operational forum meeting - national grid plc

TRANSCRIPT

Place your chosen image

here. The four corners

must just cover the

arrow tips. For covers,

the three pictures should

be the same size and in a

straight line.

Operational Forum Meeting

16 November 2016, 10:30AM

Radisson Grafton Hotel, 130 Tottenham Court Road, London.

1

Place your chosen image

here. The four corners

must just cover the

arrow tips. For covers,

the three pictures should

be the same size and in a

straight line.

System Management Principles Statement

Summary of balancing actions and breaches for September and October 2016

Performance compared to last year

2

3

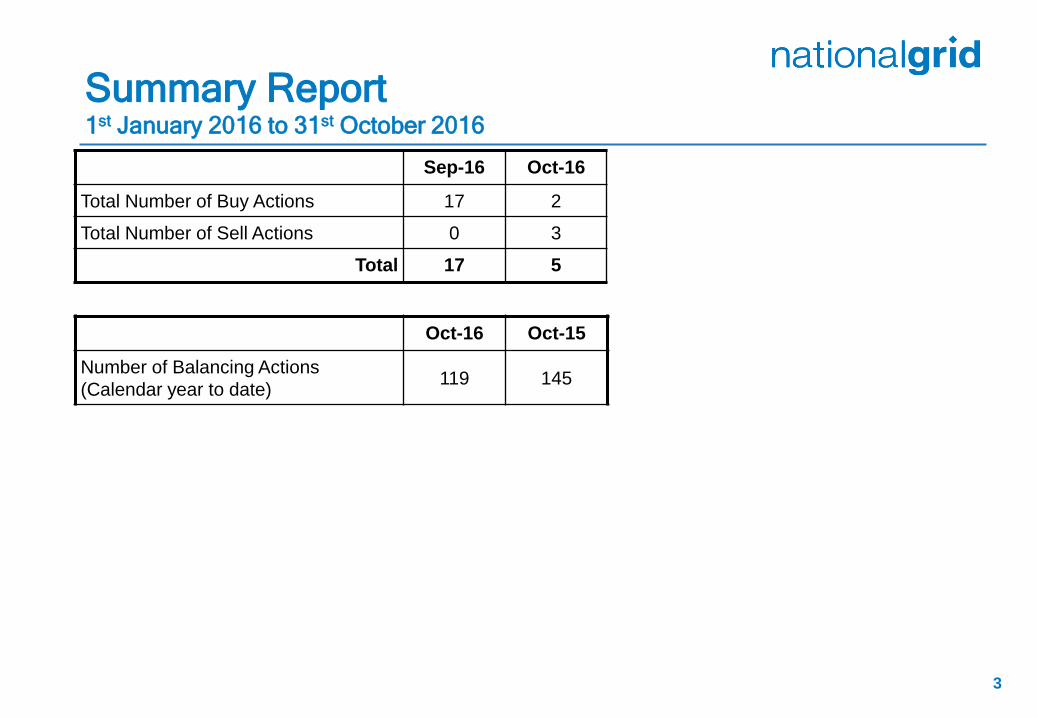

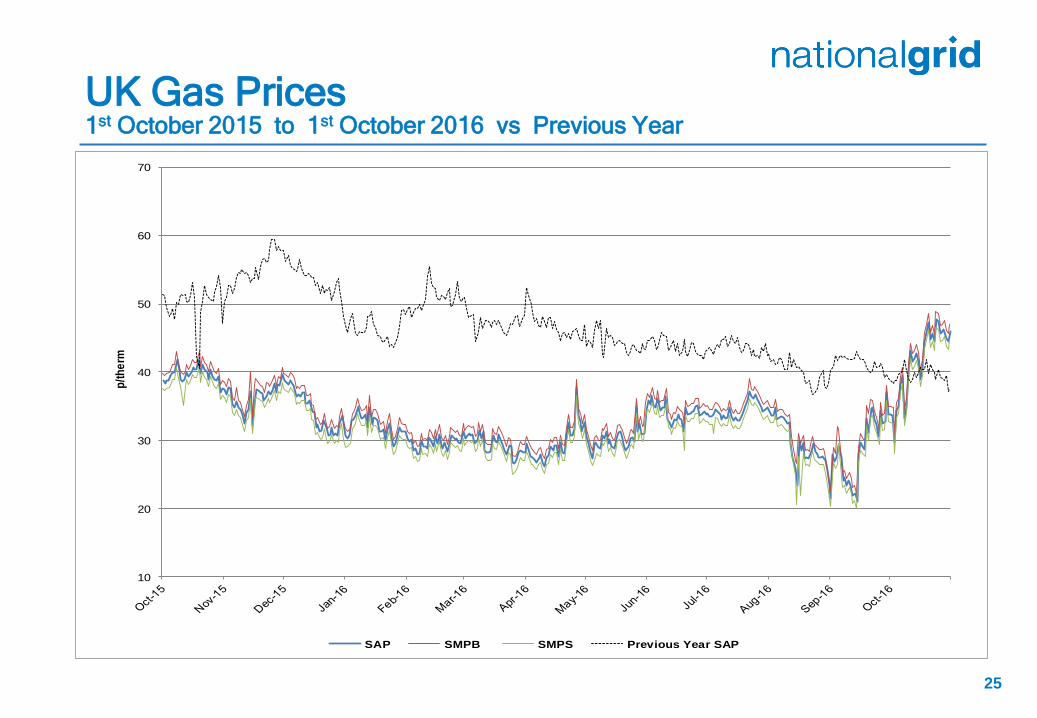

1st January 2016 to 31st October 2016

Summary Report

Sep-16 Oct-16

Total Number of Buy Actions 17 2

Total Number of Sell Actions 0 3

Total 17 5

Oct-16 Oct-15

Number of Balancing Actions

(Calendar year to date) 119 145

Place your chosen image

here. The four corners

must just cover the

arrow tips. For covers,

the three pictures should

be the same size and in a

straight line.

Operational Overview

4

Place your chosen image

here. The four corners

must just cover the

arrow tips. For covers,

the three pictures should

be the same size and in a

straight line.

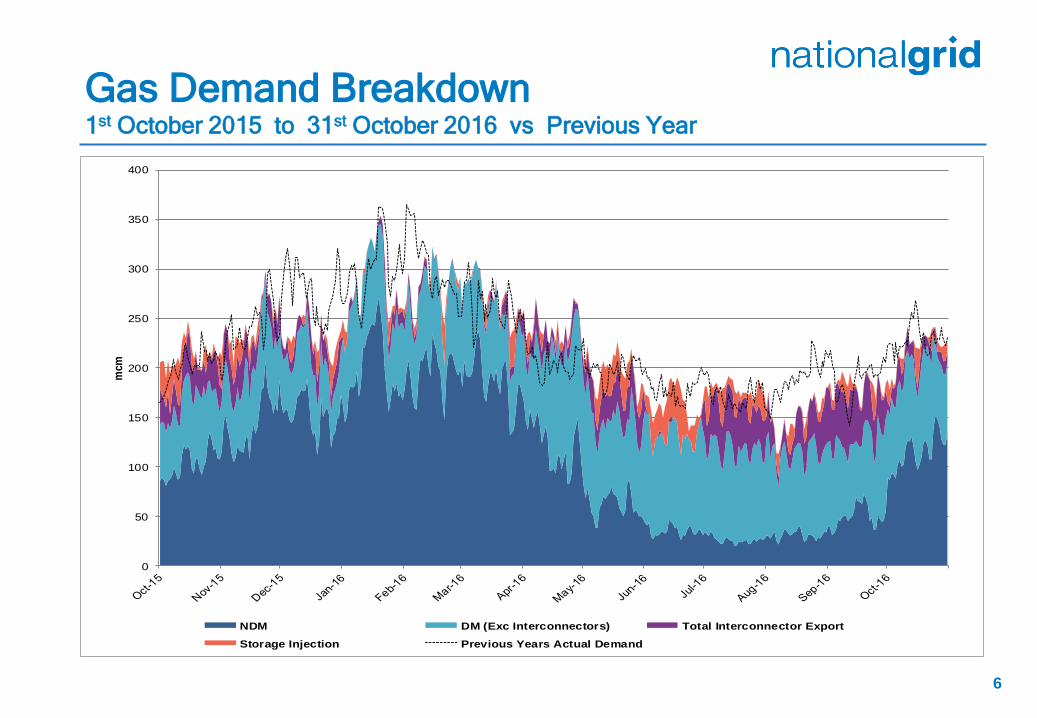

Demands

6

6

1st October 2015 to 31st October 2016 vs Previous Year

Gas Demand Breakdown

0

50

100

150

200

250

300

350

400

mcm

NDM DM (Exc Interconnectors) Total Interconnector Export

Storage Injection Previous Years Actual Demand

47% 44%

63%57%

51% 50% 52%

22%24%

17%

17%22%

18%

29%

23% 25%

8%

12% 15%20%

10%

5% 3%6% 11% 7% 8% 4%

4% 5% 5% 4% 4% 4% 5%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010 2011 2012 2013 2014 2015 2016

