on the computation of the aggregate claims distribution in the - iseg

TRANSCRIPT

On the computation of the aggregate claims distribution in the

individual life model with bivariate dependencies

Carme Ribas∗, Jesús Marín-Solano and Antonio Alegre

July 12, 2002

Departament de Matemàtica Econòmica, Financera i Actuarial

Universitat de Barcelona

Av. Diagonal, 690. 08034 Barcelona, Spain

Abstract

In this paper, we focus on the computation of the aggregate claims distribution in the

individual life model when the portfolio is composed of independent pairs of dependent

risks. First, we prove that the bivariate probabilities associated to each couple under any

intermediate positive (negative) dependency hypothesis about their mortality can always

be written as a convex linear combination between the independent and the comonotonic

(mutually exclusive) ones. Considering this structure for the bivariate probabilities, we

then obtain two recursive schemes for computing the distribution of the aggregate claims

of the portfolio. These recursions greatly facilitate the computation of the aggregate claims

distribution of a life insurance (sub)portfolio exclusively composed of dependent couples

and ease the interpretation of the impact of the dependence on the associated stop-loss

premiums. Numerical results are given to demonstrate the applicability and efficiency of the

method.

Keywords: Individual life model, aggregate claims distribution, (in)dependent risks, comono-

tonic risks, mutually exclusive risks, stop-loss order.

∗Corresponding author. Telephone/Fax +34 93 402 19 53. E-mail adress: [email protected]

1

1 Introduction

Approximating the distribution of the aggregate amount of claims incurred in an insurance

portfolio over a fixed reference period has been one of the main topics in the actuarial literature

during the past two decades. In the individual life model, exact calculations are easily obtained

since 1986, when De Pril derived an exact recursive scheme for computing this distribution. An

efficient reformulation of this algorithm is given in Waldmann (1994). Dhaene and Vanderbroek

(1995), proposed a new recursive scheme for the exact computation of the aggregate claims

distribution in the individual risk model with arbitrary positive claim amounts. This algorithm

contains the Waldmann (1994) recursion as a particular case.

The individual life model has been considered as the one closest to the real situation of

the total claims of a life insurance portfolio. It only makes the “nearly inevitable” assumption

of independence of the lifelenghts of insured persons in the portfolio. Many clinical studies,

however, have demonstrated positive dependence of paired lives such as a husband and wife.

These dependences materially increase the values of the stop-loss premiums for the aggregated

loss (for numerical illustrations the interested reader is referred, e.g., to Dhaene and Goovaerts

(1997)). It is well known that the stop-loss order is the order followed by any risk averse decision

maker and then, the simplifying hypothesis of independence constitute a real financial danger

for the company, in the sense that most of their decisions are based on the aggregate claims

distribution.

Since the beginning of the 1990’s, several papers have treated dependency between risks.

Among them, Dhaene and Goovaerts (1996, 1997), Müller (1997), Baüerle and Müller (1998),

Wang and Dhaene (1998), Hu and Wu (1999), Dhaene and Denuit (1999), Dhaene et al. (2000),

Frostig (2001) and Cossete et al. (2002) study different ordering between two portfolios of

dependent risks in the individual risk model. For a portfolio composed of independent pairs of

dependent risks, Dhaene and Goovaerts (1996) derived the distribution of the riskiest and safest

risks, i.e., the ones generating the largest and smallest stop-loss premiums for the aggregate

claim. In another work (1997), they treated multivariate dependencies in the individual life

model and found the distribution that maximizes the aggregate claims in stop-loss order, which

is also the riskiest one. Their results were generalized in Hu and Wu (1999), where the safest

distribution is found. The generalization of these bounds to the individual risk model can be

found in Müller (1997) and Dhaene et al. (2000) for the riskiest distribution and in Dhaene and

Denuit (1999) for the safest one.

2

Within the framework of the individual life model, simple expressions for computing the

riskiest and safest distribution for the aggregate claims of a life insurance portfolio with mul-

tivariate dependencies are derived in Dhaene and Goovaerts (1997) and Hu and Wu (1999),

respectively. The riskiest one follows by assuming that the multivariate distribution corres-

ponding to the dependent risks in the portfolio is given by the Fréchet upper bound (in this

case, the risks are said to be mutually comonotonic). On the contrary, the safest one corres-

ponds to the case of dependent risks with the Fréchet lower bound as multivariate distribution

when the conditions assuring that the Fréchet lower bound is a proper distribution function are

fulfilled (in this case, the risks are said to be mutually exclusive). Hence, in any life insurance

portfolio we can consider all kind of dependencies and compute easily the riskiest and safest

distributions in the stop-loss order sense. These bound distributions will help us to give an

idea of the degree of underestimation of the real risk of a portfolio with dependent risks when

computing the distribution of the aggregate claims under the traditional hypothesis of indepen-

dence. Unfortunately, they turn out to be useless as a measure of the risk of the portfolio since

the dependencies between the individual risks will be, in most real situations, nearest to the

independency than to these extreme dependency relations.

