outlook and challenges for oil supply-demand in asia · asia’s oil demand expected to rise,...

TRANSCRIPT

1

Outlook and Challenges for Oil Supply-Demand in Asia

4th IEEJ/CNPC Joint SeminarJapan-China Joint Symposium on Asian Oil & Gas

December 10th, 2010

Ken Koyama, PhDDirector

Institute of Energy Economics, Japan

©2010 Institute of Energy Economics, Japan

All rights reserved

IEEJ: January 2011

Ken Koyama, IEEJ December 10th, 2010

2

©2010 IEEJ, All rights reserved

Presentation Topic

Growing energy demand in Asia, fossil fuels as a centerpiece

Asia’s oil demand expected to rise, driven by Chinese growth, and its implications

Outlook for global gas supply-demand and the importance of Asian market

Impacts of “Advanced technology” on global/Asian energy supply-demand and its implications

Conclusion

IEEJ: January 2011

Ken Koyama, IEEJ December 10th, 2010

3

©2010 IEEJ, All rights reserved

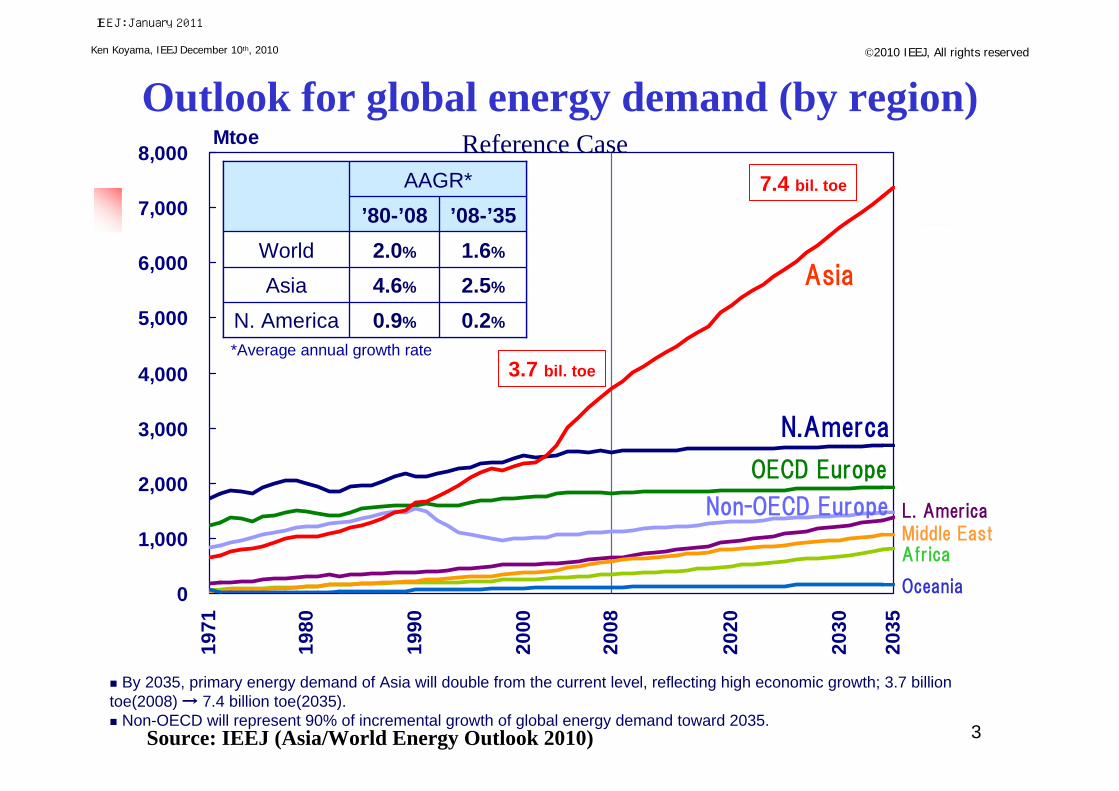

Outlook for global energy demand (by region)

Source: IEEJ (Asia/World Energy Outlook 2010)

By 2035, primary energy demand of Asia will double from the current level, reflecting high economic growth; 3.7 billion toe(2008) → 7.4 billion toe(2035). Non-OECD will represent 90% of incremental growth of global energy demand toward 2035.

