opportunities in the oilfield services markets in malaysia and indonesia

TRANSCRIPT

Opportunities in the Oilfield Services Markets in Malaysia and Indonesia

Subbu Bettadapura

Director, Energy & Power Systems

Asia Pacific

2

Competition Overview

The Upstream Industry Value Chain

Table of Contents

Upstream Industry Overview - Malaysia

Market Potential

1

2

3

4

2

MALAYSIA

INDONESIA

5

Upstream Industry Overview - Indonesia

3

1 Upstream Industry Value Chain

3

Value Chain

Source: Frost & Sullivan analysis.

Products

Exploration Phase Production Phase

Crude oil and Condensate

Natural Gas

Development Phase

Abandonment Phase

The upstream O&G industry is involved in the exploration and production (extraction) of oil or gas from onshore or offshore oil or gas fields. The key activities include exploration for O&G, appraisal of the O&G field, development, production, operations and maintenance, and then abandonment.

Greenfield Services Brownfield Services

Upstream Sector Value Chain

4

1 Upstream Industry Value Chain

4

Activities

Exploration Phase Production Phase

• Seismic activities• Drilling services• Marine support

• Engineering and project management

• Operations and maintenance services Field review and optimization

• Retrofit work• Hook-up and

Commissioning• Fabrication of structures• Structural maintenance

and upgrade• Equipment maintenance

and upgrade• Marine support

Development Phase

Abandonment Phase

Greenfield Services Brownfield Services

• Hook-up and commissioning

• Drilling services• Construction

and fabrication of structures

• Marine support

• Well plugging• Dismantling of

structures• Decommissioning

machinery and equipment

• Marine support

Activities in the Upstream Sector Value Chain

5

1 Upstream Industry Value Chain

5

Market Segmentation

Exploration Phase Production PhaseDevelopment

PhaseAbandonment

Phase

Greenfield Services Brown Field Services

Marine Support Services Market

Brown Field Services Market

6

Malaysia - Upstream Industry OverviewGrowing Complexity of Malaysia’s Reserves

Source: PETRONAS

• Malaysia’s total reserves,(2010) ~ 20.56 bboe

• Deepwater potential for oil & gas reserves is estimated to be 10bboe

• Growing Complexity in extracting Malaysia’s reserves

• Malaysia’s deepwater presents unique challenges such as complicated sea-bed relief with slope and stability issues

• Shallow hazards • Hydrate management• High CO2 content in gas

• Reserves estimate increase due to• Additions from new discoveries• Revised estimates due to EOR

2

• In Malaysia, deepwater definition ranges from depth of 200m to 1200m. Beyond 1200 meters is considered as Ultra deepwater

• Generally accepted deepwater definition - greater than 300 metres depth up to 1500 meters; Ultra deepwater - greater than 1500 meters depth

6

0.00

5.00

10.00

15.00

20.00

25.00

2005 2006 2007 2008 2009 2010

17.27 17.42 17.66 17.13 17.21 17.58

2.09 2.49 2.52 3.00 2.97 2.98

Reserves, bboeDW Reserves

SW Reserves

Deepwater Reserves, at ~ 3 bboe (2010), are 14.5% of total reserves

7

2

Increasing number of PSCs and International Companies Participation

Number of active PSCs: 82

•Currently there are 33 exploration, 15 development and 34 producing PSCs

20 international oil & gas exploration companies are present in Malaysia

16 of these operate oil & gas assets in Malaysia

Source: Petronas; Compiled by Frost & Sullivan

Malaysia - Upstream Industry Overview

7

8

Malaysia’s Upstream Expenditure – Increasing Trend

• Malaysia’s upstream expenditure has steadily increased over the years• The country’s upstream expenditure was 28.72 billion RM in FY 2010• Malaysia Upstream Expenditure, FY 2011 ~ RM 34 Billion

6.3 8.46

10 11 12.5

16.3

19.8 21.5 22.3

28.72

0

5

10

15

20

25

30

35

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

RM Billion

Year

Malaysia Upstream Expenditure, FY 2001 to FY 2010 Total number of producing fields: 106Oil : 68 Gas : 38

Oil and Gas Fields Discovered : 409Oil: 167; Gas: 242

Malaysia - Upstream Industry Overview2

Source: Petronas; Compiled by Frost & Sullivan 8

9

Deep Water is the Final Frontier – Its true for Malaysia too

Malaysia- Upstream Industry Overview

Increasing Depth

Malaysia is faced with the prospect of declining shallow water reserves – a phenomenon true for most countries (except a few OPEC and Russia)

Global Drivers for DW projects

•Decline in shallow water reserves•Strong growth in energy demand•Rising oil & gas prices•Long term sustainability•Technology now exists to tap oil at depths exceeding 3 km

