opportunities in - aicep portugal global · attributable to various cancer therapeutics in the...

TRANSCRIPT

Copyright © 2019 IQVIA. All rights reserved.

What are German companies looking for

in terms of open innovation and

technology in- licensing, R&D services

and clinical trials

Health Cluster Portugal, 30th September 2019

Opportunities in

Germany’s health market

Dr. Frank Wartenberg

President Central Europe

1

Sales trends in the German marketsegments

3

0%

5%

10%

15%

60

20

0

10

30

40

50

7065

46

20222014

59

52

2017 20182013 2015 2016 2019 2020 2021 2023

48

43 4447

55

61

68

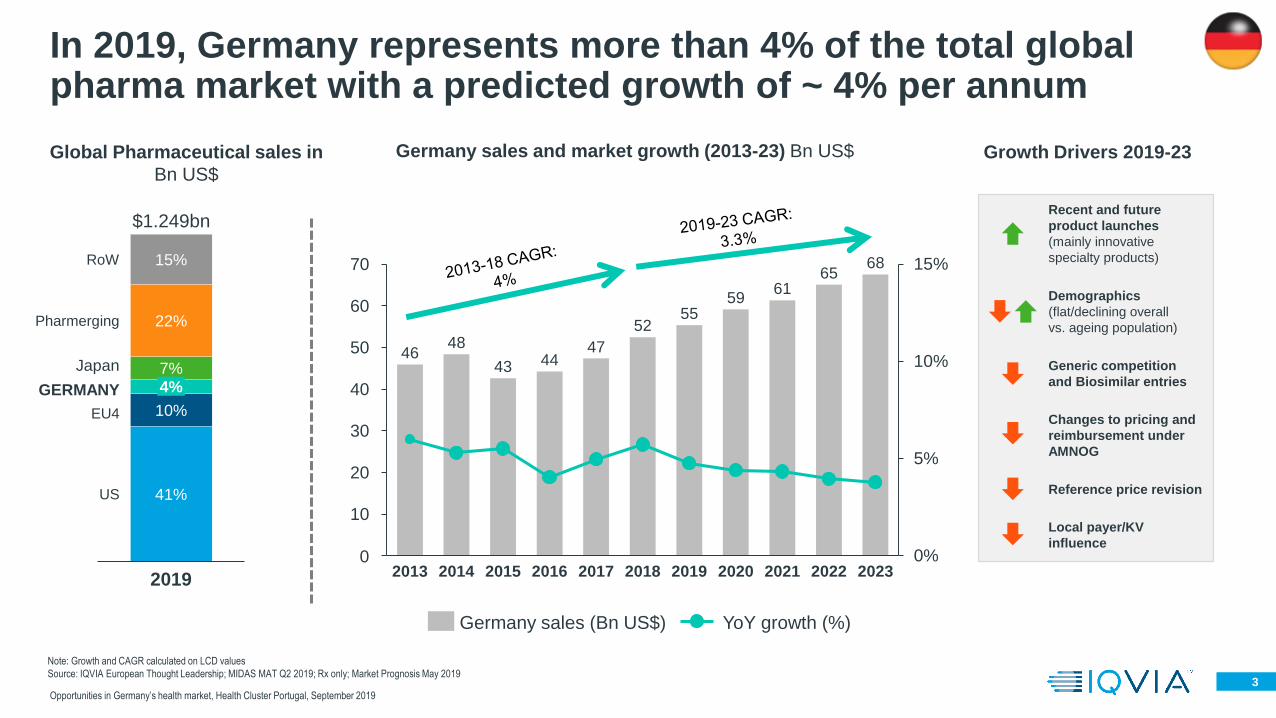

Germany sales and market growth (2013-23) Bn US$Global Pharmaceutical sales in

Bn US$

Germany sales (Bn US$) YoY growth (%)

In 2019, Germany represents more than 4% of the total global pharma market with a predicted growth of ~ 4% per annum

Growth Drivers 2019-23

Recent and future

product launches

(mainly innovative

specialty products)

Generic competition

and Biosimilar entries

Changes to pricing and

reimbursement under

AMNOG

Reference price revision

Demographics

(flat/declining overall

vs. ageing population)

Opportunities in Germany’s health market, Health Cluster Portugal, September 2019

Note: Growth and CAGR calculated on LCD values

Source: IQVIA European Thought Leadership; MIDAS MAT Q2 2019; Rx only; Market Prognosis May 2019

Local payer/KV

influence

4%7%

15%

22%

10%

41%

2019

RoW

Pharmerging

Japan

GERMANY

EU4

US

$1.249bn

4Opportunities in Germany’s health market, Health Cluster Portugal, September 2019

