on the determinants of sovereign wealth funds investment: are arab swfs different?

TRANSCRIPT

On the Determinants of Sovereign Wealth Funds’ Investments:

Are Arab SWFs different?

Washington DC, 9-10 September, 2016

Mohamed Arouri

Université d’Auvergne, France

Sabri Boubaker

ESC Troyes, France

Wafik Grais

Central Bank of the Republic of San Marino & ERF

Outline

• Motivation of the paper

• Data

• Empirical approach

• Empirical results

• Conclusion

Motivation of the paper

• SWFs control more than $ 7 trillion with an acceleration intheir growth in the recent decades until lately

• SWFs have Different goals:

- Inter-Generational Transfers: They transfer present to future times � they serve as a source of capital for future generations.

- Economic Stabilization: Stabilize funds to reduce boom and bust of commodity dependent economies � The government access fund capital to smooth out economic downturns.

- Developmental: SWF are a means to diversify the domesticeconomy and improve human capital.

What do SWFs invest in?

• They are long term institutional investors and have similar financialobjectives: maximize their risk adjusted returns by holding welldiversified portfolios (across asset classes, industries andgeographies). Their demand for liquidity reflects their long-terminvestment horizon.

• They are state owned funds � they may have sovereign objectives� take into account non-financial considerations.

• The fusion of the investment and development objectives isexpected to have portfolio allocation implications;

• A rich ongoing financial literature tests the validity of the twohypotheses : Long term financial investors versus sovereigndevelopment funds(Dyck and Morse, 2011;Knill et,2012; Megginsonand You, 2013; and Boubakri et al.,2016).

• In the literature, some recent studies have shown thatnon-financial (sovereign developmental) objectivesmatter in SWFs investment strategies [Dyck and Morse(2011), Megginson et al. (2013)].

• Some studies/reports suggest that Arab-SWF are lesstransparent and more difficult to disentangle from thelocal economy than other funds (Balding, 2012) �

They seem to serve more sovereign objectives thannon-Arab SWF.

• But those studies do not explicitly compare Arab andnon-Arab SWF investment strategies.

Contributions of the paper

• Investigate determinants of Arab SWFs’

investment decisions

• Check whether Arab SWF investment

strategies are different from non-Arab SWF.

Data

• The initial sample considered contains all sovereign wealth funds’ successful acquisitions of publicly traded firms over the period 2000–2014.

• Details of these transactions are obtained from different sources:Thomson Reuters SDC Platinum Global Database, Bureau Van DyckZephyr Database of Global Mergers& Acquisitions, and thesovereign wealth fund (SWF) Institute website(www.swfinstitute.org). Target―level financial data (in US dollars)are retrieved from the Worldscope database and country–level macro–economic data are gathered from the World Bank.

• Data on the enforcement of insider trading laws and theestablishment of the host countries’ main exchanges are retrievedfrom Bhattacharya and Daouk (2002).

• We discard all deals for which the needed

financial data of the target party are missing.