7

1st October to 31st October 2016 vs Same Period in Previous Years

Gas Demand Breakdown

Interconnector demand increased

slightly with a similar reduction seen

in LDZ demand

Interconnectors Power Station Industrial LDZ Storage

8

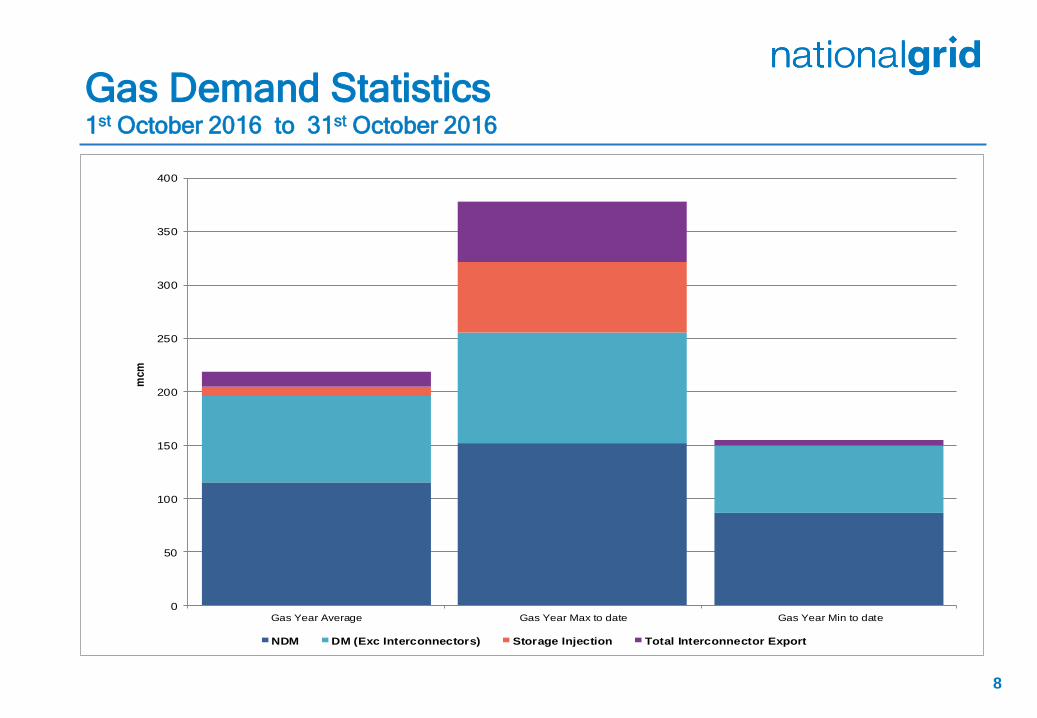

1st October 2016 to 31st October 2016

Gas Demand Statistics

0

50

100

150

200

250

300

350

400

Gas Year Average Gas Year Max to date Gas Year Min to date

mcm

NDM DM (Exc Interconnectors) Storage Injection Total Interconnector Export

9

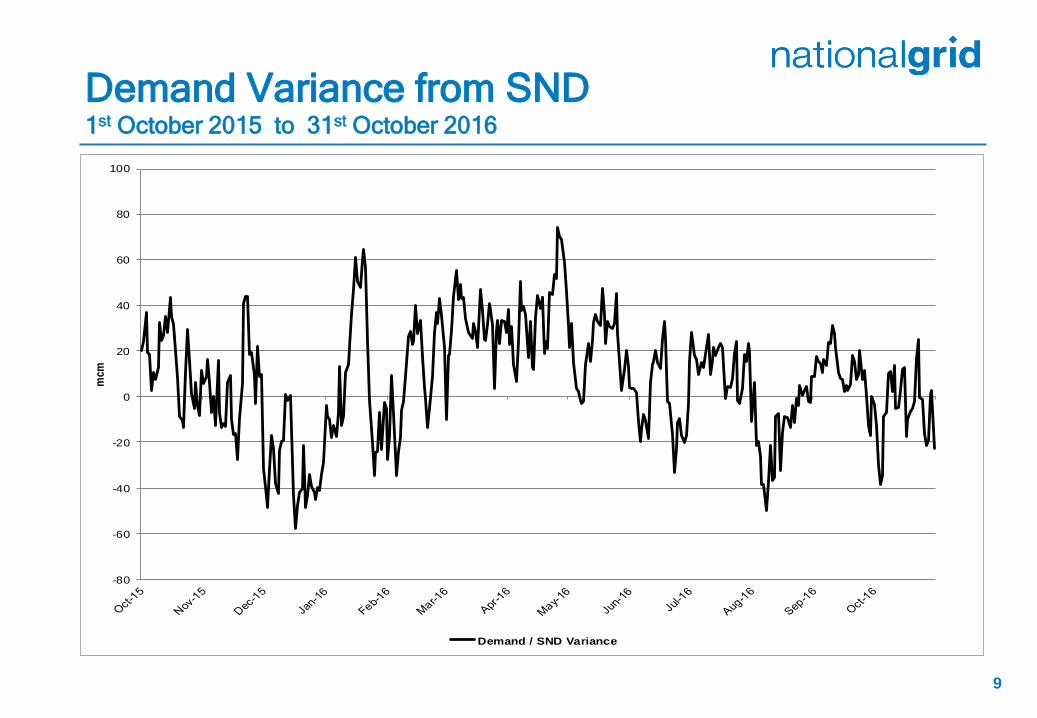

1st October 2015 to 31st October 2016

Demand Variance from SND

-80

-60

-40

-20

0

20

40

60

80

100

mcm

Demand / SND Variance

10

1st October 2015 to 31st October 2016

Gas Demand Vs SND / Cold / Warm

0

50

100

150

200

250

300

350

400

mcm

Total Demand SND Cold Warm

11

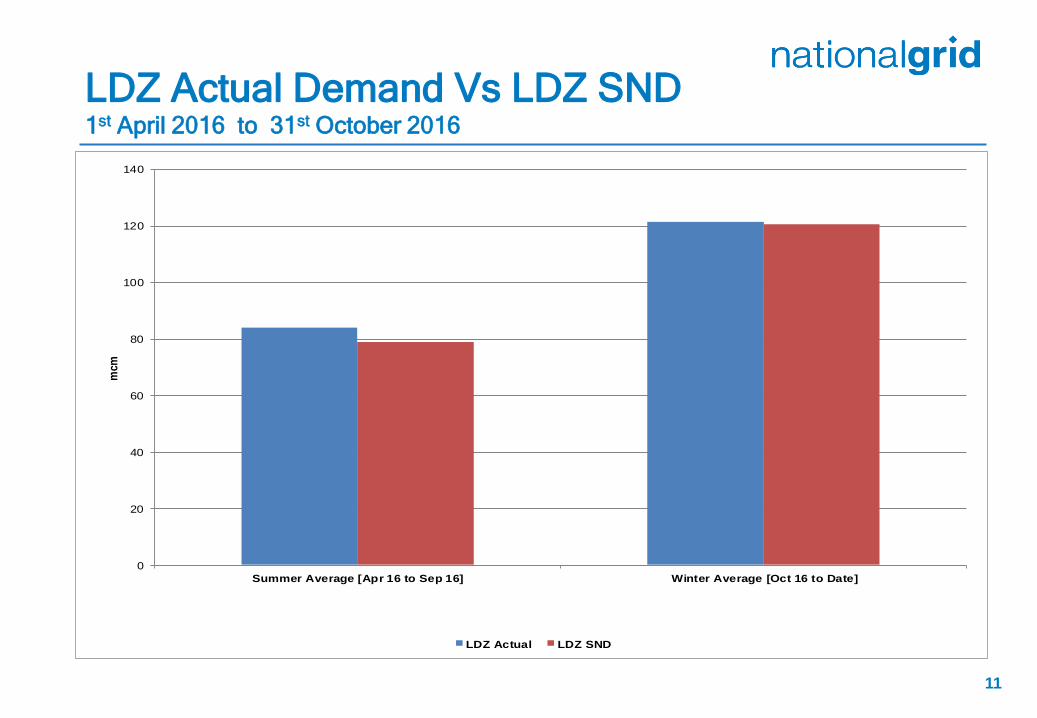

1st April 2016 to 31st October 2016

LDZ Actual Demand Vs LDZ SND

0

20

40

60

80

100

120

140

Summer Average [Apr 16 to Sep 16] Winter Average [Oct 16 to Date]

