opportunity assessment for the u.s. flexible packaging ... · flexible packaging industry ......

TRANSCRIPT

1

SAI INDUSTRIAL LLC

OPPORTUNITY ASSESSMENT FOR THE U.S. FLEXIBLE PACKAGING INDUSTRY

A presentation to

FLEXIBLE PACKAGING ASSOCIATION

February 24, 2012

VISIT SAI’S WEBSITE FOR MORE INFORMATION

www.strategicanalysis.com

BELGIUM ● BRAZIL ● CHINA ● INDIA ● JAPAN ● RUSSIA ● SINGAPORE ● UNITED STATES

The purpose of the document is to share with the client SAI’s proposed format and preliminary findings to date. The format and information contained in the document is subject to change as SAI completes its field research and analysis. In addition, any outstanding deliverables and clerical errors will be addressed in the final report. SAI will issue the formal report upon project completion.

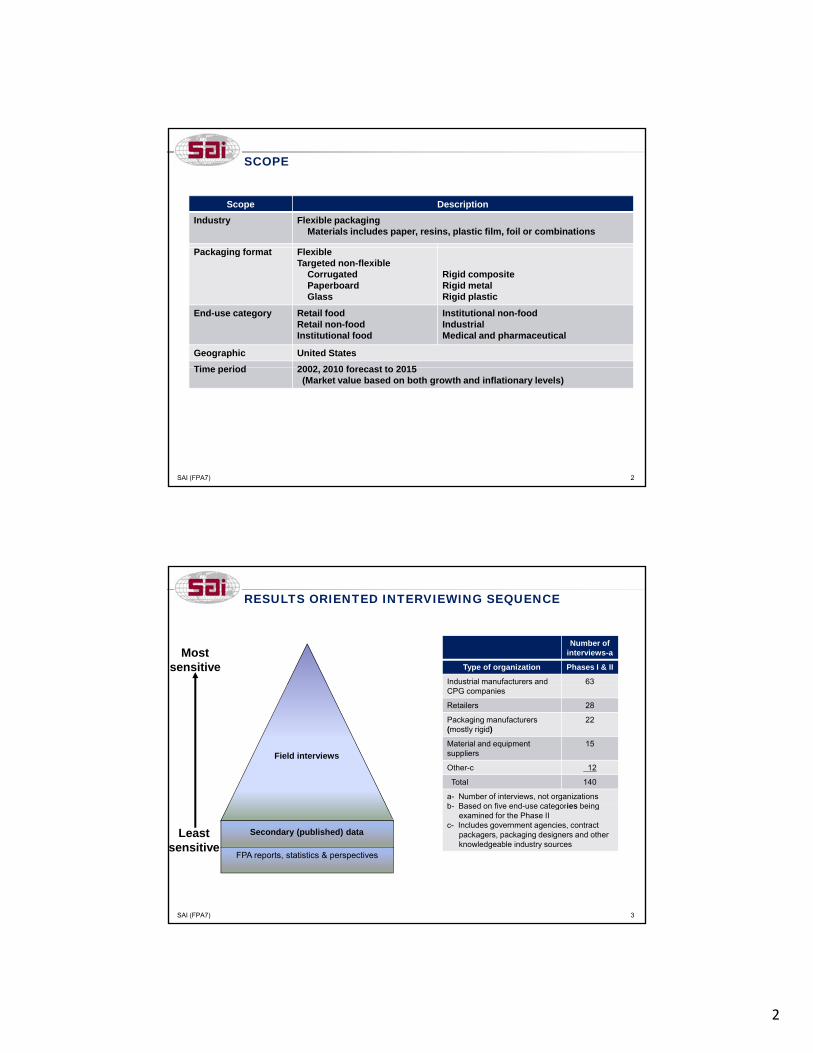

PROJECT OBJECTIVES

• Update information• Focus on trends that favor flexible• Look for low flexible penetration

