output based aid - world banksiteresources.worldbank.org/intsdnet/resources/obareview_final... ·...

TRANSCRIPT

THE WORLD BANK GROUP

Output Based Aid A Compilation of Lessons Learned and

Best Practice Guidance

Final Draft

September 2009

GPOBA and IDA-IFC Secretariat

2

Acknowledgments

This paper has been prepared by a team led by Yogita Mumssen (FEU), comprising Lars Jo-

hannes and Geeta Kumar (GPOBA) and Vyjayanti Desai (IDA-IFC Secretariat), with the support

of Inga Murariu, Daniel Coila, and Mark Njore (GPOBA), under the supervision of GPOBA

Program Manager Patricia Veevers-Carter and IDA-IFC Secretariat Director Nigel Twose.

GPOBA and the IDA/IFC Secretariat would like to extend special thanks to the peer reviewers:

Amie Batson (MDW), Andreas Schliessler (ECSSD), Dana Rysankova (AFTEG), Juan-Navas

Sabater (CITPO), Logan Brenzel (HDNHE), and Luiz Claudio Martins Tavares (AFTU1).

Additional comments and contributions were provided by the following OBA practitioners:

Carmen Nonay, Catherine Russell, and Esther Loening (GPOBA), Cledan Mandri-Perrot, Iain

Menzies and Mustafa Hussain (FEU), Xavier Chauvot de Beauchene (MNSSD), Dirk Sommer

(CIADR), and Martin Schmidt (KfW).

Special thanks to the comments and guidance provided by the OBA Advisory Committee that

met in February 2009, comprising: Alejandro Jadresic and Irving Kuczynski (GPOBA Indepen-

dent Panel of Experts), Adriana Aguinaga (CINPW), Amie Batson (MDW), Doyle Gallegos

(CITPO), Gaiv Tata (CFP), Hartwig Schafer (SDNVP), Magda Lovei (EASOP), Marc Juhel

(ETWTR), Neil Gregory (FPDVP), Penelope Brook (GIADR), Tjaarda Storm Van Leeuwen

(AFTEG), and, Vijay Jagannathan (EASIN).

3

Acronyms and Abbreviations

ACGF Africa Catalytic Grown Fund

AFR Sub-Saharan Africa Region

AusAID Australian Agency for International Development

BPHS Basic Package of Health Services

CBO Community-Based Organization

CCT Conditional Cash Transfers

CGDEV Center for Global Development

CITPO Policy Division (IBRD Telecommunications and Informatics)

COD Cash-on-delivery Aid

CREMA Contrato de Recuperación y Mantenimiento

DFID UK Department for International Development

DPL Development Policy Lending

DPO Development Policy Operation

DRC Democratic Republic of the Congo

EAP East Asia and Pacific Region

ECA Europe and Central Asia Region

ECLAC United Nations Economic Commission for Latin America and the Caribbean

EMW East-Meets West

ESCO Energy Service Company

ESMAP Energy Sector Management Assistance Program

EU European Union

FDT Fund for the Telecommunications Development

FDT Telecommunications Development Fund

FITEL Peru‘s Fund for Telecommunications Investment

FONDETEL Fund for the Telephony Development

FPD Finance and Private Sector Development

FSSAP Bangladesh Female Secondary School Assistance Project

GEF Global Environment Facility

GPOBA Global Partnership on Output-Based Aid

HH Household

IADB Inter-American Development Bank

IBRD International Bank for Reconstruction and Development

ICB International Competitive Bidding

ICR Implementation Completion Report

ICT Information and Communication Technology

IDA International Development Association

IDB Islamic Development Bank

IDCOL Infrastructure Development Company Limited

IDTR Decentralized Infrastructure for Rural Transformation

IFC International Finance Corporation

IMF International Monetary Fund

INDH National Initiative for Human Development

JHU Johns Hopkins University

KfW Kreditanstalt für Wiederaufbau

LCR Latin America and Caribbean Region

MCC Millennium Development Corporation

MDG Millennium Development Goal

MENA Middle East and North Africa Region

MFI Microfinance Institution

4

MIGA Multilateral Investment Guarantee Agency

MMR Manila Metropolitan Region

MPOH Ministry of Public Health

MSC Medium-Term Service Contract

MTR Mid-Term Review

MWC Manila Water Company

NGO Non-governmental organization

NHAI National Highways Authority of India

NHDP National Highways Development Project

NHSPT National Health Services Purchasing Team

NPV Net Present Value

NWDP National Water Development Project

O&M Operating and Maintaining

OBA Output Based Aid

OECD Organization for Economic Cooperation and Development

OPCS Operations Policy and Country Services

PBS Rural Electric Cooperatives

PER Guatemala Rural Electrification Scheme

PERMER Renewable Energy for Rural Markets Project (Argentina)