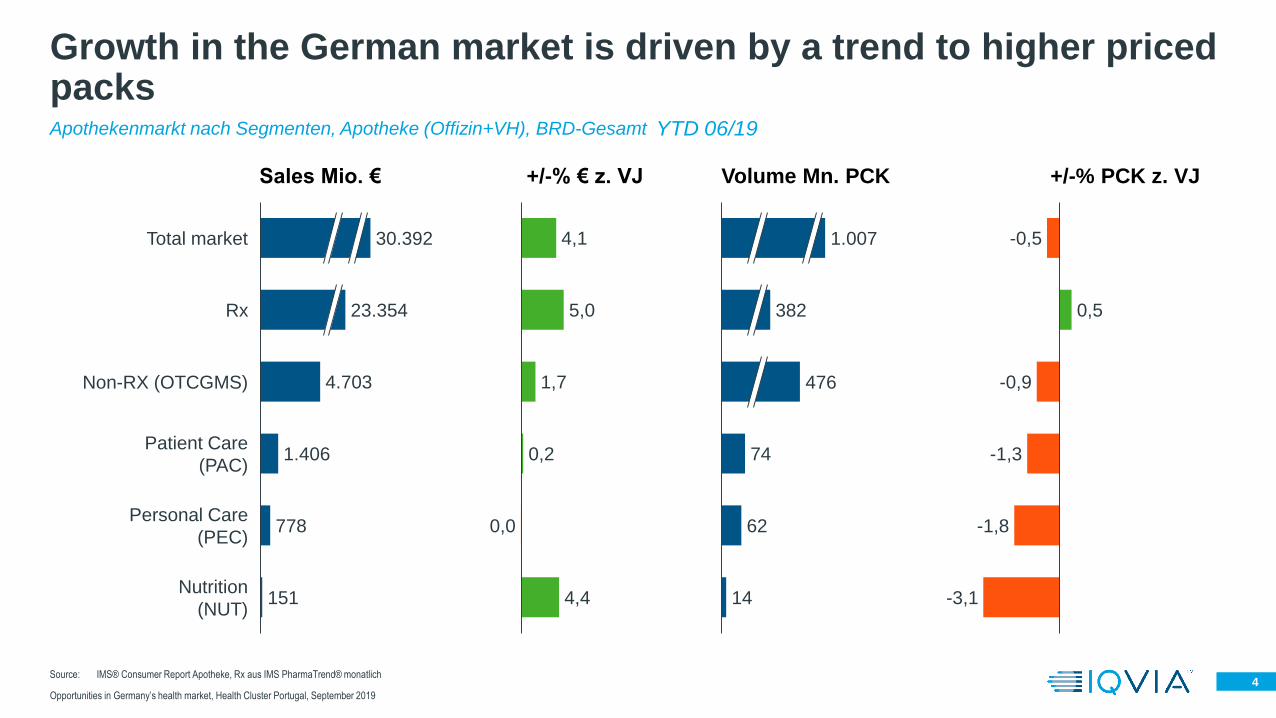

Apothekenmarkt nach Segmenten, Apotheke (Offizin+VH), BRD-Gesamt

+/-% € z. VJ

4.703

1.406

778

151

Patient Care

(PAC)

Total market

Rx

Non-RX (OTCGMS)

Personal Care

(PEC)

Nutrition

(NUT)

30.392

23.354

4,1

5,0

1,7

0,2

0,0

4,4

74

62

14

476

1.007

382

-0,5

0,5

-0,9

-1,3

-1,8

-3,1

+/-% PCK z. VJSales Mio. € Volume Mn. PCK

YTD 06/19

Growth in the German market is driven by a trend to higher priced packs

Source: IMS® Consumer Report Apotheke, Rx aus IMS PharmaTrend® monatlich

5Opportunities in Germany’s health market, Health Cluster Portugal, September 2019

Hospital and Retail sale is driving the German market growth, volume remains stable

Source: IMS Dataview® Pharmaceutical Consumption (AMV) Database: Clinic data from IMS® Hospital Index (DKM®), sales in Euro at valued hospital prices, sales in counting units; IMS PharmaScope® National, sales in Euro at the selling price of the pharmaceutical company (ApU=refund amount for AMNOG products and list price for other products) without consideration of discounts and savings from discount agreements, sales in counting units, consideration of preparations, pharmacy sales including vaccines

+10,8 %

43,9 Bn. Euro 97,7 Bn. SU

+5,7 % +1,2 %

86%Retail

14%Hospital

91%Retail

9%Hospital +0,03 %

+4,9%+1,3%

Sales Volume Sales Volume

22,5 Bn. Euro 28,8 Bn. SU

+5,2 % -0,2 %

86%

14%

Retail

Hospital

92%

8%

Retail

Hospital

2018

7,1 %+0,4 %

+4,9 %-0,3 %

H1 / 2019

6Opportunities in Germany’s health market, Health Cluster Portugal, September 2019

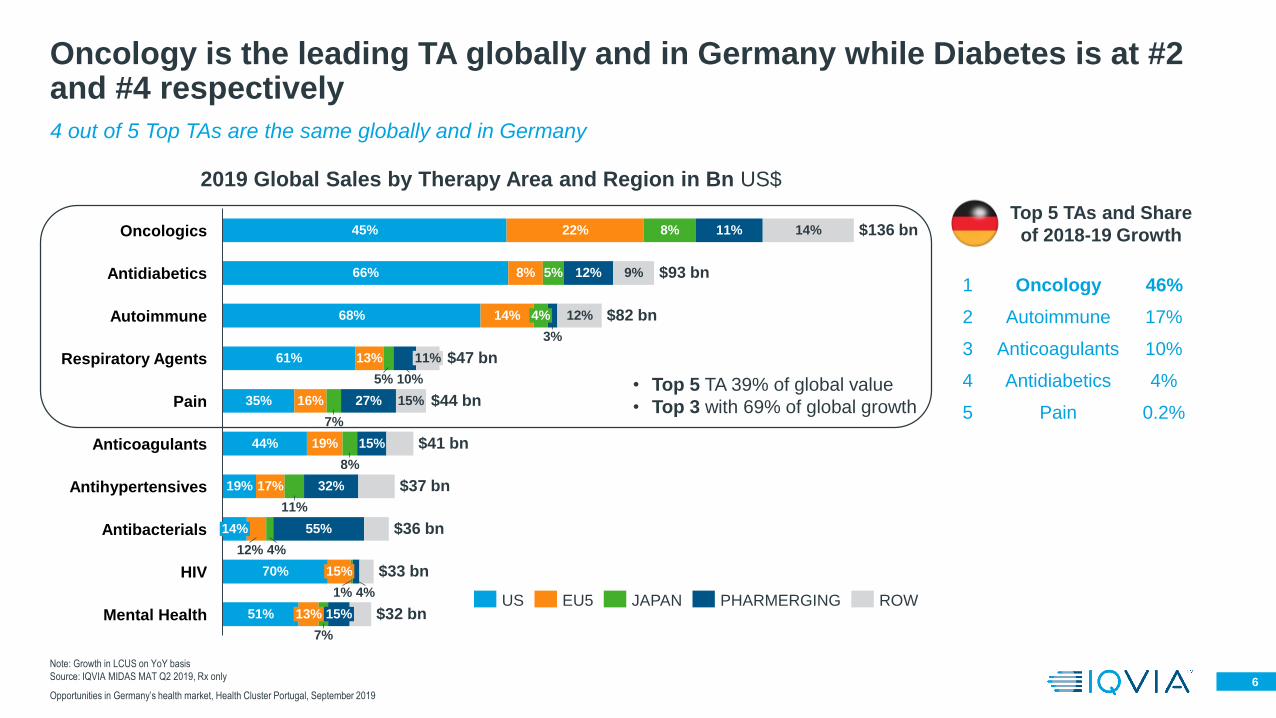

4 out of 5 Top TAs are the same globally and in Germany

Oncology is the leading TA globally and in Germany while Diabetes is at #2 and #4 respectively

