out-of-sample performance of mutual fund predictorschristoj/pdf/jones_mo.pdfout-of-sample...

TRANSCRIPT

Out-of-sample performance of mutual fund predictors∗

Christopher S. Jones Haitao Mo

Marshall School of Business Ourso College of Business

University of Southern California Louisiana State University

[email protected] [email protected]

January 2016

∗We are grateful to the participants of seminars at the University of Southern California. Data on hedgefund assets under management were kindly provided by Matti Suominen. All errors remain our own.

Out-of-sample performance of mutual fund predictors

Abstract

This study analyzes the out-of-sample performance of a variety of variables

shown in prior work to forecast future mutual fund alphas. Overall, we find that

the degree of predictability, as measured by alpha spreads from quintile sorts

of by cross-sectional regression slopes, falls by at least half following the end of

the sample and perhaps by 75% after publication. This decline is not driven

by changes in fund flows or expenses, suggesting that it is not explained by the

model of Berk and Green (2004). Rather, we find that the shrinking of alpha

spreads is associated with higher levels of arbitrage activity, and that this largely

explains the out-of-sample decline.

Keywords: mutual funds, out-of-sample performance, market efficiency

1 Introduction

A central question in the mutual fund literature is whether funds with positive alpha, net of

fees and costs, can be distinguished, ex ante, from those with negative alpha. An affirmative

answer to the question requires that some variable in the investor’s information set be asso-

ciated with future alphas. To this end, a number of studies have investigated the ability of

various theoretically or intuitively motivated variables to predict future fund alphas, and a

modest number of variables that appear to do so have now been found. Whether these alpha

predictors continue to perform outside of their original samples is a question we answer in

this paper.

In the model of Berk and Green (2004), the alphas that investors perceive given available

information is zero. Alphas that are above zero are eliminated by higher fees and disec-

onomies of scale resulting from fund inflows. If the alpha predictors we study are part of the

investor’s information set, at least after the studies that propose them are published, then

their effectiveness should be expected to decline out of sample.

In addition to highlighting limitations of the Berk and Green hypothesis, continued per-

formance of alpha predictors out of sample would also allow us to rule out the possibility of

data mining as the explanation of mutual fund alpha prediction. Academic studies would

then appear to offer some potential in guiding mutual fund investors towards better perfor-

mance.

To the extent that performance does decline out of sample, then an analysis of this

decline may help us to understand the forces that cause apparent mispricing to disappear

over time, one possibility being that alphas converge to zero in the manner that Berk and

Green suggest. An alternative is that a steady increase in arbitrage activity over the last

several decades has made stock markets more efficient, and that alpha generation has become

more difficult for mutual fund manager.

Chordia et al. (2014) investigate how the returns to asset pricing anomalies (momentum,

value, accruals, etc.) are related to various measures of arbitrage activity. Across a number of

anomalies, they find that the average return is reduced substantially by an increase in short

interest, the assets under management of hedge funds, and aggregate share turnover. We

1

follow their work by analyzing how these arbitrage activity proxies are related to abnormal

fund returns.

We find that alpha predictors largely fail, out of sample, to replicate their in-sample

success. At least half of the alpha spread generated by predictors proposed in the literature

disappears out of sample. In some specification, that number rises to 75%. Thus, to a

potential mutual fund investor, advice from the academic literature on mutual funds is at

best moderately useful, though in the brief window between the end of the sample period

and the date of publication the situation is somewhat more positive. In this window, which

lasts around four years on average, the power of the average alpha predictor falls only by

30-40%.

The finding that alpha predictability declines gradually rather than immediately following

the end of the original sample makes it unlikely that data mining is a primary explanation

for in-sample predictability. Another possibility, discussed above, is that academic studies

foster learning by mutual fund investors and management. The resulting changes in beliefs

about fund manager skill trigger fund flows and fee adjustments that, according to Berk

and Green (2004), should be expected to cause alphas to shrink to zero. We investigate

the relation between alpha predictors and flows and find a significant positive relation that

does not change out-of-sample. The relation between alpha predictors and fees is generally

negative, becoming significantly more negative out-of-sample. This is the opposite of what

the Berk and Green model would imply, suggesting that the decline in alpha predictability

is not driven by investor learning.

Finally, we examine the relation between alphas and arbitrage activity. Here we find

strong evidence that higher levels of arbitrage are associated with smaller alpha spreads.

Part of this effect is consistent with the view that market efficiency has in general increased

over the sample we examine as the result of a trend towards greater arbitrage activity. How-

ever, the relation between arbitrage and alphas also holds for detrended arbitrage activity

measures, suggesting cyclical variation in arbitrage forces are important as well. When we

include both out-of-sample and arbitrage effects within the same specification, it is arbitrage

activity that most often retains significance. This suggests to us that poor out-of-sample

performance is at least mostly the result of an overall trend towards greater market efficiency

2

over our sample.

Our paper relates to several strands of the finance literature. Most clearly, we follow a

significant literature on mutual fund performance prediction, which we review in Section II.

Our paper is also closely related to work on the persistence of asset pricing anomalies. In

addition to the work of Chordia et al. (2014), a number of studies have explored how the ex-

pected returns of anomaly strategies have held up since the original papers documenting their

existence. Schwert (2003) shows, for example, that the size anomaly largely faded following

its discovery in the early 1980s. Jones and Pomorski (2015) analyze several anomalies from

the perspective of a Bayesian investor, finding that out-of-sample investment performance

is improved by allowing, ex ante, for the possibility that the anomaly return may diminish

over time. Finally, in a study closely related to the current one, McLean and Pontiff (2015)

examine the out-of-sample performance of 97 variables shown to predict equity returns and

find a substantial decline relative to in sample averages.

This paper is also related to work seeking to characterize the distribution of mutual

fund managers. This work has generally found that the average fund alpha, net of fees and

expenses, is negative, but there is substantial disagreement over the fraction of managers

that do provide positive alphas. In the Bayesian framework of Jones and Shanken (2005) and

the bootstrap analysis of Kosowski et al. (2006), a substantial minority of funds do appear to

outperform. In contrast, Fama and French (2010) conclude that funds with positive alphas

are highly unusual, while Chen and Ferson (2015) find that they are largely nonexistent.

Interestingly, in a similar study, Barras et al. (2010) find a substantial fraction of funds with

positive alphas prior to 1996, but find that almost no positive alphas existed by 2006. Our

finding that arbitrage activity is associated with declining alpha spreads is consistent with

this observation.

In the following section we discuss the measurement of mutual fund alpha and the repli-

cation of mutual fund alpha predictors. In Section 3 we assess the out-of-sample performance

of these predictors. We test the hypotheses on flows and expenses in Section 4 and examine

the relation between alphas and arbitrage activity in Section 5. Section 6 concludes.

3

2 Mutual fund alpha predictors

A variety of variables have been found to predict future fund performance. Most of the

papers that document this predictability were published following the introduction of the

CRSP Survivor-Bias-Free US Mutual Fund database, which first appeared in the work of

Carhart (1997). The only predictor that predates this database is the lagged one-year return,

which Hendricks et al. (1993) showed to forecast future returns.

Carhart’s 1997 paper contained a number of results that were new to the literature

and that we analyze here. He showed, for instance, that expense ratios and turnover were

negatively related to future fund performance. While confirming the results of Hendricks

et al. (1993), Carhart found that past alphas from his own four-factor model were more

useful in forecasting future risk-adjusted performance.

There is also some evidence that fund size is related to future performance. Chen et al.

(2004) find that larger funds perform worse, particularly for small-cap funds, while fund

family size is positively related to performance. While the interpretation of this evidence is

somewhat controversial (see Pastor et al. (2015)) in that it is not clear whether performance

is an accurate reflection of managerial skill, the empirical relation between alphas and funds

size appears relatively strong.

The tendency of mutual funds to deviate from benchmark indexes also appears be related

to future performance. These deviations can be measured from fund holdings, as in the active

share measure of Cremers and Petajisto (2009). They can also be measured from the R2

of the fund’s returns on one or more benchmarks, as in Amihud and Goyenko (2013). In

both cases, funds that deviate more from their benchmarks perform better, suggesting that

the greater “conviction” of managers who make larger stock-specific bets is associated with

ability.

Several other measures are designed to identify managers that are more likely to display

ability in stock selection. Kacperczyk et al. (2005) argue that fund managers may have

informational advantages only in some industries, so that industry concentration indicates

investment skill. Kacperczyk and Seru (2007) find that managers who appear to rely more

on public information when making portfolio decisions tend to perform worse. Christoffersen

4

and Sarkissian (2009) find evidence that funds in larger cities, where private information may

be more accessible and knowledge spillovers are more likely, perform better than funds in

smaller cities. Finally, funds whose holdings resemble other funds with strong performance

records have been shown by Cohen et al. (2005) to offer superior performance.

Several performance measures have been derived by comparing the actual performance

of the mutual fund to the performance of the portfolio formed on the basis of the most

recent quarter-end fund holdings. The so called “return gap,” proposed by Kacperczyk et al.

(2008), is defined as the difference between the actual fund returns and the holdings-based

returns. A measure of risk shifting can be obtained, as in Huang et al. (2011), by computing

the difference between the volatility of the fund’s actual returns to that of the holdings-based

portfolio. These studies show that a higher return gap is positively related to future fund

returns, while funds that exhibit greater risk shifting perform poorly. Both results are of a

magnitude that is economically important and highly significant.

Other performance predictors are based on asset market liquidity. Da et al. (2010) find

that funds that trade stocks with a high likelihood of informed trading (the PIN measure of

Easley et al., 1996) perform better than those that do not. Liquidity at the aggregate level

also appears to be important. Cao et al. (2013) find that funds that appear to time market

liquidity by increasing market beta prior to periods of high liquidity on average perform

better.

Finally, several performance measures do not use additional fund-level characteristics

but seek to predict future fund performance as a result of improvements in methodology.

Mamaysky et al. (2007) show how back testing can be used to better identify funds with

nonzero alphas. Kacperczyk et al. (2014) propose a skill index that combines both market

timing and stock picking abilities and show that it strongly forecasts future fund returns.

In total, we find 20 different predictors from 17 papers. These 20 predictors represent

the starting point of our analysis.

2.1 Mutual fund sample

We obtain mutual fund returns (monthly) and fund characteristics such as expenses, total

net assets (TNA), fund portfolio turnovers, and investment styles, from Center for Research

5

in Security Prices Mutual Fund (CRSP MF) database, from January 1961 to January 2013.

Fund returns are net of expenses but not of loads. Quarterly fund equity holdings data

from 1980 to 2012 are from Thomson Reuters and, when we merge it with CRSP MF we

use MFLINK. We exclude fixed income, international, money market, sector, index, and

balanced funds, focusing on active US equity funds.1 We subject the fund data to a number

of screens to mitigate omission bias (Elton et al., 2002) and incubation and back-fill bias

(Evans, 2010). We exclude observations prior to the first offer dates of funds, those for which

the names of the funds are missing in the CRSP MF database, and those before the fund’s

TNA reaches $15 million. To prevent the impact of outliers when holdings data are used, we

require a fund to hold at least 10 stocks to be eligible in our sample. We combine multiple

share classes for each fund, focusing on the TNA-weighted aggregate share class.

To construct various fund predictors, we obtain additional data: CRSP stock price data,

constituents of nineteen indices from three families (S&P/Barra, Russell, and Wilshire) as

used in Cremers and Petajisto (2009), daily fund returns data from CRSP MF, analysts’

recommendation data from IBES, and monthly/daily data of Fama-French-Carhart four

factors from Kenneth French’s website. For example, we need the data of index constituents

to construct active shareness (Cremers and Petajisto, 2009), the analysts’ recommendation

data to construct reliance on public information (Kacperczyk and Seru, 2007), and the daily

fund returns to construct R-square (Amihud and Goyenko, 2013) and risk shifting (Huang

et al., 2011).

