oilvoice magazine - edition 42 - september 2015

DESCRIPTION

August has been another interesting month within our industry with some highs and somelows. We saw oil price go down into the low 40s, the largest field discovered in the NorthSea in 10 years approved for development, and plenty money exchanging hands in both exploration and production deals.But what are people talking about?- One can imagine that the main topics over a pint are currently dominated by the possibility of China heading into a recession, and the large amount of refugees gaining or trying to gain access into the Eurozone. Why not add some oil production statistics into the conversation mix instead by checking out Euan Mearns incredibly interesting article in this month’s magazine on “Oil Production Vital Statistics August 2015”.This is just one of many entertaining and informative articles in this month’s OilVoice Magazine. And if that doesn’t excite you or fulfil your desire to learn something new then check out the OilVoice Training Page for more details on a wide range of courses that will be run from now until November.TRANSCRIPT

Edition Forty Two - September 2015

OPEC's Gigantic Blunder

The oil price: how low is low?

Sunset for oil? You must be kidding, surely?

Issue 42 –August 2015

OilVoice Acorn House 381 Midsummer Blvd Milton Keynes MK9 3HP Tel: +44 207 993 5991 Email: [email protected] Advertising/Sponsorship Mark Phillips Email: [email protected] Tel: +44 207 993 5991 Social Network

Google+

Linked In

Read on your iPad You can open PDF documents, such as a PDF attached to an email, with iBooks.

Adam Marmaras

Manager, Technical Director

August has been another interesting month

within our industry with some highs and some

lows. We saw oil price go down into the low

40s, the largest field discovered in the North

Sea in 10 years approved for development,

and plenty money exchanging hands in both

exploration and production deals.

But what are people talking about?- One can

imagine that the main topics over a pint are

currently dominated by the possibility of China

heading into a recession, and the large

amount of refugees gaining or trying to gain

access into the Eurozone. Why not add some

oil production statistics into the conversation

mix instead by checking out Euan Mearns

incredibly interesting article in this month’s

magazine on “Oil Production Vital Statistics

August 2015”.

This is just one of many entertaining and

informative articles in this month’s OilVoice

Magazine. And if that doesn’t excite you or

fulfil your desire to learn something new then

check out the OilVoice Training Page for more

details on a wide range of courses that will be

run from now until November.

See you next month!

Adam Marmaras

Managing Director OilVoice

Let’s turn on the light.Look more closely at your basement with NEOS and discover what might be lurking below. Through multi-physics

imaging, NEOS maps variations in basement topography, composition and faulting, any of which can affect field

locations, EUR, or the level and BTU content of production. By illuminating your basement and seeing below the

shale, you’ll better understand thermal regimes and pinpoint where to drill for optimal recovery and economics.

Some of the world’s leading geoscientists are making brighter decisions with NEOS. Be the next.

Above, Below and Beyond neosgeo.com

YOUR BASEMENT IS FULLOF DARK SECRETS.

5

5

Table of Contents

OPEC's Gigantic Blunder by Euan Mearns

6

Sunset For Oil? You Must Be Kidding, Surely? by John Richardson

12

The North Sea isn't dead, it's just resting. by Stephen A. Brown

17

When Will Oil Prices Turn Around? by Art Berman

20

What is the price of oil telling us? by Kurt Cobb

30

Oil Prices: Why We Are Where We Are Today by John Richardson

33

The Oil Price: how low is low? by Euan Mearns

35

How Did the Oil & Gas Majors Perform in Early 2015? by Mark Young

40

Tullow Oil boss Heavey predicts oil price will hit $75 a barrel by year end by John Mulligan

44

6

6

OPEC's Gigantic Blunder

Written by Euan Mearns from Energy Matters With WTI falling below $40 and perhaps heading for $20, one needs to wonder if

OPEC's strategy is working out as planned? Why are they following this course and

what are their goals? The face value explanation, accepted by many, is that OPEC is

protecting market share especially against rampant supply growth in the OECD,

namely in the US LTO (light tight oil) patch. This post examines how OPEC's market

share has evolved with time and with past swings in the oil price.

This turned out to be more complex than expected. But scrutiny of the data shows

that following each of the three oil shocks since 1965 (Figure 1) OPEC market share

AND oil price fell (Figure 3). The most recent trend follows the 2008-2014 highs and I

believe it is this observation that is driving current behaviour.

Had OPEC decided to sacrifice about 5% market share they could have maintained

price above $100 per barrel for years to come in which time the US shale bonanza

may have burned out. It seems that OPEC may have made a colossal error that

threatens to de-stabilise their member countries. This post originally appeared on

the Energy Matters blog.

Figure 1 OPEC market

share is simply OPEC

production / global

production. It is very

difficult to make sense of

the data from this plot. In

Figure 2 the variables are

cross plotted against

each other which does

enable some sense to be

made. Shock 1 = Yom

Kippur, Shock 2 = Iranian

revolution and Shock 3 =

peak cheap conventional

oil.

7

7

Figure 2 This chart cross plots the two variables shown in Figure 1. It should be

obvious that there is no overall correlation between OPEC market share and price.

The chart is a time series that needs to be read in a counter clockwise direction

beginning in 1965. The arrow 2014 to today is conceptual since I do not have the BP

C+C+NGL YTD data available. The arrow shows a very slight increase in OPEC

share since their production has risen this year. The trends are summarised in

Figure 3. The picture is clouded by the 2008/09 crash. These years are labelled 08

(8) to 14 (4). See text for further details.

Cross plotting market share against price produces a curious pattern which is a time

series that describes different market behaviour for different time segments (Figures

2 and 3). To read the plot you have to begin in 1965 and work your way around in a

counter clockwise direction. Note that by 1992-2003 the market had almost gone full

circle. The period 1965 to 2003 is marked by two major events - the Yom Kippur war

and the Iranian revolution that was followed by the Iran-Iraq war. Combined, these

two shocks sent the oil price over $100 / bbl. The period 1979 to 2003 may be

viewed as one of relaxation and adjustment back to the starting point. Post 2003 a

new ball game began with a plateau in cheap conventional oil production. Using pre-

2003 behaviour to predict what might happen now is likely a major mistake!

8

8

OPEC's market share has varied enormously from a high of 51.2% in 1973 that

coincided with low price and a low of 27.6% in 1985 that coincided with an

intermediate price of $60 / bbl.

Figure 3 Summary of the trends evident in Figure 2.

There are three periods when OPEC enjoyed rising market share. The first, 1965 to

1973 had essentially flat prices. The second, 1985 to 1992 saw market share rising

against a backdrop of falling price. The third, 2004 to 2014 saw OPEC market share

increase marginally against a backdrop of rapidly rising prices.

The three cycles of rising market share are cancelled by three cycles of falling

market share AND falling price. Each of these cycles occur after oil price shocks and

OPEC therefore found itself in the early stage of such a cycle in 2014.

If one looks at prior falling share cycles, 1974 to 1978 was not that bad for OPEC.