Update previous research

• Cost• Materials• Equipment and capital• Market perceptions

Determine challenges

• Globalization• Sourcing strategies• Materials costsIdentify trends

SAI (FPA7) 1

• Sustainability

• Differences between flexible and rigid• Find opportunities• Identify threats

Profile

opportunities

2

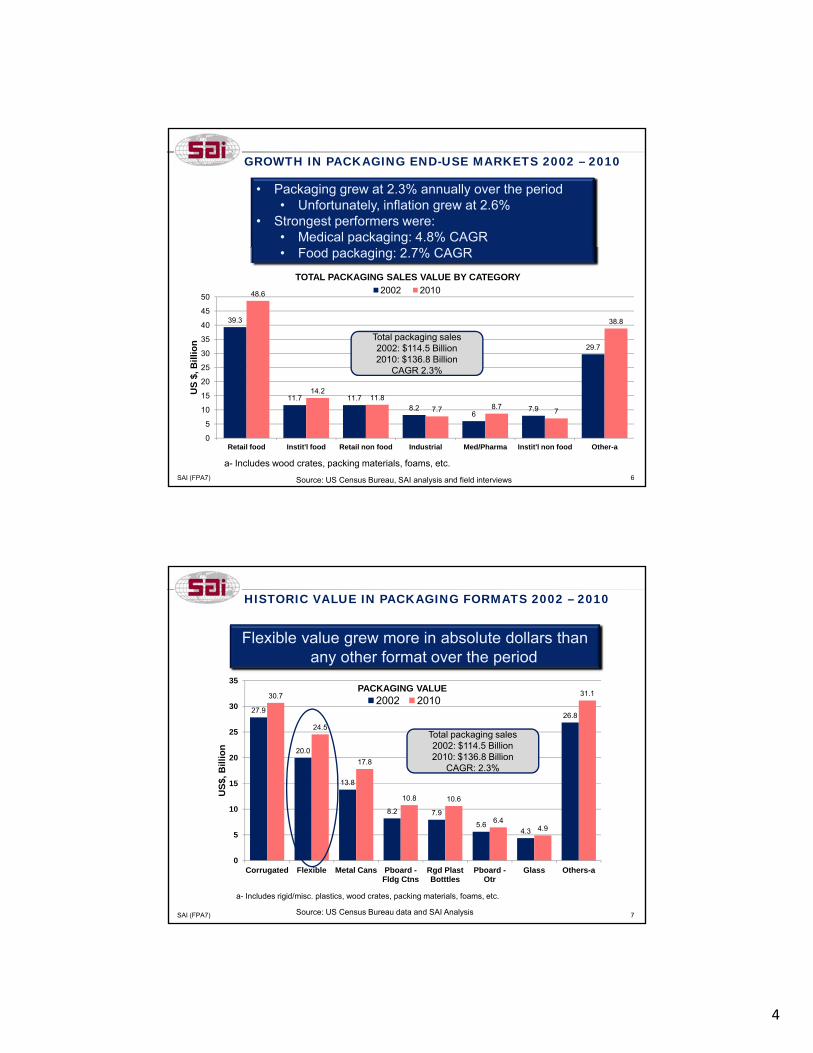

SCOPE

Scope Description

Industry Flexible packaging Materials includes paper, resins, plastic film, foil or combinations

Packaging format FlexibleTargeted non-flexible

Corrugated PaperboardGlass

Rigid compositeRigid metalRigid plastic

End-use category Retail foodRetail non-foodInstitutional food

Institutional non-foodIndustrialMedical and pharmaceutical

Geographic United States

Time period 2002 2010 forecast to 2015

SAI (FPA7) 2

Time period 2002, 2010 forecast to 2015 (Market value based on both growth and inflationary levels)

RESULTS ORIENTED INTERVIEWING SEQUENCE

Number of interviews-a

Type of organization Phases I & II

Industrial manufacturers and 63

Mostsensitive

CPG companies

Retailers 28

Packaging manufacturers(mostly rigid)

22

Material and equipmentsuppliers

15

Other-c 12

Total 140

a- Number of interviews, not organizationsb Based on five end use categories being

Field interviews

SAI (FPA7) 3

b- Based on five end-use categories being examined for the Phase II

c- Includes government agencies, contract packagers, packaging designers and other knowledgeable industry sources