In this paper, we deal with bivariate intermediate positive (negative) dependency relations

in the individual life model. Considering a life insurance (sub)portfolio exclusively composed of

dependent couples, we prove, in section 3, that the bivariate probabilities associated to each cou-

ple under any intermediate positive (negative) dependency hypothesis about their mortality can

always be written as a convex linear combination between the independent and the comonotonic

(mutually exclusive) ones. Considering such form for the bivariate distributions and assuming

that the bivariate dependency relations are completely known, two recursive schemes are derived

in section 4 for computing exactly the aggregate claims distribution. The first one is a two stage

recursion formula that follows as a particular case of Dhaene and Vanderbroek (1995) algorithm.

The second, is a one stage recursion formula that is only valid in case that both policies in each

couple have the same amount at risk. These recursions greatly facilitate the computation of the

aggregate claims distribution for a life insurance portfolio with bivariate dependencies and also

ease the interpretation of the impact of the dependence on the associated stop-loss premiums.

Furthermore, when the dependence structure between the members of each couple is not exactly

known (as will occur in practice), safe approximations for the aggregate claims distribution are

easily obtained with our proposal. Some numerical results are summarized in section 5.

3

2 Preliminaries

Let us firstly recall the classical individual risk model where all the policies are assumed to be

mutually independent.

Consider a portfolio of n independent policies which produce at most one claim within a

certain reference period (e.g., one year). Suppose that the probability of producing a claim in

the reference period and the associated claim amount distributions are given for each policy. The

aggregate claims amount of the portfolio, S, is the sum of the n individual claims, X1, · · ·,Xn,

produced by the policies. We will suppose that S has a finite mean, that the probability of

no claims is strictly positive and that the individual claim amounts are positive and integer

multiples of some convenient monetary unit, so that one can consider S as being defined on the

non-negative integers.

Let the portfolio be classified into a× b classes, as displayed in table 1

Claim amount distribution

Mortality rate

q1

q2

· · ·qi

· · ·qb

f1 (x) f2 (x) · · · fk (x) · · · fa (x)

nki

Table 1. Classification of the Portfolio

where

fk (x) : Conditional distribution of the claim amounts for a policy in column k, given that a

claim has occurred, k = 1, 2, · · ·, a and x = 1, 2, · · ·,mi.

qi : Probability that a policy in row i produces a claim, i = 1, 2, · · ·, b.

We will assume in the sequel that 0 < qi ≤ 12 , for all i.

nki : Number of policies in row i and column k.

m =aP

k=1

bPi=1

nki : Maximum possible amount of aggregate claims.

4

Each individual policy in the portfolio implies the payment, in case of claim, of an amount given

by fk (x), and then, it constitute an individual risk Xki with probability function (pf)

Pr³Xki = x

´=

1− qi if x = 0,

qi fk (x) if x = 1, 2, · · ·,mi.(1)

Hence, the aggregate claims amount of the portfolio,

S = X1 + · · ·+Xn ,

can be rewritten as

S =aX

k=1

bXi=1

³Xki + · · ·+Xk

i

´.| {z }

nki times

Let pS (s) = Pr (S = s) , s = 0, 1, ···,m. The following recursion scheme for computing pS (s)

is stated and proved in Dhaene and Varderbroek (1995), giving an optimal way to calculate

exactly the aggregate claims distribution.

Theorem 1 For the individual model the probabilities pS (s) can be computed by

pS (0) =aY

k=1

bYi=1

(1− qi)nki (2)

s pS (s) =aX

k=1

bXi=1

nki vki (s) for s = 1, 2, · · ·,m, (3)

where the coefficients vki (s) are given by

vki (s) =qi

1− qi

miXx=1

fk (x)³xp (s− x)− vki (s− x)

´for s = 1, 2, · · ·,m (4)

and vki (s) = 0 elsewhere.

The individual life model can be obtained from the individual model considered above by

choosing fk (x) = δk,x for k = 1, 2, · · ·, a, where δk,x is the Kronecker delta with

δk,x =

1 if k = x,

0 otherwise.

In this case, the pf in (1) are given two-point distributions in 0 and k

Pr³Xki = x

´=

1− qi if x = 0,

qi if x = k.(5)

5

Each individual risk in the portfolio can either produce no claim or a fixed positive claim

amount k, k = 1, 2, · · ·, a, during the reference period considered. The claim probability is the

probability that the policyholder i dies during this period, i = 1, 2, · · ·, b, which can be obtainedfrom the mortality tables.

Given the individual risk distributions in (5) several recursive methods can be found in the

actuarial literature for computing exactly the aggregate claims distribution. The first one is

due to De Pril (1986) and generalizes a formula of White and Greville (1959) for the claim

numbers distribution. Waldmann (1994) obtains an efficient reformulation of this algorithm by

rearrangement of the recursive scheme of De Pril (1986). This recursion follows from Dhaene

and Vanderbroek (1995) algorithm in theorem 1 by choosing fk (x) = δk,x.

