olivers insights - us housing sector turning the corner

TRANSCRIPT

8/2/2019 Olivers Insights - US Housing Sector Turning the Corner

http://slidepdf.com/reader/full/olivers-insights-us-housing-sector-turning-the-corner 1/2

Oliver’sInsights

Key points > Bullets

Heading 1 or 2

Shane Oliver, Head of Investment Strategy& Chief Economist

EDITION 9 – 16 MARCH 2012

quietly bottomed and is now on the rise again thanks to a surgein shale oil production. The US has huge reserves of shale oiland advances in fracking technology (by which shale kilometresbelow the surface is fractured using explosives, allowing oil to bereleased and flow to the surface) and oil prices around US$100per barrel are making it economic for these reserves to be tapped.Some even see the US becoming self sufficient in oil again in thedecades ahead.

US housing bottomingA collapse in the US housing sector was at the core of the sub-

prime mortgage crisis in the US which subsequently morphedinto the global financial crisis. US house prices and housingconstruction surged into the middle of the last decade as laxlending standards underpinned a huge surge in home ownership.Boom turned to bust, starting around 2006 as housing supplystarted to surge and it became harder for sub-prime borrowersto refinance their loans. Foreclosures rose, made worse in turnby rising unemployment as the whole process fed on itself. Thesubsequent slump has seen a 34% plunge in house prices. Thishas seen the volume of private residential investment collapseby about 60% from its peak in the mid 1990s, resulting in a hugedrag on US gross domestic product (GDP) growth.

Why the worst is likely over for US housing

There are good reasons to believe that the US housing market isbottoming and starting to recover.

The first thing to note is that most US housing indicators havestabilised. Home sales have been bouncing along a bottom since2009. Housing starts and permits to build new houses have beenbottoming since late 2009. Furthermore, the National Associationof Home Builder’s conditions index has now broken out on theupside, pointing to a rise in starts ahead.

Home builders conditions point to stronger housing starts

Source: Bloomberg, AMP Capital

Second, the number of vacant homes is now starting to fallsharply. Over time the equilibrium number of vacant homes hasincreased in line with the rising population. This is proxied bythe long-term trend line in the next chart. It can be seen thatthe gap between the actual number of vacant homes and itslong-term trend is now closing rapidly. Related to this, householdformation is likely to rise sharply. Since 2006 it has been runningwell below that implied by population growth and has collapsedfrom a record 2 million to around 700,000 last year. This reflectstough economic conditions causing young people to stay at homewith their parents for longer and is likely to rebound as economicconditions improve. If the number of vacant homes continues todecline at the same rate as the last couple of years and householdformation picks up then the overhang of housing will likely begone by year end.

Oliver’sInsights

Key points > While it’s too early to call the end of the secular bear

market in US shares, there are some signs of light in the US

economy, notably in manufacturing, energy production and

housing.

>

In particular, after triggering the global financial crisis, theUS housing slump appears to be over and a recovery in

prospect.

> This will help prolong the current US economic recovery,

boost household wealth and over time and add to global

commodity demand.

IntroductionStarting with the bursting of the technology bubble in 2000,the fortunes of the US economy have waned. Since then, theUS has seen two recessions with the last being the worst sincethe 1930s, a rising trend in unemployment, the bursting of a

corporate debt bubble with the tech wreck and the bursting of ahousing debt bubble with the sub-prime mortgage crisis. So it’slittle wonder the US share market has been spinning its wheelsin a secular bear market. Some commentators even talk of apermanent decline for the US.

The high level of US public debt, ongoing private sector deleveraging,less business friendly policies, demographic trends and the absenceof extreme share market undervaluation suggest the secular bearmarket in US shares may not be over yet. That said, it would bedangerous to write the US off. Many did this in the 1970s onlyto see it roar back with a vengeance in the 1980s and 90s. Moreimportantly, there are some signs of light at the end of the tunnel forthe US in manufacturing, oil production and housing. This note takes

a look at these sectors, focusing on the latter as housing was theoriginal driver of the global financial crisis.