51%

14%

$47 bn

19%

8%

15%

22%

5%

Oncologics

5%8%

$44 bn

66%

68%

Antidiabetics

17%

12%

10%

14%

3%

4%14%

55%

Autoimmune

13% 11%

11%

35%

9%

Pain

12%

61%Respiratory Agents

7%

70%

15%27%

15%

8%

19%44%Anticoagulants

32%

11%

Antihypertensives

12%

16%

7%

45%

Antibacterials

4%1%

HIV

15%13%

4%

$136 bn

$93 bn

$82 bn

$41 bn

$37 bn

$36 bn

$33 bn

$32 bnMental Health

2019 Global Sales by Therapy Area and Region in Bn US$

Note: Growth in LCUS on YoY basis

Source: IQVIA MIDAS MAT Q2 2019, Rx only

US ROWEU5 JAPAN PHARMERGING

• Top 5 TA 39% of global value

• Top 3 with 69% of global growth

Top 5 TAs and Share

of 2018-19 Growth

1 Oncology 46%

2 Autoimmune 17%

3 Anticoagulants 10%

4 Antidiabetics 4%

5 Pain 0.2%

7Opportunities in Germany’s health market, Health Cluster Portugal, September 2019

L01G MAB ANTINEOPLASTICS21%

B01F DIRECT FACTOR XA INHIBITOR16%

L01H PROTEINKIN.HEMM.A.NEOPL.12%

L01X OTHER ANTINEOPLASTICS10%L04C INTERLEUKIN INHIBITORS

17%

M01C ANTI-INFLAMMATORY DRUGS, SPECIFIC

10%

R07X OTHER PREPARATIONS OF THE RESPIR. SYSTEMS

9%

ÜBRIGE5%

Half of the additional SHI expenditures for drugs in the first half of 2019 are attributable to various cancer therapeutics

In the first half of 2019, the statutory health insurance funds spent an additional 712 million euros* on drugs.

In total, around half of the additional expenditure (MAB antineoplastics, protein kinase inhibitors, antineoplastics) is attributable to various

innovative oncological drugs.

The group of interleukin inhibitors contributes 10 % to the increase in expenditure. The preparations are used for the targeted therapy of

autoimmune diseases. These include, for example, severe forms of rheumatic diseases or psoriasis. Innovative therapies for the

treatment of the hereditary disease cystic fibrosis (mucoviscidosis) contribute a further 9 % to growth.

Source: IMS PharmaScope® Polo, Basis: *Turnover in euro at pharmacy retail price (AVP) less compulsory discounts to be paid by manufacturers and pharmacies, less reported discounts from reimbursement amounts in accordance with §130 SGB V; without savings from discount agreements; sales in packaging units; without vaccine

+712Mn. Euro*

German 2018 Oncology Market

Rank Company Share

1 Roche 19%

2 BMS/Celgene 16%

3 Novartis 12%

4 J&J 11%

5 Pfizer 5%

8Opportunities in Germany’s health market, Health Cluster Portugal, September 2019

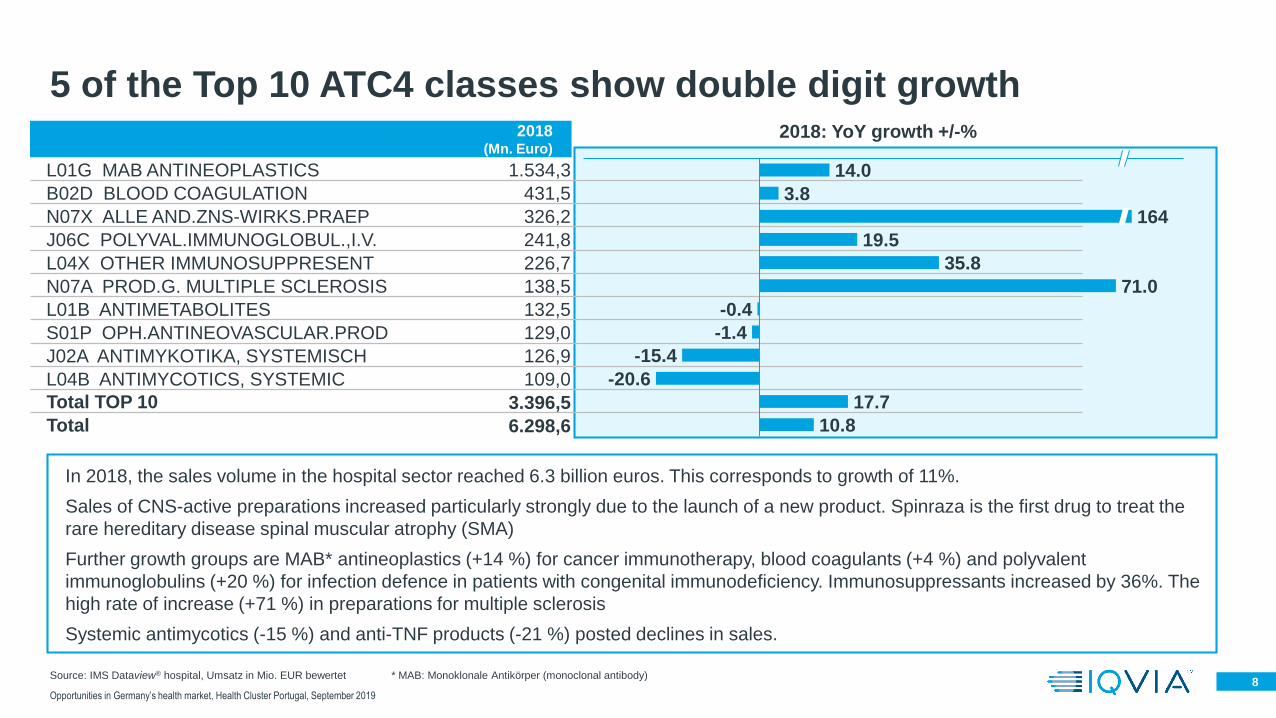

2018(Mn. Euro)

L01G MAB ANTINEOPLASTICS 1.534,3

B02D BLOOD COAGULATION 431,5

N07X ALLE AND.ZNS-WIRKS.PRAEP 326,2

J06C POLYVAL.IMMUNOGLOBUL.,I.V. 241,8

L04X OTHER IMMUNOSUPPRESENT 226,7

N07A PROD.G. MULTIPLE SCLEROSIS 138,5

L01B ANTIMETABOLITES 132,5

S01P OPH.ANTINEOVASCULAR.PROD 129,0

J02A ANTIMYKOTIKA, SYSTEMISCH 126,9

L04B ANTIMYCOTICS, SYSTEMIC 109,0

Total TOP 10 3.396,5

Total 6.298,6

14.0

-15.4

-0.4

164

35.8

3.8

19.5

10.8

71.0

-1.4

-20.6

17.7

In 2018, the sales volume in the hospital sector reached 6.3 billion euros. This corresponds to growth of 11%.