In the sequel the assumption of mutually independence is relaxed. More precisely, we will

assume that the portfolio consists of independent pairs of dependent risks. Hence, the number

of contracts in the portfolio, n, is assumed to be an even non-negative integer. Therefore, we

will group risks in table 1 in pairs by columns into a2 × (b+1)b2 classes

Amount at risk

Mortality rate

(q1, q1)

· · ·(q1, qb)

(q2, q2)

· · ·(qi, qj)

· · ·(qb, qb)

(1, 1) · · · (1, a) (2, 1) · · · (k, l) · · · (a, a)

nklij

Table 2. Life insurance portfolio with coupled risks

where

(k, l) : Amount at risk for the individual policies in each couple, k = 1, 2, · · ·, a; l = 1, 2, · · ·, a.

(qi, qj) : Mortality rate in the exposure period for the individual policies in each couple, i =

1, 2, · · ·, b; j = i, · · ·, b.

6

nklij : Number of couples with mortality rate (qi, qj) and amount at risk (k, l) .

Further, let

Xklij = Xk

i +Xlj (6)

with the marginal distributions of the Xki and Xl

j given by (5). Let

p00ij = Pr (Xi = 0,Xj = 0)

pk0ij = Pr (Xi = k,Xj = 0)

p0lij = Pr (Xi = 0,Xj = l)

pklij = Pr (Xi = k,Xj = l)

(7)

denote the non-zero bivariate probabilities corresponding to³Xki ,X

lj

´.

Observe that each couple in the portfolio constitute a risk Xklij as defined in (6) with pf defined

by

Pr³Xklij = x

´=

p00ij if x = 0,

pk0ij if x = k,

p0lij if x = l,

pklij if x = k + l

(8)

and then, the aggregate claims amount of the portfolio is

S =aX

k=1

aXl=1

bXi=1

bXj=i

³Xklij + · · ·+Xkl

ij

´| {z }

nklij times

(9)

with Xklij mutually independent. In this case, the distribution of the aggregate claims is no

longer uniquely determined by the pf (5) of the Xki . Intuitively, it is clear that for a positively

(negatively) correlated risk portfolio, assuming the independence hypothesis and computing the

pf of S with any of the recursive schemes quoted above will lead to underestimate (overestimate)

the associated stop-loss premiums. This fact has been proved in terms of stop-loss order.

Definition 2 A risk X is said to precede a risk Y in stop-loss order (written X ≤sl Y ), or alsoX is less risky than Y, if their stop-loss premiums are ordered uniformly:

E (X − d)+ ≤ E (Y − d)+

for all retentions d ≥ 0.

7

Let

S =aX

k=1

aXl=1

bXi=1

bXj=i

³Xklij + · · ·+Xkl

ij

´| {z }

nklij times

(10)

and

S0 =aX

k=1

aXl=1

bXi=1

bXj=i

³Y klij + · · ·+ Y kl

ij

´| {z }

nklij times

(11)

denote the total claim amount of the portfolio under two different hypothesis about the depen-

dency relation between the members of each couple.; i.e., the individual risks Xki and Y k

i are

identically distributed ( Xki

d= Y k

i , for i = 1, · · ·, b; k = 1, · · ·, a) and the only difference betweenboth distributions will be given by the bivariate probabilities in (7) that define the sums of

the Xklij and Y kl

ij in (8) The following theorem is due to Dhaene and Goovaerts (1997) and give

bounds for the riskiness of S.

Theorem 3 Let S, S0 be as defined in (10) and (11) and let r denote the Pearson’s correlation

coefficient. Then we have that

r³Xki ,X

lj

´≤ r

³Y ki , Y

lj

´, (i = 1, · · ·, b; j = i, · · ·, b; k, l = 1, · · ·, a)

implies

S ≤sl S0

Results in this theorem indicate that the aggregate risk of the portfolio is monotonically

increasing with respect to the correlation coefficient between the individual risks in each couple.

The expression corresponding to the correlation coefficient of any of the couples in the portfolio,³Xki ,X

lj

´, is

r³Xki ,X

lj

´=

pklij − qiqjpqi (1− qi) qj (1− qj)

(12)

and, consequently, the aggregate risk of the portfolio, measured in terms of stop-loss order,

increases when the probabilities pklij increase. Bounds for these probabilities follow immediately

from Fréchet bounds which we define next.

Definition 4 Let F1, F2 be univariate cumulative distribution functions (cdf’s, in short).

The Fréchet lower bound is a joint cdf W with margins F1, F2 defined by

W (x, y) = max {F1 (x) + F2 (y)− 1, 0} ∀x, y ∈ R.

8

The Fréchet upper bound is a joint cdf M with margins F1, F2 defined by

M (x, y) = min {F1 (x) , F2 (y)} ∀x, y ∈ R.

These two extreme bound distributions have been frequently considered in the recent ac-

tuarial literature. When the bivariate cdf associated to any pair of risks (X1,X2) is given by

the Fréchet upper bound, the risks X1 and X2 are said to be mutually comonotonic. On the

contrary, when the bivariate cdf associated to this pair is given by the Fréchet lower bound,

the risks X1 and X2 are said to be mutually exclusive. Within the framework of the individual

life model, applications of the notion of comonotonicity can be found in Dhaene and Goovaerts

(1997). The case of mutually exclusive risks has been considered in Hu and Wu (1999). In the

sequel, we will add the label ∨ to the nomenclature corresponding to each couple in the portfolio

in order to indicate that the comonotonicity assumption is established. The label ∧ will indicate

that the risks in each couple are assumed to be mutually exclusive.

