opportunities and risks in cross-border m&a

TRANSCRIPT

Brazil on the Buy-side: OppOrtunities and risks in crOss-bOrder M&a

In cooperation with

2

brazil on the buy-side: Opportunities and risks in cross-border M&a

MethodologyIn the third quarter of 2011, mergermarket interviewed C-suite executives and senior management from 30 Brazilian multinationals. Respondents were pre-screened and required to have been involved in a cross-border M&A transaction within the past three years worth a minimum of US$50m. Respondents offered their perspectives and insight into the risk and human capital issues Brazilian firms encounter when undertaking cross-border transactions.

respOndent deMOgraphic

ontentsMethodology 2Foreword 3highlights 4Brazil Goes Global 6risks and Protection 9human Capital assessment 13lessons learned 23

Contents

Chief Executive Officer

President

Board member

Director of Strategy

Director of Investor Relations

Director of Mergers & Acquisitions

Chief Financial Officer/Director of Finance

53%

17%

10%

7%

7%

3%

3%

Foreword

3

ForewordAs companies around the world shake off the last few years of market malaise, many have reset their priorities. They are seeking accelerated growth by moving into new markets and by transforming the way they do business.

Mergers and acquisitions (M&A) has emerged as an integral part of that growth strategy for most organizations, and with Brazilian companies in particular. But expanding into new countries and operating globally is one of the hardest business challenges an employer can face.

To assess these changes taking place on the front lines of many Brazilian companies, Marsh and Mercer partnered with mergermarket in the third quarter of 2011 to survey leaders of some of the largest and most respected Brazilian multinational organizations. In a series of interviews, these senior leaders helped shed light on the latest M&A trends, the rapidly changing global growth value proposition, and best practices for positioning firms and their people for future growth. On the following pages, we outline these leaders’ most pressing concerns and solutions for managing a global growth strategy through cross-border acquisitions.

Developing a global presence requires a commitment to finer details:

• Innovation that differentiates the business plan in each new market to meet more dynamic and complex demands

• A corporate culture ready and able to operate anywhere in the world

At the same time, Brazilian companies face several challenges in their quest towards globalization:

• Finding Brazilian professionals with the skills to be globally mobile, thus requiring a global mindset profile which includes multicultural leadership skills

• Employing detailed internal and external risk management when working in new business environments

Given the dynamism of emerging economies, a realignment is occurring in the axis of power among nations. This will demand changes at a pace that will challenge the sustainability of company growth rates. We should also not lose sight of the fact that companies are people connected by an organizational culture of whom we expect rapid adaptation and transformation in this new environment.

Companies whose global expansion strategies will be successful are those whose growth strategy, process discipline, culture and people best adapt to the relationships of global interdependencies.

We hope you find this report of value as you pursue new deals and strive to realize maximum value from them.

Eugenio Paschoalbrazil president and ceOMarsh

Paulo Baptistabrazil private equity M&a servicesMarsh

Alberto MondelliMarket Leader south Latin americaMercer

Luiza Barguil brazil Market LeaderM&a consulting services Mercer

4

brazil on the buy-side: Opportunities and risks in cross-border M&a

Key findings include:•Brazilian multinationals will continue to be acquisitive: 50% of

respondents will acquire targets outside of Brazil in the next 12-24 months

•Greater than 50% of respondents will focus on China and India for acquisition targets: Western developed nations are a lesser priority

•Cross-border deals increase exposure to risk: 50% of respondents have terminated a deal due to risks associated with a foreign target, citing lack of proper resources to assess and account for potential risk

•Many deals are failing to close simply because additional risk management methods are not being explored: Only 18% of respondents discussed implementing insurance solutions to preserve the transaction

•Political instability and market risks are primary cross-border concerns: Respondents are most concerned with being exposed to political uncertainty and market conditions when expanding outside of Brazil

•Directors and officers are concerned about personal liabilities: Over three quarters of respondents say expanding into new jurisdictions creates concern for their personal liabilities due to the way Brazilian firms are structured

HighlightsBrazil has increased its presence on the global stage with recent economic growth. This is evidenced by the fact that Brazilian acquirers racked up a reported US$14.3bn in deals with foreign targets in 2010 – which surpassed the previous three years combined.

This report examines three key areas of cross-border M&A opportunities: risk assessment, human capital and culture. Through interviews with senior executives of Brazilian multinationals who have recently completed M&A transactions, Marsh and Mercer, in cooperation with mergermarket, garnered the current thinking and strategy as it relates to these areas. The final results suggest that increased attention across all three dimensions — risk, human capital and culture — often make or break deals. By addressing these areas, transaction success can materially improve.

highlights

5

•HR is part of C-Level: Two thirds of respondents state that HR executives are part of the senior management team and play an increasing role in deal success

•Understanding culture is critical to deal success: 50% of respondents rank national and organizational culture differences as the top integration challenge, and seek better ways to assess and influence behavior to achieve desired outcomes

•Most multinationals in this survey (80%) have not yet developed a structured approach to effectively diagnose, manage and integrate organizational culture despite the wide recognition and agreement on the importance of addressing culture in a deal

•Leadership retention issues are cited as one of the most significant people challenges by 43% of respondents: This suggests customized approaches to retention management and engagement should be implemented

• 83% of Brazilian multinationals recognize the importance of leadership assessment prior to deal signing and use executive interviews to assess current roles, experience, contribution and alignment with the business strategy of the “new” company

•Effective, proactive employee communications and early organizational culture assessment and measurement are two areas of focus for improved M&A success in their next transaction

6

brazil on the buy-side: Opportunities and risks in cross-border M&a

Brazil Goes GlobalBrazilian multinationals to be active cross-border acquirers

50%

37%

13%

0

10

20

30

40

50

60

70

80

Brand acquisitionsAcquire technologyDistressed opportunities

Low valuationsDiversification of product/services

Economies of scale/reduce costs

Global expansion for current

products & services

Industry consolidation

73%

67%

57%

40%37%

33%30%

27%

Half of survey respondents plan to include cross-border deals as part of their M&A strategy over the next 12-24 months. Key factors driving the activity include industry consolidation, global expansion of current products and services and economies of scale/cost reduction.

