These forward-looking statements can be identified by the use of forward-looking terminology, including the terms ‘targets’, ‘believes’, ‘anticipates’, ‘expects’, ‘estimates’, ‘intends’, ‘plans’, ‘will’, ‘may’, ‘could’ or ‘should’ or similar expressions or by discussions of plans, objectives, goals, strategies, future events or performance and underlying assumptions. These forward-looking statements include matters that are not historical facts or are statements regarding the Company’s intentions, beliefs or current expectations. Forward-looking statements are based on current plans, estimates and projections, and therefore too much reliance should not be placed upon them. Such statements are subject to risks and uncertainties, most of which are difficult to predict and generally beyond the Company's control. If the assumptions underlying any of these statements prove incorrect, the Company’s actual results of operations, financial condition and liquidity and the development of the industry in which the Company operates may materially differ from those made in, or suggested by, the forward-looking statements contained in this Presentation. The Company expressly disclaims any obligation or undertaking publicly to review or confirm analysts expectations or estimates or to release publicly any updates or revisions to any forward-looking statements contained herein to reflect any changes in the Company's expectations with regard thereto or any change in events, conditions or circumstances on which any such statement is based.

This Presentation is not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident of, or located in, any locality, state, country or other jurisdiction where such distribution or use would be contrary to law or regulation or which would require any registration or licensing within such jurisdiction.

Unsa

ve

d D

ocu

me

nt

/ 0

1/0

5/2

01

2 /

08

:12

2

Oil & Gas Market Challenges: A Trading House Perspective

1. Who are the traders and what do they do?

2. A changing trader business model

3. Dealing with risk & the impact of new regulations

4. New sources & new constraints in oil supply

5. The macro economy & oil demand uncertainty

6. The downstream market dimension

7. Oil price dynamics

8. Evolving gas and coal markets

Unsa

ve

d D

ocu

me

nt

/ 0

1/0

5/2

01

2 /

08

:12

3

A) DEFINING TRADING & THE TRADERS

Unsa

ve

d D

ocu

me

nt

/ 0

1/0

5/2

01

2 /

08

:12

4

Gunvor History

• 1997: Shareholders open new trading company based in Tallinn, Estonia.

• 2000: Gunvor is formalised.

• 2003: Main trading facilities move to Geneva to take advantage of city’s trading talent.

• 2007: Opened Singapore Office

• 2009: Broaden energy portfolio and moved into coal, natural gas, LNG, power and carbon emissions.

• 2011: Began operations at Ust Luga, world’s largest oil transshipment terminal.

• 2012: Bought former Petroplus refineries in Antwerp and Ingolstadt, becoming in the process a 210 kb/d European refiner

Unsa

ve

d D

ocu

me

nt

/ 0

1/0

5/2

01

2 /

08

:12

5

What is commodity trading?

source: KPMG

• Commodity trading involves the optimisation of arbitrage operations using logistics, ensuring the transformation of stock and facilitating storage and transportation towards points of consumption

• Traders deploy their global logistical presence, access to funding and market intelligence to capitalise on market imbalances & arbitrage opportunities

Unsa

ve

d D

ocu

me

nt

/ 0

1/0

5/2

01

2 /

08

:12

6

Arbitrage, not absolute price, is what counts

Geographical

arbitrage

Price differentials for

same product

between different

locations

Deploy global

logistics network to

source commodity in

one place & ship to

another by tanker,

pipe, truck , rail

Commodity

(transformation)

arbitrage

Price differentials

between grades,

types or blends of

commodities

Exploit differentials

by blending,

processing,

substitution or

conversion (refinery,

power plant)

Time arbitrage Differentiated price

between prompt and

forward delivery

Carry trades via

financing and storage

Unsa

ve

d D

ocu

me

nt

/ 0

1/0

5/2

01

2 /

08

:12

7

Pump It Move It Refine It Store It Sell It Move It

Traders provide liquidity across the supply chain

• The commodity trader paradox:

• Exploit episodes of supply chain imbalance & price volatility

• But, by providing streamlined, cost-effective linkage between suppliers and consumers, they help re-establish physical (& price) equilibrium

Unsa

ve

d D

ocu

me

nt

/ 0

1/0

5/2

01

2 /

08

:12

8

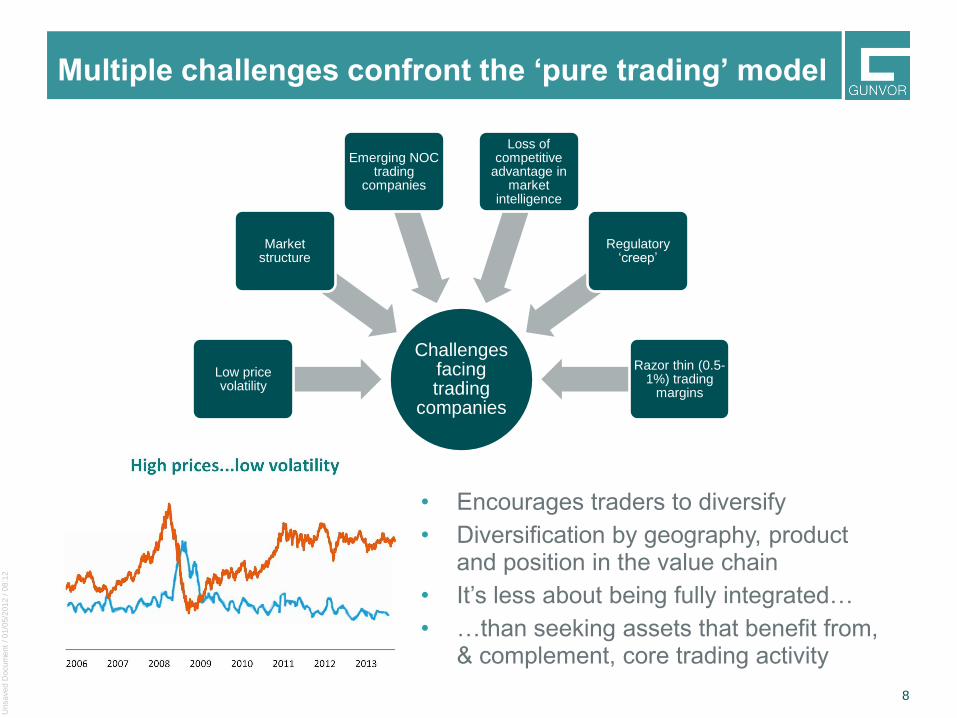

Multiple challenges confront the ‘pure trading’ model

Challenges facing trading

companies

Low price volatility

Market structure

Emerging NOC trading

companies

Loss of competitive

advantage in market

intelligence

Regulatory ‘creep’

Razor thin (0.5-1%) trading

margins

• Encourages traders to diversify

• Diversification by geography, product and position in the value chain

• It’s less about being fully integrated…

• …than seeking assets that benefit from, & complement, core trading activity

Unsa

ve

d D

ocu

me

nt

/ 0

1/0

5/2

01

2 /

08

:12

9

Gunvor: diversifying by product & geography

Asia & Middle East 20%

WesternEurope

North America

Latin America

AfricaAsia & Middle East 30%

Western Europe

North America

Latin America

Africa

2009: USD $50.4 bn 2012: USD $93 bn

Crude Oil

(60%)Fuel Oil

Gasoil

Gasoline

Naphtha

LPG Biofuel

Crude Oil

(30%)

Fuel Oil

Gasoil

NatGas +

LNG

Coal

Gasoline

Naphtha

LPG Biofuel

2009: 110 mn tons 2012: 130 mn tons

Revenue by region

Trading volumes

Unsa

ve

d D

ocu

me

nt

/ 0

1/0

5/2

01

2 /

08

:12

10

Gunvor strategy – integrating along the value chain

• Ust Luga Oil Products Terminal (Russia)

• Ust Luga Crude Pipeline (Russia)