Drivers specific to Malaysia

•Capability development & local participation•Goal to grow competency to be DW regional hub and global player

2010200620021983

Deep water projects more expensive and carry more risks

Oil price estimates for project to break even -•Shallow water: $40•Shallow water, marginal: $65•Deepwater: $ 80•Ultra deepwater: $80 to $100

2

9

10

2

Source: Compiled by Frost & Sullivan

Deepwater Fields Being Developed

Gumusut/Kakap (Block J & K)Development Stage

Recoverable: 620mboeDepth: 1,100m

Onstream: 2011/2012Operator: Shell

Malikai (Block G)Development Stage

Recoverable: 108mboeDepth: 480m

Onstream: 2012/2013Operator: Shell

KebabanganDevelopment StageRecoverable: 2.2tscf

Depth: >200mOnstream: 2012/2013

Operator: KPOC

Jangas (Block J)Pre-Development StageRecoverable: 81mmboe

Depth: >1000mOnstream: 2012/2013

Operator: Murphy

Ubah Crest (Block G)Pre-Development StageRecoverable: 215mmboe

Depth: >1000mOnstream: 2013/2014

Operator: Shell

Pisangan (Block J)Pre-Development StageRecoverable: 56mmboe

Depth: >1000mOnstream: 2013/2014

Operator: Shell

KamunsuPre-Development Stage

Recoverable: 2.2tscfDepth: >1000m

Onstream: 2014/2015Operator: KPOC

North Siakap – PetaiPre-Development Stage

Limbayong, Block GPre-Development Stage

Malaysia – Upstream Industry Overview

10

11

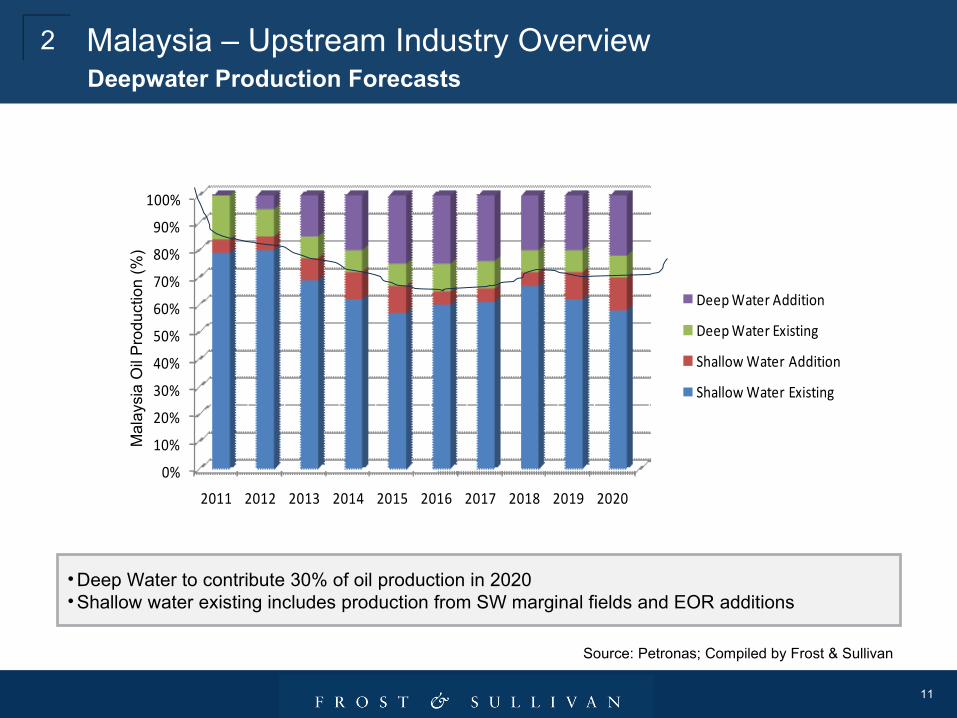

Deepwater Production Forecasts

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Deep Water Addition

Deep Water Existing

Shallow Water Addition

Shallow Water Existing

Mal

aysi

a O

il P

rodu

ctio

n (%

)

• Deep Water to contribute 30% of oil production in 2020• Shallow water existing includes production from SW marginal fields and EOR additions

2 Malaysia – Upstream Industry Overview

Source: Petronas; Compiled by Frost & Sullivan

11

12

Development Solutions for Malaysia Deepwater Projects

2

Malikai

North Siakap Petai

Gumusut Kakap

Kikeh Kebabangan

Sub-sea

TLP

Fixed PlatformSPAR

FPSO

FPSSabah Oil

& Gas Terminal

Malaysia – Upstream Industry Overview

12

13

Wells Drilling Forecast, Malaysia

2 Malaysia – Upstream Industry Overview

Forecast includes both shallow water and deepwater (Exploration, Appraisal and Development) Wells