As Brazil’s economy surged through recovery after the financial collapse, Brazilian corporations expanded both

domestically and internationally. In 2010, Brazilian buyers purchased 184 targets worth a reported total of US$52.2bn (35 were cross-border transactions worth over US$14.3bn), according to research by mergermarket. This surpasses the previous three years combined.

While 20111 has seen a healthy level of Brazilian acquirers (130 deals worth US$27bn), cross-border activity has been

slightly muted (16 deals worth US$3.9bn), as multinationals focus on domestic targets. This affirms what nearly three quarters of respondents state about the necessity of consolidation in order to compete with larger firms. Similarly, 67% believe companies will be driven by the initiative to take products and services global.

Brazilian multinational companies are often motivated by

dO yOu pLan tO engage in a crOss-bOrder M&a transactiOn in the next 12-24 MOnths?

What WiLL be the MOst iMpOrtant drivers OF yOur OrganizatiOn’s M&a strategy Over the next 12-24 MOnths?

Yes

No

Uncertain

1 mergermarket data as of September 23, 2011.

7

brazil goes global

7

more than one of these drivers in their bid to become global. The creation of Brasil Foods (BRF), a result of the merger between Sadia and Perdigão, clearly aims to achieve scale to be even more competitive globally. BRF also targets cross-border acquisitions to expand its products, thus having greater proximity to its consumer. To further illustrate several of these drivers, in the largest Brazilian cross-border acquisition of 2011, Companhia Siderúrgica Nacional, the listed Brazil-based steel producer has acquired steel and cement assets from Alfonso Gallardo SA, the Spain-based company for US$1.35bn. Additionally, seven of the top 10 largest Brazilian multinationals have made cross-border acquisitions in the past two years. Most of these acquisitions were aimed at improving efficiency and expanding products and services, such as Vale’s US$2.5bn purchase of a Channel Islands-based mining company, BSG Resources (Guinea) Limited, in April 2010.

In any acquisition, the most sensitive aspect is people. In an international acquisition, the culture component is an added factor. As such, retaining local leaders and acting through them will reduce the level of workforce anxiety. Together, with clear and all-embracing communication, good and bad news must be delivered quickly. José antonio do prado Fay - president - brasil Foods

“1 mergermarket data as of September 23, 2011.

8

brazil on the buy-side: Opportunities and risks in cross-border M&a

Priorities are staying close to home and China, india

0

10

20

30

40

50

60

70

80

AustraliaMiddle EastAfricaWestern Europe

Japan, KoreaEastern Europe

North America

China, India, SE Asia

BrazilLatin America (excl. Brazil)

23%

3% 7%

23%17%

3%

3%7% 13%

7%3%

7%

3%

7% 3%7%

17%

3%17%

13%

3%

50%

43%

Respondents were asked about their M&A strategy and stated intentions to evenly focus on domestic and foreign transactions. While domestic M&A will remain a part of respondents’ strategy, outside Brazil these dealmakers are primarily looking to expand across the Latin American region where, according to mergermarket data, 44% of Brazilian cross-border targets from Q1 2010 through Q3 2011 were based. Greater than half of respondents will

also make their Asian counterparts in India and China, “the growth markets,” a major target, representing a more recent M&A trend in Brazil.

Signaling a shift in the global market for M&A targets, the world’s developed economies in North America, Western Europe, Japan and Korea fall behind emerging regions, especially Brazil and Latin America, according to

rank the tOp three regiOns Or cOuntries yOu expect tO be MOst iMpOrtant tO yOur M&a strategy Over the next 12-24 MOnths.

Per

cent

age

of r

espo

nden

ts

First

Second

Third

respondents. Indeed, the banking collapse and the European sovereign debt crisis hit the G7 industrial nations the hardest while the E7 emerging nations (China, India, Brazil, Russia, Mexico, Indonesia and Turkey) fared better. The E7 nations continue to experience rapid GDP growth and are projected to surpass the G7 by 2050, according to industry analysts. Brazil and its multinationals are set to be major players in reshaping the global economy.

risks and protection

9

Risks and ProtectionPolitical risk most concerning for executives

0

20

40

60

80

100

Natural disasters

Supply chain disruptions

Regulatory frameworks

Environmental risksCorruptionMarket risksPolitical instability

7% 3%

20%

17%

20% 13%

27%

37%

13%

20%

27%

30%

33%

7%3%

34%

20%

13%

13%

10%

20%

34%

13%

13%

30%

10%

20%

23%

30%

34%

13%

20%

20%

43%

10%

Executives in Brazil consider political instability as the greatest risk when expanding into foreign countries, rated “extremely important” by 43% of respondents. Many respondents say the disparate and constantly changing tax and regulatory policies account for their concerns of political instability, though one head of finance comments that “political instability is the bigger concern since we do not have any kind of management to reduce this type of risk.”

taking intO accOunt the risks yOu cOnsider beFOre expanding yOur business Outside OF braziL, rate the FOLLOWing FactOrs in Order OF iMpOrtance.

Per

cent

age

of r

espo

nden

ts

Extremely important

Very important

Moderately important

Slightly important

Not important

Political risk insurance

Political instability remains prevalent in many parts of the world and instances of political violence can occur with little warning in countries previously considered relatively stable. Given the recent events, there is now a trend to purchase global programs covering broader geographical exposures with more comprehensive perils.