It is easy to prove that for the individual risks we are considering here, i.e., those with

marginal pf defined by (5), the risks Xki and X l

j are mutually comonotonic,µ ∨Xki ,∨X lj

¶, if and

only if∨pklij= min (qi, qj) .

This means that the death of the younger one in the couple (the one with higher survival

probability) implies the death of the older one.

By symmetry, the risks Xki and X l

j are mutually exclusive,µ ∧Xki ,∧X lj

¶, if and only if

∧pklij= 0,

i.e., if the death of both policyholders can never occur in the reference period considered.

It follows immediately that

∧pklij≤ pklij ≤

∨pklij , (i = 1, · · ·, b; j = i, · · ·, b; k, l = 1, · · ·, a)

and then by combining the results in theorem 3 with the expression in (12), we can conclude

that∧S ≤sl S ≤sl

∨S .

These bound distributions for the aggregate claims in stop-loss ordering can be improved by

considering that the portfolio only contains either positively or negatively correlated risks. If

9

r³Xki ,X

lj

´≥ 0, (i = 1, · · ·, b; j = i, · · ·, b; k, l = 1, · · ·, a) ,

then

−pklij ≤ pklij ≤

∨pklij , (i = 1, · · ·, b; j = i, · · ·, b; k, l = 1, · · ·, a) , (13)

where the label − indicates that the risks Xki and X l

j are assumed to be mutually independent.

Hence, for a portfolio exclusively composed of positively dependent couples

−S ≤sl S ≤sl

∨S . (14)

From a similar reasoning, follows that if the portfolio is exclusively composed of negatively

dependent couples, i.e., r³Xki ,X

lj

´≤ 0, (i = 1, · · ·, b; j = i, · · ·, b; k, l = 1, · · ·, a),

∧S ≤sl S ≤sl

−S . (15)

Bounds in (14) and (15) were firstly obtained by Dhaene and Goovaerts (1997) and Hu and Wu

(1999), respectively. They indicate that if the risks in the portfolio are positively (negatively)

dependent, taking the traditional independence assumption will always lead to underestimate

(overestimate) the stop-loss premiums of the portfolio under consideration. Remark that the

pf of∧S and

∨S can be immediately obtained. Indeed, considering such two extreme dependence

relations, the sum distributions in (8) follow from the individual pf given in (5) and no additional

information about the bivariate dependency relations is needed. Unfortunately, they turn out to

be useless for most practical situations. In contrast to the independency assumption, assuming

comonotonicity (mutually exclusivity) turns out to be an extremely prudent (riskiness) strategy.

The main dependency relations that we could find in any real life insurance portfolio will be

closer to the independence than to the comonotonicity (mutually exclusivity) and this last

hypothesis can never been accepted for different purposes than giving the best upper (lower)

bound if the only information available consist of the individual risk distributions.

3 Intermediate types of dependence

In view of previous results, it is clear that more realistic approximations to the aggregate claims

distribution than the ones stated in (14) and (15) are only possible in the measure we can intro-

duce some additional information concerning the way of dependency of the components of each

10

couple in the portfolio. Restricting ourselves to a portfolio exclusively composed of positively

(negatively) dependent couples, we investigate in this section the nature of this information.

Let us consider one of the couples in the portfolio³Xki ,X

lj

´and assume that the individual

risks Xki and X l

j correspond to a xi-year-old and xj-year-old policyholders. We will denote by

Txi and Txj their remaining lifetimes (or time-until-death random variables).

Theorem 5 For any i = 1, · · ·, b; j = i, · · ·, b; k, l = 1, · · ·, a,

r³Xki ,X

lj

´= r

¡I (Txi ≤ t) , I

¡Txj ≤ t

¢¢, (16)

where I denotes the indicator function and t the reference period in years.

Proof. It follows immediately that the expression for r¡I (Txi ≤ t) , I

¡Txj ≤ t

¢¢is the one

given in (12) since Pr (Txi ≤ t) = qi, Pr (Txi ≤ t) = qj and Pr¡Txi ≤ t, Txj ≤ t

¢= pklij . ¤

Results in theorem 5 indicate that the correlation coefficient corresponding to the risks

in each couple depend on the correlation between the bivariate remaining lifetimes for the

reference period considered. We prove next that these last quantities, define completely the

bivariate probabilities in (7).

Case 1. r³Xki ,X

lj

´≥ 0 (i = 1, · · ·, b; j = i, · · ·, b; k, l = 1, · · ·, a)

Theorem 6 For any i = 1, · · ·, b; j = i, · · ·, b; the real value for sij in [0, 1] such that

r¡I (Txi ≤ t) , I

¡Txj ≤ t

¢¢= sij r

µI

µ ∨T xi≤ t

¶, I

µ ∨T xj≤ t

¶¶(17)

defines the following relations valid for any k, l = 1, · · ·, a,

pklij = sij∨pklij +(1− sij)

−pklij ,

pk0ij = sij∨pk0ij +(1− sij)

−pk0ij ,

p0lij = sij∨p0lij +(1− sij)

−p0lij ,

pklij = sij∨p00ij +(1− sij)

−p00ij .

