osisko corporate presentation - mines & money london 2016

TRANSCRIPT

THE LEADING INTERMEDIATE ROYALTY COMPANYCorporate Presentation

2016 Mines and Money London – Nov. 28 - Dec.1, 2016

Certain statements contained in this presentation may be deemed "forward-looking statements". All statements in this release, other than statements of historical fact, that addressfuture events, developments or performance that Osisko (the “Corporation”) expect to occur including managements’ expectations regarding the Corporation’s growth, results ofoperations, estimated future revenues, requirements for additional capital, future demand for and prices of commodities, business prospects and opportunities are forward lookingstatements. Forward looking statements are statements that are not historical facts and are generally, but not always, identified by the words "expects", "plans", "anticipates", "believes","intends", "estimates", "projects", "potential", "scheduled" and similar expressions or variations (Including negative variations), or that events or conditions "will", "would", "may", "could"or "should" occur including, without limitation, that all conditions precedent to the transaction will be met and the realization of the anticipated benefits deriving therefrom forshareholders of the Corporation, the view on (i) the quality and the potential of the Corporation’s assets, production forecasts for properties in which the corporation holds a royalty.Although the Corporation believes the expectations expressed in such forward-looking statements are based on reasonable assumptions, such statements involve known and unknownrisks, uncertainties and other factors and are not guarantees of future performance and actual results may accordingly differ materially from those in forward looking statements. Factorsthat could cause the actual results to differ materially from those in forward-looking statements include, without limitation: fluctuations in the prices of the commodities that driveroyalties held by the Corporation; fluctuations in the value of the Canadian dollar relative to the U.S. dollar; risks related to the operators of the properties in which the Corporation holdsa royalty; development, permitting, infrastructure, operating or technical difficulties on any of the properties in which the Corporation hold a royalty or other interest; rate and timing ofproduction differences from resource estimates or production forecasts by operators of properties in which the Corporation hold a royalty or other interest; risks and hazards associatedwith the business of exploring, development and mining on any of the properties in which the Corporation hold a royalty or other interest, including, but not limited to unusual orunexpected geological and metallurgical conditions, slope failures or cave-ins, flooding and other natural disasters or civil unrest; regulatory changes by national and local government,including corporate law, permitting and licensing regimes and taxation policies; regulations and political or economic developments in any of the countries where properties in which theCorporation hold a royalty or other interest are located or through which they are held); continued availability of capital and financing and general economic, market or businessconditions; business opportunities that become available to, or are pursued by the Corporation; the impossibility to acquire royalties and to fund precious metal streams; other uninsuredrisks. The forward looking statements contained in this presentation are based upon assumptions management believes to be reasonable, including, without limitation: the ongoingoperation of the properties in which the Corporation holds a royalty or other interest by the owners or operators of such properties in a manner consistent with past practice; theaccuracy of public statements and disclosures made by the owners or operators of such underlying properties; no material adverse change in the market price of the commodities thatunderlie the asset portfolio; no adverse development in respect of any significant property in which the Corporation holds a royalty, stream or other interest; the accuracy of publiclydisclosed expectations for the development of underlying properties that are not yet in production; and the absence of any other factors that could cause actions, events or results todiffer from those anticipated, estimated or intended. For additional information on risks, uncertainties and assumptions, please refer to the Corporation’s most recent Annual InformationForm filed on SEDAR at www.sedar.com. The Corporation cautions that the foregoing list of risk and uncertainties is not exhaustive. Investors and others who base themselves on theforward looking statements contained herein should carefully consider the above factors as well as the uncertainties they represent and the risk they entail. The Corporation believes thatthe expectations reflected in those forward-looking statements are reasonable, but no assurance can be given that these expectations will prove to be correct and such forward-lookingstatements included in this presentation should not be unduly relied upon. These statements speak only as of the date of this presentation. The Corporation undertakes no obligation topublicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, other than as required by applicable law.

Safe Harbour Statement:This PowerPoint presentation has been prepared for informational purposes only in order to assist prospective investors in evaluating an investment in Osisko Gold Royalties Ltd. Byaccepting delivery of this confidential information or any other material in connection with an investment in the Company, the investor agrees: (1) to keep strictly confidential thecontents of this confidential information presentation and such other material and not to disclose such contents to any third party or otherwise use the contents for any purpose otherthan evaluation by such offered of an investment in the securities; (2) not to copy all or any portion of this confidential PowerPoint presentation, other confidential information or anysuch other material.

Inquiries regarding this confidential PowerPoint presentation can be made to the senior management of the Company.