Sales of CNS-active preparations increased particularly strongly due to the launch of a new product. Spinraza is the first drug to treat the

rare hereditary disease spinal muscular atrophy (SMA)

Further growth groups are MAB* antineoplastics (+14 %) for cancer immunotherapy, blood coagulants (+4 %) and polyvalent

immunoglobulins (+20 %) for infection defence in patients with congenital immunodeficiency. Immunosuppressants increased by 36%. The

high rate of increase (+71 %) in preparations for multiple sclerosis

Systemic antimycotics (-15 %) and anti-TNF products (-21 %) posted declines in sales.

5 of the Top 10 ATC4 classes show double digit growth2018: YoY growth +/-%

Source: IMS Dataview® hospital, Umsatz in Mio. EUR bewertet * MAB: Monoklonale Antikörper (monoclonal antibody)

9® 2019 IQVIA Commercial – Health Cluster Portugal, Sep. 2019

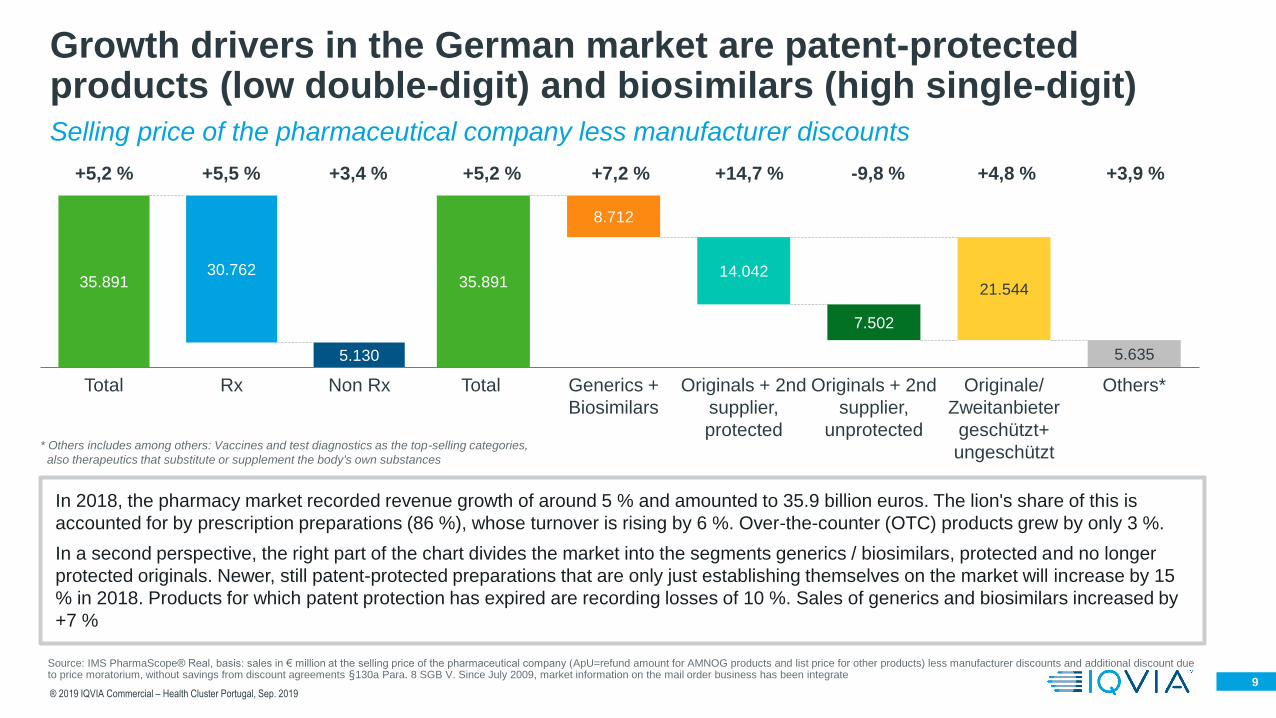

In 2018, the pharmacy market recorded revenue growth of around 5 % and amounted to 35.9 billion euros. The lion's share of this is

accounted for by prescription preparations (86 %), whose turnover is rising by 6 %. Over-the-counter (OTC) products grew by only 3 %.

In a second perspective, the right part of the chart divides the market into the segments generics / biosimilars, protected and no longer

protected originals. Newer, still patent-protected preparations that are only just establishing themselves on the market will increase by 15

% in 2018. Products for which patent protection has expired are recording losses of 10 %. Sales of generics and biosimilars increased by

+7 %

* Others includes among others: Vaccines and test diagnostics as the top-selling categories,

also therapeutics that substitute or supplement the body's own substances

Selling price of the pharmaceutical company less manufacturer discounts

Growth drivers in the German market are patent-protected products (low double-digit) and biosimilars (high single-digit)

Source: IMS PharmaScope® Real, basis: sales in € million at the selling price of the pharmaceutical company (ApU=refund amount for AMNOG products and list price for other products) less manufacturer discounts and additional discount due to price moratorium, without savings from discount agreements §130a Para. 8 SGB V. Since July 2009, market information on the mail order business has been integrate