mcm

LDZ Actual LDZ SND

12

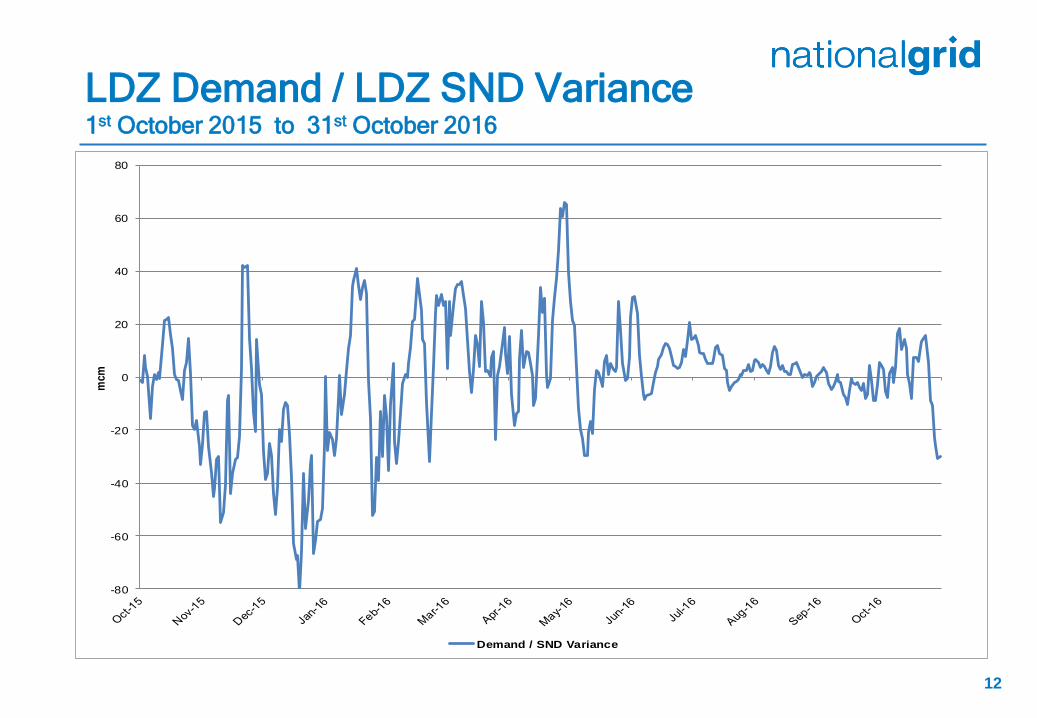

1st October 2015 to 31st October 2016

LDZ Demand / LDZ SND Variance

-80

-60

-40

-20

0

20

40

60

80

mcm

Demand / SND Variance

13

1st October 2015 to 31st October 2016

Gas Consumption for Power Generation

0

10

20

30

40

50

60

70

80

90

mcm

Actual for Power Generation Previous Year

Place your chosen image

here. The four corners

must just cover the

arrow tips. For covers,

the three pictures should

be the same size and in a

straight line.

Supplies

14

15

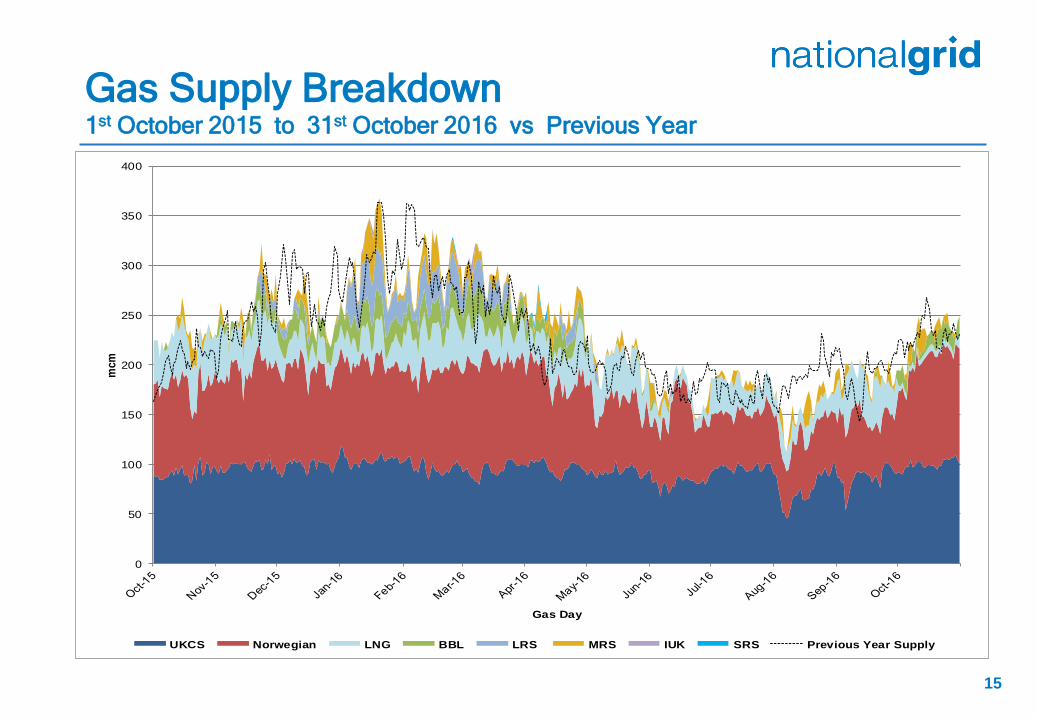

1st October 2015 to 31st October 2016 vs Previous Year

Gas Supply Breakdown

0

50

100

150

200

250

300

350

400

mcm

Gas Day

UKCS Norwegian LNG BBL LRS MRS IUK SRS Previous Year Supply

48% 48%

39%44% 41% 40%

43%

24% 22% 39%36% 43%

38%

45%

18% 22% 5%10% 5% 19%

3%6%

6%

13%7% 6%

0%6%

3% 2% 3% 3% 5% 2% 3%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010 2011 2012 2013 2014 2015 2016