They lost 5% market share and the oil price shed $5. The second falling share cycle,

1979 to 1985, saw market share fall 18% (39% in relative terms) and price fall by

9

9

$45. This was truly a bad period for OPEC and I dare say it is this that Saudi Arabia

wants to avoid this time. This period also witnessed global oil demand in decline as

the global economy adjusted to the sharply higher oil price. Hence at this time OPEC

were getting a smaller share of a smaller pie. The third falling share cycle, 2008-

2014 has seen market share fall a trivial 2.5% and price fall about $8 from record

highs. And in this period most OPEC countries have been pumping at capacity and

at record combined levels over 36 M bpd C+C+NGL. 2008-2014 has been an

amazing pink patch for OPEC, too good to be true and too good to last.

Have OPEC just made a gigantic blunder?

Has the current OPEC strategy of flooding the market with their cheap oil turned out

as planned or has it turned into a gigantic blunder? Figure 4 shows schematically

three scenarios and alternative courses that may have been followed. The first is

where we were heading. With the flood of oil that has come to market in 2015

combined with weak demand it is likely that OPEC would have had to cut production

incrementally to have maintained the trajectory of slowly falling share and price.

Scenario 2 shows what might have happened with a continuation of recent policy of

supporting price. Trimming 4 M bpd from production (5% share) incrementally may

have maintained prices of $100 / bbl. Scenario 3 shows what has come to pass and

where we are heading.

Figure 4 Three

conceptual scenarios

for different courses of

action that OPEC may

have followed.

10

10

I think it is safe to presume that, with the benefit of hindsight, OPEC's preference

would be within the vicinity of the 2008-2014 cluster. At present it therefore looks like

OPEC have made a gigantic blunder. Their actions can only be vindicated if they do

manage to break the back of the US LTO producers and other OECD and non-

OECD producers like Gazprom and to some time soon end up with significantly

increased share and price. Since OPEC is already pumping flat out, the only way to

significantly increase share is if global production falls. This would herald another

global recession since GDP and oil consumption are generally correlated.

Had OPEC pursued option 2 they may have benefited from unpredictable global

events working in their favour. In choosing option 3 they now appear to have elected

economic suicide for many members. I'm sure that was not the intention.

What happens next? I believe that OPEC and Russia will hang tough for a while yet,

until at least US oil linked debts are re-determined at the end of the third quarter. The

outcome of that is in itself uncertain. While most predict a blood bath in the LTO

patch, and I am not disagreeing that this is likely, strategic events are unpredictable.

There is much hubris involved on both sides. Will the USA really sit back and watch

its shale industry get kicked into the long grass?

Near term I think it likely we see WTI flirt with $20 and Brent below $30. At that point

the global oil industry will be on its knees, including OPEC, the OECD and Russia.

Russia may then either join or form an alliance with OPEC and we then see

production cuts, incrementally up to 4 Mbpd and the price rise back towards that

magic $100 / bbl number. I think it is safe to say that the oil industry and global

economy are equally focussed on stability as they are price and many will be asking

what was the point? Meanwhile, in an increasingly meta-stable world, events may

sweep all this into oblivion.

Finally, a concluding thought. Had OPEC defended price as opposed to share they

may have seen production fall by 5 M bpd and a price close to $100 maintained. The

current course of defending 36 M bpd may take the oil price down to $20.

11

11

32 M bpd @ $100 is worth $1168 billion per year

36 M bpd @ $20 is worth $263 billion per year

The difference of $905 billion per year could make this one of the costliest blunders

of all time.

Figure 5 The notional value of OPEC production calculated by multiplying daily

production by price by 365.

All data from the 2015 BP Statistical Review.

View more quality content from

Energy Matters

12

12

Sunset For Oil? You Must Be Kidding, Surely?

Written by John Richardson from ICIS SURE, you can very easily argue that the oil industry is many, many decades away

from going down the same path as the coal industry, where, in countries such as the

US, it is going bankrupt.

The biggest case for oil's longevity is its role in transportation, it is altogether from

different coal, which has mainly lost out to cleaner-burning natural gas in power

generation. Coal does not have any role in the transportation sector, with the

exception of just about only China where they turn coal into diesel and gasoline. And

even China makes most of its transportation fuels from crude.

(By the way, I will look at natural gas in a separate blog post as the arguments

around its future are a little different).

And for over one hundred years now, oil has been tightly bound into global

transportation. This has left us with billions of dollars' worth infrastructure investment

in pipelines and refineries etc. that would have to be replaced at an enormous cost if

you were to make a significant switch from gasoline and diesel to, say, natural gas or

battery-powered vehicles.

This is assuming, of course, that it is even worth considering replacing all this

infrastructure. Before this can even be thought about, we would have to find

alternatives to oil in transportation that a.) We could produce in the enormous

volumes needed and b.) At a cost that makes global economic sense.

Here are a couple of other objections to the idea that oil is anywhere close to being a

sunset industry, and I am sure you can think of many more:

What about all the jobs that would be lost in the oil industry. What would you

do with all these people?

13

13

And how would the innovators overcome political resistance from the oil and

autos companies that benefit so enormously from the hydrocarbons-driven

global economy? 'Big Oil' in the US will not role-over and die. Of course not.

Neither will the petro-states of the Middle East, Africa and elsewhere, which

rely hugely on oil for the very economic survival.

The above arguments took me just a few minutes to summarise because they are

part of our shared understanding. We all know them, probably as well as we know

the old nursery rhymes we were taught in school.

But shared understanding isn't the always the same as the truth, as we have found

out with China very recently. The shared understanding on China was that its

economy would never suffer a serious, long-term downward correction. This has

been proved wrong.

And with oil, where there is an economic will there might just be a way, as a

Financial Times interview with Bill Gates in June of this year indicated:

As a parting shot Mr Gates compared the search for renewable technologies with the

early days of the technology industry and predicted that some investors would make

a lot of money by backing companies that would one day be successful.

'If I came and talked to you about software in the late 1970s, I would tell you: 'Hey,

somebody's going to make a lot of money. Now there's a tonne of software

companies whose names will never be remembered. . . If you happened to pick

Microsoft, Apple or Google, you would have made lots of money.'

Mr Gates, in the same article, urged governments to switch more resources from

subsidising renewable energy into basic research. At present, government subsidies

amounted to more than $100 billion with only $6 billion a year being invested in

renewable energy R&D, he said.

Hence, his belief is that if this happens major new global companies will emerge

from nowhere, just as Google did from 1998 onwards.

One the examples of new technologies that he gave is something called solar-

chemical power. If successful, this technology would actually piggy-back on oil

pipelines and gasoline tanks inside existing cars So there potentially goes the

14

14

infrastructure objection to the 'Sunset for Oil' theory.

And what if we can find ways of storing electricity much more effectively? This would

make both solar and wind power and electric cars much more viable. Research here

includes looking at ways of using capacitors, or electrical fields to store power.

Another way to go could be to replace today's lithium-ion batteries with, say,

magnesium-ion batteries.