Secondary (published) dataLeastsensitive

FPA reports, statistics & perspectives

3

EXAMPLES OF PHASE II INTERVIEWS: RETAIL FOOD AND NON-FOOD

SAI (FPA7) 4

EXAMPLES OF PHASE II INTERVIEWS: INDUSTRIAL, INSTITUTIONAL, MEDICAL

SAI (FPA7) 5

4

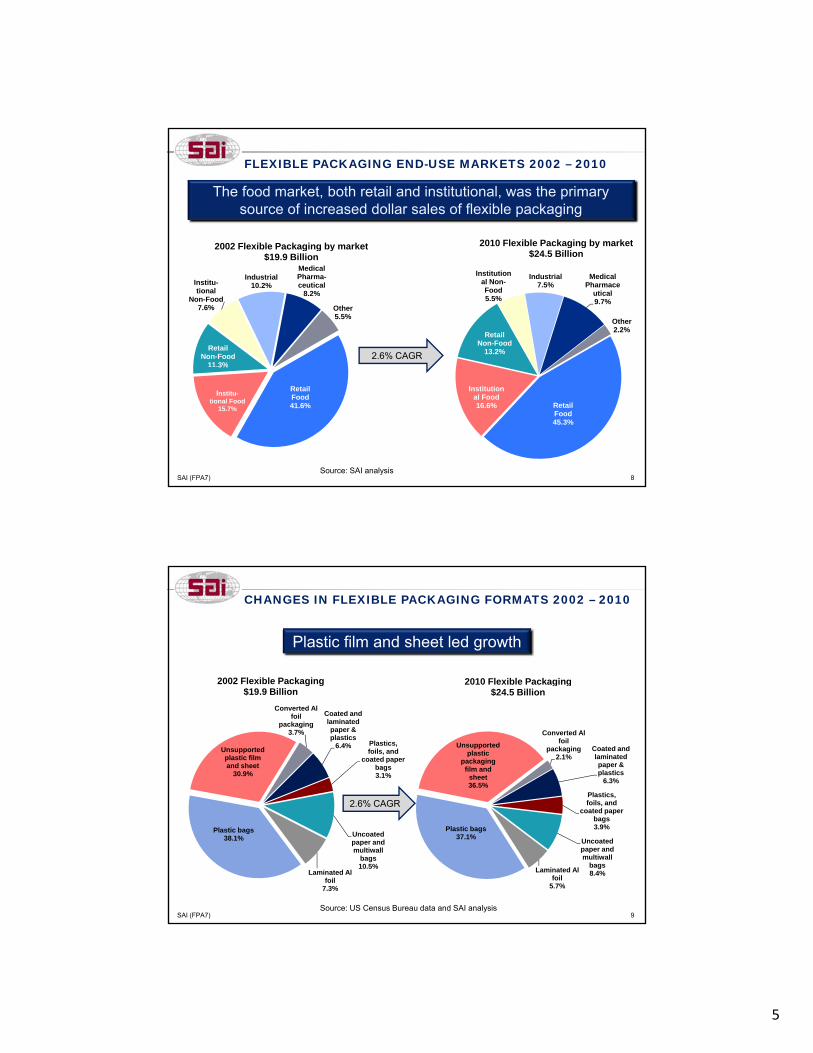

GROWTH IN PACKAGING END-USE MARKETS 2002 – 2010

• Packaging grew at 2.3% annually over the period• Unfortunately, inflation grew at 2.6%

• Strongest performers were:• Medical packaging: 4.8% CAGR

39.3

29.7

48.6

38.8

25

30

35

40

45

50

Bil

lio

n

TOTAL PACKAGING SALES VALUE BY CATEGORY

2002 2010

Total packaging sales2002: $114.5 Billion2010: $136.8 Billion

CAGR 2 3%

• Food packaging: 2.7% CAGR

SAI (FPA7) 6

11.7 11.78.2

67.9

14.211.8

7.7 8.77

0

5

10

15

20

25

Retail food Instit'l food Retail non food Industrial Med/Pharma Instit'l non food Other-a

US

$, B CAGR 2.3%

Source: US Census Bureau, SAI analysis and field interviews

a- Includes wood crates, packing materials, foams, etc.

HISTORIC VALUE IN PACKAGING FORMATS 2002 – 2010

Flexible value grew more in absolute dollars than any other format over the period

35PACKAGING VALUE

27.9

20.0

13.8

26.8

30.7

24.5

17.8

10.8 10.6

31.1

15

20

25

30

US

$, B

illi

on

PACKAGING VALUE2002 2010

Total packaging sales2002: $114.5 Billion2010: $136.8 Billion

CAGR: 2.3%

SAI (FPA7) 7Source: US Census Bureau data and SAI Analysis

8.2 7.9

5.64.3

6.44.9

0

5

10

Corrugated Flexible Metal Cans Pboard -Fldg Ctns

Rgd Plast Botttles

Pboard -Otr

Glass Others-a

a- Includes rigid/misc. plastics, wood crates, packing materials, foams, etc.

5

FLEXIBLE PACKAGING END-USE MARKETS 2002 – 2010

2002 Flexible Packaging by market 2010 Flexible Packaging by market

The food market, both retail and institutional, was the primary source of increased dollar sales of flexible packaging