16

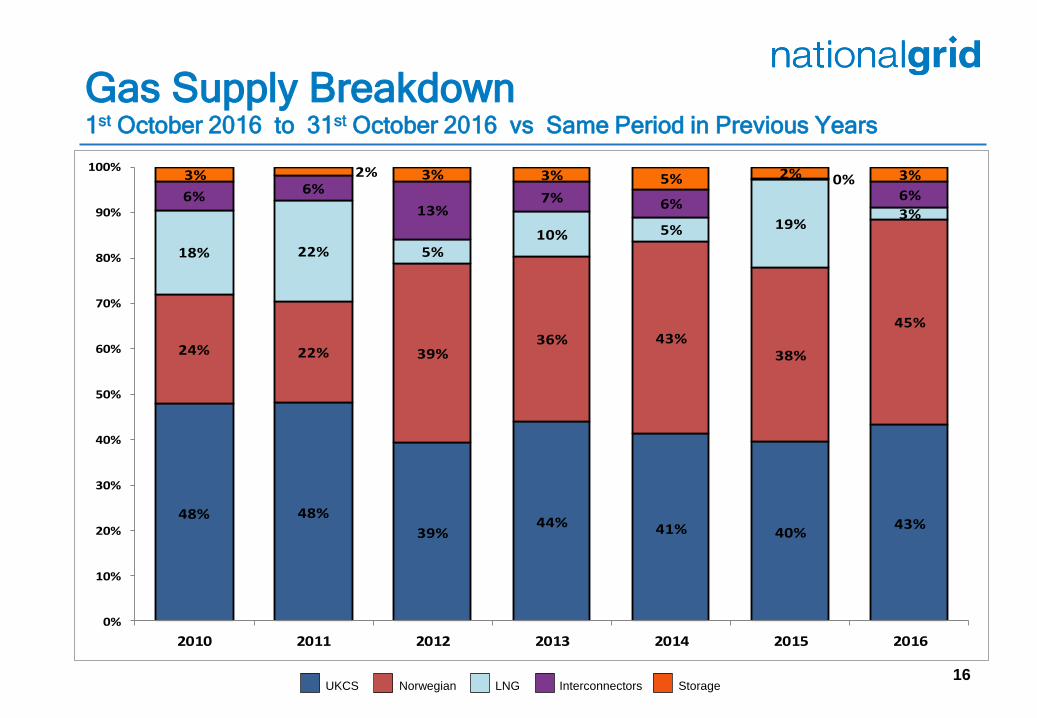

1st October 2016 to 31st October 2016 vs Same Period in Previous Years

Gas Supply Breakdown

Interconnectors UKCS LNG Norwegian Storage

17

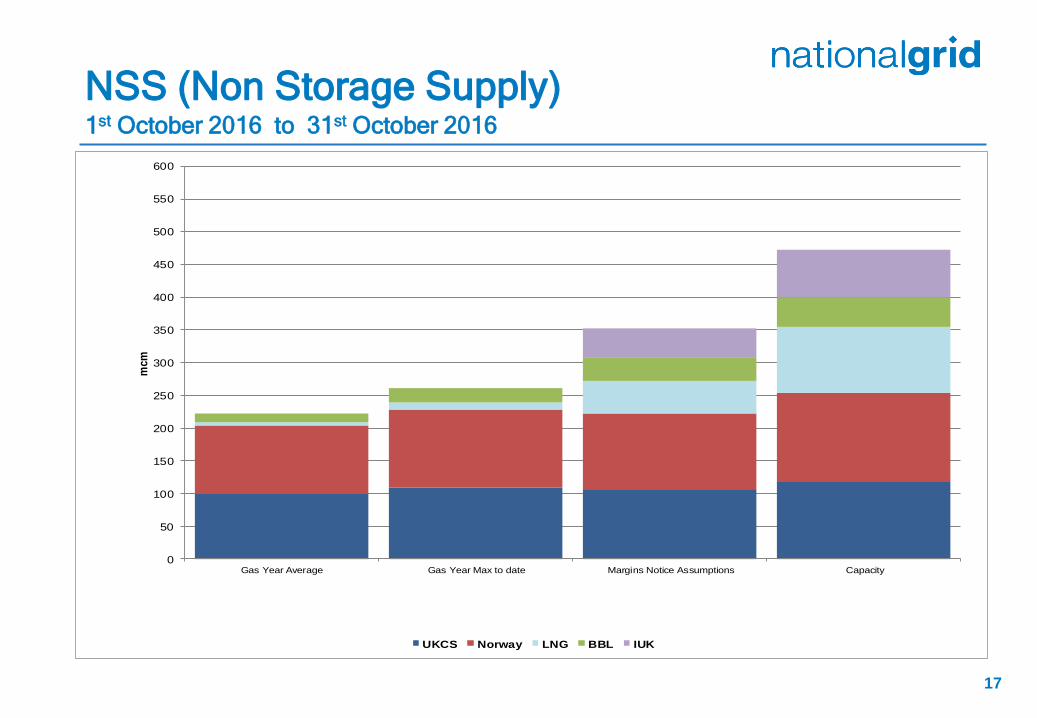

1st October 2016 to 31st October 2016

NSS (Non Storage Supply)

0

50

100

150

200

250

300

350

400

450

500

550

600

Gas Year Average Gas Year Max to date Margins Notice Assumptions Capacity

mcm

UKCS Norway LNG BBL IUK

18

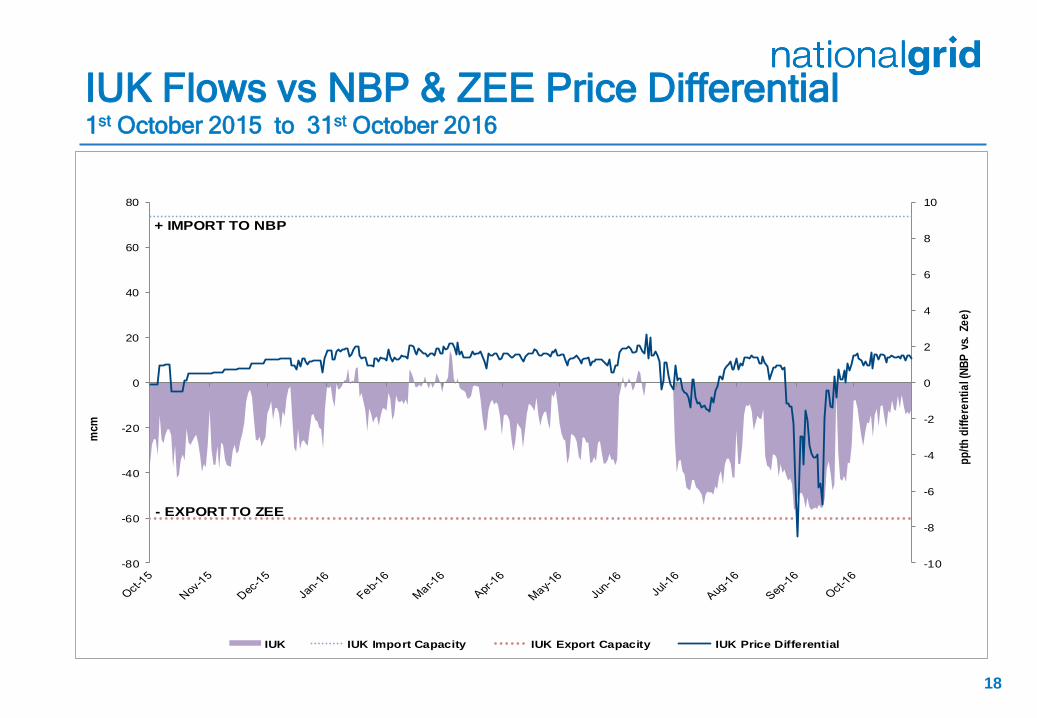

1st October 2015 to 31st October 2016

IUK Flows vs NBP & ZEE Price Differential

-10

-8

-6

-4

-2

0

2

4

6

8

10

-80

-60

-40

-20

0

20

40

60

80

pp

/th

dif

fere

nti

al (

NB

P v

s. Z

ee

)