Here is another 'what if'. What if another new technology - Driverless cars - really

takes off? This could reduce the volume of traffic on the roads by as much as 90%

as most of us would be want to rent or lease a car, per ride, than actually own one.

I also mentioned above how the autos companies would fight against the end of oil.

But if driverless cars really do take hold, auto companies as we know them might not

even be around anymore. Luis Martinez of the International Transport Forum, a

division of the OECD, told The Economist:

The value in carmaking will shift from hardware to software and from products to

services. That would shake existing carmakers, just as smartphones upended Nokia

and Kodak. Already, high-tech newcomers such as Google, Uber and Tesla are

muscling in.

Bill Gates is backing his words with his money: He plans to double his investment in

renewable energy research from $1bn and $2bn over the next five years.

'No disrespect to Mr Gates as he is a brilliant man, but this is chickenfeed in terms of

the overall money that will be needed to replace oil,' I can here you say.

True, but Mr Gates and others like him have the economic will to make these

relatively small investments because they sense there has been a huge change in

the political will. Thus, the returns on their investments could be equally big.

The climate change debate is essentially over, whether you like it or not.

Governments the world over believe that humans are the cause of climate change.

So they will be taking a close look at numbers such as these, which were

published in an IMF report released in May of this year:

15

15

Post-tax fossil fuel subsidies are dramatically higher than previously

estimated—$4.9 trillion (6.5% of global GDP) in 2013, and projected to reach

$5.3 trillion (6.5% of global GDP) in 2015.

Post-tax subsidies are large and pervasive in both advanced and developing

economies and among oil-producing and non-oil-producing countries alike.

The fiscal, environmental, and welfare impacts of energy subsidy reform are

potentially enormous. Eliminating post-tax subsidies in 2015 could raise

government revenue by $2.9 trillion (3.6% of global GDP), cut global CO2

emissions by more than 20%, and cut pre-mature air pollution deaths by more

than half. After allowing for the higher energy costs faced by consumers, this

action would raise global economic welfare by $1.8 trillion (2.2% of global

GDP).

So much therefore for the argument that moving away from oil would be too

damaging for the global economy.

You can instead easily make the opposite argument that the shift would create many

new jobs in new industries, whilst also potentially reducing the enormous economic

costs of climate change, if by shifting from oil, in transportation and everything else,

we can minimise the rise in global temperatures.

This shift might also limit the human cost of climate change that right now is set to be

mainly borne by the world's poorest people as they often live in equatorial regions. It

is these equatorial, or tropical, regions that are most at risk from rising sea levels and

droughts.

Do you still dismiss all of this as nonsense? So be it, but the move away from an oil-

driven global economy could happen a lot quicker than many people think. It is a

scenario that any oil or chemicals company planner with a 20 or even ten-year

horizon must consider.

And here's the thing: As we move towards a potentially ex-oil economy, what will this

mean for the demand growth for oil over the next five years, if you only think in

much-shorter timeframes?

View more quality content from

ICIS

*Replica of original published data

Landmark

Joining up the exploration process

Unlocking a region’s full hydrocarbon potential requires a comprehensive understanding of subsurface structure. The Neftex Regional Frameworks Module delivers unique, isochronous depth grids for key stratigraphic surfaces, bringing vital insight into mega-regional depth structure trends.

As the first Neftex offering deliverable in Landmark’s DecisionSpace® Geosciences software, the module provides a robust framework into which proprietary data can be dynamically added. This forms a powerful basis for essential play analysis on a regional scale.

Support faster, more integrated exploration

Contact us today: Website: www.neftex.com Halliburton I Landmark: www.landmarksoftware.com Email: [email protected] Tel: +44 (0)1235 442699 LinkedIn: linkedin.com/company/Neftex Neftex • 97 Jubilee Avenue • OX14 4RW • UK

17

17

The North Sea isn't dead, it's just resting.

Written by Stephen A. Brown from The Steam Oil Production Company Ltd

I wrote before about my calculations of the breakeven point for some recent and

some upcoming North Sea projects, but time marches on and cost estimates and

reserve estimates change so I thought it worth updating the picture.

I am doing this calculation with publicly available data, so I doubt that I will have

been able to make a truly accurate calculation, or one that matches company's

internal estimates, or even the published CPR estimates. Part of that will be down to

data availability and part will be down to the methodology I chose. For simplicity, I

discount the production profile and the operating costs, but I don't bother discounting

the capital costs as it is only rarely that I can lay my hands on how those capital

costs are phased. That means the breakeven price I calculate will be higher than it

should be, but my method has the virtue that I can apply it to projects where the only

data I have is a production profile (check out the Environmental Statements for those

if there isn't a CPR) and a total capital cost; operating costs can always be estimated

at 4% of capex per annum.

The other consequence of that simplification is that it sets the bar a little higher than

just making a return that is equal to the theoretical cost of capital, so I could make a

case that the breakeven value I calculate is more realistic, if you think of it as a

hurdle oil price for the project. But the main reason I do it the way I do is so that I can

do the calculation for as many projects as possible.

So here is an updated chart with the projects ranked by breakeven price. A few

investments that made sense when the oil price was $110/bbl aren't looking quite so

good now, but we don't know to what extent the operators of those projects can add

incremental reserves or squeeze some costs out of the system. It is very hard to

18

18

change the cost of something you have already built or are in the middle of building,

but a few extra barrels could help some of those projects a lot. For clarity, these are

pseudo-project economics not company economics which can often look a lot better

(or worse) depending on acquisition or farm-in or farm-out arrangements.

At today's price of just under $50/bbl it is hard to see any new project getting off the

blocks, and with the long run price now under $70/bbl it will be a brave company or

financier that pulls the trigger on a project. But I firmly believe that those will be the

companies or financiers that will reap rewards in the long run. BP, LASMO et al

sanctioned the Andrew development project on a day when the oil price had fallen to

$12/bbl, they reaped the rewards in lower costs during construction and higher oil

prices when the field actually came on stream; but on the day that the final

investment decision was taken the outlook couldn't have been bleaker.

19

19

Getting a development project across that final investment decision hurdle will, in

many cases, require a radical rethink of what the project looks like and how the

project gets implemented. That is just what we did on the Andrew project, we took

six months out to reshape the project before we went for the final investment

decision, the plant had been designed to produce 45,000 bbls/day, but with the

horizontal wells we had planned the well capacity was quite a bit better so we

debottlenecked the plant before we built it and realised we could handle nearly

60,000 bbls/day. The structural engineers did their bit too, when they established

that we could securely fasten the platform to the seabed with 12 piles not the original

16 we had planned.

That is the kind of process which can drive costs out of a project but the best way to

drive down the breakeven cost per barrel is to find a way to squeeze (or steam) more

barrels out of the field. Engineering ingenuity runs out of road eventually and

pressuring your contractors only goes so far (if it goes anywhere at all).