(18)

Proof. Note first that the inequalities in (13) assure the existence of the sij in [0, 1] that defines

(17). Since Txid=∨T xi for i = 1, · · ·, b, by combining (12), (16) and (17), we have that

11

pklij−−pklij= sij

Ã∨pklij −

−pklij

!

which achieves the proof of the first relation in (18). In order to prove that the remaining

relations also hold, note that

pk0ij = qi − pklij = sij

Ãqi−

∨pklij

!+ (1− sij)

Ãqi−

−pklij

!= sij

∨pk0ij +(1− sij)

−pk0ij ,

p0lij = qj − pklij = sij

Ãqj−

∨pklij

!+ (1− sij)

Ãqj−

−pklij

!= sij

∨p0lij +(1− sij)

−p0lij ,

p00ij = 1− qi − qj + pklij = sij

Ã1− qi − qj+

∨pklij

!+ (1− sij)

Ã1− qi − qj+

−pklij

!

= sij∨p00ij +(1− sij)

−p00ij .

Case 2. r³Xki ,X

lj

´≤ 0 (i = 1, · · ·, b; j = i, · · ·, b; k, l = 1, · · ·, a)

Theorem 7 For any i = 1, · · ·, b; j = i, · · ·, b; the real value for sij in [0, 1] such that

r¡I (Txi ≤ t) , I

¡Txj ≤ t

¢¢= sij r

µI

µ ∧T xi≤ t

¶, I

µ ∧T xj≤ t

¶¶(19)

defines the following relations valid for any k, l = 1, · · ·, a,

pklij = sij∧pklij +(1− sij)

−pklij ,

pk0ij = sij∧pk0ij +(1− sij)

−pk0ij ,

p0lij = sij∧p0lij +(1− sij)

−p0lij ,

pklij = sij∧p00ij +(1− sij)

−p00ij .

(20)

Proof. Similar to the proof of theorem 6. ¤

From results in theorem 6 (theorem 7), we can conclude that the values of the sij that define

the relations in (17), (19), turn out to be the key quantity for the exact knowledge of the bivariate

probabilities in (7) associated to each couple in the portfolio. Given these values, the bivariate

probabilities result, in each point, as a convex linear combination between the corresponding

bivariate probabilities when the hypothesis with respect to the dependency relations of the risks

12

in each pair are independency and comonotonicity (mutually exclusivity), respectively. Once

the probabilities in (7) are given, the sum distributions in (8) are known. Then, the distribution

of the aggregate claims of the portfolio can be exactly computed with any of the recursive

schemes presented in next section. Nevertheless, at this point, we want to remark that the

importance of the results in this paper consist in giving improved upper (lower) bounds for the

riskiness of the portfolio but not in obtaining exact results for the aggregate claims distribution.

Indeed, exact values are only possible in the measure the information available allows us to

compute exactly the joint distributions of the¡Txi , Txj

¢, i = 1, · · ·, b; j = i, · · ·, b, and this will

never occur in practice, except in case of comonotonic (mutually exclusive) risks. Considering

any intermediate type of dependence, e.g., a life insurance (sub)portfolio exclusively composed

of married couples, the available information consists at most of a bivariate data set containing

the ages at death of some couples. In this case, the joint distributions of the¡Txi , Txj

¢can only

be approximations, which can be obtained by using, e.g., the methodology proposed by Genest

and Rivest (1993) for identifying a copula form in empirical applications as has been done in

Denuit et al. (2001) were a data set with the ages of death of 533 married couples was available.

Once the joint distributions of the¡Txi , Txj

¢are approximated, the approximative values for

the sij that define the relations in (17) or (19) (depending on the sign of the dependencies in the

portfolio) can be obtained. On what concerns to these values, notice that when the risks in the

couples are positively dependent, results in theorems 3 and 6 indicate that the coefficients sij are

monotonically increasing with respect to the aggregate risk of the portfolio, measured in terms of

stop-loss order. Hence, our proposal consists in giving approximative values for the coefficients

sij in (17) combining two criteria: they have to be smaller enough to describe reality, but, they

also have to be larger enough to guarantee they will never be exceeded. For safety reasons, the

latter criteria has to prevail in our approximations and then, the upper bound obtained turns

out to be sharper than the resultant when the comonotonicity hypothesis is assumed for the

risks in each couple. On the contrary, when the risks in the couples are negatively dependent,

results in theorems 3 and 7 indicate that the coefficients sij are monotonically decreasing with

respect to the aggregate risk of the portfolio. In this case, the approximative values for the

coefficients sij in (19) have to be higher enough to describe reality, but also smaller enough to

guarantee safety. The lower bound obtained this way turns out to be sharper than the resultant

when the risks of each couple are assumed to be mutually exclusive.

13

4 Exact recursive procedures

In this section, we assume that the coefficients sij ∈ [0, 1] , i = 1, · · ·, b; j = i, · · ·, b, in (17),(19), are exactly known, so that the probabilities in (18), (20), can be exactly computed. Two

recursive schemes for computing exactly the probabilities pS (s) corresponding to the aggregate

claims amount of the portfolio are next derived.