Forward Looking Statements

2

Osisko is subject to the reporting requirements of the applicable Canadian securities laws, and as a result reports its mineral reserves according to Canadian standards. Canadianreporting requirements for disclosure of mineral properties are governed by NI 43-101. The definitions of NI 43-101 are adopted from those given by the Canadian Institute of Mining,Metallurgy and Petroleum (“CIM”). U.S. reporting requirements are governed by the Commission’s Industry Guide 7 (“Guide 7”). This presentation includes estimates of mineralreserves and mineral resources reported in accordance with NI 43-101. These reporting standards have similar goals in terms of conveying an appropriate level of confidence in thedisclosures being reported, but embody different approaches and definitions. For example, under Guide 7, mineralization may not be classified as a “reserve” unless thedetermination has been made that the mineralization could be economically and legally produced or extracted at the time the reserve determination is made. Consequently, thedefinitions of “Proven Mineral Reserves” and “Probable Mineral Reserves” under CIM standards differ in certain respects from the standards of the Commission. Osisko also reportsestimates of “mineral resources” in accordance with NI 43-101. While the terms “Mineral Resource,” “Measured Mineral Resource,” “Indicated Mineral Resource” and “InferredMineral Resource” are recognized by NI 43-101, they are not defined terms under standards of the Commission and, generally, U.S. companies are not permitted to report estimatesof mineral resources of any category in documents filed with the Commission. As such, certain information contained in this presentation concerning descriptions of mineralizationand estimates of mineral reserves and mineral resources under Canadian standards is not comparable to similar information made public by United States companies subject to thereporting and disclosure requirements of the Commission. Readers are cautioned not to assume that all or any part of Measured Mineral Resources or Indicated Mineral Resourceswill ever be converted into Mineral Reserves. Readers are also cautioned not to assume that all or any part of an Inferred Mineral Resource exists, or is economically or legallymineable. Further, an “Inferred Mineral Resource” has a great amount of uncertainty as to its existence and as to its economic and legal feasibility, and a reader cannot assume thatall or any part of an Inferred Mineral Resource will ever be upgraded to a higher category. Under Canadian rules, estimates of Inferred Mineral Resources may not form the basis offeasibility or other economic studies.

Cautionary Note to U.S. Investors Regarding theUse of Mineral Reserve and Mineral Resource Estimates

3

As at November 28, 2016

TSX & NYSE:OR

$1.4BMARKET CAP

$40.7MOPERATING CASH FLOWYTD 2016

$393M CASH & CASH EQUIVALENTS(at September 30, 2016)

$150-$200MAVAILABLE CREDIT

34,500-37,200 ozATTRIBUTABLE GOLDOUNCES EXPECTED FOR 2016

TWO OF THE PREMIER ROYALTY

ASSETS IN THE GOLD SECTOR

STRONG CASH POSITION

QUARTERLY DIVIDEND

OVER 50 ROYALTIES

TRACK RECORD OF SUCCESS

GOLD FOCUSED

THE LEADING INTERMEDIATE GOLD ROYALTY COMPANY

28,793 ozAuEq YTD 2016

$40.7M IN OPERATING CASH FLOW

YTD 2016

ON TRACK TO ACHIEVE

GUIDANCE

4

$1,379 $1,369

$1,498$1,467

$1,485 $1,491

$1,636 $1,631

$1,743

$1,200

$1,300

$1,400

$1,500

$1,600

$1,700

$1,800

Q3 2014 Q4 2014 Q1 2015 Q2 2015 Q3 2015 Q4 2015 Q1 2016 Q2 2016 Q3 2016

A Great Time to Own Canadian Gold

Osisko Quarterly Realized Gold Price (C$/oz)

Strong upward momentum in Canadian gold price Increased industry activity in Québec/Canadian exploration

Peak London PM Fixing in CAD:$1,877/oz on Sep. 6, 2011

5

$342

$234 $231

$192$164

$143 $138$118

$0

$50

$100

$150

$200

$250

$300

$350

$400

Penasquito Stillwater CanadianMalartic

Detour Lake Cortez Éléonore Gold Quarry Goldstrike

Worldwide Ranking of Gold Royalties - 5% NPV (US$ M)

Osisko holds two of the highest quality gold royalties in the sector

Source: BMO Capital Markets Equity Research. NPV shown using a 5% discount rate and BMO commodity pricing for gold of US$1,292/oz for 2016, US$1,350/oz for 2017,US$1,250/oz for 2018 and US$1,200/oz for 2019 and LT.