Finding a way to produce the extra barrels that will make MER:UK (that's Maximising

Economic Recovery in the UK for those who don't read the Wood report every day) a

reality will take innovation and fortitude, cutting costs will

take ingenuity and collaboration, but we have the capability to do that in the UKCS,

of that I am sure.

That's why I say the North Sea isn't dead, it's just resting. Sadly, I'm afraid that

Norwegian Blue's a goner.

View more quality content from

The Steam Oil Production Company Ltd

20

20

When Will Oil Prices Turn Around?

Written by Art Berman from The Petroleum Truth Report Look for some good news about oil prices this week...maybe.

EIA releases its Short-Term Energy Outlook (STEO) on Tuesday (August 11) and

IEA publishes its August Oil Market Report (OMR) on Wednesday (August 12). I

hope to see a small increase in world demand and relatively flat supply. That will

bring the market somewhat closer to balance and prices may increase or, at least,

stop falling.

Meanwhile, the view among most analysts is grim. On Monday, The Wall Street

Journal's Money & Investing headline read 'No Relief in Sight for Crude: Oil's

Malaise could last for years.' In late September, Bloomberg wrote, 'Oil Warning: The

Crash Could Be the Worst in More Than 45 Years.' As recently as mid-June,

analysts were confident that oil prices were rebounding toward 'normal' because

both Brent and WTI had risen from low $40- to low-$60 levels.

When many were celebrating a return to higher prices, I warned that prices would

fall. Now, when most are proclaiming lower oil prices ahead, I am looking for a

bottom to the price slump.

Don't get me wrong: this is not going to be anything dramatic but, if I'm right, it will

add another month of data that suggests flattening production and increasing

demand.

I have not changed my view that we have crossed a boundary and things are

fundamentally different than before. My colleague Rune Likvern published a post

today that details the key reasons why this substantive market shift has occurred.

As I wrote in late June, the world is a fundamentally different place post-the 2008

Financial Collapse and some markets, including oil, no longer respond as they did

before. This is a function of even more massive debt than prior to the Collapse and

monetary policies that have sustained artificially low interest rates for 6 years. Cheap

money has fostered the expansion of oil and other commodity supplies beyond the

21

21

weakened global economy's capacity to absorb them. Also, the anticipated de-

leveraging of debt has not occurred.

Market Fundamentals

So, where are we today?

Oil prices have fallen about 25% from May and June highs (Figure 1). The

exuberance of rising prices in March and April has given way to a view that prices

may continue to fall and may remain low for years or decades.

Figure 1. Crude oil spot prices, January 1-August 3, 2015. Source: EIA and Labyrinth

Consulting Services, Inc.

WTI futures closed at $43.87 on Friday, August 7, almost at the previous low during

this price cycle of $43.39 on March 17. Brent futures closed at $48.61 on August 7,

still a few dollars above its previous low of $45.13 on January 13.

It seems reasonable that oil prices may have fallen to or at least near some natural

22

22

bottom.

Traders are looking for hope that tight oil production will decline. IEA data showed

that U.S. production fell 50,000 bopd in June (Figure 2). Assuming that OPEC over-

production is partly aimed at reducing U.S. tight oil production, that process seems to

have finally begun, albeit in a small way so far.

Figure 2. IEA top producers monthly liquids production change, June 2015. IEA and

Labyrinth Consulting Services, Inc.

The problem continues to be over-supply coming mostly from OPEC whose

production increased 340,000 bpd in June (Figure 2).

Although there are positive indicators for demand growth for gasoline in the U.S. and

China, production growth has continued to outpace increases in demand. The

production surplus (supply minus demand) in the second quarter 2015 grew more

than 1 million bpd compared to the first quarter (Figure 3).

23

23

Figure 3. World liquids production surplus or deficit comparison, EIA vs. IEA. Source:

EIA, IEA and Labyrinth Consulting Services, Inc.

That is what must change in order for prices to turn around. The fact that IEA and

EIA estimates vary by almost 700,000 bpd shows that there is considerable

uncertainty in the data.

We may get better resolution by using EIA monthly data rather than IEA quarterly

data. EIA shows that the production surplus in June declined 1.2 million bpd

compared to May to 1.9 million bpd (Figure 4).

24

24

Figure 4. World liquids production, consumption and relative production surplus or

deficit. Source: EIA and Labyrinth Consulting Services, Inc.

This is because world demand reached a new high of 93.86 million bpd, an increase

of 1.3 million bpd over May. Another month of demand growth and slowing

production growth might go a long way towards turning prices around.

Second Quarter 2015 Earnings

Pessimism increased about oil prices last week as second quarter earnings for U.S.

E&P companies were released. Many tight oil producers including Pioneer, Whiting

and Devon announced higher production guidance for 2015. Others, however,

like EOG andSouthwestern Energy said they would continue to show restraint in

production until prices improved.

Despite ongoing macho declarations from tight oil company executives that they

are winning the war against Saudi Arabia and OPEC, the truth is that second quarter

results were pretty awful, and that is good for oil prices because it may signal falling

future production.

25

25

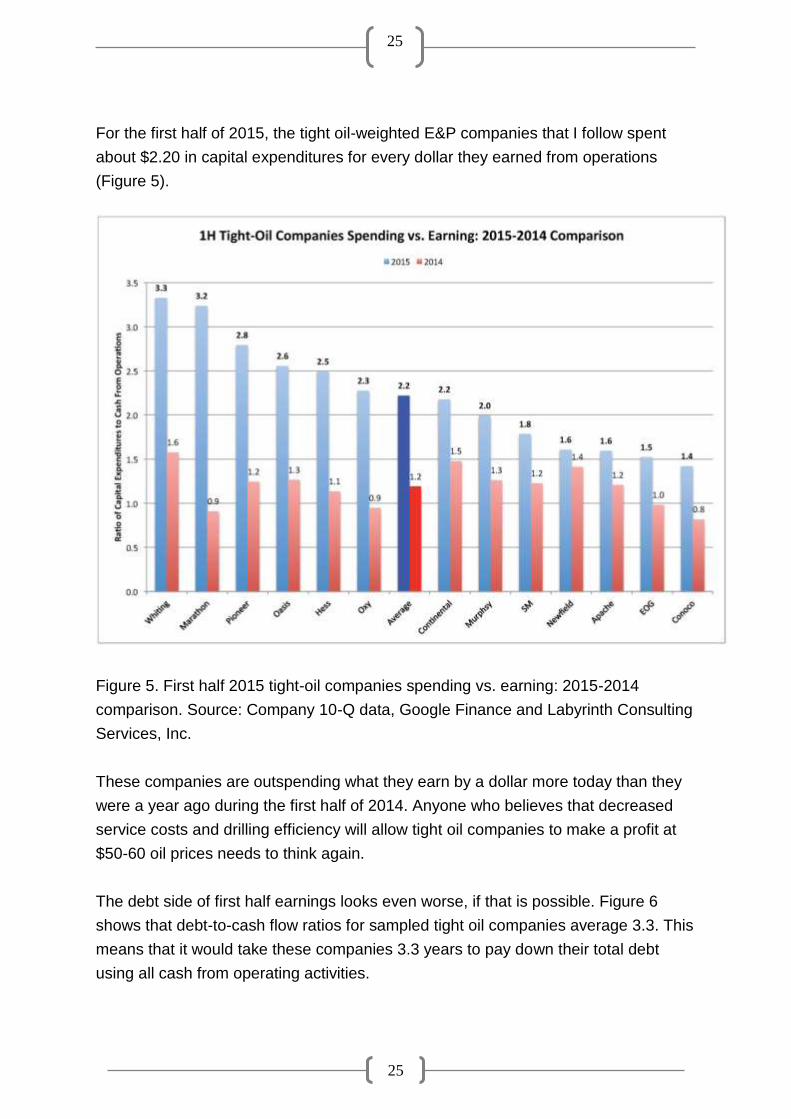

For the first half of 2015, the tight oil-weighted E&P companies that I follow spent

about $2.20 in capital expenditures for every dollar they earned from operations

(Figure 5).