To help mitigate the various political and credit risks Brazilian companies face when trading and investing in foreign countries, they should strongly consider insurance solutions.

Examples of insurance solutions we have implemented for our clients include:

Cover for Equity Investments: Expropriatory actions by the host government including forced divestiture and denial of justice. Currency inconvertibility is often added on to cover cross-border payments such as dividends and intercompany loans.

Cover for assets: Property damage and subsequent business interruption due to Political Violence (including terrorism, sabotage, strikes, riots, civil commotion, revolution, rebellion, war, civil war), forced abandonment, and deprivation of ownership and use. Cover for Contracts: Counter-party non-performance due to government actions and/or counter-party credit risk.

10

brazil on the buy-side: Opportunities and risks in cross-border M&a

transactional risk insurance

Sophisticated corporate buyers are adopting innovative insurance solutions to eliminate deal breaking issues and facilitate the closing of transactions; these “Transactional Risk” solutions are increasingly being implemented on M&As around the world and are available to Brazilian companies.

On the buy-side, some of the motivations for using Transactional Risk insurance are to provide for additional protection beyond the indemnity cap in the purchase agreement and to limit post-closing adversarial proceedings with the seller.

A Transactional Risk insurance solution is particularly attractive if your company plans to make acquisitions in less familiar geographies or is concerned about the strength of the seller’s covenants. For example the buyer would be able to make a claim against an insurance policy in the event of a breach of a representation/warranty, or tax covenant by the seller.

On the human capital side, in addition to the benefits noted above, this structure also allows recovery of the loss without the need to litigate or recover the loss from the management team should it remain post-transaction.

lack of consensus can terminate a deal; insurance a neglected solution

While Brazilian companies’ outbound M&A has grown significantly, 50% of respondents report that potential deals or transactions have not been closed due to risks identified with the target company. Respondents note that they do not have the proper resources to assess and account for the impact of potential risk, thus deals have been terminated.

Because of the numerous risks associated with a transaction, M&A discussions include talk of warranties and indemnities.

When negOtiating an acquisitiOn OppOrtunity Outside OF braziL, have any risks OF the target cOMpany prevented the deaL FrOM cLOsing?

did any party suggest an insurance pOLicy tO try and resOLve the diFFerences?

50%50%

Yes

No

18%

82%

Yes

No

As with many aspects of negotiations, there is often a gap between the buyer and seller on these issues, and half of respondents admit that a deal has been terminated due to the lack of consensus on warranties and indemnities. When parties are unable to agree to terms of protection after risk assessment, only 18% of respondents mention that an insurance solution was discussed to preserve the transaction. Many deals are failing to close simply because additional methods of risk management are not being explored.

risks and protection

11

Not concerned

Slightly concerned

Moderatelyconcerned

Very Concerned

Extremely concerned

3%

14%

7%

31%

45%

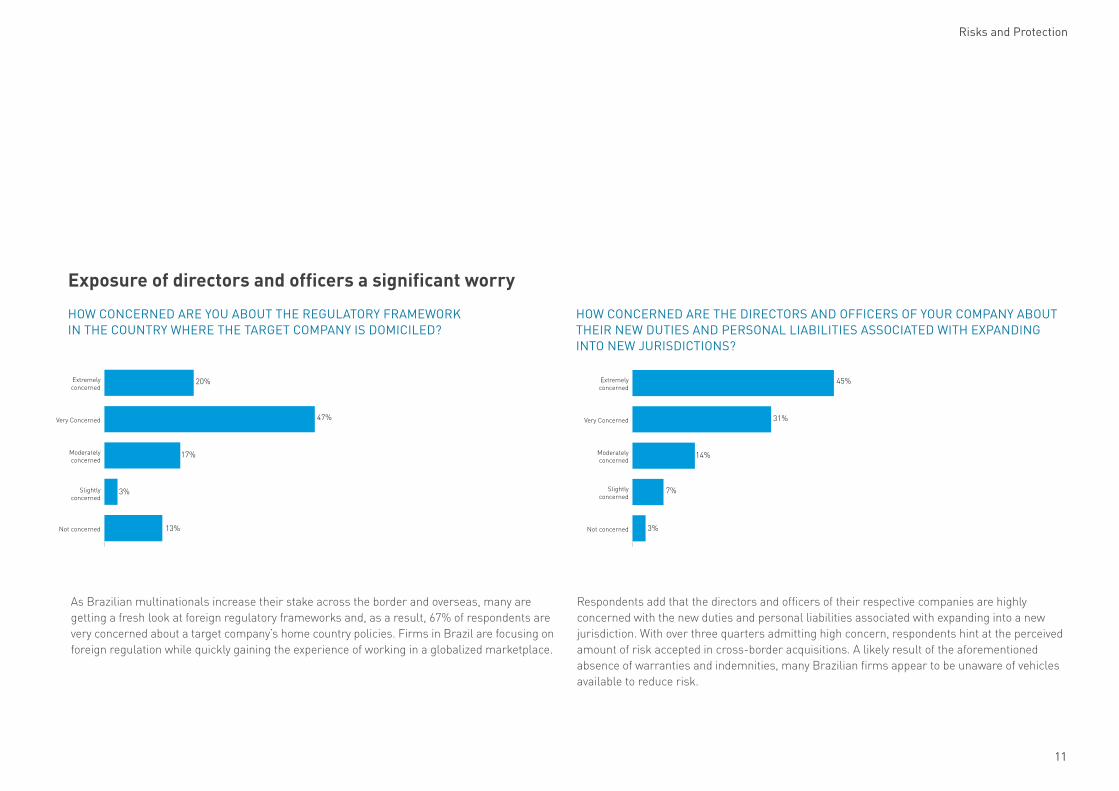

exposure of directors and officers a significant worry

hOW cOncerned are yOu abOut the reguLatOry FraMeWOrk in the cOuntry Where the target cOMpany is dOMiciLed?

hOW cOncerned are the directOrs and OFFicers OF yOur cOMpany abOut their neW duties and persOnaL LiabiLities assOciated With expanding intO neW JurisdictiOns?

