optimising ireland’s oil and gas resources · optimising ireland’s oil and gas resources ......

TRANSCRIPT

Optimising Ireland’s Oil andGas Resources

Report of the SIPTU Oil & Gas Review Group

Contents

Introduction Page 5

Chapter 1; Terms and Potential Page 9

Chapter 2; Fiscal Regime –

International Comparisons Page 11

Chapter 3; Licensing Systems Page 13

Known offshore and onshore reserves Page 15

Chapter 4; Best Alternative Options

for Ireland Page 19

Chapter 5; Conclusions Page 21

Chapter 6; Recommendations Page 23

Economic and Employment Potential

of Oil and Gas production Page 25

Observations on the Environmental

Costs of Carbon Resource Usage Page 27

Brief History of Oil and Gas

Industry in Ireland Page 29

Bibliography Page 32

Chart of Oil and Gas finds Page 33

Abbreviations;

BBOE Billion Barrels of Oil Equivalent

DCENR Department of Communications, Energy and Natural Resources

DCMNR Department of Communications, Marine, and Natural Resources

GAO Government Accountability Office (United States)

INPC Irish National Petroleum Corporation

IOC International Oil Company

NOC National Oil Company

PAD Petroleum Affairs Division

PRRT Profit Resource Rent Tax

PSC Production Sharing Contract

SA Service Agreement

TCF Trillion Cubic Feet

3

Op t im i s i n g I r e l a nd ’ s O i l a n d Ga s R e s o u r c e s

Op t im i s i n g I r e l a nd ’ s O i l a n d Ga s R e s o u r c e s

4

The Department of Communications, Energyand Natural Resources (DCENR) estimates atotal reserve potential in the order of 10 billionbarrels of oil equivalent (bboe) beneath theseabed off the west coast of Ireland. On thebasis of geological studies, seismic surveysand drilling results these estimated reservesdivide approximately into 6.5 billion barrels ofoil and 20 trillion cubic feet of gas. This quan-tity of estimated reserves, if found and ex-ploited, would be sufficient to meet Ireland’sdemand for hydrocarbons for over 100 years,based on current usage.

Ireland’s offshore and onshore oil and gas re-serves are managed by the Petroleum AffairsDivision (PAD) of the DCENR which issues dif-ferent authorisations for exploration and pro-duction activities1 under a licensing system2.This system governs petroleum prospecting licences, licensing options, exploration licences and petroleum leases. The licensingregime includes fiscal terms (for example ratesof taxation) and non-fiscal terms (such as theduration of licences, commitments to drillwells etc.).

This discussion document seeks to assesswhether the licensing system under whichcompanies explore and develop oil and gasreserves is appropriate for this country at thisdifficult time in our history. The report com-pares the Irish licensing regime with those ofother countries and examines possiblechanges that could improve the return to theIrish exchequer from any future oil and gasfinds. It also assesses the potential employ-ment benefits from oil and gas explorationand production, and related services, and re-views the experience of the industry in thiscountry over recent decades.

In particular, it examines the significantchanges to the 1975 licensing terms which al-lowed for a 50% State holding, royalties and a50% tax on profits accruing from an oil or gasfind and development. In 1987 royalties andstate participation were abolished and in 1992the corporate tax rate was reduced from 50%to 25%. There were further changes to theregime in 2007 which allows for an improvedreturn to the State from very large finds.

The Irish Government has said that it intendsto keep the licensing terms, both fiscal andnon-fiscal, under review while focusing on attracting a larger share of mobile interna-tional exploration investment to Ireland.

While significant reserves have been discov-ered off shore, most notably in the Corrib fieldin the Atlantic margin, the scale of Ireland’srecoverable oil and gas resources remains unknown. To date, four discoveries off theIrish coast have been declared commercialwhile 13 other discoveries in the Irish offshoreare currently under assessment. There havebeen two offshore oil finds and three gas findssince 2002. There has also been a significantonshore discovery of natural gas in the NorthWest Carboniferous and Clare basins whichcover an area of approximately 8000 squarekilometres in parts of south Donegal, Cavan,Leitrim, Sligo, Mayo, Monaghan, Roscommon,Fermanagh, Clare, Cork, Kerry and Limerick.

By the end of March 2011, three petroleumleases, 13 exploration licences (under the1992 terms) and 8 exploration licenses underthe 2007 terms had been awarded and re-mained in place. The PAD is currently review-ing applications from two other explorationlicence holders for lease undertakings in theCeltic Sea (off the south coast). A lease under-

Op t im i s i n g I r e l a nd ’ s O i l a n d Ga s R e s o u r c e s

5

1Authorisations for exploration and production activities include: petroleum prospecting licences; licensing options; exploration licences (3kinds – standard, deep-water and frontier); lease undertakings; petroleum leases; and reserved areas licences. 2The current licensing system was established in 1992 and revised in 2007. Authorisations granted between 1992 and January 1, 2007 are sub-ject to the1992 Licensing Terms for Offshore Oil and Gas Exploration and Development. The Licensing Terms for Offshore Oil and Gas Explo-ration, Development and Production 2007 are applied to authorisations granted from 2007.

Introduction

taking means that the exploration licence hold-ing company has made a discovery of gas/oiland that the licensee is not yet in a position to declare the find commercial but expects to do so in the near future.

A licensing round aimed at encouraging further exploration in the Atlantic margin off the west coast closed at the end of May 2011.Covering an area of over a quarter of a millionsquare kilometres, this licensing round was thelargest ever opened. The DCENR is currentlyassessing 15 applications for licensing optionsunder this latest round. This compares to justtwo applications for the 2009 offshore licensinground and confirms a renewed interest in theIrish offshore.

As new technologies allowing for the exploitation of previously inaccessible reserves emerge, and the rising cost of oil andgas makes investment in exploration and pro-duction more economically viable, a review of the Irish licensing terms is timely. In-deed, given the rapidly changing world energymarket and the spiralling cost of oil and gas, it is

essential that government policy with regard tothe exploitation of any hydrocarbon reservesshould be re-assessed before any new licensesare issued.

It is noted that the Minister for Communications,Energy and Natural Resources has acceptedthat the current licensing terms for oil and gasexploration and production should be reviewedby an Oireachtas committee. (see Dáil EireannDebate Vol. 730. No. 3. 19th April 2011)

Liberty HallDublinJune 2011

6

Op t im i s i n g I r e l a nd ’ s O i l a n d Ga s R e s o u r c e s

This report is intended to contribute to thepublic debate as the proposed Oireachtasreview approaches.

In this regard it is the considered view of the SIPTU Oil

and Gas Review Group that no new exploration licenses

for oil and gas should be issued by the DCENR until a

detailed reassessment of the current licensing system is

completed. It is also our view that the

proposed Oireachtas review should

have the widest possible brief to

consider not only possible changes in

the licensing terms which might in-

clude the imposition of royalties, State

equity stakes and increased taxes, but

should also examine alternatives in-

volving a more direct State involve-

ment in oil and gas exploration and

production.

The review should examinethe potential for job creationand skills development of arevived oil and gas industryand should also investigatethe implications of oil andgas production on climate change.

The Oireachtas committee should also be charged with

considering actions aimed at getting the companies

which have announced discoveries of oil and gas to

either get these finds into production or declare them

non-commercial and relinquish control of them.

It should consider a new approach to the management

of Irish hydrocarbons that offers the prospect of greater

sovereign control over our natural resources in line with

international best practice and that ensures a better

return for Ireland while remaining profitable for investors.

A new approach to the management of Irish hydrocar-

bons should also involve a reduction in dependence on,

and consumption of, oil and gas. This will help to miti-

gate against the known and increasing dangers arising

from global climate change.

The potential scale of Ireland’s hydrocarbon resources

underlines the necessity to create the conditions for the

development of an indigenous oil and gas industry that

can help to generate long term employment, technologi-

cal skills and revenues. Furthermore, increased levels of

financial returns from a revised fiscal system could be

used to fund a transition to renewable energies reducing

demand for fossil fuels and growing renewable energy

supplies which are critical to our energy security.

In relation to onshore exploration the realconcerns over the potential damage tohuman health and the environment arisingfrom the use of hydraulic fracturing or‘fracking’ in the extraction of natural gasfrom shale must be addressed and an alternative, safe, process for the developmentof these known onshore resources identified.