Originals + 2nd

supplier,

protected

Total

35.891

7.502

Generics +

Biosimilars

8.712

Originals + 2nd

supplier,

unprotected

Originale/

Zweitanbieter

geschützt+

ungeschützt

14.04221.544

5.635

Others*Non Rx

35.891

RxTotal

30.762

5.130

+5,2 % +5,5 % +3,4 % +5,2 % +7,2 % +14,7 % -9,8 % +4,8 % +3,9 %

10

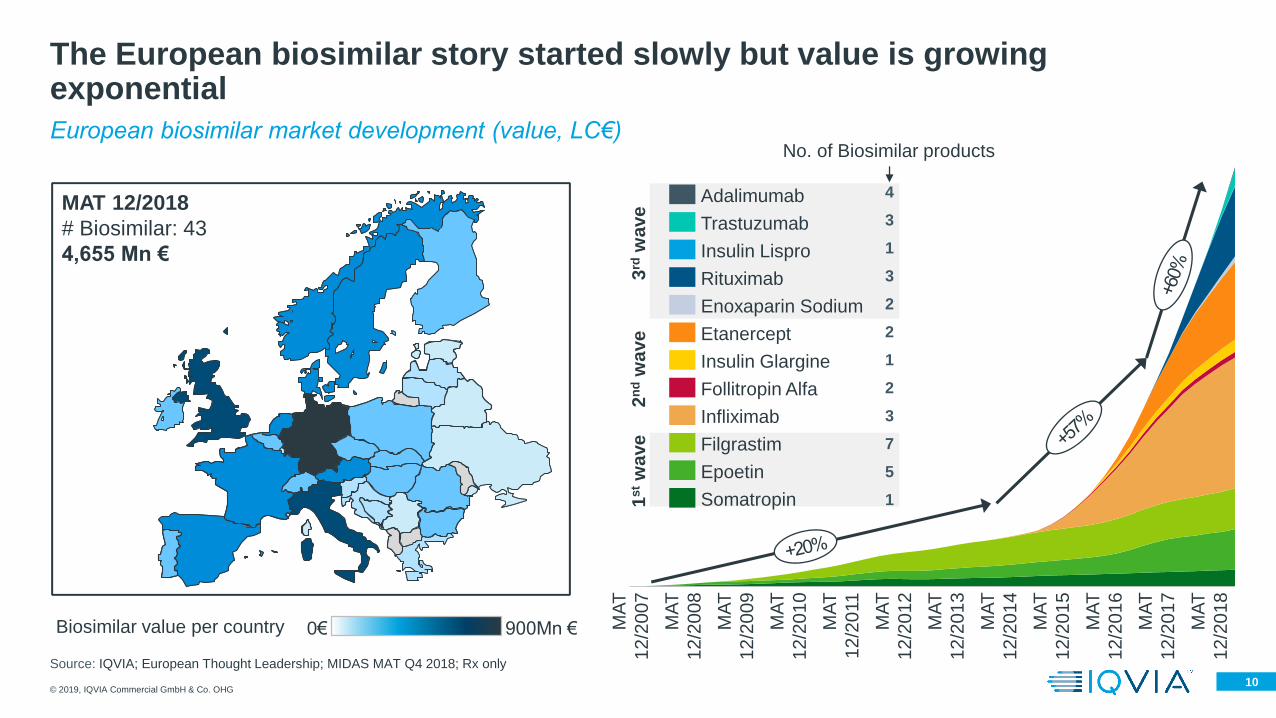

European biosimilar market development (value, LC€)

The European biosimilar story started slowly but value is growing exponential

Enoxaparin Sodium

Adalimumab

Insulin Lispro

Trastuzumab

Epoetin

Rituximab

Etanercept

Filgrastim

Infliximab

Insulin Glargine

Follitropin Alfa

Somatropin

© 2019, IQVIA Commercial GmbH & Co. OHG

900Mn €0€Biosimilar value per country1

stw

ave

2n

dw

ave

3rd

waveMAT 6/2007

# Bs: 1

1 Mn €

MAT 6/2008

# Bs: 6

18 Mn €

MAT 6/2009

# Bs: 10

66 Mn €

MAT 6/2010

# Bs: 11

146 Mn €

MAT 6/2011

# Bs: 12

237 Mn €

MAT 6/2012

# Bs: 12

344 Mn €

MAT 6/2013

# Bs: 12

426 Mn €

MAT 6/2014

# Bs: 15

521 Mn €

MAT 6/2015

# Bs: 18

682 Mn €

MAT 6/2016

# Bs: 20

1,162 Mn €

MAT 6/2017

# Bs: 24

1,998 Mn €

MAT 6/2018

# Bs: 33

3,206 Mn €

Source: IQVIA; European Thought Leadership; MIDAS MAT Q4 2018; Rx only

MA

T

12

/20

13

MA

T

12

/20

11

MA

T

12

/20

10

MA

T

12

/20

07

MA

T

12

/20

08

MA

T

12

/20

09

MA

T

12

/20

12

MA

T

12

/20

14

MA

T

12

/20

15

MA

T

12

/20

16

MA

T

12

/20

17

MA

T

12

/20

18

MAT 12/2018

# Biosimilar: 43

4,655 Mn €

4

3

1

3

2

3

7

5

1

2

1

2

No. of Biosimilar products

11® 2019 IQVIA Commercial – Pharma Trends 2019

Large Pharma under pressure – What does it mean for Germany?

• Lower growth, less favorable operating margins

• Rising R&D and pipeline cost

• Higher commercial complexity for novel therapies

• Rising price pressure in key markets

Conclusions

• Germany remains a must win market

• Often launching into new and small but

highly competitive therapy segments

• With complexity around right pricing,

reimbursement, positioning and even

delivery to patients

• Having more limited launch budgets…

• … still facing high expectations from HQ

Source: IQVIA

12

Key events and trends

With digital progress,

RWE expands

at two ends

Primary care rises from

the ashes

Digitally supported

promotion reaches a

tipping point

Substantial biosimilar

savings impact

Pharma under pressure

to manage costs

(R&D, …)

Cell/gene therapies

search for the right

commercial model

Source: IQVIA Thought Leadership

13

Opportunities in the German market

14

DEMONSTRATING

VALUE

UNLOCKING

DIGITALNEW CHANNEL

STRATEGIES

Continued increase in cost

containment measures are driving

a need to work with public policy

makers and payers to enhance

product value propositions

beyond simple price cuts

Technology adoption to existing

processes/systems continues, with

the focus shifting to innovative

coordinated approaches to

increase engagement across the

value chain via technology

A shift of service delivery and touch

points for customer interaction due to

policy focus and a strengthening

retail segment, gives rise to change

in channel strategy

Source: IQVIA research & analysis © 2019, IQVIA Commercial GmbH & Co. OHG. All rights reserved

We see three potential starting points for growth supportive actions in Rx, medical devices and OTC markets

15

Real World Data are increasingly important and currently expanding at two ends: 2. Patient/Consumer

® 2019 IQVIA Commercial – Pharma Trends 2019

Lab/biomarkerdata

Genomicsdata

Patient apps

Wearables/devices

Real-World Data

PayerClaims

Medicalrecords

PatientRegistries

HospitalEHRs

Pharmacydata

High science Patient

Increasing volume of

individual body

composition data

Increasing volume of

patient-generated

data

Source: IQVIA

16

Novel strategies to boost maturing brands and to launch innovations successfully are needed

Opportunities in Germany’s health market, Health Cluster Portugal, September 2019

Source: IQVIA European Thought Leadership White Paper “Rising from the Ashes; Primary Care is Alive and Well” 2018

