opeb investments the danger in playing it safe

TRANSCRIPT

OPEB Investments: The DANGER in Playing

it Safe

Mary Fedorak

MACM Regional Product Specialist

222 North LaSalle

Suite 910

Chicago, IL 60601

(312) 523-2438

www.pfm.com

Donn Hanson

Director

800 Nicollet Mall

Suite 2710

Minneapolis, MN 55402

(612) 371-3720

www.pfm.com

January 17, 2013

Mark D. Meyer, JD, FSA

Van Iwaarden Associates

840 Lumber Exchange

10 South Fifth Street

Minneapolis, MN 55402

(888) 596-5960

www.vaniwaarden.com

Tony Jacobs

Treasurer, LCWM School Board

607 Knights Lane

Lake Crystal, MN 56055

(507)726-2323

• OPEB Basics

• Actuarial Implications

• Investment Implications

• Board Implications

• Questions and Answers

Presentation Overview

2

Other

Post-Employment

Benefits

GASB Accounting for OPEB

3

Background of GASB Statements

4

OPEB in the Media

“School districts struggle to pay retirees' health benefits”

“The next retirement time bomb”

“Officials continue to grapple with liability issue”

“District is stretching out OPEB burden”

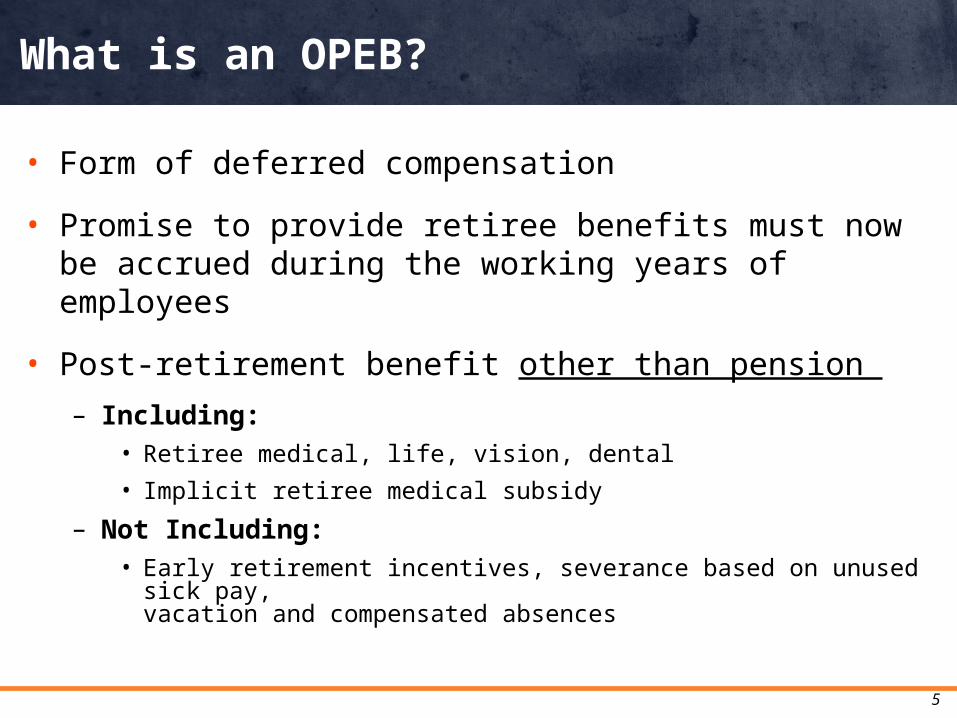

• Form of deferred compensation

• Promise to provide retiree benefits must now be accrued during the working years of employees

• Post-retirement benefit other than pension

– Including:• Retiree medical, life, vision, dental

• Implicit retiree medical subsidy

– Not Including:• Early retirement incentives, severance based on unused sick pay,

vacation and compensated absences

What is an OPEB?

5

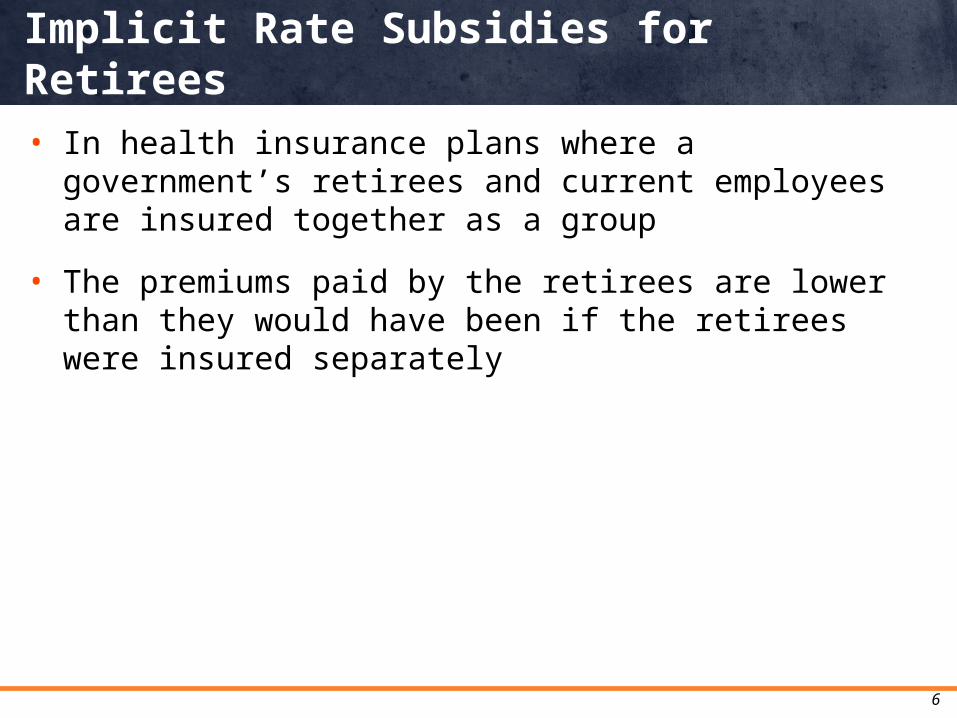

• In health insurance plans where a government’s retirees and current employees are insured together as a group

• The premiums paid by the retirees are lower than they would have been if the retirees were insured separately

Implicit Rate Subsidies for Retirees

6

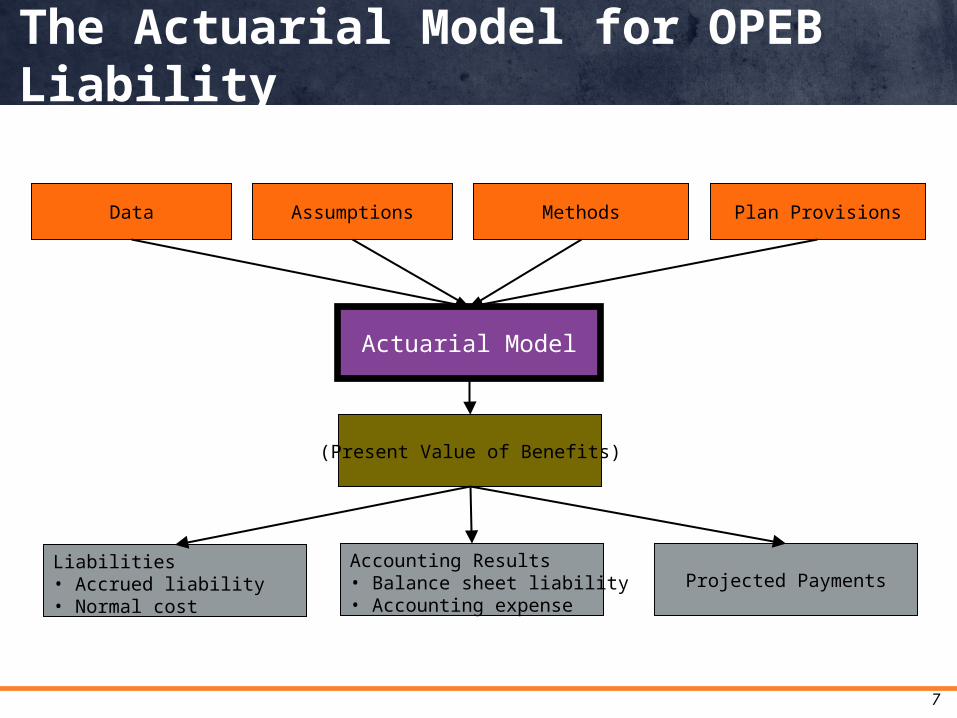

The Actuarial Model for OPEB Liability

7

Plan ProvisionsAssumptionsData Methods

Actuarial Model

Accounting Results• Balance sheet liability• Accounting expense

Liabilities• Accrued liability• Normal cost

Projected Payments

(Present Value of Benefits)