US manufacturing renaissanceRecently there have been numerous examples of companiessetting up manufacturing plants or expanding production inthe US over locations in Canada, Mexico, Japan or the emergingworld. These include Maserati, Toyota, Honda, Nissan, Kia, Intel,Whirlpool and Caterpillar. In fact for the first time in over 35

years, annual growth in manufacturing employment is exceedingemployment growth elsewhere in the US economy. The keydrivers of America’s manufacturing renaissance are restrainedunit labour costs in manufacturing (which have been unchangedfor the past 30 years), rising wages in emerging countries, thelow US dollar (US$) after a decade long slump, and cheap energyprices helped by surging natural gas supply. While it’s early days

yet, America’s manufacturing renaissance has further to go.

Surging oil productionUS natural gas supply has been surging for years resulting inlow prices. More significantly, a few years ago US oil production

The US housing sectorturning the corner

0

500

1000

1500

2000

2500

86 88 90 92 94 96 98 00 02 04 06 08 10 120

10

20

3040

50

60

70

80US HousingStarts, '000(LHS)

National Assoc of Home Builders'conditions index (RHS)

8/2/2019 Olivers Insights - US Housing Sector Turning the Corner

http://slidepdf.com/reader/full/olivers-insights-us-housing-sector-turning-the-corner 2/2

. . .

Contact usIf you would like to know more about how AMP Capital can help you, please visit ampcapital.com.au, or contact one of the following:

Financial Advisers Your Business DevelopmentManager or call 1300 139 267

Personal Investors Your Financial Adviser or callus on 1800 188 013

Wholesale Investors AMP Capital’s Client ServicesTeam on 1800 658 404

Important note: While every care has been taken in the preparation of this document,AMP Capital Investors Limited (ABN 59 001 777 591) (AFSL 232497) makes no

representation or warranty as to the accuracy or completeness of any statement in itincluding, without limitation, any forecasts. Past performance is not a reliable indicator

of future performance. This document has been prepared for the purpose of providinggeneral information, without taking account of any particular investor’s objectives,financial situation or needs. An investor should, before making any investmentdecisions, consider the appropriateness of the information in this document, andseek professional advice, having regard to the investor’s objectives, financial situation

and needs. This document is solely for the use of the party to whom it is provided. O I_ 1 6 0 3 1 2

The US inventory of vacant houses has almost fallen back

to its long-term trend

Source: US Census, AMP Capital

Third, the stock of unsold new homes has largely vanished. It isnow at its lowest level since the 1950s. This seems more extremewhen it is compared with the fact that the US population hasmore than doubled since then.

The stock of unsold single family homes for sale has almost

vanished

Source: Bloomberg, AMP Capital

Fourth, while the US mortgage foreclosure rate remains high,the delinquency rate is slowing as are the number of newforeclosures, pointing to a decline in foreclosures ahead.

Falling mortgage delinquencies point to falling foreclosures

Source: Mortgage Bankers Assoc of America, AMP Capital

Finally, housing affordability has reached a record level. While this hasnot been acted upon given the excess supply of housing and tougheconomic conditions, we are likely to see greater demand for housesas the excess supply dwindles and economic conditions improve.