•6 deep water fields (of the total wells forecast, 20% are in deepwater)•22 new Shallow Water Blocks•10 Marginal fields•6 fields identified for Enhanced Oil Recovery (EOR)

13

Source: Frost & Sullivan Estimates

0

10

20

30

40

50

60

70

80

90

2009 2010 2011 2012 2013 2014 2015

59 62 65 71 73 77 83 Wells Drilled

14

Upstream Expenditure

3 Indonesia - Upstream Industry Overview

14

• Indonesia’s upstream expenditure has increased steadily since 2001.The country’s upstream expenditure for FY 2011 is forecast to be $17.0 billion.

Upstream Expenditure, 2001-2010Indonesia

1.92.5 2.6 2.8

3.44.2

8.5

1210.8

13.2

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Year

Source: Frost & Sullivan analysis.

15

Oil Production and Consumption

3 Indonesia – Upstream Industry Overview

15

Oil Production & Consumption, Indonesia

Oil Exporter Turned Importer

•Increasing domestic demand•Falling domestic production

Remediation

•Brown fields to be rejuvenated•More exploration to improve reserves•Reduce demand

The demand for oil is expected to ease as natural gas increasingly substitutes oil in the power sector.

Approximately $10.0 billion is needed to halve the current oil consumption and replace it with gas.

16

Oil Production Outlook

3 Indonesia – Upstream Industry Overview

16

Oil Production Outlook, 2010-2015Indonesia

• To meet these two targets, E&P investments and good project management have become important

• Data acquisition techniques are necessary for new discoveries

Source: BP MIGAS

954

MBOPD – 1000 Barrels per Day

Actual(MBOPD)

920* 920*

• Oil production to decrease or at best stay at current levels in 2011 and 2012

• Forecast

Source: Frost & Sullivan analysis.

17

Natural Gas Production Outlook

3 Indonesia – Upstream Industry Overview

17

Natural Gas Production Outlook, 2010-2020Indonesia

Source: BP MIGAS, Frost & Sullivan analysis.

• If this potential is not realized, Indonesia is likely to be a net gas importer by 2021

Bringing projects onstream on time assumes importance if all contracted commitments and projected demand increase are to be met

18

Offshore Prospects

3 Indonesia – Upstream Industry Outlook

18

Source: Planning Dept, Govt of Indonesia; Petroleum Geo-Services; Frost & Sullivan analysis.

Offshore Potential, IndonesiaDeepwater Potential: Tarakan basin; Papalan Basin

Thrust from Government for faster development of gas projects for meeting domestic and export gas demand

East Kalimantan

Masela Block10 TCF Reserves; water

depth 300m to 1000mInpex to invest $ 4.9 billionfor floating LNG plant (2.5 mmtpa) with production

start-up in 2016

Makassar StraitGehem, Gendalo, Gandang, Maha and Bangka

fieldsChevron to develop East Kalimantan deepwater

fields, and Gehem and Gendalo projects.Investment $7.0-$8.0 billion.

Plan Of Development approved

Shallow Water Bukit Tua

Deep Water•Gehem•Gendalo

• INPEX Masela FLNG• Petramina FSRU

Prospective FPSO Projects

19

4 Competition OverviewKey Players

19

Note: Licensing is an essential pre-requisite to compete in this industry.

Key Players in Malaysia include SapurCrest Petroleum, Kencana, Petra Energy, Dialog Group, Bumi Armada, etcKey Players in Indonesia include Apexindo, Elnusa, Gearindo, PT Wintermar Offshore Marine, etc

TRENDDecreasing Stable Increasing

▼ ●● ▲

Competitor Overview , Oilfield Services Market: Malaysia & Indonesia

Source: Frost & Sullivan analysis.