There are 3514 unique funds in our final sample from January 1961 to January 2013 and

the average number of months for a fund in our sample is 128.

1 We identify and remove index funds both by CRSP index fund flag and by searching the funds’ nameswith key words “exchange-traded|exchange traded|etf|dfa|index|inde|indx|inx|idx|dow jones|ishare|s&p|s&p|s& p|s & p|500|WILSHIRE|RUSSELL|RUSS|MSCI.” US equity funds are defined as those with pol-icy code CS; Weisenberger objective codes G, G-I, GCI, LTG, MCG, SCG, IEQ, I, I-G, SCG, AGG, G, G-S,S-G, GRO, LTG, I, I-S, IEQ, ING, GCI, G-I, G-I-S, G-S-I, I-G, I-G-S, I-S-G, S-G-I, S-I-G, GRI, MCG;SI objective codes AGG, GMC, GRI, GRO, ING, SCG; Lipper class codes EIEI, G, I, GI, LCCE, LCGE,LCVE, MCCE, MCGE, MCVE, MLCE, MLGE, MLVE, SCCE, SCGE, SCVE; or an average equity holdingbetween 80% and 105% in the fund asset.

6

2.2 Computing alpha spreads

The ultimate object of interest in our study is mutual fund alpha. In order to control for

standard risk exposures and to allow alphas to vary over time, we follow Carhart (1997)

by computing alphas based on rolling window estimates of factor betas. Specifically, for

each fund at each date, we use the previous 36 months to estimate the betas on the Fama

and French (1993) and Carhart factors. We then use those betas to risk-adjust the current

month’s excess return. Given the lagged nature of the risk adjustment, we refer to the result

as the “ex post alpha.” We label this quantity for fund i and time t as αit.

A large part of our analysis is focused on the behavior of spreads in mutual fund alphas.

These are formed by measuring the relation between fund alphas and some fund-level pre-

dictor xijt, where the i subscript denotes the fund and j the predictor. For compactness

of notation we specify the date as t but note that the predictor is always known as of the

end of month t − 1. In all cases, the predictor variable is defined such that high values are

associated with good performance and low values with bad performance. This determination

is made on the basis of the original paper in which the predictor was proposed, and we find

no cases in which the sign of the prediction changes when we replicate the original paper’s

results.

We measure alpha spreads in two ways, by sorting and by cross-sectional regression.

Sort-based alphas are computed by sorting on xijt and computing the difference between the

equal weighted average alphas in the top and bottom quintiles. For shorthand we denote

this spread as “Q5-Q1.” We also use cross-sectional regression to produce alpha spreads. In

this approach, we simply run univariate monthly regressions of fund alphas on the predictor.

The slope coefficients of these regressions constitute the “CSR” alpha spread.

We feel that including both types of alpha spread is potentially important. Cross-sectional

regression maximizes dispersion in the predictor, which potentially allows funds with very

large or very small values of the predictor to have more influence on the spread. This

is appropriate if we believe that those funds are more heavily affected by whatever force

underlies the effectivenes of that predictor. This is undesirable, however, if the relation

between predictor and alpha is nonlinear. In this case, computing spreads based on extreme

7

quintiles makes more sense. Given no guidance to choose one approach or the other, we

include them both.

2.3 Criteria for including predictors

As discussed in Section 2, we have identified 20 predictors that have been found in the mutual

fund literature to forecast future fund performance. Unfortunately, four are impossible to

replicate given that they rely on proprietary or hand collected data.2 This leaves us with 16

predictors that we were able to analyze.

Since our goal is to understand the out-of-sample performance of these predictors, we

must first document in-sample performance. We follow McLean and Pontiff (2015) in re-

quiring that predictors exhibit a degree of success in-sample that falls somewhat short of

statistical significance. Specifically, we require that the average in-sample alpha spread have

a t-statistic above 1.4.3 For the extreme quintile (Q5-Q1) results, this t-statistic is computed

on the basis of in-sample Q5-Q1 spreads. For the cross-sectional regression (CSR) results,

the t-statistic is based on CSR spreads.

Out of the 16 predictors we consider, 10 exceed the t-statistic threshold for both Q5-Q1

and CSR. Two predictors meet the criteria for Q5-Q1 but not CSR, and two meet the criteria

for CSR but not Q5-Q1. Two predictors have t-statistics below 1.4 for both Q5-Q1 and CSR.

It is important to keep in mind that a failure to obtain a t-statistic of 1.4 or more does

not indicate that the original study is incorrect, as many studies employ methods that are

different than the ones we use here. In some studies, for instance, predictors are shown to

be significant only in the context of regressions in which other control variables are include.

In addition, the data on which we base our analysis can be different from that used in prior

work. The CRSP Mutual Fund Database, for example, has undergone several significant

revisions.

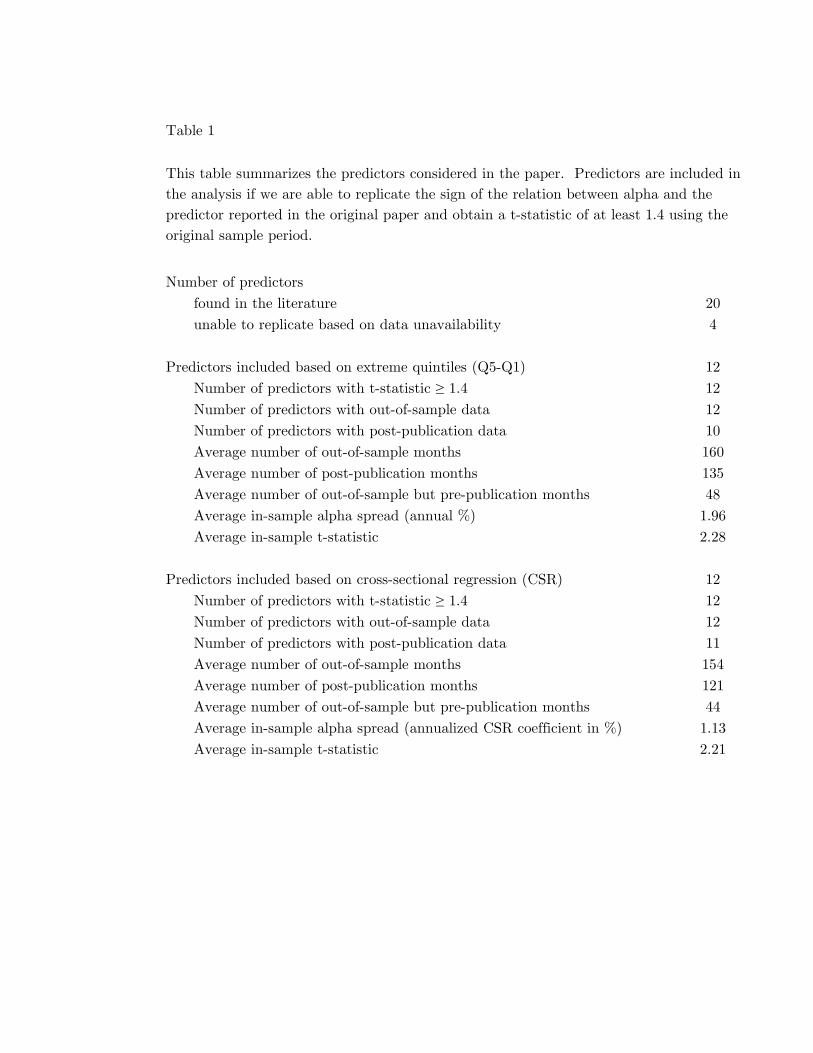

Table 1 summarizes the process of in-sample replication. On average, the Q5-Q1 sort

produces an in-sample alpha spread of 1.96% per year, with an average t-statistic of 2.28.

2 In these cases obtaining data from the authors of the original studies does not help us since the datasetsneed to be extended beyond the original sample periods.

3 McLean and Pontiff (2015) require a t-statistic of 1.5 or more. We use a slightly lower cutoff so thattwo more predictors can be included.

8

The predictors included in the Q5-Q1 analysis have an average of 160 months of data past

the end of their sample period and 135 months of data after their date of publication.

The interpretation of CSR-based alpha spreads is not as straightforward. Recall that the

CSR-based alpha spread is the slope of a cross-sectional regression. Because slopes computed

in this way would not be comparable, for this table we normalize predictors to have zero

mean and unit standard deviation. The average CSR alpha spread is the average coefficient

on these normalized predictors, multiplied by 12. The 1.13 value implies, approximately,

that a one standard deviation increase in a predictor increases average fund alpha by 1.13%

per year.

3 Post-sample performance

The central question we answer in this paper is whether mutual fund alpha predictors con-

tinue to work out of sample. We address this question in several ways. We first follow

McLean and Pontiff (2015) by analyzing how alpha spreads change following the end of the

in-sample period. We then consider a new framework for analyzing predictability in a panel

of mutual funds.

3.1 Predictor-level averages

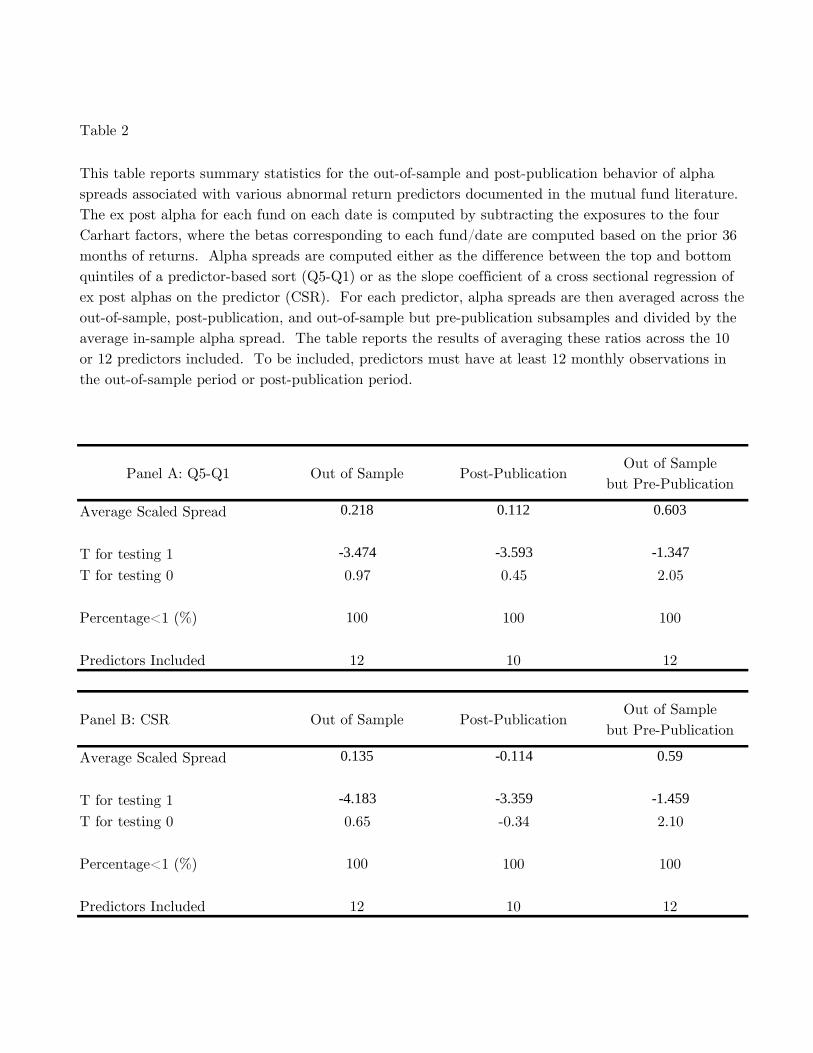

Given the alpha spread corresponding to each predictor in each month, we can analyze the

out-of-sample behavior of alpha spreads simply by dividing the average out-of-sample spread

by the average in-sample spread of the same predictor. The first column of Table 2 contains

the results of doing so. For the Q5-Q1 method, the average scaled spread is just 0.218,

indicating that the out-of-sample spread in alphas is only about 22% of the average in-

sample spread. For the CSR-based method, the average out-of-sample spread is only 13.5%

of its in-sample value. Both of these results suggest that the out-of-sample performance of

mutual fund alpha predictors is at best marginal.