PHSPT Provincial Health Services Purchasing Team

PMMR Performance-Based Maintenance and Management of Roads

PNFP Private Not-For-Profit

PPA Performance-Based Partnership Agreements

PPER Senegal Rural Electrification Priority Programs

PPIAF Public Private Infrastructure Advisory Facility

PPP Public Private Partnership

PRSC Poverty Reduction Support Credit

PSD Private Sector Development

PV Photo-Voltaic

QEII Queen Elizabeth II Hospital

RBF Results-Based Financing

REB Rural Electrification Board

REF Rural Electrification Funds

SANRAL South African National Road Agency

SAR South Asia Region

SDN Sustainable Development Network

SHS Solar Home Systems

SIAS Guatemala‘s Integrated Healthcare System

SIDA Swedish International Development Cooperation Agency

SMME Small, Medium, and Micro Enterprises

SOE State Owned Enterprises

SPUG Small Power Utility Group

STD Sexually Transmitted Disease

SWAp Sector Wide Approach

UAF Universal Access Funds

UNDP United Nations Development Program

USAID United States Agency for International Development

USF Universal Service Funds

WASIS Water Services and Institutional Support Project

WBG World Bank Group

WSP Water and Sanitation Program

5

Table of Contents

Executive Summary ...................................................................................................................................... 8 1. Introduction ............................................................................................................................................. 14

1.1 Background .................................................................................................................. 14 1.2 Objective and Audience ............................................................................................... 14

1.3 Execution of Review/Methodology .............................................................................. 14 1.4 Structure of Report ....................................................................................................... 16

2. Context ................................................................................................................................................... 17 2.1 Definitions .................................................................................................................... 17

2.2 Traditional vs. OBA approaches .................................................................................. 17 2.3 Contracting out service delivery: the spectrum ............................................................ 19 2.4 Applications of the OBA approach .............................................................................. 20

2.5 OBA as part of the Results-Based Agenda .................................................................. 21 3. Snapshot of OBA in the WBG and Beyond ........................................................................................... 22

3.1 Universe of OBA under review .................................................................................... 22 3.2 Funding OBA ............................................................................................................... 24

3.3 Sector focus .................................................................................................................. 26 4. Lessons Learned: Cross-cutting Challenges and Best Practice .............................................................. 27

4.1 Transparency: Explicit targeting of subsidies for the poor .......................................... 29 4.2 Accountability: Shifting performance risk to providers ............................................... 33

4.3 Private sector capital and expertise .............................................................................. 42 4.4 Innovation and efficiency ............................................................................................. 46 4.5 Sustainability, Tariffs and the Enabling Environment ................................................. 50

4.6 Monitoring of results .................................................................................................... 55 5. Key Considerations and Next Steps ....................................................................................................... 57

5.1 ―External‖ challenges and possible responses by the WBG ........................................ 57 5.2 ―Internal‖ challenges and possible responses by WBG ............................................... 60

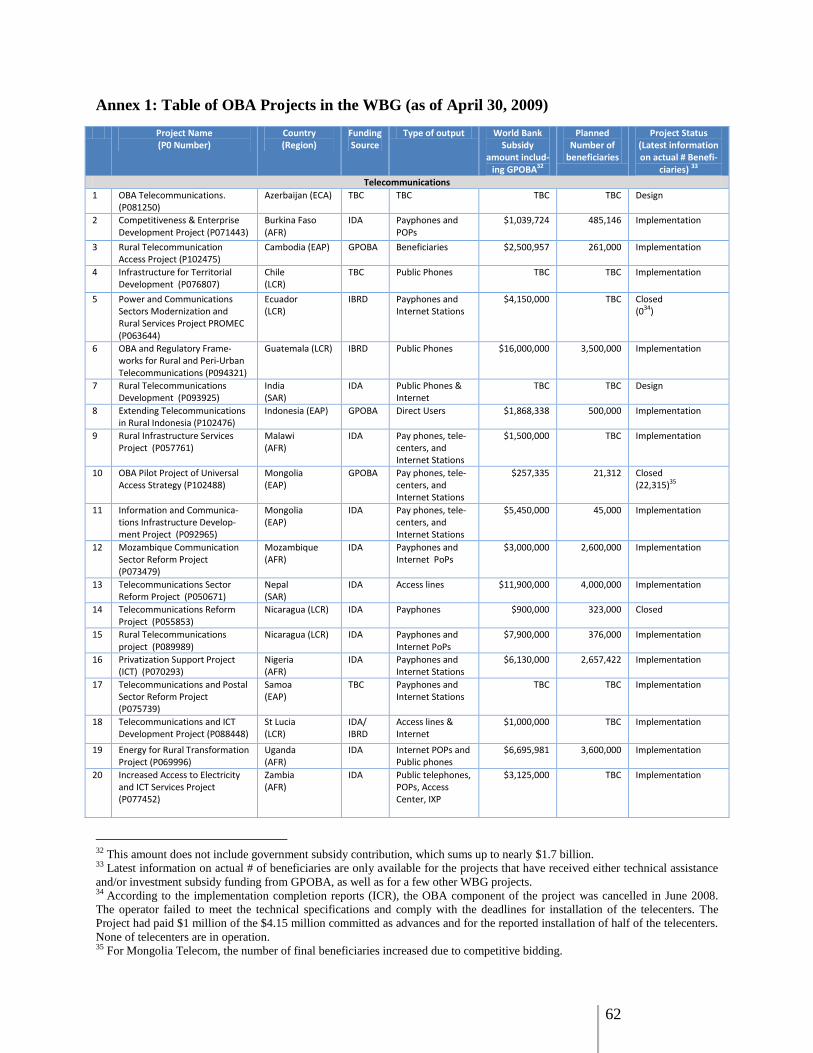

Annex 1: Table of OBA projects in the WBG (as of April 30, 2009) .......................................... 62