Retail Non-Food

11.3%

Institu-tional

Non-Food7.6%

Industrial10.2%

Medical Pharma-ceutical

8.2%

Other5.5%

2002 Flexible Packaging by market$19.9 Billion

Retail Non-Food

13.2%

Institutional Non-Food5.5%

Industrial7.5%

Medical Pharmace

utical9.7%

Other2.2%

g g y$24.5 Billion

2.6% CAGR

SAI (FPA7) 8

Retail Food41.6%

Institu-tional Food

15.7%

3%

Retail Food45.3%

Institutional Food16.6%

Source: SAI analysis

CHANGES IN FLEXIBLE PACKAGING FORMATS 2002 – 2010

2002 Flexible Packaging 2010 Flexible Packaging

Plastic film and sheet led growth

Coated and laminated paper & plastics

6.4% Plastics, foils, and

coated paper bags3.1%

Unsupported plastic film and sheet

30.9%

Converted Al foil

packaging3.7%

g g$19.9 Billion

Coated and laminated paper & plastics

6.3%

Plastics, foils, and

Unsupported plastic

packaging film and

sheet36.5%

Converted Al foil

packaging2.1%

g g$24.5 Billion

2 6% CAGR

SAI (FPA7) 9

Uncoated paper and multiwall

bags10.5%

Laminated Al foil

7.3%

Plastic bags38.1%

foils, and coated paper

bags3.9%

Uncoated paper and multiwall

bags8.4%Laminated Al

foil5.7%

Plastic bags37.1%

2.6% CAGR

Source: US Census Bureau data and SAI analysis

6

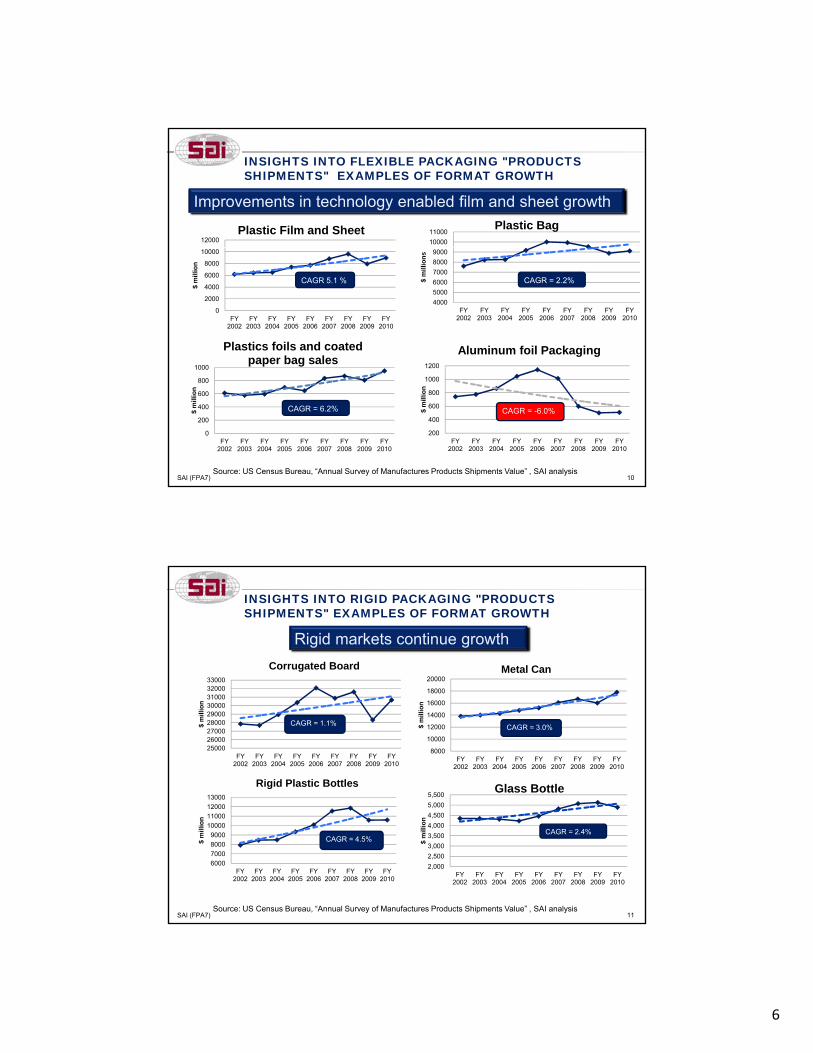

INSIGHTS INTO FLEXIBLE PACKAGING "PRODUCTS SHIPMENTS" EXAMPLES OF FORMAT GROWTH

Improvements in technology enabled film and sheet growth

12000Plastic Film and Sheet

10000

11000Plastic Bag

0

2000

4000

6000

8000

10000

FY 2002

FY 2003

FY 2004

FY 2005

FY 2006

FY 2007

FY 2008

FY 2009

FY 2010

$ m

illio

n

4000

5000

6000

7000

8000

9000

FY 2002

FY 2003

FY 2004

FY 2005

FY 2006

FY 2007

FY 2008

FY 2009

FY 2010

$ m

illio

ns

CAGR = 2.2%CAGR 5.1 %

1000

Plastics foils and coated paper bag sales

1200

Aluminum foil Packaging

SAI (FPA7) 10Source: US Census Bureau, “Annual Survey of Manufactures Products Shipments Value” , SAI analysis

0

200

400

600

800

1000

FY 2002

FY 2003

FY 2004

FY 2005

FY 2006

FY 2007

FY 2008

FY 2009

FY 2010

$ m

illio

n

CAGR = 6.2%

200

400

600

800

1000

1200

FY 2002

FY 2003

FY 2004

FY 2005

FY 2006

FY 2007

FY 2008

FY 2009

FY 2010

$ m

illio

n

CAGR = -6.0%

INSIGHTS INTO RIGID PACKAGING "PRODUCTS SHIPMENTS" EXAMPLES OF FORMAT GROWTH

Rigid markets continue growth

33000

Corrugated Board20000

Metal Can

2500026000270002800029000300003100032000

FY 2002

FY 2003

FY 2004

FY 2005

FY 2006

FY 2007

FY 2008

FY 2009

FY 2010

$ m

illio

n

CAGR = 1.1%

8000

10000

12000

14000

16000

18000

FY 2002

FY 2003

FY 2004

FY 2005

FY 2006

FY 2007

FY 2008

FY 2009

FY 2010

$ m

illio

n

CAGR = 3.0%

12000

13000

Rigid Plastic Bottles

5 000

5,500Glass Bottle

SAI (FPA7) 11

6000

7000

8000

9000

10000

11000

12000

FY 2002

FY 2003

FY 2004

FY 2005

FY 2006

FY 2007

FY 2008

FY 2009

FY 2010

$ m

illio

n

CAGR = 4.5%

Source: US Census Bureau, “Annual Survey of Manufactures Products Shipments Value” , SAI analysis