In the light of the 2010 oil spill disaster at a BP facility in

the Gulf of Mexico it is also essential that a review takes

place of the regulatory and supervisory powers of the

State in relation to oil exploration and production,

particularly in the more hostile offshore territories of the

Atlantic Margin.

7

In this regard it is the considered view of the SIPTU Oiland Gas Review Group that no new exploration

licenses for oil and gas should be issued by the DCENR until

a detailed reassessment of the current licensing system is

completed. It is also our view that the proposed Oireachtas

review should have the widest possible brief to consider not

only possible changes in the licensing terms which might

include the imposition of royalties, State equity stakes and

increased taxes, but should also examine alternatives

involving a more direct State involvement in oil and gas

exploration and production.

Op t im i s i n g I r e l a nd ’ s O i l a n d Ga s R e s o u r c e s

8Kinsale, Co. Cork

Chapter 1;Terms and Potential

It has long been asserted that the current li-censing terms and conditions are excessivelygenerous to the oil and gas companies partic-ularly since the changes made to the regimeby Fianna Fáil led governments in the late1980s and early 1990s. The reason given forthe abolition of royalties and the reduction intax on profits from 50% to 25% (which canbe written off against exploration, develop-ment, close down and other costs) was inorder to encourage greater levels of explo-ration. Since that time a major gas find hasbeen made in the Corrib field off thenorth-west coast of Mayo while significantprospects exist off the west and southwest coasts.

In 2006, the Petroleum Affairs Division(PAD) of the Department of Communi-cations, Energy and Natural Re-sources (DCENR) estimated apotential 10 billion barrels of oilequivalent (gas and/or oil) in the Atlantic Margin West of Ireland).

This 10 bboe figure does not includethe South or South East of Irelandwhere there has been commercial pro-duction (Kinsale, Ballycotton and Sev-enheads) and other shows of offshore oiland gas or any onshore reserves. At cur-rent market prices of around €75 or over$100 dollars a barrel of oil (June 2011),the resources in the Atlantic margin arepotentially worth €750 billion.

Fifteen applications under the latest AtlanticMargin licensing round were submitted bythe end of May 2011 and successful compa-nies will be awarded licensing options over250,000 square kilometres of the Atlantic shelf,an area three times as large as the Irish land-mass. Once these licensing options, which arevalid for a period of up to two years, are

granted the option holder has the first right toan exploration licence or licences. With the

current licencing terms, the PAD essentiallycommits to granting petroleum leases to ex-ploration licence holders if commercially re-coverable amounts of hydrocarbons arefound.

Once granted a petroleum lease companiesare subject to the fiscal and non-fiscal condi-tions outlined in the specific Licensing Termsunder which the initial authorisation (such as a licensing option or exploration licence) wasgranted. This means that if an exploration li-cence was granted between 1992 and 2007and the petroleum lease was granted after2007, the petroleum lease holding companywill be subject to the 1992 Licensing Terms.Under the 1992 Licensing Terms for OffshoreOil and Gas Exploration, companies are onlyrequired to pay nominal fees and a 25% taxrate against which companies can offset allcosts related to the project accrued over a

9

Fifteen applications under the latest Atlantic Margin licensing round were

submitted by the end of May 2011 and

successful companies will be awarded

licensing options over 250,000 square kilometres of the Atlantic shelf, an areathree times as large as the Irish land-mass.

Once these licensing options, which are

valid for a period of up to two years, are

granted the option holder has the first right to

an exploration licence or licences.

Op t im i s i n g I r e l a nd ’ s O i l a n d Ga s R e s o u r c e s

previous 25 year period. This includes explorationcosts and the costs of closing down a project oncompletion. In a 2006 review of Ireland’s fiscalterms, the Department of Communications, Marine and Natural Resources (DCMNR*) de-scribed the 1992 terms as ‘simple and extremely attractive, so much so that Ireland has had thebest fiscal terms in the world for exploration andproduction.’ (Executive Summary of Ireland’s Fiscal Terms August 2006. A report and proposalfrom Petroleum Affairs Division, DCMNR).

While heralded as an improvement on these gen-erous pro-corporate terms, the introduction of the2007 licensing terms with its new Profit ResourceRent Tax (PRRT) also results in few additionalbenefits for the State. The PRRT is calculated on a graded basis of profitability (profit ratio), aftercosts have been offset and tax has been paid,with companies potentially paying a PRRT of between 5% and 15% on their profits. For verylarge finds the tax rate can go up to 40% (25 %tax rate and PRRT of between 5 to 15%). Exceptin the case of very profitable fields, Ireland willsee little additional revenue from the 2007 terms.This PRRT is only applied to authorisationsgranted after 2007.

The current licensing terms essentially offer companies with exploration licences a ‘first refusal’ on petroleum leases to develop potentially productive oil and gas fields in areas coveredunder the company’s exploration licence. In theevent of such discoveries, the 1992 and 2007 licensing terms both state that it shall be the duty

of the Minister to grant a petroleum lease, whichpermits companies to produce Irish gas and oil ina specific area, if the Minister is satisfied by theapplicant’s likely production profile, the appli-cant’s outline development, financial and market-ing plans and an outline statement of the likelyeffects of the proposed development on the envi-ronment.

It would appear that these elements of the licens-ing system bind the Irish State into fixed contractterms without it having prior knowledge of thevalue of the reserves in the relevant field. Underthe current licensing terms, the State effectivelypasses ownership of any finds to the petroleumlease holding company. In return, the companypays 25% tax on its profits in the case of small andmedium sized finds, rising to 40% on large findsunder the terms of the PRRT which only applies tolicenses granted after 2007.

*(The name of the Department was changed tothe Department of Communications, Energy and Natural Resources (DCENR) on foot of legislation introduced in 2007).

10

Gas pipeline

Op t im i s i n g I r e l a nd ’ s O i l a n d Ga s R e s o u r c e s

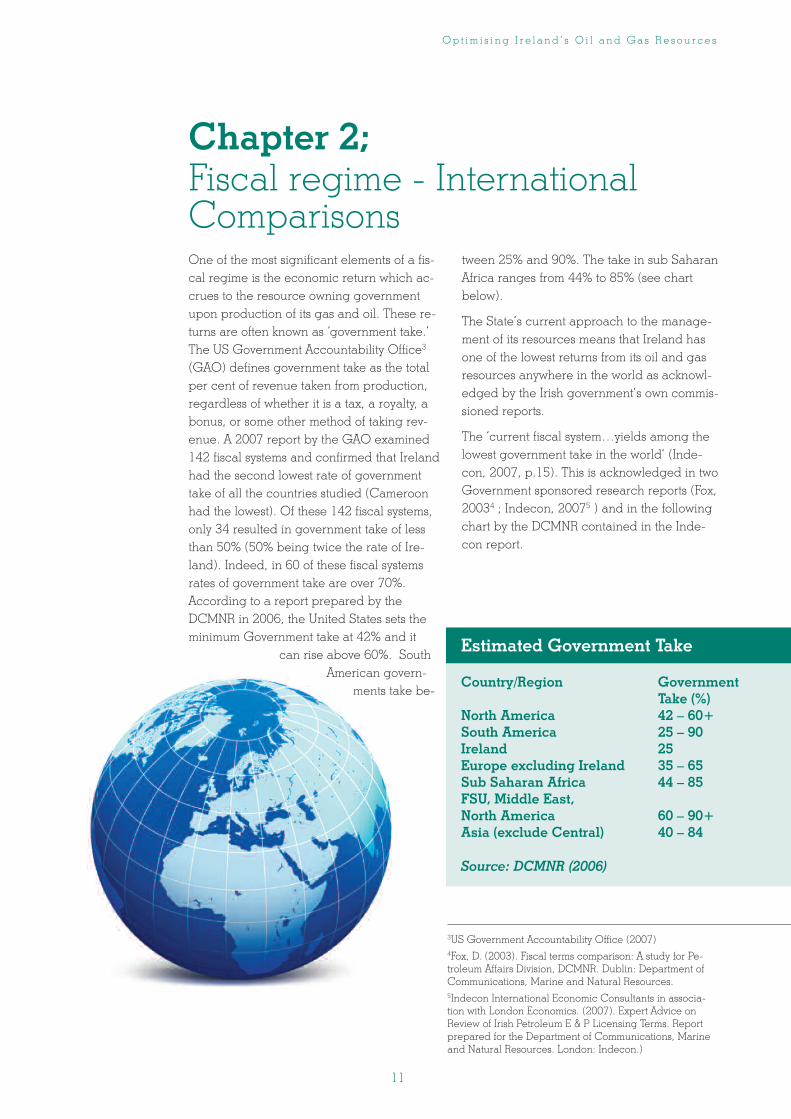

Chapter 2; Fiscal regime - InternationalComparisonsOne of the most significant elements of a fis-cal regime is the economic return which ac-crues to the resource owning governmentupon production of its gas and oil. These re-turns are often known as ‘government take.’The US Government Accountability Office3