mcm

IUK IUK Import Capacity IUK Export Capacity IUK Price Differential

+ IMPORT TO NBP

- EXPORT TO ZEE

19

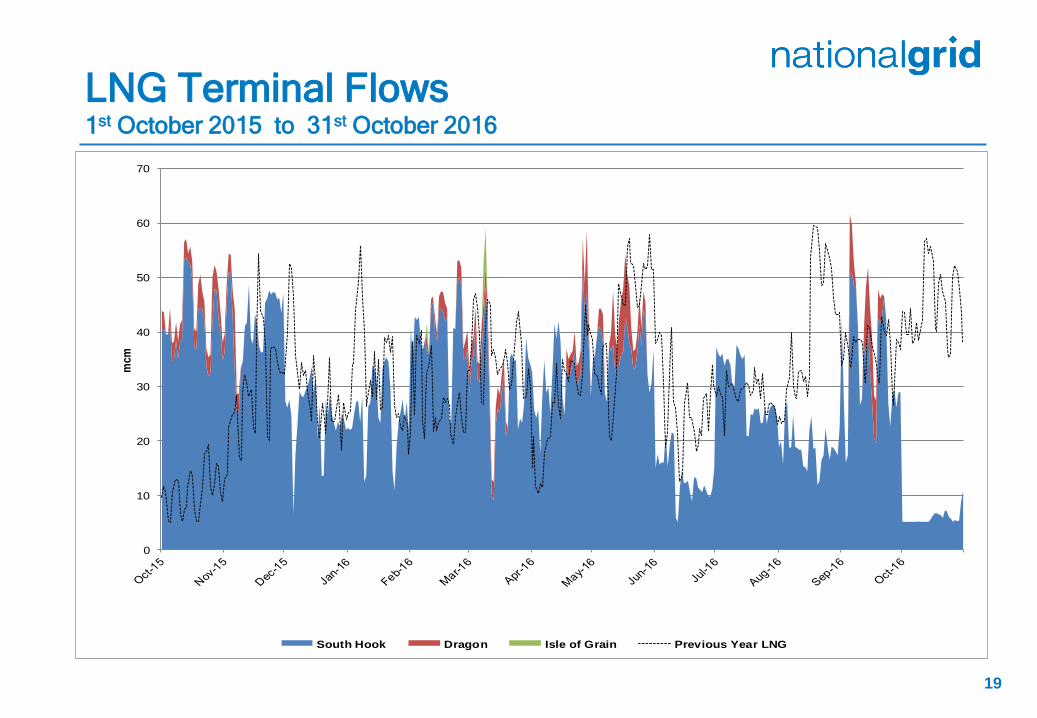

1st October 2015 to 31st October 2016

LNG Terminal Flows

0

10

20

30

40

50

60

70

mcm

South Hook Dragon Isle of Grain Previous Year LNG

20

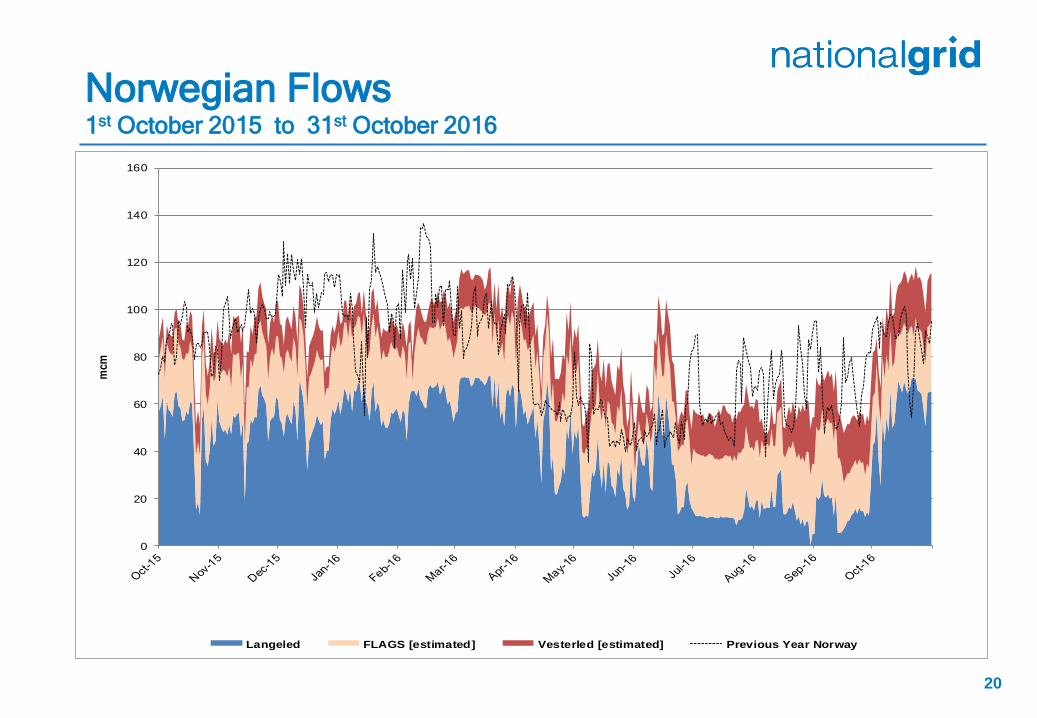

1st October 2015 to 31st October 2016

Norwegian Flows

0

20

40

60

80

100

120

140

160

mcm

Langeled FLAGS [estimated] Vesterled [estimated] Previous Year Norway

21

1st October 2015 to 31st October 2016

Storage Withdrawal vs Injection

-80

-60

-40

-20

0

20

40

60

80

100

120

mcm

Withdrawal Injection

22

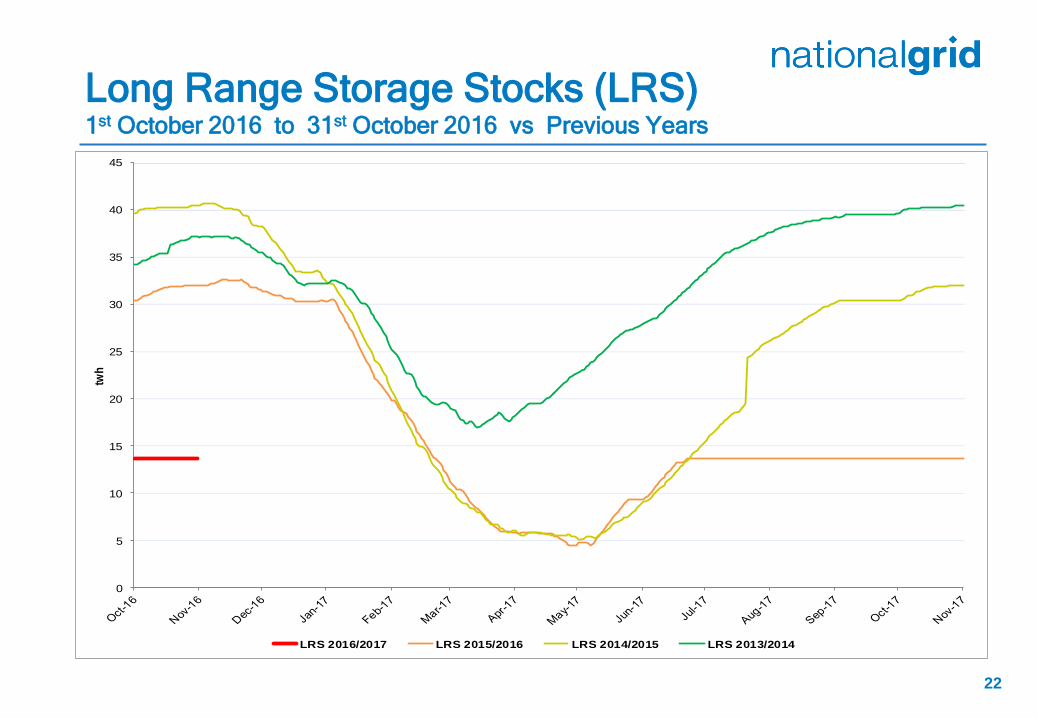

1st October 2016 to 31st October 2016 vs Previous Years

Long Range Storage Stocks (LRS)

0

5

10

15

20

25

30

35

40

45

twh

LRS 2016/2017 LRS 2015/2016 LRS 2014/2015 LRS 2013/2014

23

1st October 2016 to 31st October 2016 vs Previous Years

Medium Range Storage Stocks (MRS)

0

2

4

6

8

10

12

14

16

twh

MRS 2016/2017 MRS 2015/2016 MRS 2014/2015 MRS 2013/2014

24

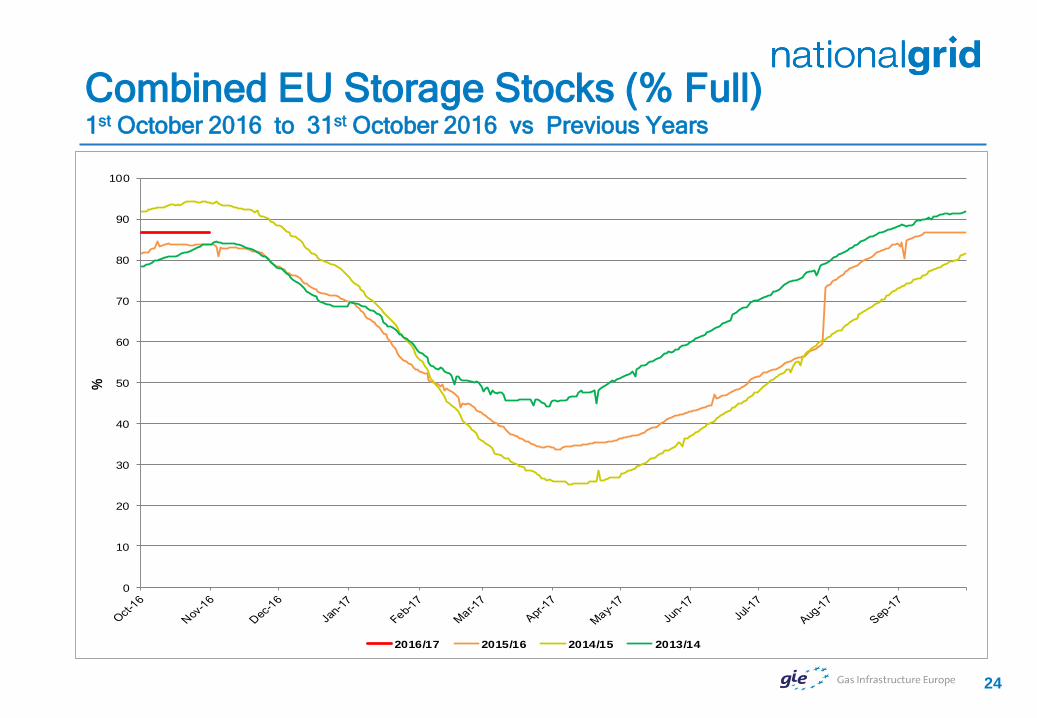

1st October 2016 to 31st October 2016 vs Previous Years

Combined EU Storage Stocks (% Full)