2,000

2,500

3,000

3,500

4,000

4,500

5,000

FY 2002

FY 2003

FY 2004

FY 2005

FY 2006

FY 2007

FY 2008

FY 2009

FY 2010

$ m

illio

n

CAGR = 2.4%

7

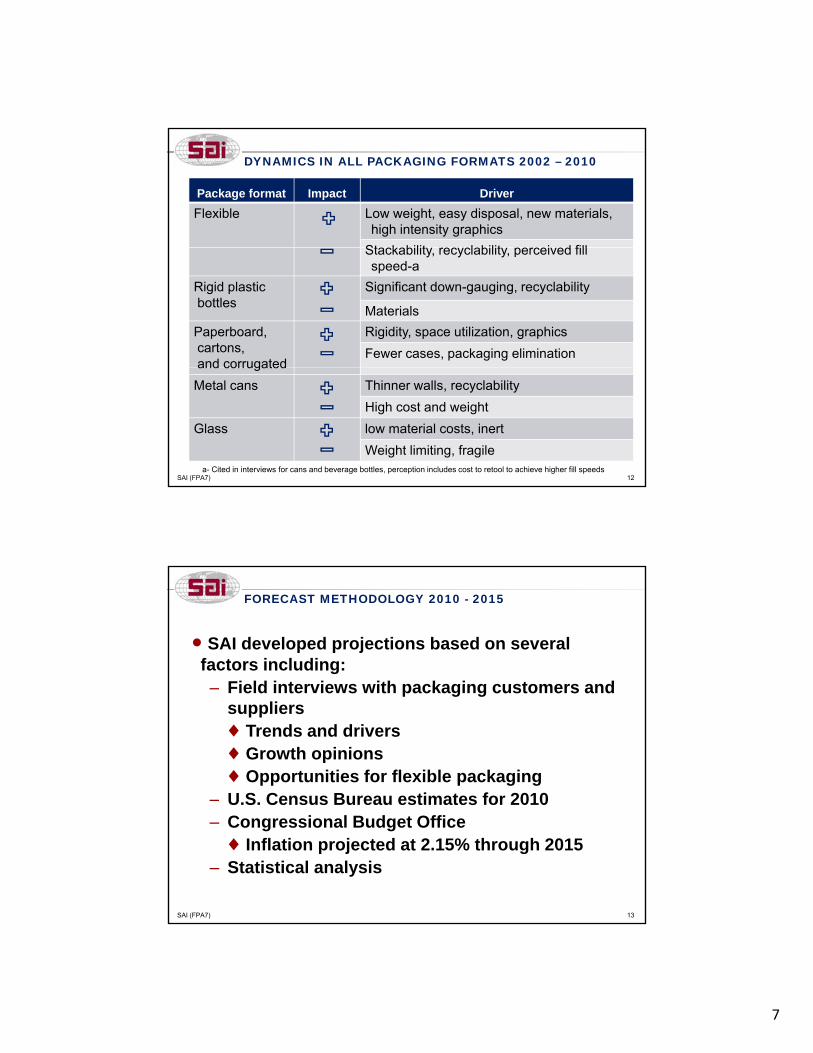

DYNAMICS IN ALL PACKAGING FORMATS 2002 – 2010

Package format Impact Driver

Flexible Low weight, easy disposal, new materials, high intensity graphics

Stackabilit rec clabilit percei ed fillStackability, recyclability, perceived fill speed-a

Rigid plasticbottles

Significant down-gauging, recyclability

Materials

Paperboard, cartons, and corrugated

Rigidity, space utilization, graphics

Fewer cases, packaging elimination

SAI (FPA7) 12

and corrugated

Metal cans Thinner walls, recyclability

High cost and weight

Glass low material costs, inert

Weight limiting, fragilea- Cited in interviews for cans and beverage bottles, perception includes cost to retool to achieve higher fill speeds

FORECAST METHODOLOGY 2010 - 2015

● SAI developed projections based on several factors including:

Field interviews with packaging customers and– Field interviews with packaging customers and suppliers♦ Trends and drivers♦ Growth opinions♦ Opportunities for flexible packaging

– U.S. Census Bureau estimates for 2010U.S. Census Bureau estimates for 2010– Congressional Budget Office♦ Inflation projected at 2.15% through 2015

– Statistical analysis

SAI (FPA7) 13

8

TECHNOLOGY DRIVERS AND TRENDS

ItemApplicable

market Trend/Driver

Light-weighting/ sustainability

RF, IF Reduces cost, uses less material Requires new dies, processing equipment and materials

New films RF, IF, MP Woven and laminated structures, bio films, others to reduce cost, improve barrier properties, sustainability