High Quality Gold Royalties

6

ZERO-COST GOLD IN CANADA

GOLD EQUIVALENT OUNCES EARNED (oz AuEq)

21% increase in gold equivalent ounces year over year.On track to achieve guidance.

GUIDANCE (oz Au)

34,500 - 37,200 oz Au

2016E

YTD: 28,793

1. Gold equivalent ounces earned is a non-IFRS measure and includes NSR royalties in gold, silver, other cash royalties. Silver was converted to gold equivalent ounces by multiplying the silver ounces by the average silver price for the period and dividing by the average gold price for the period. Cash royalties were converted into gold equivalent ounces by dividing the associated revenue by the average gold price for the period. For Q3 2016, the average per ounce commodity prices were as follows: $1,742 gold (Q3 2015: $1,472), $25.60 silver (Q3 2015: $19.52).

8,264 oz Au

9,902 oz Au

103 oz AuEq (Ag and cash royalties)

201 oz AuEq (Ag and cash royalties)

Q3 2015 Q3 2016

21% Increase

8,367 oz AuEq

10,103 oz AuEq

7

$1.5

$6.5

$12.6

$8.4

$9.8

$15.9$15.0

$0.0

$2.0

$4.0

$6.0

$8.0

$10.0

$12.0

$14.0

$16.0

$18.0

Q1 2015 Q2 2015 Q3 2015 Q4 2015 Q1 2016 Q2 2016 Q3 2016

Increasing Cash Flows

Net Cash Flows from Operating Activities ($C M)

8

Focusing on the Royalty & Streaming Business

Earn-in agreement with Osisko Mining Inc. on Québec exploration properties sets stage for a leaner royalty business

Osisko retains 1.5% - 3.5% NSR royalty

Optionality on northern Québec exploration

Simplifies Osisko’s business model

No longer directly participates in exploration activities (with the exception of the Coulonproject)

Reduces G&A by ~ $5 million per year

28 employees from receptionist to CEO

Further streamlining to take place

9

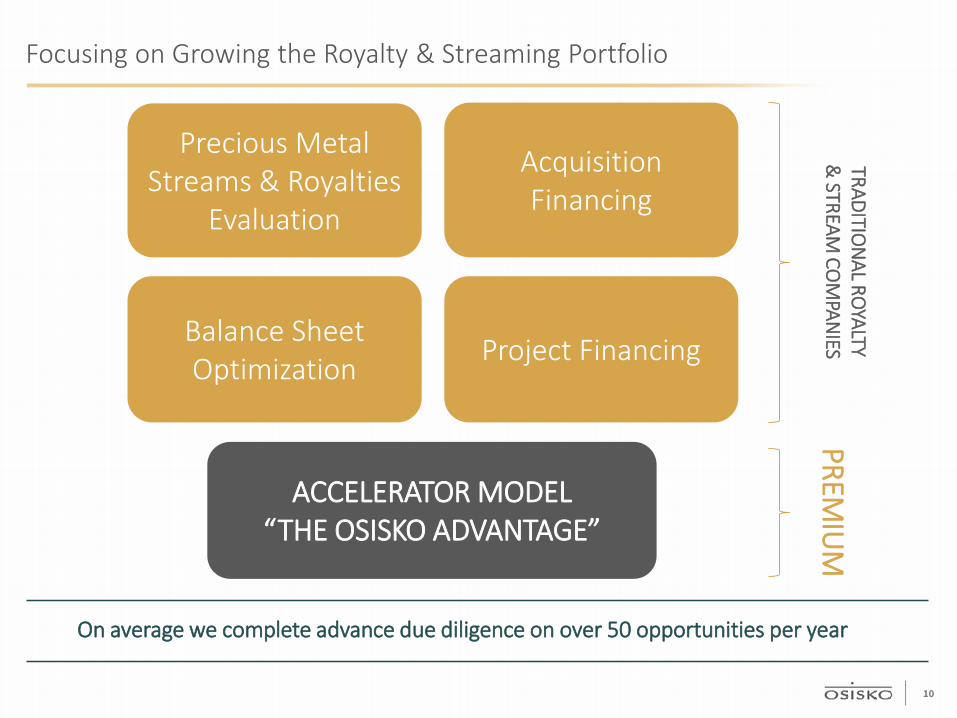

Focusing on Growing the Royalty & Streaming Portfolio

Precious Metal Streams & Royalties

Evaluation

Project Financing

ACCELERATOR MODEL“THE OSISKO ADVANTAGE”