17

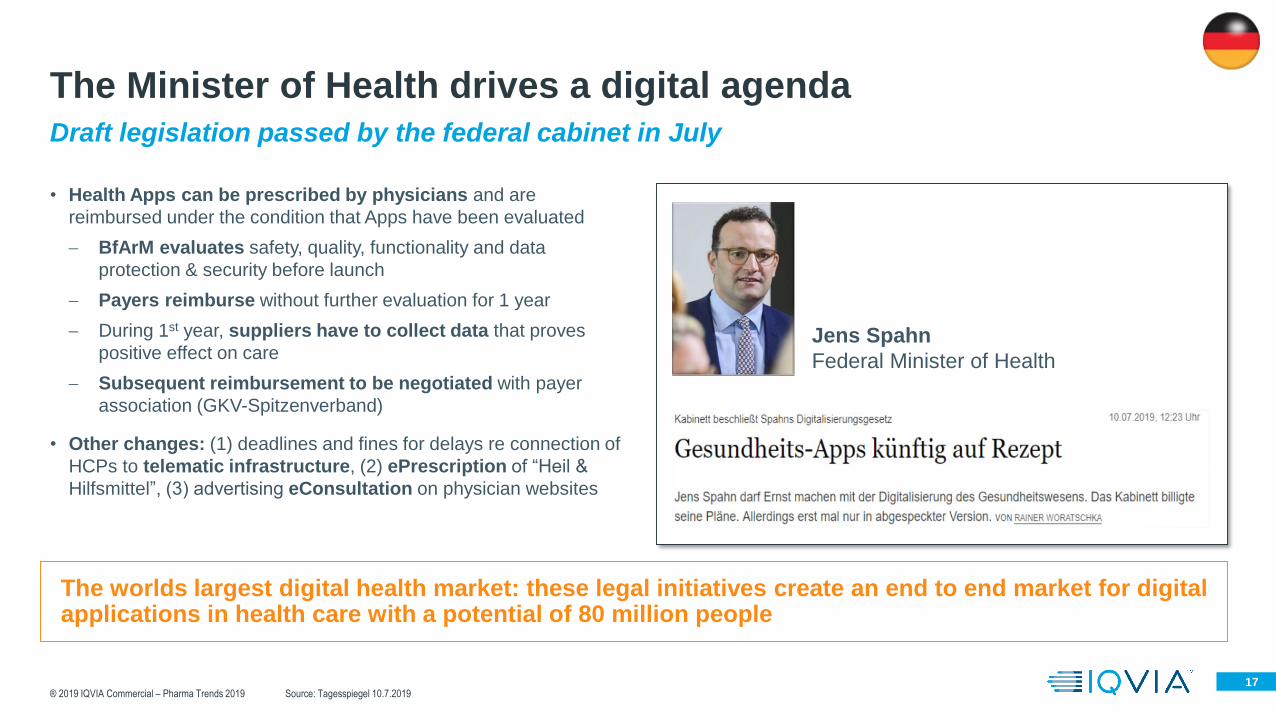

Draft legislation passed by the federal cabinet in July

The Minister of Health drives a digital agenda

• Health Apps can be prescribed by physicians and are

reimbursed under the condition that Apps have been evaluated

− BfArM evaluates safety, quality, functionality and data

protection & security before launch

− Payers reimburse without further evaluation for 1 year

− During 1st year, suppliers have to collect data that proves

positive effect on care

− Subsequent reimbursement to be negotiated with payer

association (GKV-Spitzenverband)

• Other changes: (1) deadlines and fines for delays re connection of

HCPs to telematic infrastructure, (2) ePrescription of “Heil &

Hilfsmittel”, (3) advertising eConsultation on physician websites

® 2019 IQVIA Commercial – Pharma Trends 2019

The worlds largest digital health market: these legal initiatives create an end to end market for digital applications in health care with a potential of 80 million people

Source: Tagesspiegel 10.7.2019

Jens Spahn

Federal Minister of Health

18

Payers have already moved forward supporting health apps

Opportunities in Germany’s health market, Health Cluster Portugal, September 2019

SHI-reimbursed app: “Online therapeutic” Selfapy

• Offers online therapy courses and personal coaching for various

diseases (depression, eating disorders, anxiety, chronic pain,…)

• Bridging waiting time for a therapy slot

• Proven clinical effectiveness

• Data gathering since 2016 to develop personalized treatment algorithm

ADA claims

• Artificial Intelligence, based on database with thousands of medical

cases from >100 physicians, plus information from studies & literature

• "Ada" knows several thousand diseases and symptoms

• 30,000 new cases per day added by users of the Ada app

• University of Essen and Giessen/Marburg intend to study whether

"Ada" can be used for better patient control in emergency departments

Source: IQVIA; TK https://www.tk.de/presse/mediathek/kuenstliche-intelligenz-fuer-eine-bessere-versorgung-2051404;

https://www.selfapy.de/?gclid=EAIaIQobChMIxKLR1d6k4AIVkNdkCh1hugc7EAAYASAAEgIj1vD_BwE#

Ada partners with TK: In 2019 patients can check

symptoms based on Artificial Intelligence via TK-Doc-App

19® 2019 IQVIA Commercial – BAH Mitgliederversammlung Sep. 2019

Sales teams can

optimize the impact of

multi-channel

promotional

investments by

analyzing the response

rates from past

campaigns. They can

focus on the right

healthcare professional

(HCP), segmenting them

into the right channel at

the right time

AI and ML transform the sales and marketing process – Pharma companies exploring new partnerships

Identify highly-

specific patient

populations

Customize digital

engagement

Predictive analytics can

provide insight into

prescribing patterns for

precision medicine

candidates through

patient genomics and

biological data. The

technology can identify

which patients should

start treatment. This

helps sales teams to

accurately target the

most relevant physicians

AI & ML powered digital

engagement solutions

can optimize channel

effectiveness,

recommending the

timing, frequency, and

content of email

messages. This

targeted approach at the

individual HCP level

reduces physician churn

rates and maximizes the

impact of digital

campaigns

Many drugs have

multiple indications and

are distributed through

multiple channels. AI &

ML-powered analytics

can paint a clearer

picture of how multi-

indication products are

used. Teams can track

product performance by

indication, specialty,

region and source of

business to inform their

future marketing efforts

Local retail pharmacy

sales analytics can

deliver precise targeting

lists highlighting

individual pharmacy

sales potential and

behavioral profiles that

prioritize marketing

and inform strategies

— i.e. offer discounts in

price-conscious markets

versus value-add

opportunities in high

sales shops

Multichannel

optimization

Leverage multi-

indication analyticsEnhance HCP

profiling,

segmentation and

targeting

Source: IQVIA European Thought Leadership, White Paper: Using AI & Machine Learning to Drive Commercial Success in the EU March 29, 2019