As Brazilian multinationals increase their stake across the border and overseas, many are getting a fresh look at foreign regulatory frameworks and, as a result, 67% of respondents are very concerned about a target company’s home country policies. Firms in Brazil are focusing on foreign regulation while quickly gaining the experience of working in a globalized marketplace.

Respondents add that the directors and officers of their respective companies are highly concerned with the new duties and personal liabilities associated with expanding into a new jurisdiction. With over three quarters admitting high concern, respondents hint at the perceived amount of risk accepted in cross-border acquisitions. A likely result of the aforementioned absence of warranties and indemnities, many Brazilian firms appear to be unaware of vehicles available to reduce risk.

Not concerned

Slightly concerned

Moderatelyconcerned

Very Concerned

Extremely concerned

13%

3%

17%

47%

20%

12

brazil on the buy-side: Opportunities and risks in cross-border M&a

Combining internal and external expertise is the best approach for risk assessmentAs the results highlight, companies must pay close attention to risks while assessing potential targets. While a handful of respondents indicate that they conduct the entire risk assessment process either internally or externally, the majority express the view that a combination of the two is the most successful approach. Respondents typically seek out external advisors for risks associated with macro issues, such as the environment, regulatory frameworks and market conditions. They tend to internalize the more micro aspects dealing with specific companies, including financial, operational and strategic risk.

Given that in recent years many Brazilian companies have started to engage in cross-border M&A for the first time, their directors and officers may be neglecting or underestimating that, as their companies expand overseas, they are navigating dangerous new waters in terms of individual liabilities, increasing the risks to their reputation and personal assets. solon cunha - partner - Machado Meyer

“

hidden M&a risks for directors and officers

When a Brazilian company is involved in a cross border acquisition (or joint venture), its directors and officers are exposed to a potentially higher level of risk and sometimes unknown litigation environment. In addition, there are significant financial interests of the company’s shareholders and lenders at stake. As a result of the acquisition there will be new employees, vendors, customers, creditors and shareholders, as well as different rules and regulations with which to comply. Directors frequently must make strategic decisions with less than perfect information in a compressed timeframe. Also, once completed, such deals are closely watched by investors, anti-trust agencies, unions, the press and many other interested third parties.

Records show that the potential for and frequency of claims against the directors and officers increases if a company is involved in an acquisition. Claims result not only from the failure of the deal itself, but also from pre-acquisition wrongful management acts.

Marsh provides assistance to our clients to address the unique and challenging M&A issues that arise when structuring a comprehensive Directors & Officers (D&O) insurance program. Policies should have proper run-off clauses to cover future claims arising from prior acts as well as coverage to automatically include newly acquired entities. Coverage should include claims made in any foreign jurisdiction where the claimants, insured entity or directors have legal domicile. Given the myriad of potential acquisition structures, Marsh ensures that policies are tailored to the specific type of acquisition vehicle that is utilized.

human capital assessment

13

Human Capital Assessmentthe human resource function is playing an increasing role in deal success

17%

83%

When are hr Managers brOught intO the M&a prOcess?

dO yOu pLan tO change this in the Future?

In today’s world, management and retention of critical talent provides a competitive advantage for many firms, and the human resources (HR) function is increasingly a driver of organizational success. Having a clear understanding of the human capital opportunities and risks in M&A transactions and executing on your investment thesis is essential to integrating the target company.

In order to understand senior managers’ perspectives on the

Yes

No

When making an international acquisition, culture is fundamental and the due diligence process needs to go beyond the financial and legal aspects. It has to be extended in order to understand and become familiar with the culture of the company being acquired. Culture “fit” is essential to the success of the transaction. cleber Morais - president - bematech

“Limited/no involvement

During the integration of the companies

Immediately after the deal has been signed

When conducting due diligence

When considering potential targets

33%

23%

20%

7%

17%

14

brazil on the buy-side: Opportunities and risks in cross-border M&a

role HR plays in an organization, respondents were asked a series of questions about HR managers’ current roles and how they will change in the future.

Two thirds of respondents indicate that HR managers are part of their C-Level management team. There does not, however, appear to be a significant correlation between HR membership in the C-level team and their involvement in the M&A process. A company whose HR is not represented in the senior management team will bring HR in to evaluate acquisitions as often as a company whose senior management includes HR.

The majority of respondents (56%) say they bring HR into the equation before deal signing. An additional 17% bring HR in immediately after the deal is signed. On the other hand, only 7% indicate limited or no use of HR. Furthermore, respondents do not expect to change their strategy. Among the 17% of respondents that say the stage of HR inclusion will change, most plan to bring them in earlier in the process.

While somewhat surprising to see little relationship between C-Level membership and HR involvement in M&A transactions, the senior managers typically have the greatest

say at this stage. One respondent explains that acquiring foreign targets is a relatively new venture for them, and while HR is not a part of the C-Level, they bring HR in during the due diligence phase and do not have specific plans to change this.

Among those corporations that bring HR in during the integration phase, the vast majority intend to leave the method unchanged. However, one director of finance suggests that because HR takes part from the beginning of the process to better evaluate the company fit the role of HR within his company is being reconsidered. Since a considerable portion of integration falls under HR’s responsibility, they need more time to assess, strategize and implement a cohesive plan.