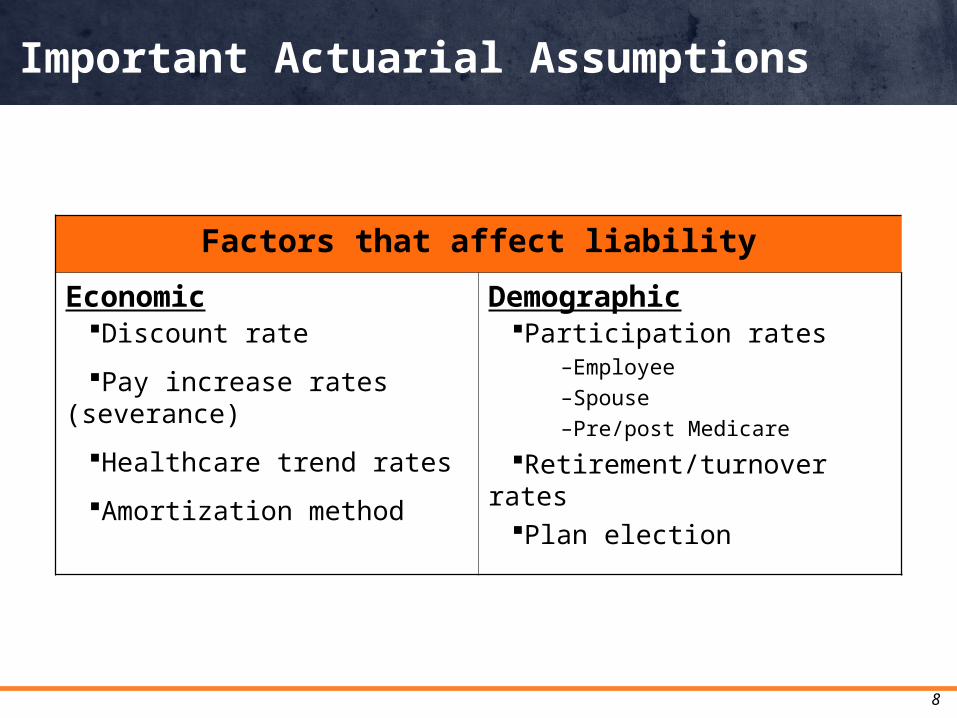

Important Actuarial Assumptions

Factors that affect liability

Economic Demographic

8

Discount rate

Pay increase rates (severance)

Healthcare trend rates

Amortization method

Participation rates–Employee–Spouse–Pre/post Medicare

Retirement/turnover ratesPlan election

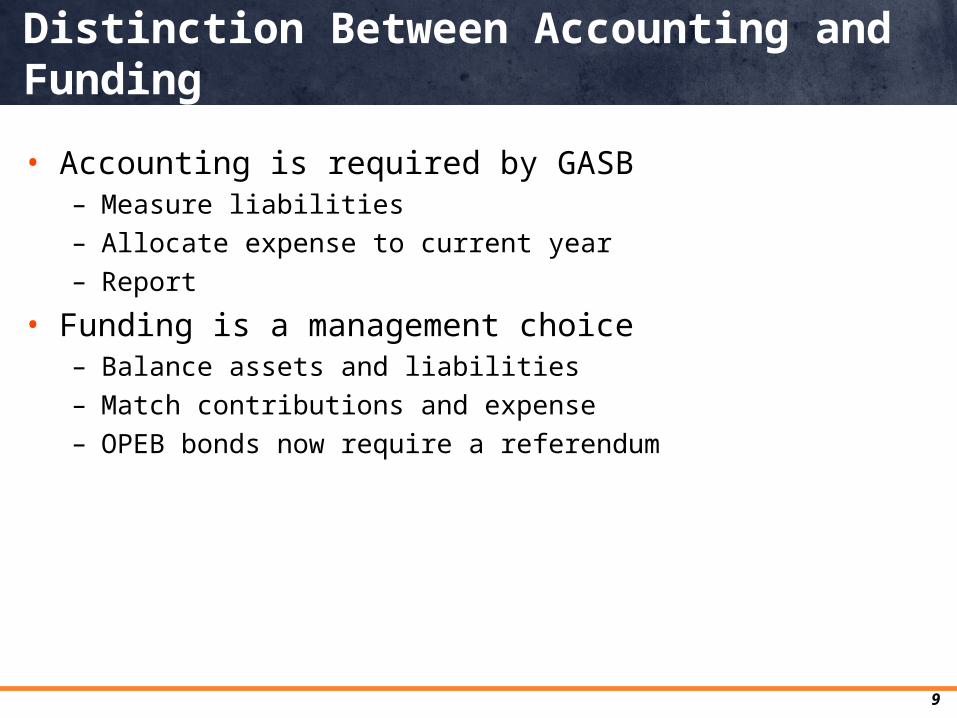

Distinction Between Accounting and Funding

• Accounting is required by GASB– Measure liabilities– Allocate expense to current year– Report

• Funding is a management choice– Balance assets and liabilities– Match contributions and expense– OPEB bonds now require a referendum

9

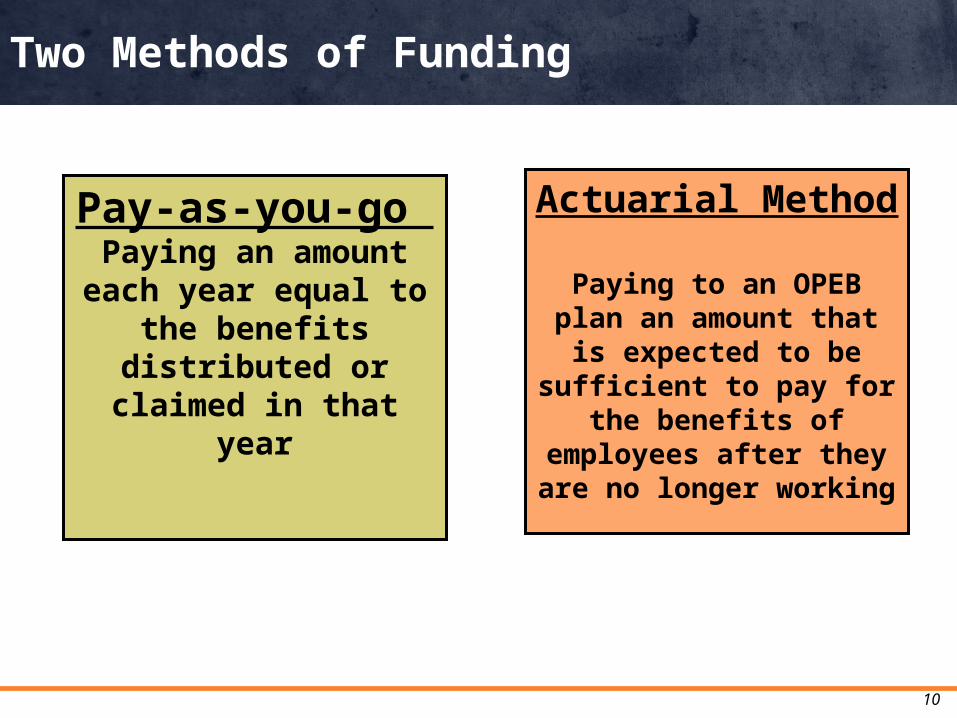

Two Methods of Funding

Actuarial Method Paying to an OPEB plan

an amount that is expected to be

sufficient to pay for the benefits of employees

after they are no longer working

Pay-as-you-go Paying an amount each

year equal to the benefits distributed or

claimed in that year

10

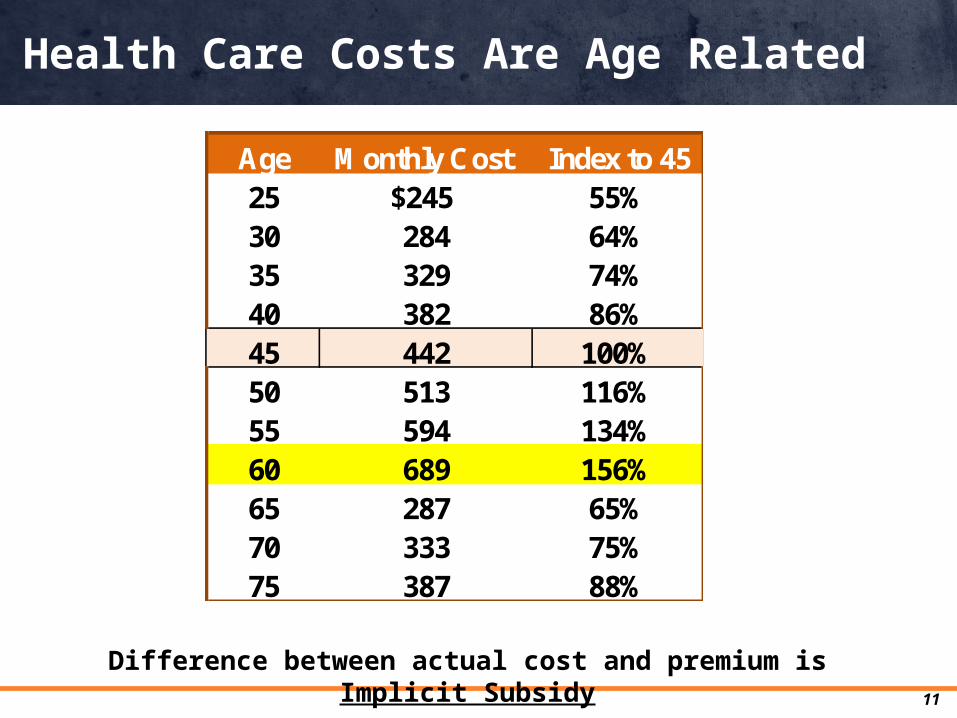

Health Care Costs Are Age Related

11

Age Monthly Cost Index to 4525 $245 55%30 284 64%35 329 74%40 382 86%45 442 100%50 513 116%55 594 134%60 689 156%65 287 65%70 333 75%75 387 88%