(GAO) defines government take as the totalper cent of revenue taken from production,regardless of whether it is a tax, a royalty, abonus, or some other method of taking rev-enue. A 2007 report by the GAO examined142 fiscal systems and confirmed that Irelandhad the second lowest rate of governmenttake of all the countries studied (Cameroonhad the lowest). Of these 142 fiscal systems,only 34 resulted in government take of lessthan 50% (50% being twice the rate of Ire-land). Indeed, in 60 of these fiscal systemsrates of government take are over 70%.According to a report prepared by theDCMNR in 2006, the United States sets theminimum Government take at 42% and it

can rise above 60%. SouthAmerican govern-

ments take be-

tween 25% and 90%. The take in sub SaharanAfrica ranges from 44% to 85% (see chartbelow).

The State’s current approach to the manage-ment of its resources means that Ireland hasone of the lowest returns from its oil and gasresources anywhere in the world as acknowl-edged by the Irish government’s own commis-sioned reports.

The ‘current fiscal system…yields among thelowest government take in the world’ (Inde-con, 2007, p.15). This is acknowledged in twoGovernment sponsored research reports (Fox,20034 ; Indecon, 20075 ) and in the followingchart by the DCMNR contained in the Inde-con report.

11

3US Government Accountability Office (2007)4Fox, D. (2003). Fiscal terms comparison: A study for Pe-troleum Affairs Division, DCMNR. Dublin: Department ofCommunications, Marine and Natural Resources.5Indecon International Economic Consultants in associa-tion with London Economics. (2007). Expert Advice onReview of Irish Petroleum E & P Licensing Terms. Reportprepared for the Department of Communications, Marineand Natural Resources. London: Indecon.)

Estimated Government Take

Country/Region Government Take (%)

North America 42 – 60+South America 25 – 90Ireland 25Europe excluding Ireland 35 – 65Sub Saharan Africa 44 – 85FSU, Middle East, North America 60 – 90+Asia (exclude Central) 40 – 84

Source: DCMNR (2006)

Op t im i s i n g I r e l a nd ’ s O i l a n d Ga s R e s o u r c e s

12

The DCENR’s use of a licensing system, as opposed to production sharing contracts orservice agreements, means that once Irish oil and gas is produced, ownership of theseresources is transferred to the petroleumlease holding companies with the State es-sentially conceding control over its resourcesto these corporations. Companies are not re-quired to sell this oil and/or gas to the Irishmarket and if they choose to sell to consumersin Ireland, they can do so at full market pricesas they are not obliged to sell these resourcesat a reduced price.

Considering the current high oil prices, maturing North Sea fields and heightenedgeo-political tensions over security of supply,the lack of restrictions on the selling and sup-ply of Irish oil and gas is most problematic,particularly when one considers that Irelandimports all of its oil (primarily from the UK andNorway) and most of its gas yet is not guaran-teed a supply of its own resources. While theCorrib field could provide a certain securityof supply its operators (Shell/Statoil/Vermil-lion) are not obliged to sell the gas to the Irishmarket.

The concerns over security of supply are separate to the even more significant issue ofthe lack of economic return to the State fromits resources, including the potential for significant onshore and downstream job creation.

Not only does the State’s current approach to the management of Irish oil and gas meanthat Ireland has one of the lowest rates of re-turns to a government anywhere in the world,there is no state participation in exploration,development or production. In addition, com-panies are under no obligation to use Irishservices, goods or workforce and aren’t re-

quired to land Irish hydrocarbons in thecountry. Indeed modern technology wouldpermit operators to extract oil at sea and loadand transport it by tanker without ever land-ing its product in Ireland. An area of furtherconcern is the acceleration of licensingrounds by the PAD in recent years, throughwhich the DCENR invites companies to applyfor exploration licences or licensing optionsfor onshore and offshore acreage. Recentrounds include inviting applications for licences in the Rockall Basin (2009), the 2010onshore round in the North West Carbonifer-ous and Clare Basins (allowing companies toapply for licensing options for blocks across8,000 square km in counties such as Done-gal, Sligo, Leitrim, Mayo, Clare and Kerry)and the recent Atlantic Margin offshoreround. In this 2011 round, the PAD invitedcompanies to apply for licensing options inthe largest amount of acreage ever opened –around 250,000 sq km.

By the end of March 2011, three petroleumleases, 13 exploration licences (under the1992 terms) and 8 exploration licenses underthe 2007 terms had been awarded and remained in place. The PAD is currently reviewing applications from two other explo-ration licence holders for lease undertakingsin the Celtic Sea (off the south coast).

Op t im i s i n g I r e l a nd ’ s O i l a n d Ga s R e s o u r c e s

13

6Easo (2009, p. 35)7Easo (2009, pp. 37-38)8Johnston et al. (2008, p. 4)9Johnston (2008)10Ernst and Young (2009, p.219)

The exceptionally low rate of return to theIrish State is only one questionable feature ofthe DCENR’s approach to the management ofIrish oil and gas. Another issue lies in the ac-tual use of a licensing system. Licensing sys-tems, also known as concessionary orroyalty/tax systems, are one of two main ap-proaches used by countries across the worldto manage their resources. The other ap-proach is commonly known as a contractualsystem. While a licensing system transfersownership of a state’s resources to the pro-ducing oil company, a contractual systemmeans that the resource-owning state retainsstrong control over its resources. A contrac-tual system typically comprises production-sharing contracts (PSCs) and/or serviceagreements (SAs) with PSCs ‘likely to be thepreferred contract type in new acreagerounds.6’

Under a production sharing contract/agree-ment, the state as owner of the hydrocarbons,permits the international oil company (IOC)as a contractor to carry out exploration andproduction work, often in partnership with astate-owned national oil company, in ex-change for an IOC entitlement to a stipulatedshare of revenues from the hydrocarbons pro-duced (rather than ownership of all the re-sources), as compensation for the risks takenand services rendered7. Johnston, Johnstonand Rogers (2008, p. 4) suggest that under aproduction sharing contract, unlike a licens-ing system, the government receives a largershare of oil and/or gas ‘which can be com-mercialised and monetised according to thehost government’s development programmesand economic needs.’ They add that slightly

over half of the governments with hydrocar-bon production worldwide use PSCs whichare the system of choice in countries such asMalaysia, India, Nigeria, Angola, Trinidad,the Central Asian Republics (of the FSU, for-mer Soviet Union), Algeria, Egypt, Yemen,Syria, Mongolia, and China – countries whichall have higher rates of government take thanIreland.

The service contract is a regime under whichthe state retains full ownership of all the hy-drocarbons being produced on its soil andthe international oil company performs theexploration and production work as a serviceto the State8. With a service contract, the State‘at all times…maintains ownership of the hy-drocarbons produced and usually the IOC(contractor) does not acquire any rights to oiland/or gas, except when a contractor is paidits fee in kind (oil and/or gas) or is given apreferential right to purchase production.9’

In a 2008 study of 45 fiscal systems10, 21 ofthe systems studied were licensing/ conces-sionary, 18 were production sharing contractsand 6 were service agreements (meaning 24were contractual). Ireland, as one of the 21licensing systems studied, had the lowest rateof government tax rate (estimated at a maxi-mum of 28%, even with the 2007 terms) withthe second lowest rate of government tax takeof between 38% and 42%.

Of the licensing systems studied, 15 (includ-ing the US, UK*, Canada, Australia andAlaska) resulted in government take of over50%. Seven licensing systems resulted in gov-ernment take of over 60% – more than twicethe rate of return to Ireland from its oil and

Chapter 3;Licensing systems

Opt im i s i n g I r e l a nd ’ s O i l a n d Ga s R e s o u r c e s

gas. This study also served to emphasise howcountries with higher rates of governmenttake utilised production sharing contracts orservice agreements, ensuring that alongsidehigher returns, the Government retained con-trol and ownership of its hydrocarbons withadditional benefits occuring through localemployment, service provision and supply ofgoods. Fifteen of the countries with PSCs (in-cluding Indonesia, Malaysia, China, Trindadand Tobago, and Libya) received governmenttake in excess of 70%. Of the six serviceagreements studied, two countries,Venezuelaand Iran, had a government take of over 90%.

