operational guidelines for nbfcs

TRANSCRIPT

8/6/2019 Operational Guidelines for NBFCs

http://slidepdf.com/reader/full/operational-guidelines-for-nbfcs 1/34

OPERATIONAL GUIDELINES FOR INVESTMENT CREDIT REFINANCE TO NBFCs

1. IntroductionNBFCs have been approved to be included in the class of eligible institutions forrefinance under section 25 of NABARD Act, 1981.

2. Eligibility criteria for drawal of refinance

2.1 The NBFCs can draw refinance from NABARD subject to compliance of thefollowing criteria:a. The NBFC should have a certificate of registration under section 45-IA of theRBI Act, 1934 to function as an approved non banking financial institution.b. Both deposit taking NBFC (NBFC-D) and non-deposit taking NBFC (NBFC-ND)are eligible to be considered for refinance from NABARD.c. The NBFC should have been carrying on lending business at least for last 5years.d. The NBFC should maintain capital adequacy ratio as stipulated by RBI fromtime to time ( at 10%/12%/15%, depending on the type of NBFCs).e. The NBFC should have recorded net profit during 3 consecutive financial yearspreceding the previous year and should not have accumulated losses.f. The NBFCs with net NPAs not exceeding 5% as at the end of the previousaccounting year shall only be eligible for refinance.g. The NBFC should have the highest rating for long term borrowing viz. 'AAA' ofCRISIL or equivalent rating from any other SEBI approved rating agency.h. The Memorandum of Association of the NBFC should have a provision forborrowing from higher financing agencies.

2.2 NBFCs borrowing from NABARD are required to execute a General Refinance

Agreement with NABARD, furnish a resolution approved by the Board of Directors ofthe company and a letter of authority addressed to their bank. The formats areenclosed as Annexure – I, II & III .

2.3 The NBFCs shall submit to the concerned Regional Office of NABARD, thenecessary financial information to determine the eligibility of the NBFCs for availingrefinance assistance. ROs may also obtain the audited balance sheet / annual reportof the NBFCs and after the complete analysis of the NBFC concerned, fix the eligiblequantum of refinance for the year.

3. Eligible Purposes

3.1 Refinance to NBFCs will be available for Agriculture and Small and Micro

Enterprise Sector (SME Sector). Agriculture which includes horticulture, animalhusbandry, forestry, dairy and poultry, pisciculture and other allied activities will besupported by way of refinance irrespective of location of the project. Agro-processing/ Agro- Industries irrespective of their location and also the amount of investment inplant and machinery are eligible for refinance from NABARD.

3.2 In case of Small and Micro Enterprise Sector, NABARD will provide refinancefor such activities in rural areas / other areas which can be treated as rural areas asdefined in the NABARD Act, 1981 (i.e.. any area with population up to 50,000 is, atpresent, considered as rural area). Small and Micro Enterprises are defined as under:

(a) Small (manufacturing) Enterprises

1

8/6/2019 Operational Guidelines for NBFCs

http://slidepdf.com/reader/full/operational-guidelines-for-nbfcs 2/34

Enterprises engaged in the manufacture/production, processing or preservation ofgoods and whose investment in plant and machinery [original cost excluding land andbuilding and the items specified by the Ministry of Small Scale Industries vide itsnotification no. S.O. 1722 (E) dated October 5, 2006] does not exceed Rs. 5 crore.

(b) Micro (manufacturing) Enterprises

Enterprises engaged in the manufacture/production, processing or preservation ofgoods and whose investment in plant and machinery [original cost excluding land andbuilding and such items as specified by the Ministry of Small Scale Industries vide itsnotification no. S.O. 1722 (E) dated October 5, 2006] does not exceed Rs.25 lakh.

(c) Small (service) Enterprises

Enterprises engaged in providing/rendering of services and whose investment inequipment (original cost excluding land and building and furniture, fittings and otheritems not directly related to the service rendered or as may be notified under the

MSMED Act, 2006) does not exceed Rs.2 crore.(d) Micro (service) Enterprises

Enterprises engaged in providing/rendering of services and whose investment inequipment (original cost excluding land and building and furniture, fittings and suchitems not directly related to the service rendered or as may be notified under theMSMED Act, 2006) does not exceed Rs.10 lakh.

(e) The small and micro (service) enterprises shall include small road & watertransport operators, small business, professional & self-employed persons, and allother service enterprises.

(f) Khadi and Village Industries Sector (KVI) All advances granted to units in the KVIsector, irrespective of their size of operations, location and amount of originalinvestment in plant and machinery will be included in small enterprises.

4 . Nature of AccommodationNABARD will provide refinance assistance to the NBFCs under two windows namely,i) Automatic Refinance Facility and ii) Pre-Sanction Procedure.

4.1 Automatic Refinance Facility (ARF)

4.1.1 Automatic Refinance Facility is intended to enable the NBFCs to obtainrefinance from NABARD, without going through the detailed procedure of pre-sanctionformalities. The NBFCs are expected to appraise the proposals at their own level, besatisfied about the technical feasibility, financial viability etc. and finance theborrowers. The NBFCs will furnish the disbursement particulars in the prescribedformat (Drawal Application ), for claiming refinance from NABARD.

4.1.2 Farm Sector

2

8/6/2019 Operational Guidelines for NBFCs

http://slidepdf.com/reader/full/operational-guidelines-for-nbfcs 3/34

Any unit in the farm sector with total financial outlay upto Rs. 50 lakh will be eligiblefor refinance under ARF. Any other project will be covered under the pre-sanctionprocedure.

4.1.3 Small and Micro Enterprise (SME) SectorAny unit in SME Sector with financial outlay not exceeding Rs. 50 lakh will be eligiblefor refinance under ARF.

4.1.4 The NABARD will not refinance the loan unless the refinance is approved by itbefore expiry of 12 months from the date on which the loan was granted by theconcerned financing institution. The period of 12 months would be reckoned as fromthe date of disbursement of loan or in the case of loan disbursed in instalments fromthe date of disbursement of the instalment in respect of which refinance is required.

4.2 Pre-sanction Procedure - Sanction of Projects4.2.1 The refinance assistance to NBFCs above the ARF cut off level will be providedunder Pre-Sanction procedure. NBFC is required to forward the project proposal for

sanction to the concerned Regional Office after appraising the project and beingsatisfied about it’s technical feasibility, financial viability and bankability.

4.2.2 Time LimitThe NABARD will not refinance the loan unless it (the project) is approved by it beforeexpiry of 12 months from the date on which the loan was granted by the concernedfinancing institution. The period of 12 months would be reckoned as from the date ofdisbursement of loan or in the case of loan disbursed in instalments from the date ofdisbursement of the instalment in respect of which refinance is required.

4.2.3 Memorandum for Sanction

The project on submission will be independently appraised by NABARD from theangle of technical feasibility and determination of its financial viability for which amemorandum for sanction is to be prepared by the appraisal team for obtainingsanction of the scheme by the competent authority.

4.2.4 Withdrawal of SchemeIf the clarifications / additional particulars are not received from the NBFC within sixweeks, the scheme may be treated as withdrawn after giving due notice to thecompany.