Hypothesis testing for these averages is somewhat suspect. Standard errors are computed

simply by examining the dispersion across the 12 scaled spreads divided by the square root of

12. This measure ignores differences in the volatilities of different spreads, the length of the

9

different out-of-sample periods, and any cross-sectional correlation between alpha spreads

formed on the basis of different predictors. For these reasons, we follow McLean and Pontiff

(2015) by examining similar results in more reliable panel regression setting below, but with

the above caveats in mind we simply note that we cannot reject the null hypothesis that the

ratio of out-of-sample to in-sample alpha spreads is on average zero. We can strongly reject

reject the null hypothesis that the ratio is equal to one.

Table 2 also describes the behavior of alpha spreads following the publication of the

paper on which each predictor is based. If the publication of the paper leads to learning

by mutual fund investors or management companies about which funds are likely to be

better performers, then it is possible that publication may be more closely associated with a

decline in performance. In the Berk and Green (2004) model, this could be accomplished by

investors increasing their holdings of funds with favorable predictors and decreasing holdings

of funds with unfavorable predictors. The model would also predict that as fund companies

are better able to identify which funds are likely to offer superior performance, they alter

fund expense ratios to be more aligned with those assessments.

We find that the performance of the alpha predictors deteriorates further in the post-

publication period, with ratios of out-of-sample to in-sample alpha spreads that are close to

and insignificantly different from zero.

Finally, Table 2 examines the period in between the end of the sample and the date

of publication. While this period is typically short, on average only around 44-48 months,

it paints a much different picture than the other two subsamples. For both methods, the

average alpha spread prior to publication but still out of sample is around 60% of its in-

sample value. This spread is significantly different from zero and insignificantly different

from one.

It is somewhat hazardous to draw strong conclusions given the questionable assumptions

involved in the hypothesis testing thus far, but our tentative findings suggest two interesting

possibilities. One is that out-of-sample performance is poor, which is consistent with fund

investors or management companies learning about how to better predict performance. The

other is that this poor performance is unlikely to be explained, at least primarily, as the

result of data mining, since the magnitude of alpha spreads remains reasonably high at least

10

for a short time out of sample.

3.2 Predictor panel

Given the limitations of the previous analysis, we follow McLean and Pontiff (2015) by

reassessing the out-of-sample performance of mutual fund predictors in a panel regression

setting where all predictors are analyzed jointly. To do so, first define Ajt as the time-t alpha

spread corresponding to predictor j. The dependent variable in the regression is then set

equal to Ajt/Aj, where Aj is the average value of Ajt over the in-sample period of predictor

j.4

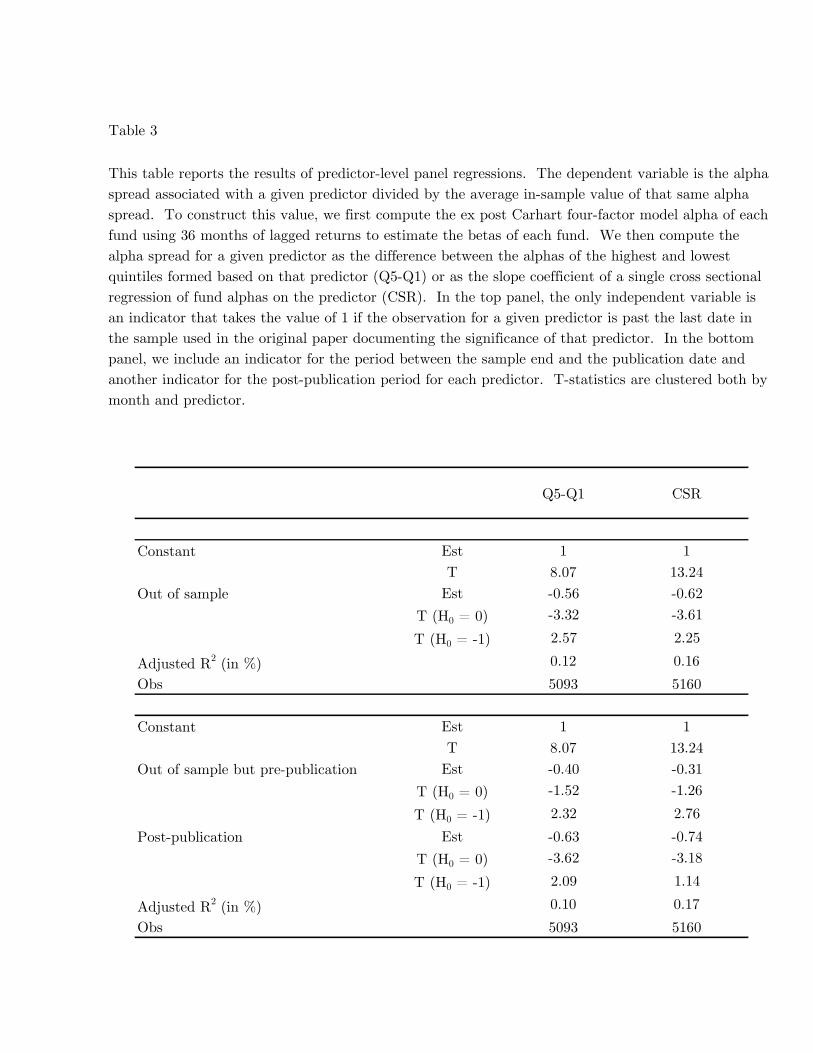

The top panel of Table 3 shows the result of regressing this variable on the indicator

variable Djt, which takes the value of one if predictor j is out of sample as of month t.

In the bottom panel of the table we include separate indicators for the out-of-sample but

pre-publication period and for the post-publication period, both of which differ for each

predictor. The table reports coefficient estimates for these indicator variables as well as

t-statistics that are computed with clustering both by date and by predictor.

In short, results are similar to those from Table 2but are slightly more muted. For

both the Q5-Q1 and CSR methods, the coefficient on the out-of-sample indicator variable is

around -0.6, which implies that the alpha spread shrinks by about 60% on average following

the end of the sample. In this specification, we can easily test the hypothesis of no dete-

rioration in out-of-sample performance (coefficient equal to zero) as well as the hypothesis

of complete disappearance of out-of-sample performance (coefficient equal to -1). We reject

both hypotheses.

In the lower panel of Table 3 we consider the out-of-sample but pre-publication and post-

publication periods separately. We find that, in the window between the end of the sample

period and the publication date, the size of the alpha spread appears to shrink by 30-40%,

with the Q5-Q1 method suggesting a greater decrease in predictability. For both methods,

we cannot reject the null hypothesis of no decline in alpha spreads, and we do reject the null

of complete disappearance.

4 As in McLean and Pontiff (2015), one result of this definition is that the intercept of this regression isexactly equal to 1.

11

Post-publication, alpha spreads decrease further on average. Using the Q5-Q1 approach,

post-publication alphas are, on average, just 37% of their in-sample values. Using the CSR

approach, they are only 26% of the in-sample value on average. For both methods, we can

strongly reject the null that post-publication alpha spreads are as large as in-sample spreads.

Only for the Q5-Q1 results can we reject the null that any alpha spread remains following

publication.

Overall, these results reinforce the interpretation of Table 2. Out-of-sample spreads

in alphas, particularly over the post-publication period, are much smaller than in-sample

counterparts, suggesting that the economic value of the average predictor is modest at best.

At the same time, in-sample alpha predictability is clearly not merely the result of data

mining, as we see significant evidence that predictors continue to generate spreads in alphas

in the out-of-sample periods, particularly prior to publication.

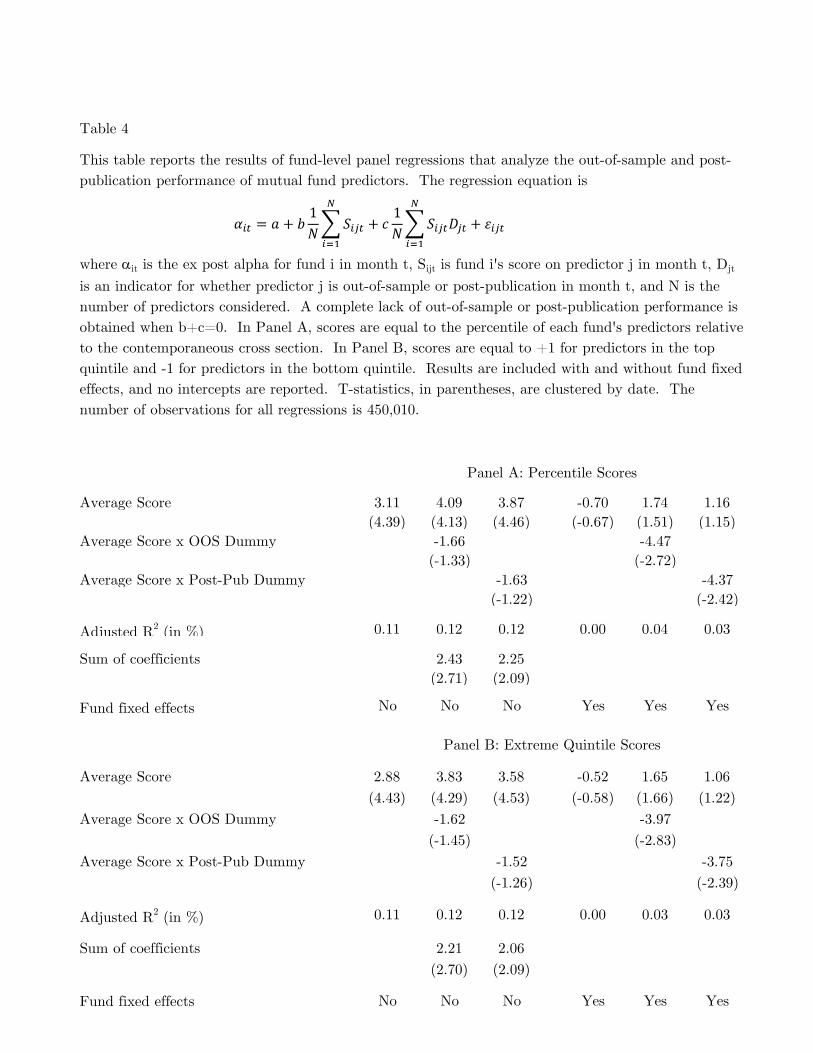

3.3 Fund panel

We also analyze the out-of-sample and post-publication predictability of mutual fund alphas

in a mutual fund-level panel regression. We do so for several reasons. One is that individual

funds are likely to display substantial variation in alpha predictors relative to fund averages,

such as those created as the result of a quintile sort. With larger variation in expected

alpha, we may better be able to detect when realized alphas fall short of expected alphas,

for instance due to a publication effect. In examining individual funds, we will also find

cases where a fund displays multiple characteristics associated with good performance. This

will also increase predicted alpha and again give us the best chance to detect any changes in

the relationship between predicted and realized alphas. A final reason to pursue a fund-level

analysis is that it will allow us to examine fund expense ratios and asset growth in a natural

way. We leave that analysis for Section 4.

