olt offshore lng toscana alessandro fino – · pdf file · 2017-05-18wobbe...

TRANSCRIPT

Small Scale to large MarketStrategies & Technologies towards the Mediterranean Area

"La logistica primaria per la distribuzione del GNL"

OLT Offshore LNG Toscana

Alessandro Fino – CEO

1

Golar LNG (2.69%)

Golar LNG is an LNG shipping company, belonging to the Fredriksen Group(owner of the largest oil tanker fleet in the world), engaged in the acquisition,ownership, operation and chartering of LNG carriers and FSRUs

IREN Group (49.07%)

IREN Group is listed on the Italian Stock Exchange and was founded in July2010 from the merger between IRIDE and ENIA - 49,07% (including 2,28%shares of ASA)

UNIPER Global Commodities SE (48.24%)

One of the largest energy groups in the world with entirely private capital, listedon the Frankfurt Stock Exchange

OLT Shareholders

2

“FSRU Toscana” milestones

� Conversion of the LNG carrier 'Golar Frost' H1444 into the floating storage andregasification unit ‘FSRU Toscana’, moored 12 nautical miles offshore theTuscany coast, (sea depth of 120 m), connected to the existing national gasgrid through a pipeline, operated by Snam Rete Gas S.p.A;

� The Terminal arrived offshore Livorno at the end of July 2013 and entered intocommercial operation on 20th December 2013;

� Terminal is completely self-sufficient and has the same operational featuresas typical onshore regasification terminals;

� Equipped with a Wobbe Index corrector installed on board that can allow toreceive almost all the LNG produced in the world;

� 95% of weather availability: during the last two operational years 87% of theslots were suitable for StS operations without any delay. 8% of the slots with adelay of no more than 2 days from the Arrival Window scheduled for therelevant slot, and without any impact on the following scheduled delivery slots.

Wobbe Index Corrector Unloading arms Single point mooring Regasification plant

Golar Frost

3

High flexibility as Italian regulated LNG Terminal

� FSRU Toscana Regasification Terminal is fully regulated and was declared by MSE decree as essentialItalian infrastructure, therefore a transparent and not discriminatory TPA is offered;

� TPA process is in compliance with all the relevant rules defined by the Italian Regulatory Authority forElectricity, Gas and Water (AEEGSI) - Resolution 167/05 according to criteria set forth in DL 164/00;

� An annual capacity of 6,356,250 Liq m3 (equivalent to 3.75 bm3 regasified GN) is offered with amaximum associated number of Delivery Slots equal to 41. On average 1 slot every 8.5 days isscheduled;

� Annual and multiannual (≤ 5 years) capacity is offered in May each year before the Annual UnloadingSchedule process takes place. Following such process the capacity is offered as Delivery Slot on rollingbasis;

� Send out flow rate with high flexibility, from a minimum send out, up to 15 MSm3/d can provide theusers with high trading value. Such flexibility can be used to recover cargo delays or adverse weatherconditions in order to nominate quantities out of the Terminal upon trading needs;

� The Terminal is allowed to receive approximately 90% of the current LNG carrier fleet with a cargocapacity from 65.000 to around 180.000 m3 (New Panamax class); the list of the LNG carriers alreadyapproved is available on the OLT website (currently around 70 LNG carriers).

4

European Security of Supply

� A key part of ensuring secure andaffordable supplies of energy toEuropeans involves diversifyingsupply routes. This includesidentifying and building new routesthat decrease the dependence of EUcountries on a single supplier ofnatural gas and other energyresources.

� Development and increasing of gasgrid connections between Europeancountries (counter flow).

� Create a Mediterranean gas hub inthe South of Europe to help diversifyits energy suppliers and routes.

� LNG imported to Europe through LNGterminals is a source of diversificationthat contributes to competition in thegas market and security of supply.