When making an acquisition it is fundamental to define how we are going to deal with the workforce from Day One. Laércio cosentino - president - tOtvs

“

15

looking back: challenges that require attention early and often

0

10

20

30

40

50

Employee engagement

Employee retention

Integration issues

Leadership assessment and selection

Employee communications

and change management

National culture differences

Compensation and benefit programs alignment

Leadership/management

retention issues

Organizational/business

culture differences

23% 23%

7%

20% 27%7%

10%13%

7% 7%

3%3%7%

3%

17%

13%

7%

7%

20%7%

7%

17%

13%13%

10% 10%

LOOking back at yOur Last transactiOn, rank the three MOst signiFicant peOpLe chaLLenges yOur OrganizatiOn has Faced.

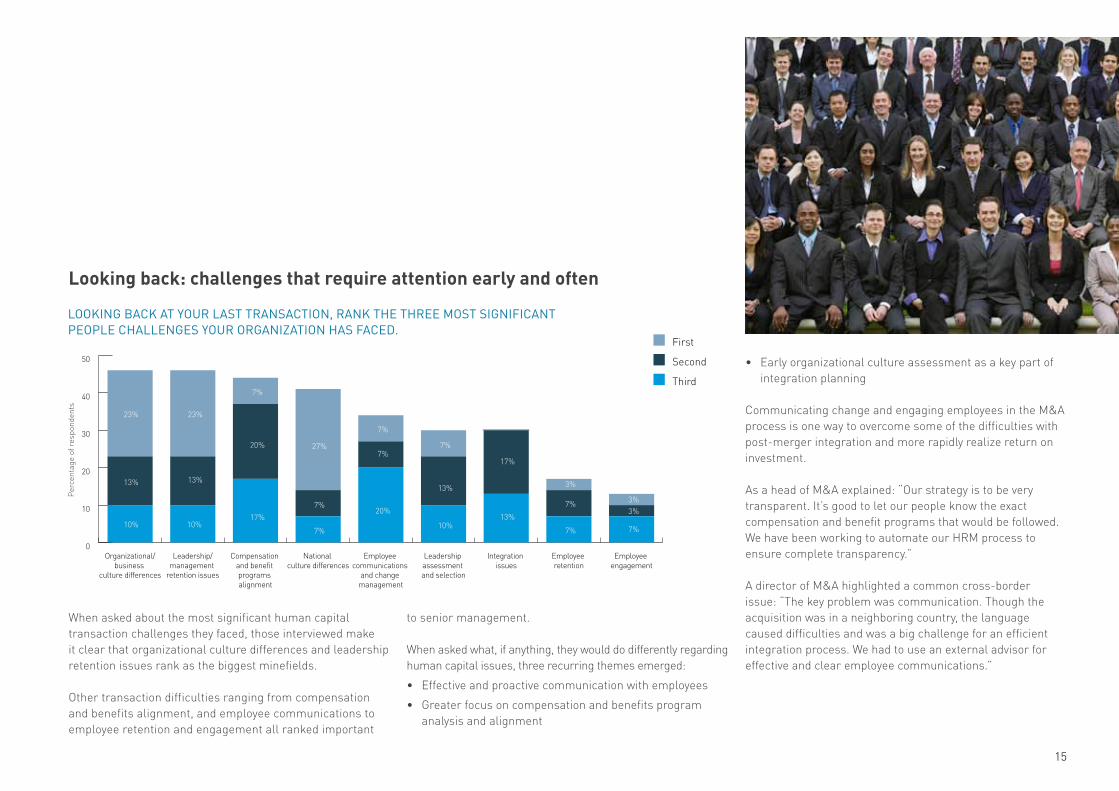

When asked about the most significant human capital transaction challenges they faced, those interviewed make it clear that organizational culture differences and leadership retention issues rank as the biggest minefields.

Other transaction difficulties ranging from compensation and benefits alignment, and employee communications to employee retention and engagement all ranked important

Per

cent

age

of r

espo

nden

ts

First

Second

Third

to senior management.

When asked what, if anything, they would do differently regarding human capital issues, three recurring themes emerged:

• Effective and proactive communication with employees

• Greater focus on compensation and benefits program analysis and alignment

• Early organizational culture assessment as a key part of integration planning

Communicating change and engaging employees in the M&A process is one way to overcome some of the difficulties with post-merger integration and more rapidly realize return on investment.

As a head of M&A explained: “Our strategy is to be very transparent. It’s good to let our people know the exact compensation and benefit programs that would be followed. We have been working to automate our HRM process to ensure complete transparency.”

A director of M&A highlighted a common cross-border issue: “The key problem was communication. Though the acquisition was in a neighboring country, the language caused difficulties and was a big challenge for an efficient integration process. We had to use an external advisor for effective and clear employee communications.”

16

brazil on the buy-side: Opportunities and risks in cross-border M&a

retaining your best people

One of the most frequently asked questions Mercer receives from organizations engaged in an M&A deal pertains to retention practices –“How do I retain my key people?” Leading companies address these concerns up front through variousapproaches, including strategic retention programs. Cash bonuses, equity and development opportunities are the elements to be considered as proven tools to keep key players. According to Alberto Mondelli, South Latin America Market Leader, Mercer: “As a rule of thumb, retention packages should be equal to severance packages, or better. Cash bonuses are more effective than equity (stock options, restricted stocks and performance units) in reducing turnover rates in a shorter period of time. Payments made within the first two years of the transaction are more effective for retention purposes. Companies usually reward employees required for the short term integration effort with cash instead of equity and enhanced severance packages. In our experience, companies must address engagement and career development as well as compensation elements for long term value creation. Effective use of promotions to a more senior level and lateral moves to new roles are effective ways to retain key leaders, and send a positive signal that may help retention efforts.” Continued focus and monitoring of the effectiveness of the retention plan is a condition for success. The objective is to make sure high-performing individuals – those with key skills – are retained to ensure business continuity, transition to a new structure or to benefit the new organization over time.