To understand our fund-level regressions, first imagine the regression that we would run

if we were using just a single alpha predictor:

αit = a+ bSit + cSitDt + εit

In this regression, St represents a score computed based on fund i’s date-t value of the

12

predictor (which is assumed known prior to date t). As an example, the score might take

the value +1 if the fund was in the bottom quintile based on the predictor and -1 if it was

in the top quintile, The variable Dt is an indicator variable that takes the value 1 if t is

past the end of the original sample used in the paper where the predictor was first proposed.

Thus, c = 0 corresponds to the case in which the out-of-sample impact of the predictor is

unchanged from its in-sample impact. If b + c = 0, then the predictor ceases to have any

ability to forecast ex post alpha out of sample.

With multiple predictors, we must make an assumption about how predictability aggre-

gates. We do so by simply assuming that alphas are related to the average score across all

predictors. If there are N predictors, we assume that

αit = a+ b1

N

N∑j=1

Sijt + c1

N

N∑j=1

SijtDjt + εit, (1)

where the j coefficient denotes the predictor. Under this specification, it remains true that

c = 0 implies no deterioration in predictive ability out of sample, and that b+ c = 0 implies

that no predictability can result from any predictor following the end of that predictor’s

original sample period.

We consider two different specifications of the score variable Sijt. One is the extreme

quintile score described above, where funds in the top predictor quintile receive a score of

+1 and funds in the bottom quintile receive a score of -1. This corresponds roughly to the

Q5-Q1 approach in our earlier results. The other score is equal to the percentile of the

predictor of a given fund, rescaled to lie between -1 and +1, within the contemporaneous

cross section. This is more related to, but not analogous to, the earlier CSR results. We

have experimented with other definitions of the score and find little effect on our results.

The results, shown in Table 4, are mixed. When we do not include fund fixed effects, the

overall effect of higher average scores is large and significant, but no significant out-of-sample

or post-publication declines are detected. For example, in the first column of Panel A, the

3.11 coefficient on the average score implies that a fund whose predictors are all in the 75th

percentile (with a score of 0.5) will on average have an alpha that is 3.11% higher than

a fund whose predictors are all in the 25th percentile (with a score of -0.5). In the second

column, this coefficient rises with the introduction of the interaction term included to capture

13

declining out-of-sample predictability. This interaction term is insignificant, however, both

for out-of-sample and post-publication effects, a result that is unchanged when we instead

base scores on extreme quintiles. When we examine the sum of the direct and interacted

effects (denoted as “sum of coefficients”) we find positive and significant values, consistent

with continued predictability out of sample.

Only after adding fund fixed effects do we see a significant decrease in predictive ability in

the out-of-sample or post-publication periods. In doing so, however, we lose the significance

of the baseline average score variable, presumably because average score does not vary enough

over time within each fund to identify its direct effect.

In all, we view this evidence as generally consistent with the prior results based on a

panel of predictors rather than funds. Results here are weaker than anticipated for reasons

that are unknown at this point.

4 Flows and expenses

The previous section showed strong evidence that variables that forecast future mutual fund

alphas lose much of their predictive ability out of sample. The decline, however, takes some

time to occur. In particular, in the typically short interval between the end of the original

sample period and the date of publication, most of the predictive power, perhaps 30-40%,

remains intact. Only after publication does the decay in predictive ability reach its terminal

level.

The continued performance of predictors out of sample would seem to rule out data

mining as a primary explanation of in-sample predictability. The apparently larger decay

post-publication suggests the possibility that fund investors, managers, or management com-

panies may be learning about the distribution of fund alphas based on the results of published

studies.

The idea that learning may affect expected return has been discussed in several papers

investigating asset pricing anomalies, most recently Jones and Pomorski (2015) and McLean

and Pontiff (2015). In these papers, the mechanism of how learning affects asset prices is well

understood – learning from an academic study that a set of securities offers positive alpha

14

induces greater investment to those securities, which raises their prices and eliminates the

alpha. In the mutual fund setting, the effects of learning are likely not as straightforward.

One set of predictions is implied by the model of Berk and Green (2004). In that model, an

increase in the predicted fund alpha would either drive the fund to increase its management

fee or investors to increase their holdings of the fund. The former directly reduces alphas,

which are measured net of expenses. The latter does so indirectly as the result of assumed

diseconomies of scale. Either way, if learning causes all parties to conclude that a fund has

positive alpha, then the future performance of that fund (net of fees) should be expected to

decrease.

While the effects of raising fees are straightforward, there is some disagreement in the

literature about whether fund inflows are likely to have a significant effect on the typical

fund’s alpha generation ability. Pastor et al. (2015) find inconclusive evidence and summarize

conflicting results found elsewhere in the literature. Thus, a finding that the out-of-sample

decay in alpha is associated with changing flow behavior would provide new support for a

somewhat unsubstantiated hypothesis.

It is also possible that learning may affect predictability through a channel unrelated to

Berk and Green (2004). If the publication of academic research does affect mutual fund flows

or allow some managers to raise fees, then fund managers may use that research to better

mimic fund types that have been shown to offer better performance on average. For example,

a fund manager with a low “active share,” which Cremers and Petajisto (2009) show signals

to have poor performance, may decide to switch to a high active share strategy, even though

his ability to generate good performance is unchanged. By doing so, this and other managers

corrupt the active share measure, reducing its predictive power. Since they only have an

incentive to do so if it generates inflows or allows them to raise fees, this hypothesis may be

observationally equivalent to the one based on the Berk and Green model.

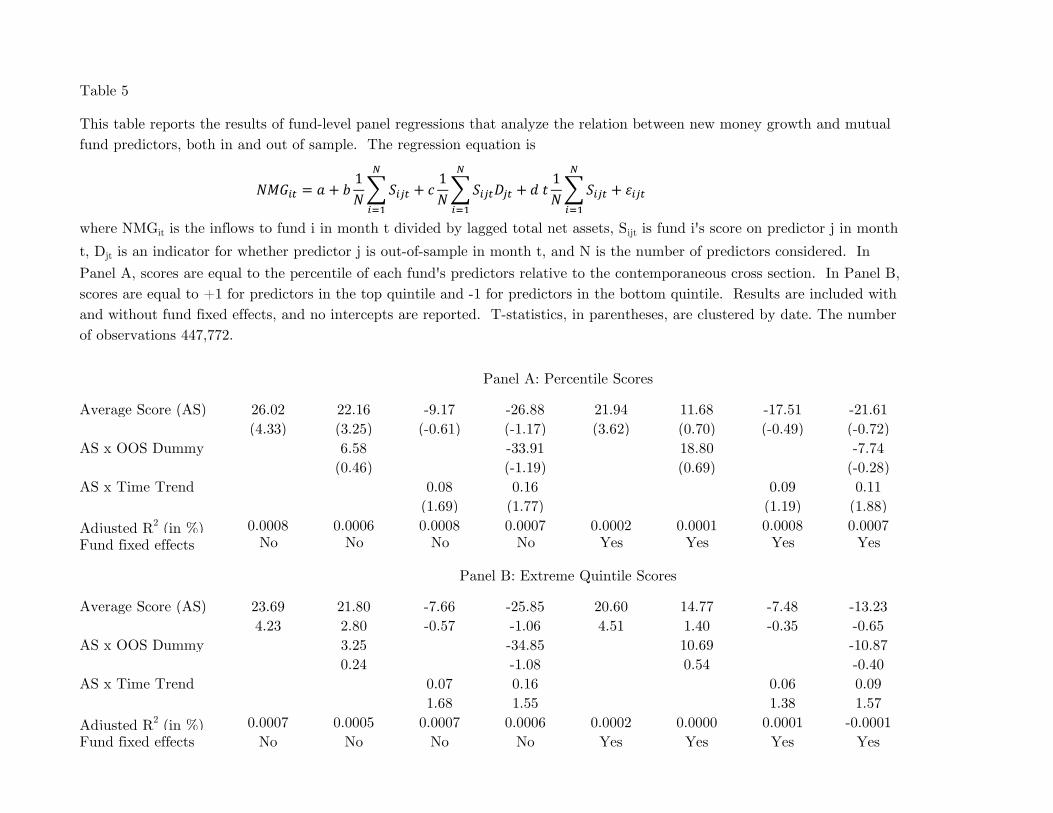

We first investigate the relation between flows and alpha predictors in a framework that

is similar to the fund panel analyzed in Section 3.3. We define new money growth (NMGit)

as the net inflows to the fund within a month divided by the total net assets of the fund at

the end of the prior month. We regress this on the average score variable, the average score

15

interacted with out-of-sample indicators, and the average score interacted with a time trend:

NMGit = a+ b1

N

N∑j=1

Sijt + c1

N

N∑j=1

SijtDjt + d t1

N

N∑j=1

SijtDjt + εit (2)

Results for this and restricted specifications are shown in Table 5. As in the previous fund-

level panel regression, we include results both with and without fund fixed effects.

Table 5 is easily summarized. There is a strong and significant tendency for mutual

funds with higher average scores, whose alphas are more likely to be positive, to have higher

inflows. This result is obtained for both scoring methods, regardless of whether fixed effects

are included.

We find little else beyond that result. In some of the specifications the interaction of the

average score with a time trend approaches statistical significance, suggesting that flows may

have become more responsive to alpha predictors over time. We find no evidence that flows

are more or less responsive to alpha predictors out-of-sample. If we examine post-publication

effects rather than out-of-sample effects, none of these results changes meaningfully.

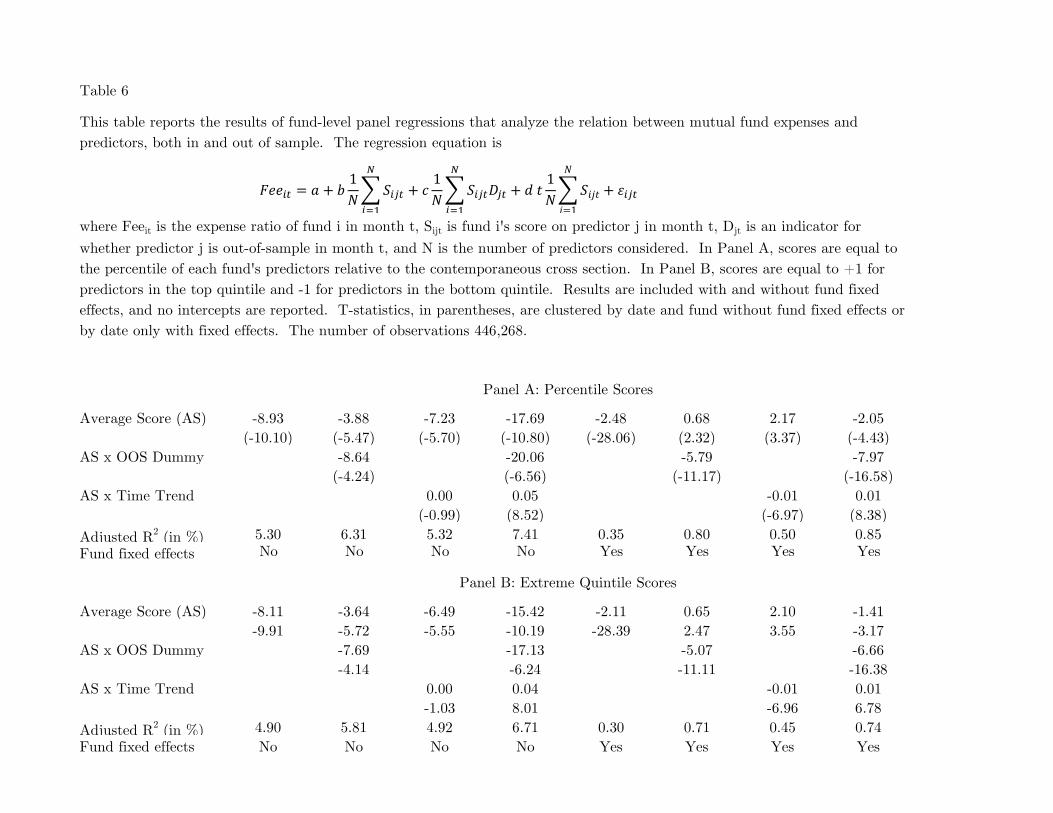

We next examine mutual fund expense ratios in the same regression framework, where

fees are defined as annual expense ratios charged (CRSP MF item exp ratio, decimal format).