• Karimun Products Terminal JV (Indonesia)

• Novorossiysk Fuel Oil Terminal (Russia)

• Petroterminal de Panama, S.A. (Panama)

• Independent Belgium Refinery BV (Belgium)

• Gunvor Raffinerie Deutschland GmbH (Germany)

• TAL Pipeline (Italy, Austria, Germany)

• Signal Peak (United States)

• LLC Kolmar (Russia)

• Keaton Energy Holdings Ltd (South Africa)

• Lagansky Block (Caspian Sea)

• PA Resources (North Sea, North and West Africa)

Midstream

Downstream

Upstream

Unsa

ve

d D

ocu

me

nt

/ 0

1/0

5/2

01

2 /

08

:12

11

Shift to assets + high prices = rising financing reqs.

• Surge in financing requirements met by either a) public flotation or b) recourse to public debt markets

• Most of the traders have preferred to retain the flexibility, speed of response and risk tolerance afforded by staying private

• But tapping the financial markets has seen trading houses open up to hitherto unprecedented financial and operational scrutiny

Public equity and debt offerings of physical commodity traders, $US billion

Source: First Reserve Corp 2013

?

Unsa

ve

d D

ocu

me

nt

/ 0

1/0

5/2

01

2 /

08

:12

12

Risk management at Gunvor

Commodity Price Risk

• Offset risks on multiple purchase & sale transactions

• 95%+ of physical is hedged

• Already mostly cleared

• VaR traditionally <<1% of equity

Liquidity Risk

• Diversified pool of banks

• Policy of gradually boosting liquidity reserve

Counterparty Risk

• >80% of customers are long-standing

• Conservative credit risk policy

• No material non-payment losses (<0.1% turnover)

Currency Risk

• Trades and borrowings primarily in USD

• Exceptions are gas/LNG, biofuels and operational expenses

Unsa

ve

d D

ocu

me

nt

/ 0

1/0

5/2

01

2 /

08

:12

13

Stretching supply chains and diverse price risks

• Price risk all along the supply chain

• Wellhead to petrol pump for crude & oil products can be anything from 20-90 days

• Risk management tools have to be flexible enough to cover a variety of crude and product qualities…

• …plus transport, storage, processing and blending complexities too

• Does the emerging, post-regulatory slate of risk management & financing tools provide the necessary flexibility?

source: EIG

Unsa

ve

d D

ocu

me

nt

/ 0

1/0

5/2

01

2 /

08

:12

14

Regulatory changes on top of competitive pressures

• The myth of ‘unregulated’ traders (70+ banks, exchanges, natl./intl. regulators)

• Environmental regulations augment existing competitive pressures on EU refining

• Evolving and diverse supply chains require flexible risk hedging tools

• Proposals for position limits, benchmarks/PRAs, swapsclearing, one-size-fits-all disclosure & risk management requirements all pose risks

• Issues: proportionality, recognition of market specifics, international consistency

• Risk of undermining participation, transparency, liquidity, physical market function and, ultimately, raising costs to energy consumers

• Laudable post-2008 G7/G20 policy goals to a) minimise systemic financial risk & b) encourage lower, stable energy prices – but these can sometimes be inconsistent

Unsa

ve

d D

ocu

me

nt

/ 0

1/0

5/2

01

2 /

08

:12

15

Trading houses: are they becoming too big to fail?

• “Commodity trading companies active in multiple markets have used easy access to finance to expand physical

holdings, creating potential ‘systemic’ risk” CEPS/ECMI

• 5 criteria for systemically important entities: large size, financial system interconnections, global reach, complex structure/difficult to unwind, difficult-to-replicate services

FSB consultation document, Jan 2014

• “Traders are less leveraged than banks, have smaller balance sheets, largely short-term liabilities, are not major

providers of credit, and their assets are re-deployable” Pirrong/Trafigura study 2014