Pouchtechnology

RF, IF, IN Improved materials and equipmentMore sizes, dispensing/closure/sealing designs,

faster fill speeds

Microwave packaging

RF Convenience, new food products

Market codes: RF Retail Foods IF Institutional Foods MP Medical PharmaceuticalMarket codes: RF- Retail Foods, IF- Institutional Foods, MP- Medical Pharmaceutical, IN- Industrial, RNF- Retail Non-Food

SAI (FPA7) 14

“Manufacturers of packaged goods everywhere face two constant challenges. One is to reduce their environmental footprint to the minimum. The other is to cut costs.” –Manager, Packaging

CONSUMER PACKAGED GOODS MARKET TRENDS AND DRIVERS

ItemApplicable

market Trend/Driver

Right sized packaging RF, IF, MP Proliferation of pack sizes

Market timing RF, IF, MP Requires more pack sizes based on pay cycles, more SKUs – Wal-Mart leading

Sustainability All Broader definition of “sustainability”Tipping point for purchaseCorporate and consumer pressure More regulation

Concentrates RF, IF, IN, MP Increased concentration reduces units

Private label RF, IF, RNF, MP

Value mindset, retailers don’t want to give fitMP up profits

Market codes: RF- Retail Food, IF- Institutional Foods, MP- Medical Pharmaceutical, IN- Industrial, RNF- Retail Non-Food

SAI (FPA7) 15

“The paycheck cycle we’ve talked about before remains extreme…..adjusting pack sizes, large pack sizes at the beginning of the month, small pack sizes at the end of the month.” Bill Simon, CEO of Wal-Mart U.S.

9

CONSUMER TRENDS AND MARKET DRIVERS

ItemApplicable

market Trend/Driver

Focus on All Cost consciousness holdingFocus on price

All Cost consciousness holding

Varied sizes RF, IF, INF Ease of use through single serve, family packaging, re-sealable packages, etc.

Natural content

RF, IF Consumer trend to seek natural content impacts packaging

Private label RF, RNF, MP Continuing value with no significant sacrifice. Retailers unlikely to give back shelf space

Market codes: RF Retail Food IF Institutional Foods MP Medical PharmaceuticalMarket codes: RF- Retail Food, IF- Institutional Foods, MP- Medical Pharmaceutical, IN- Industrial, RNF- Retail Non-Food

SAI (FPA7) 16

FINANCIAL TRENDS AND DRIVERS

ItemApplicable

market Trend/Driver

Raw material costs All Drive to reduce costChanges in raw materials

Capital investment All Reluctance to invest slowed pimplementation of new technologies

Economic recovery All Weak recovery resulted in reluctance to invest in development, expansion and capital

Corporate consolidations

All Industry continues to consolidate, changing competitive pressures

Market codes: RF- Retail Food, IF- Institutional Foods, MP- Medical Pharmaceutical, IN- Industrial, RNF- Retail Non-Food

SAI (FPA7) 17

“Resin obsoletions, increased raw material costs, and increased energy prices. Our business has made a concerted effort to tighten our control over raw-material supply.” Manager, Medical Flexibles

“Companies will use more flexible packaging if it is cheaper. Cost is a major hurdle since investment in new packaging equipment is necessary!” Packaging Manager, Beverage Manufacturer

10

CHANGES IN FLEXIBLE VERSUS RIGID 2010 - 2015

150

PROJECTED PACKAGING SALES Rigid Flexible

● Increases reflect economic recovery and long-term industry growth● Flexible is projected to gain share from rigid

2010 Packaging$136.8 Billion

2015 Packaging$161.1Billion

112.3131.1

24.5 30.1

0

50

100

150

2010 2015

US

$, B

illi

on

g

-a

-a

a- Rounded

SAI (FPA7) 18

Flexible 17.9%

Rigid 82.1%

Flexible18.7%

Rigid81.3%Total: 3.3% CAGR

FLEXIBLE PACKAGING END-USE MARKET GROWTH 2010 –2015

2010 Flexible Packing$24 5 Billion

2015 Flexible Packaging$30 1 Billion

Growing economy will lift all marketsparticularly non-food markets

Retail Food

Institutional Non-

Industrial7.5%

Medical Pharmace

utical9.7%

Other2.2%

$24.5 Billion

Retail Food

Industrial7.4%

Medical Pharma-ceutical

9.1%

Other5.8%

$30.1 Billion

4.2% CAGR

SAI (FPA7) 19Source: SAI analysis

Food45.3%

Institutional Food

16.6%

Retail Non-Food

13.2%

Food5.5%

Food43.5%

Institu-tional Food15.5%

Retail Non-Food13.1%

Institu-tional Non-Food5.5%

11

FLEXIBLE PACKAGING MATERIAL GROWTH 2010 - 2015

Improved technology will benefit film and sheet due to an expanding market and some substitution within flexible packaging