Difference between actual cost and premium is Implicit Subsidy

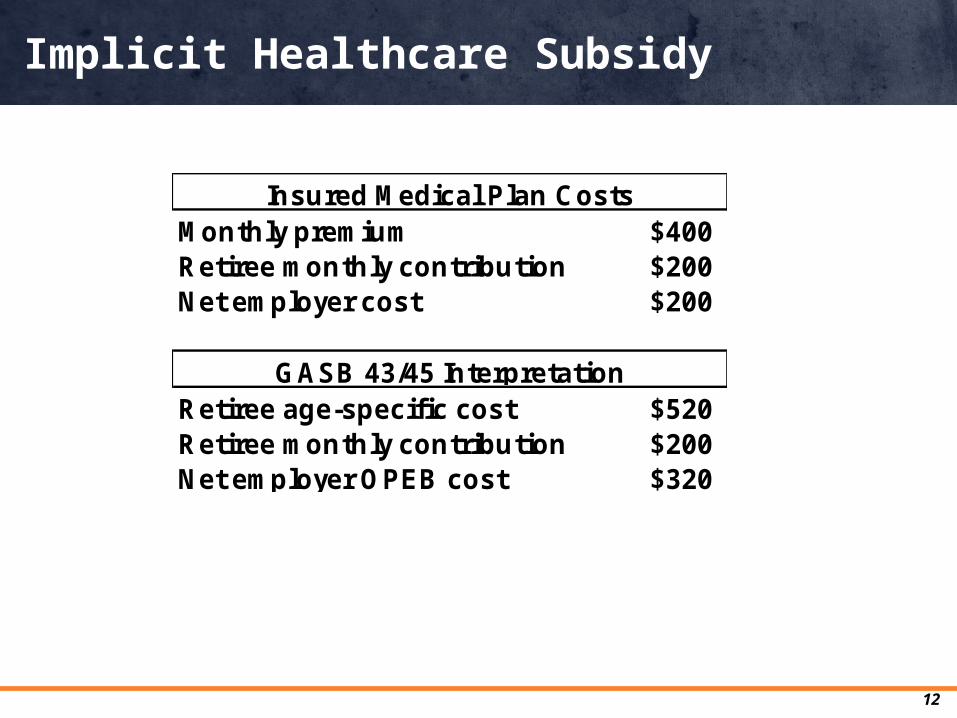

Implicit Healthcare Subsidy

12

Monthly premium $400Retiree monthly contribution $200Net employer cost $200

Retiree age-specific cost $520Retiree monthly contribution $200Net employer OPEB cost $320

GASB 43/45 Interpretation

Insured Medical Plan Costs

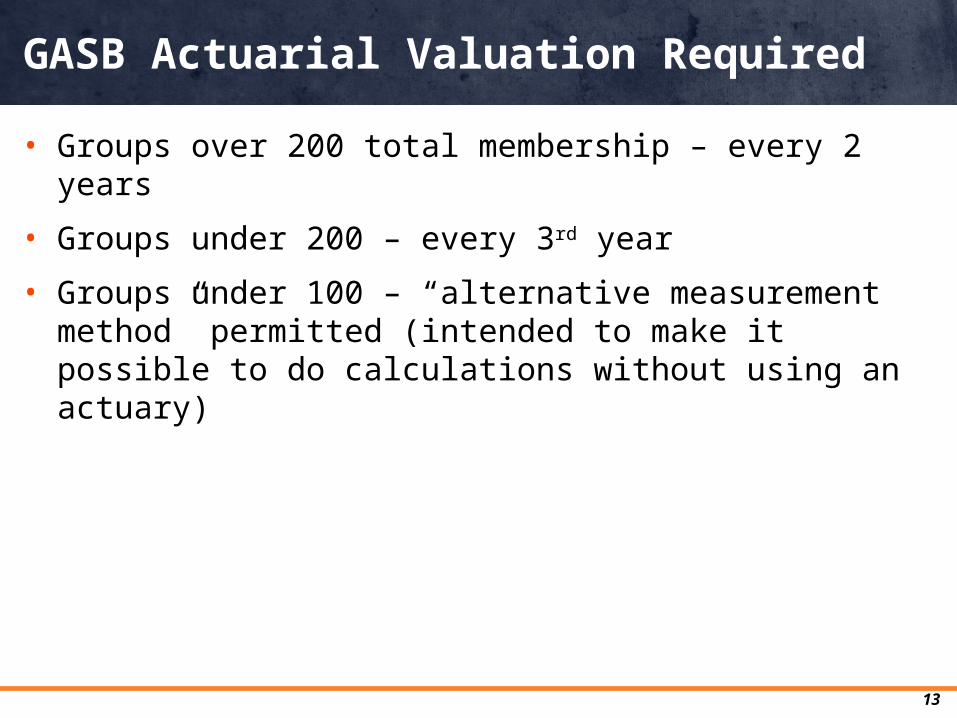

• Groups over 200 total membership – every 2 years

• Groups under 200 – every 3rd year

• Groups under 100 – “alternative measurement method” permitted (intended to make it possible to do calculations without using an actuary)

GASB Actuarial Valuation Required

13

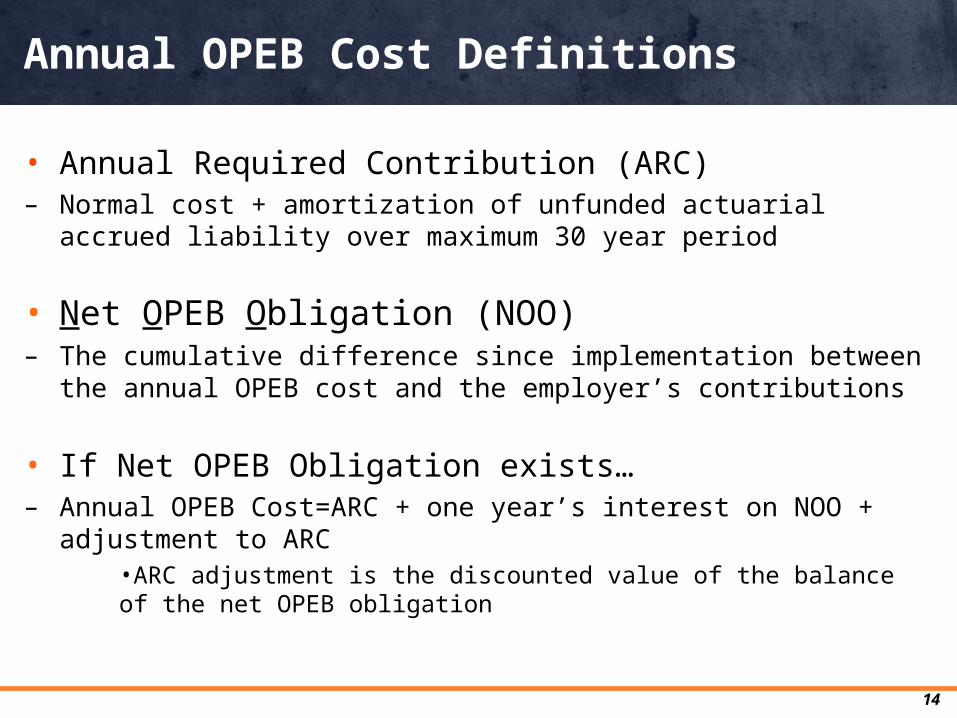

• Annual Required Contribution (ARC) – Normal cost + amortization of unfunded actuarial accrued liability over

maximum 30 year period

• Net OPEB Obligation (NOO)– The cumulative difference since implementation between the annual

OPEB cost and the employer’s contributions

• If Net OPEB Obligation exists…– Annual OPEB Cost=ARC + one year’s interest on NOO + adjustment to

ARC•ARC adjustment is the discounted value of the balance of the net OPEB obligation

Annual OPEB Cost Definitions

14

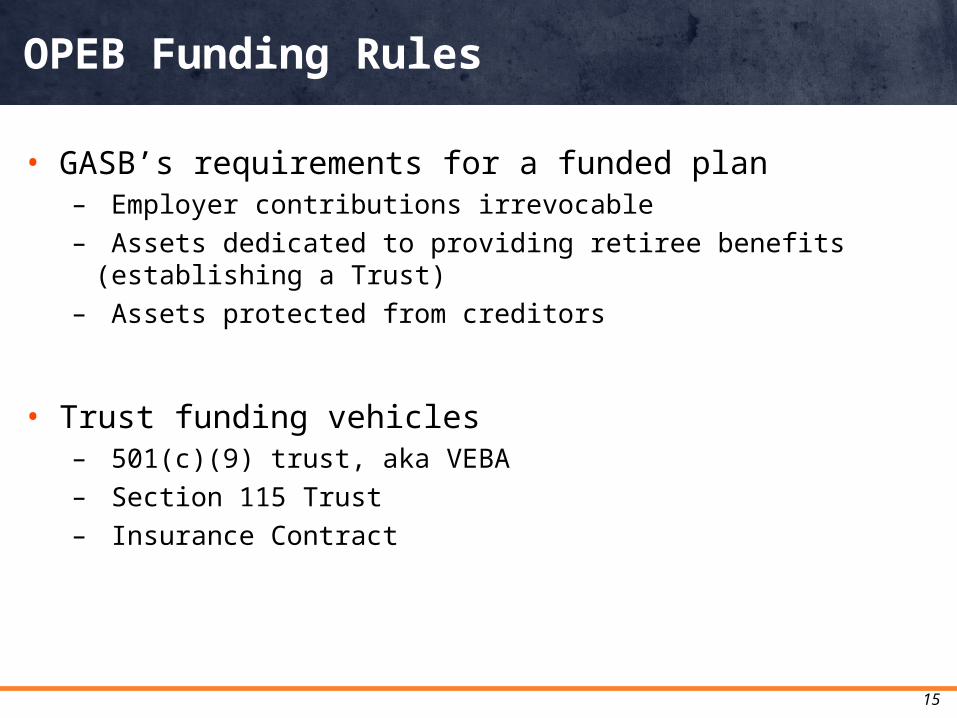

• GASB’s requirements for a funded plan– Employer contributions irrevocable– Assets dedicated to providing retiree benefits (establishing a Trust)– Assets protected from creditors