• “As highlighted by the collapse of Enron, one of the largest energy trading companies of its time, physical traders are highly unlikely to pose systemic risks - their positions are largely physical, hedged, liquid and short-term. Trading

houses should be allowed to fail and, when they have, there has been little or no disruption to the orderly functioning of

markets or the supply of commodities.” Vitol, 2013

Unsa

ve

d D

ocu

me

nt

/ 0

1/0

5/2

01

2 /

08

:12

16

B) THE OIL & ENERGY MARKET BACKGROUND

Unsa

ve

d D

ocu

me

nt

/ 0

1/0

5/2

01

2 /

08

:12

17

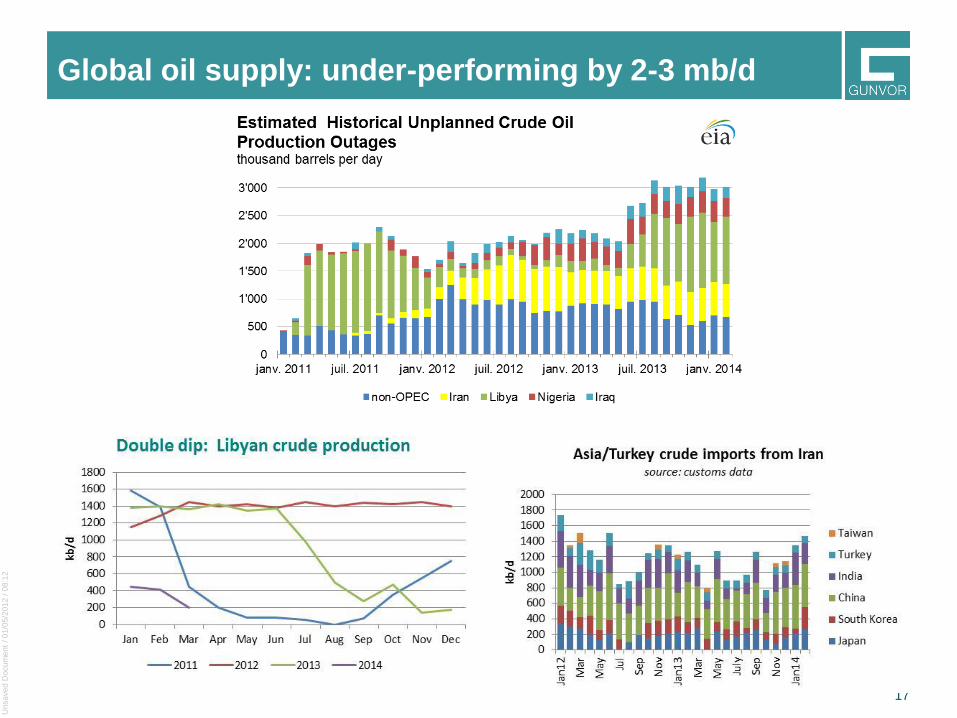

Global oil supply: under-performing by 2-3 mb/d

Unsa

ve

d D

ocu

me

nt

/ 0

1/0

5/2

01

2 /

08

:12

18

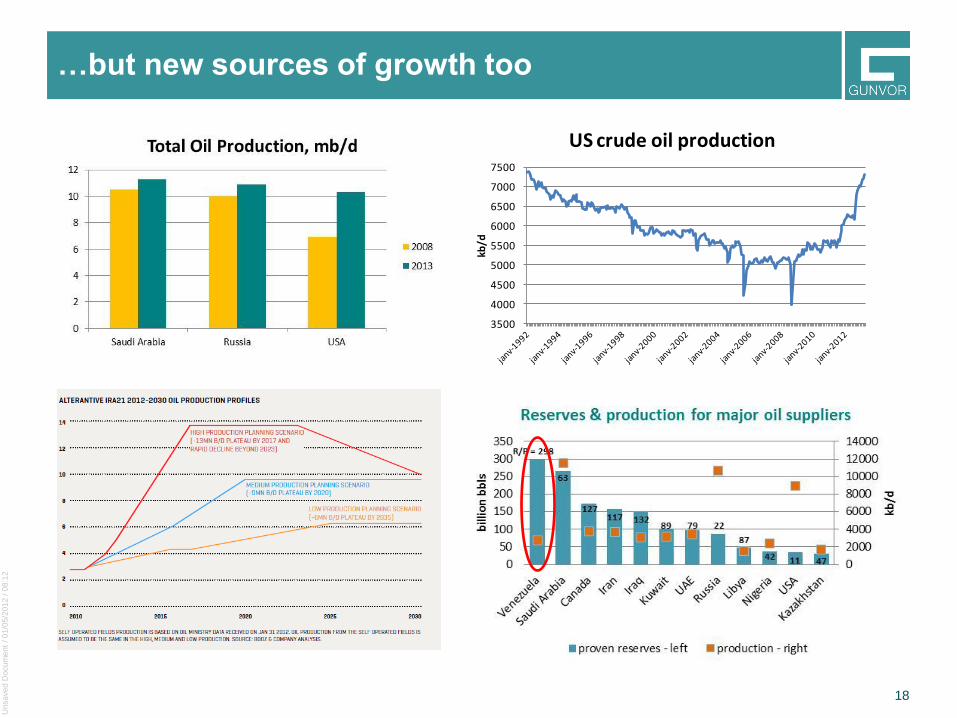

…but new sources of growth too

3500

4000

4500

5000

5500

6000

6500

7000

7500

kb/d

US crude oil production

Unsa

ve

d D

ocu

me

nt

/ 0

1/0

5/2

01

2 /

08

:12

19 19

US shale oil: mixed views on sustainability of growth

Plus points for major growth:

• Resource & reservoir behaviour becoming better understood

• Transport infrastructure is being built-out, belatedly

• High up-front cash flow continues to drive investment if prices stay robust, & there’s scope for cost reduction

• Infill drilling & well spacing improvements

• Technology – pad drilling & longer laterals

Risks:

• Energy security concerns impede decisions on export policy, logistics

• Macro-slow down, oil price risk & refinery tolerance if exports restricted

• Sweet spots targeted first, so yields could fall & costs could also rise

• Sufficient skilled workforce & supply chain resilience?