*(The British government recently introduceda plan to increase its take to 62% and up to80% of future profits in order to fund a 1pence cut in fuel duty).

14

Op t im i s i n g I r e l a nd ’ s O i l a n d Ga s R e s o u r c e s

Known offshore and onshore reserves

The Dunquin prospect (Block number44) off the south west of Kerry has a re-serve estimated by Davy’s at 9 trillioncubic feet of gas – equivalent to 1.5billion barrels of oil and of similar sizeto the Corrib reserve off north WestMayo. The licence was issued to Provi-dence Resources a company ownedby Tony O’Reilly which sold on a sub-stantial part of its holding to ExxonMo-bile in 2005 for a reported €100million leaving Providence with a 20%stake and ExxonMobile taking up thecost of development.

If the State had retained control of theexploration licence or used a contrac-tual system (either a production shar-ing or service agreement) it couldhave done the deal with Exxon directlythus raising substantial revenues forthe exchequer while retaining an in-terest in the find. Now Exxon Mobileand Italian oil company, ENI, eachhold 40% with Providence controllingthe remainder.

The Dooish prospect (12/2) some 150kilometres off the Donegal coast wasdrilled by Shell in 2008 after earlierdrillings in 2001 and 2003 confirmedthe presence of a “substantial gascondensate column.”

A prospect off Spanish Point (35) incounty Clare yielded both oil and gasflows when first drilled in 1981. The li-cence was first acquired by Provi-dence Resources in 2004 and thecompany still has a 56% stake. It is es-timated to contain 1.4 TCF and 160million barrels of recoverable oil. TheBurren prospect nearby has alsoyielded small flows of oil.

StatoilHydro (19/8) controls the Cashelprospect which contains an estimated250 million bbbe according to pub-lished estimates.

The Kish (33) in Dublin Bay was firstdrilled in 1977 by Amoco, in 1986 byCharterhouse and in 1997 by Enter-prise. In 2010, Providence said there isan estimated 870 million barrels of oilin the area, worth an estimated €60billion at current prices and an-nounced it intended to re-start drillingand is also looking for possible gasstorage structures in the area.

The Connemara (26/28) prospect wasowned by Island Oil and Gas sincetaken over by Irish company, San LeonEnergy, which has recently talked upits potential for development. It flowedoil when drilled by Statoil in 1997. SanLeon has estimated that there couldbe 12 trillion cubic feet of gas in itsKillala, Kingfisher and Inishmoreprospects off the west coast - theequivalent of 12 Corrib gas fieldswhile its Tir na nÓg prospect off thesouth west coast could hold 5.8 billionbarrels of oil, according to the com-pany.

The Slyne prospect owned by SanLeon Energy and Lundin Petroleum(50% each) is potentially as largeas the Corrib gas field, accordingto the operators.

The Helvick/Hook Head/Dunmoreprospects are owned by Providencewhich announced its intention inMay, 2010 to intensify explorationin the area.

15

Op t im i s i n g I r e l a nd ’ s O i l a n d Ga s R e s o u r c e s

The Dunquin prospect (Block number 44) off thesouth west of Kerry has a reserve estimated byDavy’s at 9 trillion cubic feet of gas – equivalentto 1.5 billion barrels of oil and of similar size tothe Corrib reserve off north West Mayo. The licence was issued to Providence Resources, acompany owned by Tony O’Reilly, and SosinaExploration Ltd. In 2005, the prospect wasfarmed out to oil and gas major, ExxonMobil.The terms of the farm-out agreement provide for ExxonMobil to conduct a significant explo-ration work program in return for 80% of theDunquin Prospect. Providence retained a 16%interest, and Sosina, a 4% interest. ExxonMobilintends to drill a well by 2012 at an estimatedcost of over €100 million.

The Seven Heads and Ballycottonprospects off the Cork coast arelinked to the Kinsale field whichsupplied gas to the Irish grid forseveral decades.

There are considerable differencesin the accessibility of the oil andgas finds that have been disclosedand the costs of their development.The Kish Bank off Dublin Bay, forexample, is in relatively shallowwater compared to the Dooish dis-covery at a depth of 1500 metres oreven the Corrib field at 300 metres.This raises the question of whetherthere should be different incentivesor tax breaks for the exploration ofmore difficult prospects.

In August 2009, Canadian firm Ver-million Energy Trust announcedthat it was to pay $400 million(€280 million) for the 18.5% in theCorrib gas field owned byMarathon Oil. The balance isowned by Dutch owned, Shell andthe partly State owned Norwegiancompany, Statoil. The purchaseputs a value on the field in 2009 ofjust €1.5 billion but the actualprofits will be multiples of that.Under the current regime Shelland its partners can write off allexploration and development costsand the cost of abandoning thefind before declaring a taxableprofit.

16

Op t im i s i n g I r e l a nd ’ s O i l a n d Ga s R e s o u r c e s

Onshore

Irish Lough Allen Natural Gas set upin July 2010 by Dublin based ThomasAnderson and Askeaton based MartinLawrence Keeley has been granted alicence to explore for gas in the bor-der counties along with an Australiancompany, Tamboran Resources PTYLtd. Full details have yet to be dis-closed but reports prepared in themid-1990s on the basis of pastdrillings in the Lough Allen area indi-

cated that three sandstone reservoirscould potentially contain over 10 trillion cubic feet of gas.

British based company, Enegi Oil plcwhich has exploration interests inNewfoundland was also granted a licence to explore onshore. Enegi’s licences covers an area in the ClareBasin which includes parts of Clare,Limerick and Kerry.

These latest onshore licences cover anarea of over 750 square miles (1948 sqkm) which is about as large as thewhole of County Wicklow from an orig-inal acreage on offer of over 8000 sqkilometres in the North-West and Clarebasins. A case can be made for leav-ing offshore exploration to the expertswith deep pockets while ensuring thatthe State gets an adequate share.

Onshore explorationis well within the ca-pability of varioussemi-State and Stateorganisations.

Exploring onshore isrelatively cheap com-pared with offshoreexploration and de-velopment costs arealmost certain to belower although thereare major difficultiesin exploiting the typeof shale gas likely tobe found. Most of thegas has often to beleft in the ground.There are also major

potential environmental costs, giventhe need to fracture the undergroundshale with pressurised water to whichchemicals, including known carcino-gens, are added. The hydraulic frac-turing or ‘fracking’ process has beenhalted in some countries, includingmost recently in France, due to envi-ronmental and health concerns and isthe subject of growing controversy inthe US and in the counties surround-ing Lough Allen in the north-west.

Lough Allen

17

Op t im i s i n g I r e l a nd ’ s O i l a n d Ga s R e s o u r c e s

18Rig workers

Chapter 4;What are the best alternativeoptions for Ireland?There are a number of options open to Ire-land to ensure that it begins to benefit fullyfrom its own resources. It is arguable that untilan alternative model can be devised andagreed, a moratorium is required on thegranting of new authorisations and on exist-ing exploration licences, lease undertakings,petroleum leases, and the opening of newacreage.

The following section outlines three optionsfor Ireland;

1. Licensing systemIt is highly apparent that the current licensingsystem offers few benefits to the Irish state andat the least requires modification, if notreplacement, as this type of systemconcedes control and ownership of re-sources to international oil companiesin exchange for very limited financialreturns. If a licensing system were tobe used, the current system could bemodified in the following ways:• Increase taxes (Norway has a

tax rate of 78%)• Re-introduce royalties. The US

Federal Government receives royalties from production in on-shore federal lands and offshore in areas such as the Gulf of Mexico.

• Introduce a ‘State Direct Financial Interest’ as in Norway.

• Introduce signature or other bonus payments as in Indonesia, Iraq and the US.

• Grant licences to an Irish national oil company to explore and produce Irish hydrocarbons with profits from this

company returned to the State. • Introduce a requirement upon

companies to guarantee supply to the Irish market at agreed prices.

• Make licensing, regulatory and planning processes (from the opening of acreage to the granting of authorisations to the decommissioning of wells) open and genuinely participative. The Corrib gas project is a graphic example of the failure of regulatory, planning and political processes.