For better readability of estimates, we rescale the expense ratios by 1000 before applying in

the regressions Here we obtain a somewhat richer set of results, which are shown in Table 6.

The first result from this analysis is that fees are on average lower for funds with high

average predictor scores, which is not dependent on the scoring method or whether fixed

effects are included. For example, the coefficient of -8.11 from the first column of Panel B

implies that a fund with all zero scores (no predictor in the top or bottom quintile) would

on average have an annual expense ratio that is 0.811 percent higher than a fund with all

predictors in the top quintile (Sijt = 1 for all j). This result suggests that part of the reason

that alpha predictors work is that they are correlated with fund fees.

The second result is that this negative relation between alpha predictors and fees is

significantly stronger in the out-of-sample period.5 This is important because it effectively

negates the possibility that rising fees are responsible for disappearing alpha predictability.

Funds with high average scores on average have positive alphas. Under the Berk and Green

5 As with new money growth, specifications using post-publication indicators result in similar findings.

16

(2004) hypothesis, a fund that is believed to have positive alpha will have a tendency to

increase fees. To the extent that academic work identifying alpha predictors affects the

beliefs of mutual fund investors and management companies, the impact appears to be the

opposite.

Table 6 also reports the results of specifications in which a time trend is interacted with

the average score. These are included because out-of-sample indicators are also increasing

over time and could therefore possibly capture a trend in alpha predictability rather than

a shift at the end of the sample. While the time trend interaction term has different signs

depending on the specification, including it does not change earlier conclusions about the

sign and significance of the out-of-sample term.

Overall, we believe that the results in Tables 5 and 6 suggest that learning about expected

fund performance is not a likely explanation of the decline of alpha predictability. Funds with

higher predicted alphas do not experience higher inflows and in fact have a strong tendency

to charge lower fees. Thus, while our results do not preclude the possibility that the Berk

and Green (2004) model may receive support elsewhere, it does not appear to describe the

dynamics in alphas that we observe.

5 Time-varying arbitrage activity

An alternative explanation for diminished out-of-sample alpha spreads is that increases in the

level of market efficiency over time have made alpha generation (either positive or negative)

more and more difficult. This is the conclusion of Chordia et al. (2014), who show that

measures of the intensity of arbitrage activity are inversely correlated with the profitability

of many of the best-known asset pricing anomalies. Out of the 12 anomalues they consider,

11 are decreasing in the amount of hedge fund assets under management, 10 are decreasing

in the level of aggregate short interest, and 11 are decreasing in aggregate share turnover.

In this section we follow Chordia et al. by examining the relation between arbitrage activity

and market efficiency, but where we measure the latter based on the spread of alphas.

17

5.1 Arbitrage activity proxies

Following Chordia et al. (2014), we consider three different proxies of market-level arbitrage

activity – aggregate short interest, aggregate share turnover, and aggregate hedge fund asset

size. Aggregate short interest is the value-weighted monthly short interest scaled by the

previous month’s outstanding shares. Stock short interest data is from Compustat, and our

final aggregate short interest spans from January 1973 to December 2012. Aggregate share

turnover is the monthly value-weighted share turnover using the market capitalization at

the end of the previous year as the weight. Monthly share turnover is share trading volume

scaled by shares outstanding, which are all from CRSP. Our final aggregate share turnover

spans from January 1961 to December 2012. Aggregate hedge fund asset size is hedge fund

monthly assets under management (AUM) scaled by the market capitalization for NYSE

and AMEX stocks in the previous month. Hedge fund monthly AUM from March 1977 to

December 2010 are from Jylha and Suominen (2011). We extend this series through 2012

using annual AUM data from Hedge Fund Research. Our final aggregate hedge fund asset

size therfore spans from March 1977 to December 2012.

In Chordia et al. (2014), each of the arbitrage activity proxies is detrended by regressing

the measure on a time trend prior to its inclusion in a regression. We believe that detrended

measures are useful in that they potentially identify effects that cannot be explained by a

simple trend towards market efficiency. At the same time, if markets have become more effi-

cient over time as the result of an overall positive trend in arbitrage activity, then detrending

will remove some of the variation driving alpha dynamics. Without a strong rationale to

choose one over the other, we consider both detrended and non-detrended series.

In addition, we create composite arbitrage activity series by first normalizing each mea-

sure and then averaging across the three measures. One average is computed for detrended

arbitrage proxies, and one average is computed for non-detrended proxies.

5.2 Arbitrage and alpha

Our first set of results on arbitrage activity follows the predictor panel approach used in

Section 3.2. For each predictor, we compute an alpha spread either using the Q5-Q1 or

18

CSR approach and run a panel regression of those alpha spreads on some arbitrage proxy.

A negative coefficient indicates that greater arbitrage activity reduces the ability of the

predictors to generate spreads in mutual fund alphas.

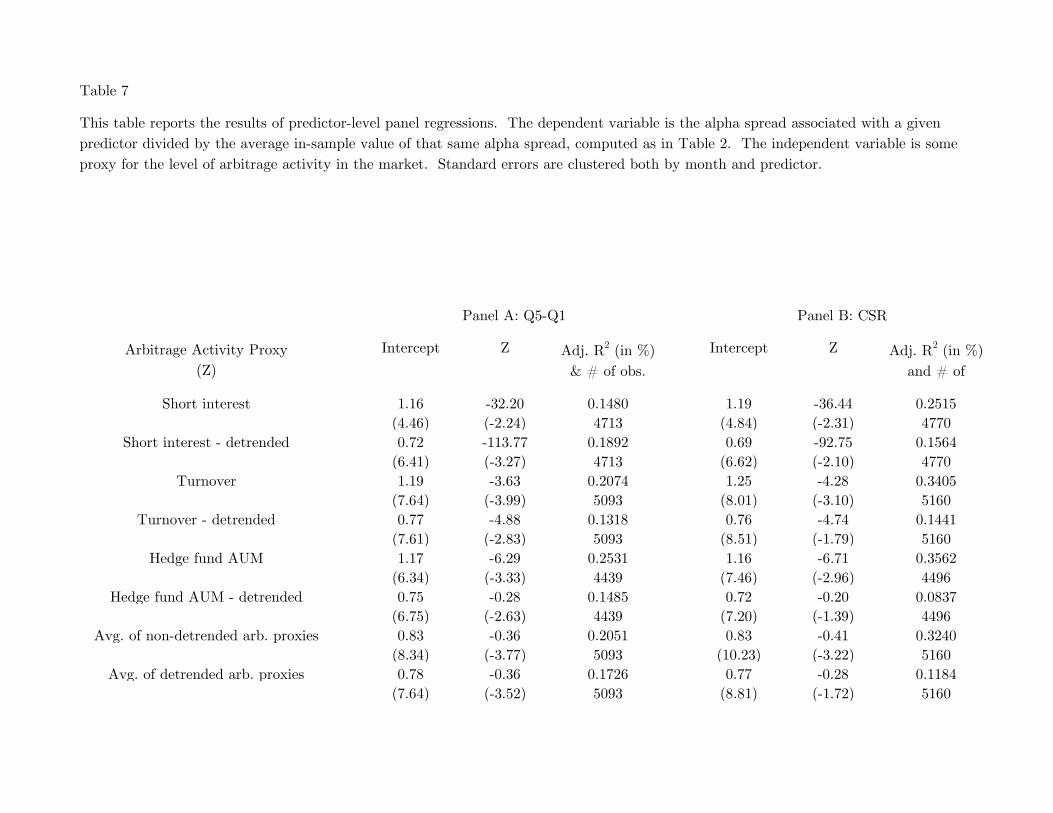

Table 7 contains the results of this analysis. In short, with few exceptions, greater

arbitrage activity appears to be inversely and significantly related to mutual fund alpha

spreads. Results are slightly stronger for the Q5-Q1 results, but even for the CSR results we

find that non-detrended arbitrage variables are highly significant, with detrended variables

somewhat more marginal.

The coefficients on the two composite measures vary from -0.28 to -0.41. The -0.36

coefficient for the Q5-Q1 results implies that if all three arbitrage proxies increased by one

standard deviation, then the average alpha spread would fall by 36 basis points. Given the

intercept estimates, which are all close to 0.8, the results imply that all spreads disappear

when arbitrage proxies are a little more than two standard deviations below their respective

means.

Next, we investigate the role of arbitrage activity within the fund panel framework de-

scribed in Section 3.3. In this approach, we compute the average score,

Avg.Sit =1

N

N∑j=1

Sijt,

for each fund i at each time t and run the regression

αit = a+ bAvg.Sit + cZtAvg.Sit + εit,

where Zt, known at the start of date t, is one of the arbitrage activity proxies or composite

measures discussed above. As in Table 4, this regression is run both with and without fund

fixed effects. T-statistics are always clustered by date.

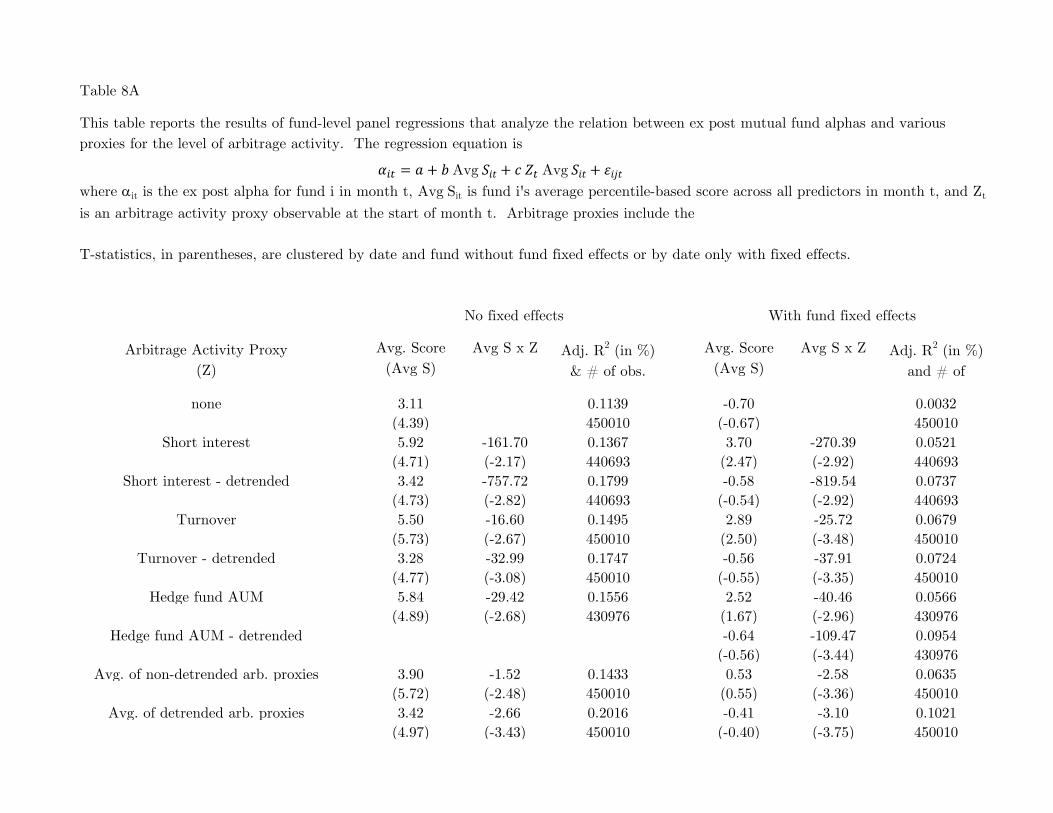

The results for scores computed based on predictor percentiles are contained in 8A. They

mirror those from Table 7 but are in fact even stronger. In all cases, heavier arbitrage activity

reduces the predictability of fund alphas, in that predictors are significantly less positively

related to fund alphas when arbitrage activity is high.