• Trust funding vehicles– 501(c)(9) trust, aka VEBA – Section 115 Trust– Insurance Contract

OPEB Funding Rules

15

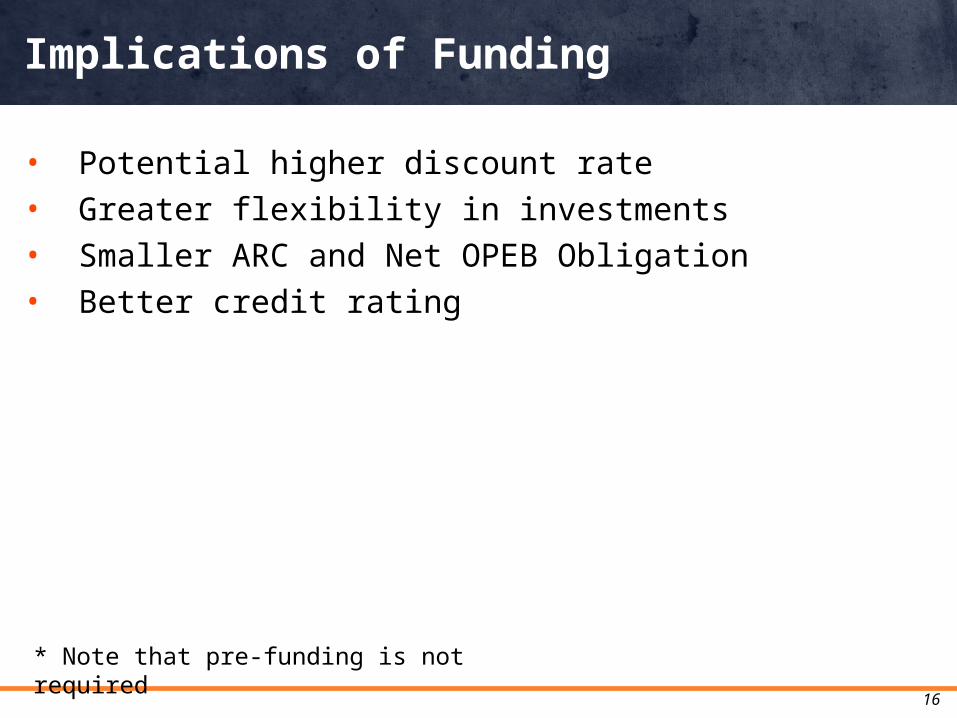

• Potential higher discount rate• Greater flexibility in investments• Smaller ARC and Net OPEB Obligation• Better credit rating

Implications of Funding

16

* Note that pre-funding is not required

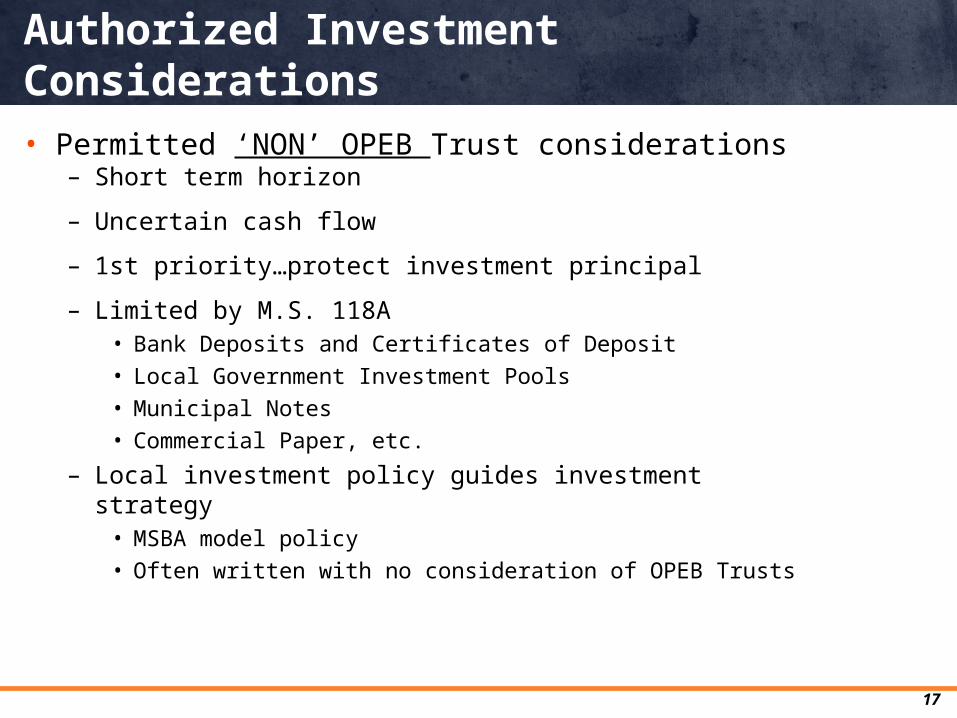

• Permitted ‘NON’ OPEB Trust considerations– Short term horizon

– Uncertain cash flow

– 1st priority…protect investment principal

– Limited by M.S. 118A• Bank Deposits and Certificates of Deposit

• Local Government Investment Pools

• Municipal Notes

• Commercial Paper, etc.

– Local investment policy guides investment strategy• MSBA model policy

• Often written with no consideration of OPEB Trusts

Authorized Investment Considerations

17

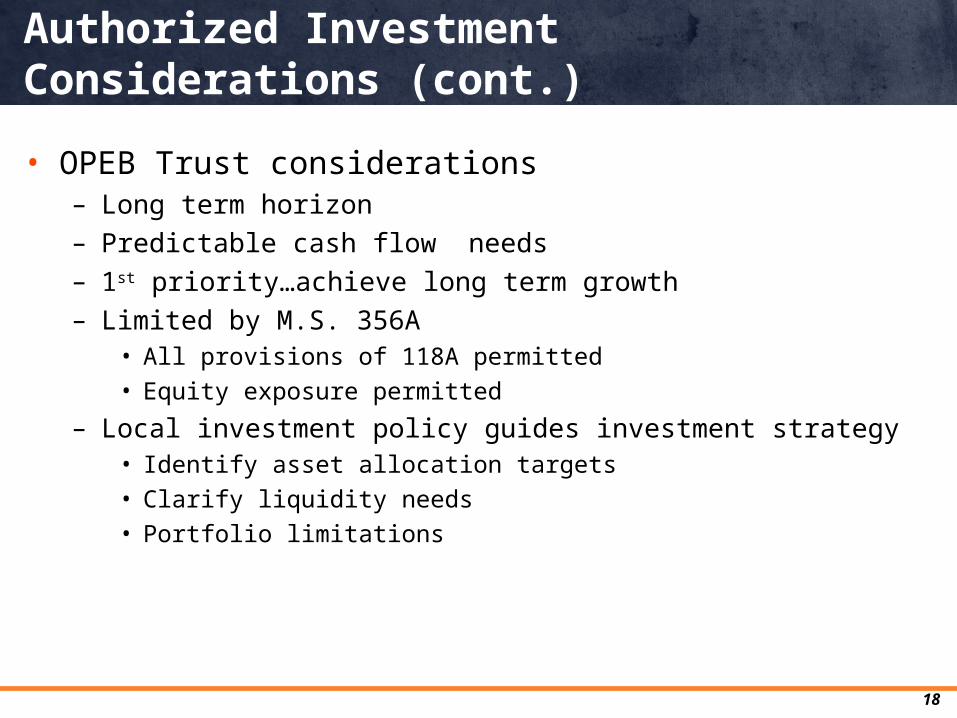

• OPEB Trust considerations– Long term horizon– Predictable cash flow needs– 1st priority…achieve long term growth– Limited by M.S. 356A

• All provisions of 118A permitted

• Equity exposure permitted

– Local investment policy guides investment strategy• Identify asset allocation targets

• Clarify liquidity needs

• Portfolio limitations

Authorized Investment Considerations (cont.)