5. Area Development Projects (ADPs)

Considering the large number of small and marginal farmers and people below thepoverty line in the country and as also the extensiveness of agriculture and ruraldevelopment, there could be need for promoting single purpose small projects on acluster basis. These cluster based single purpose small projects .i.e. AreaDevelopment Projects (ADPs) could be sanctioned to a single NBFC or to a number ofbanks and NBFCs. Example:- financing of Dairy units, financing of dug wells/ pumpsets/ bore wells/ shallow tube wells etc., financing of sericulture, other horticulturecrops, farm forestry projects etc. under a banking plan. ADP facilitates planning andprovision of infrastructure facilities viz., backward and forward linkages for fullrealisation of the benefits of the projects. The infrastructure projects could also beplanned and executed with credit support. For example, in the areas identified for

development of dairy, there would be scope to promote units related to processing,cold storage and marketing units in the area. If the needs of inter-related activities are

3

8/6/2019 Operational Guidelines for NBFCs

http://slidepdf.com/reader/full/operational-guidelines-for-nbfcs 4/34

addressed in a focussed manner, the overall results will be self sustaining. Thus,ADPs could focus on existing infrastructure, state of present development of theactivity, scope for increasing the activity, number of units to be set up, Governmentsupport available, status of ancillary activities, services required to support the mainactivity, credit support needed to expand and strengthen the activity, etc. An ADP

could also be considered for utilising the existing infrastructure developed under RIDFor any other programme. For example, if a dairy cooperative has extra capacity forprocessing milk with necessary milk routes and the villages have scope for rearingcattle, dairy activity could be undertaken along with calf rearing, fodder cultivation,animal feed units, etc. ADPs may be prepared in consultation with the linedepartments of the State Govt. and the NBFCs / bankers in the area. Targets could bedecided and achievements monitored at periodical intervals.

6. Rephasement of SchemeThe Schemes will have a definite time frame and project outlay. There could be aneed for revising any one/both of the project parameters. This revision is called

Rephasing. The NBFCs could approach NABARD for rephasing as and when suchneed arises and keeping in view the merits of the case, technical feasibility, financialviability etc. NABARD may permit such rephasing.

7 . Quantum of RefinanceThe refinance assistance will be extended to NBFCs at 50% of the loans disbursed.

8. Rate of interest on refinanceRate of interest on refinance will be reviewed from time to time taking into accountthe cost of funds, market conditions etc. The present rate of interest on refinance toNBFCs is 10.25% per annum. In case of default in repayment of refinance on duedate, NABARD will levy additional interest on the default amount for the period duringwhich default persists.

9 . Unit costUnit costs are to be decided by the financing institutions.

10. SecurityThe need for submitting Government Guarantee or any other security has been waivedby the Board of Directors for NBFCs.Under Sec. 29 of NABARD Act, 1981, all sums received by a borrowing institution inrepayment or realisation of loans and advances refinanced either wholly or partly byNABARD shall be deemed to have been received in trust for National Bank and shallbe repaid to NABARD on due dates to the extent of outstanding borrowings fromNABARD. Similarly, under Sec. 29 (2), all securities held or which may be held bythe borrowing institution, shall be held by such institution, in trust for NABARD.

11 . Repayment period11.1 The repayment period at ultimate borrower level is fixed on the basis ofeconomic life of the asset and the surplus generated out of the investment.

Accordingly, and also as a matter of practice, the maximum period for repayment atultimate borrower level is fixed not exceeding 15 years.

4

8/6/2019 Operational Guidelines for NBFCs

http://slidepdf.com/reader/full/operational-guidelines-for-nbfcs 5/34

The refinance is expected to be repaid on the due date prescribed by NABARD. As ageneral policy, the repayment period fixed in respect of NABARD refinance, does notexceed the repayment period fixed by the bank to it’s ultimate borrower. As a matterof general principle, all recoveries due from the ultimate borrowers are required to berepaid to NABARD and the own share of NBFCs is to be recovered by the NBFCs only

after NABARD refinance has been fully repaid. NBFCs are required to repay the duesto NABARD on the due dates irrespective of the recovery from the ultimate borrower . All repaymentsreceived by NBFCsagainst loansrefinanced

Repayment of Refinance

i. From 1 January to 30June of each year

31st July each year

ii. From 1 July to 31December of each year

31st January of next year

(Note ) : If the repayment date falls on a Saturday / Sunday / Holiday, the payment

date will be the previous working day).

11.2 Notwithstanding the above, NBFC may opt for repayment period of 5 years forrepayment of refinance under ARF- FS, irrespective of the repayment period drawn forthe ultimate borrowers. In such cases, the repayment period of 5 years will bereckoned from the date of release of refinance .

11.3 It is to be ensured that the last date of repayment does not fall beyond theperiod stipulated for repayment of loan (which is reckoned from the date of firstdisbursement of refinance) except for marginal extension on account of fixed duedates. Therefore, before fixing the repayment schedule for refinance, the period of

repayment of loan, grace period, repayment schedule, etc., at the ultimate borrowerlevel need be carefully studied.

12. Commitment ChargesIn the event of the bank not availing of refinance as per the prescribed time scheduleindicated in the sanction letter, NABARD is entitled to require the NBFC to paycommitment charges on the shortfall of drawals at 1/3 of 1% per annum at the end ofeach year on a cumulative basis as indicated in the General Refinance Agreement.However, Management Committee has decided not to enforce this provision.

13. Evaluation FeeThe NBFC may charge the borrower a "once-and-for-all" evaluation fee of 1% of thecost of investment. However, this fee could be waived by the NBFCs at theirdiscretion, based on merits of each case.

14 . Rate of interest for ultimate borrowersThe rate of interest to ultimate borrowers will be decided by NBFCs. However, sameshould be reasonable and their margin is suggested to be kept within 3%.

15. Security to be obtained /Margin Requirements (from ultimate borrowers):For loan accounts covered by NABARD refinance NBFCs may develop their securitynorm/ margin requirement. However, it is suggested that they could consider tofollow the security norm/ margin requirement as per the guidelines issued by RBI for

Commercial Banks from time to time .

5

8/6/2019 Operational Guidelines for NBFCs

http://slidepdf.com/reader/full/operational-guidelines-for-nbfcs 6/34

16. Reschedulement - Relief Measures to borrowers affected bynatural calamities

(i) Borrowers affected by natural calamities may be given the facility of reschedulingof current demand by extending the period of loan. In other words, in areas affectedby natural calamities, the recovery of loan instalments representing only the current

demand due from the concerned borrower, may be allowed to be postponed by oneyear. Care should be taken to ensure that the repayment period for the loan, afterpostponement of current demand, does not exceed the economic life of the asset. Inno case an overdue instalment be postponed. Besides, the facility should beextended only to those borrowers who have actually suffered loss.

(ii) In cases where there is a total/partial loss of asset (such as death of milch animal,destruction of poultry sheds etc.), NBFCs may give fresh loans for rehabilitation /replacement of asset with refinance support from NABARD.

(iii) NBFCs are also advised NOT to charge compound interest or penal interest. They

should refund penal interest, if any, already charged.(iv) While granting postponement of loans and reschedulement of term loans, theNBFC should be guided by the State Govts. notification declaring the areas affectedby natural calamities.

17 . Refinance Operations17.1 Refinance under Presanction Procedure : Under pre-sanction procedure, before applying for refinance, NBFCs have to acceptthe terms and conditions of NABARD's sanction in a format (Annexure IV) and thensubmit the application for refinance in respect of the schemes sanctioned. For thefirst and subsequent drawals, NBFCs are required to submit drawal application as inAnnexure V & VI and for NFS in Annexure VII &VIII respectively .

17.2 Drawal Applications under Automatic Refinance Facility

The formats of drawal application in respect of ARF for various activities under ARF-FS / NFS and Self Help Groups are given in Annexure IX and X respectively.

17.3 Time limit for submission of drawal applications under Pre-SanctionProcedure and ARFNBFCs are free to prefer drawal applications at any time during the phasing of thescheme. Even after the phasing has come to an end, drawal applications can besubmitted within a period of six months, provided disbursements to the ultimateborrowers have been made before the closure of the scheme phasing. However,NBFCs are required to claim refinance as quickly as possible after the disbursementof the loans by them.The policy in this connection is as under:

"The NABARD will not refinance the loan unless it (the scheme) is approved by itbefore expiry of 12 months from the date on which the loan was granted by theconcerned financing institution. The period of 12 months would be reckoned as fromthe date of disbursement of loan or in the case of loan disbursed in instalments fromthe date of disbursement of the instalment in respect of which refinance is required".The above policy is applicable to ARF lending also .

6

8/6/2019 Operational Guidelines for NBFCs

http://slidepdf.com/reader/full/operational-guidelines-for-nbfcs 7/34

17.4 Minimum amount of RefinanceAs far as possible, each drawal application should be for a minimum amount of Rs.2lakh. This is only a suggestion and not a rule and exceptions could be made at thediscretion of the concerned Regional Office of NABARD.