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

1971

1980

1990

2000

2008

2020

2030

2035

Mtoe

Asia

N.Amerca

OECD Europe

Non-OECD Europe L. AmericaMiddle EastAfrica

Oceania

2.5%4.6%Asia0.2%0.9%N. America

1.6%2.0%World’08-’35’80-’08

AAGR*

2.5%4.6%Asia0.2%0.9%N. America

1.6%2.0%World’08-’35’80-’08

AAGR*

3.7 bil. toe

7.4 bil. toe

*Average annual growth rate

Reference Case

IEEJ: January 2011

Ken Koyama, IEEJ December 10th, 2010

4

©2010 IEEJ, All rights reserved

0

500

1,000

1,500

2,000

2,500

3,000

3,500

1971 1980 1990 2000 2008 2020 2030 2035

石油換算百万トン

2.2%2.9%Oil

1.9%5.3%Coal

4.2%7.6%Gas

2.5%4.6%Total

’08-’35’80-’08

Reference caseAAGR

Oil29%→26%

Coal53%→45%

Gas10%→16%

Nuclear3.7%→6.4%

Renewable1.7%→4.9%

Hydro2.1%→2.0%

Fossil fuel93%→87%

Share in 08→ in 2035

Outlook for energy demand in Asia (by fuel)

Source: IEEJ (Asia/World Energy Outlook 2010)

MTOE Reference Case

IEEJ: January 2011

Ken Koyama, IEEJ December 10th, 2010

5

©2010 IEEJ, All rights reserved

0

500

1000

1500

2000

1971 1980 1990 2000 2008 2020 2030 2035

China IndiaJapan KoreaTaiwan IndonesiaMalaysia PhilippinesThailand VietnamSingapore Hong KongOther Asia Tech. Adv.

Mtoe

8%

46%

17%

20%

14%

34%China

India

Japan

Though the vehicles’ fuel efficiency may be improved, and clean energy vehicles may expand, oil demand in China will expand from 7.4 million B/D in 2008 to 19.0 million B/D in 2035, due mainly to its escalating vehicle ownership. The share of China and India together in Asian oil demand will grow from 46% in 2008 to 61% in 2035. Even in the Tech. Adv. Scenario, oil demand will not peak out and grow continuously. Projected oil demand saving will be equal to 21% of the Reference Scenario in 2035.

20081.07 bil

(216 mbd)↓

2035Reference

1.91 bil (386 mbd)Tech. Adv.

1.49 bi l(301 mbd)

4.1 bil

(21%)Reduction

AAGR China India Japan Korea Taiwan Singapore

1980-2008 5.2% 5.4% -0.3% 4.4% 2.7% 2.9%2008-2035 3.3% 3.0% -1.6% 0.4% 0.4% 0.6%

Indonesia Malaysia Phi l i ppi nes Thailand Vietnam Other As ia

3.9% 4.2% 0.8% 4.9% 7.5% 3.6%2.1% 2.0% 3.3% 1.8% 3.7% 3.8%

Outlook for oil demand in Asia (by country)Reference Case and Tech. Advanced Case

Source: IEEJ (Asia/World Energy Outlook 2010)