18

Annualized 5 Year Rolling Equity & Bond Returns

Interval: 60

Return Values

-10.0%

30.0%

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

20.0%

22.0%

24.0%

26.0%

28.0%

Dec1950

Dec2012

Dec1955

Dec1960

Dec1965

Dec1970

Dec1975

Dec1980

Dec1985

Dec1990

Dec1995

Dec2000

Dec2005

DOMESTIC EQUITYGeometric Mean: 10.67%

DOMESTIC EQUITYGeometric Mean: 10.67%

AGGREGATEFIXED INCOME

Geometric Mean: 5.60%

AGGREGATEFIXED INCOME

Geometric Mean: 5.60%U.S. INFLATION

Geometric Mean: 3.86%

U.S. INFLATION

Geometric Mean: 3.86%

Long-term Equity and Bond Returns Have Outpaced Inflation

19

_____ Consumer Price Index

S&P 500 TR Barclays Aggregate Bond (1976-2011) and 50% Intermediate Corporate; 25% Int. Govt; and 25% US Long-term Govt (1950-1976)

Source: Morningstar En Corr/ Ibbotson Associates

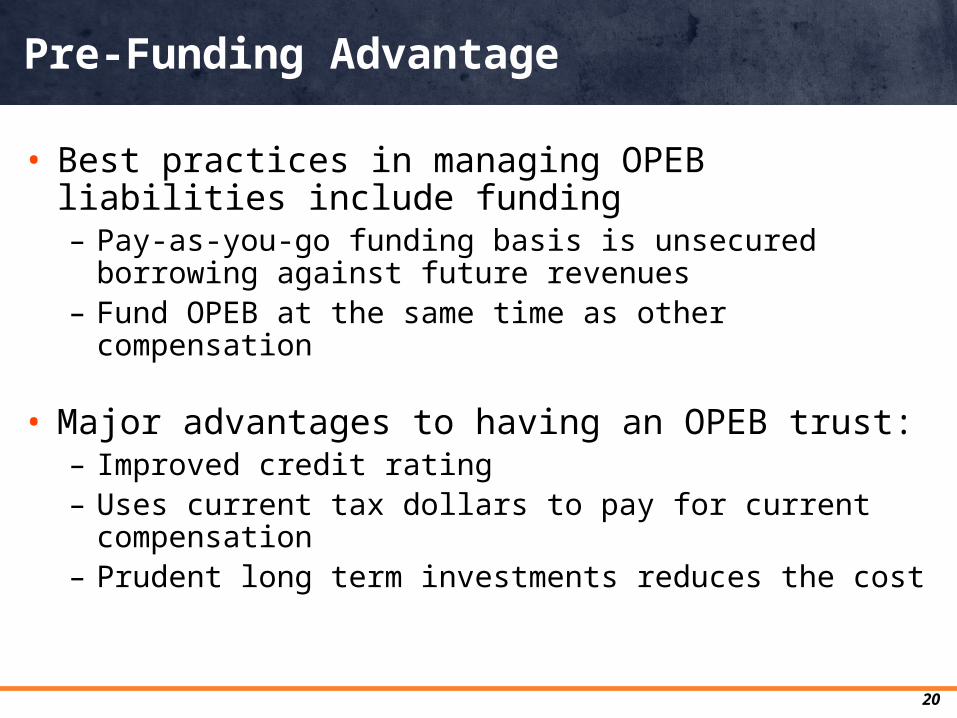

• Best practices in managing OPEB liabilities include funding– Pay-as-you-go funding basis is unsecured borrowing

against future revenues– Fund OPEB at the same time as other compensation

• Major advantages to having an OPEB trust:– Improved credit rating– Uses current tax dollars to pay for current compensation– Prudent long term investments reduces the cost

Pre-Funding Advantage

20

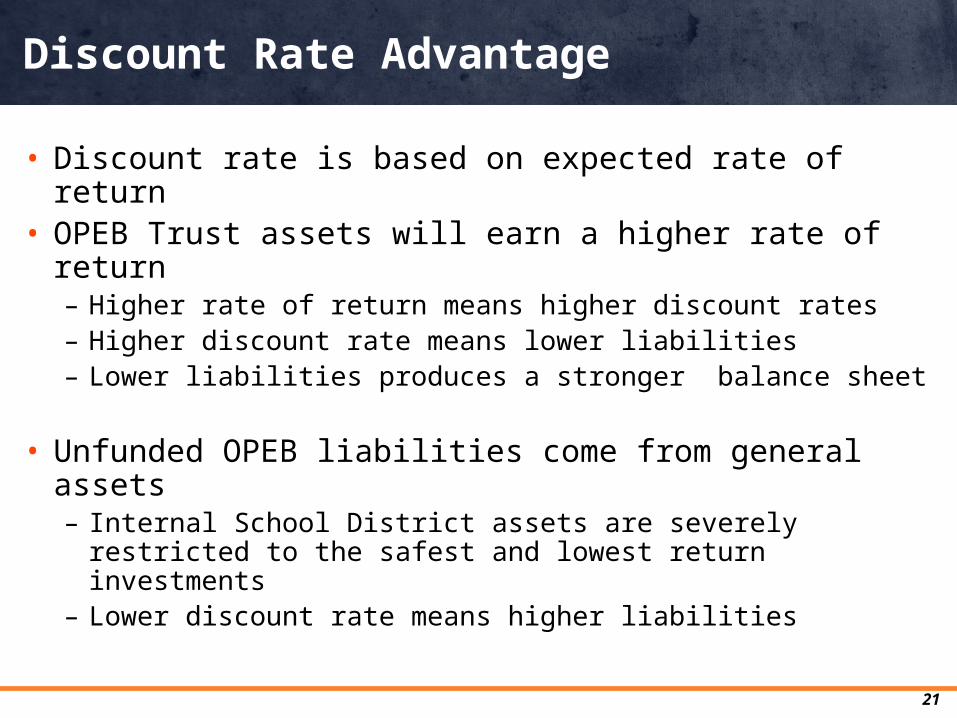

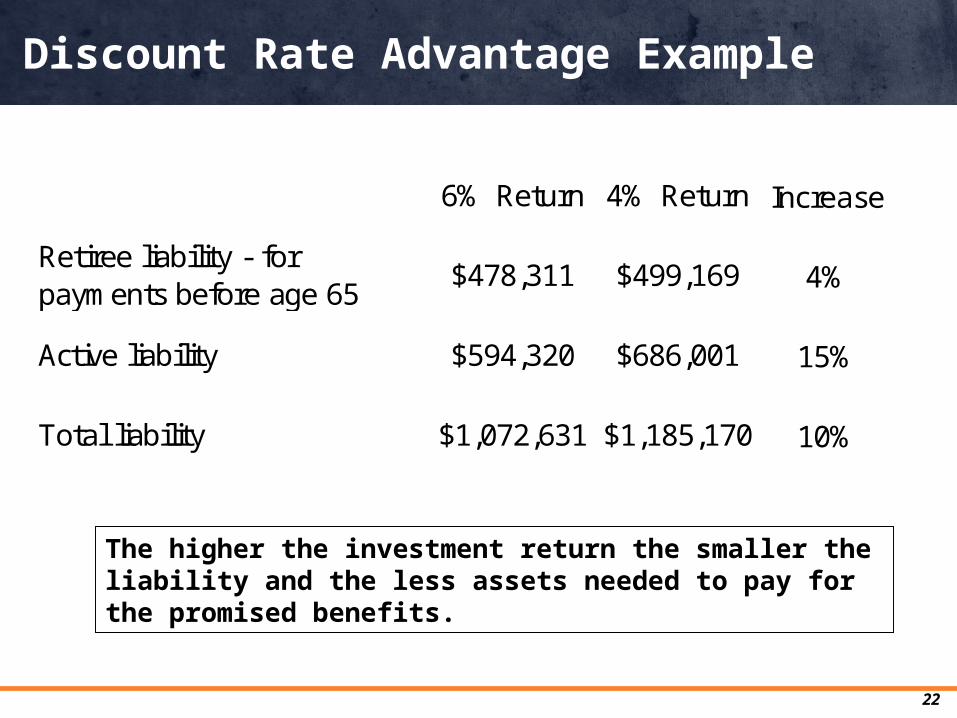

• Discount rate is based on expected rate of return• OPEB Trust assets will earn a higher rate of return

– Higher rate of return means higher discount rates– Higher discount rate means lower liabilities– Lower liabilities produces a stronger balance sheet

• Unfunded OPEB liabilities come from general assets – Internal School District assets are severely restricted to the

safest and lowest return investments– Lower discount rate means higher liabilities

Discount Rate Advantage

21

6% Return 4% Return Increase

Retiree liability - for payments before age 65

$478,311 $499,169 4%

Active liability $594,320 $686,001 15%

Total liability $1,072,631 $1,185,170 10%

Discount Rate Advantage Example

22

The higher the investment return the smaller the liability and the less assets needed to pay for the promised benefits.