17.5 Date and period of disbursementThe date of disbursement, particularly the date of first disbursement is absolutelyessential, as the period of loan, grace period and repayment schedule depend on it. Itshould also be ensured that the details of physical units financed are furnished alongwith the drawal application in the prescribed statement.

17.6 Disbursements and outstandingsThe amount which qualifies for refinance is the amount disbursed to the ultimateborrowers or the consolidated outstanding loan amount against such borrowers,whichever is lower. It is possible that in some cases, the outstandings may be lowerthan the loans disbursed on account of advance recoveries or repayments received

and therefore in such cases only the outstandings will be considered for refinance.Further, if any instalments have fallen due, as per the terms and conditions ofsanction, before release of refinance, such instalments whether recovered or not bythe NBFC from the borrowers, will be deducted from the amount disbursed or amountoutstanding as the case may be and eligible refinance will be worked out accordingly.In the case of loans involving subsidy either from State Govt/Govt. of India, the drawalapplication under ARF should inter alia indicate the amount disbursed, and thesubsidy and outstanding amount of subsidy. It will enable the RO to work out eligiblerefinance and release the amount.

18. Fixing of Repayment schedule

18.1 NBFCs should invariably furnish the repayment schedule both in respect of theamount of refinance applied for as well as that fixed for the ultimate beneficiary, inthe drawal applications both under pre-sanctioned schemes and ARF as it will enableRO of NABARD to fix repayment schedule realistically in respect of NABARD refinance.

18.2 When the repayment schedule given in the drawal application is incorrect or isnot in accordance with the terms and conditions of sanction in the case of pre-sanctioned schemes, the same may be changed and correct repayment schedule maybe advised to the NBFC.

18.3 The principle involved in fixing the repayment schedule is that all recoveriesmade from the ultimate borrowers should first be apportioned for repayment of

refinance. In other words, the repayment of refinance by NBFCs is based on the loaninstalments, which will be repaid by the ultimate borrowers, as per the terms andconditions of sanction. Therefore, the repayment of the instalment of refinance dueeach year/half-year will depend on the amount of recoveries to be made fromborrowers every year or during the half-year. The NBFCs may determine therepayment schedule on the basis of the amount of loan disbursed or outstanding.Again, if for any reason, refinance has to be restricted to an amount lower than thatapplied for, (i.e. if refinance claimed is more than the sanctioned amount or refinanceis restricted to the eligibility of NBFC) only those disbursements made by the NBFC inrespect of which NABARD proposes to release refinance should be taken into accountfor determining the repayment schedule. The NBFCs have to repay the instalments

as per repayment schedule, on the due date, whether or not they effect recoveriesfrom the borrowers.

7

8/6/2019 Operational Guidelines for NBFCs

http://slidepdf.com/reader/full/operational-guidelines-for-nbfcs 8/34

18.4 Notwithstanding the above, as NBFC may opt for repayment period of 5 yearsfor repayment of refinance under ARF- FS, irrespective of the repayment period drawnfor the ultimate borrowers, the repayment period of 5 years will be reckoned from thedate of release of refinance .

18.5 Repayments of refinance to NABARD are to be made on 31st January and 31stJuly every year and accordingly the repayment schedules should stipulate the samedue dates. All recoveries of loans made at the NBFC level (as per condition of sanctioni.e. either yearly or half-yearly or monthly basis) between 1st January and 30th Juneshould be appropriated towards the repayment of the instalment of refinance due on31st July of that year and all recoveries of loans effected between 1st July and 31stDecember should be appropriated towards repayment of the instalment of refinancedue on 31st January of the following year. Interest due is payable on 1 January and 1July every year. The repayment schedule should be determined in such a way that

each instalment of refinance, as far as possible, is in multiples of hundreds.

(Note ) : If the repayment date falls on a Saturday / Sunday / Holiday, the paymentdate will be the previous working day).

19 Procedure for Release of refinance

19.1 The actual disbursement of funds shall be effected by the Finance and Accountssection of the RO. For this purpose the NBFCs shall submit the refinance drawalapplications to the Regional Office of NABARD in the state where the financing has

been done.19.2 Refinance is to be released as per instructions given by the applicant NBFC. Itmay be credited to the current account of the NBFC or credited to the NBFC’saccount with the designated bank branch with suitable instructions to remit theamounts by a cheque or electronic transfer. Refinance is not to be normally disbursedby Demand Drafts. Where, however, the NBFC has specifically agreed to such a modeof remittance in writing, with a provision that National Bank can charge interest, fromthe date of disbursement of refinance, this mode can be acceded to and the Draftcharges in such cases may be borne by the concerned NBFC.

8

8/6/2019 Operational Guidelines for NBFCs

http://slidepdf.com/reader/full/operational-guidelines-for-nbfcs 9/34

ANNEXURE - 1

DOCUMENTS FOR INVESTMENT CREDIT REFINANCE TO NBFCs

GENERAL REFINANCE AGREEMENT

MEMORANDUM OF AGREEMENT made this day of 200

between a non banking financial company

incorporated / established under the Companies Act 1956 and having its registered /

Head Office at

(hereinafter referred to as "the Financing Institution") of the one part

and National Bank for Agriculture and Rural Development, a body corporate

established under the National Bank for Agriculture and Rural Development Act, 1981

and having its Head Office at Plot No.24, 'G' Block, Bandra Kurla Complex, Bandra,Mumbai 400 051 and a Regional Office at

(hereinafter referred to as "the NABARD") of the other part.

WHEREAS

The Financing Institution is desirous of granting loans and advances to its

constituents for the purpose of promoting agriculture and rural development in India

under schemes approved / to be approved by the NABARD and is desirous of applying

to the NABARD for loans and advances either by way of refinance or otherwise on

such terms and conditions as may be agreed to between the Financing Institution and

the NABARD.

AND WHEREAS

The Financing Institution has requested the NABARD to sanction loans and advances

by way of refinance or otherwise on the terms and conditions to be mutually agreed

upon.

AND WHEREAS

The NABARD has agreed to grant loans and advances to the Financing Institution, by

way of refinance or otherwise on the terms and conditions hereinafter appearing.

NOW IT IS HEREBY AGREED by and between the parties hereto as follows :

1. The Financing Institution will submit from time to time to the NABARD for its

approval, schemes for grant of financial assistance by the Financing Institution to

its constituents (borrowers of the financing institution) for promoting agriculture and

rural development in India.

2. "The NABARD may, in it absolute discretion but without any obligation on its part

so to do, sanction loans and advances to the Financing Institution by way of

9

8/6/2019 Operational Guidelines for NBFCs

http://slidepdf.com/reader/full/operational-guidelines-for-nbfcs 10/34

refinance or otherwise in respect of such loans and advances granted / to be

granted by the Financing Institution to its constituents under any of the said

schemes, to such extent and on such terms and conditions as the NABARD may

decide".

i. The loans and advances by way of refinance in respect of any scheme approved

by the NABARD shall be disbursed by it in accordance with a schedule of

disbursement to be stipulated by the NABARD in its letter of sanction in respect

of such scheme (hereinafter referred to as "the said letter of sanction") and shall

bear interest at such rate as may be stipulated by the NABARD in the said letter

of sanction. The refinance along with interest shall be repaid by the Financing

Institution in accordance with the schedule of repayment stipulated by the

NABARD in the said Letter of Sanction. The said schedule of disbursement andof repayment may be varied by mutual agreement.

ii. If the Financing Institution delays or defaults in the payment of interest or

repayment of principal, such defaults shall attract additional interest at rates

that may be prescribed by NABARD from time to time.

iii. In case of the Financing Institution repaying to the NABARD, the whole or any

part of the loan or other dues earlier than the due date i.e., the date on which

sums or part thereof falls due for repayment as per the repayment schedule,

the NABARD may at its discretion accept the same subject to the terms and

conditions prescribed by it from time to time.