Figure 5. First half 2015 tight-oil companies spending vs. earning: 2015-2014

comparison. Source: Company 10-Q data, Google Finance and Labyrinth Consulting

Services, Inc.

These companies are outspending what they earn by a dollar more today than they

were a year ago during the first half of 2014. Anyone who believes that decreased

service costs and drilling efficiency will allow tight oil companies to make a profit at

$50-60 oil prices needs to think again.

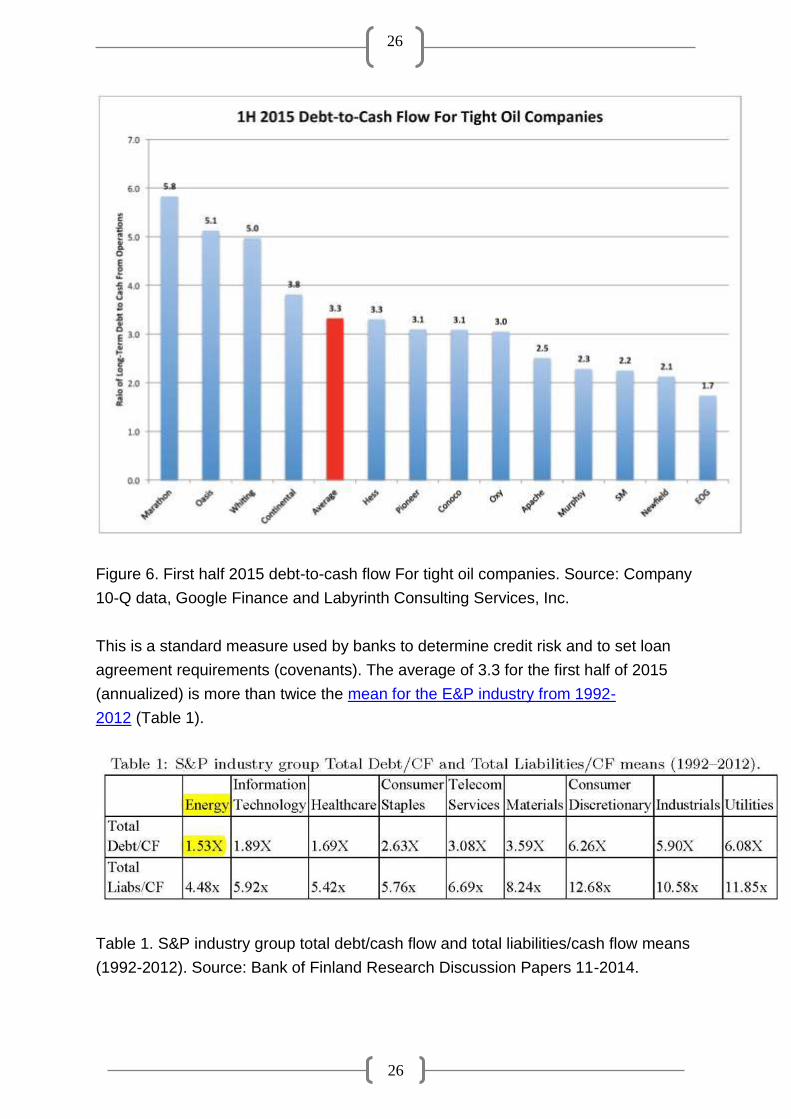

The debt side of first half earnings looks even worse, if that is possible. Figure 6

shows that debt-to-cash flow ratios for sampled tight oil companies average 3.3. This

means that it would take these companies 3.3 years to pay down their total debt

using all cash from operating activities.

26

26

Figure 6. First half 2015 debt-to-cash flow For tight oil companies. Source: Company

10-Q data, Google Finance and Labyrinth Consulting Services, Inc.

This is a standard measure used by banks to determine credit risk and to set loan

agreement requirements (covenants). The average of 3.3 for the first half of 2015

(annualized) is more than twice the mean for the E&P industry from 1992-

2012 (Table 1).

Table 1. S&P industry group total debt/cash flow and total liabilities/cash flow means

(1992-2012). Source: Bank of Finland Research Discussion Papers 11-2014.

27

27

This has profound implications for debt re-determinations that will happen during the

third quarter of this year. It means that most of the companies shown in Figure 6 with

debt-to-cash flow ratios above 2.0 may have considerably less access to revolving

credit lines going forward. That equals more limited capability to drill and complete

wells.

At the same time, favorable hedge positions, that allow companies to realize prices

higher than current spot markets pay, will begin to expire in coming months. The

drop in value for long-dated futures contracts since oil prices slumped in July means

that tight oil companies are unable to hedge much above current low prices.

My colleague Euan Mearns recently did a forecast for U.S. tight oil plays and

concluded that production from the Eagle Ford, Bakken and Permian would decline

by about 830,000 bopd by the end of 2015. His estimate assumed that rig counts

had stabilized but tight oil horizontal rig counts have increased 20 during the last 4

weeks.

The EIA forecasts approximately 390,000 bopd of production decline by year-end

(Figure 7).

28

28

Figure 7. EIA U.S. crude oil production and forecast, 2015-2016. Source: EIA and

Labyrinth Consulting Services, Inc.

What It Means

The significance of these production forecasts and the second quarter earnings

reports is that U.S. tight oil production will decline. The fact that production has

remained strong despite a 60% decrease in the tight oil rig count has incorrectly lead

some analysts to conclude that production will not fall because of the ingenuity and

efficiency of U.S. producers.

It takes time for production to decline because there are months of lag between the

beginning of drilling and first production, and more months of lag before production

data is released. Also, many of the rigs that were released were drilling marginal

locations that didn't contribute much to overall production-the 80-20 rule. And, there

is the inventory of uncompleted wells that are unaffected by rig count.

Will a decline of 400,000 to 800,000 bopd in U.S. tight oil production make a

difference in the global market balance? Obviously, it depends on what other

producers do but it is certainly important to OPEC's strategy of gaining market share

from unconventional producers.