• Make all elements of the system transparent – Norway has an open approach to information sharing and the public can easily access information

on licence-holding companies, returns tothe State, and on-going exploration and production works.

19

It is arguable that until an alternative model can be devised and agreed, a moratorium is required on the granting of new authorisations and on existing exploration licences, lease undertakings, petroleum leases, and the opening of new acreage.

Op t im i s i n g I r e l a nd ’ s O i l a n d Ga s R e s o u r c e s

2. Contractual systemThe introduction of a contractual system could positivelytransform the Irish State’s model of resource manage-ment, ensuring stronger control and greater benefits forthe country. Using the under-utilised, state-owned IrishNational Petroleum Corporation (INPC) or through theformation of a new national oil company, Ireland couldenter into production sharing contracts or service agree-ments with oil companies to explore and produce Irishhydrocarbons. Or the State could carry an interest andpermit the oil companies to conduct the work with theState sharing in the proceeds from production.

It is acknowledged that the offshore and onshore skillsbase developed in Ireland in the 1970’s and 1980’s toservice the Kinsale field and other exploration activitieshas diminished but that experience shows that withproper management and foresight they can be revived.

While the INPC, or a new national oil company (NOC),may not have the capital, human or technical resourcesfor production sharing, it is possible to devise a contractin which the NOC is carried through the exploration,development and production phases with a requirementthat its staff are subject to training and involvement inthe international oil companies’ operations, with a signif-icant proportion of the NOC’s share of profits initiallygoing towards the development of the company.

Upon developing the necessary expertise and resources,the NOC could then become an equal partner in pro-duction or could conduct operations on its own (this ap-proach could also be applied to a NOC under alicensing system). When developing its model ofresource management

Norway ensured it developed its technological abilitiesthrough international oil companies being required towork with Statoil which was a state owned company. Al-though partially privatised in more recent times, the Nor-wegian State still owns 67% of Statoil.

Service contracts are another option for Ireland and byoffering financial, or other, incentives the Irish statecould contract oil companies to carry out the explo-ration, development and production work, while ensur-ing strong state control and meaningful financialreturns.

3. Hybrid systemA third option is to develop a hybrid system which con-tains both licensing and contractual elements. Thiswould improve state control and find a mid-point be-tween a ‘free market’ approach and state controlledproduction. Such a system could include productionsharing agreements being implemented alongside im-proved terms and conditions under a licensing system,meaning exploration and production would be con-ducted by both international oil companies and the Irishstate. If a licensing system is used alongside contractualarrangements such as production sharing contracts orservice agreements the current fiscal terms (namely the1992 and 2007 licensing terms) will need to be re-placed with terms which will bring additional benefits tothe Irish state.

An interesting model to examine is Peru which operatesa licence system and service contracts. Peruvian oil andgas exploration and production activities are conductedunder licence or service contracts granted by the gov-ernment. Under a licence contract, the contractor paysa royalty and tax, whereas under a service contract thegovernment pays remuneration to the contractor. Asstated in the Peruvian Constitution and the Organic Lawfor Hydrocarbons, a licence contract does not imply atransfer or lease of property over the area of explorationor exploitation. By virtue of the licence contract, thecontractor acquires the authorisation to explore or to ex-ploit hydrocarbons in a determined area and Perupetro(the entity that holds the Peruvian state interest) transfersthe property right in the extracted hydrocarbons to thecontractor, who must pay a royalty to the state . Compa-nies are also subject to a corporate income tax of 30%.

20

Op t im i s i n g I r e l a nd ’ s O i l a n d Ga s R e s o u r c e s

21

Chapter 5; Conclusions

As established throughout this report, the verygenerous fiscal, regulatory and licensingregime governing oil and gas development inIreland must be reviewed. This report intendsto contribute to public debate on this topic asthe proposed Oireachtas review approaches.There are many reasons why changes to theState’s approach to the management of its oiland gas are required from an economic, so-cial responsibility and sustainability perspec-tive. These include the necessity to realise anappropriate andjust return to theState of the valueof developedcarbon resourcesand in order tobring the fiscaland regulatoryregime into linewith best interna-tional standards.It is also requiredin order to max-imise the eco-nomic,employment, ed-ucation and skillstraining potentialof the oil and gas industry.

In addition, a number of specific reasons forchange have arisen since the 1992 Termswere introduced. These include the on-goingappreciation in the value of carbon resourceswhich has generated massive windfall profitsto oil and gas corporations worldwide; thegreater understanding of climate change andthe enormous costs associated with its mitiga-tion; and, finally, the extent of the recessionwhich requires a meaningful and proportion-ate contribution from all sectors of the econ-omy and society.

The appreciation in the value of natural gasalso means that the investment – return ratio isnow much more favourable than before whilethe threshold for determining the commercial-ity of finds has been greatly reduced. This isof particular significance in the Irish context.Finds previously declared non-commercialmay now in fact be so.

While it is clear that there is no easy or quickway to access the potential offshore resources

it is equally evidentthat the current fis-cal and licensingregime is generousto the oil and gascompanies. Thosecompanies that getcontrol of new ex-ploration licenseswill enjoy the benefitof the current gen-erous terms whenand if they decide toexploit any finds.

It is also withoutquestion that thecurrent price of oil

and gas and the availability of new deep seaexploration and production technologies havemade the Irish offshore a more viable invest-ment prospect than in the early 1990s whenthe current terms were largely devised.

There have been two oil and three gas findssince 2002. However, there have often beenlengthy delays between discovery of a findand confirmation of its commerciality. Speed-ier assessment and either exploitation or relin-quishment of authorisations for the 14 findsthat have been already made and not yet de-clared commercial should be encouraged bythe DCENR.

Op t im i s i n g I r e l a nd ’ s O i l a n d Ga s R e s o u r c e s

22

Any review must re-consider whether it is ap-propriate or financially sensible for the Stateto guarantee that companies with explorationlicenses will automatically secure petroleumleases to develop potentially productive oiland gas fields without the State having priorknowledge as to the value of the reserves inthe relevant field. This binds the Irish Stateinto fiscal and non-fiscal arrangements with-out having vital information about the value ofthese resources. Increased levels of financialreturns from a revised fiscal system could beused to fund a transition to renewable ener-gies reducing demand for fossil fuels andgrowing renewable energy supplies whichare critical to our energy security.

Op t im i s i n g I r e l a nd ’ s O i l a n d Ga s R e s o u r c e s

Gas pipeline

23

Chapter 6; Recommendations

It is the considered view of the SIPTUOil and Gas Review Group that nonew exploration licenses for oil andgas should be issued by the DCENRuntil a detailed reassessment of thecurrent licensing system is completedunder the proposed Oireachtas review.

It is our view that the proposedOireachtas review should have thewidest possible brief to consider possi-ble changes in the licensing termswhich might include the imposition ofroyalties, State equity stakes and in-creased taxes.

It should also examine alternativemodels for the development of oil andgas resources and the growing globaltrend towards increasing direct Stateinvolvement in the exploitation andproduction of hydrocarbons.

The review should examine the poten-tial for economic development, jobcreation, skills enhancement andtraining in an advanced oil and gasindustry and seek information and ad-vice from countries that have success-fully managed and grown theirhydrocarbon production.

It should also investigate the impact ofoil and gas production on climatechange.

The Oireachtas review should also becharged with considering actionsaimed at getting the companies whichhave announced discoveries of oil andgas as far back as 1963 to either getthese finds into production or declarethem non-commercial and relinquishthe authorisations.

The review must re-consider the li-censing terms offer of a ‘first refusal’to companies with exploration licensesfor petroleum leases to develop po-tentially productive oil and gas fieldsas this would appear to bind the IrishState into fixed contract terms withoutit having prior knowledge of the valueof the reserves in the relevant field.

The review should consider whetherincreased levels of financial returnfrom a revised fiscal system should beused to fund a transition to renewableenergies reducing demand for fossilfuels and growing renewable energysupplies which are critical to our en-ergy security.

Attention should also be paid to theabsence of requirements for oil or gasdiscoveries to be landed in Ireland. Itmay make economic sense for oil fromsome small finds to be shipped directly to refineries abroad but inmarginal situations the State should,at the very least, retain the right to en-sure companies land the produce inIreland even if that doesn’t maximiseprofit for the company.