TRADITION

AL ROYALTY

& STREAM

COM

PANIES

PREMIU

M

Balance Sheet Optimization

Acquisition Financing

On average we complete advance due diligence on over 50 opportunities per year

10

(C$ millions) Sept 30, 2016

CASH & CASH EQUIVALENTS $392.7

CONVERTIBLE DEBT $45.6

TOTAL ASSETS $1,399.0

EQUITY $1,200.7

Financial Position

~$600MIN CASH & AVAILABLE CREDIT

STRONG CASH POSITION

Well positioned to compete and add quality assets

STRONG FINANCIAL PARTNERS

11

NEW NYSE LISTING

July 6, 2016

12

Producing Royalties

ÉLÉONORE2.0-3.5% NSR

ISLAND GOLD1.7%-2.55% NSR

VEZZA5% NSR – 40% NPI

CANADIAN MALARTIC5% NSR

IRON ORE COMPANY OF CANADA (LIF)0.7% PASS-THROUGH SALES ROYALTY

13

OPERATORS: Agnico Eagle (50%) / Yamana Gold (50%)

LOCATION: Malartic, Québec

RESERVES: Current reserves of 7.72 M oz Au1

ROYALTY:

5% NSR royalty $0.40/tonne on milled ore from

outside the current property area for life of mill starting in June 2021

2015 PRODUCTION: 572.0 k oz

YTD 2016 PRODUCTION: 445.1 K oz2 (152.9 K oz for Q3)

GUIDANCE: 2016: 560 to 580 k oz 2017: 590 to 600 k oz 2018: 610 k oz

OSISKO ATTRIBUTABLE GOLD OUNCES:

2016: 28.0 to 29.0 k oz 2017: 29.5 to 30.0 k oz 2018: 30.5 k oz

1. See Appendix A for full disclosure on Reserves & Resources.2. Based on Agnico Eagle’s press release dated October 26th, 2016, titled: “Agnico Eagle Reports Third Quarter 2016 Results:…”.

CANADIAN MALARTIC – 5% NSR

THE LARGEST GOLD MINE IN

CANADA

Canadian MalarticProduction (k oz Au)

560-580 k oz outlook

2016

Osisko Gold Royalties Attributable Royalty

Ounces (k oz Au)

28.0-29.0 k oz outlook

2016

YTD: 445.1 K oz09/30/2016

YTD: 22.0 K oz09/30/2016

14

CANADIAN MALARTIC EXPLORATION | ODYSSEY NORTH & SOUTH

113 holes (89,774 metres) completed Showing similarities to the Goldex mine deposit in terms of grade and potential

amenability to underground bulk mining Odyssey North has been traced from a depth of 600 to 1,300 metres below surface

along a strike length of approximately 1.5 kilometres Odyssey South currently has a strike length of 0.5 kilometres, and has been located

between approximately 200 and 550 metres below surface Additional drilling totalling $5.5 million (35,000 metres) has been added to the original

budget of $8.0 million (60,000 metres) for a total of $13.5 million for 2016

OSISKO HOLDS A 5% NSR ROYALTY ON THE ODYSSEY SOUTH ZONE AND A 3% NSR ROYALTY ON THE ODYSSEY NORTH ZONE

Initial inferred mineral resource estimate for the Odyssey zones expected in Q1 2017