Table 8B repeats this analysis when scores are instead based on extreme quintiles. Arbi-

trage activity proxies continue to have a significant depressive effect on alpha predictability.

19

Differences with the percentile-based results are small in statistical and economic terms.

5.3 The out-of-sample effect revisited

In this section we ask whether it is possible that the declining out-of-sample predictabil-

ity is consistent with time-varying arbitrage activity. To answer this question we consider

specifications that include both out-of-sample indicators and measures of arbitrage activity.

We also include time trends in some regressions. As noted above, out-of-sample indicator

variables and non-detrended arbitrage proxies are all, to some extent, trending upwards over

time. By including time trends we hope to distinguish these effects from generic trends.

We first consider the issue within the panel of mutual fund alpha predictors. To limit the

number of results, we only include the composite arbitrage activity proxies, both detrended

and non-detrended. Regressions using individual arbitrage proxies are slightly weaker but

very consistent with the regressions that we include here.

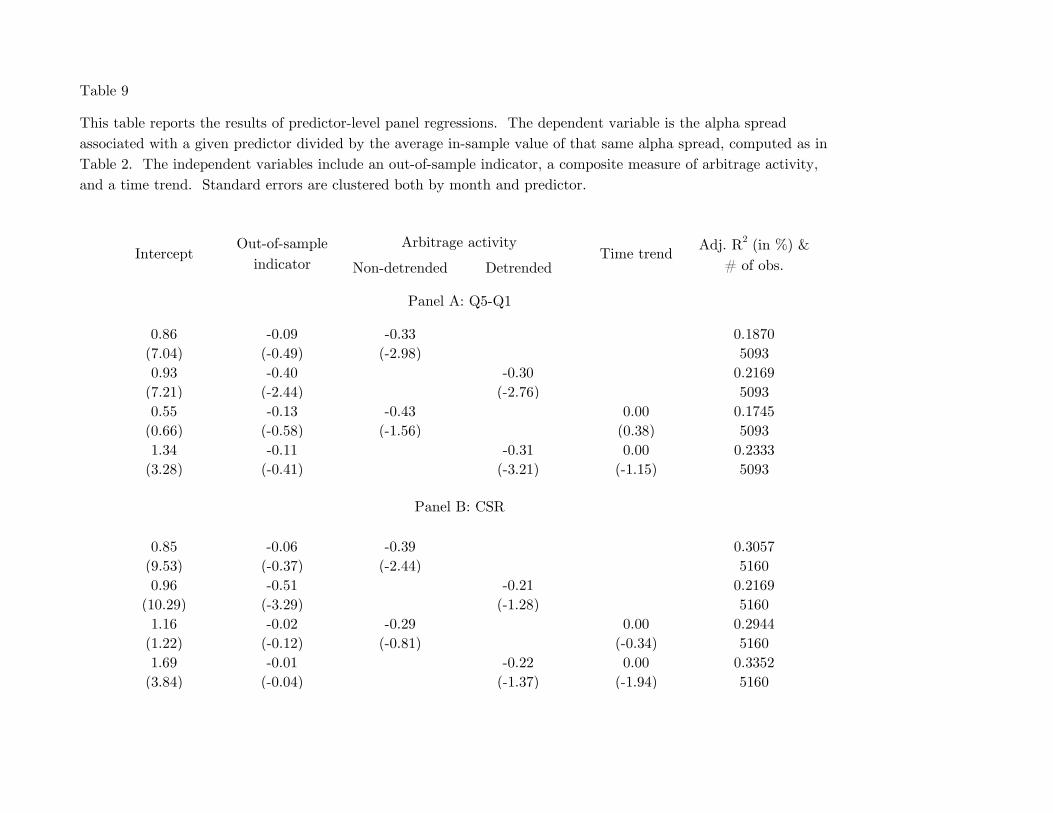

The results, shown in Table 9, are somewhat mixed. In the Q5-Q1 results, in which alpha

spreads are computed based on the extreme quintiles of sorts on the predictors, the out-of-

sample effect is significant in only one out of four specifications. In that specification, which

does not include a time trend, the arbitrage proxy is also significant. Out of the three other

Q5-Q1 specifications, the arbitrage proxy is significant in two. Overall, including a time trend

eliminates the significance of the out-of-sample effect and also weakens the significance of

the arbitrage activity measure if that measure is not already detrended. Detrended arbitrage

activity is unaffected by the inclusion of a trend and is highly significant.

For the CSR-based alpha spreads, as in earlier sections, results are weaker. The out-of-

sample effect is significant in one specification and the arbitrage effect is significant in one

other.

We next consider the mutual fund panel in Table 10. We estimate full and restricted

versions of the specification

αit = a+ b1

N

N∑j=1

Sijt + c1

N

N∑j=1

SijtDjt + dZt1

N

N∑j=1

Sijt + e t1

N

N∑j=1

Sijt + εit, (3)

As before, the b coefficient captures the baseline relation between average predictor scores

and alpha, c measures the out-of-sample effect, d captures the relation with arbitrage activity,

20

and e measures how the impact of alpha predictors is affected by a time trend.

Results in the fund panel are somewhat more clear cut. The out-of-sample effect is never

statistically significant though most point estimates remain negative. Arbitrage activity

has a negative affect on alpha prediction in all 16 specifications, and it is significant in

14. Interestingly, including a time trend seems to strengthen the significance of the non-

detrended arbitrage activity proxy, the opposite of its effect in Table 9. It also strengthens

the out-of-sample effect, though not enough for that variable to reach significance. As with

earlier results, computing predictor scores based on percentiles or extreme quintiles does not

have a material effect.

6 Summary

Whether academic finance research is useful or not in practice largely rests on whether or

not its findings continue to hold out of sample. In the case of variables shown in the finance

literature to forecast future mutual fund alphas, we find that the out-of-sample performance

is somewhat disappointing. Using several different econometric approaches, we find that

most of the predictability in fund alphas disappears following the end of the sample. The

post-publication decline appeared to be even larger.

One possible explanation for these results was that academic studies represent a source

for learning by mutual fund investors and management companies. Any change in the

expectation of future performance should lead to changes in equilibrium fees and fund sizes.

A fund newly perceived as being a good likely performer will have an incentive to raise fees,

thereby decreasing future performance. Higher inflows can also worsen performance if, as in

the model of Berk and Green (2004), funds face diseconomies of scale. Alternatively, if funds

do see greater inflows as the result of investors learning that a certain fund characteristic is

associated with good future performance, then unskilled fund managers will have an incentive

to mimic the favored characteristic. This would lead to a corruption of that characteristic,

causing it to deteriorate as a predictor of fund alpha even if the alpha of each fund was

unchanged.

When we analyze fund fees and flows, however, we find no shift out-of-sample or post-

21

publication that would suggest that any of these dynamics are at play. Flows are positively

related to alpha predictors, but this relation does not change out-of-sample. Fund fees are

negatively related to predicted alpha, and this relation only gets stronger out-of-sample,

which is the opposite of the prediction above.

We find instead that a more consistent explanation is that an upward trend in arbitrage

activity over our sample period has increased market efficiency, causing all fund alphas to

shrink towards zero. These arbitrage activity variables, aggregate measures of short interest,

share turnover, and hedge fund AUM, have been shown by Chordia et al. (2014) to be

associated with shrinking alphas on asset pricing anomalies like size and momentum. We

find that these variables are correlated with mutual fund alphas as well and largely explain

the decline in mutual fund alpha generation ability.

Key questions remain. Are the same forces causing the attenuation of all mutual fund

alpha predictors, or does the strength of different predictors depend on different forces?

What is the channel by which arbitrage activity affects mutual fund performance? Can

arbitrage activity in one market segment affect mutual fund performance in another? We

leave these questions for future work.

22

References

Amihud, Yakov and Ruslan Goyenko (2013), “Mutual fund’sR2 as predictor of performance.”

Review of Financial Studies, 26, 667–694.

Barras, Laurent, Olivier Scaillet, and Russ Wermers (2010), “False discoveries in mutual fund

performance: Measuring luck in estimated alphas.” Journal of Finance, 65, 179–216.

Berk, Jonathan B. and Richard Green (2004), “Mutual fund flows and performance in ra-

tional markets.” Journal of Political Economy, 112, 1269–1295.

Cao, Charles, Timothy T. Simin, and Ying Wang (2013), “Do mutual fund managers time

market liquidity?” Journal of Financial Markets, 16, 279–307.

Carhart, Mark M. (1997), “On persistence in mutual fund performance.” Journal of finance,

52, 57–82.

Chen, Joseph, Harrison Hong, Ming Huang, and Jeffrey D. Kubik (2004), “Does fund size

erode mutual fund performance? the role of liquidity and organization.” American Eco-

nomic Review, 94, 1276–1302.

Chen, Yong and Wayne Ferson (2015), “How many good and bad funds are there, really?”

working paper.

Chordia, Tarun, Avanidhar Subrahmanyam, and Qing Tong (2014), “Have capital market

anomalies attenuated in the recent era of high liquidity and trading activity?” Journal of

Accounting and Economics, 58, 41–58.

Christoffersen, Susan and Sergei Sarkissian (2009), “City size and fund performance.” Jour-

nal of Financial Economics, 92, 252–275.

Cohen, Randolph B., Joshua D. Coval, and L’ubos Pastor (2005), “Judging fund managers

by the company they keep.” Journal of Finance, 60, 1057–1096.

Cremers, Martijn and Antti Petajisto (2009), “How active is your fund manager? a new

measure that predicts performance.” Review of Financial Studies, 22, 3329–3365.

23

Da, Zhi, Pengjie Gao, and Ravi Jagannathan (2010), “Impatient trading, liquidity provision,

and stock selection by mutual funds.” Review of Financial Studies, 24, 675–720.

Easley, David, Nicholas M. Kiefer, Maureen O’Hara, and Joseph B. Paperman (1996), “Liq-

uidity, information, and infrequently traded stocks.” Journal of Finance, 51, 1405–1436.

Elton, Edwin J., Martin J. Gruber, and Christopher R. Blake (2002), “A first look at the ac-

curacy of the CRSP mutual fund database and a comparison of the CRSP and Morningstar

mutual fund databases.” 56, 2415–2430.

Evans, Richard B. (2010), “Mutual fund incubation.” The Journal of Finance, 65, 1581–

1611.

Fama, Eugene F and Kenneth R French (1993), “Common risk factors in the returns on

stocks and bonds.” Journal of financial economics, 33, 3–56.

Fama, Eugene F. and Kenneth R. French (2010), “Luck versus skill in the cross-section of

mutual fund returns.” Journal of Finance, 65, 1915–1947.

Hendricks, Darryll, Jayendu Patel, and Richard Zeckhauser (1993), “Hot hands in mutual

funds: Short-run persistence of relative performance, 1974-1988.” Journal of Finance,

93–130.

Huang, Jennifer, Clemens Sialm, and Hanjiang Zhang (2011), “Risk shifting and mutual

fund performance.” Review of Financial Studies, 2575–2616.

Jones, Christopher S. and Lukasz Pomorski (2015), “Investing in disappearing anomalies.”