It is important that any significantfinds that are developed to productionare landed in Ireland and contributeto the revival of the onshore servicingand supply industry as well as otherpotential educational, skills develop-ment (including at third level and pro-fessional level) and job creationinitiatives, particularly in coastaltowns with harbour facilities.

In relation to onshore exploration, thereview must examine the real con-

Op t im i s i n g I r e l a nd ’ s O i l a n d Ga s R e s o u r c e s

24

15IOOA, (2007). Securing our energy future.

cerns over the potential damage tohuman health and the environmentarising from the use of hydraulic frac-turing, or ‘fracking’, in the extractionof natural gas from shale and seek toensure that a safe, alternative processfor the development of these knownresources is deployed.

In the light of the 2010 oil spill disas-ter at a BP facility in the Gulf of Mex-ico it is also essential that a reviewtakes place of the regulatory and su-pervisory powers of the State in rela-tion to oil exploration and production,particularly in the more hostile off-shore territories of the Atlantic Mar-gin.

The Oireachtas review should con-sider the establishment of a bodywhich would involve industry stake-holders, including the oil and gascompanies, trade unions, governmentnominees, environmental and com-munity representatives in order to im-prove communications between thevarious interests and ensure that themaximum potential for Ireland is de-rived from all aspects of hydrocarbondevelopment. In this context the re-view should also consider the futurerole and remit of the Petroleum AffairsDivision of the DCENR.

Op t im i s i n g I r e l a nd ’ s O i l a n d Ga s R e s o u r c e s

25

Many countries have developed an industryfor the servicing and supply of offshore oiland gas operations. Indeed, in Ireland in the1970’s and early 1980’s when there was ex-tensive offshore exploration a new industryemerged which employed several thousandworkers, including many that became mem-bers of the ITGWU (which merged with FWUIin 1990 to form SIPTU).

Oil and gas exploration started in Irish watersin 1970 and a commercial gas field was dis-covered by Marathon Oil off Kinsale Head.Over an eight year period until 1978, whengas production at Kinsale Head began, manyIrish based companies and workers got in-volved in all aspects of oil and gas explo-ration, appraisal and production activities inthe Celtic Sea. Marathon’s Alpha and Bravogas production platforms for the Kinsale Headfield were constructed at Cork and New Ross,county Wexford providing employment forhigher skilled marine trades, including ship-builders, engineers, riggers, welders, craneoperators, dockers, painters and general op-eratives. The construction company was Mi-corpori, an Italian company.

Other services such as shipping, supplyboats, container services, food, fuel, engi-neering, diving, transport, manufacturing,training, administration services, constructionof gas onshore receiving facilities, pipelineconstruction, transport infrastructure,haulage, housing, etc, all significantly devel-oped as Marathon’s gas production pro-gramme got under way. The infrastructurallink by Bord Gais of the Kinsale Head supplyinto the developing national natural gas grid

expanded the economic benefits of this indigenous hydrocarbon resource.

Many offshore oil rig jobs were created for platform operators, drillers, assistantdrillers, derrickmen, roughnecks, roustabouts,maintenance roustabouts, cooks, painters,welders, mechanics, subsea engineers, mechanics, motormen, geologists, radio operators, stewards, seamen, mud loggers,and medics while shore based personnelwere involved in logistics, port services andadministration. A large skills pool developedin the Cork area that responded to the needsof the oil industry.

The then State training agency Anco (laterFÁS), in conjunction with the oil companies,drilling companies and supply boat ownersdeveloped offshore fire-fighting and survival courses. The main impetus for the development of an Irish offshore oil and gasservices sector came from the ITGWU (nowSIPTU) in Cork’s number 3 Branch with thesupport of Cork number 5 Branch. The eco-nomic spin-off to the local economy was en-sured by this approach of the Union insecuring both offshore and onshore job opportunities. Highly skilled Irish based seamen secured work with the offshore supply companies such as Doyle’s and Mainport. Many skilled rig workers returnedfrom abroad to work in the industry.

From 1977, offshore exploration companiescommenced exploration activities along thewest coast of Ireland from south west of Kerryto Donegal. From 1975 to 1985, seventy threeexploration wells were drilled in Irish waters,

Economic and EmploymentPotential of Oil and Gas production

Opt im i s i n g I r e l a nd ’ s O i l a n d Ga s R e s o u r c e s

and ports such as Fenit, Foynes, and Galwayon the west coast and Dublin on the east coastwere involved in offshore hydrocarbon relatedactivity. Cork port was used for further explo-ration along the south coast. Offshore and onshore jobs and related supply of goods andservices developed around these ports. Work-ers with transferable skills such as mechanicsand fishermen were trained in oil rig and related work.

There were significant employment and eco-nomic benefits to the Irish economy from theupstream and downstream oil and gas explo-ration/production related activities. However,the depth of water of west coast offshore areassuch as the Porcupine Basin along the West-ern Atlantic Margin, allied to the strong Atlantic weather and sea swells hindered exploration and production. Deep water production technology had yet to developwhile lower oil and gas prices did not providean economic incentive in Irish waters. (In sub-sequent years, Norway and other oil provinceshave developed the necessary technology fordeep-water oil and gas production).

In 200711 the Irish Offshore Operators Association (IOOA), the organisation whichrepresents oil and gas companies claimed that“expenditure on offshore exploration has ex-ceeded €2 billion and of this figure 30% hasbeen direct expenditure in Ireland” since1970.

Less than a decade ago, 400 Irish companieshad the capacity for oil and gas related activity in Ireland according to a directory ofthe industry compiled by Enterprise Ireland.

In 2002, the then Fianna Fáil led governmentsold Ireland’s only oil refinery at Whitegate,Cork together with the massive Whiddy oil terminal in Bantry Bay to multi-national ConocoPhillips for €77 million. Five yearslater the company sold on the refinery for€380 million.

26

Op t im i s i n g I r e l a nd ’ s O i l a n d Ga s R e s o u r c e s

11 IOOA, (2007). Securing our energy future.

Contemporary society is about to undergo aprofound change. The society that we have developed in the Western world is one that hasbeen dependent on carbon resources. We havedesigned a society based on cheap and readilyavailable supplies of carbon resources. Not onlyhas carbon provided us with physical power,electricity, transportation and the capability forglobal market expansion, it has also determinedour clothing and food resources. 95% of all ourfood products require oil use. Based on cheapand available carbon resources we have builtan industrial and consumer wonderland formany people in the Western world. The reality isthat this is now coming to an end.12

Historically, the West’s dependence on, and useof, carbon resources has caused it to create twoserious dysfunctions. The first is that it has ledthe West into a series of aggressive militaristicwars and collaborations with oppressiveregimes throughout the world, most particularlyin the Middle East. This has resulted in thedeath and abuse of hundreds of thousands,perhaps millions, of people. Second, the exploitation of carbon resources has caused extraordinary levels of direct pollution, whichhas impacted on human life and health and onbiodiversity. The most notable recent examplehas been the Gulf of Mexico oil spill disaster in2010.

To these on-going dysfunctions have now beenadded two profound new realities. First, we are at, or close to, the peak carbon resourceproduction point. From now, the reserves ofavailable, commercially recoverable carbon resources will decline and their cost will rapidlyappreciate. The result is that over the comingfew decades the cost of carbon resources willsimply become too high and consequently the

Observations on the Environmental Costs ofCarbon Resource Usage

To these on-going

dysfunctions have now

been added two profound

new realities. First, we

are at, or close to, the

peak carbon resource

production point. From

now, the reserves of

available, commercially

recoverable carbon

resources will decline and

their cost will rapidly

appreciate. The result is

that over the coming few

decades the cost of carbon

resources will simply

become too high and

consequently the

configuration of the

global economy will

profoundly alter.

26 27

Op t im i s i n g I r e l a nd ’ s O i l a n d Ga s R e s o u r c e s

12 See Jeremy Leggott (2005) ‘Half Gone: Oil, Gas,Hot Air and The Global Energy Crisis.’ London:Portobella Books.

configuration of the global economy willprofoundly alter. Second, it is now clear thatthe burning of carbon resources has precip-itated a climate change event of unprece-dented scale. The evidence and data on thisis now overwhelming and compelling. Oneof the key drivers in this has been the con-centration of Carbon Dioxide (CO2) in theatmosphere. CO2 is a direct consequence of carbon resource burning. In simple terms,we are returning solid carbon back into theatmosphere in the form of gas which is trapping heat on the planet’s surface.