Theorem 8 For the aggregate claims amount of the portfolio defined in (9), the probabilities

pS (s) can be computed by

pS (0) =aY

k=1

aYl=1

bYi=1

bYj=i

¡1− p00ij

¢nklijs pS (s) =

aXk=1

aXl=1

bXi=1

bXj=i

nklij vklij (s) for s = 1, 2, · · ·,m,

where the coefficients vklij (s) are given by

vklij (s) =1

p00ij

hpk0ij

³k p (s− k)− vklij (s− k)

´+ p0lij

³l p (s− l)− vklij (s− l)

´+ pklij

³(k + l) p (s− (k + l))− vklij (s− (k + l))

´ifor s = 1, 2, · · ·,m

and vklij (s) = 0 elsewhere.

Proof. Observe that the pf of the Xklij in (8) can be rewritten as

Pr³Xklij = x

´=

p00ij if x = 0,³1− p00ij

´fkl (x) if x = 1, · · ·, a,

where the conditional claim amount distributions are defined by

fkl (x) =

pk0ij /(1− p00ij ) if x = k,

p0lij/(1− p00ij ) if x = l,

pklij/(1− p00ij ) if x = k + l

and fkl (x) = 0 elsewhere. Then, the recursion immediately follows from Dhaene and Varder-

broek (1995) recursion in theorem 1. ¤

In next theorem, we assume that the individual policies in each couple have the same amount

at risk, i.e., each couple in the portfolio has an amount at risk given by (k, k) , k = 1, · · ·, a,so that, table 2 consists of a× (b+1)b

2 classes, meanwhile thePb

i=1 nki in table 1 are assumed to

be non-negative integers. In next theorem we prove that, in this special case, the probabilities

pS (s) can be computed by a one stage recursion formula.

14

Theorem 9 Let

a (i, j, k, t, r) =

µ1p00ij

¶t ³pk0ij + p0kij

´t−r ³pkkij

´rand

A (k, t, r) = (−1)t+1 kbX

i=1

bXj=i

nkij a (i, j, k, t, r) .

Then, for s = 1, 2, · · ·,m, the following recursion holds:

pS (0) =aY

k=1

bYi=1

bYj=i

¡p00ij¢nkkij (21)

s pS (s)=

min(a,s)Xk=1

[ sk ]Xl=1

lXt=] l+12 [

³t−1l−t´A (k, t, l − t) + 2

l−1Xt=] l2 [

³t−1l−t−1

´A (k, t, l − t)

pS (s− lk)

(22)

where [x] denote the greatest integer less than or equal to x and ]x[ denote the greatest integer

larger than or equal to x.

Proof The probability generating function of the aggregate claims is given by

GS (u) =mXs=0

pS (s)us =

aYk=1

bYi=1

bYj=i

³GXk

ij(u)´nkkij

=aY

k=1

bYi=1

bYj=i

hp00ij +

³pk0ij + p0kij

´uk + pkkij u

2kinkkij

(23)

Putting u = 0 in (23) leads to (21). In order to proof (22), take

lnGS (u) =aX

k=1

bXi=1

bXj=i

nkkij

·ln p00ij + ln

µ1 +

µpk0ijp00ij+

p0kijp00ij

¶uk +

pkkijp00ij

u2k¶¸

By expanding we get

lnGS (u) =aX

k=1

bXi=1

bXj=i

nkkij

"ln p00ij +

∞Xt=1

(−1)t+1t

µµpk0ijp00ij+

p0kijp00ij

¶uk +

pkkijp00ij

u2k¶t#

(24)

Taking the derivative of both sides of (24)

G 0S (u) = GS (u)

aXk=1

bXi=1

bXj=i

k³pk0ij + p0kij + 2p

kkij u

k´nkkij

∞Xt=1

(−1)t+1µ

1p00ij

¶t ³pk0ij + p0kij + pkkij u

k´t−1

ukt−1

15

and by applying the binomial theorem lead to

G 0S (u) = GS (u)

aXk=1

bXi=1

bXj=i

k³pk0ij + p0kij + 2p

kkij u

k´nkkij

∞Xt=1

(−1)t+1µ

1p00ij

¶t

ukt−1

t−1Xr=0

¡ t−1r

¢ ³pk0ij + p0kij

´t−r−1 ³pkkij u

k´r

Hence,

G 0S (u) = GS (u)

aXk=1

∞Xt=1

t−1Xr=0

¡ t−1r

¢ hA (k, t, r)uk(t+r)−1 + 2A (k, t, r + 1)uk(t+r+1)−1

i(25)

Let

v (u) =aX

k=1

∞Xt=1

t−1Xr=0

¡t−1r

¢ hA (k, t, r)uk(t+r)−1 + 2A (k, t, r + 1)uk(t+r+1)−1

iSince

Gs−1)S (0) = (s− 1)! pS (s− 1)

and

vs−1) (0) = (s− 1) !min(a,s)X

k=1/ sk=[ sk ]