IEEJ: January 2011

Ken Koyama, IEEJ December 10th, 2010

6

©2010 IEEJ, All rights reserved

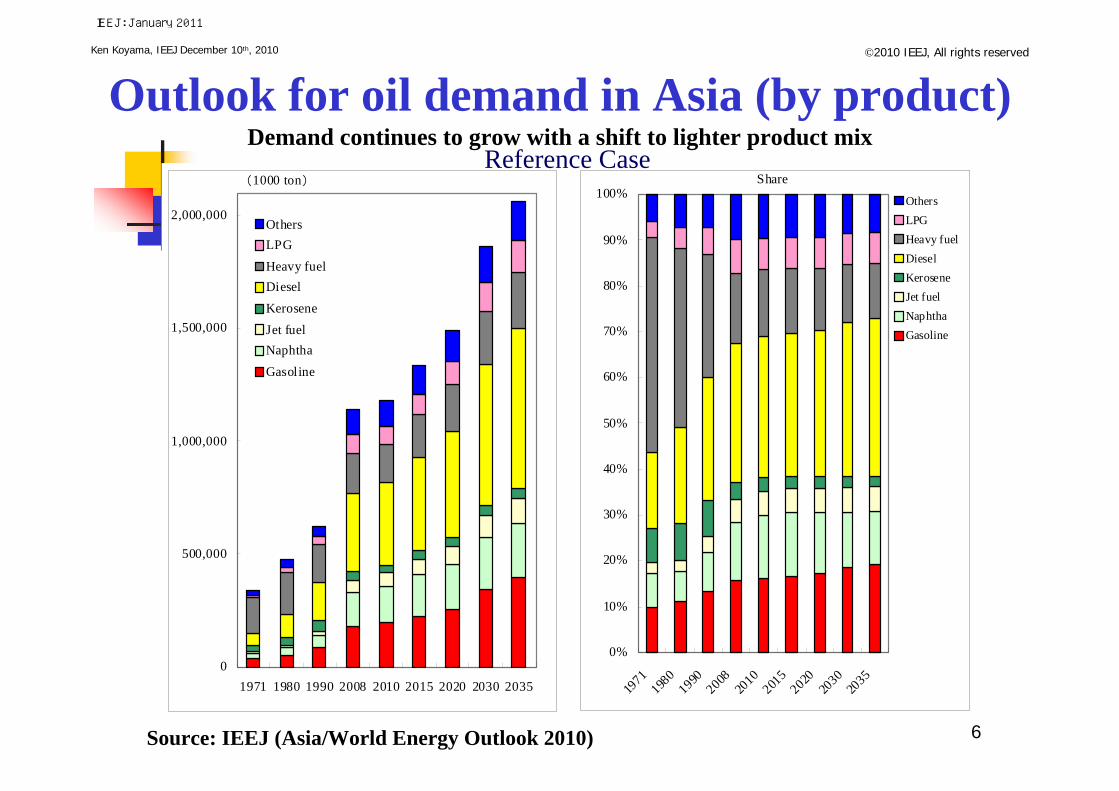

Outlook for oil demand in Asia (by product)Demand continues to grow with a shift to lighter product mix

Source: IEEJ (Asia/World Energy Outlook 2010)

0

500,000

1,000,000

1,500,000

2,000,000

1971 1980 1990 2008 2010 2015 2020 2030 2035

OthersLPGHeavy fuelDieselKeroseneJet fuelNaphthaGasoline

(1000 ton)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1971

1980

1990200820

10201

5202020

3020

35

OthersLPGHeavy fuelDieselKeroseneJet fuelNaphthaGasoline

ShareReference Case

IEEJ: January 2011

Ken Koyama, IEEJ December 10th, 2010

7

©2010 IEEJ, All rights reserved

Outlook for oil supply-demand in AsiaOil import dependence expected to rise in Asia

Source: IEEJ (Asia/World Energy Outlook 2010)

479612

1,067

1,380

1,720

1,901

229304 372 390 367 353

250 308

695

990

1,353

1,548

0

500

1,000

1,500

2,000

2,500

1980 1990 2008 2020 2030 2035

Demand Production Net import

52%51%

63%

72%

79%81%

76%Mtoe Tech. Adv.

Net oil import in Asia will expand from 14 mb/d (695 Mtoe) in 2008 to 31 mb/d (1,548 Mtoe) in 2035. Oil production in Asia (such as China, India, Indonesia and Malaysia) will marginally increase, while oil demand will steadily increase. Therefore, net oil import ratio will reach 81% in the Reference Scenario, and 76% in the Tech. Adv. Scenario by 2035 (compared with 63% in 2008).

Reference Case

IEEJ: January 2011

Ken Koyama, IEEJ December 10th, 2010

8

©2010 IEEJ, All rights reserved

Competition for Access to Energy Resources

Growing import dependence is perceived as “vulnerability”

Strategy being taken as a counter measure: Domestic energy resource development Energy diversification Overseas resource development Promotion of NOCs

Excessive (exclusive) pursuit of “Mercantilism”may lead to politicize and destabilize world energy markets

Behavior of emerging giants attracts attentions in global energy community

IEEJ: January 2011

Ken Koyama, IEEJ December 10th, 2010

9

©2010 IEEJ, All rights reserved

9

China’s importance in global energy landscape

Political/strategic aspects Growing influence in global politics, economy and energy market Rapidly expanding China’s presence and concerns for China’s

“Assertiveness” Uncertainty over future economic growth and social stability Strategy implementation to enhance energy security and its impacts Climate change policy and its impacts on international negotiation

Energy demand 2nd largest in total energy consumption, oil consumption and oil

import in 2009. The respective global share is 20%、10%、10%

Annual consumption growth rates in 2009 are: 9% for total energy; 7% for oil; 9% for gas; and 10% for coal

Demand continued to grow even in 2008-2009. Increasingly higher presence in global market

Energy demand is expected to grow in the long run, backed by economic growth, motorization, etc.