OPEC is producing more than half of the world production surplus and has the

capacity to cut production by the entire amount of the surplus. This will not happen

until its goals are achieved but Saudi Foreign Minister al-Jubeir will meet with

Russian Foreign Minister Sergei Lavrov August 11 in Moscow to discuss global

energy markets and other topics. EIA will release its STEO on the same day and IEA

will release its OMR the next day.

I am hopeful that something positive will emerge that will at least help to stop the

decline in oil prices.

View more quality content from

The Petroleum Truth Report

PICK A WINNERFOR THESE CHALLENGINGTIMES

Stay ahead of the game, and don’t wait for partners to show you the value in your assets! Find out more at

ikonscience.com/jifi

With the industry’s current focus on cost control, it is remarkable that more and more forward-thinking oil & gas companies are stepping up to invest in Ikon Science’s revolutionary RokDoc Ji-Fi®, a new tool to build reliable seismically-driven geological models. Ji-Fi breaks the mold of traditional workflows and opens up a whole new realm of possibilities. The cost/benefit of Ji-Fi is so compelling it redefines how customers leverage data and knowledge to drive success in their exploration, development and production activities.

The Present And Future Of GeoPrediction

ikonscience.com

C

M

Y

CM

MY

CY

CMY

K

Ji-Fi A4.pdf 1 20/05/2015 08:05:25

30

30

What is the price of oil telling us?

Written by Kurt Cobb from Resource Insights Market fundamentalists tell us that prices convey information. Yet, while our barbers

and hairdressers might be able to give us an extended account of why their prices

have changed in the last few years, commodities such as oil--which reached a six-

year low last week--stand mute. To fill that silence, many people are only too eager

to speak for oil. And, they have been speaking volumes. So much information in that

one price!

First, as prices fell last year when OPEC refused to cut its oil production in the face

of slowing world demand, the industry kept saying that it could continue to produce

from American tight oil fields at around $80 a barrel and be profitable. Then, as

prices fell further,the industry and its consultants assured everyone that while growth

in tight oil production would slow, it would still be profitable for the vast majority of

wells planned.

Petroleum geologist and consultant Art Berman is probably the best representative

from the skeptical camp. For many years Berman has been pointing to the high cost

of getting fracked oil out of the ground. And, those costs led to negative free cash

flow for most tight oil operators for several years in a row--that is, they spent

considerably more cash than they took in, making up the balance with debt and

stock issuance. Not surprisingly, the operators took that money and kept drilling as

fast as they could.

It was a recipe for oversupply and a crash, one that is now threatening the solvency

of many fracking-dependent U.S. oil companies.

As if to the rescue, the giant consulting firm Deloitte called a bottom in the oil

price when U.S. futures prices hit $48 a barrel on February 4--a little prematurely it

seems. Friday's price for September futures on the NYMEX closed at $42.50.

Not to worry. Two major international oil companies, Chevron and Exxon, declared

back in December that $40-a-barrel oil won't be a problem for them. One of the

31

31

sources cited was Exxon CEO Rex Tillerson whose company has had trouble

replacing its oil reserves for more than a decade at much higher average prices. In

fact, oil majors have been cutting exploration budgets since early 2014 when oil

prices were still hovering above $100.

It seemed as if the message that the price of oil was sending from about the middle

of last year until just recently was going unheeded by American oil producers. U.S.

oil production kept rising despite dramatically falling prices. But when production

growth finally stopped in June, there was hope that less supply would be weighing

on prices, and predictions abounded that the price would go higher.

The reasoning behind this call was that continuing economic growth worldwide would

combine with stagnating growth in oil supplies to squeeze the market enough to

move prices up.

While low oil prices were supposed to 'spur the global economy' according the the

International Monetary Fund, The Economist magazine took a more measured view.

It also looked at the decline in employment and investment in oil which had

previously been booming.

High-cost oil from the Canadian tar sands is also taking a significant hit as

investment is slashed in the face of low prices.

With the recent renewed slump in oil prices, the industry is trotting out the same kind

of stories it trotted out when oil was around $80 and then $60. Oil at $30 a barrel will

be no problem for a special breed of drillers in the Bakken Formation of North

Dakota, we are told. If you actually read the story, it is stating the obvious: That

break-even prices vary from well to well. And, the writer refers to 'realized' prices, not

the NYMEX futures price. It turns out that because Bakken lacks pipelines for

transporting oil, it must use oil trains. That's expensive.

So, those buying oil from North Dakota take the freight costs into account. The

average realized price on Friday $28.75 for the type of oil extracted from Bakken's

deep shales in North Dakota. While wells that are already drilled often produce

regardless of price because those who operate them must pay back debt, it is

doubtful that very many new wells would be profitable at this price. And, it is worth

noting those investing their capital do not as a rule seek to break even. A break-even

proposition usually sends them looking elsewhere to invest their money.

32

32

Beyond this, there is a broader consideration. And, it is something which very few

people seem to be talking about when it comes to all the information that is

supposed to be conveyed by the oil price.

As the world's central energy commodity, oil is a good indicator of economic activity.

With the nearly universal conviction that the previous bounce in oil prices to around

$60 signaled a stronger economy and thus stronger oil demand, logic would dictate

that we now consider the opposite: That the new slide in oil prices is signaling new

weakness in the world economy. If so, it's the kind that ought to frighten even the

optimists this time.

Having said all this, it might be wise to take any day's price reports in the same way

as the low or high temperatures on a particular day. A cool morning in summer does

not mean winter is right around the corner. Nor does a hot day in mid-winter spell the

end of the season. What's more important is to look at the overall picture to see if the

season is changing--or even more important, if the climate itself has shifted, both

literally and metaphorically.

That takes a lot more analysis than the daily market reports can provide and than

most people--even those whose job it is to follow markets--have patience for.

In that regard the long view suggests that the acute investment slump in oil which is

unfolding will lead to tight supplies in a few years (because of all the wells that are

not going to be drilled to replace the depletion from existing wells). That would set us

up for a price spike at some point as it takes a considerable amount of time to ramp

up new drilling after a long period of decline.

All this assumes that the current seeming weakness in the economy doesn't morph

into something that would cause a long-term economic decline or stagnation which

would keep oil prices low for a much longer period.

View more quality content from

Resource Insights

33

33

Oil Prices: Why We Are Where We Are Today

Written by John Richardson from ICIS

TWO months ago, when I was delivering a training course, people responded with

deep scepticism when I suggested that oil-price stability at around $65 a barrel

wouldn't be sustained during the second half of the year. And when I suggested the

price would soon fall to below $50 a barrel, the reaction of the audience was even

more disbelieving.

It continues. Only last week, when I suggested that there was no reason why crude

might not fall below $40 a barrel later this year, the reaction of several chemical

industry contacts was again, 'Surely not?'

So why have I maintained my bearish view on crude? Here are my five main

reasons:

1. Oil markets, for too many years now, haven't followed the fundamental laws of

supply and demand. Vast quantities of easy economic stimulus money flowed

into futures-market speculation, creating the need by these speculators,

because of their positions, to constantly talk-up up the price of oil to ensure

that it stayed in the region $100 a barrel. It didn't matter if the facts didn't

actually fit their story. All that mattered was that they convinced enough of the

people for enough of the time that their story was right.