• Tighter env.reg. – flaring/fracking/rail restrictions, access to Federal lands

• Types of operators & availability of finance – nb rising interest rates

Light tight oil will continue to grow, but more slowly

Unsa

ve

d D

ocu

me

nt

/ 0

1/0

5/2

01

2 /

08

:12

20

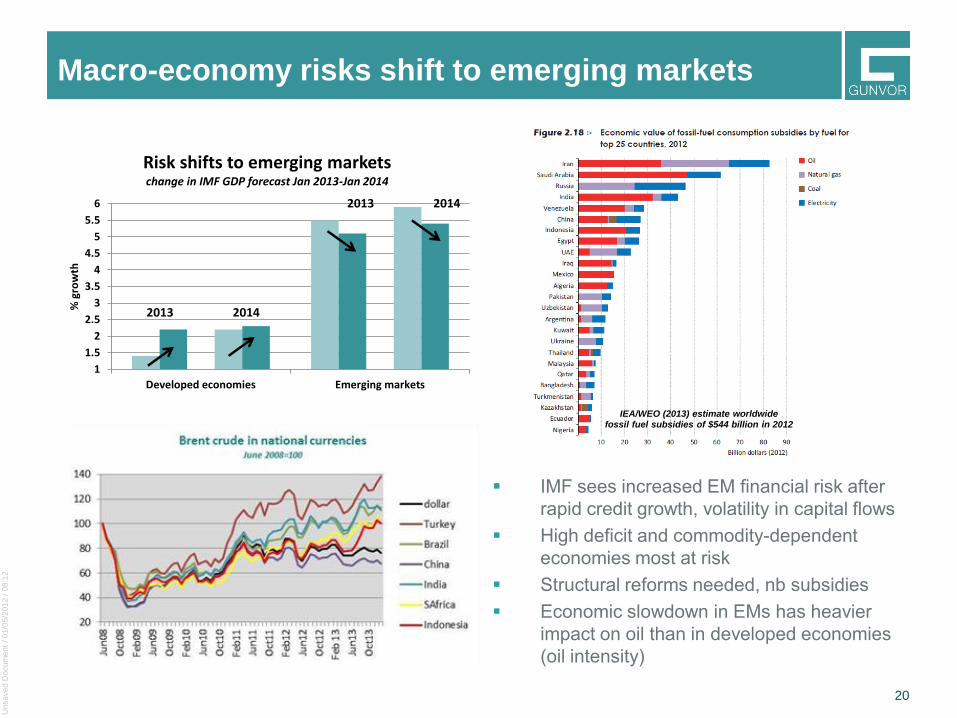

Macro-economy risks shift to emerging markets

1

1.5

2

2.5

3

3.5

4

4.5

5

5.5

6

Developed economies Emerging markets

% g

row

th

Risk shifts to emerging marketschange in IMF GDP forecast Jan 2013-Jan 2014

2013 2014

2013 2014

IEA/WEO (2013) estimate worldwide fossil fuel subsidies of $544 billion in 2012

IMF sees increased EM financial risk after

rapid credit growth, volatility in capital flows

High deficit and commodity-dependent

economies most at risk

Structural reforms needed, nb subsidies

Economic slowdown in EMs has heavier

impact on oil than in developed economies

(oil intensity)

Unsa

ve

d D

ocu

me

nt

/ 0

1/0

5/2

01

2 /

08

:12

21

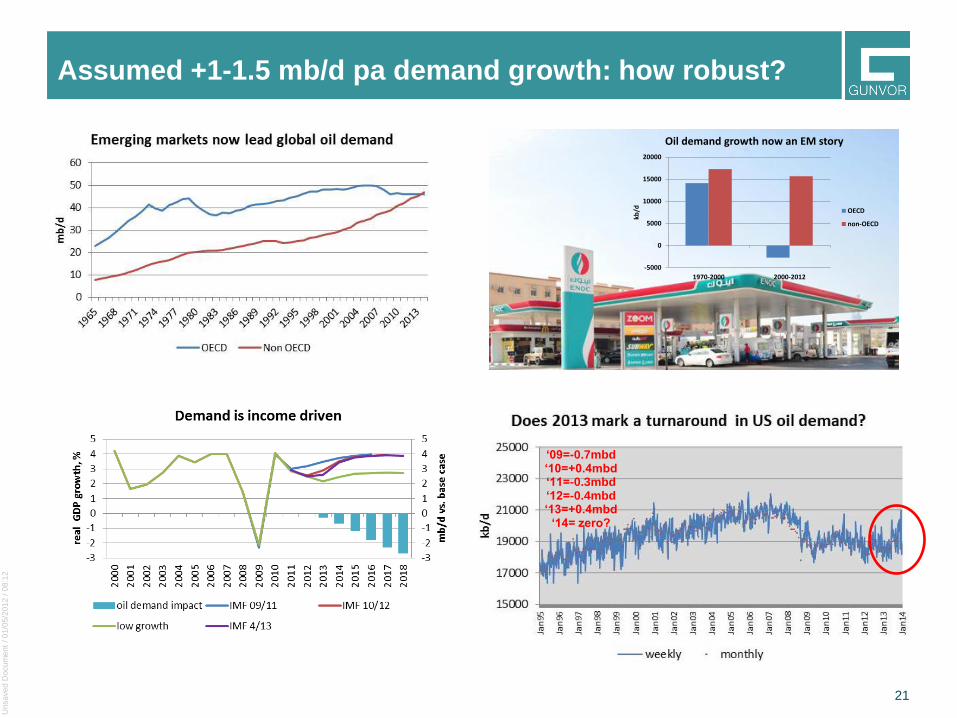

Assumed +1-1.5 mb/d pa demand growth: how robust?