For these two primary reasons, the age ofcarbon resources is now coming to an end.This is the context within which we must examine the continuing exploration and exploitation of carbon resources. We need to make a transition to a non-carbon econ-omy as quickly as possible. For these reasons,we need to radically question governmentpolicy in regards to the utility and ethics ofany further exploration for oil and gas and weneed to examine the fiscal regime surround-ing existing commercial finds.

The principles governing fiscal policy should include:

Carbon taxes [levies, etc.] have been misapplied to users when they should be applied to suppliers. This re-configurationshould be on the logic of seeking to changebehaviour and forcing the energy companiesto develop new energy sources whether international or state owned. Taxes [levies,etc.] are needed to pay for external costs associated with climate change and are also required to pay for the transition to a sustainable resource economy.

28

Opt im i s i ng I r e l and ’ s O i l and Gas Re sou rce s

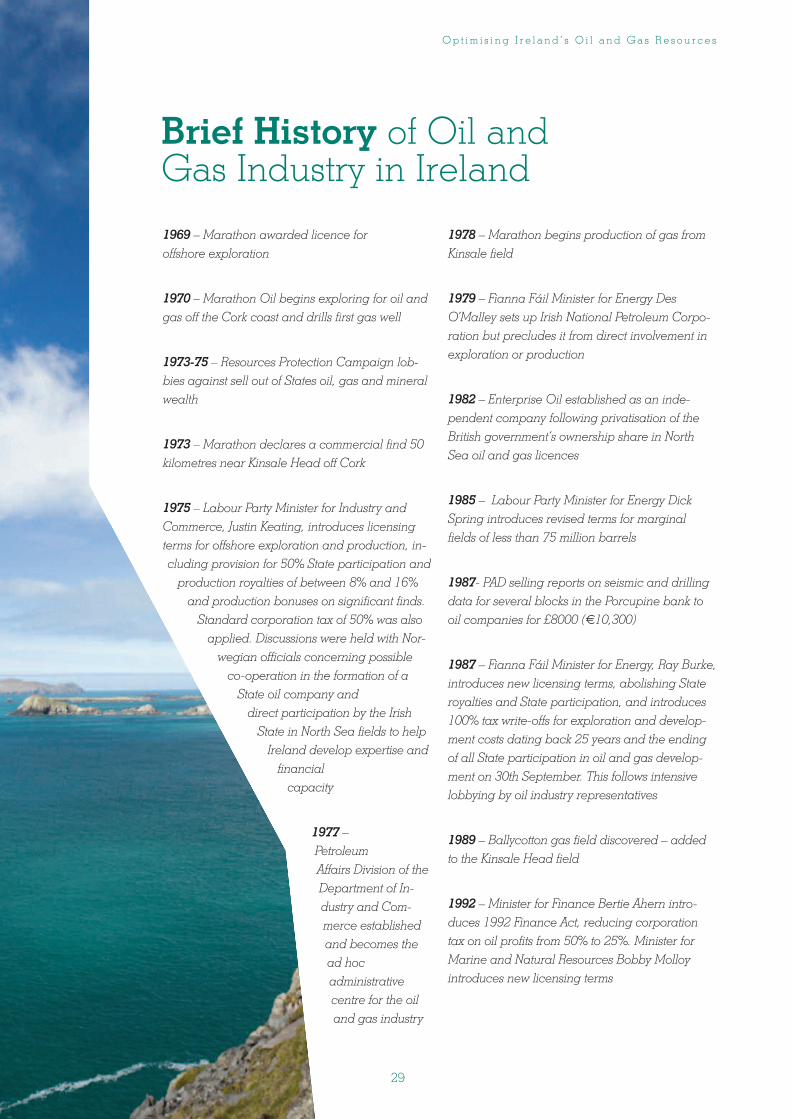

1969 – Marathon awarded licence for offshore exploration

1970 – Marathon Oil begins exploring for oil andgas off the Cork coast and drills first gas well

1973-75 – Resources Protection Campaign lob-bies against sell out of States oil, gas and mineralwealth

1973 – Marathon declares a commercial find 50kilometres near Kinsale Head off Cork

1975 – Labour Party Minister for Industry andCommerce, Justin Keating, introduces licensingterms for offshore exploration and production, in-cluding provision for 50% State participation andproduction royalties of between 8% and 16%and production bonuses on significant finds.Standard corporation tax of 50% was alsoapplied. Discussions were held with Nor-wegian officials concerning possibleco-operation in the formation of aState oil company and direct participation by the IrishState in North Sea fields to helpIreland develop expertise and financial capacity

1977 – Petroleum Affairs Division of theDepartment of In-dustry and Com-merce establishedand becomes thead hoc administrativecentre for the oiland gas industry

1978 – Marathon begins production of gas fromKinsale field

1979 – Fianna Fáil Minister for Energy DesO’Malley sets up Irish National Petroleum Corpo-ration but precludes it from direct involvement inexploration or production

1982 – Enterprise Oil established as an inde-pendent company following privatisation of theBritish government’s ownership share in NorthSea oil and gas licences

1985 – Labour Party Minister for Energy DickSpring introduces revised terms for marginalfields of less than 75 million barrels

1987- PAD selling reports on seismic and drillingdata for several blocks in the Porcupine bank tooil companies for £8000 (€10,300)

1987 – Fianna Fáil Minister for Energy, Ray Burke,introduces new licensing terms, abolishing Stateroyalties and State participation, and introduces100% tax write-offs for exploration and develop-ment costs dating back 25 years and the endingof all State participation in oil and gas develop-ment on 30th September. This follows intensivelobbying by oil industry representatives

1989 – Ballycotton gas field discovered – addedto the Kinsale Head field

1992 – Minister for Finance Bertie Ahern intro-duces 1992 Finance Act, reducing corporationtax on oil profits from 50% to 25%. Minister forMarine and Natural Resources Bobby Molloy introduces new licensing terms

Brief History of Oil and Gas Industry in Ireland

29

Op t im i s i n g I r e l a nd ’ s O i l a n d Ga s R e s o u r c e s

January 1993 – Enterprise Oil (Enterprise EnergyIreland) awarded deep-water exploration licencefor block 18/20, which contains Corrib gas field

October 1996 – Enterprise Oil announces discov-ery of the Corrib gas field in the Slyne basin 80kilometres off the northwest coast of Mayo. Enter-prise Oil incorporated in the Bahamas

July 2000 – Government passes Gas (Amend-ment) Act of 2000

September 2000 – Bertie Ahern introduces Statu-tory Instrument 110, transferring powers over pro-duction pipelines from Department of PublicEnterprise to Department of the Marine and Natu-ral Resources

2001 – Appraisal well drilled on the Seven Headsstructure off Cork and declared commercial twoyears later with small levels of oil brought onshore

January 2001 – EEI applies to Department ofMarine and Natural Resources for petroleumlease. Mayo County Council requests further in-formation from EEI

August 2001 – Mayo County Council grantsplanning permission for the Corrib Gas terminal;Rossport residents immediately appeal decision toAn Bord Pleanála

15 November 2001 – Fianna Fáil minister, FrankFahey introduces Statutory Instrument 517, giving

him as Minister for the Marine and Natural Re-sources powers to grant compulsory acquisitionorders for land along the route of the proposedCorrib gas pipeline

16 November 2001 – Frank Fahey grants petro-leum lease to EEI; Bord Pleanála announces oralhearings into appeal against Mayo County Coun-cil planning decision for the terminal at Bal-linaboy

21 November 2001 – EEI submits new environ-mental impact statement (EIS) to Department ofMarine and Natural Resources in support of ap-plication to build a gas pipeline from sub-sea fa-cilities to the processing plant at Ballinaboy. EEIapplies for approval of its plan of development,foreshore licence and consent to construct thepipeline

April 2002 – Shell buys Enterprise Oil. FrankFahey issues consent for plan of development andfor pipeline at Ballinaboy

2003 – After a lengthy oral hearing, ABPs plan-ning inspector refuses permission for the Corribgas terminal arguing that it was in the wrong lo-cation and posed a significant environmentalthreat. Following a re-application planning per-mission was again granted by Mayo CountyCouncil and upheld by An Bord Pleanála. Licens-ing round for Porcupine basin

June 2005 – Shell workers attempt to enter landand are refused permission by

30

Op t im i s i n g I r e l a nd ’ s O i l a n d Ga s R e s o u r c e s

landowners; Five Rossport men are jailed forbreach of high court injunction and contempt ofcourt. (Since the five men were released in Oc-tober 2005, protests and opposition to the routeof the pipeline and the location of the terminalhave continued with over €14.245 million ex-pended on Garda overtime and allowancesalone. The on-going opposition to the projectand issues around policing have resulted in a serious breakdown in relations between Shell,its partners and the local communities.)