1

skX

t=] s+k2k [

³t−1sk−t

´A¡k, t, sk − t

¢+ 2

sk−1X

t=] s2k [

³t−1

sk−t−1

´A¡k, t, sk − t

¢

Taking, according to Leibnitz’s formula, the derivative of order s− 1 of both sides of (25) andsetting u = 0 leads to

s pS (s) =sX

l=1

min(a,l)Xk=1/ l

k=[ lk ]

lkX

t=] l+k2k [

µt−1lk−t

¶A¡k, t, lk−t

¢+ 2

lk−1X

t=] l2k [

µt−1lk−t−1

¶A¡k, t, lk−t

¢ pS (s− l)

and by rearranging terms the recursion (22) follows. ¤

Remark that, although the apparently limitation of the conditions stated in theorem 9, the

recursion obtained this way will be useful for many real situations. Indeed, in any life insurance

portfolios a large number of bivariate dependencies presumably arise from married couples and,

in most cases, both contracts will have the same amount at risk.

1k ∈ V (s) , where V (s) =©k ∈N / 1 ≤ k ≤ min (a, s) ∧ s

k=£sk

¤ª

16

5 Numerical example

In this section, we illustrate previous results by a numerical example. Remark that only positive

dependencies are considered since they will constitute the greater part of dependencies in any

real portfolio. Nevertheless, numerical results for negatively dependent risks follow easily by a

similar procedure.

We consider as starting point, the portfolio discussed in Kornya (1983) which is represented in

the following table.

Claim amount distribution

Mortality rate

0.00094

0.00191

0.00501

0.01320

0.03407

1 2 3 4 5

12 1 0 19 6

23 0 3 32 14

2 6 13 24 1

14 7 31 5 36

20 0 0 31 22

Table 3. Kornya’s portfolio

The portfolio consists of 322 risks. We suppose that it contains 52 positively dependent

couples which are presented in table 4, meanwhile the restating 218 risks in table 3 are mutually

independent.

Claim amount distribution

Mortality rate

(0.00094, 0.00191)

(0.00191, 0.00501)

(0.00501, 0.01320)

(0.01320, 0.03407)

(0.03407, 0.03407)

(1, 1) (2, 2) (3, 3) (4, 4) (5, 5)

2 0 0 8 0

2 0 2 5 1

0 3 6 3 0

5 0 0 2 4

3 0 0 2 4

Table 4. Positively dependent couples in Kornya’s portfolio

For simplicity reasons, we assume that all the couples in table 4 arise from the same kind

of dependency relations (e.g., married couples) so that sij = s for i = 1, · · ·, 5; j = i, · · ·, 5.

17

Moreover, observe that the amounts at risk for the two risks in each couple have been assumed

to be equal, so that the aggregate claims distribution follow either by applying the recursions

in theorem 8 and 9.

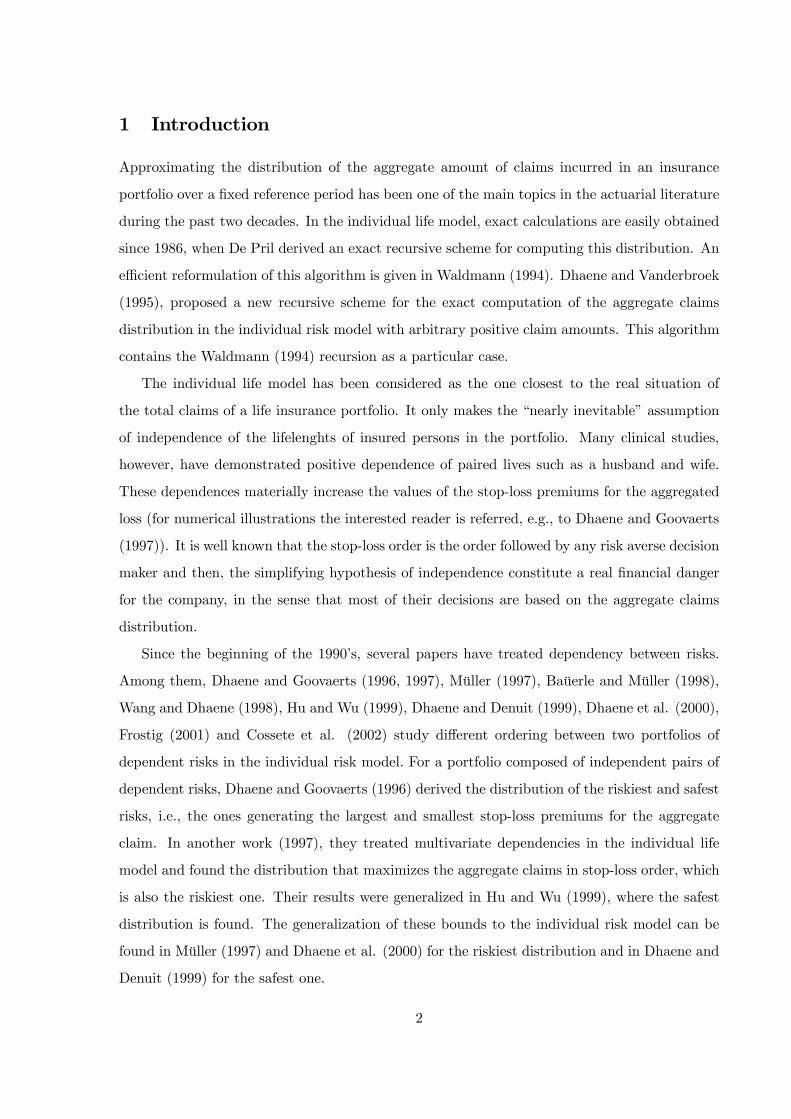

We give in Fig. 1a and b, the exact values of the cumulative distribution functions FS and