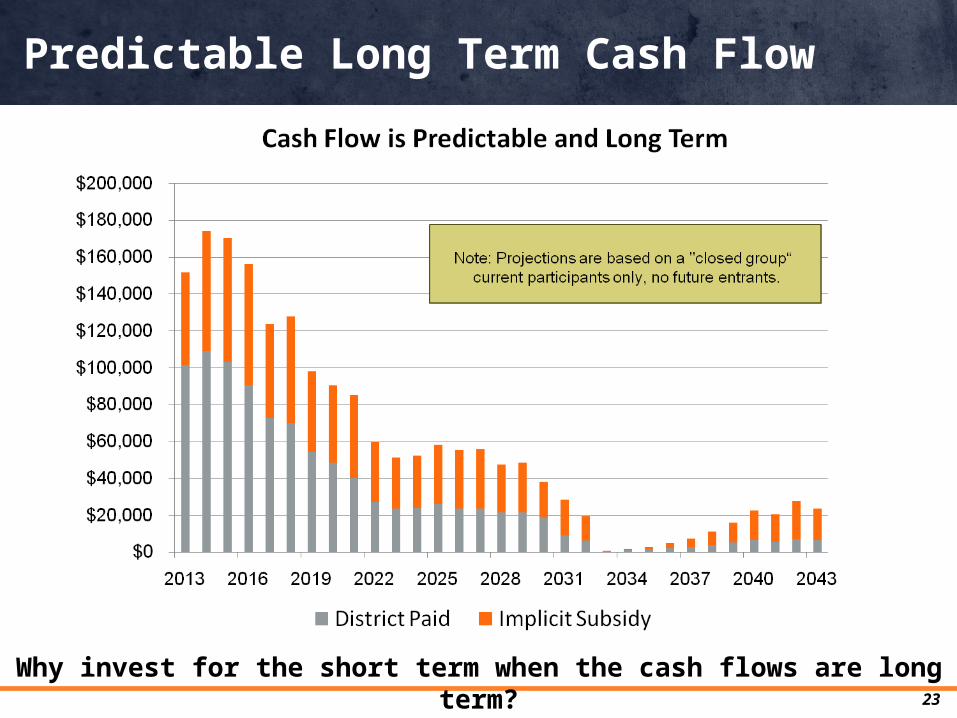

Predictable Long Term Cash Flow

23

Why invest for the short term when the cash flows are long term?

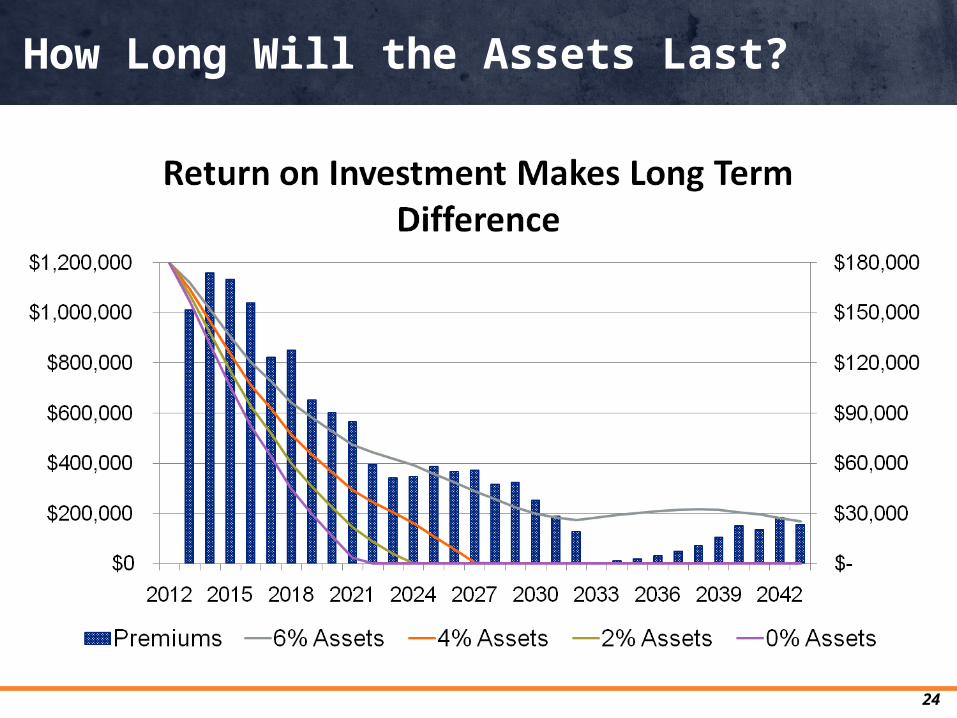

How Long Will the Assets Last?

24

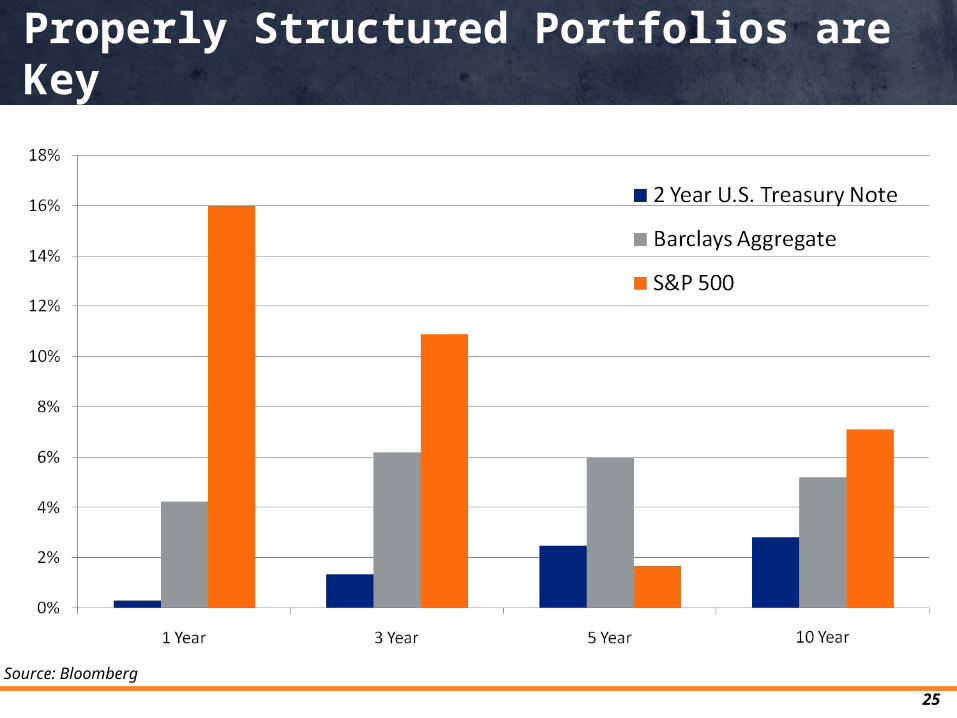

Properly Structured Portfolios are Key

25

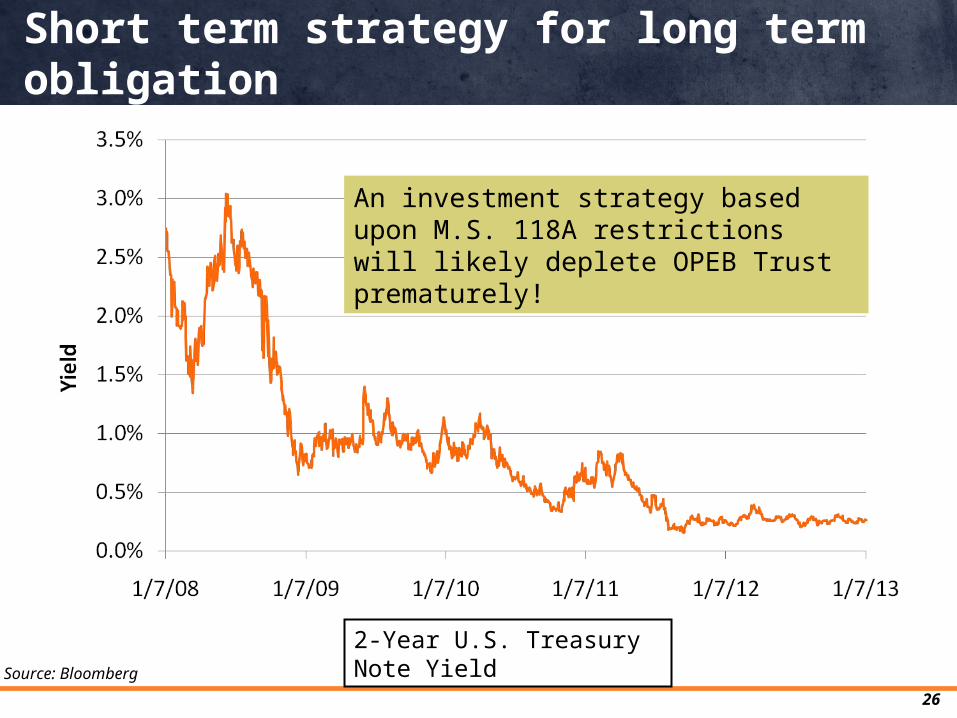

Source: Bloomberg

Short term strategy for long term obligation

Source: Bloomberg

2-Year U.S. Treasury Note Yield

An investment strategy based upon M.S. 118A restrictions will likely deplete OPEB Trust prematurely!