0

10

20

30

40

50

60

70

80

90

100

%

2016/17 2015/16 2014/15 2013/14

25

1st October 2015 to 1st October 2016 vs Previous Year UK Gas Prices

10

20

30

40

50

60

70

p/t

he

rm

SAP SMPB SMPS Previous Year SAP

26

What Operational Issues Affected Users?

Place your chosen image

here. The four corners

must just cover the

arrow tips. For covers,

the three pictures should

be the same size and in a

straight line.

Transporter Actions and Neutrality

Energy Balancing

Capacity

28

28

October 2015 to October 2016 vs Previous Year

Transporter Energy Traded on the OCM NGG Monthly Buys and Sells

-700

-600

-500

-400

-300

-200

-100

0

100

200

300

400

500

600

700

-700

-600

-500

-400

-300

-200

-100

0

100

200

300

400

500

600

700

Gw

h

Buy 2015/16 Buy Prev Year Sell 2015/16 Sell Prev Year

29

October 2015 to October 2016

Days of Default SMP Prices (SMPB)

0

10

20

30

40

50

60

70

80

90

100

%

SMPB [NG Set Price] SMPB [Default Marginal]

30

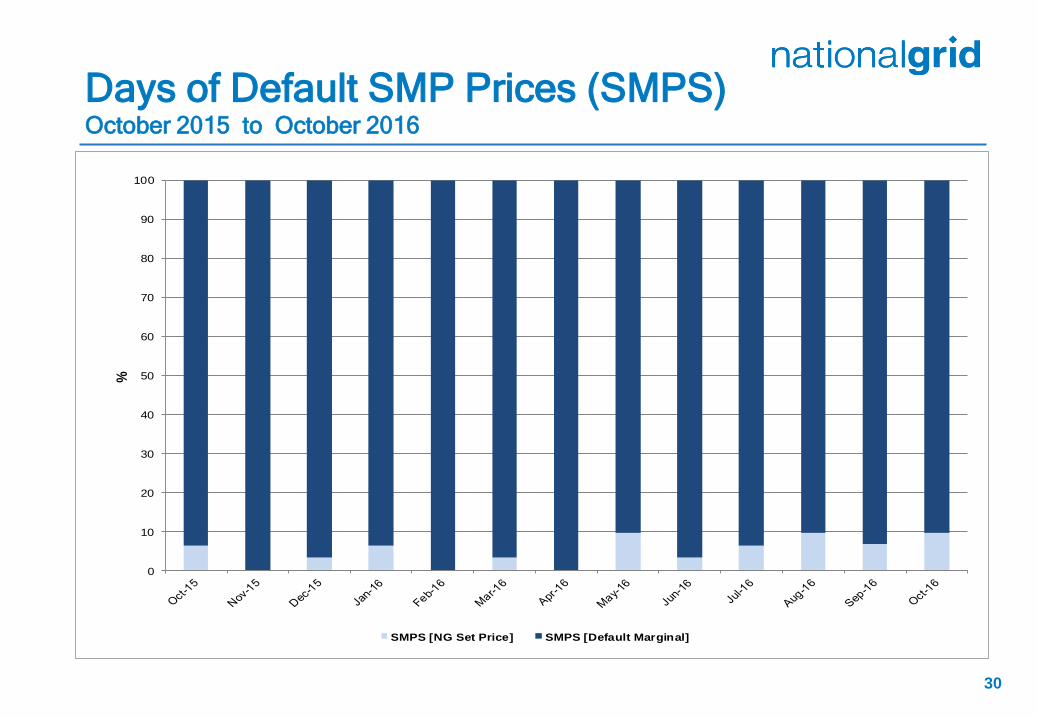

October 2015 to October 2016

Days of Default SMP Prices (SMPS)

0

10

20

30

40

50

60

70

80

90

100

%

SMPS [NG Set Price] SMPS [Default Marginal]