NO1 emitter of CO2 in 2009 (global share 24%)

Energy supply Domestic oil production grew only gradually, and China became a

net importer of oil in 1993. Net import continued to grow strongly China also became net gas and coal importer

IEEJ: January 2011

Ken Koyama, IEEJ December 10th, 2010

10

©2010 IEEJ, All rights reserved

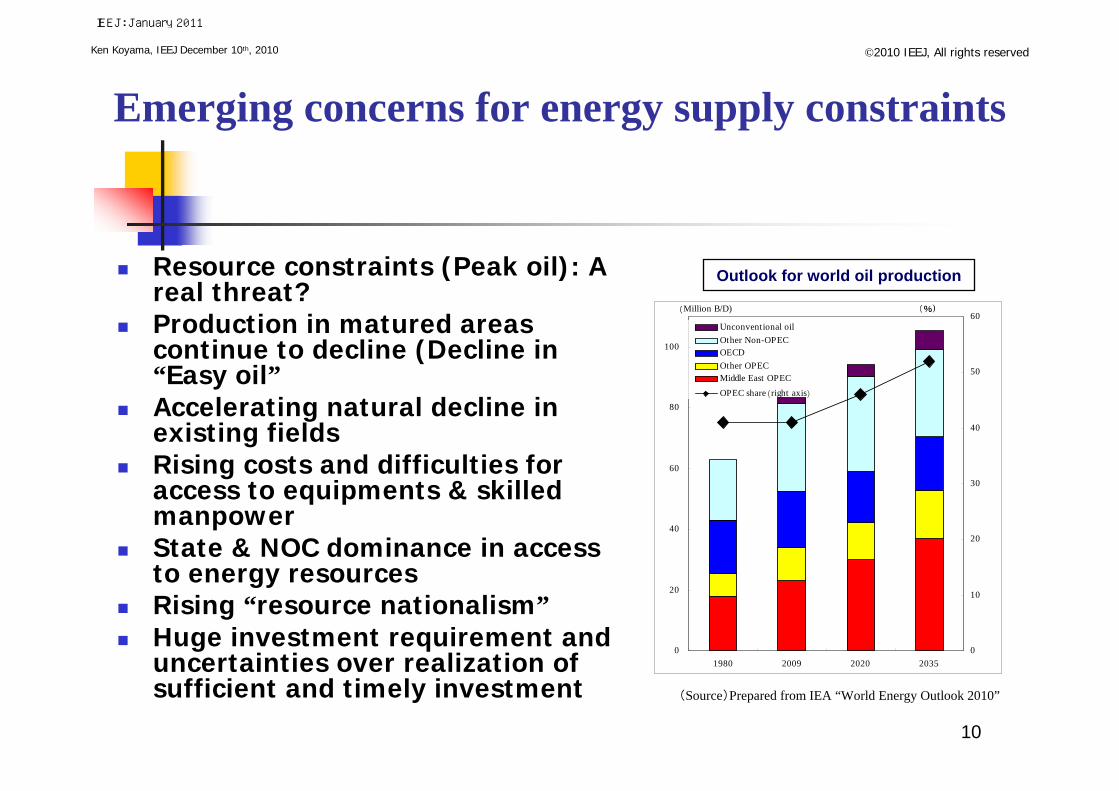

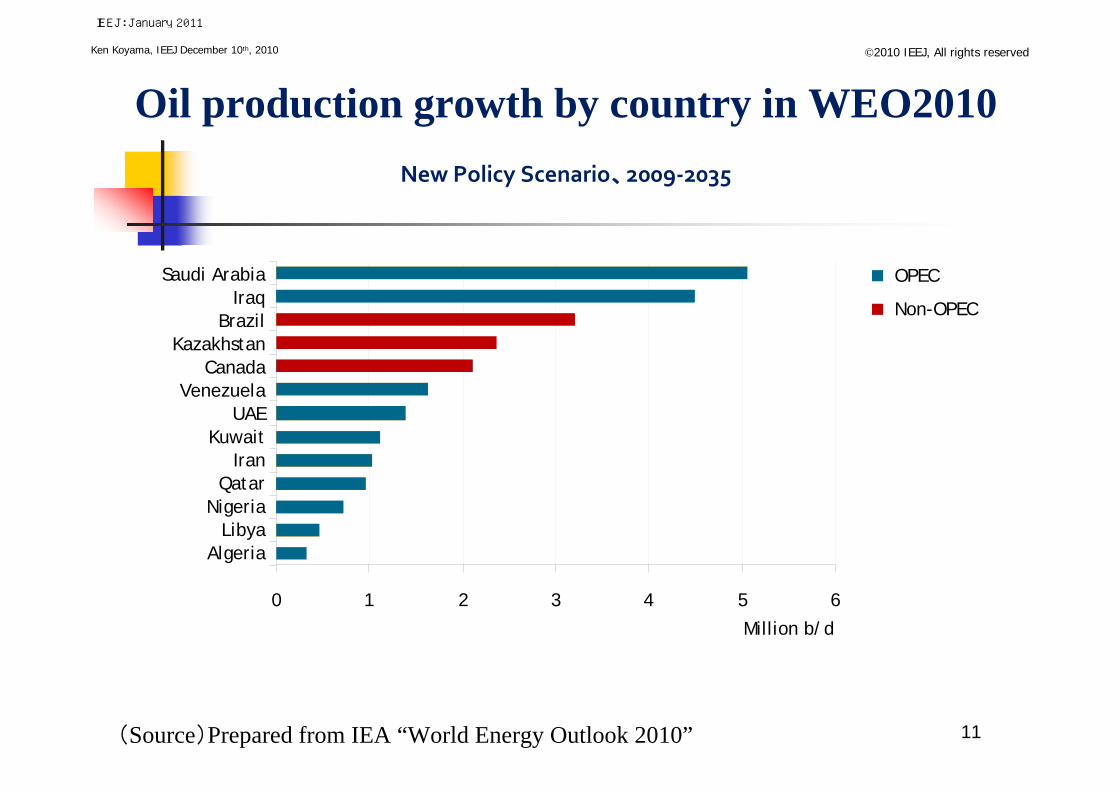

Outlook for world oil production

(Source)Prepared from IEA “World Energy Outlook 2010”

Resource constraints (Peak oil): A real threat?

Production in matured areas continue to decline (Decline in “Easy oil”

Accelerating natural decline in existing fields

Rising costs and difficulties for access to equipments & skilled manpower

State & NOC dominance in access to energy resources

Rising “resource nationalism” Huge investment requirement and

uncertainties over realization of sufficient and timely investment

Emerging concerns for energy supply constraints

0

20

40

60

80

100

1980 2009 2020 20350

10

20

30

40

50

60Unconventional oilOther Non-OPECOECDOther OPECMiddle East OPEC

OPEC share(right axis)

(Million B/D) (%)

IEEJ: January 2011

Ken Koyama, IEEJ December 10th, 2010

11

©2010 IEEJ, All rights reserved

Oil production growth by country in WEO2010

0 1 2 3 4 5 6

AlgeriaLibya

NigeriaQatar

IranKuwait

UAEVenezuela

CanadaKazakhstan

BrazilIraq

Saudi Arabia

Million b/d

OPEC

Non-OPEC

New Policy Scenario、2009‐2035

(Source)Prepared from IEA “World Energy Outlook 2010”