3. In the event of the Financing Institution not drawing, within the period stipulated

in the said Letter of Sanction for drawal by way of refinance, the whole or any part

of the loans and advances by way of refinance sanctioned by the NABARD, the

NABARD shall be entitled to require the Financing Institution to pay to the

NABARD at the end of the period so stipulated, commitment charges at 1/3 of 1%

per annum or at such rates that may be prescribed from time to time, for the said

period, on the amount in short fall of withdrawal.

4. The terms / facts mentioned in the applications for loans and advances made by

the Financing Institution in respect of each scheme shall constitute the basis of

the sanction.

and grant of relative loan and advance in respect of such application.

5. The security for the loans and advances by way of refinance or otherwise shall be

such as may be specified by the NABARD in the respective Letter of Sanction. Theproperty of the constituent offered as security for the refinance should, unless

10

8/6/2019 Operational Guidelines for NBFCs

http://slidepdf.com/reader/full/operational-guidelines-for-nbfcs 11/34

otherwise agreed to by the NABARD, be got valued by the Financing Institution

either at its or its constituent's cost by a competent person and a valuation report

furnished to the NABARD before the first installment of the relative refinance is

drawn.

6. The Financing Institution shall, whenever required by the NABARD to do so assign

to the NABARD at its own expense all other securities and security documents and

the benefit of any personal guarantee obtained by the Financing Institution which

the Financing Institution may hold in respect of the loans and advances and the

indebtedness of its constituents under the scheme.

7. The Financing Institution shall, from time to time, until repayment of the relative

loan and other dues is made in full and whenever required by the NABARD to do

so, furnish the NABARD with true reports in such form as the NABARD mayprescribe regarding the solvency of the constituents on each bill or promissory note

and agree to advise the NABARD promptly of any change in the position of any

such party which can reasonably be considered to affect the security furnished to

the Financing Institution and / or the NABARD.

8. The financing Institution shall maintain separate accounts in respect of the

financial assistance received from NABARD in respect of each scheme. The

Financing Institution further agrees that it shall not during the subsistence of the

credit facility availed from NABARD close the said account without the consent of

NABARD.

9. The Financing Institution, shall, notwithstanding any enquiry made by or

information furnished to the NABARD in respect of the credit of the Financing

Institution's constituents and notwithstanding creation of any security by its

constituents or any assignment made in favour of the NABARD in pursuance of

Clause 6 hereof, the security therefor made in favour of the NABARD, remain

always liable as a principal debtor to the NABARD for the due repayment of any

refinance granted by the NABARD.

10. The Financing Institution agrees that if and whenever it realises any of the

securities held by it either alone or jointly with the NABARD, as security for the

said loans and advances or whenever any repayment is received or recovery made

by the Financing Institution from the ultimate borrowers, the Financing Institution

will pay over to the NABARD all such realisations or recoveries to the extent

required to repay the Financing Institution's obligations hereunder and till so paidover to NABARD, the amounts shall be held by the Financing Institution in the

11

8/6/2019 Operational Guidelines for NBFCs

http://slidepdf.com/reader/full/operational-guidelines-for-nbfcs 12/34

manner specified by Section 29 of the National Bank for Agriculture and Rural

Development Act, 1981.

11. The Financing Institution agrees :

i. that it shall not allow on any account of the constituents, any operation

inconsistent with such advances, or which are likely to jeopardise such advances;

ii. unless otherwise required by the NABARD, to inspect periodically the affairs of

the constituents financed and to submit a report of such inspections to the NABARD

once a year, indicating the progress made in respect of the scheme and whether the

advance has been utilised by the constituents for the purpose for which it was

granted;

iii. to furnish to the NABARD all such information as the NABARD may require from

time to time regarding constituents or about the Financing Institution itself.12. The Financing Institution shall ensure that the loan agreement obtained by the

Financing Institution from each of its constituents is in consonance with the

provisions of this Agreement and the said letter of sanction. In particular, such

loan agreement shall, inter alia, provide for the following matters :

i. Financing Institution shall be at liberty to assign the debt and the benefit of the

securities therefor and the security documents to the NABARD as security for any

refinance obtained by the Financing Institution from NABARD in respect of the loan

agreed to be advanced by the Financing Institution to the borrower, and the borrower

shall, if and whenever required by the Financing Institution, do and execute all such

acts, things, deeds, documents or assurances as the Financing Institution may deem

necessary for giving effect to such assignment;

ii. the Borrower shall not, without the written consent of the Financing Institution

and the NABARD, create in any manner any mortgage, charge, lien or other

encumbrance on the security given to the Financing Institution and / or the NABARD

in respect of such advances or create any interest in such security in favour of any

other party or person;

iii. the Borrower shall allow duly authorised representative(s) of the Financing

Institution and / or of the NABARD to inspect at any time the Borrower's premises

and plant and the Borrower's books of accounts and all other relevant records; and

iv. the Financing Institution shall be at liberty to furnish to the NABARD such

information or reports as the NABARD may require, regarding the Borrower/s.

13. The Financing Institution agrees that the rate of interest payable by theultimate borrowers under each scheme shall be open to review by the NABARD at

12

8/6/2019 Operational Guidelines for NBFCs

http://slidepdf.com/reader/full/operational-guidelines-for-nbfcs 13/34

any time. The Financing Institution shall ensure that suitable provision to this

effect is incorporated in the loan agreement obtained from the ultimate borrower.

14. The Financing Institution will undertake the responsibility of arranging for the

working capital requirements of its constituents under the relative schemes if they

are not in a position to provide for the same from their own resources.

15. The Financing Institution shall make proper arrangements for supervising the

utilisation of the loans granted to its constituents under the schemes approved by

the NABARD and shall not disburse any installment of a loan unless it is satisfied

that the previous installments have been properly utilised.

16. The NABARD shall be entitled to depute one or more of its officers to inspect at

any time the Financing Institution or the premises and the plants and the books of

accounts of the constituents to whom loans have been granted and also to inspectthe security for such loans.

17. In the event of breach by the Financing Institution of any of the terms and

conditions on which loans and advances are sanctioned by the NABARD, the

NABARD may recall the entire loan or any portion thereof along with interest and

other dues and enforce the security.

18. In the event of the Financing Institution making any default in repayment of any

sum due to the NABARD on the due date, the NABARD shall be entitled to recall at

once the relative loan and enforce the security.

19. The Financing Institution further agrees that in the event of its constituents

failing to repay the Financing Institution in accordance with the terms governing

such payment, the NABARD shall have the right (but shall not be obliged) without

being required to obtain the concurrence of the Financing Institution, to take

either on behalf of itself or also on behalf of the Financing Institution, all steps to

realise the security held by the Financing Institution, and in the event of its

realising the security on behalf of the Financing Institution, to apply the same in

repayment of the relative refinance made available by it to the Financing

Institution.

20. The Financing Institution hereby agrees to issue/execute a separate irrevocable

Letter of Authority authorizing its bank/s to debit its account on the advice of

NABARD with the amount specified by NABARD and pay the same to NABARD.

The Financing Institution further agrees that if it commits default in making any

payment or repayment of any sum due to the NABARD in accordance with theaforesaid Mandate / Letter of Authority, the NABARD shall be at liberty to advise

13

8/6/2019 Operational Guidelines for NBFCs

http://slidepdf.com/reader/full/operational-guidelines-for-nbfcs 14/34

the ............................................ bank or banks with which the Financing

Institution maintains an account or accounts to debit such account or accounts

which the NABARD may specify with the amount due by way of such payment or

repayment and pay the same to the NABARD.

21. The Financing Institution also agrees that any debit made by the

............................ bank or banks with which the Financing Institution maintains

an account or accounts in pursuance of an advice received from the NABARD,

shall as between the Financing Institution and the aforesaid bank or banks, be

binding on, and not liable to question by the Financing Institution.