26

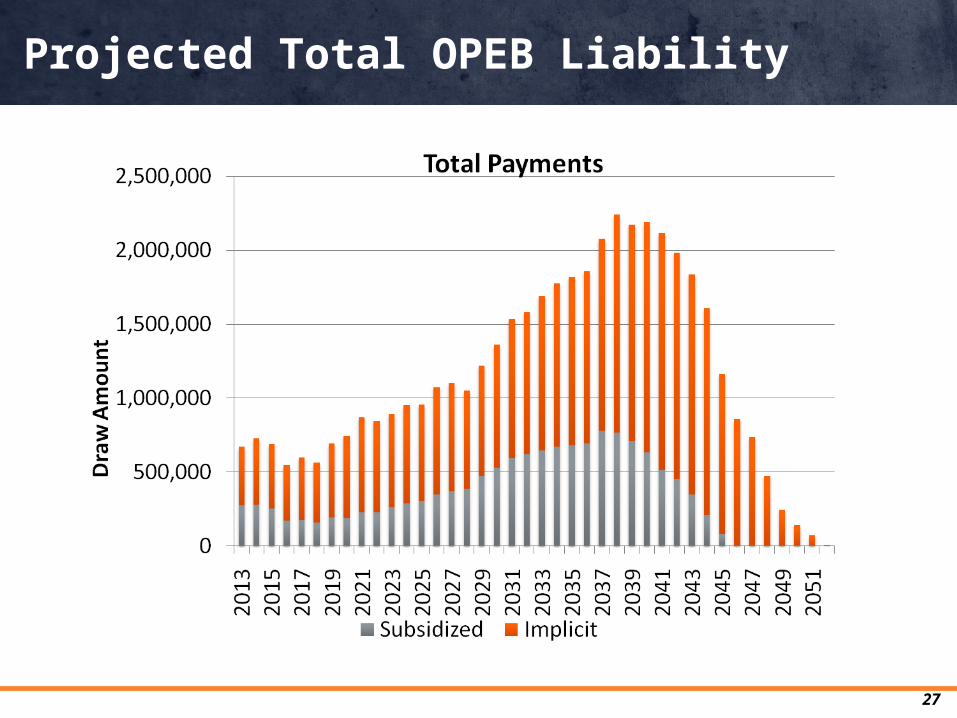

27

Projected Total OPEB Liability

28

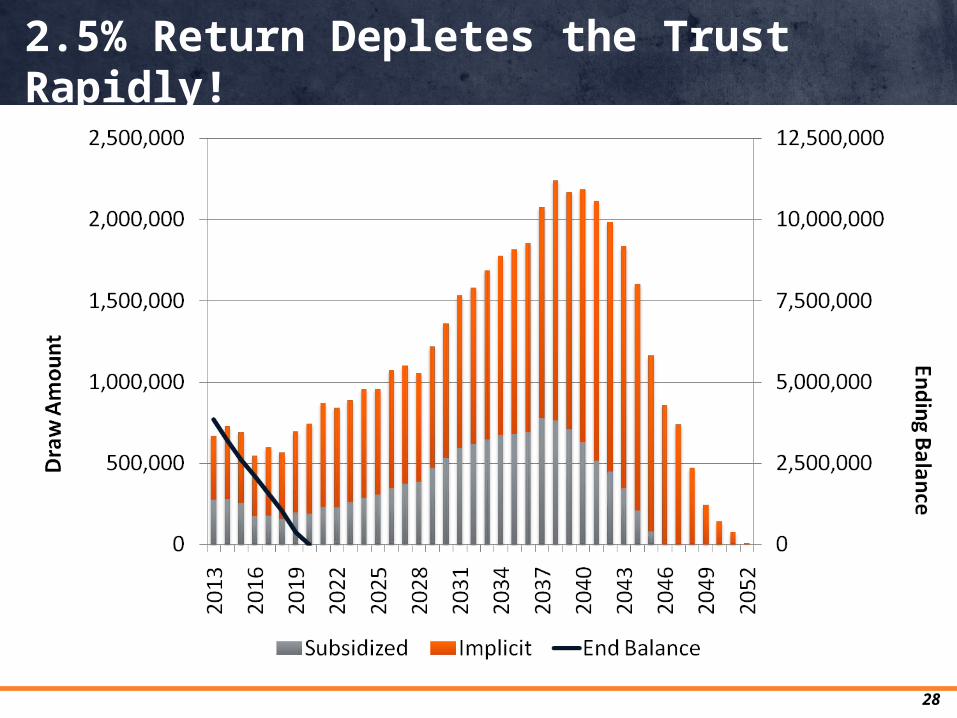

2.5% Return Depletes the Trust Rapidly!

29

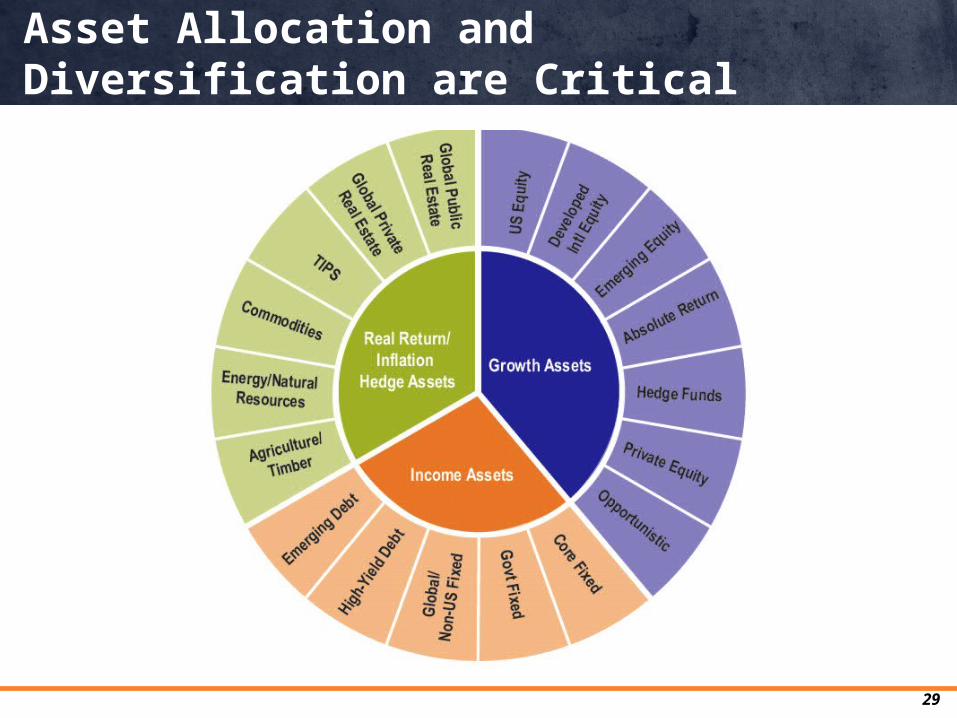

Asset Allocation and Diversification are Critical

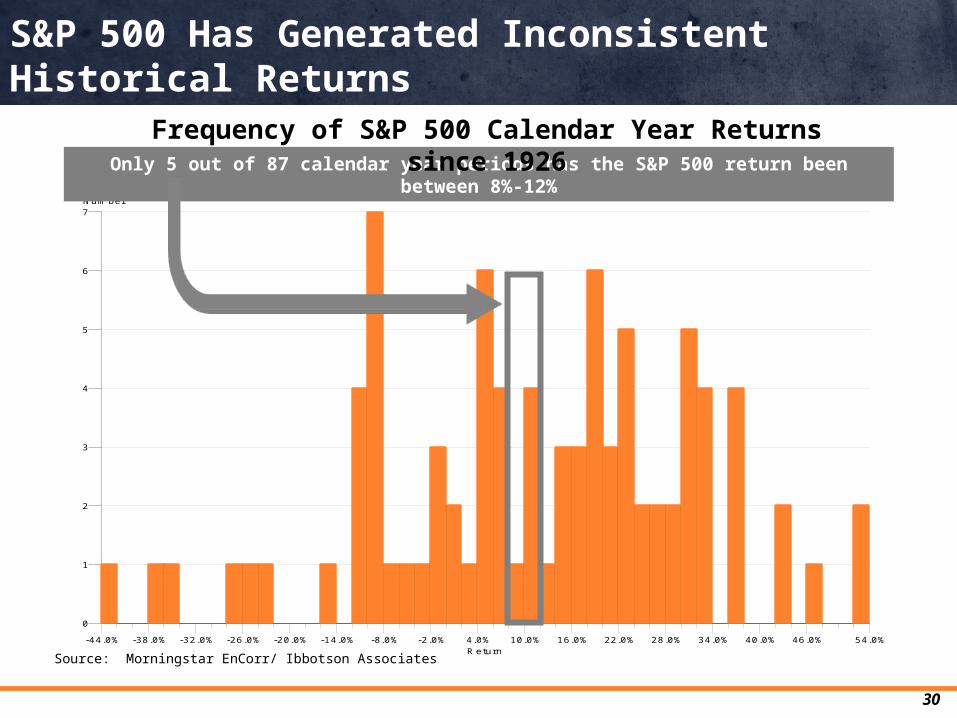

S&P 500 Has Generated Inconsistent Historical Returns

Source: Morningstar EnCorr/ Ibbotson Associates

30

IA S BBI S &P 500 T R US D: De ce m b e r 1926 - De ce m b e r 2012

Return

Num berIA S BBI S &P 500 T R US D: De ce m b e r 1926 - De ce m b e r 2012

-44.0% 54.0%-38.0% -32.0% -26.0% -20.0% -14.0% -8.0% -2.0% 4.0% 10.0% 16.0% 22.0% 28.0% 34.0% 40.0% 46.0%