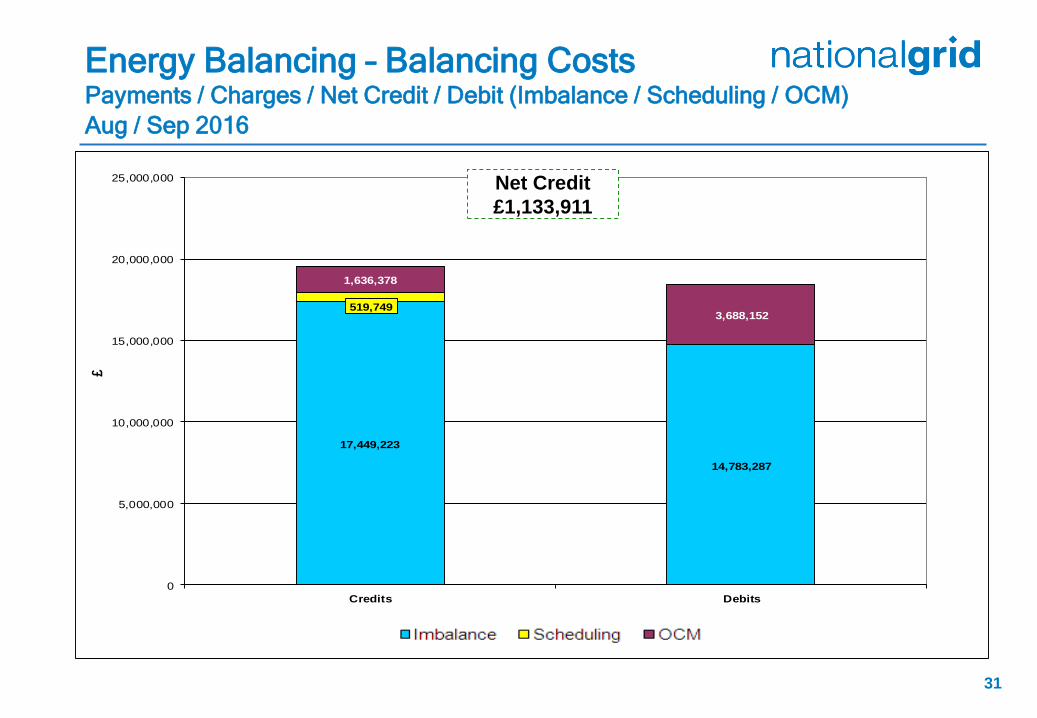

17,449,223

519,749

1,636,378

14,783,287

3,688,152

0

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

Credits Debits

£

31

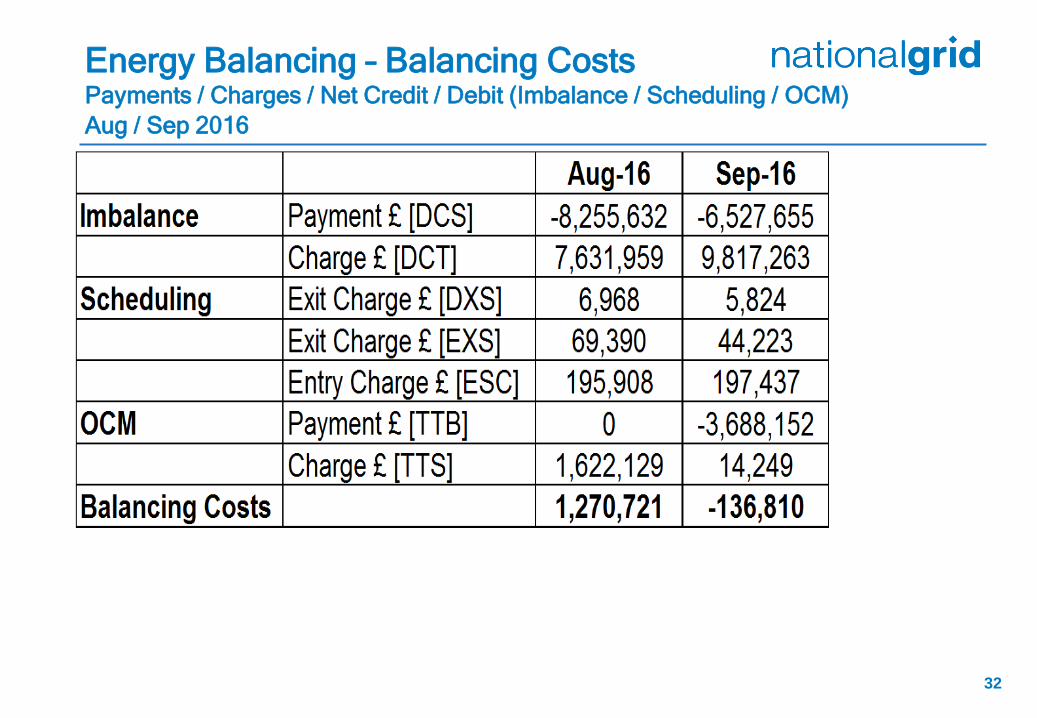

Aug / Sep 2016

Energy Balancing – Balancing Costs Payments / Charges / Net Credit / Debit (Imbalance / Scheduling / OCM)

Net Credit

£1,133,911

32

Aug / Sep 2016

Energy Balancing – Balancing Costs Payments / Charges / Net Credit / Debit (Imbalance / Scheduling / OCM)

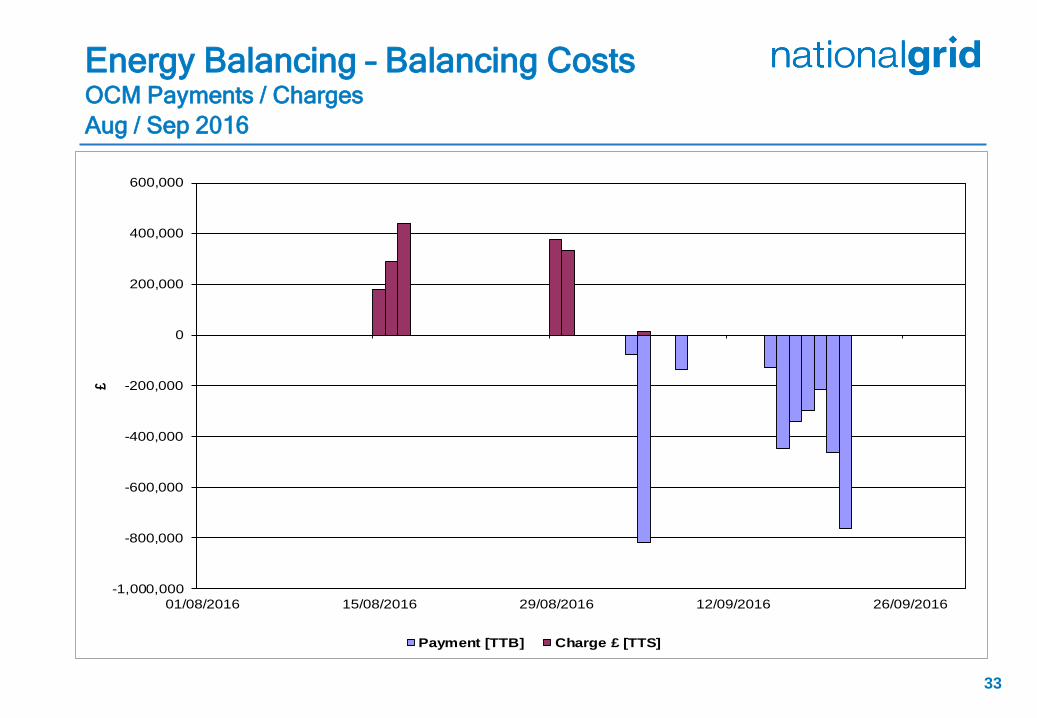

33

Aug / Sep 2016

Energy Balancing – Balancing Costs OCM Payments / Charges

-1,000,000

-800,000

-600,000

-400,000

-200,000

0

200,000

400,000

600,000

01/08/2016 15/08/2016 29/08/2016 12/09/2016 26/09/2016

£

Payment [TTB] Charge £ [TTS]

34

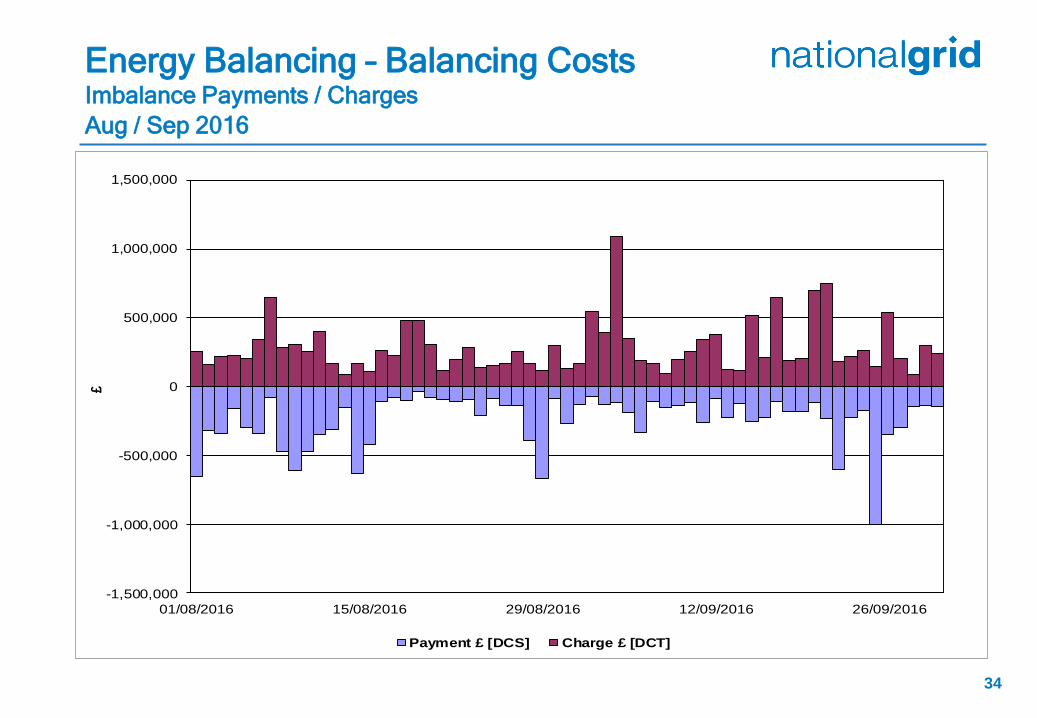

Aug / Sep 2016

Energy Balancing – Balancing Costs Imbalance Payments / Charges

-1,500,000

-1,000,000

-500,000

0

500,000

1,000,000

1,500,000

01/08/2016 15/08/2016 29/08/2016 12/09/2016 26/09/2016

£

Payment £ [DCS] Charge £ [DCT]