Brazilian companies need to learn to be a ‘head office’. This involves mature and consistent governance, processes, policies and management practices. The crucial matter, however, when putting into practice a globalization strategy, is that multicultural collaboration is not to be taken lightly. After all, when we are considering taking the company’s culture abroad, we are talking about taking people. And, as Brazilians feel very attached to an environment of affection, this presents us with an additional challenge. alfredo setubal – executive vice president - banco itaú

“

human capital assessment

17

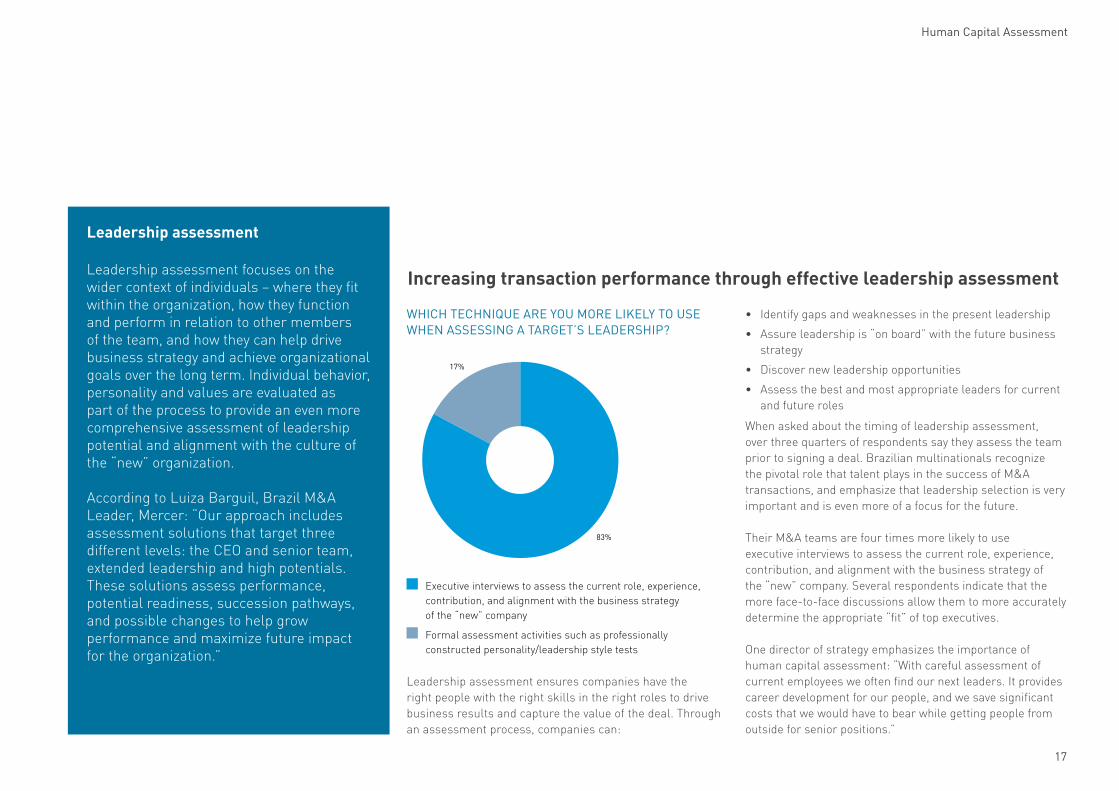

increasing transaction performance through effective leadership assessment

Leadership assessment ensures companies have the right people with the right skills in the right roles to drive business results and capture the value of the deal. Through an assessment process, companies can:

17%

83%

Which technique are yOu MOre LikeLy tO use When assessing a target’s Leadership?

Executive interviews to assess the current role, experience, contribution, and alignment with the business strategy of the “new” company

Formal assessment activities such as professionally constructed personality/leadership style tests

leadership assessment

Leadership assessment focuses on the wider context of individuals – where they fit within the organization, how they function and perform in relation to other members of the team, and how they can help drive business strategy and achieve organizational goals over the long term. Individual behavior, personality and values are evaluated as part of the process to provide an even more comprehensive assessment of leadership potential and alignment with the culture of the “new” organization.

According to Luiza Barguil, Brazil M&A Leader, Mercer: “Our approach includes assessment solutions that target three different levels: the CEO and senior team, extended leadership and high potentials. These solutions assess performance, potential readiness, succession pathways, and possible changes to help grow performance and maximize future impact for the organization.”

• Identify gaps and weaknesses in the present leadership

• Assure leadership is “on board” with the future business strategy

• Discover new leadership opportunities

• Assess the best and most appropriate leaders for current and future roles

When asked about the timing of leadership assessment, over three quarters of respondents say they assess the team prior to signing a deal. Brazilian multinationals recognize the pivotal role that talent plays in the success of M&A transactions, and emphasize that leadership selection is very important and is even more of a focus for the future.

Their M&A teams are four times more likely to use executive interviews to assess the current role, experience, contribution, and alignment with the business strategy of the “new” company. Several respondents indicate that the more face-to-face discussions allow them to more accurately determine the appropriate “fit” of top executives.

One director of strategy emphasizes the importance of human capital assessment: “With careful assessment of current employees we often find our next leaders. It provides career development for our people, and we save significant costs that we would have to bear while getting people from outside for senior positions.”