5

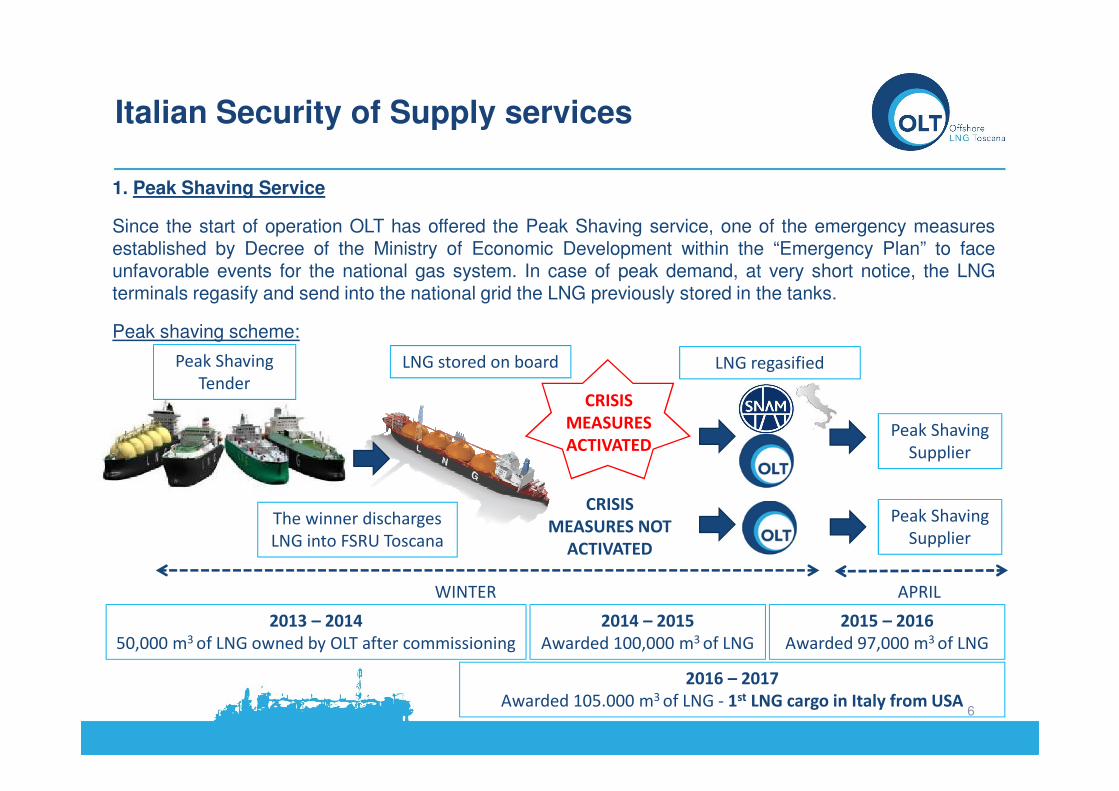

Italian Security of Supply services

1. Peak Shaving Service

Since the start of operation OLT has offered the Peak Shaving service, one of the emergency measuresestablished by Decree of the Ministry of Economic Development within the “Emergency Plan” to faceunfavorable events for the national gas system. In case of peak demand, at very short notice, the LNGterminals regasify and send into the national grid the LNG previously stored in the tanks.

Peak shaving scheme:

Peak Shaving

Supplier

WINTER APRIL

Peak Shaving

Tender

The winner discharges

LNG into FSRU Toscana

LNG stored on board

CRISIS

MEASURES

ACTIVATED

LNG regasified

CRISIS

MEASURES NOT

ACTIVATED

Peak Shaving

Supplier

2013 – 2014

50,000 m3 of LNG owned by OLT after commissioning

2014 – 2015

Awarded 100,000 m3 of LNG

2015 – 2016

Awarded 97,000 m3 of LNG

2016 – 2017

Awarded 105.000 m3 of LNG - 1st LNG cargo in Italy from USA6

2. Bundled service

During the first quarter of 2016, Italy adopted another important measure for the security of supply, thebundled service of the national storage system, managed by STOGIT and all the national LNG Terminals.The aim of this service is to offer the regasification service during the spring/summer seasons to benefitfrom the lower prices of the LNG market and to start to fill the Italian storage system for the winter seasonwith the regasified LNG.