0

7

1

2

3

4

5

6

Only 5 out of 87 calendar year periods has the S&P 500 return been between 8%-12%

Frequency of S&P 500 Calendar Year Returns since 1926

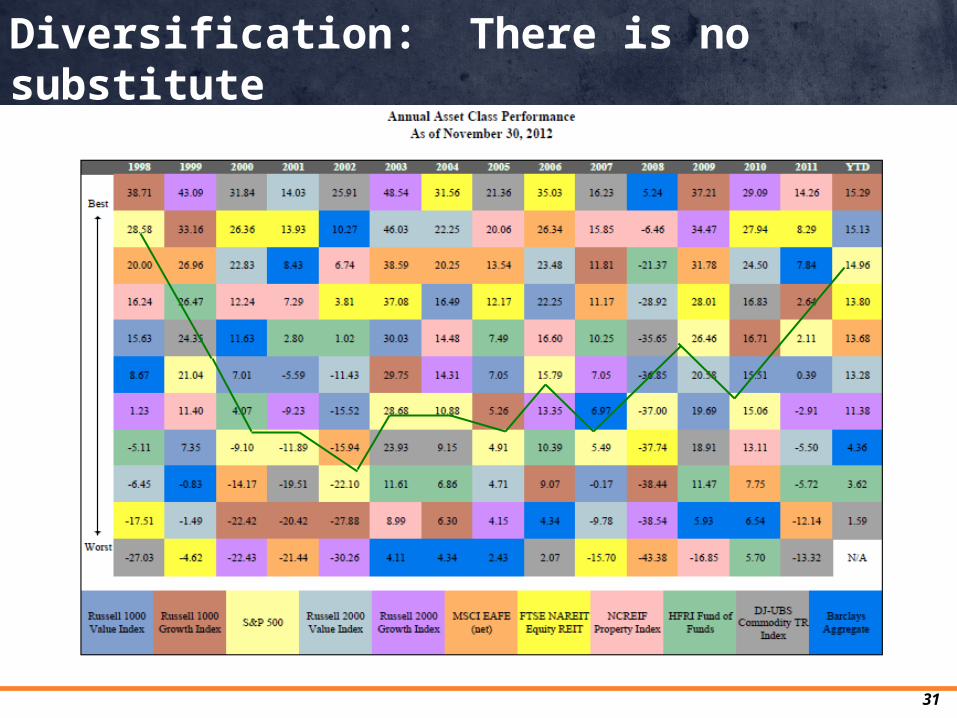

Diversification: There is no substitute

31

32

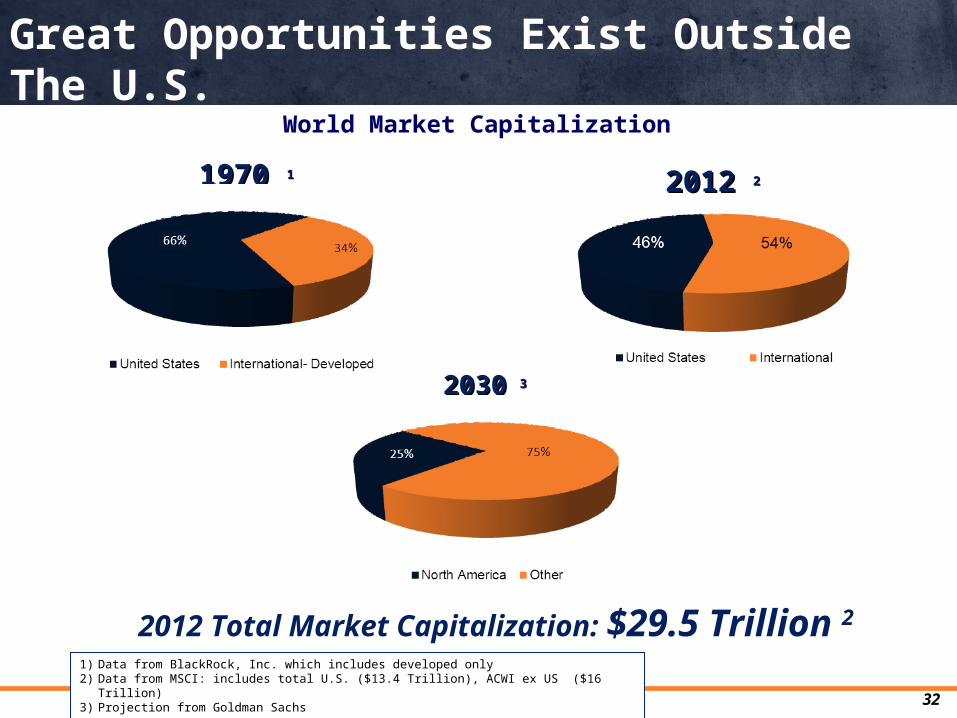

Great Opportunities Exist Outside The U.S.

World Market Capitalization

2012 Total Market Capitalization: $29.5 Trillion 2

1) Data from BlackRock, Inc. which includes developed only2) Data from MSCI: includes total U.S. ($13.4 Trillion), ACWI ex US ($16 Trillion)3) Projection from Goldman Sachs

1970 1970 11 2012 2012 22

20302030 33

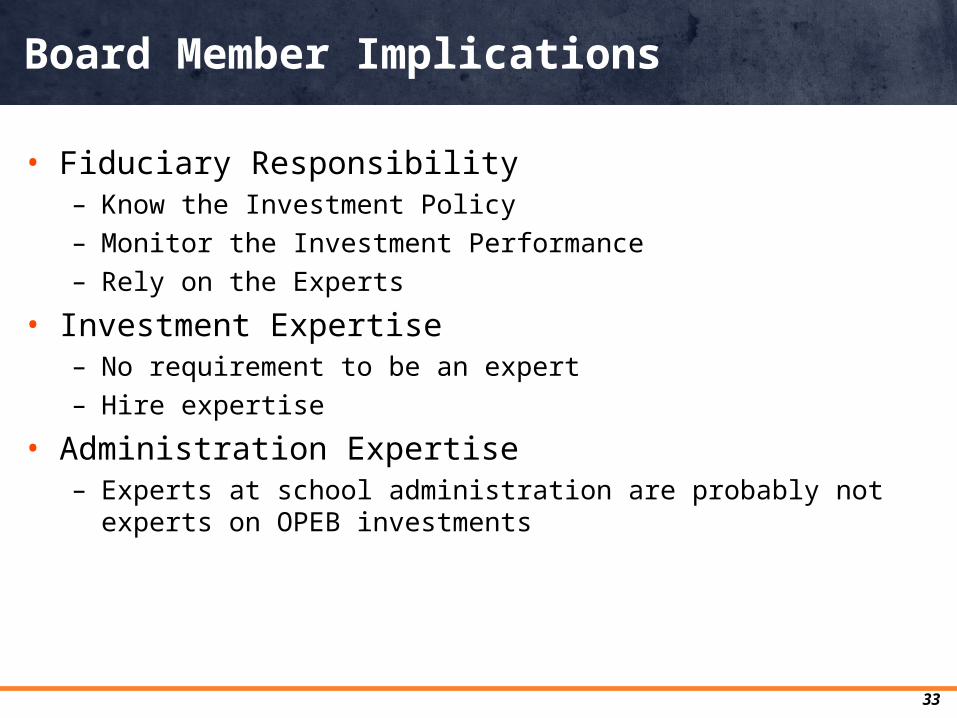

• Fiduciary Responsibility– Know the Investment Policy– Monitor the Investment Performance– Rely on the Experts

• Investment Expertise– No requirement to be an expert– Hire expertise

• Administration Expertise– Experts at school administration are probably not experts on OPEB

investments

Board Member Implications

33

DANGER in Playing it Safe

• Safe does not automatically mean prudent– Fiduciary duty to be prudent

• Bond proceeds may be depleted prior to final bond payment • Investment earnings may be lower than bond interest• Disappointed constituents• Less money for school operations• Lost opportunity cost• Headline risk

34

35

School Board Action Plan

• Estimate the projected life of the OPEB Trust• Review investment policy and its handling of OPEB• Amend policy and investment strategy appropriately

A detailed actuarial report is the start of the process

• Retiree medical cash flows are less predictable than retirement benefits

• Changes in federal health care laws and benefits materially affect the projected benefits

• Changes in investment policy materially affect investment return expectations and the discount rate

• Health care cost inflation is higher and more variable than general consumer price inflation

Actuarial Caveats

36

Any investment advice in this document is provided solely by PFM Asset Management LLC. PFM Asset Management LLC (“PFMAM”) is an investment advisor registered under the Investment Advisers Act of 1940. PFM Advisors is a division of PFM Asset Management LLC. Public Financial Management Inc. is not providing and is not responsible for any investment advice herein.

This material is based on information obtained from sources generally believed to be reliable and available to the public, however PFM Asset Management LLC cannot guarantee its accuracy, completeness or suitability. This material is for general information purposes only and is not intended to provide specific advice or a specific recommendation. All statements as to what will or may happen under certain circumstances are based on assumptions, some but not all of which are noted in the presentation. Assumptions may or may not be proven correct as actual events occur, and results may depend on events outside of your or our control. Changes in assumptions may have a material effect on results. Past performance does not necessarily reflect and is not a guaranty of future results. The information contained in this presentation is not an offer to purchase or sell any securities.

Disclaimers

37