18

brazil on the buy-side: Opportunities and risks in cross-border M&a

organizational culture differences ranked as the most significant challenge

Nearly two thirds of respondents have experienced signifi-cant challenges when integrating corporate culture.

However you define culture – and whether or not you use the term “culture” – getting value out of your transaction is often highly dependent on how you deal with the differences (and similarities) in organizational behaviors. How well do the two organizations “fit” in terms of values and work practices, leadership styles, communications, risk tolerance, decision-

37%

63%

have yOu ever been invOLved in a deaL Where OrganizatiOnaL cuLture Was a signiFicant chaLLenge during integratiOn?

making approaches, speed, etc.?

When dealt with superficially, culture differences can impede productivity, limit revenue generation and, ultimately, erode deal value. Rapidly expanding Brazilian multinationals must take national, as well as organizational culture, into account to validate and capture intended synergies.

As one head of finance explains: “Multiple challenges exist when integrating cultures, such as differences in attitudes toward work, time and decision making by management.”

But despite the wide recognition and agreement of the importance of addressing culture in a deal, most acquisitive organizations in this survey (80%) have not yet developed a structured approach to effectively diagnose, manage and integrate organizational cultures.

As for how to best address M&A cultural integration issues within Brazilian multinationals, respondents offered the following tips:

• Replace existing management with professionals who are already aligned with the “new” corporate culture

• Distribute employee questionnaires and use responses to develop and execute the “right” strategy for integration

Yes

No

• Prepare and distribute clear and consistent communica-tion with employees in a timely and effective manner

• Engage outside advisors who have the experience and resources to help prioritize, organize and manage the integration effort

Right from Day One a strong organizational culture, which we can believe in as a value, must be present and implemented into the companies acquired. Furthermore, Brazil has a critical mass of managers with the ability to take on this challenge. We have to rely on our team.pedro passos - Founder and co-chairman of the board - natura

“

human capital assessment

1919

advantages of external advisors

Since 40% or more of all companies’ revenues today are spent on people (wages, benefits and training), dealmakers must pay close attention to human capital issues in every phase of the M&A process – and the earlier the better. For example, rising wage inflation in China and a shortage of technically trained people in India have made expansion into these countries increasingly difficult. Added to inflation and currency values placing upward pressure on wages at home, human capital for Brazilian business owners is becoming tougher to manage.

For these, and other reasons, three quarters of respondents reported hiring of external advisors to help with these human capital challenges. Respondents frequently cite skill assessment and labor risks as some of the main areas in which they seek advice. As one CFO stated: “We will need more external support in the future because M&A transactions are growing increasingly complex.”

early-stage, non-invasive cultural due diligence takes off

Mercer is undertaking an increasing number of early-stage cultural due diligence assignments for our clients. The purpose of this is to help frame negotiation strategy and systematically address the critical cultural integration risks inherent in a deal. Completed during an early phase of a deal, these largely “hands-off” analyses are used to:• Informbetterdecisionsaboutwhichtargetislikelytobemost compatible from a cultural perspective • Gainaclearerviewaboutorganizationfitandtheissuesthatneed to be addressed early • Factorculturaldifferencesandsimilaritiesintothenegotiationprocess• Guideduediligenceinvestigations• Testalignmentofseniorleadersonbothsidesofthetransactionand educate them about the strengths and differences in how they operate today and how they need to operate in the future • Createaplatformtoengageandcommunicatewithemployees• BuildmorerobustintegrationplansA comprehensive report is developed based on insights gained from a structured process to collect and draw inferences from public and archival data on several key organizational dimensions, such as organizational vision and mission, leadership, organization design, operating model, brand and reputation, corporate responsibility, cultural identity, reward and recognition, talent management, training and skills, diversity and employee relations. Where access is available, the report is often supplemented with interviews and/or a quick executive culture survey.

This high-value information is provided quickly and at the “right” time to positively influence negotiations and integration planning.

2010 was the year when we hired our 1,000th employee: a Russian designer to work at our unit in China, in a team headed up by an Indian and providing services to a Japanese client. This was symbolic, for we realized that we had dived head first into a multicultural arena of talent. cesar gon - ceO and Founder ci&t

“

20

brazil on the buy-side: Opportunities and risks in cross-border M&a

Marsh and Mercer’s Integrated Transaction Team will help your company derive value from an acquisition or joint venture by addressing the critical risk factors associated with the transaction. We will work closely with your due diligence teams and third party advisors to target issues that impact deal negotiations and to mitigate the risks that affect the long-term financial success of the transaction.

We have local offices and M&A experts on the ground throughout the world. We will assist your due diligence team by enhancing the traditional accounting, legal and investment banking due diligence services. Our services include:

• Identifying and evaluating the type and scope of existing risks and liabilities from a risk management/insurance/human capital perspective consistent with your practices and the target country requirements.

• Evaluating all insurance and human capital policies of the target company in order to provide analysis of the adequacy of coverage, scope and local practices, as well as determine the solvency of the insurance carriers.

• Projecting costs and potential savings, or additional costs associated with amending certain coverage requirements in order to be consistent with your risk management, insurance and people practices and as

Setting the Foundation for Deal Success: Risk and Human Capital Due Diligence

required in the target country.

• Uncovering hidden or understated liabilities as well as uninsured or underinsured exposures.

• Designing coverage for outstanding liabilities that are discovered during the due diligence process (including protecting the investment from catastrophic loss), structuring the right compensation & benefits architecture, and communicating them.

• Evaluating potential environmental risks and when appropriate we will structure an environmental insurance solution.

• Identifying major premium and benefit related long-term liability surcharges, retrospective adjustments and other policy clauses that may result in unexpected additional post-closure expenses.