Review of Finance.

Jones, Christopher S. and Jay Shanken (2005), “Mutual fund performance with learning

across funds.” Journal of Financial Economics, 78, 507–552.

Jylha, Petri and Matti Suominen (2011), “Speculative capital and currency carry trades.”

Journal of Financial Economics, 99, 60–75.

Kacperczyk, Marcin, Stijn Van Nieuwerburgh, and Laura Veldkamp (2014), “Time-varying

fund manager skill.” Journal of Finance, 69, 1455–1484.

24

Kacperczyk, Marcin and Amit Seru (2007), “Fund manager use of public information: New

evidence on managerial skills.” Journal of Finance, 62, 485–528.

Kacperczyk, Marcin, Clemens Sialm, and Lu Zheng (2005), “On the industry concentration

of actively managed equity mutual funds.” Journal of Finance, 60, 1983–2011.

Kacperczyk, Marcin, Clemens Sialm, and Lu Zheng (2008), “Unobserved actions of mutual

funds.” Review of Financial Studies, 21, 2379–2416.

Kosowski, Robert, Allan Timmermann, Russ Wermers, and Hal White (2006), “Can mutual

fund “stars” really pick stocks? new evidence from a bootstrap analysis.” Journal of

finance, 61, 2551–2595.

Mamaysky, Harry, Matthew Spiegel, and Hong Zhang (2007), “Improved forecasting of mu-

tual fund alphas and betas.” Review of Finance, 11, 359–400.

McLean, R. David and Jeffrey Pontiff (2015), “Does academic research destroy stock return

predictability?” Journal of Finance, 1, 1–999.

Pastor, L’ubos, Robert F. Stambaugh, and Lucian A. Taylor (2015), “Scale and skill in

active management.” Journal of Financial Economics, 116, 23–45.

Schwert, G. William (2003), “Anomalies and market efficiency.” In Handbook of the Eco-

nomics of Finance (Milton Harris Constantinides, George and Rene M. Stulz, eds.), chap-

ter 15, 939–974, North-Holland.

25

Number of predictors

found in the literature 20

unable to replicate based on data unavailability 4

Predictors included based on extreme quintiles (Q5-Q1) 12

Number of predictors with t-statistic ≥ 1.4 12

Number of predictors with out-of-sample data 12

Number of predictors with post-publication data 10

Average number of out-of-sample months 160

Average number of post-publication months 135

Average number of out-of-sample but pre-publication months 48

Average in-sample alpha spread (annual %) 1.96

Average in-sample t-statistic 2.28

Predictors included based on cross-sectional regression (CSR) 12

Number of predictors with t-statistic ≥ 1.4 12

Number of predictors with out-of-sample data 12

Number of predictors with post-publication data 11

Average number of out-of-sample months 154

Average number of post-publication months 121

Average number of out-of-sample but pre-publication months 44

Average in-sample alpha spread (annualized CSR coefficient in %) 1.13

Average in-sample t-statistic 2.21

This table summarizes the predictors considered in the paper. Predictors are included in

the analysis if we are able to replicate the sign of the relation between alpha and the

predictor reported in the original paper and obtain a t-statistic of at least 1.4 using the

original sample period.

Table 1

Table 2

Panel A: Q5-Q1 Out of Sample Post-PublicationOut of Sample

but Pre-Publication

Average Scaled Spread 0.218 0.112 0.603

T for testing 1 -3.474 -3.593 -1.347

T for testing 0 0.97 0.45 2.05

Percentage<1 (%) 100 100 100

Predictors Included 12 10 12

Panel B: CSR Out of Sample Post-PublicationOut of Sample

but Pre-Publication

Average Scaled Spread 0.135 -0.114 0.59

T for testing 1 -4.183 -3.359 -1.459

T for testing 0 0.65 -0.34 2.10

Percentage<1 (%) 100 100 100

Predictors Included 12 10 12

This table reports summary statistics for the out-of-sample and post-publication behavior of alpha

spreads associated with various abnormal return predictors documented in the mutual fund literature.

The ex post alpha for each fund on each date is computed by subtracting the exposures to the four

Carhart factors, where the betas corresponding to each fund/date are computed based on the prior 36

months of returns. Alpha spreads are computed either as the difference between the top and bottom

quintiles of a predictor-based sort (Q5-Q1) or as the slope coefficient of a cross sectional regression of

ex post alphas on the predictor (CSR). For each predictor, alpha spreads are then averaged across the

out-of-sample, post-publication, and out-of-sample but pre-publication subsamples and divided by the

average in-sample alpha spread. The table reports the results of averaging these ratios across the 10

or 12 predictors included. To be included, predictors must have at least 12 monthly observations in

the out-of-sample period or post-publication period.

Table 3

Q5-Q1 CSR

Constant Est 1 1

T 8.07 13.24

Out of sample Est -0.56 -0.62

T (H0 = 0) -3.32 -3.61

T (H0 = -1) 2.57 2.25

Adjusted R2 (in %) 0.12

%

0.16

%Obs 5093 5160

Constant Est 1 1

T 8.07 13.24

Out of sample but pre-publication Est -0.40 -0.31

T (H0 = 0) -1.52 -1.26

T (H0 = -1) 2.32 2.76

Post-publication Est -0.63 -0.74

T (H0 = 0) -3.62 -3.18

T (H0 = -1) 2.09 1.14

Adjusted R2 (in %) 0.10

%

0.17

%Obs 5093 5160

This table reports the results of predictor-level panel regressions. The dependent variable is the alpha

spread associated with a given predictor divided by the average in-sample value of that same alpha

spread. To construct this value, we first compute the ex post Carhart four-factor model alpha of each

fund using 36 months of lagged returns to estimate the betas of each fund. We then compute the

alpha spread for a given predictor as the difference between the alphas of the highest and lowest

quintiles formed based on that predictor (Q5-Q1) or as the slope coefficient of a single cross sectional

regression of fund alphas on the predictor (CSR). In the top panel, the only independent variable is

an indicator that takes the value of 1 if the observation for a given predictor is past the last date in

the sample used in the original paper documenting the significance of that predictor. In the bottom

panel, we include an indicator for the period between the sample end and the publication date and

another indicator for the post-publication period for each predictor. T-statistics are clustered both by

month and predictor.

Table 4

Average Score 3.11 4.09 3.87 -0.70 1.74 1.16

(4.39) (4.13) (4.46) (-0.67) (1.51) (1.15)

Average Score x OOS Dummy -1.66 -4.47

(-1.33) (-2.72)

Average Score x Post-Pub Dummy -1.63 -4.37

(-1.22) (-2.42)

Adjusted R2 (in %) 0.11 0.12 0.12 0.00 0.04 0.03

Sum of coefficients 2.43 2.25

(2.71) (2.09)

Fund fixed effects No No No Yes Yes Yes

Average Score 2.88 3.83 3.58 -0.52 1.65 1.06

(4.43) (4.29) (4.53) (-0.58) (1.66) (1.22)

Average Score x OOS Dummy -1.62 -3.97

(-1.45) (-2.83)

Average Score x Post-Pub Dummy -1.52 -3.75

(-1.26) (-2.39)

Adjusted R2 (in %) 0.11

%

0.12

%

0.12

%

0.00

%

0.03

%

0.03

%Sum of coefficients 2.21 2.06

(2.70) (2.09)

Fund fixed effects No No No Yes Yes Yes

Panel B: Extreme Quintile Scores

Panel A: Percentile Scores

This table reports the results of fund-level panel regressions that analyze the out-of-sample and post-

publication performance of mutual fund predictors. The regression equation is

where ait is the ex post alpha for fund i in month t, Sijt is fund i's score on predictor j in month t, Djt

is an indicator for whether predictor j is out-of-sample or post-publication in month t, and N is the

number of predictors considered. A complete lack of out-of-sample or post-publication performance is

obtained when b+c=0. In Panel A, scores are equal to the percentile of each fund's predictors relative

to the contemporaneous cross section. In Panel B, scores are equal to +1 for predictors in the top

quintile and -1 for predictors in the bottom quintile. Results are included with and without fund fixed

effects, and no intercepts are reported. T-statistics, in parentheses, are clustered by date. The

number of observations for all regressions is 450,010.

𝛼𝑖𝑡 = 𝑎 + 𝑏1

𝑁

𝑖=1

𝑁

𝑆𝑖𝑗𝑡 + 𝑐1

𝑁

𝑖=1

𝑁

𝑆𝑖𝑗𝑡𝐷𝑗𝑡 + 𝜀𝑖𝑗𝑡

Table 5

Average Score (AS) 26.02 22.16 -9.17 -26.88 21.94 11.68 -17.51 -21.61

(4.33) (3.25) (-0.61) (-1.17) (3.62) (0.70) (-0.49) (-0.72)

AS x OOS Dummy 6.58 -33.91 18.80 -7.74

(0.46) (-1.19) (0.69) (-0.28)

AS x Time Trend 0.08 0.16 0.09 0.11

(1.69) (1.77) (1.19) (1.88)

Adjusted R2 (in %) 0.0008 0.0006 0.0008 0.0007 0.0002 0.0001 0.0008 0.0007

Fund fixed effects No No No No Yes Yes Yes Yes

Average Score (AS) 23.69 21.80 -7.66 -25.85 20.60 14.77 -7.48 -13.23

4.23 2.80 -0.57 -1.06 4.51 1.40 -0.35 -0.65

AS x OOS Dummy 3.25 -34.85 10.69 -10.87

0.24 -1.08 0.54 -0.40

AS x Time Trend 0.07 0.16 0.06 0.09

1.68 1.55 1.38 1.57

Adjusted R2 (in %) 0.0007 0.0005 0.0007 0.0006 0.0002 0.0000 0.0001 -0.0001

Fund fixed effects No No No No Yes Yes Yes Yes

This table reports the results of fund-level panel regressions that analyze the relation between new money growth and mutual

fund predictors, both in and out of sample. The regression equation is

where NMGit is the inflows to fund i in month t divided by lagged total net assets, Sijt is fund i's score on predictor j in month

t, Djt is an indicator for whether predictor j is out-of-sample in month t, and N is the number of predictors considered. In

Panel A, scores are equal to the percentile of each fund's predictors relative to the contemporaneous cross section. In Panel B,

scores are equal to +1 for predictors in the top quintile and -1 for predictors in the bottom quintile. Results are included with

and without fund fixed effects, and no intercepts are reported. T-statistics, in parentheses, are clustered by date. The number

of observations 447,772.

Panel A: Percentile Scores

Panel B: Extreme Quintile Scores

𝑁𝑀𝐺𝑖𝑡 = 𝑎 + 𝑏1

𝑁

𝑖=1

𝑁

𝑆𝑖𝑗𝑡 + 𝑐1

𝑁

𝑖=1

𝑁

𝑆𝑖𝑗𝑡𝐷𝑗𝑡 + 𝑑 𝑡1

𝑁

𝑖=1

𝑁

𝑆𝑖𝑗𝑡 + 𝜀𝑖𝑗𝑡

Table 6

Average Score (AS) -8.93 -3.88 -7.23 -17.69 -2.48 0.68 2.17 -2.05

(-10.10) (-5.47) (-5.70) (-10.80) (-28.06) (2.32) (3.37) (-4.43)

AS x OOS Dummy -8.64 -20.06 -5.79 -7.97

(-4.24) (-6.56) (-11.17) (-16.58)

AS x Time Trend 0.00 0.05 -0.01 0.01

(-0.99) (8.52) (-6.97) (8.38)

Adjusted R2 (in %) 5.30 6.31 5.32 7.41 0.35 0.80 0.50 0.85

Fund fixed effects No No No No Yes Yes Yes Yes

Average Score (AS) -8.11 -3.64 -6.49 -15.42 -2.11 0.65 2.10 -1.41

-9.91 -5.72 -5.55 -10.19 -28.39 2.47 3.55 -3.17

AS x OOS Dummy -7.69 -17.13 -5.07 -6.66

-4.14 -6.24 -11.11 -16.38

AS x Time Trend 0.00 0.04 -0.01 0.01

-1.03 8.01 -6.96 6.78

Adjusted R2 (in %) 4.90 5.81 4.92 6.71 0.30 0.71 0.45 0.74

Fund fixed effects No No No No Yes Yes Yes Yes

This table reports the results of fund-level panel regressions that analyze the relation between mutual fund expenses and

predictors, both in and out of sample. The regression equation is

where Feeit is the expense ratio of fund i in month t, Sijt is fund i's score on predictor j in month t, Djt is an indicator for

whether predictor j is out-of-sample in month t, and N is the number of predictors considered. In Panel A, scores are equal to

the percentile of each fund's predictors relative to the contemporaneous cross section. In Panel B, scores are equal to +1 for

predictors in the top quintile and -1 for predictors in the bottom quintile. Results are included with and without fund fixed

effects, and no intercepts are reported. T-statistics, in parentheses, are clustered by date and fund without fund fixed effects or

by date only with fixed effects. The number of observations 446,268.