IEEJ: January 2011

Ken Koyama, IEEJ December 10th, 2010

12

©2010 IEEJ, All rights reserved

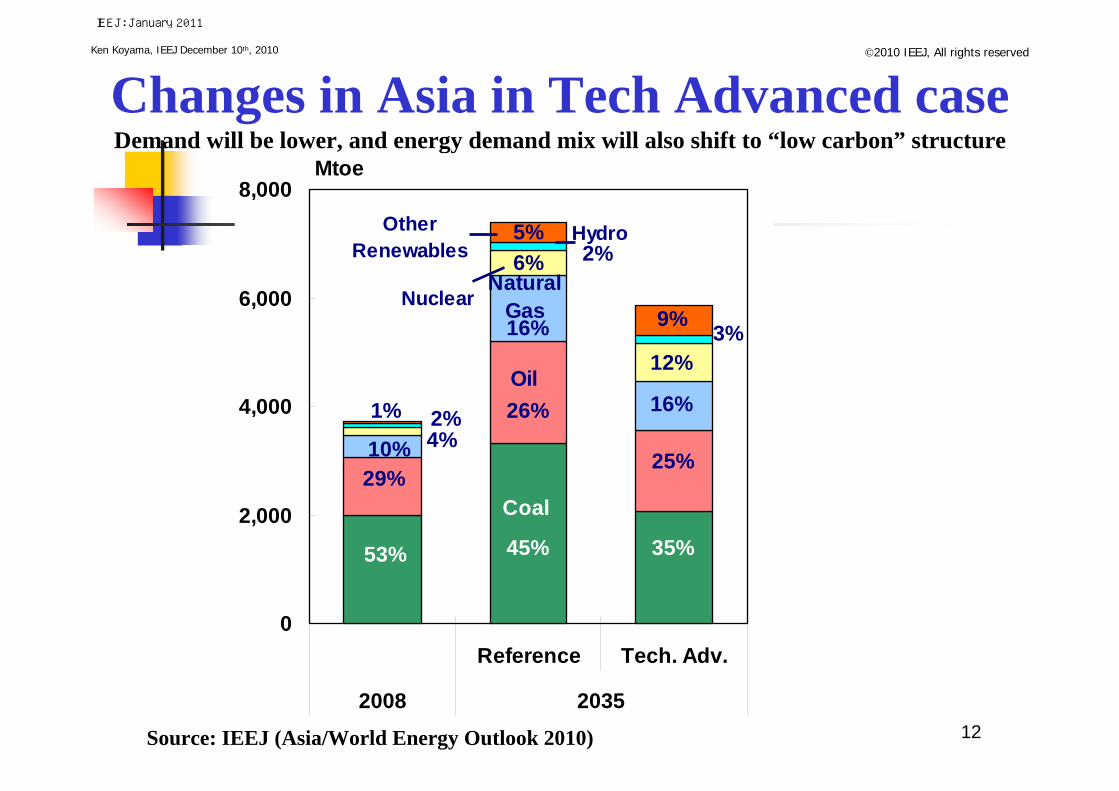

Changes in Asia in Tech Advanced caseDemand will be lower, and energy demand mix will also shift to “low carbon” structure

Source: IEEJ (Asia/World Energy Outlook 2010)

0

2,000

4,000

6,000

8,000

Reference Tech. Adv.

2008 2035

Mtoe

53%

29%10% 4%

45%

26%

16%

6% 2%5%

35%

25%

16%

12%3%9%

2%1%

Coal

Oil

NaturalGasNuclear

HydroOtherRenewables

IEEJ: January 2011

Ken Koyama, IEEJ December 10th, 2010

13

©2010 IEEJ, All rights reserved©2010 IEEJ, All rights reserved

Middle East Oil Export Destination

(Source)BP Statistical Review of World Energy 2010

April 8th, 2010 Ken Koyama, IEEJ

0

5,000

10,000

15,000

20,000

25,000

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

40

45

50

55

60

65

70

75OthersEuropeUSAsiaAsia's share

(1,000B/D) (%)

IEEJ: January 2011

Ken Koyama, IEEJ December 10th, 2010

14

©2010 IEEJ, All rights reserved

Outlook for Russian oil productionUncertainty over long term prospects for oil production. Frontier development is a key

(Source) prepared from EIA、IEA、OPEC data

Russian oil production outlook by organization Russian government oil production outlook

(Source)prepared from “Russia’s energy strategy 2030”

0)

10.0

10.2 10.2

9.1

10.2

12.8

9.5

9.4

10.6

7

8

9

10

11

12

13

00 05 10 15 20 25 30 35

milli

on b

/d

Actual

IEA/OMR (Nov.10)

MTOMR (2010)

IEO (2010)

WEO (2010)

OPEC (2010)

0

100

200

300

400

500

600

2005 2008 2013-15 2020-22 2030

milli

on to

ns

Far East

East Siberia

Tomsk

Caucasus/CaspianUral

Volga

Northwest

Tyumeni

IEEJ: January 2011

Ken Koyama, IEEJ December 10th, 2010

15

©2010 IEEJ, All rights reservedImpact and implication of US unconventional gas revolution Impacts

Lower US LNG demand impacts on global gas market Higher expectation for role of Gas in US, as important domestic energy source as well as

low carbon/clean energy Expectation for unconventional gas development outside US

Challenges Lower gas price and it impacts on gas development economics Unconventional gas development and its impacts on environmental/pollution problem

World unconventional gas resourceDownward revision for US LNG demand by EIA

Source:“Tight Gas Sands”, Journal of Petroleum Technology(2006/6)

CBM Shale gas Tight gas TotalRegion tcf tcf tcf tcfN America 3,017 3,840 1,371 8,228C&S America 39 2,116 1,293 3,448W Europe 157 509 353 1,019C&E Europe 118 39 78 235FSU 3,957 627 901 5,485Middle East / N Africa 0 2,547 823 3,370Sub-Sahara Africa 39 274 784 1,097China and Plannned Economy Asia 1,215 3,526 353 5,094OECD Pacific 470 2,312 705 3,487Other Asia 0 313 549 862S Asia 39 0 196 235World 9,051 16,103 7,406 32,560

14

15

16

17

18

19

20

21

22

23

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23

tcf

0

10

20

30

40

50

60

70

80

90

100

LNG

milli

on to

ns

Domestic production(AEO2010)

Domestic production(AEO2008)

LNG imports(AEO2008)

LNG imports(AEO2010)

IEEJ: January 2011

Ken Koyama, IEEJ December 10th, 2010

16

©2010 IEEJ, All rights reserved

Issues for global gas supply-demand

Global gas demand expected to grow in the long run While impact of climate change policy on gas demand remain uncertain, expectation

for gas is rising worldwide, as gas being regarded as important and realistic low carbon/clean energy option as well as domestic energy source

Gas supply security will become important agenda in many countries, as gas demand continues to grow which results in higher gas import dependence

Ample supply potential exists to meet growing demand In addition to conventional source, unconventional resource potential is very large Supply can keep up with demand, if timely investment is materialized Share of unconventional gas supply will increase gradually in global supply mix

Issues to be considered for future outlook How long the current supply surplus can last? To what extent will US “shale gas revolution” affect and change other regional gas

market including Asian market What is the impact of expanded gas utilization on other source of energy?