2. Easy stimulus money also flowed into oil-supply investments, particularly in

the US, regardless of the signs as early as in 2011 that global demand would

not be sufficiently strong to absorb these new supplies.

3. And the problem is that we are talking about truly vast new supplies of both oil

and gas during a period when the global economy is a lot weaker than many

people had expected.

4. US shale-oil producers, for the time being at least, continue to maintain high

levels of output. This is partly because, as I first argued last October, a few

34

34

cents profit on each barrel of oil is better than no cents at all if you are trying

to pay-back your debts. The cost efficiency of the shale process is

also constantly improving.

5. The Saudis are playing the long game in order to maintain market share -

hence, June saw another record level of production. Saudi Arabia also knows

that global oil consumption growth is likely to slow very dramatically because

of climate-change concerns.They don't want to end up being forced to leave

their most valuable national asset in the ground, and so they intend to pump

as hard as they can for as long as they can.

Why did prices recover from February onwards to a high for Brent of $69.39 a barrel

on 5 May? This was again because of futures markets. A large number of

speculators gambled that supply was about to tighten, even though the evidence had

yet to emerge of significantly tighter supply.

Throughout this rally, it always felt as if it was only a matter of time until this

expectation was proven to be unfounded. That time has now arrived as we also

prepare for a sharp increase, rather than decrease, in supply because of the Iranian

nuclear deal.

Global demand is also getting weaker, mainly because of events in China.

Yesterday, for instance, it was announced that the final Caixin/Markit China

Manufacturing Purchasing Managers' Index for July had dropped to 47.8 from 49.4 in

June. This was the lowest in two years.

Nobody can predict geopolitics. But other than an unforeseen major geopolitical

event, it is hard to see how crude will not continue to fall over the next few months as

it continues to its return to its long-term historic average price of $30 a barrel. And as

this process unfolds, prices could well dip below $30 a barrel.

View more quality content from

ICIS

35

35

The Oil Price: how low is low?

Written by Euan Mearns from Energy Matters With West Texas Intermediate (WTI) and Brent close to their January 2015 lows

some readers are wondering how these lows compare with historic lows when the oil

price is adjusted for inflation (deflated). BP just happen to provide an oil price series

that is adjusted for inflation (Figure 1). The data are annual averages and based on

Brent since 1984. Annual averages conceal the extreme swings in price that tend to

be short lived. At time of writing WTI front month future contract was $44.42 and

Brent front month future was $49.92.

36

36

Figure 1 The blue line gives the annual average oil price (Brent since 1984) in

money of the day and the red line adjusted for inflation expressed in $2014. Three

large spikes in the oil price are evident in the 1860s, 1970s and 2010s. It is notable

that the magnitude of each spike is similar, of the order $100 to $120 (adjusted to

2014 $). The 1860s and 1970s spikes were followed by long bear markets for the oil

price, lasting for 110 years in the case of 1864 to 1973.

To understand what was going on 1861 to 1973 I suggest readers read The Prize:

The Epic Quest for Oil Money and Power that earned author Daniel Yergin the

Pulitzer Prize. It is a tremendous read. Most of us are however, more interested in

how today's prices compare with recent slumps, most notably the slump of 1986 and

1998 (Figure 2).

Figure 2 The main events, Acts 1 to 6, are described briefly below.

37

37

To get straight to the point. Brent will need to fall below $30 to match the lows seen

in 1986 and to below $20 to match the lows seen in 1998. WTI in particular is trading

close to its support level of $43.39 marked on 17 March 2015. If traders push the

price below that level then the price could fall a lot lower for a brief period. At the

fundamental level, supply and demand need to be rebalanced and the main problem

is over-supply of LTO from the USA and of OPEC crude depending upon which way

one views the problem. The recent price action since September 2014 has been

brutal on producers but not yet brutal enough to remove the 3 million bpd over

supply from the system. I do not believe that the white knight of increased demand is

about to gallop over the hill and therefore see a risk of substantially lower price in the

months ahead. Colleague Arthur Berman has a somewhat more upbeat perspective.

Historic Fundamentals

The large scale structure of oil price history is shaped by supply and demand driven

by both political dimensions and industry action and innovation. The main landmarks

are:

1. The 1973 Yom Kippur war followed by the 1974 oil embargo. The amount of crude

withheld from market by OPEC was relatively small (Figure 3) but was sufficient to

cause the first oil price shock.

Figure 3 Oil

exports for selected

OPEC countries

based on BP 2014.

38

38

2. The 1979 Iranian Revolution followed by the 1980 Iran-Iraq war led to the second

oil shock. The price reaction at this time did not reflect the fundamentals of supply

and demand and gravity soon took over sending the price down again in the years

that followed together with OPEC market share.

3. The 1986 slump was caused by OPEC reasserting its authority and trying to

reclaim market share that led to a prolonged bear market that culminated in 1998

when the world was awash in oil.

4. The low point since the first oil shock was marked by $10 oil (money of the day) in

1998. I remember it well since I was running an oil related business at that time. This

heralded in a new era for the industry that went through a massive restructuring with

many household names being swallowed up by the super-majors.

5. The commodities bull run that began around 2002 that lasted to 2008 or 2014

depending upon one's perspective had complex reasons from a perceived peak in

conventional oil production, the Chinese industrial revolution, expansion of debt, zero

interest rate policy (ZIRP) and bubblenomics. Rune Likvern gives a good account of

the links between the oil price and economic policies.

6. The 2008 financial crash brought an end to phase 1 of the bull run that was re-

inflated by OPEC cutting supply and QE blowing more liquidity into the bubble until

2014.

Rune argues that an end to QE in the USA is implicated in recent global currency

adjustments and the rout of the oil price and that is surely part of the story. But the

OPEC policy of maintaining market share and over supply of either LTO or OPEC

crude have also played a prominent role in Act 7 that is still being played out and still

has a way to run before a new market equilibrium is reached.

View more quality content from

Energy Matters

SUPPORTING THE DEVELOPMENT OF NATURAL RESOURCES

rpsgroup.com/energy [email protected]

Operations Support | Technical Studies | Advisory Services Project HSE & Risk Management | Training

40

40

How Did the Oil & Gas Majors Perform in Early 2015?

Written by Mark Young from Evaluate Energy

As Q2 results continue to flood in, Evaluate Energy has reviewed the performance of

the world's oil and gas majors - BP, Chevron, ConocoPhillips, ExxonMobil, Royal

Dutch Shell and Total - to gauge the impact of the price collapse of late 2014 on their

respective starts to 2015, with the main focus on their upstream earnings, production

and capital expenditures.