22. (i) The General terms and conditions contained in this Agreement shall be in

addition to those to be stipulated by the NABARD in the respective letter of

sanction.(ii) The Financing Institution also agrees that it shall be bound by the instructions

issued or to be issued by NABARD under its relative circulars, including any

modifications thereto from time to time.

23. It is agreed by and between parties hereto that this agreement shall be

effective from and all the loans and advances by way of refinance or otherwise that

have been hereto obtained by the Financing Institution from the NABARD shall be

deemed to have been obtained pursuant to this agreement and this agreement

shall continue to be in force and bind the parties hereto in respect of all refinance

provided or that may be provided to the Financing Institution from time to time

and shall come to an end only on written notice to that effect served by the

NABARD or the Financing Institution.

Provided, however, that such notice shall not in any way affect the rights and

obligations of parties hereto in respect of any refinance outstanding as on the date of

such notice and the rights and obligations of parties hereto in respect of such

outstanding sums shall continue to be governed by the terms of this agreement as if

the agreement is not rescinded in respect of those sums.

Testimonium and Subscription Clauses :

In witness whereof the NABARD has set its hand hereunto at ..................... through its

Chief General Manager and duly authorised official, at ...................... and Financing

Institution has through.............. * and its duly authorised official set its hand

hereunto at ................... on the respective dates mentioned below :Subscription Clause :

14

8/6/2019 Operational Guidelines for NBFCs

http://slidepdf.com/reader/full/operational-guidelines-for-nbfcs 15/34

Signed and delivered by the said NABARDby its Chief General Manager and dulyauthorised official, this the .................. dayof ...............

} }}}}

Signature

} 1) Signed and delivered by the said financinginstitution by .....................* and dulyauthorised official, this the .......................day of .................

}}}}}

2)

Witness From NABARD : Name

SignatureWitness

From Borrowing Institution NameSignature

* The testimonium and subscription clauses relating to signatory of Financing

Institution to be suitably inserted depending upon the provisions of Articles of

Association and it's Board Resolution.

15

8/6/2019 Operational Guidelines for NBFCs

http://slidepdf.com/reader/full/operational-guidelines-for-nbfcs 16/34

ANNEXURE - II

RESOLUTION TO BE PASSED BY THE BOARD OF THE FINANCING INSTITUTIONAUTHORISING THE BORROWINGS FROM THE NABARD AND ALSO DELEGATINGTHE POWER TO BORROW FROM THE NABARD UNDER THE MEMORANDUM OF

AGREEMENT

RESOLVED

1. That the Company do borrow with or without security from the National Bank

for Agriculture and Rural Development (hereinafter referred to as "the

NABARD") by way of refinance from time to time for the purpose of promoting

Agriculture and Rural Development under the schemes on the terms and

conditions set out in the draft Memorandum of Agreement forwarded by the

NABARD with its letter / circular No. ............................. a copy whereof duly

authenticated by has been circulated to the members of the

Board.

2. That the aforesaid borrowings by way of refinance from the NABARD, together

with interest, commitment charges, costs and other charges stipulated in and

/ in pursuance of the said Memorandum of Agreement be, if so required by the

NABARD, secured by an equitable sub-mortgage / sub-hypothecation in favour

of the NABARD, of the properties mortgaged / hypothecated to the Company

by the ultimate borrowers as security for its loans and advances to them for

the purposes mentioned herein above, or by joint equitable mortgage to be

created by the concerned borrowers, of their properties in favour of the

Company and the NABARD, and that in such an event an officer of the

Company be and is hereby authorised to deposit with the NABARD the title

deeds of the properties offered as security as above, to accept, in case of joint

equitable mortgage, the deposit of title deeds of the properties offered as

security as above, for and on behalf of the Company as also on behalf of the

NABARD when so authorised by the NABARD.

3. That the draft Memorandum of Agreement forwarded by the NABARD with its'

letter / circular No.................................. be and is hereby approved, and the

Managing Director of the bank be and is hereby authorised to accept on behalf

of the Company such changes in the draft Memorandum of Agreement as may

be agreed to by the NABARD; and

4. That the Managing Director be and is hereby authorised to execute theMemorandum of Agreement under his signature duly witnessed.

16

8/6/2019 Operational Guidelines for NBFCs

http://slidepdf.com/reader/full/operational-guidelines-for-nbfcs 17/34

5. That the Agreement executed in accordance with the resolution shall be in

force with effect from

6. That ........................ Officer be and is hereby authorised severally to borrow

with or without security from the NABARD by way of refinance for the aforesaid

purposes, from time to time, upon the terms and conditions set out in the said

draft Memorandum of Agreement with such modifications as might have been

agreed to on behalf of the Company, and if so required by the NABARD, create

equitable sub-mortgage or sub-hypothecation of properties mortgaged /

hypothecated to the Company by the concerned borrowers as security for such

refinance, or obtain joint equitable mortgage / hypothecation of the borrowers

properties in favour of the Company and the NABARD as security for the

refinance by the NABARD as also for the loans and advances made by theCompany and accept and convey acceptance on behalf of the Company to the

NABARD to the letters of sanction that may be issued by the NABARD from

time to time in connection with the said borrowings.

7. That the following officials of the Company namely (1) ................... and / or

(2) .................... (mention designation) be and are hereby authorised to

execute on behalf of the Company and in favour of the NABARD such other

deeds and documents instruments, declarations and other writings

whatsoever, as the NABARD may require, from time to time, in connection with

the aforesaid borrowings by way of refinance.

8. That the following officials of the Company namely (1) ..........................., (2)

..................... (mention designation) be and are hereby severally authorised to

accept deposit of title deeds made by the concerned borrowers by way of

equitable mortgage for the loans and advances granted by the Company and /

or to accept deposit of title deeds made by the concerned borrowers by way of

joint equitable mortgage in favour of the Company and the NABARD, for the

aforesaid loans and advances and the refinance.

17

8/6/2019 Operational Guidelines for NBFCs

http://slidepdf.com/reader/full/operational-guidelines-for-nbfcs 18/34

ANNEXURE - III

Letter of Authority to be executed by theNon Banking Financial Company to its Bankerfor Debiting their Current Account with the Banker

PLACE :

DATE :

The Manager

.............Bank

..............................

..............................

Dear Sir

Our Current Account No................ Standing instructions ......................

The National Bank for Agriculture and Rural Development (hereinafter referred to as

'NABARD') at our request has agreed to provide at its discretion refinance facilities to

us (................... NBFC) (hereinafter called as "the borrower") under various provisions

of the National Bank for Agriculture and Rural Development Act, 1981.

2 . The relevant clauses of the General Refinance Agreement executed by us in this

regard stipulates that NABARD will be authorised by us to require you to debit our

above current account/s with you in the event of any default on our part in the

repayment of the principal or payment of the interest and other charges, if any, in

respect of any loan or loans, by way of refinance or otherwise or any other sums

drawn by us under the credit limits or schemes sanctioned to us by the NABARD from

time to time, on the respective due dates, with such sums as may be in default by us,

and remit the same to the NABARD in such manner as they may require by debiting

to our said current account/s maintained with you.

3 . Accordingly we hereby authorise and request you that as and when a written

requisition is received by you from the NABARD and notwithstanding any dispute that

may exist or arise between us and NABARD, you may without reference to us debitour said Current Account with such sums as may be specified by NABARD in its

18

8/6/2019 Operational Guidelines for NBFCs

http://slidepdf.com/reader/full/operational-guidelines-for-nbfcs 19/34

written request and pay the same to the NABARD in such manner as they desire

under advice to us.

4 . We agree that the fact that NABARD has approached you in writing for debiting

our Current Account/s with you shall be a conclusive proof that a default has arisen in

respect of payment of the sums by us to NABARD and it shall not be necessary for us

to admit to the fact of default by means of a separate advice.

5 . This letter of authority shall also be enforceable against any current account/s

which may be opened with you by our successors or assigns.

6 . This letter of authority shall not be revoked by us except with the prior

concurrence of NABARD and you may act upon this authority until such time this

authority is so revoked and a written communication thereof is received by the

Manager, ................. Bank ................... (mention the centre). 7 . You are requested to ensure that the said account is not closed without prior

consent of NABARD.