15

CANADIAN MALARTIC EXPLORATION | ODYSSEY NORTH & SOUTH

Source: Agnico Eagle 16

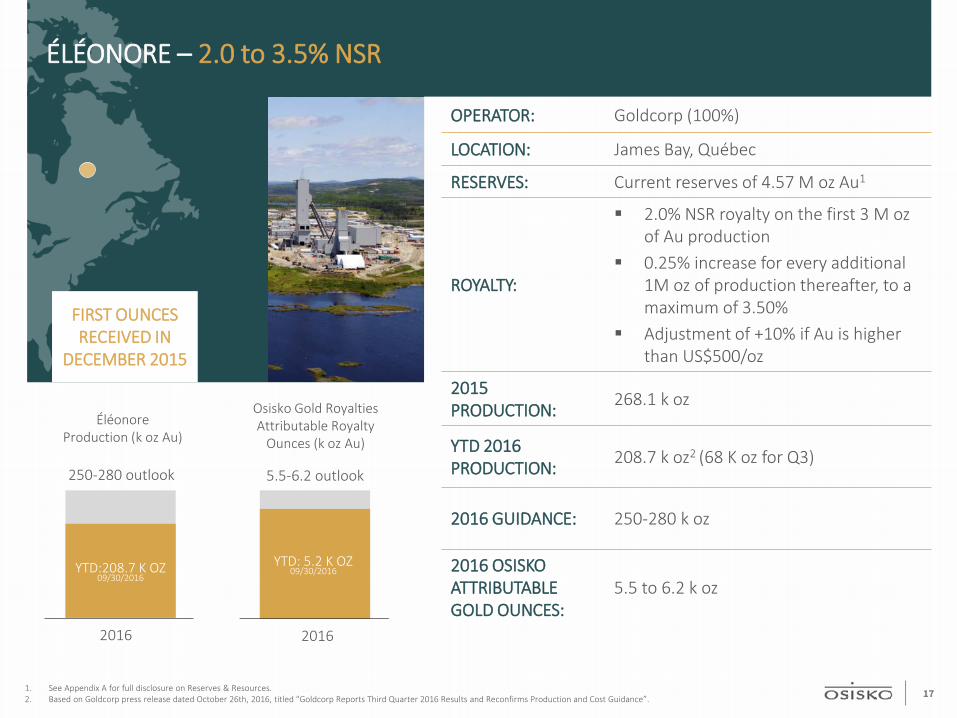

1. See Appendix A for full disclosure on Reserves & Resources.2. Based on Goldcorp press release dated October 26th, 2016, titled “Goldcorp Reports Third Quarter 2016 Results and Reconfirms Production and Cost Guidance”.

OPERATOR: Goldcorp (100%)

LOCATION: James Bay, Québec

RESERVES: Current reserves of 4.57 M oz Au1

ROYALTY:

2.0% NSR royalty on the first 3 M ozof Au production

0.25% increase for every additional 1M oz of production thereafter, to a maximum of 3.50%

Adjustment of +10% if Au is higher than US$500/oz

2015 PRODUCTION: 268.1 k oz

YTD 2016 PRODUCTION: 208.7 k oz2 (68 K oz for Q3)

2016 GUIDANCE: 250-280 k oz

2016 OSISKO ATTRIBUTABLE GOLD OUNCES:

5.5 to 6.2 k oz

ÉLÉONORE – 2.0 to 3.5% NSR

FIRST OUNCES RECEIVED IN

DECEMBER 2015

ÉléonoreProduction (k oz Au)

250-280 outlook

2016

Osisko Gold Royalties Attributable Royalty

Ounces (k oz Au)

5.5-6.2 outlook

2016

YTD:208.7 K OZ09/30/2016

YTD: 5.2 K OZ09/30/2016

17

Source: Goldcorp public disclosure.

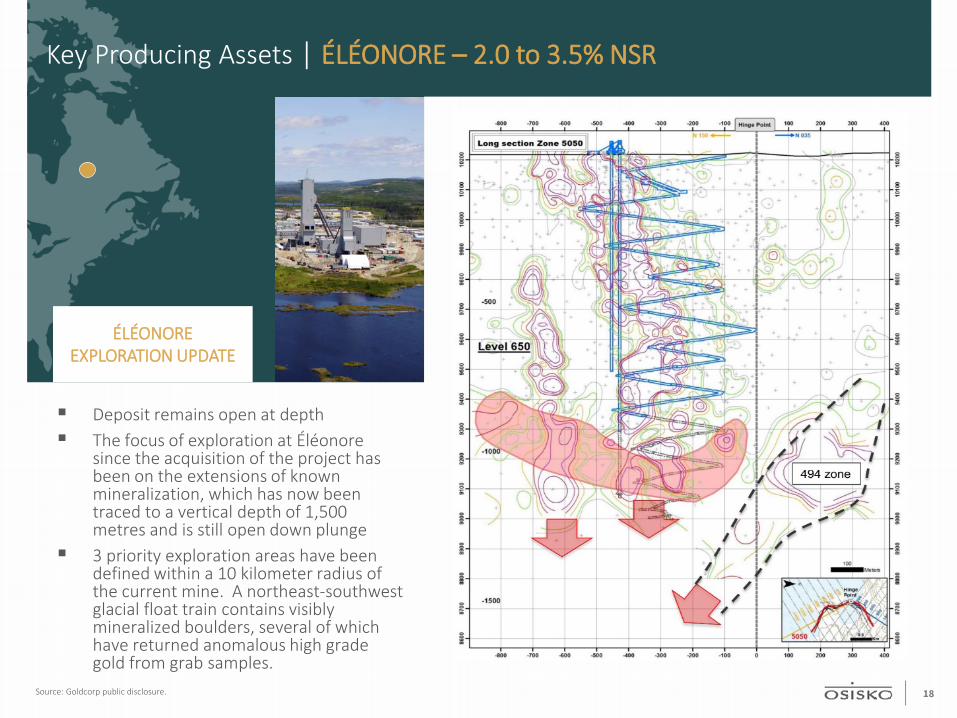

Deposit remains open at depth The focus of exploration at Éléonore

since the acquisition of the project has been on the extensions of known mineralization, which has now been traced to a vertical depth of 1,500 metres and is still open down plunge