20

5

Source: Compiled by Frost & Sullivan

Offshore Potential in the Asia Pacific Region; Offshore Prospects

KG Basin6.76 TCF

Offshore Sabah (10 TCF) & Sarawak (45

TCF) 4.2Bboe proven; 8Bboe potential

Gulf of Thailand

Arthit 1.9TCF

Bohai Bay 7.35 Bboe

Carnarvon 95.5 TCF

East Kalimantan 47 TCF

Makassar Strait6 TCF

Kikeh 700 mmboe

Masela 10 TCF

Phu Khanh Basin

2.48Bboe

Shwe Gas Field

8 TCF

Browse 30.3 TCF

M9 Field, Gulf of

Martaban 1.76 TCF

Bonaparte29.5 TCF

Gippsland10.65 TCF

• Asia Pacific – a significant deepwater region

Market Potential

20

21

5 Market PotentialMalaysia as the Oilfield Services Hub: Key Success Factors

Infrastructure

Government Policies

Location1

2

3

Cost Competitiveness4

21

22

Development of Labuan and Sabah Region as the Deep Water Services Hub

5

Labuan and Sabah region has the potential to be developed into a deep water services hub

Drivers for Development of Labuan and Sabah

Gumusut / Kakap, Malikai, Jangas, Ubah Crest, Pisangan and Kamunsu deep water fields are being developed

Sabah Oil and Gas Terminal (SOGT)

Development of logistics - MOU between Labuan Shipyard & Engineering (LSE) and Asian Supply Base (ASB)

Important to leverage the deepwater oil & gas reserves, operators, specialised equipment manufacturers, service providers and offshore engineering companies

Market Potential

22

23

Key Activities Kikeh Gumusut

Kakap

Malikai Kebabangan, North

Siakap–Petai, UbahCrest,

Pisangan, KemunsuEast

All future

deep water

projects

Subsurface

Studies/Field

Development Plan

Malaysia North America Malaysia Malaysia Malaysia

Engineering

•pre-FEED

•FEED

•Detail Design

Malaysia

North America

Europe

Malaysia

North America

Malaysia Malaysia Malaysia

Procurement Malaysia

North America

Europe

Malaysia

North America

Malaysia Malaysia Malaysia

Fabrication

•Topside

•Hull

•Subsea

Malaysia

Europe

Malaysia Malaysia Malaysia Malaysia

Petronas Aspires to Transfer Development and Operation Activities to Malaysia

5 Market Potential

23

Source: Petronas

24

5 Market PotentialEstimation of Market Potential: Malaysia

24

Source: Frost & Sullivan analysis.

Revenues ($

Million)

Y-o-Y %

Growth

Rate

2010 243.0 19.9%

2016 415.4 9.0%

Brownfield Services Market

Marine Support Services Market

Revenues

($ Million)

Y-o-Y %

Growth

Rate

2010 131.8 12.0%

2016 230.4 8.5%

This estimation assesses the outsourced component for Marine Support

(includes marine support for both greenfield and brownfield services)

The Market Size includes marine support assets such as:

Work Boat, Work Barge, Crew Boat, Utility Vessels (UV), Diving Support

Vessels, Platform Service Vessels (PSV), Anchor Handling Tug Supply

(AHTS)

This excludes FPSOs, Drill Ships, Semi-Subs and Jack-ups

This estimation assesses the outsourced component.

Includes brownfield services (including marine support services for

brownfields)

•Equipment Packaging & Supply

•Marine Support

•Retrofit

•Minor Structure Fabrication

•Operation & Maintenance

•Decommissioning Services

25

5 Market PotentialEstimation of Market Potential: Indonesia

25

Source: Frost & Sullivan analysis.

Revenues

($ Million)

Y-o-Y %

Growth

Rate

201

0585.4 18.5%

201

61707.8 19.2%

Brownfield Services Market

Marine Support Services Market

Revenues

($ Million)

Y-o-Y %

Growth

Rate

2010 317.3 17.5%

2016 910.5 16.5%

This estimation assesses the outsourced component for Marine Support

(includes marine support for both greenfield and brownfield services)

The Market Size includes marine support assets such as:

Work Boat, Work Barge, Crew Boat, Utility Vessels (UV), Diving Support

Vessels, Platform Service Vessels (PSV), Anchor Handling Tug Supply

(AHTS)

This excludes FPSOs, Drill Ships, Semi-Subs and Jack-ups

This estimation assesses the outsourced component.

Includes brownfield services (including marine support services for

brownfields)

•Equipment Packaging & Supply

•Marine Support

•Retrofit

•Minor Structure Fabrication

•Operation & Maintenance

•Decommissioning Services

26

http://twitter.com/frost_sullivan

Follow Frost & Sullivan on Facebook, LinkedIn, SlideShare, and Twitter

http://www.facebook.com/pages/Frost-Sullivan/249995031751?ref=ts

http://www.linkedin.com/companies/4506

http://www.slideshare.net/FrostandSullivan

27

For Additional Information

Donna JeremiahCorporate CommunicationsAsia Pacific+603 6204 [email protected]

Carrie LowCorporate CommunicationsAsia Pacific+603 6204 [email protected]

Subramanya BettadapuraDirectorEnergy & Power [email protected]

Dewi NurainiCorporate CommunicationsIndonesia+62 21 571 [email protected]