Bundled service scheme:

Italian Security of Supply services

Suppliers

SPRING-SUMMER WINTER

Bundled service Tender

The winners discharge

LNG into FSRU Toscana

LNG regasified NG stored in the national storage system

Bundled Service 2017 – 2018

1,500,000,000 m3 NG auctioned;

The II tender for the storage Gas Year 2017/2018

is ongoing

Bundled Service 2016 – 2017

1,000,000,000 m3 NG auctioned; awarded capacity by OLT

440,000,000 m3 equivalent to 5 delivery slots between June

and August – 1st LNG cargo in Italy from Perù

7

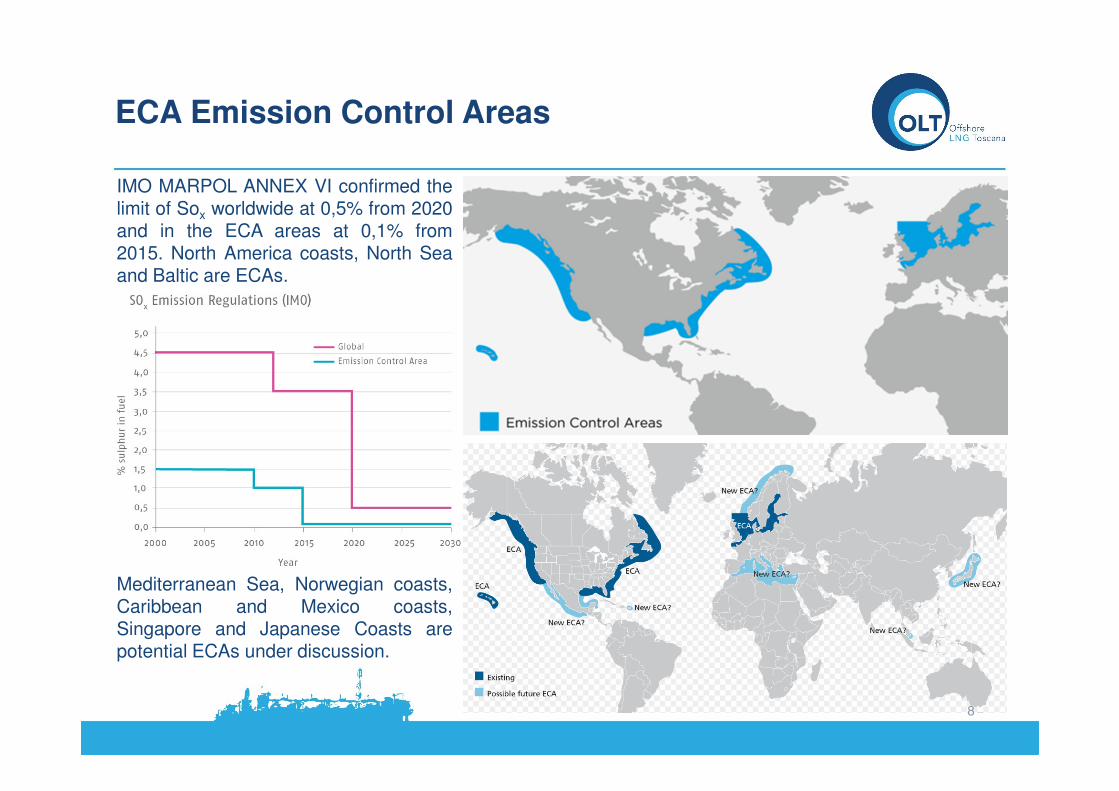

ECA Emission Control Areas

IMO MARPOL ANNEX VI confirmed thelimit of Sox worldwide at 0,5% from 2020and in the ECA areas at 0,1% from2015. North America coasts, North Seaand Baltic are ECAs.

Mediterranean Sea, Norwegian coasts,Caribbean and Mexico coasts,Singapore and Japanese Coasts arepotential ECAs under discussion.

8

SSLNG: Key Factors in the Logistic Model

LNG terminalsTrucks/Trains/ISO containers

(50-80 m3)

The main infrastructures onshore and offshore

can receive the LNG carriers from the suppliers

Transport

Industrial or civil facilities

REGASIFICATION

TERMINALSTRANSPORT END USERS

Mini LNG carriers (1000-30000 m3)

Bunker barges (400-1000 m3)

9

European Union policies

The Directive 2014/94/EU (DAFI) of the European Parliament and of the Council of 22 October 2014requires Member States to develop national policy frameworks for the market development of alternativefuels and their infrastructure; foresees the use of common technical specifications for recharging andrefueling stations; paves the way for setting up appropriate consumer information on alternative fuels,including a clear and sound price comparison methodology.The required coverage and the timing by which this coverage must be put in place is as follows:

Following a public consultation process started in 2015, the Italian Government implemented the Directive2014/94/EU (DAFI) with the Legislative Decree n. 257, approved on 16th December 2016. This latterincludes the National Plan for the use of LNG in Italy, providing the guidelines for the development of sectorregulations. The target is to build 5 LNG sea bunkering stations by 2020 and to reach the number of 10 by2025.