Our M&A services are performed as entirely separate activities from the core client services, thus preserving the confidentiality and independence of each engagement. Such an independent evaluation prior to the closing of the transaction will reduce the burden on your risk management and human capital teams and provide the optimal platform post-close.

In short, this type of communication management delivers deal value. At the beginning of any transaction announcement, there is a dip in productivity. In addition to the time lost purely in speculation and gossip, some key employees inevitably join integration teams, often being asked to double up on their work to fulfill these new duties. There is suddenly a whole layer of team meetings and project management around the transaction. As the deal progresses, it starts to reach that crossover point where you begin to see the value creation that the deal promised in the first place. A smooth employee experience is one of the factors that can bring on value creation sooner, just like a negative or poorly managed employee experience can delay it. Keeping employees talking on point to customers, and aligning sales forces and leadership, is driven by managing the employee experience throughout the deal.

By following this approach to communication management, organizations are able to avoid simply reacting to the need to share information as decisions are made. Instead, the effort becomes more about delivering what employees need —promoting the desired employee experience to drive deal value.

To learn more, visit: www.mercer.com/mergers-acquisitions/managethemessage

Today’s environment leaves less time to plan, fewer effective retention tools and increasing potential for quick-spreading misinformation. This can be particularly damaging to cross-border transactions, where proclivity and sensitivity to miscommunication is heightened. To keep employees informed and engaged during a transaction, businesses must plan for and execute a thoughtful communication strategy over the deal life cycle.

Mercer’s perspective on M&a communication management includes a comprehensive, cohesive approach to running deal communications.

The way to ensure a smooth employee transition is to identify a group or person responsible for defining and creating a total employee experience, and empower them to manage, adapt and change organizational communication over the life of the transaction. Once appointed, this communication management group develops a comprehensive strategy in conjunction with business leadership and all integration workstreams and functions. This way, their strategy touches all parts of the transaction that affect employees, and they can manage to or revise that strategy over time, and create and publish content that reflects the full spectrum of information employees want and need.

Managing the MESSage

22

brazil on the buy-side: Opportunities and risks in cross-border M&a

Top executives know that for their companies to become strong global players, their leadership must have a global mindset and be experienced in working across borders. Companies are finding it increasingly difficult, however, to manage mobility in an efficient way, especially attracting, retaining and managing the right globally mobile talent.

the changing value propositionFor many organizations, opportunities for growth, efficiency and even survival are dependent on how well they manage in the global economy. Mobility strategy must help facilitate and execute business goals, rather than lag behind and play “catch up” to operating needs. A proactive approach that integrates workforce planning, talent strategy, reward strategy and governance is needed.

“Next generation mobility” will be more strategic, focused on value creation, will include segmentation by assignee and assignment type, and be connected to human capital and business goals.

How Leading Multinationals are Confronting – and Mastering – Global Mobility

According to Alberto Mondelli, “Organizations must manage people with the same rigor as they manage other tangible assets. Mobility leaders must think like investors and ensure that investments in a talent portfolio generate the desired return. These leaders must develop and operate creative and cost-effective programs that support new types of assignments. By leveraging the data and fact-based analytics underlying their people decisions, leaders can diagnose, predict and evaluate outcomes; with objective measures, they can correctly track the return on people investments.”

deployment of talent in a global environmentIdentify business drivers for mobility: The business case for mobility is rooted in specific objectives: growth or operating imperatives in specific locations, shortage of talent in new markets, talent gaps in key businesses, and the need to deploy specific skills within and across regions. Also, businesses are searching for new sources of global leadership, deep technical

expertise that isn’t available locally, talent development, knowledge transfer and improved governance.

Shape the workforce: Increasingly, the management of mobility and reward packages is being linked to talent management. As deployments increase, organizations are looking more closely at how they manage their international talent. These organizations continue to seek trusted, seasoned leaders to take on demanding assignments, and continue to use mobility to develop an international mindset among high-potential talent and future leaders. They are trying to improve how they identify and fill critical roles across businesses and how they manage talent pools within regions. In the process, they are recognizing that addressing all these talent questions requires a much better linkage than they had in the past between mobility programs and related talent processes.

Mercer’s perspective is that assignments differ in the value they deliver to the business as assignees move through different career cycles. Segmentation allows for differentiation across the range of assignment types and practices for talent deployment.

Lessons LearnedBrazilian multinationals are growing as quickly as their home country’s economy and simultaneously carving out a role in the global markets. However, according to our survey findings, global expansion via cross-border acquisitions may be tempered by undefined risks and human capital issues. As noted by the majority of respondents, such factors are costly and often affect the success of an M&A transaction. Companies ignore these issues at their own peril. A clear picture of the target’s exposure to various risks and its organizational culture are essential parts of the strategic approach to a successful acquisition. Once Brazil-based firms implement an apt system of risk and human capital assessment and management, they will have a stronger foundation on which to build and expand their operations in the dynamic global market.

Addressing one of their top business priorities, international growth, includes addressing the changing workforce and the complex risk environment.

These are trying times. What it takes to be a successful global leader is evolving as businesses are transforming, and there is an increasing emphasis on managing across borders and through change. However, Brazilian multinational companies are survivors after several years of unprecedented challenges in the domestic market. But in this new economy and shrinking world, nothing comes easy. It takes diligence, foresight and analytics to keep ahead of the latest trends. And today, these organizations are poised for success.

Marsh and Mercer wish to thank the companies participating in this survey.

For more information, please contact:

Paulo Baptistabrazil private equity M&a [email protected](11) 3741-1149

Luiza Barguilbrazil M&a consulting [email protected](11) 3049-5986

Brazil on the Buy-side: OppOrtunities and risks in crOss-bOrder M&a

In cooperation with