8. Please acknowledge receipt of this letter and also return the duplicate copy

thereof duly confirmed by you to the ............... R.O. of NABARD.

Yours faithfully

for and on behalf of the .................. NBFC

Authorised Official

@ Delete whichever is not applicable.

Confirmation of the Reserve Bank of India on the duplicate copy of the letter of

authority.

Returned to the NABARD

The Reserve Bank of India hereby agrees to comply with the requisitions as may be

issued by the National Bank from time to time in terms of the above letter of

authority.

For Reserve Bank of India

Authorised official

Place

Date

Official seal

19

8/6/2019 Operational Guidelines for NBFCs

http://slidepdf.com/reader/full/operational-guidelines-for-nbfcs 20/34

ANNEXURE IV

(Under Pre Sanction Procedure)

ACCEPTANCE OF TERMS AND CONDITIONS

Name of the NBFC :Address of the forwarding office of the NBFC :

Ref . No. Date :

Dear Sir

Subject : Scheme .............................................................

Acceptance of terms and conditions

Please refer to your letter No.NB( )ICD/ .............................. dated

...................sanctioning to our Company a refinance assistance of Rs. .....................

lakhs under the captioned scheme. We are agreeable to the terms and conditions

stipulated in the above sanction letter.

Yours faithfully

For & on behalf of

............................................................. Company.

20

8/6/2019 Operational Guidelines for NBFCs

http://slidepdf.com/reader/full/operational-guidelines-for-nbfcs 21/34

ANNEXURE -V

(Under Pre Sanction Procedure)

(Application for first drawal)

Name of the NBFC :Address of the forwarding office of the NBFC :

Ref. No. Date:

Dear Sir

Subject : Scheme--------------------------------------------------------------

Please refer to your H.O/R.O.letter No. .............................. dated ..................sanctioning refinance of Rs. ..................... under the above mentioned scheme to ourCompany. We confirm having sanctioned a term loan of Rs. ................. to ourconstituent/s, (hereinafter referred to as “the borrowers”) under the abovementioned scheme of development approved by the National Bank for Agriculture andRural Development (NABARD) for which our Company intends to avail of the refinancesanctioned by the NABARD under your above mentioned letter. We note that theNABARD had waived security for its said refinance.

2. We advise that out of the aforesaid loan sanctioned by us, our Company hasadvanced a sum of Rs. ...................... to the borrower/s upto ........................ . Theamount outstanding from the borrower/s against our above disbursement as on thisday is Rs................... .

3. We confirm that we have obtained the agreement from the borrower/s for the totalloan sanctioned under the scheme in a form which is in consonance with the provisionof the Agreement dated ................................... and the sanction letter dated........................ .

4. Interest on the above amount already disbursed to the borrower/s is payable at...................... per annum.

5. The action taken by our Company on the conditions / suggestions as required bythe NABARD in its letter of sanction dated .................... under reference is indicatedin the annexure enclosed.

6. We now request you to disburse to us a sum of Rs. .................... by credit to ouraccount with the

21

8/6/2019 Operational Guidelines for NBFCs

http://slidepdf.com/reader/full/operational-guidelines-for-nbfcs 22/34

(mention place) against our advances already made to the borrowers under thescheme as mentioned under paragraph 1 earlier. The refinance to be drawn by ourcompany as above will be repaid to the NABARD on the dates indicated below :

Amount to be repaid on or before

31st January 31st July

Year (Rs.) (Rs.)

To enable you to release the refinance requested for as above, we are now furnishingthe following further information and documents required by you.

(i) Our company has already obtained adequate security both primary and collateralfrom the borrower/s for the loan sanctioned by us, for which the said refinance isclaimed.

(ii) We hereby declare and undertake that whatever security we have obtained or mayobtain from time to time from the borrower/s to secure the loan in question will beheld for and on behalf of the NABARD and any realisations or recoveries from theborrower/s under the said loans will be applied as required under Section 29 of theNational Bank for Agriculture and Rural Development Act, 1981.

Yours faithfully,

For and on behalf of ----------------------------------------------- Company.

22

8/6/2019 Operational Guidelines for NBFCs

http://slidepdf.com/reader/full/operational-guidelines-for-nbfcs 23/34

ANNEXURE VI

(Under Pre Sanction Procedure)

(Application form for second and Subsequent drawals)

Name of the NBFC :Address of the forwarding office of the NBFC :

Ref. No. Date :

Dear Sir

Subject : Scheme--------------------------------------------------------------------

In continuation to our letter No. ...................................................................dated .................. with regard to the above mentioned scheme, we advise that ourcompany has advanced a further sum of Rs. .................... upto / during....................... to our constituents (hereinafter referred to as the “said borrowers”)under the scheme for financing ............................................................. and therefinance sanctioned by the National Bank for Agriculture and Rural Development(NABARD ) under its letter No. .............................................................................................. dated ............................... . The amountof loan under the refinance sanctioned by NABARD outstanding against our saidborrowers as on date is Rs. .................................. which is exclusive of thedisbursement made upto / covered in our previous drawals mentioned above. Wealso confirm that the above disbursement of loan was made by us after satisfyingourselves that the previous instalments of loans advanced to the said borrowers andagainst which our company has drawn refinance from NABARD was properly utilisedby the said borrowers for the purposes and in the manner specified under thedevelopment scheme approved by the NABARD for granting of refinance to ourcompany.

2. Interest on the above amount already disbursed to the borrowers is payableat................................ % per annum.

3. We now request you to disburse a sum of Rs........................... by credit to ouraccount with ..................................................... (mention place) against theinstalment of loans already disbursed by our company to the borrowers under thescheme as mentioned under paragraph 1 earlier.The refinance to be drawn by our company as above will be repaid to the NABARD onthe dates indicated below :

Amount to be repaid on or before31st January 31st July

Year (Rs.) (Rs.)To enable you to release the refinance requested for as above, we are now furnishingthe following further information and documents required by you.

23

8/6/2019 Operational Guidelines for NBFCs

http://slidepdf.com/reader/full/operational-guidelines-for-nbfcs 24/34

(i) Our company has already obtained adequate security both primary and collateralfrom the borrower/s for the loan sanctioned by us, against which the said refinance isclaimed.

(ii) We hereby declare and undertake that whatever security we have obtained or mayobtain from time to time from the said borrowers to secure the loan in question willbe held for and on behalf of the NABARD and any realisations or recoveries from thesaid borrowers under the said loans will be applied as required under Section 29 ofthe National Bank for Agriculture and Rural Development Act, 1981.

(iii) We also confirm that we have obtained the agreement from the said borrowerscovered by this application for the drawal of refinance for the total loan sanctioned tothem in a form which is in consonance with the provision of the agreement dated................ and sanction letter No. ................................................................... dated....................... .

Yours faithfully

For and on behalf of _____________________________________ Company

24

8/6/2019 Operational Guidelines for NBFCs

http://slidepdf.com/reader/full/operational-guidelines-for-nbfcs 25/34

ANNEXURE TO DRAWAL APPLICATIONName of the Scheme (Rs. in tho

Name of

theBranchand

CodeNo.

Loan amount and physical units (Quantity*) covered by the

present drawal application

Refinance

applied for

Rate of

interestcharged

Prog

physica

Particulars of disbursement of loans Physicalunits

financed

Amt.disbursed

(Net ofsubsidy

andrecoveries,

if any)

No. unit

comple

Type ofunit

financed

Unit costadopted

Month & yearof

disbursementof loan

SF OF SF OF

(1) (2) (3) (4) (5) (6) (7) (8) (9) (10) (11

Note : 1. In case of plantation/horticulture the bank should indicate whether the finance is for plantation or maintenance.2. Separate repayment schedule for refinance proposed to be drawn from NABARD against finance provided to SF & OF may

given in the drawal application.Repayment schedules may be prepared for borrower to NBFC and NBFC to NABARD.------------------------------------------------------------------------------------------------------------------------------------------* Quantity : Depending on nature of schemes for which normally measures of quantity of physical items is mentioned in thesanction letter.