20

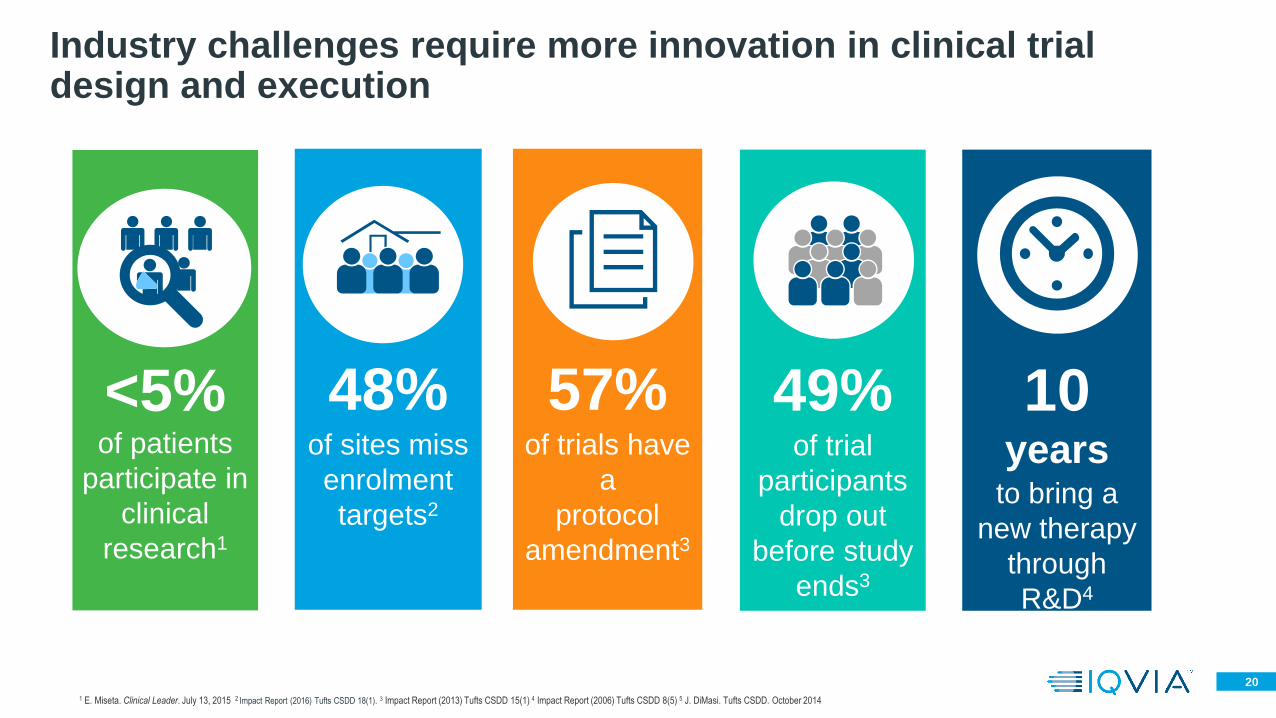

Industry challenges require more innovation in clinical trial design and execution

1 E. Miseta. Clinical Leader. July 13, 2015 2 Impact Report (2016) Tufts CSDD 18(1). 3 Impact Report (2013) Tufts CSDD 15(1) 4 Impact Report (2006) Tufts CSDD 8(5) 5 J. DiMasi. Tufts CSDD. October 2014

48%of sites miss

enrolment

targets2

49%of trial

participants

drop out

before study

ends3

10years

to bring a

new therapy

through

R&D4

<5%of patients

participate in

clinical

research1

57%of trials have

a

protocol

amendment3

21Opportunities in Germany’s health market, Health Cluster Portugal, September 2019

Germany scores favourable for conducting clinical trials, but cost are relatively high

• Size of market/ eligible

patients in region

• Speed of MoH*/Ethics

approvals

• Government financial/

tax incentives

• Cost of running trials in

relevant market

• Disease management

system/ networks

Investigator

drivenHospital

Environment

drivenCost

Source: IQVIA European Thought Leadership,; Marta Gehring et al. BMJ Open 2013;3:e002957, 2013 by British Medical Journal Publishing Group; appliedclinicaltrialsonline.com/selecting-study-appropriate-clinical-sites-3-steps; rcri-inc.com/clinical-trial-

site-selection-best-practices/;

• Investigator interest

• Previous experience in

similar studies

• Concurrent trial

workload

• Recruitment and

retention track record in

prior trials

• Publication track record

• Site personnel study

experience and training

• Site personnel

language capabilities

• Facilities (lab, imaging)