Analysis based on the follow-up of changing global gas situation is essential

IEEJ: January 2011

Ken Koyama, IEEJ December 10th, 2010

17

©2010 IEEJ, All rights reserved

Global gas demand outlook(dotted line for Tech Advanced case)

Outlook for global and Asian gas demandGas demand in Asia (and in China) is key to global demand growth, which will affect global supply-demand balance

Source: IEEJ (Asia/World Energy Outlook 2010)

Asia gas demand outlook(dotted line for Tech Advanced case)

Asia

N.America

Europe

Others

0

1000

2000

3000

4000

5000

1971 1980 1990 2000 2008 2020 2030 2035

27%

15%

29%

30%

15%

24%

39%

21%

1.9 bil.toe

Mtoe

33

794

266

783

2%

42%

14%

42%

Asia N.America Europe Others

Increase from 2008~2035

0

300

600

900

1200

1971 1980 1990 2000 2008 2020 2030 2035

China India

Japan Korea

Taipei Indonesia

Malaysia Philippines

Thailand Vietnam

Singapore Hong Kong

Other Asia Tech. Adv.

China

IndiaJapan

Mtoe

7%

35%

14%

9%

17%

21%

AAGR China India Japan Korea Taipei Singpore

1980-2008 6.4% 12.7% 5.0% - 7.1% -

2008-2035 6.9% 5.9% 0.3% 1.5% 4.0% 2.7%

Indonesia Malaysia Phi l i ppi nes Thailand Vietnam Other As ia

6.9% 10.6% - - - 6.7%4.7% 2.6% 4.5% 3.1% 3.1% 4.2%

IEEJ: January 2011

Ken Koyama, IEEJ December 10th, 2010

18

©2010 IEEJ, All rights reserved

0

500

1,000

1,500

2,000

2,500

3,000

3,500

1971 1980 1990 2000 2008 2020 2030 2035

Mtoe

2.2%2.9%Oil

1.9%5.3%Coal

4.2%7.6%Natural Gas

2.5%4.6%Total

’08-’35

’80-’08

ReferenceAAGR

Oil29%→26% [25%]

Coal53%→45% [35%]

Natural Gas10%→16% [16%]

Nuclear3.7%→6.4%

[12%]Other

Renewables1.7%→4.9%

[9.3%]Hydro

2.1%→2.0%[2.6%]

Fossil fuel93%→87% [76%]

Solid line: ReferenceDotted line: Tech. Adv.

Share:2008→2035(Reference)

[2035(Tech. Adv.)]

Coal and oil will continue to maintain the dominant share in Asian energy demand through 2035. The share of natural gas will increase substantially reaching 16% by 2035, driven mainly by power generation. Coal share in the Tech. Adv. Scenario will significantly decrease, but will maintain the largest share (35% of total) in primary energy mix by 2035.

Source: IEEJ (Asia/World Energy Outlook 2010)

Outlook for energy demand in Asia (by fuel)IEEJ: January 2011

Ken Koyama, IEEJ December 10th, 2010

19

©2010 IEEJ, All rights reserved

Fossil fuel demand will peak in 2035 under the Tech. Adv. Scenario. In the Tech. Adv. Scenario, the world oil demand will decrease from 82 mbd in 2008 to 78 mbd in 2050, and world coal, from 4.6 Btce in 2008 to 3.4 Btce in 2050. By contrast, natural gas demand will continue to increase towards 2050 even in the Tech. Adv. Scenario. Adequate investment needs to be maintained to explore and develop natural gas resources.

Oil

Coal

Gas

Nuclear

Other RenewablesHydro

* Solid line: ReferenceDotted line: Tech. Adv.

Fossil Fuel (Right Axis)

Source: IEEJ (Asia/World Energy Outlook 2010)

Outlook for global energy demand up to 2050

IEEJ: January 2011

Ken Koyama, IEEJ December 10th, 2010

20

©2010 IEEJ, All rights reserved

Conclusion

Many challenges and uncertainty remain in global energy landscape

Under the circumstance, Asia’s energy demand will grow substantially lead by China’s growth

Asia’s growth is the driver for global demand for oil and gas. The demand growth results in challenges for supply-demand balance and market stability

Advanced technology will change Asia’s energy supply-demand. However, oil and gas will remain as important energy in the region, and its market stability continues to be crucial agenda