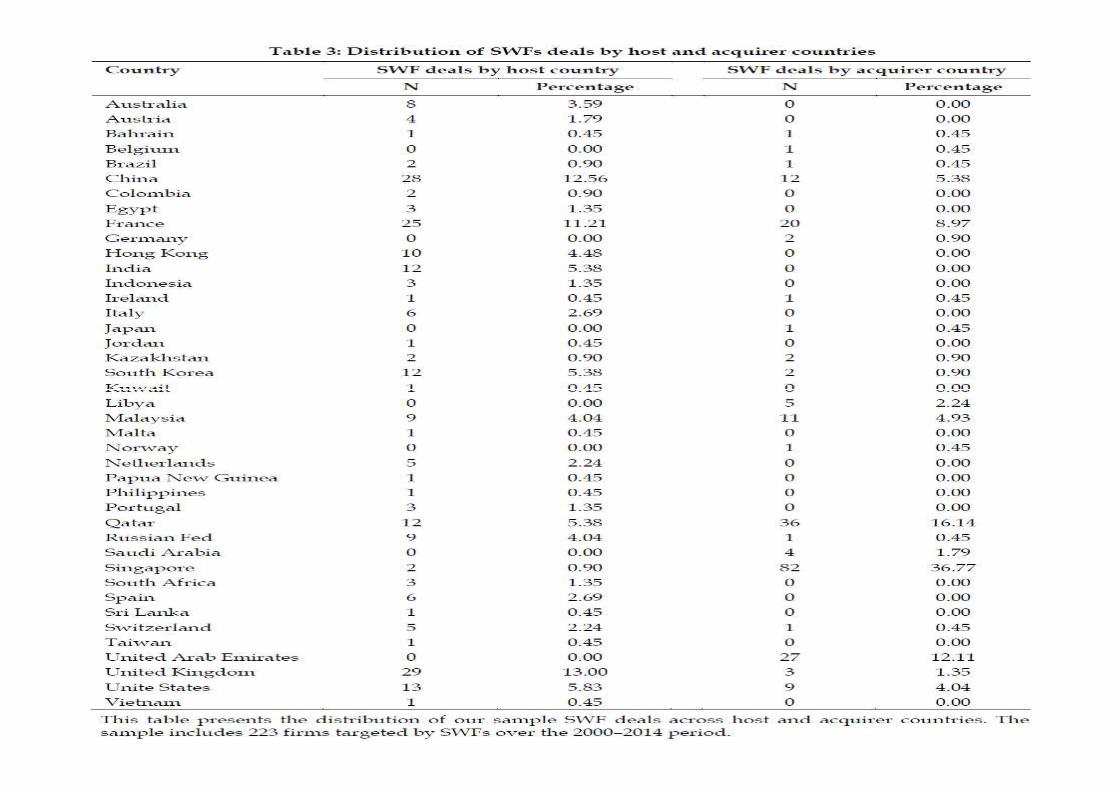

• The final sample includes 223 firms targeted

by SWFs over the 2000–2014 period, among

which 73 (33%) are targeted by SWFs owned

by Arab countries: Bahrain (1), Libya (5), Qatar

(36), Saudi Arabia (4), and United Arab

Emirates (UAE) (27).

Empirical approach

• A Probit model is used to investigate the determinantsof Arab SWFs’ decisions to invest in publicly tradedfirms.

• A right hand side variable is Arab_SWF, a dummyvariable set to one if the firm is targeted by a SWFowned by an Arab country, and zero otherwise.

• The model also contains a set of independent variablesshown in previous studies to bear on SWFs investmentdecisions: Target―level variables andCountry―specific variables

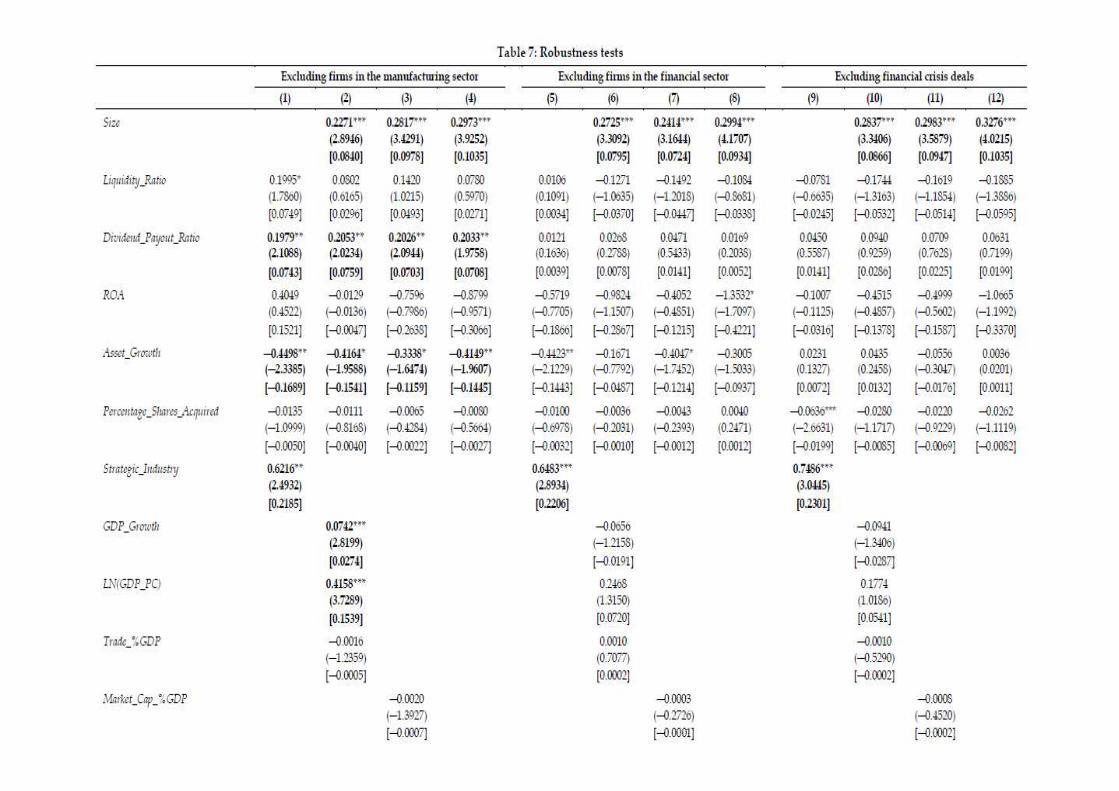

Empirical results

Conclusion

• We studied the determinants of Arab SWFs’ investment decisions using a sample of 223 firms targeted by SWFs over the 2000–2014 period (among which 73 are targeted by SWFs owned by Arab countries).

• We show that :

- Arab SWFs have higher preferences for larger firms in comparison tonon―Arab SWFs.

- Targets operating in strategic industries (such as the financial sector,mining, telecommunication, utilities) are more likely to be acquired byArab SWFs than firms in other industries.

- Firm―related variables measuring investment targets’ liquidity,profitability, growth or dividend payout are not the main drivers of ArabSWF investments.

- Additional results show that target countries with higher levels ofeconomic and capital market development are more attractive for ArabSWFs in comparison to non―Arab SWFs.