Coated and laminated

pkg materials

6.3%

Plastics, foils, and coated

paper bags3.8%

Uncoated paper and multiwall

bagsPlastics

Aluminum foil

packaging2.4%

2010 Flexible Packaging$24.5 Billion Coated and

laminated pkg

materials6.4%

Plastics, foils, and coated

paper bags4.9%

Uncoated paper and multiwall

bags7.2%

FlexiblePlastics

Aluminum foil

packaging1.7%

2015 Flexible Packaging$30.1 Billion

SAI (FPA7) 20

8.8%

Flexible packaging

foil6.7%

Plastic bags

38.0%

packaging film and sheet34.0%

Flexible packaging

foil4.7%

Plastic bags

33.8%

Plastics packaging film and sheet41.2%

4.2% CAGR

MARKET PENETRATION OPPORTUNITYRETAIL/INSTITUTIONAL – CANS – SOUPS,VEGETABLES, OTHER

Item Requirement

Potential application Pouches for condensed, concentrated or other soups, canned vegetables

Current packaging “Tin can” is the common package – all sizes

Packaging requirement Long shelf life, food safety, good display graphics, shelf display/presentation, shelf space utilization

Motivation for switching

Lower weight, sustainableEasy to open and useLong shelf life

Technical/commercial requirements

Investment is the key issueShelf displaySt k bilit

SAI (FPA7) 21

StackabilityCustomer acceptance

Hurdles Shelf space and stackabilityfill speed

Other considerations FDA/USDA compliance, sustainability, recyclability, carbon footprint

Leading edge products Restaurant and single serve pouches12 lbs

12

MARKET PENETRATION OPPORTUNITYRETAIL FOOD – GLASS – HIGHLY PROCESSED FOODS, FRUITS, OTHER

Item Requirement

Potential application Replace glass in all marketsFruits, gravies, sauces, other

Current packaging Glass bottles, jars

Packaging requirement Product safety/protectionFDA/USDA regulationsSustainability/Cost

Motivation for switching Lighter weightShrinkage protection

Technical/commercial requirements

Cost to change including investmentRecyclability

SAI (FPA7) 22

Hurdles Long shelf life, safetyCapital equipment expense

Other considerations Wal-Mart’s sustainability index ranks flexible packaging higher than glass

Leading edge product Specialties

MARKET PENETRATION OPPORTUNITYRETAIL FOOD – PLASTIC BOTTLES – NON-CARBONATED

Item Requirement

Potential application

Individual serve packages for juices, energy drinks,others

Current packaging Mixed group of bottles, pouches, boxesCurrent packaging Mixed group of bottles, pouches, boxes

Packaging requirement

Light weight, cost savings, sustainable, resealable Display ready

Motivation for switching

Easy to grab, open and useNew cost effective plastic materialsSustainable packages

Technical/commercial requirements

Use of existing pouch equipment is a plusHigh fill speeds

SAI (FPA7) 23

Hurdles Cost of changeRecyclability

Other considerations Use of existing equipment Consumer acceptanceCompetition from thinner plastic bottles