3 priority exploration areas have been defined within a 10 kilometer radius of the current mine. A northeast-southwest glacial float train contains visibly mineralized boulders, several of which have returned anomalous high grade gold from grab samples.

ÉLÉONOREEXPLORATION UPDATE

Key Producing Assets | ÉLÉONORE – 2.0 to 3.5% NSR

18

Operating since 2007 Recently announced an updated PEA

on Deep resources at the Island Gold Mine

2015 production: 55,040 oz Au 142,000m Phase 2 drilling campaign

underway 1,081 oz of gold earned for the first

nine months of 2016

9.8% equity position in Labrador Iron Ore Royalty Corporation (“LIF”)

Investment in LIF provides exposure to Iron Ore Canada (“IOC”)

– 7.0% top-line royalty

– 15% equity interest in IOC

– $0.10/t commission on all iron ore sales by IOC

Equivalent to 0.7% pass-through sales royalty

Operating since 1954

$4.7 million in dividends received for the first nine months of 2016

IRON ORE COMPANY OF CANADA (IOC)

0.7% PASS-THROUGH SALES ROYALTY

ISLAND GOLD 1.7%-2.55%

NSR

Producing Royalties

Operated by Ressources Nottaway inc. (private company)

The property is located 25km from Matagami, Québec

Custom milling at IAMGOLD’s Westwood (Doyon) facility

VEZZA5% NSR40% NPI

19

KEY GROWTH ROYALTIES

ODYSSEY NORTH3% NSRUPPER BEAVER

KIRKLAND LAKE CAMP2% NSR

CARIBOO1.5% NSR

MARBAN0.425% NSR

LAMAQUE1.7% NSR

PANDORA2% NSR

WINDFALL1.5% NSR

HERMOSA1% NSR

HORNE 51% NSR

GUERRERO9,600 KM2 AREA IN

GUERRERO, MEXICO

EXPLORATION PROPERTIES

OVER 50 ROYALTIES IN THE

PORTFOLIO TO PROVIDE UPSIDE

TO “OR” SHAREHOLDERS

FOCUSED ON NORTH AMERICA

JAMES BAY – LABRADOR TROUGH PROPERTIES

(OSK)1.5% - 3.5%

COULON POLYMETALLIC

PROJECT

20

Positive Royalty Portfolio Developments

HORNE 5ROYALTY: 1% NSR Significant increase in resource: 7.1 M oz AuEq M&I / 1.7 M oz AuEq Inferred $36.5 M bought deal financing completed in November 2016 35,000 m of drilling in 2016 will expand project footprint.

ODYSSEYROYALTY: 3-5% NSR 89,774 m drilled in 2016 Maiden resource expected in Q1 2017

HERMOSA

ROYALTY: 1% NSR Maiden resource announced on Taylor deposit:

31.1 M tons at 10.9% ZnEq Indicated / 82.7 M tons at 11.1% ZnEq Inferred Deposit still open in all directions Aggressive drilling to continue on the property

WINDFALLROYALTY: 1.5% NSR 150,000 m drilling program ongoing Advanced exploration programs ongoing to define deposit

MARBANROYALTY: 0.425% NSR New resource announced in 2016: 1.48 M oz M&I / 0.13 M oz Inferred 20,000 m drilling in 2016

Significant progress on Osisko’s royalty properties; Over 50 royalties in Osisko’s portfolio

ISLAND GOLDROYALTY: 1.7-2.55% NSR 172,000 m drilling campaign PEA underway for expansion to 1,100 tpd Increased 2016 gold production guidance to 75-80 k oz