2005 – Licensing round for Northeast RockallBasin

2006 – Five applications from four countries received for Frontier exploration licence in theSlyne/Erris/Donegal licensing round

2007 Licensing round for the Porcupine Basinoff the west coast

2007 – New licensing terms introduced byGreen Party Minister for Communications, Energy and Natural Resources, Eamon Ryan

2009 – An Bord Pleanála opens new hearingon modified onshore pipeline route to Ballinaboy terminal. Off shore pipeline fromCorrib gas field laid despite protests by localfishermen, other members of the communityand supporters. ABP rules that half of the modified route is unacceptable on safetygrounds. Licensing round for Rockall off thenorth-west

2010 – Licensing round for onshore licensingoptions opened. New round for licensing op-tions in the Atlantic Margin opened with appli-cations sought by May 2011

2010 – ABP oral hearing on third proposed onshore pipeline route to Ballinaboy through a special area of conservation and underSruwaddacon Bay

2011 – ABP approves new route. Permissionsgranted by Minister Pat Carey just before Fianna Fáil leaves office in March. Applicationdate for new offshore exploration licenses in Atlantic margin expires end of May. New FineGael/ Labour Government defeats Sinn Feinmotion for introduction of a 50% tax on profitsfrom any oil and gas find and a return to 51%State participation and 7.5% royalties. Ministerfor Communications, Energy and Natural Resources, Pat Rabbitte agrees to Oireachtascommittee review of oil and gas licensing terms

The SIPTU Oil and Gas Review Group was convened in early 2010 by SIPTU General President,

Jack O’Connor, and asked to consider the potential that could accrue to the Irish exchequer from a

change to the current licensing regime that governs the exploration, development and production

of Ireland’s offshore and onshore oil and gas reserves. The Group includes Jack O’Connor;

Noel Dowling and Padhraig Campbell of the SIPTU National Offshore Committee; Amanda Slevin

UCD Phd Candidate; Dr Mark Garavan Lecturer GMIT; Marie Sherlock SIPTU Economist; Colm

Rapple financial journalist; and Frank Connolly SIPTU Head of Communications.

31

Op t im i s i n g I r e l a nd ’ s O i l a n d Ga s R e s o u r c e s

32

Bibliography

Easo, J. (2009). Licences, concessions, production sharing agreements and service contracts. In G. Picton-Turbervill (Ed), Oil and gas: A practical handbook. London: Globe Law and Business.

Ernst & Young. (2009). Global oil and gas tax guide 2009. Dublin: Ernst & Young.

Fox, D. (2003). Fiscal terms comparison: A study for Petroleum Affairs Division, DCMNR. Dublin: Department of Communications, Marine and Natural Resources.

Indecon International Economic Consultants in association with London Economics. (2007). Expert Advice on Review of Irish Petroleum E & P Licensing Terms. Report prepared for the Departmentof Communications, Marine and Natural Resources. London: Indecon.

Irish Offshore Operators Association, (2008). Securing our energy future. Dublin. IOOA.

Johnston, D. (2008). Changing fiscal landscape. Journal of World Energy Law and Business, 1(1) ,31-54.

Johnston, D., Johnston, D. & Rogers, T. (2008). International Petroleum Taxation. Independent PetroleumAssociation of America (pp. 1-55). Hancock, New Hampshire: Daniel Johnston & Co., Inc.

Kaiser, M.J. & Pulsipher, A.G. (2006). Capital investment decision making and trends: Implications onpetroleum resource development in the U.S. Gulf of Mexico. New Orleans: Mineral Management Service, U.S. Department of the Interior.

United States Government Accountability Office. (2007). Oil and gas royalties: A comparison of theshare of revenue received from oil and gas production by the Federal Government and other resourceowners. Washington DC: US Government Accountability Office.

Jeremy Leggott (2005) ‘Half Gone: Oil, Gas, Hot Air and The Global Energy Crisis.’ London: Portobella Books.

Op t im i s i n g I r e l a nd ’ s O i l a n d Ga s R e s o u r c e s

33

Chart of Oil and Gas finds

Discovery Hydrocarbon Status Current Discovery Discovery Original Well AreaName Type Operator Year Well Operator

Bandon Oil Under Serica Energy 2009 27/4-1,1z Serica Energy Slyne Basinassessment

Hook Head Oil Under Providence 2007 (Initially 50/11-3 Providence North Celtic assessment Resources identified 1971 Resources Sea Basin

Schull Gas Under Island Oil and Gas 2007 (Initially 57/2-3 Island Oil North Celticassessment identified 1987) and Gas Sea Basin

Old Head Gas Under Island Oil and Gas 2006 49/23-1 Island Oil North Celticof Kinsale assessment and Gas Sea Basin

Dooish Gas Under Shell 2002 12/2-1 Enterprise Rockall Condensate assessment Energy Ireland Basin

Corrib Gas Undergoing Shell 1996 18/20-1 Enterprise Oil Slyne Basindevelopment

Ballycotton Gas In production PSE Kinsale Energy 1989 48/20-2 Marathon North Celtic Sea Basin

Dunmore Oil Under Providence Resources 1985 50/6-1 Gulf North Celtic assessment Sea Basin

Galley Head Gas Under Lansdowne Oil and Gas 1985 48/18-1 BP North Celtic assessment Sea Basin

Helvick Oil Under Providence Resources 1983 49/9-2 Gulf North Celtic assessment Sea Basin

Spanish Point Gas Condensate Under Providence Resources 1981 35/8-2 Phillips Porcupine assessment Basin

Connemara Oil Under Island Oil and Gas 1979 26/28-1 BP Porcupine assessment Basin

Burren Oil Under Providence Resources 1978 35/8-1 Phillips Porcupine assessment Basin

Ardmore Gas Under Providence Resources 1974 49/14-1 Marathon North Celtic assessment Sea Basin

Barryroe Oil Under Lansdowne Oil and Gas 1973 48/24-1 Esso North Celtic assessment Sea Basin

Seven Heads Gas In production PSE Seven Heads 1973 48/24-1 Esso North Celtic Sea Basin

Kinsale Head Gas In production PSE Kinsale Energy 1971 48/25-2 Marathon North Celtic Sea Basin

Dowra Gas Under assessment 1963 Dowra-1 Ambassador Onshore NW and under Irish Oil Carboniferous application Company Basin

Op t im i s i n g I r e l a nd ’ s O i l a n d Ga s R e s o u r c e s

While only four discoveries offshore Ireland have so far been declared commercial, another fourteen are still being assessed. The table issued in April 2011 details the 18 significant hydrocarbon onshore and offshore discoveries.

34

“I saw the thing that had happened all over the

world…. Irish governments were so anxious to

get a little bit of revenue that they wrote condi-

tions that were much too soft. I don’t know the

extent of their agreements now. I’m terrified that

they have detailed unbreakable agreements

which will be very dis-advantageous to us

which…were made at a time when oil was much

cheaper and in much greater supply. They were

made at a bad time and I would like to add this

thought, which is a thought about the future. If

we waste this resource it will be a crime against

the Irish people. We are in danger of doing it.

I would like to see the abrogation or long

fingering of existing agreements and to open up

the situation to the world…Oil is $100 a barrel

and the technologies of deep water drilling are

developed. We should go again fresh in the light

of current circumstances and not the circum-

stances of a decade ago when nobody ever

believed oil would start to run out.”

Interview in April 2008

Justin Keating, former Labour Party

Minister for Industry and

Commerce who introduced the

1975 terms for offshore exploration.

He died in December 2009.

Op t im i s i n g I r e l a nd ’ s O i l a n d Ga s R e s o u r c e s

Produced by the SIPTU Communicat ions Department.Printed by Trade Union Labour.

Services Industrial Professional andTechnical Union

Liberty HallDublin 1Tel: 1890 747881Email: [email protected]

ISBN

978

-0-9

5558

23-3

-2