IEEJ: January 2011

Ken Koyama, IEEJ December 10th, 2010

21

©2010 IEEJ, All rights reserved

Annex

IEEJ: January 2011

Ken Koyama, IEEJ December 10th, 2010

22

©2010 IEEJ, All rights reserved

Annex 1 Oil price assumption in WEO 2010 (IEA)

0

20

40

60

80

100

120

140

1980 1990 2000 2010 2020 2030 2035

$/bb

l (20

09 P

rice

Current Policy Scenario

New Policy Scenario

450 Scenario

(Source)Prepared from IEA “World Energy Outlook 2010”

IEEJ: January 2011

Ken Koyama, IEEJ December 10th, 2010

23

©2010 IEEJ, All rights reserved

Annex 2 Outlook for oil product demand in China

Source: IEEJ (Asia/World Energy Outlook 2010)

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

900,000

1,000,000

1971 1980 1990 2008 2010 2015 2020 2030 2035

OthersLPGHeavy fuelDieselKeroseneJet fuelNaphthaGasoline

(1000 ton)

0%

20%

40%

60%

80%

100%

1971

1980

1990200820

10201

5202020

3020

35

OthersLPGHeavy fuel

DieselKeroseneJet fuelNaphthaGasoline

Share

IEEJ: January 2011

Ken Koyama, IEEJ December 10th, 2010

24

©2010 IEEJ, All rights reserved

24

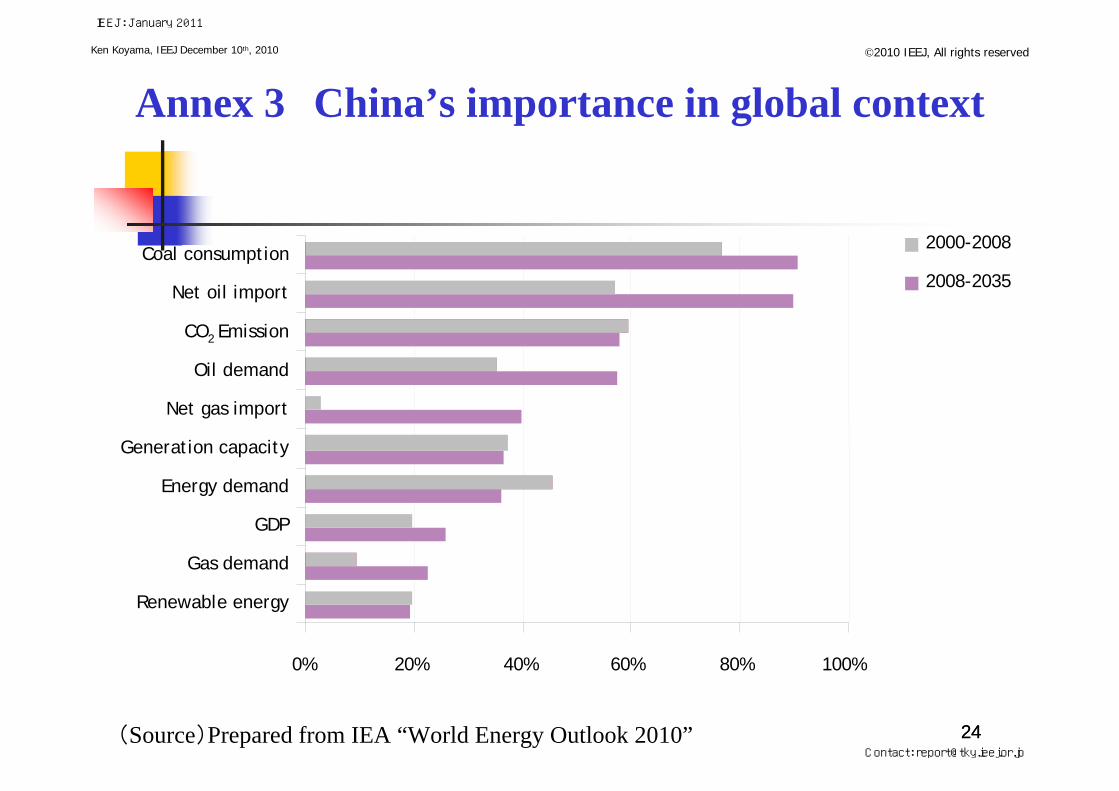

Annex 3 China’s importance in global context

0% 20% 40% 60% 80% 100%

Renewable energy

Gas demand

GDP

Energy demand

Generation capacity

Net gas import

Oil demand

CO2 Emission

Net oil import

Coal consumption2000-2008

2008-2035

(Source)Prepared from IEA “World Energy Outlook 2010”

IEEJ: January 2011

Contact: [email protected]