US housing affordability is at record high

Source: Bloomberg, AMP Capital

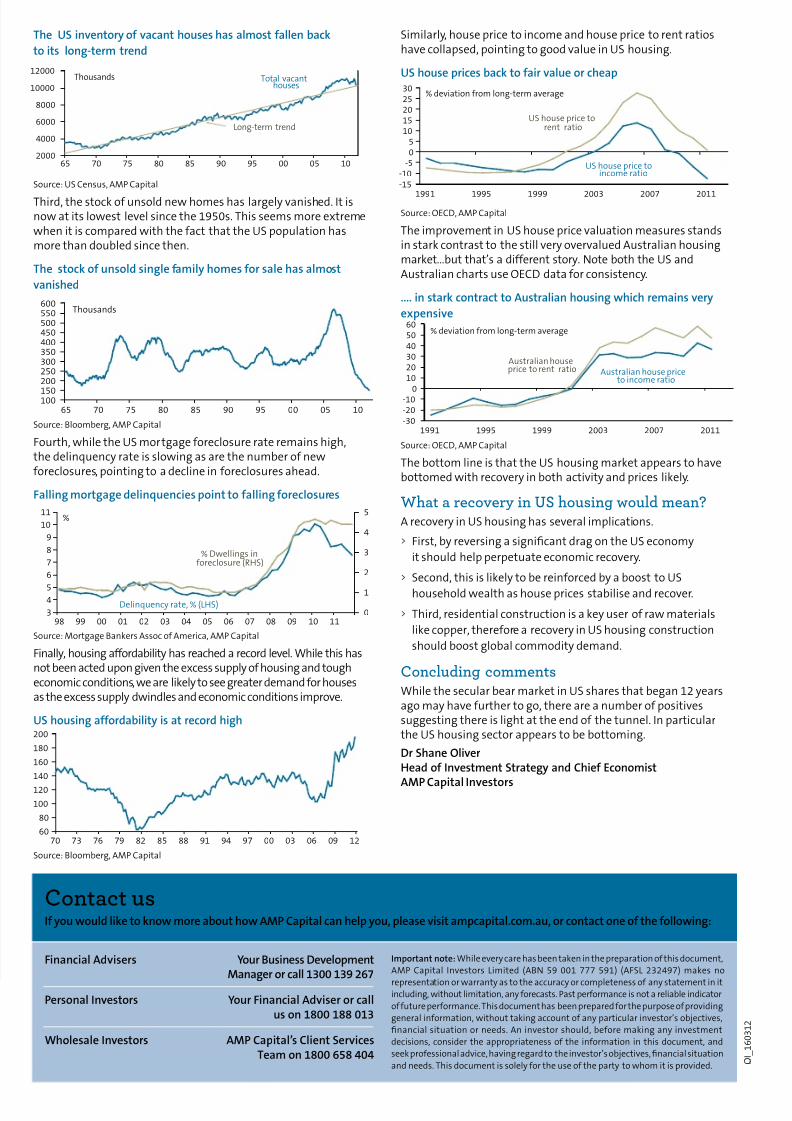

Similarly, house price to income and house price to rent ratioshave collapsed, pointing to good value in US housing.

US house prices back to fair value or cheap

Source: OECD, AMP Capital

The improvement in US house price valuation measures standsin stark contrast to the still very overvalued Australian housingmarket…but that’s a different story. Note both the US andAustralian charts use OECD data for consistency.

.... in stark contract to Australian housing which remains very

expensive

Source: OECD, AMP Capital

The bottom line is that the US housing market appears to havebottomed with recovery in both activity and prices likely.

What a recovery in US housing would mean?A recovery in US housing has several implications.

> First, by reversing a significant drag on the US economy

it should help perpetuate economic recovery.

> Second, this is likely to be reinforced by a boost to US

household wealth as house prices stabilise and recover.

> Third, residential construction is a key user of raw materials

like copper, therefore a recovery in US housing construction

should boost global commodity demand.

Concluding commentsWhile the secular bear market in US shares that began 12 yearsago may have further to go, there are a number of positivessuggesting there is light at the end of the tunnel. In particularthe US housing sector appears to be bottoming.

Dr Shane OliverHead of Investment Strategy and Chief Economist

AMP Capital Investors

2000

4000

6000

8000

10000

12000

65 70 75 80 85 90 95 00 05 10

Thousands

Long-term trend

Total vacanthouses

100150

200250300350400450500550600

65 70 75 80 85 90 95 00 05 10

Thousands

60

80

100

120

140

160

180

200

70 73 76 79 82 85 88 91 94 97 00 03 06 09 12

3

45

6

7

8

9

10

11

98 99 00 01 02 03 04 05 06 07 08 09 10 110

1

2

3

4

5

% Dwellings inforeclosure (RHS)

Delinquency rate, % (LHS)

%

-15-10

-505

1015202530

1991 1995 1999 2003 2007 2011

% deviation from long-term average

US house price torent ratio

US house price toincome ratio

-30-20-100

102030405060

1991 1995 1999 2003 2007 2011

% deviation from long-term average

Australian houseprice to rent ratio Australian house price

to income ratio