21

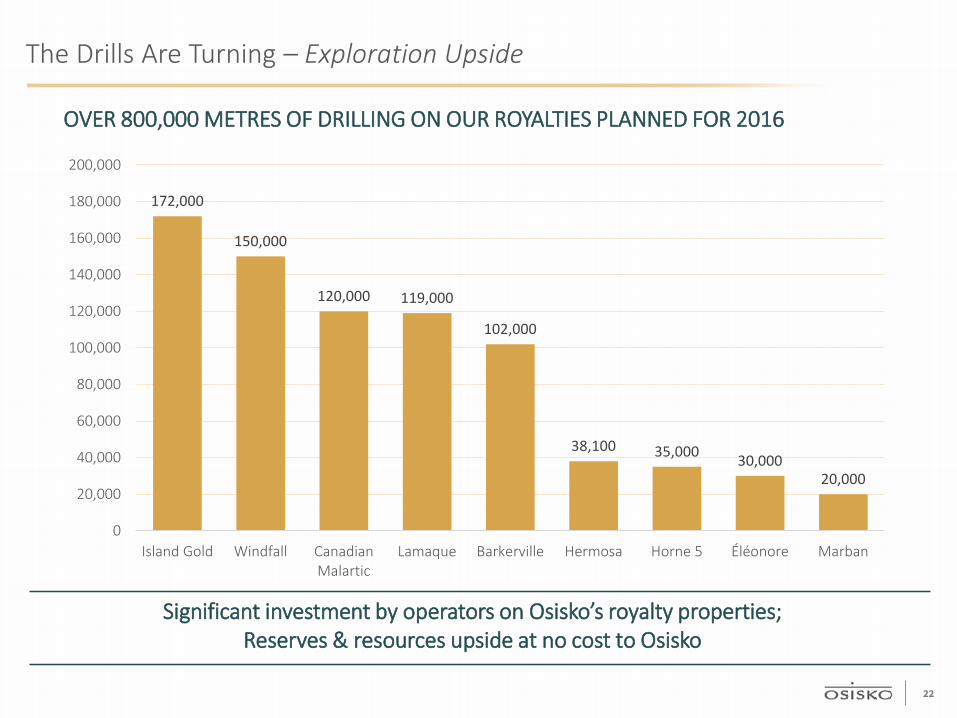

Significant investment by operators on Osisko’s royalty properties; Reserves & resources upside at no cost to Osisko

The Drills Are Turning – Exploration Upside

OVER 800,000 METRES OF DRILLING ON OUR ROYALTIES PLANNED FOR 2016

172,000

150,000

120,000 119,000

102,000

38,100 35,000 30,00020,000

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

200,000

Island Gold Windfall CanadianMalartic

Lamaque Barkerville Hermosa Horne 5 Éléonore Marban

22

Accelerator Model

FUNDAMENTAL CONCEPT

Use Osisko’s solid experience in exploration, engineering, construction & financing to advance projects on which Osisko owns royalties

Support accelerator companies at board level and key management roles Maintain key shareholder position to drive further benefits to OR

Tax efficient way of deploying capital as investments in flow-through shares shelter royalty income

KEY ACCELERATOR COMPANIES

OR Representation:

CEO: Luc LessardCFO: Vincent MetcalfeChairman: Sean RoosenEquity Investment: $3.7 millionRoyalty Investment: $10.0 millionRoyalty: 1% NSRStream: Ability to apply royalty as

prepayment against a gold/silver stream

OR Representation:

CEO: John BurzynskiChairman: Sean RoosenEquity Investment: $28.2 millionRoyalty Investment: $9.8 millionRoyalties: 1.5% NSR Windfall

0.425% Marban

23

Accelerator Model – Acquiring Royalties at Discounted Valuations

Net Cost of Royalty Purchase at Sept 30, 2016 (C$ M)

Purchased a 1.5% NSR in February 2016 Purchased a 1% NSR in April 2016

1. Non-IFRS measure representing the difference between the fair value of marketable securities less acquisition cost

$25.0

$18.1 1

$6.9

Cost to purchaseroyalty

Unrealized gain onequity investment

Net cost of royalty

$10.0

$17.9 1

($7.9)Cost to purchase

royaltyUnrealized gain onequity investment

Net cost of royalty

24

Significant Value in Investment Portfolio

Value of Investment Portfolio1 (C$ M)

Unrealized gain2 of approximately $114 million at quarter end

1. Fair value of marketable securities in associates and other as at September 30, 2016, excluding Labrador Iron Ore Royalty Corporation2. Non-IFRS measure representing the difference between the fair value of marketable securities less acquisition cost

$148.6

$262.5

Cost Base Market Value at Sep. 30, 2016

25

Key Objectives – Next 12 Months

Add Long Life Cornerstone Cash Flow Asset

Continue to develop accelerator model through Supporting Project Financing Opportunities