35

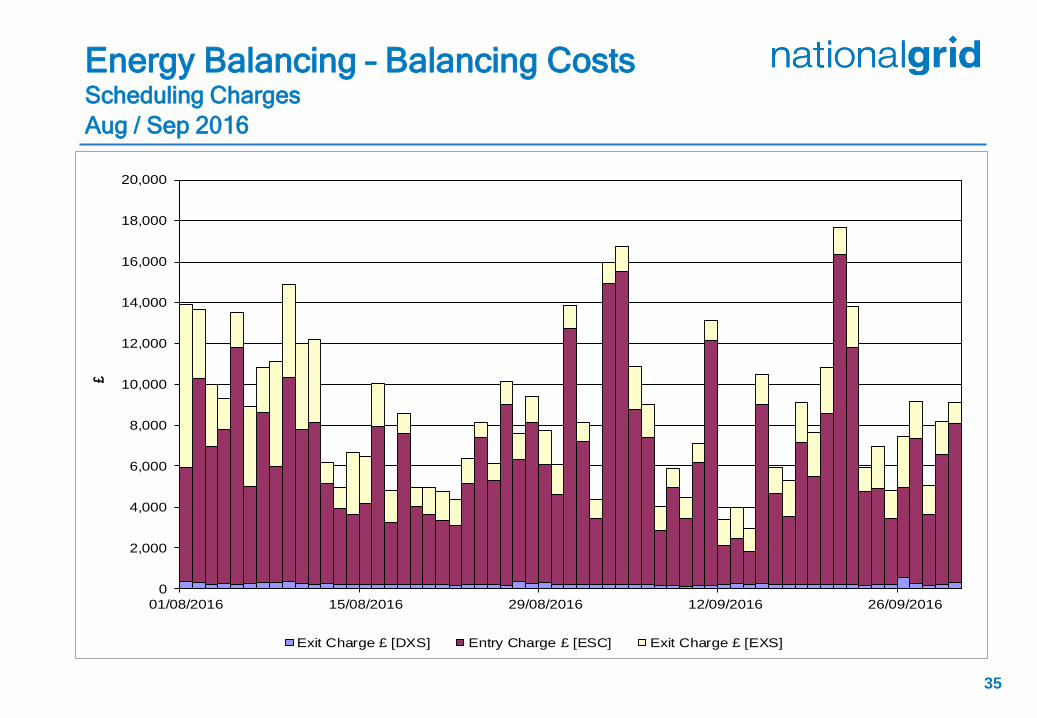

Aug / Sep 2016

Energy Balancing – Balancing Costs Scheduling Charges

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

01/08/2016 15/08/2016 29/08/2016 12/09/2016 26/09/2016

£

DayExit Charge £ [DXS] Entry Charge £ [ESC] Exit Charge £ [EXS]

36

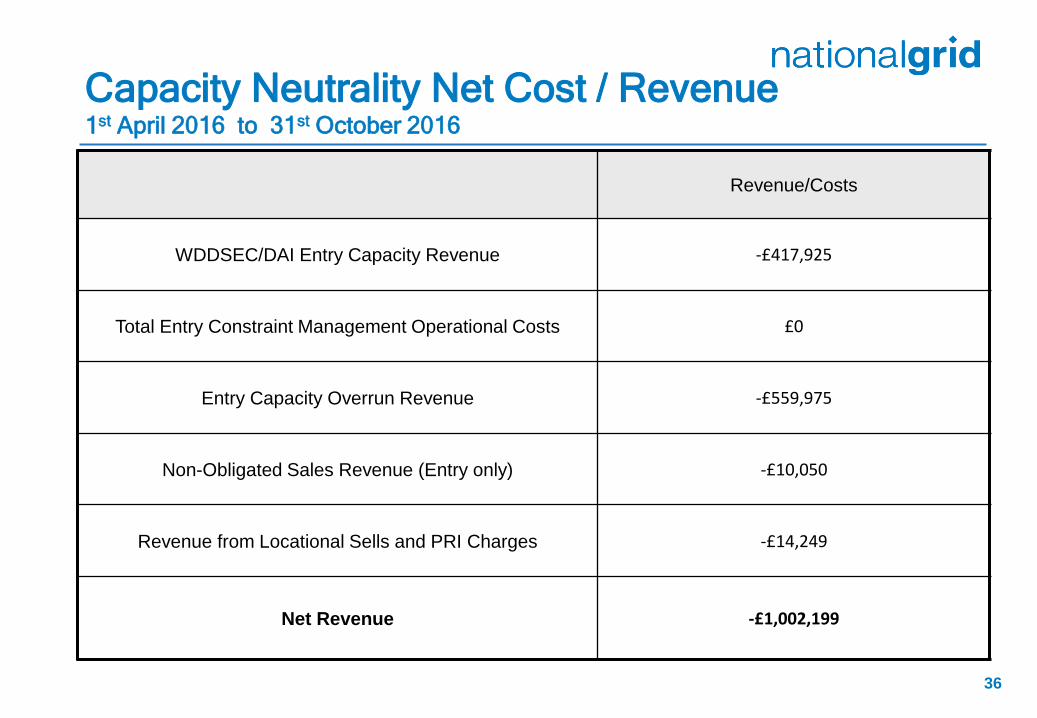

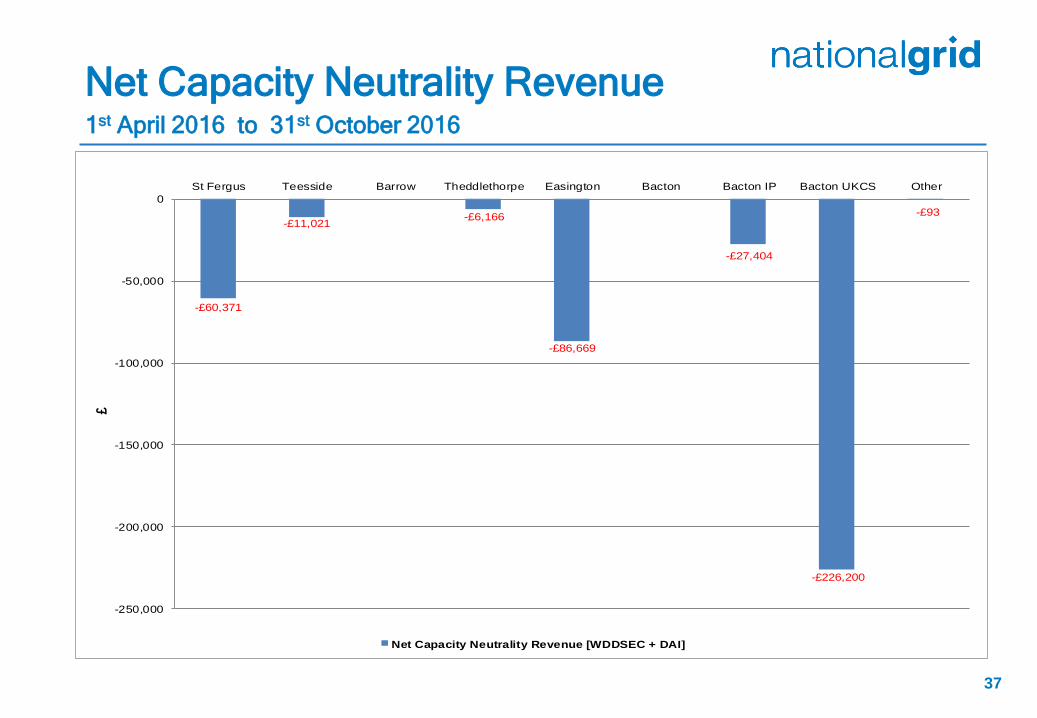

1st April 2016 to 31st October 2016

Capacity Neutrality Net Cost / Revenue

Revenue/Costs

WDDSEC/DAI Entry Capacity Revenue -£417,925

Total Entry Constraint Management Operational Costs £0

Entry Capacity Overrun Revenue -£559,975

Non-Obligated Sales Revenue (Entry only) -£10,050

Revenue from Locational Sells and PRI Charges -£14,249

Net Revenue -£1,002,199

37

1st April 2016 to 31st October 2016

Net Capacity Neutrality Revenue

-£60,371

-£11,021-£6,166

-£86,669

-£27,404

-£226,200

-£93

-250,000

-200,000

-150,000

-100,000

-50,000

0

St Fergus Teesside Barrow Theddlethorpe Easington Bacton Bacton IP Bacton UKCS Other

£

Net Capacity Neutrality Revenue [WDDSEC + DAI]

38

1st April 2016 to 31st October 2016

Month Locational Sells and PRI

charges revenue

Apr-16 £0

May-16 £0

Jun-16 £0

Jul-16 £0

Aug-16 £0

Sep-16 -£14,249

Oct-16 £0

Nov-16

Dec-16

Jan-17

Feb-17

Mar-17

Total £0 (FY16/17)

Month Entry Cap Overrun

Revenue

Non-obligated sales

revenue (entry)

Apr-16 -£110,246 -£148

May-16 -£79,691 -£21

Jun-16 -£193,290 -£188

Jul-16 £-59,400 -£1,740

Aug-16 -£78,428 -£32

Sep-16 -£38,921 -£495

Oct-16 £0 -£7,426

Nov-16

Dec-16

Jan-17

Feb-17

Mar-17

Total -£559,975 (FY16-17) -£10,050 (FY16-17)

Capacity Neutrality