-5000

0

5000

10000

15000

20000

1970-2000 2000-2012

kb/d

Oil demand growth now an EM story

OECD

non-OECD

‘09=-0.7mbd ‘10=+0.4mbd ‘11=-0.3mbd ‘12=-0.4mbd ‘13=+0.4mbd

‘14= zero?

Unsa

ve

d D

ocu

me

nt

/ 0

1/0

5/2

01

2 /

08

:12

22

Challenging refining environment, notably in Europe

Unsa

ve

d D

ocu

me

nt

/ 0

1/0

5/2

01

2 /

08

:12

23

But midstream & downstream opportunity too

• Distressed European refining assets: integrate with trading, and optimise

• New refining hubs (N.America, Mid.East), India & China also emerge as key exporters

• Global products trade growing faster than crude, much of it on new, long haul routes

• Products tanker order book is rising (86% of new orders in 2013)

• Opportunities for refiner-traders: access to flow, flexible operations, diversified arbitrage opportunities, aggressive hedging strategy

Teesside

Grangemouth

(Petrochina)

Stanlow:

Essar -> Shell

Milford Haven

WhitegateCoryton

Gothenburg:

Shell -> St1

Harburg

Heide:

Shell -> Klesch

Wilhelmshaven

Vlissigen (Lukoil)

Gonfreville-l’Orcher

Antwerp: Petroplus -> Vitol; Petroplus GunvorGelsenkirchen (Rosneft)

Dunkirk

Ingolstadt:

Petroplus -> Gunvor

Karlsruhe (Rosneft)

Lavera (Petrochina)

Berre-l’Étang

ReichstettPetite-Couronne

Priloi & Melilli (Lukoil)

Milazzo (Kuwait Petroleum)Saras

(Rosneft)

Rome

Cremona

Cressier

Petroplus -> Vitol

Ballshi

Fieri

Szazhalombatta

(Surgutneftegaz)

Brod (Zarubezneft)

Novi Sad (Gazprom)

Pancevo (Gazprom)

Gibraltar

(IPIC)

Huelva

(IPIC)

Capacity

ReductionTerminal

Closure For Sale

Sale

(Part)Owned Russian/Indian/

Chinese/ Middle Eastern

Burgas (Lukoil)

Mantova

Unsa

ve

d D

ocu

me

nt

/ 0

1/0

5/2

01

2 /

08

:12

24

How long will range-bound prices persist?

• Macro-economic uncertainty and geopolitical risk/supply outages providing price ceiling & floor

• Market ‘colour’ coming from other, sometimes highly specific, policy-related events

Unsa

ve

d D

ocu

me

nt

/ 0

1/0

5/2

01

2 /

08

:12

25

Costs & IOC/state reqs. provide price floor

• US light tight oil, ‘big-ticket’ IOC upstream developments and OPEC budgets all require prices at or above $80/bbl

• Long dated Brent steady in $85-$95/bbl range, leaving front of the curve to oscillate in a $100-$120 range

Saudi Arabia budget break-even prices Source: Credit Suisse

Unsa

ve

d D

ocu

me

nt

/ 0

1/0

5/2

01

2 /

08

:12

26

Gas markets remain regional, globalising slowly

source: IGU, 2014

Unsa

ve

d D

ocu

me

nt

/ 0

1/0

5/2

01

2 /

08

:12

27

Coal challenged, but won’t disappear overnight

Source: IEA World Energy Outlook, 2013

source: ExxonMobil, Energy Outlook 2013

Which sector drives future energy demand growth?

Unsa

ve

d D

ocu

me

nt

/ 0

1/0

5/2

01

2 /

08

:12

29

Benchmark imperfections, but resistance to change

What makes a good oil

benchmark

No resale restrictions

No dominant buyer or

seller

Aligned with fiscal regime

Can it be hedged? Stable

domestic political regime

Infrastructure for exports &

arbitrage

Physical liquidity

Unsa

ve

d D

ocu

me

nt

/ 0

1/0

5/2

01

2 /

08

:12

30

Changing oil demand dynamics