26

Invest in Osisko

OVER 50ROYALTIES

~$600MIN CASH & AVAILABLE

CREDIT

DIVIDEND YIELD

1.2%

TWO OF THE PREMIER

ROYALTY ASSETS IN THE GOLD

SECTOR

GOLD FOCUSED TRACK RECORD OF SUCCESS

30,125ZERO-COST ozIN CANADA IN

2015

34,500 to 37,200 oz

ATTRIBUTABLE GOLD OUNCES FOR

2016

ON TRACK TO ACHIEVE GUIDANCE WELL POSITIONED TO COMPETE AND ADD QUALITY ASSETS

27

Appendix A – Reserves & Resources

Appendix A – Reserves and Resources

1. Agnico Eagle and Yamana public disclosure – as at December 31, 20152. See Goldcorp press release dated October 26, 2016, titled “Goldcorp Reports Third Quarter 2016 Results and Reconfirms Production and Cost Guidance”.3. See Richmont press release dated February 9, 2016, titled “Richmont Increases Mineral Reserves by 187% and Island Gold Mine Increases Mineral Reserves by 206%, With a 29% Increase in Reserve Grade”

CANADIAN MALARTIC1

RESERVES*

CATEGORY AU GRADE (G/T) AU (M OZ) TONNES (MT)

Proven 0.97 1.72 54.9

Probable 1.12 6.00 166.6

Total Proven & Probable 1.08 7.73 221.5

*Cut-off grade: 0.345-0.351 g/t | Gold Price: $1,150/oz Au

GLOBAL RESOURCES (EXCLUDING RESERVES)*

CATEGORY AU GRADE (G/T) AU (M OZ) TONNES (MT)

Measured 1.32 0.15 3.5

Indicated 1.55 1.10 22.2

Total Meas. & Ind. 1.51 1.25 25.7

Inferred 1.47 0.43 9.0*Cut-off grade: 0.34-0.40 g/t and 1.0 g/t below open pit | Gold Price: $1,150/oz Au | exchange rate of CAN$1.24 = US$1.00

ÉLÉONORE2

RESERVES*

CATEGORY AU GRADE (G/T) AU (M OZ) TONNES (MT)

Total Proven & Probable 6.07 4.57 23.44

GLOBAL RESOURCES (EXCLUDING RESERVES)

CATEGORY AU GRADE (G/T) AU (M OZ) TONNES (MT)

Total Meas. & Ind. 5.66 0.93 5.14

Inferred 7.52 2.35 9.73

ISLAND GOLD3

RESERVES - ABOVE 400M*

CATEGORY AU GRADE (G/T) AU (K OZ) TONNES (KT)

Proven 7.00 21.80 97.0

Probable 6.88 54.90 248.0

Total Proven & Probable 6.91 76.70 345.0

GLOBAL RESOURCES (EXCLUDING RESERVES) – ABOVE 400M*

CATEGORY AU GRADE (G/T) AU (K OZ) TONNES (KT)

Measured 5.80 1.35 7.5

Indicated 6.96 52.7 235.5

Total Meas. & Ind. 6.92 54.1 243.0

Inferred 7.44 98.7 412.5

*Based on a gold price of US$1,300/oz and an exchange rate of CAN$1.2037 = US$1.00.

RESERVES – BELOW 400M*

CATEGORY AU GRADE (G/T) AU (K OZ) TONNES (KT)

Proven 7.72 66.1 266.5

Probable 8.66 418.9 1,504.0

Total Proven & Probable 8.52 485.0 1,770.5

GLOBAL RESOURCES (EXCLUDING RESERVES) – BELOW 400M*

CATEGORY AU GRADE (G/T) AU (K OZ) TONNES (KT)

Indicated 5.20 17.65 105.5

Inferred 8.67 669.35 2,402.5

*Based on a gold price of US$1,300/oz and an exchange rate of CAN$1.2037 = US$1.00.

29

Appendix B – Q3 Results

2016 Q3 Results

3 MONTHS ENDED

(C$ 000) Sept 30, 2016 Sept 30, 2015

GOLD PRODUCTION (oz) 9,902 8,264

SILVER PRODUCTION (oz) 9,234 7,780

REALIZED GOLD PRICE (C$ per oz) 1,743 1,485

REVENUES $17,570 $11,724

DIVIDEND INCOME $1,572 $1,560

NET CASH FLOW FROM OPERATIONS $14,978 $12,594

NET EARNINGS $17,675 $9,809

NET EARNINGS PER SHARE - BASIC $0.17 $0.10

Investments in flow-through shares (accelerator model) in 2016have contributed to offsetting taxes on royalty income

31