• Hospital quality

assurance process

• Hospital institutional

approval system/

contracts

• Cost of running a trial

in the relevant market

for phase II

• Cost of running a trial

in the relevant market

for phase III

• Germany and

Switzerland have the

highest cost in Europe

*MoH= Ministry of Health

22

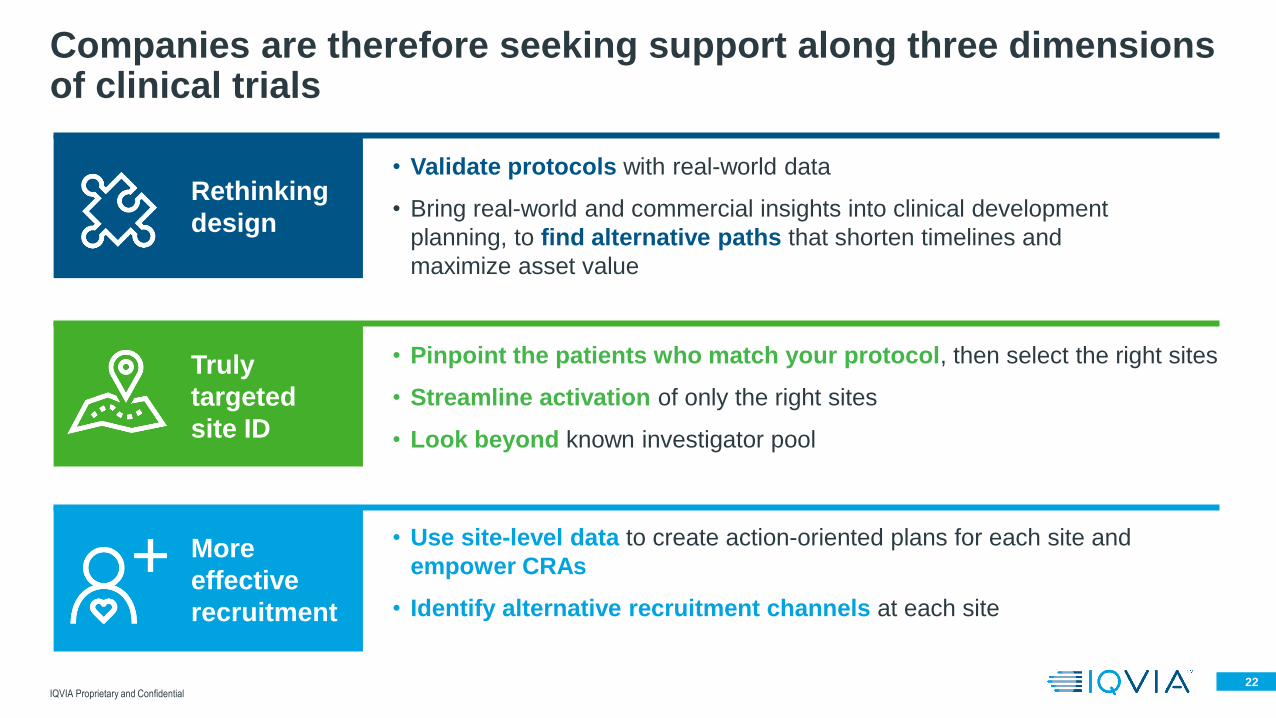

Companies are therefore seeking support along three dimensions of clinical trials

IQVIA Proprietary and Confidential

• Validate protocols with real-world data

• Bring real-world and commercial insights into clinical development

planning, to find alternative paths that shorten timelines and

maximize asset value

• Pinpoint the patients who match your protocol, then select the right sites

• Streamline activation of only the right sites

• Look beyond known investigator pool

• Use site-level data to create action-oriented plans for each site and

empower CRAs

• Identify alternative recruitment channels at each site

Rethinking

design

More

effective

recruitment

Truly

targeted

site ID

23IQVIA Confidential. Not approved by management For internal use only.

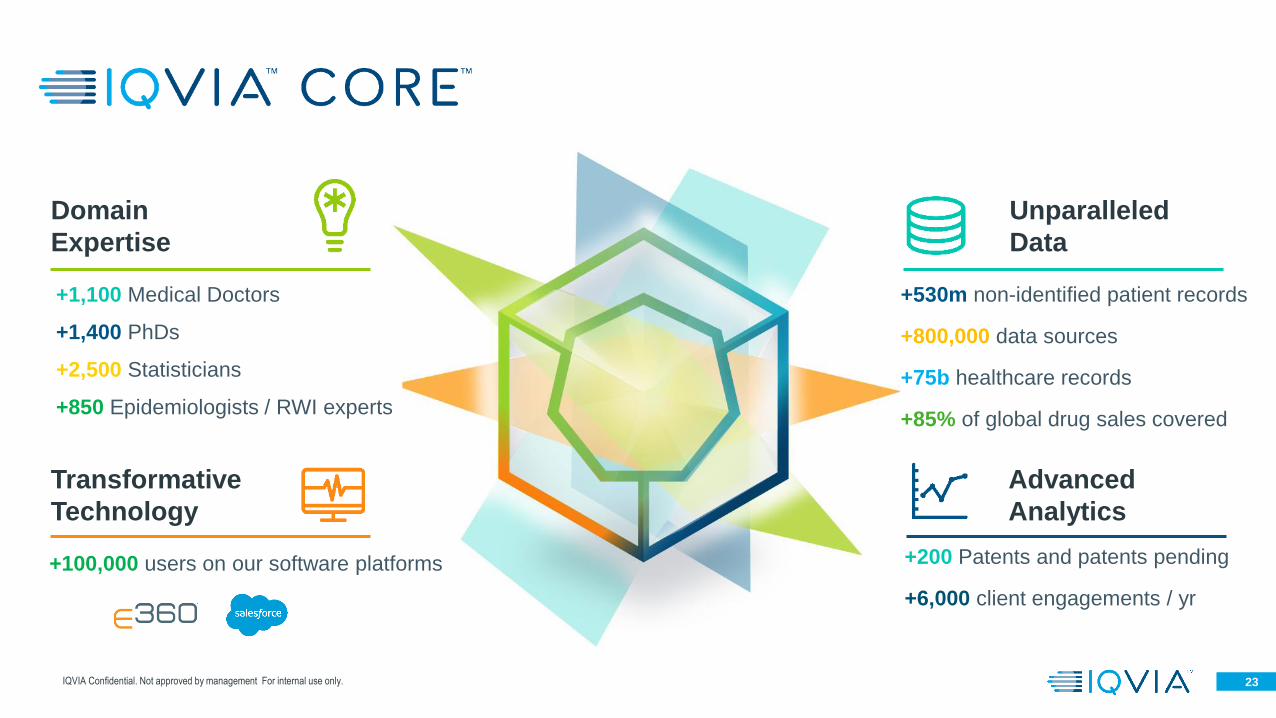

Domain

Expertise

Transformative

Technology

Unparalleled

Data

Advanced

Analytics

+530m non-identified patient records

+800,000 data sources

+75b healthcare records

+85% of global drug sales covered

+1,100 Medical Doctors

+1,400 PhDs

+2,500 Statisticians

+850 Epidemiologists / RWI experts

+200 Patents and patents pending

+6,000 client engagements / yr

+100,000 users on our software platforms

24

▪ Demog. change leads to an increasing need for treatment with parallel reduction of existing care provision structures

▪ Economical aspects cause a shift from individual practices to larger units and the establishment of chains

▪ The interdisciplinary cooperation progresses, driven by the advancing possibilities in telemedicine. The general

practitioner is assumed to have a leading role in the coordination of the care pathwayRetail

▪ Sustained consolidation to larger units and increasing specialization, aiming at improving profitability and care quality

▪ The trend towards privatization continues, combined with enhanced vertical integration in surrounding care provision

structures

▪ Stronger coordinating role in regional outpatient care provision requiredClinics

Others

▪ Entry of new investors into the healthcare market increases, but remains limited due to regulatory elements

▪ Introduction of Advanced Therapies results in significant market adjustments, e.g. healthcare infrastructure

▪ Increasing relevance of data-based evidence, e.g. on the efficacy of new therapies, leads to additional requirements for

the collection and processing of data from health care research and to new stakeholders

Sector Outlook

Current market trends amplify cross-sectorally until 2025

Opportunities in Germany’s health market, Health Cluster Portugal, September 2019

For further information, contact

Dr. Frank Wartenberg

President Central Europe

+49 (0) 69 6604-0

@ FrankWartenberg

© 2019, IQVIA Commercial GmbH & Co. OHG

All rights reserved. The information may not be duplicated, stored, further processed, nor be made accessible in whole or in part to any third

party without the prior express written consent of IQVIA. IQVIA employs high sophisticated technologies and methods which ensure all its

Information Services to meet the applicable data-protection requirements, regardless the way data are combined with one another.