Panel A: Percentile Scores

Panel B: Extreme Quintile Scores

𝐹𝑒𝑒𝑖𝑡 = 𝑎 + 𝑏1

𝑁

𝑖=1

𝑁

𝑆𝑖𝑗𝑡 + 𝑐1

𝑁

𝑖=1

𝑁

𝑆𝑖𝑗𝑡𝐷𝑗𝑡 + 𝑑 𝑡1

𝑁

𝑖=1

𝑁

𝑆𝑖𝑗𝑡 + 𝜀𝑖𝑗𝑡

Table 7

Arbitrage Activity Proxy

(Z)

Intercept Z Adj. R2 (in %)

& # of obs.

Intercept Z Adj. R2 (in %)

and # of

observationsShort interest 1.16 -32.20 0.1480 1.19 -36.44 0.2515

(4.46) (-2.24) 4713 (4.84) (-2.31) 4770

Short interest - detrended 0.72 -113.77 0.1892 0.69 -92.75 0.1564

(6.41) (-3.27) 4713 (6.62) (-2.10) 4770

Turnover 1.19 -3.63 0.2074 1.25 -4.28 0.3405

(7.64) (-3.99) 5093 (8.01) (-3.10) 5160

Turnover - detrended 0.77 -4.88 0.1318 0.76 -4.74 0.1441

(7.61) (-2.83) 5093 (8.51) (-1.79) 5160

Hedge fund AUM 1.17 -6.29 0.2531 1.16 -6.71 0.3562

(6.34) (-3.33) 4439 (7.46) (-2.96) 4496

Hedge fund AUM - detrended 0.75 -0.28 0.1485 0.72 -0.20 0.0837

(6.75) (-2.63) 4439 (7.20) (-1.39) 4496

Avg. of non-detrended arb. proxies 0.83 -0.36 0.2051 0.83 -0.41 0.3240

(8.34) (-3.77) 5093 (10.23) (-3.22) 5160

Avg. of detrended arb. proxies 0.78 -0.36 0.1726 0.77 -0.28 0.1184

(7.64) (-3.52) 5093 (8.81) (-1.72) 5160

Panel A: Q5-Q1 Panel B: CSR

This table reports the results of predictor-level panel regressions. The dependent variable is the alpha spread associated with a given

predictor divided by the average in-sample value of that same alpha spread, computed as in Table 2. The independent variable is some

proxy for the level of arbitrage activity in the market. Standard errors are clustered both by month and predictor.

Table 8A

Arbitrage Activity Proxy

(Z)

Avg. Score

(Avg S)

Avg S x Z Adj. R2 (in %)

& # of obs.

Avg. Score

(Avg S)

Avg S x Z Adj. R2 (in %)

and # of

observationsnone 3.11 0.1139 -0.70 0.0032

(4.39) 450010 (-0.67) 450010

Short interest 5.92 -161.70 0.1367 3.70 -270.39 0.0521

(4.71) (-2.17) 440693 (2.47) (-2.92) 440693

Short interest - detrended 3.42 -757.72 0.1799 -0.58 -819.54 0.0737

(4.73) (-2.82) 440693 (-0.54) (-2.92) 440693

Turnover 5.50 -16.60 0.1495 2.89 -25.72 0.0679

(5.73) (-2.67) 450010 (2.50) (-3.48) 450010

Turnover - detrended 3.28 -32.99 0.1747 -0.56 -37.91 0.0724

(4.77) (-3.08) 450010 (-0.55) (-3.35) 450010

Hedge fund AUM 5.84 -29.42 0.1556 2.52 -40.46 0.0566

(4.89) (-2.68) 430976 (1.67) (-2.96) 430976

Hedge fund AUM - detrended -0.64 -109.47 0.0954

(-0.56) (-3.44) 430976

Avg. of non-detrended arb. proxies 3.90 -1.52 0.1433 0.53 -2.58 0.0635

(5.72) (-2.48) 450010 (0.55) (-3.36) 450010

Avg. of detrended arb. proxies 3.42 -2.66 0.2016 -0.41 -3.10 0.1021

(4.97) (-3.43) 450010 (-0.40) (-3.75) 450010

This table reports the results of fund-level panel regressions that analyze the relation between ex post mutual fund alphas and various

proxies for the level of arbitrage activity. The regression equation is

where ait is the ex post alpha for fund i in month t, Avg Sit is fund i's average percentile-based score across all predictors in month t, and Zt

is an arbitrage activity proxy observable at the start of month t. Arbitrage proxies include the

T-statistics, in parentheses, are clustered by date and fund without fund fixed effects or by date only with fixed effects.

No fixed effects With fund fixed effects

𝛼𝑖𝑡 = 𝑎 + 𝑏 Avg 𝑆𝑖𝑡 + 𝑐 𝑍𝑡 Avg 𝑆𝑖𝑡 + 𝜀𝑖𝑗𝑡

Table 8B

Arbitrage Activity Proxy

(Z)

Avg. Score

(Avg S)

Avg S x Z Adj. R2 (in %)

& # of obs.

Avg. Score

(Avg S)

Avg S x Z Adj. R2 (in %)

and # of

observationsnone 2.88 0.1092 -0.52 0.0021

(4.43) 450010 (-0.58) 450010

Short interest 5.44 -147.23 0.1299 3.25 -231.39 0.0431

(4.68) (-2.13) 440693 (2.41) (-2.79) 440693

Short interest - detrended 3.15 -679.71 0.1680 -0.42 -727.13 0.0642

(4.75) (-2.72) 440693 (-0.45) (-2.79) 440693

Turnover 5.09 -15.35 0.1432 2.63 -22.55 0.0591

(5.82) (-2.73) 450010 (2.57) (-3.49) 450010

Turnover - detrended 3.04 -30.34 0.1668 -0.40 -33.88 0.0647

(4.82) (-3.14) 450010 (-0.45) (-3.36) 450010

Hedge fund AUM 5.44 -27.51 0.1504 2.33 -35.51 0.0490

(4.97) (-2.75) 430976 (1.74) (-2.93) 430976

Hedge fund AUM - detrended -0.44 -97.70 0.0852

(-0.45) (-3.41) 430976

Avg. of non-detrended arb. proxies 3.61 -1.40 0.1372 0.55 -2.24 0.0543

(5.77) (-2.52) 450010 (0.66) (-3.32) 450010

Avg. of detrended arb. proxies 3.17 -2.43 0.1909 -0.26 -2.75 0.0907

(5.02) (-3.43) 450010 (-0.30) (-3.70) 450010

This table reports the results of fund-level panel regressions that analyze the relation between ex post mutual fund alphas and various

proxies for the level of arbitrage activity. The regression equation is

where ait is the ex post alpha for fund i in month t, Avg Sit is fund i's average extreme quintile-based score across all predictors in month t,

and Zt is an arbitrage activity proxy observable at the start of month t. Arbitrage proxies include the

T-statistics, in parentheses, are clustered by date and fund without fund fixed effects or by date only with fixed effects.

No fixed effects With fund fixed effects

𝛼𝑖𝑡 = 𝑎 + 𝑏 Avg 𝑆𝑖𝑡 + 𝑐 𝑍𝑡 Avg 𝑆𝑖𝑡 + 𝜀𝑖𝑗𝑡

Table 9

Non-detrended Detrended

0.86 -0.09 -0.33 0.1870

(7.04) (-0.49) (-2.98) 5093

0.93 -0.40 -0.30 0.2169

(7.21) (-2.44) (-2.76) 5093

0.55 -0.13 -0.43 0.00 0.1745

(0.66) (-0.58) (-1.56) (0.38) 5093

1.34 -0.11 -0.31 0.00 0.2333

(3.28) (-0.41) (-3.21) (-1.15) 5093

0.85 -0.06 -0.39 0.3057

(9.53) (-0.37) (-2.44) 5160

0.96 -0.51 -0.21 0.2169

(10.29) (-3.29) (-1.28) 5160

1.16 -0.02 -0.29 0.00 0.2944

(1.22) (-0.12) (-0.81) (-0.34) 5160

1.69 -0.01 -0.22 0.00 0.3352

(3.84) (-0.04) (-1.37) (-1.94) 5160

Panel A: Q5-Q1

Panel B: CSR

InterceptOut-of-sample

indicator

Arbitrage activity

This table reports the results of predictor-level panel regressions. The dependent variable is the alpha spread

associated with a given predictor divided by the average in-sample value of that same alpha spread, computed as in

Table 2. The independent variables include an out-of-sample indicator, a composite measure of arbitrage activity,

and a time trend. Standard errors are clustered both by month and predictor.

Time trendAdj. R

2 (in %) &

# of obs.

Table 10

2.99 (2.21) 2.14 (0.78) -2.21 (-1.75) 0.1480 No

3.33 (3.28) 0.16 (0.12) -2.69 (-3.24) 0.2015 No

-7.16 (-2.51) -0.69 (-0.22) -4.83 (-3.22) 0.03 (3.12) 0.1882 No

2.08 (1.08) -0.85 (-0.28) -2.70 (-3.31) 0.00 (0.49) 0.2028 No

0.53 (0.38) -0.01 (-0.00) -2.58 (-2.11) 0.0633 Yes

0.86 (0.76) -2.37 (-1.53) -2.81 (-3.41) 0.1104 Yes

-8.69 (-2.86) -2.69 (-0.90) -4.80 (-3.08) 0.03 (2.63) 0.0907 Yes

0.42 (0.23) -2.72 (-0.93) -2.81 (-3.40) 0.00 (0.18) 0.1103 Yes

2.93 (2.45) 1.65 (0.68) -1.93 (-1.71) 0.1404 No

3.15 (3.44) 0.02 (0.02) -2.43 (-3.21) 0.1907 No

-6.52 (-2.56) -0.84 (-0.31) -4.39 (-3.23) 0.03 (3.26) 0.1794 No

1.86 (1.09) -1.00 (-0.37) -2.45 (-3.30) 0.00 (0.57) 0.1924 No

0.71 (0.61) -0.40 (-0.18) -2.11 (-2.02) 0.0542 Yes

0.89 (0.92) -2.15 (-1.61) -2.49 (-3.33) 0.0988 Yes

-7.84 (-2.90) -2.71 (-1.12) -4.22 (-3.02) 0.02 (2.78) 0.0811 Yes

0.12 (0.08) -2.74 (-1.15) -2.49 (-3.32) 0.00 (0.38) 0.0990 Yes

Fund FE

Panel B: Extreme quintile scores

Panel A: Percentile scores