10

Transposition of Italian “DAFI” Directive

AEEGSI Resolution n. 141 of 16th March envisages some important rules regarding SSLNG services:� SSLNG is not a regulated activity (less LNG storages supplying the gas pipeline in Sardinia)� SSLNG activities may affect the regulated Regasification activities therefore the AEEGSI will

define rules to avoid any interferences;� Rules on accounting separation between Regasification and SSLNG activities will be defined.

As Italian Mediterranean LNG infrastructure, OLT is working to be able to successfully achieve thechallenges of the next future and as first link of the logistic chain of the Small Scale LNG business iscommitted to work in cooperation with the Italian institution in providing the services that LNG terminals arealready providing in the North sea and in the Baltic sea.

The main arguments that can have an high impact on the development of the SSLNG market:

� Authorization Process

� Support to isolated and not methanised areas

� Fiscal treatment

� Unbundling for regulated infrastructures

FSRU Toscana loading operation spring 201711

SSLNG: Key Factors in the Logistic Model

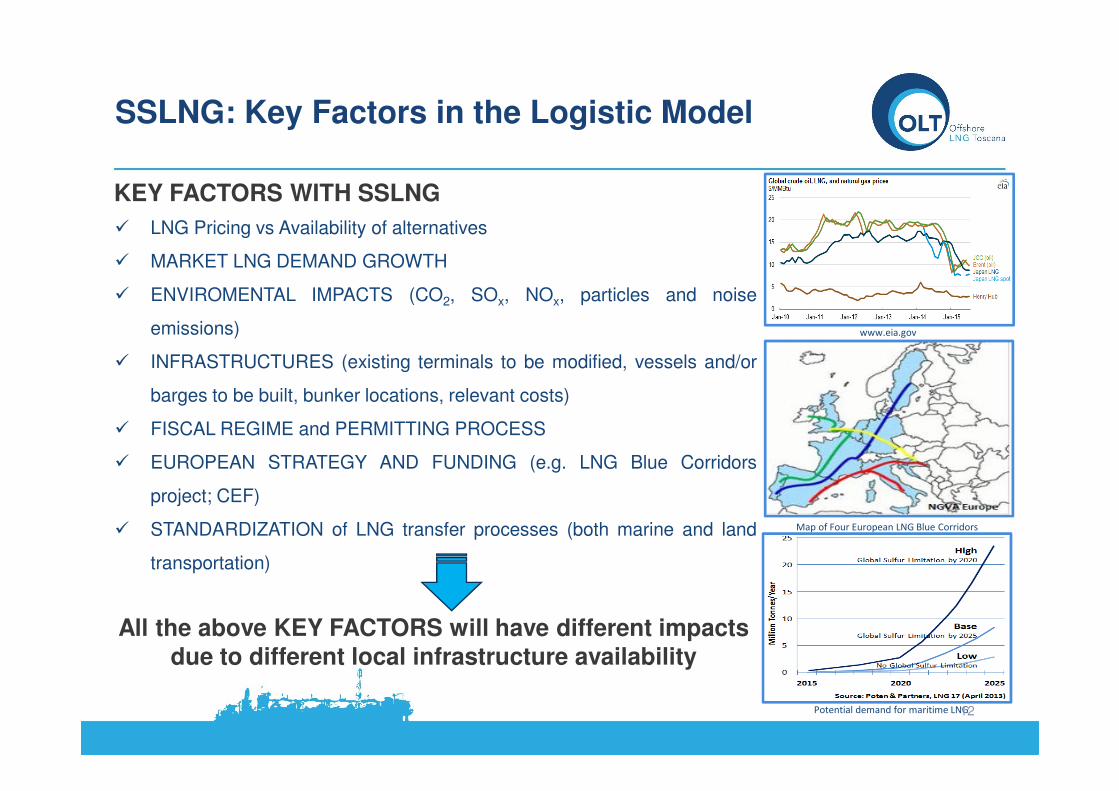

� LNG Pricing vs Availability of alternatives

� MARKET LNG DEMAND GROWTH

� ENVIROMENTAL IMPACTS (CO2, SOx, NOx, particles and noise

emissions)