the stop-loss premiums E (S − d) for four portfolios. They differ in the value attributed to

the parameter s (that defines the relations in (17)) which determines the degree of dependence

between the risks of each couple. We have chosen values of 0, 0.15, 0.25 and 1 for s, where

s = 0 corresponds to the independence hypothesis for all the risks in the portfolio, meanwhile

s = 1 corresponds to the comonotonicity hypothesis for both risks in each couple. In table

5, we give E (S) and V ar (S) for each portfolio. It is clear from Fig. 1a and b that the

dependency significantly influences both FS (s) and E (S − d). In fact, we observe that, for

any fixed retention level d, the value of the stop-loss premiums increases with s, the degree

of dependency between the members of each couple. Hence, sharper upper bounds than the

comonotonic one are easily obtained in case some information concerning the bivariate remaining

lifetimes is available.

s E (S) V ar (S)

Independence 4.653 18.463

s = 0.15 4.653 20.597

s = 0.25 4.653 22.019

Comonotonicity 4.653 32.688

Table 5

18

(a)

1.05

0.2

F1s

F2s

F3s

F4s

300 s0 5 10 15 20 25 30

0.2

0.4

0.6

0.8

1

(b)

5

0.1

sl1 d

sl2 d

sl3 d

sl4 d

200 d0 2 4 6 8 10 12 14 16 18 20

0

1

2

3

4

5

Independences = 0.15s = 0.25Comonotonicity

Fig. 1.(a). Cumulative distribution functions FS(s) and (b) stop-loss premiums E (S − d).

19

References

[1] Baüerle, N. and A. Müller (1998). Modeling and comparing dependencies in multivariate

risk portfolios. ASTIN Bulletin 28, 59-76.

[2] Cossette, H., Gaillardetz, P., Marceau, E. and Rioux, J. (2002). On two dependent indi-

vidual risk models. Insurance Mathematics and Economics 30, 153-166.

[3] De Pril, N. (1986). On the exact computation of the aggregate claims distribution in the

individual life model. ASTIN Bulletin 16, 109-112.

[4] Denuit, M., Dhaene, J., Le Bailly de Tilleghem, C and Teghem, S. (2001). Measuring the

impact of dependence among insurance lifelenghts. Belgian Actuarial Bulletin 1.

[5] Dhaene, J. and M. Vanderbroek (1995). Recursions for the individual model. Insurance

Mathematics and Economics 16, 31-38.

[6] Dhaene, J. and Goovaerts, M.J. (1996). Dependency of risks and stop-loss order. ASTIN

Bulletin 26. 201-212.

[7] Dhaene, J. and Goovaerts, M.J. (1997). On the dependency of risks in the individual life

model. Insurance Mathematics and Economics 19, 243-253.

[8] Dhaene, J. and Denuit, M. (1999). The safest dependence structure among risks. Insurance

Mathematics and Economics 25, 11-21.

[9] Dhaene, J., S. Wang, V. R. Young and M. J. Goovaerts (2000). Comonotonicity and max-

imal stop-loss premiums. Mitteilungen der Schweizerischer Aktuarvereinigung 2000(2),

99-113.

[10] Frostig, E. (2001). Comparision of portfolios which depend on multivariate Bernoulli ran-

dom variables with fixed marginals. Insurance Mathematics and Economics 29, 319-331.

[11] Genest, Ch. and Rivest, L.P. (1993). Statistical inference procedures for bivariate

archimedean copulae. Journal of the American Statistical Association 88, 1034-1043.

[12] Gerber, H. U. (1979). An introduction to mathematical risk theory. Huebner Foundation

Monograph 8. Wharton Scool, Philadelphia.

20

[13] Hu, T. and Wu, Z. (1999). On dependence of risks and stop-loss premiums. Insurance

Mathematics and Economics 24, 323-332.

[14] Kaas, R., van Heerwaarden, A E. and Goovaerts, M.J. (1994). Ordering of Actuarial Risks.

Caire education series, vol. 1. Belgium.

[15] Müller, A. (1997). Stop-loss order for portfolios of dependent risks. Insurance Mathematics

and Economics 21, 219-223.

[16] Waldmann, K. (1994). On the exact calculation of the aggregate claims distribution in the

individual life model. ASTIN Bulletin 24, 89-96.

[17] Wang, S. and J. Dhaene (1998). Comonotonicity, correlation order and stop-loss premiums.

Insurance Mathematics and Economics 22, 235-243.

[18] White, R. P. and T. N. E. Greville (1959). On computing the probability that exactly

k of n independent events will occur. Transactions of the society of actuaries 11, 88-95.

Discussion 96-99.

21