Leading edge product Single serve, toss and go

13

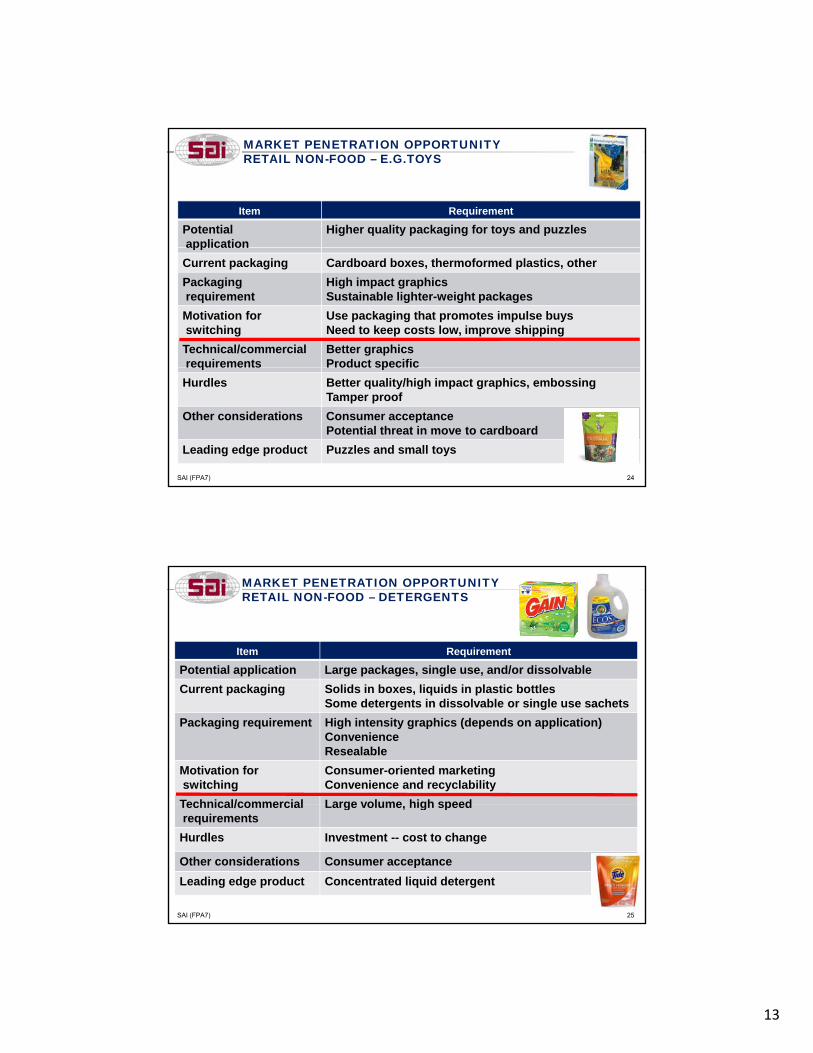

MARKET PENETRATION OPPORTUNITYRETAIL NON-FOOD – E.G.TOYS

Item Requirement

Potential application

Higher quality packaging for toys and puzzlesapplication

Current packaging Cardboard boxes, thermoformed plastics, other

Packaging requirement

High impact graphicsSustainable lighter-weight packages

Motivation for switching

Use packaging that promotes impulse buys Need to keep costs low, improve shipping

Technical/commercial requirements

Better graphics Product specific

SAI (FPA7) 24

requirements Product specific

Hurdles Better quality/high impact graphics, embossingTamper proof

Other considerations Consumer acceptancePotential threat in move to cardboard

Leading edge product Puzzles and small toys

MARKET PENETRATION OPPORTUNITYRETAIL NON-FOOD – DETERGENTS

Item Requirement

Potential application Large packages, single use, and/or dissolvable

C t k i S lid i b li id i l ti b ttlCurrent packaging Solids in boxes, liquids in plastic bottlesSome detergents in dissolvable or single use sachets

Packaging requirement High intensity graphics (depends on application)ConvenienceResealable

Motivation for switching

Consumer-oriented marketingConvenience and recyclability

Technical/commercial Large volume high speed

SAI (FPA7) 25

Technical/commercial requirements

Large volume, high speed

Hurdles Investment -- cost to change

Other considerations Consumer acceptance

Leading edge product Concentrated liquid detergent

14

MARKET PENETRATION OPPORTUNITYRETAIL NON-FOOD – PERSONAL CARE

Item Requirement

Potential application Body wash, shampoo, conditioner, etc.Refill pouches

Current packaging Plastic bottles, small volume of refill pouches, sachets

Packaging requirement

High quality, attractive shelf appearance

Motivation for switching

Less material, lower cost, transportation advantages

Technical/commercial requirements

Capital cost required to change to new packagingHigh volume requires fast fill speed

SAI (FPA7) 26

requirements High volume requires fast fill speed

Hurdles fill speedRecyclability

Other considerations Customer acceptance

Leading edge product Liquid soap refill

NEW MARKET OPPORTUNITYINDUSTRIAL – AGRICULTURAL CHEMICALS

Item Requirement

Potential application Replacement of 1 to 5 gallon containers

C t k i HDPE l b t l l th l tiCurrent packaging used

HDPE, polycarbonate, polypropylene, other plastic bottles, buckets and bags

Packaging requirement

Agricultural chemicals considered hazardousMust contain materials, and survive transportation,accidents, etc.

Motivation for switching

Lightweight, disposability and sustainability

Technical/commercial Packages must meet UN Packaging Requirements

SAI (FPA7) 27

Technical/commercial requirements

Packages must meet UN Packaging Requirements U.S. DOT/49 CFR

Hurdles Meet company and government specifications

Other considerations Resealability a plus

Leading edge product Under developmentNew

Concept

15

NEW MARKET OPPORTUNITYINSTITUTIONAL FOOD – BULK DRIED FRUIT

Item Requirement

Potential application Bulk dried fruit specifically Wholesale food overallWholesale food overall

Current packaging Boxes and rigid totes

Packaging requirement Suitable for transport of bulk dried fruits and other products

Motivation for switching Weight reduction Storage of emptiesCost

T h i l/ i l C it l dit f ki d h dli

SAI (FPA7) 28

Technical/commercial requirements

Capital expenditure for packing and handling equipment

Hurdles Cost to change

Other considerations Customer acceptance

Leading edge product Wholesaler requestNew

Concept

KEY FINDINGS FOR FLEXIBLE PACKAGING

Strengths

Low cost

Light weight

New barrier and physical properties

Weaknesses

High cost of switching

Fill speed

Stackability

Shelf densityp p

Net sustainable

Graphics

Easy to store and use

Shelf density

Not easily recyclable

New to consumer

Opportunities

Plastic bottle, tin cans and glass replacement

Potential low cost polyethylene

Threats

Competition from lightweight cans and plastic bottles

Energy and material price

SAI (FPA7) 29

Potential low cost polyethylene feedstockUse of new materials and bio-based materialsContinued penetration in the food market

Energy and material price spikes

Consumer acceptance

Perceived environmental/safety