� INFRASTRUCTURES (existing terminals to be modified, vessels and/or

barges to be built, bunker locations, relevant costs)

� FISCAL REGIME and PERMITTING PROCESS

� EUROPEAN STRATEGY AND FUNDING (e.g. LNG Blue Corridors

project; CEF)

� STANDARDIZATION of LNG transfer processes (both marine and land

transportation)

KEY FACTORS WITH SSLNG

Map of Four European LNG Blue Corridors

All the above KEY FACTORS will have different impacts

due to different local infrastructure availability

Potential demand for maritime LNG

www.eia.gov

12

Challenges under the EU policies

In 2014 - 2015 a pre-feasibility study co financed by EU TEN-T program called “SEA Terminal project”, incooperation with Valencia Port Foundation and Livorno Port Authority under the supervision of MIT,confirmed that “FSRU Toscana” can be able, with minor modifications, to perform the re-load service.Small LNG carriers can dock on the port side of the terminal and receive the quantities of LNG to bedelivered in to the main Tyrrhenian ports.

13

The pre-feasibility study that identified the capability of the terminal to perform the transfer of LNG to SmallLNG carriers gave the following main output:

• Mini LNGC between a cargo capacity from 1,000 m3 to 7,500 m3

• Mini LNGC Length: between 60 m to 110 m

• Loading rate between 250 m3 and 900 m3 (the timing is the same required for larger LNG carriers)

• Manifold in accordance to OCIMF recommendation

• ESD in accordance to SIGTTO recommendation.

OLT “Sea terminal” study outputs

7,500 m3 berthing layout

Small LNG carrier cargo capacity 7,500 m3

Small LNG carrier cargo capacity 2,500 m3

Currently OLT is involved in a further project called GAINN_IT under the EU CEF (Connecting EuropeFacility) program in cooperation with many industrial partners and MIT for a detailed study for SSLNGservices.

14

SSLNG development news from Northern Europe

2016 September 19, the SSLNGc 7,500 m3 Coral Methane loaded first LNG at therecently opened third jetty at the Gate LNG terminal in Rotterdam. The third jetty atthe Gate terminal enables the loading of small volumes of LNG, from 1,000 m3 up to20,000 m3, with the potential for increase to 40,000 m3 in the long term.

2017 January 2, first small-scale LNG reload operation in the Lithuanian port ofKlaipeda. Coral Energy loaded 15,000 m3 of LNG from the FSRU Independence willbe further transported to one of the small-scale LNG terminals in the coastal regionsof the Baltic Sea. The Lithuanian LNG terminal is currently the only facility in the BalticSea that can reload liquefied natural gas to smaller LNG carriers.

2017 April 4, Norway Skangas new LNG bunkering vessel, Coralius, would bedelivered in June. The Coralius, LNG bunkering vessel has a cargo capacity of 5,800m3 and is 99.6 meters long. It has a Finnish/Swedish Ice Class 1A. The ships’ mainoperation area will be from the Kiel Canal to mid-Norway, including part of the NorthSea. Skangas will also use the Coralius to supply the chilled fuel to Statoil’s platformsupply vessels and tugs along the Norwegian west coast.

2017 April 7, the world’s first purpose-built LNG bunkering vessel, Engie Zeebrugge,completed the first loading operation at Zeebrugge liquefied natural gas terminal’ssecond jetty. The Gas4Sea partnership, 5,000 m3 LNG bunkering vessel will operatefrom the port of Zeebrugge supplying marine fuel to ships operating in NorthernEurope.

SSLNGc Engie Zeebrugge 5.000 m3

Skangas Coralius 5.800 m3

Reload SSLNGc 7500 m3 - Gate

FSRU Independence - Lithuania

Source LNG World News website 15

Thank you for your timewww.oltoffshore.it

16