Earnings Down, Production Slightly Up

Predictably, in terms of unadjusted earnings (see note 1) in the upstream sector, the

start to 2015 has not been the six month period the majors will have hoped for. The

fall in prices saw all six companies report lower quarterly earnings in Q1 and Q2 than

their respective average quarterly earnings from 2014, with half of the group

recording upstream losses in Q2; BP's Q2 earnings were impacted by a loss of over

$10 billion related to the Gulf of Mexico spill response, whilst Chevron - remarkably

recording its first unadjusted upstream quarterly loss in since Q4 2001 - and

ConocoPhillips both suffered impairment charges to account for their own upstream

losses in Q2.

Production was a different story, however, with all companies apart from Shell

averaging a slightly higher rate over the first six months of 2015 compared with the

full year 2014.

41

41

All companies did record a slightly lower average production rate in Q2 2015

compared to Q1 2015, but, with Shell's acquisition of BG in the pipeline, all the

majors are looking at the prospect of higher production than they had in 2014 as we

enter the latter half of the year.

Capital Expenditure Cuts

E&P capital expenditure budgets were the first thing that many companies adjusted

when faced with the prospect of prolonged lower commodity prices - but the majors

did not cut as drastically as everybody else.

In a quick study of 60 U.S. listed companies (see note 2) that cut upstream capex

spends in Q1 2015 compared with the average spend per quarter in 2014, the

average cut was around 33%, with some companies slashing upstream capex by

nearly 80% compared to last year's average quarterly spend. In contrast, Total

bucked the trend and spent more in Q1 compared to 2014's quarterly average, whilst

the other 5 majors average only a 20% cut between them. Moving into Q2, 53 of the

60 U.S. companies continued to drop capex spends from Q1 levels at an average of

32%. As for the majors, ConocoPhillips - the only company of the 6 not to have a

refining sector to bolster its overall earnings by taking advantage of lower raw

42

42

material costs - was the only one that continued to significantly drop its spending,

whilst BP, Chevron, ExxonMobil and Shell all maintained Q1 levels and Total

dropped spending from its high Q1 outlay. For Total, this means its 2015 average

quarterly spend is now back in line with average 2014 levels.

Of course, it's not easy to pull the plug on large-scale projects, which tend to be the

domain of the majors, and capital will be committed to them regardless of price

movement. While this dynamic will have played some role in the majors not cutting

their spending as much as smaller companies, the apparent lack in reaction by the

majors compared to the rest of the industry does stand out.

However, should commodity prices continue to drop or fail to rebound any time soon,

it wouldn't be the greatest of surprises to eventually see the majors cut their

spending more deeply.

Notes

1. The term 'unadjusted earnings' used throughout refers to income including the

impact of non-recurring items, such as impairments, legal or restructuring

charges, as well as gains or losses on asset sales. Apart from BP, all majors

report this item for the upstream segment on a post-tax basis. BP reports this

item on a pre-tax basis.

43

43

2. The 60 U.S. listed companies that dropped capex in Q1 2015 compared to

average 2014: Abraxas Petroleum Corp., Anadarko Petroleum Corp., Antero

Resources Corp., Apache Corp., Approach Resources Inc., Atlas Resource

Partners L.P., Bill Barrett Corp., Bonanza Creek Energy Inc., Breitburn Energy

Partners L.P., Cabot Oil & Gas Corp., California Resources Corp., Callon

Petroleum Co., Carrizo Oil & Gas Inc., Chesapeake Energy Corp., Cimarex

Energy Co., Clayton Williams Energy Inc., Comstock Resources Inc.,

CONSOL Energy Inc., Denbury Resources Inc., Devon Energy Corp.,

Diamondback Energy Inc., Emerald Oil Inc., Enerplus Corp., EOG Resources

Inc., EP Energy Corp., EV Energy Partners L.P., Freeport-McMoRan Inc.,

Goodrich Petroleum Corp., Gulfport Energy Corp., Halcon Resources Corp.,

Hess Corp., Laredo Petroleum Inc., Linn Energy LLC., LRR Energy L.P.,

Marathon Oil Corp., Matador Resources Co., Memorial Production Partners

L.P., Murphy Oil Corp., Noble Energy Inc., Northern Oil & Gas Inc., Oasis

Petroleum Inc., Parsley Energy Inc., Penn Virginia Corp., PetroQuest Energy

Inc., Pioneer Natural Resources Co., QEP Resources Inc., Rex Energy Corp.,

Rice Energy Inc., Rosetta Resources Inc., RSP Permian Inc., Sanchez

Energy Corp., SandRidge Energy Inc., SM Energy Co., Southwestern Energy

Co., Stone Energy Corp., Swift Energy Co., Ultra Petroleum Corp., Unit Corp.,

W & T Offshore Inc., Warren Resources Inc.

3. Upstream capex in this study excludes the impact of any asset dispositions.

All data here is taken from the Evaluate Energy database, which provides Evaluate

Energy subscribers with over 25 years' coverage of the world's biggest and most

significant oil and gas companies. Evaluate Energy also has a mergers &

acquisitions database, covering all E&P asset, corporate and farm-in deals back to

2008, as well as refinery, LNG, midstream and oil service sector deals. For more on

Evaluate Energy and its products, please download our brochure.

View more quality content from

Evaluate Energy

44

44

Tullow Oil boss Heavey predicts oil price will hit $75 a barrel by year end

Written by John Mulligan from Independent.ie

Tullow Oil boss Aidan Heavey has predicted that oil prices will level off about $75 a

barrel this year but insisted the industry can still make money if prices were to keep

falling.

'The oil industry is very robust. We've made money at $20 a barrel, at $15 and at

$30,' the told the Irish Independent. 'The industry is geared towards adjusting itself,

whatever the oil environment is.'

He was speaking as Tullow Oil announced that first-half results that were broadly in

line with expectations, as revenue fell 35pc to $820m and pre-tax losses narrowed to

$10m from $29m. Its net loss was $68m - much better than analysts expected. It was

helped by lower exploration write-downs. It will spend a total of between $200m and

$250m this year on exploration. Tullow, whose primary operational focus is in Africa,

has been re-engineering its business in light of the oil price slump. It's cutting $500m

(€453m) in costs over the next three years and has reduced staff numbers.

The price of Brent Crude - an industry benchmark - has fallen about 50pc in the past

year and is now hovering around $50 a barrel. Shares in Tullow have fallen about

70pc in the same period, raising speculation that it could become a takeover target.

'The problem today is that you don't have a stabilised commodity prices worldwide,'

said Mr Heavey.

'Unless you get stability in there, companies like ourselves do exactly what we have

just done and reset the business to be competitive in a low oil price environment.'

He said Tullow's first-half results don't reflect the impact of its cost cutting, which will

become more fully evident in the current half and next year.

45

45

'We have completed a major cost-cutting exercise and restructured our financial

facilities. We've focused on the really high margin-producing assets and hedged

them to secure them,' he added.

Tullow's main asset is the Jubilee field off Ghana, where it's also progressing

another major offshore project due to come on stream in 2016. Tullow is active in

countries including Kenya.

Indo Business

View more quality content from

Independent.ie