For instance - i) Actual number of wells, pumpsets, etc., and number of animals in the case of dairy development, sheep rearing,piggery and poultry etc.

ii) Area in the case of inland fisheries, plantation and horticulture, land development, etc.iii) Length in metres in case of lining of field channels, pipelines, etc.

1

8/6/2019 Operational Guidelines for NBFCs

http://slidepdf.com/reader/full/operational-guidelines-for-nbfcs 26/34

Note : In reporting the progressive total of physical units financed under the scheme, care may be taken in respect of those investmentwhich disbursements are made in instalments so that the same unit is not counted again in the progressive total.

2

8/6/2019 Operational Guidelines for NBFCs

http://slidepdf.com/reader/full/operational-guidelines-for-nbfcs 27/34

ANNEXURE -VII

(Pre Sanction Procedure - NFS)

Form of Application Requesting for Disbursement of Refinance(Application Form for first drawal - NFS)

(to be submitted in duplicate)

Ref No: Date

The Chief General Manager/ General Manager

National Bank for Agriculture

and Rural Development

Dear Sir,

Disbursement of refinance -

(Name of industrial unit)

Please refer to your letter No. sanctioning to our

company refinance of Rs. under the above mentioned scheme. We confirm

having sanctioned a term loan of Rs. to our constituent /s, viz.

(hereinafter referred to as “the borrower/s) under the above mentioned scheme of

development approved by the NABARD, for which our company intends to avail of the

refinance sanctioned by the NABARD under your above mentioned letter.

1. We advise that out of the aforesaid loan sanctioned by us, our company has

advanced a sum of Rs. to the borrower/s upto .

The amount outstanding from the borrower/s against our above disbursement as on

this day is Rs. .

2. We confirm that loans in respect of which refinance is sought hereunder are not

more than 12 months old. The above disbursement sought to be refinanced is also

net of subsidy / recovery already received.

3. We confirm that the present loan together with previous loans, if any, granted to

the above constituents are within the exposure limit of our company.

4. We confirm that we have obtained the Agreement from the borrower/s for the total

loan sanctioned under the scheme in a form which is in consonance with the

provisions of the Agreement dated (date of General Refinance

1

8/6/2019 Operational Guidelines for NBFCs

http://slidepdf.com/reader/full/operational-guidelines-for-nbfcs 28/34

Agreement to be given) and the sanction letter dated .Interest on

the above amount already disbursed to the borrower is payable at p.a.

5. The action taken by our company on the conditions/ suggestions as required by

the NABARD in its letter of sanction under reference is indicated in the Annexure

enclosed (where applicable).

6. We now request you to disburse to us a sum of Rs. by credit to

our account with the (name of the

company) against our advances already made to the borrowers under the scheme as

mentioned under paragraph 1 earlier. The refinance to be drawn by our company as

above will be repaid to NABARD on the dates indicated below:

Amount to be repaid on or before

Year 31st January (Rs) 31st July (Rs)

7). To enable you to release the refinance requested for as above, we are now

furnishing the following further information and documents required by you.

i. Our company has already obtained adequate security both primary and collateral

from the borrower/s for the loan sanctioned by us, for which the said refinance is

claimed.

ii. We hereby declare and undertake that whatever security we have obtained or may

obtain from time to time from the borrower/s to secure the loan in question will be

held in trust for and on behalf of NABARD and any realisations or recoveries from the

borrowers under the said loans will be applied as required under Section 29 of the

National Bank for Agriculture and Rural Development Act, 1981.

Yours faithfully,

(Authorised signatory)

For and on behalf of Company

2

8/6/2019 Operational Guidelines for NBFCs

http://slidepdf.com/reader/full/operational-guidelines-for-nbfcs 29/34

ANNEXURE - VIII

(Pre Sanction Procedure - NFS)

Form of Application Requesting for Disbursement of Refinance

(Application for second and subsequent drawals - NFS)

(to be submitted in duplicate)

Ref No: Date

The Chief General Manager/ General Manager

National Bank for Agriculture

and Rural Development

Dear Sir,

Disbursement of refinance -

(Name of industrial unit)

-----------------------------------

------------------------------------

In continuation to our letter no. dated

with regard to the above mentioned scheme, we advise that our company has

advanced a further sum of Rs. upto / during to our

constituents, viz. (hereinafter referred as the said borrower/s ) under the scheme.

The amount of loan under the refinance sanctioned by your bank outstanding against

our said borrowers as on date is Rs. (which is exclusive of the

disbursement made upto covered in our previous drawals

mentioned above). We also confirm that the above disbursement of loan was made by

us after satisfying ourselves that the previous instalments of loans advanced to the

said borrowers and against which our company has drawn refinance from NABARD

was properly utilised by the said borrower/s for the purposes and in the manner

specified under the development scheme approved by NABARD for the granting of

refinance to our company.

2. We confirm that loans in respect of which refinance is sought hereunder are

not more than 12 months old. The above disbursement sought to be refinance is alsonet of subsidy / recovery already received.

3

8/6/2019 Operational Guidelines for NBFCs

http://slidepdf.com/reader/full/operational-guidelines-for-nbfcs 30/34

3. We confirm that the present loan together with previous loans, if any, granted

to the above constituents are within the exposure limit of the Company.

4. Interest on the above amount already disbursed to the borrower is payable at

p.a.

5. We now request you to disburse a sum of Rs. by credit to our

account with the (name of the company) against the

instalments of loans already disbursed by our company to the borrowers under the

scheme as mentioned under paragraph 1 earlier.

6. The refinance to be drawn by our company as above will be repaid to the

NABARD on the dates indicated below:

Amount to be repaid on or before

Year 31st January (Rs) 31st July (Rs)

7. To enable you to release the refinance requested for as above, we are now

furnishing the following further information and documents required by you.

i. Our company has already obtained adequate security both primary and collateral

from the borrowers for the loan sanctioned by us for which the said refinance is

claimed.

ii. We hereby declare and undertake that whatever security we have obtained or may

obtain from time to time from the said borrower/s to secure the loan in question will

be held in trust for and on behalf of NABARD and any realisations or recoveries from

the borrowers under the said loans will be applied as required under Section 29 of the

National Bank for Agriculture and Rural Development Act, 1981.

iii. We also confirm that we have obtained the Agreement from the said borrower/s

covered by this application for the drawal of refinance, for the total loan sanctioned to

them in a form which is in consonance with the provisions of the Agreement dated

(date of General Refinance Agreement to be given) and the sanction letter dated

Yours faithfully,

(Authorised Signatory)

For and on behalf of Company.

4

8/6/2019 Operational Guidelines for NBFCs

http://slidepdf.com/reader/full/operational-guidelines-for-nbfcs 31/34

ANNEXURE IX

DRAWAL APPLICATION FOR SANCTION AND RELEASE OF REFINANCE UNDER ARF

Ref. No. Date:

From : (Name and address of the NBFC)

The Chief General Manager/General Manager/Officer-in-ChargeNational Bank for Agriculture

and Rural DevelopmentRegional Office,

______________________

Dear SirSHG Bank Linkage Programme - Application for sanction and release ofRefinance against lendings to SHGs/NGOs for on-lending to SHGs--------------------------------------------------------------------------------------We advise having sanctioned and disbursed during the quarter ended June /September / December / March * ------- (year) a sum of Rs. ...................... (Rupees.......................................... ........................................................... ) to Self HelpGroups / NGOs for on-lending to SHGs, the details of which are given in the enclosedstatement. We request you to sanction and release refinance of Rs......................... (Rupees .................................................................................. ) thereagainst.

2. We agree to abide by all the terms and conditions of NABARD forfinancing at ground level and that of refinance, stipulated from time to time.

3. We agree to repay the refinance in half-yearly instalments, irrespective of therepayment period fixed by us at the borrower level.

Yours faithfully

Signature of theauthorised official

Encl : * Strike out whichever is not applicable

From Borrower to NBFC From NBFC to NABARD(Repayments receivable during) (Repayable on)

DateAmount

DateAmount

01 July ……… to31 December…….

31 January ………..

01 January……. to30 June ……………

31 July ………..

5

8/6/2019 Operational Guidelines for NBFCs

http://slidepdf.com/reader/full/operational-guidelines-for-nbfcs 32/34

ANNEXURE- X

ARF – FORMATAll loans other than SHG loans

DRAWAL APPLICATION FOR SANCTION / RELEASE OF REFINANCE UNDERAUTOMATIC REFINANCE FACILITY (ARF)

Ref. No. Date :

From (Name & Address of the NBFC)

To

The Chief General Manager/General Manager/Officer-in-ChargeNational Bank for Agriculture

and Rural DevelopmentRegional Office,

_______________________

Dear Sir

Investment Credit - Automatic Refinance Facility -Application for sanction / release of refinance

We hereby apply for sanction and release of refinance aggregating Rs..................……..(Rupees ......................................................................................................only) inrespect of financial assistance provided by us to our constituents, the particulars inrespect of which are furnished in the Annexure. We agree to repay the refinanceavailed of by our NBFC as per the repayment schedule appended to this drawalapplication. We also agree that the repayment schedule(s), if revised andcommunicated by NABARD, in respect of refinance claimed in this applicationincluding the grace period and repayment period applicable to the ultimateborrowers, the same will be followed scrupulously by us.

2. We certify that:

i. The individual loan proposals conform to the policies, procedures and guidelineslaid down as per the refinance schemes of NABARD from time to time.

ii. The individual investment proposals have been appraised by us / our branchesand are found to be technically feasible and financially viable.

iii. Only economic units have been financed with realistic unit costs arrived at,depending upon the local conditions and merits of each case.

6

8/6/2019 Operational Guidelines for NBFCs

http://slidepdf.com/reader/full/operational-guidelines-for-nbfcs 33/34

iv. We have not applied earlier for refinance against the loans covered by thisdrawal application.

v. The loan amount is exclusive of recoveries / subsidies/margin money received /receivable if any and also working capital / production credit.

vi. In respect of loans under government sponsored programmes, the loans havebeen disbursed to borrowers identified and whose applications were sponsoredby nodal departments/agencies implementing the scheme.

vii. Adequate working capital / production credit has been provided / will beprovided to the units / our constituents covered under this application on acontinuous basis to ensure optimum capacity utilization and regular incomegeneration.

viii.We have obtained consent letters from our constituents to the effect that theyhave no objection to our furnishing to NABARD all such information as it mayrequire from time to time.

ix. NABARD shall have the right to seek any information as it may require from timeto time and also for inspection of the unit/ farm during the currency of loan/refinance

x. NABARD shall have the right to inspect our books and loan accounts coveredunder this application and /or call for copies of the relative memoranda/sanction notes/ any other relevant information in this behalf.

xi. Loans granted under DRI scheme have been excludedxii. All the units financed under Non Farm Sector (NFS) in respect of which refinance

is claimed are located in rural areas as defined by RBI/NABARD and are eligiblefor refinance.

xiii.We have satisfied ourselves that public passenger vehicles under SRWTOscheme financed by us are used for carrying both goods and passengers.

xiv. The loans sanctioned to the borrowing units do not exceed the maximumloan limits prescribed under the respective Refinance schemes.

xv. Loans disbursed under Minor Irrigation (MI) are in blocks with sufficientpotential. Further, the loans disbursed for pumpsets are selected and installedas per guidelines given in BIS-10804-86.

3. We further certify that the amount of refinance already availed of by us andoutstanding as on date together with the proposed availment would be within theborrowing limit of our NBFC.

4. We also certify that the rates of interest charged on the loan amount conform tothe rates wherever stipulated by RBI / NABARD from time to time.

5. We agree that if on verification of our records and of our constituents, NABARDcomes to the conclusion that the accounts against which the disbursement of loanhas been made does not conform to the guidelines laid down by it from time to time,NABARD will have the right to recall the entire refinance disbursed in respect of suchaccounts, as per General Refinance Agreement.

6. Quantum-wise break up of loans in respect of which refinance has been claimed isgiven below:

7

8/6/2019 Operational Guidelines for NBFCs

http://slidepdf.com/reader/full/operational-guidelines-for-nbfcs 34/34

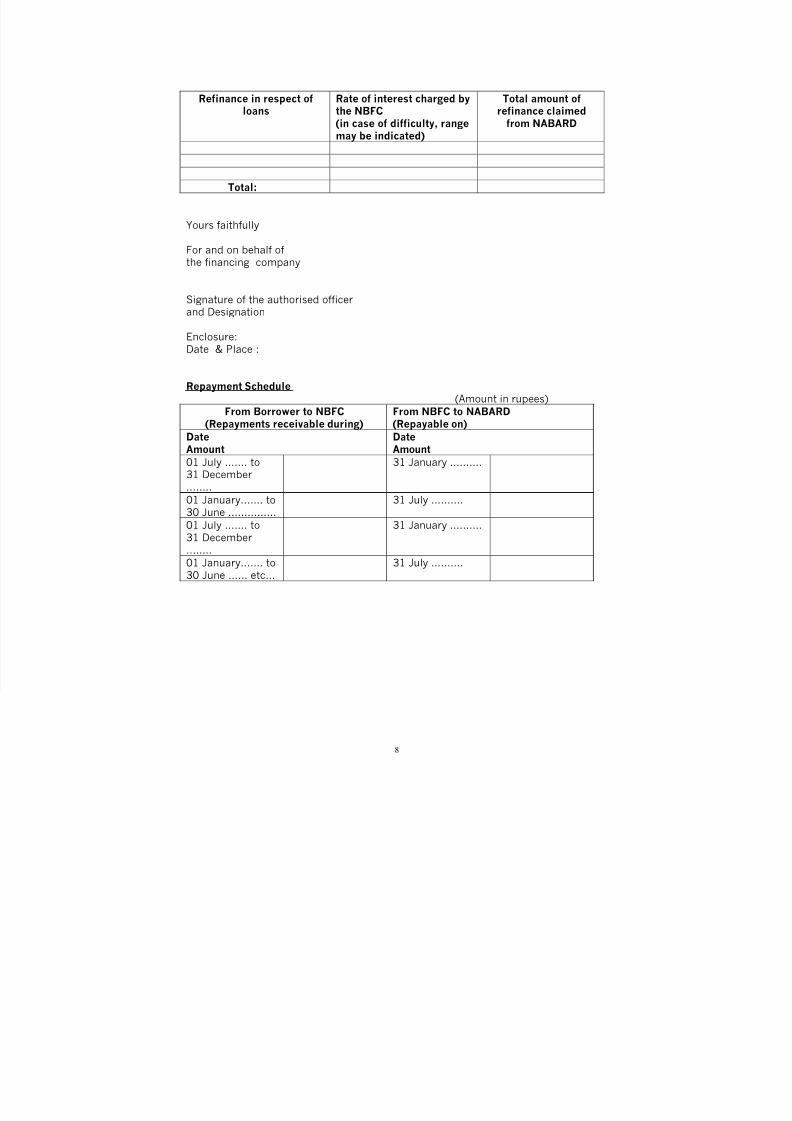

Refinance in respect ofloans

Rate of interest charged bythe NBFC

Total amount ofrefinance claimed

(in case of difficulty, range

may be indicated)

from NABARD

Total:

Yours faithfully

For and on behalf ofthe financing company

Signature of the authorised officerand Designation

Enclosure:Date & Place :

Repayment Schedule(Amount in rupees)

From Borrower to NBFC From NBFC to NABARD(Repayments receivable during) (Repayable on) DateAmount

DateAmount

01 July ……. to31 December..……

31 January ……….

01 January……. to30 June ……………

31 July ……….

01 July ……. to31 December

..……

31 January ……….

01 January……. to30 June …… etc…

31 July ……….