Annex II: Sector Specific Lessons ............................................................................................... 68 A. ICT ................................................................................................................................ 68

B. Roads ............................................................................................................................ 77 C. Energy .......................................................................................................................... 87 D. Water ............................................................................................................................ 98 E. Health ......................................................................................................................... 107 F. Education .................................................................................................................... 117

Annex III: Comparison of OBA portfolio to total WBG portfolio FY 2000 – 2009 .................. 123

6

Figures, Tables, and Boxes

Figures

Figure 1: Volume of OBA Subsidy by Sector and Region in the WBG ....................................................... 9 Figure 2: Number of Projects by Project Status ............................................................................................ 9 Figure 3: Contrast of a Traditional Input-based Approach to an Output-based Approach ......................... 18 Figure 4: Contracting Spectrum .................................................................................................................. 19 Figure 5: Volume of OBA Subsidy by Sector and Region in the WBG ..................................................... 22 Figure 6: Comparison of WBG OBA Portfolio to Total WBG Portfolio ................................................... 23 Figure 7: Comparison Portfolio vs. Number of Projects in IDA, IBRD and Blend Countries ................... 24 Figure 8: Distribution of Subsidy for All GPOBA Projects (Including Design Stage) .............................. 25 Figure 9: Distribution of OBA Portfolio by Sector and Region ................................................................. 26 Figure 10: Number of Projects by Project Status ........................................................................................ 27 Figure 11: Comparison of Performance of OBA and Traditional Projects ................................................. 35 Figure 12: Distribution of OBA ICT Projects ............................................................................................. 69 Figure 13: Global Application of Performance-Based Contracting for Roads ........................................... 78 Figure 14: Distribution of WBG OBA Projects in Transport ..................................................................... 79 Figure 15: Distribution of WBG OBA Energy Projects ............................................................................. 87 Figure 16: Distribution of WBG OBA Schemes in Water and Sanitation .................................................. 98 Figure 17: The Universe of Results-Based Financing .............................................................................. 108 Figure 18: Distribution of WBG OBA Projects in Health ........................................................................ 109

Tables

Table 1: Benchmarks/Criteria and Cross-cutting Lessons from OBA Portfolio ......................................... 11 Table 2: Distribution of OBA Projects ....................................................................................................... 23 Table 3: Distribution of OBA Portfolio by Sector and Region ................................................................... 26 Table 4: Cost and Effectiveness of Targeting Mechanisms ........................................................................ 33 Table 5: Universe of Output-Based Aid in ICT .......................................................................................... 69 Table 6: Defining ―Performance‖ in the Provision of ICT Services ........................................................... 74 Table 7: Performance Indicators for Transport Projects ............................................................................. 83 Table 8: Health Service Providers in Contracts to Provide Health Services ............................................ 113 Table 9: Parties Responsible for M&E in Contracts to Provide Health Services ..................................... 115

Boxes Box 1: Applications of OBA – Subsidy Design Mechanisms .................................................................... 20 Box 2: Nepal Biogas Support Program—Geographic Plus Self-selection Targeting ................................. 31 Box 3: CREMA – Phases I and II ............................................................................................................... 38 Box 4: Limitations to Shifting Risks to Service Providers ......................................................................... 41 Box 5: Colombia Natural Gas Distribution for Low Income Families in the Caribbean Coast – OBA and

the Private Sector ................................................................................................................................... 43 Box 6: Bank Procurement in OBA Projects ............................................................................................... 49 Box 7: Fund for Telephony Development in Chile ..................................................................................... 71 Box 8: Development of Telephony Fund in Guatemala ............................................................................. 76 Box 9: Argentina: Pilot Project for Performance-Based Maintenance: Roads Maintenance and Sector

Rehabilitation Project ............................................................................................................................. 80 Box 10: Successful Performance Based Rehabilitation and Maintenance Contracts in Chad .................... 81 Box 11: Annuity Concessions in India ....................................................................................................... 85 Box 12: Bangladesh -- Rural Electrification and Renewable Energy Development Project (2002-2009) . 89 Box 13: The ESCO Model: Argentina PERMER Concession ................................................................... 95 Box 14: Senegal Rural Electrification Priority Programs (PPER) .............................................................. 96

7

Box 15: Mozambique Water: OBA and IDA ............................................................................................ 100 Box 16: Manila Water Supply Project ...................................................................................................... 102 Box 17: Phasing in Payments Due to Access-to-finance Constraints in Uganda‘s Water Sector ............. 103 Box 18: Kenya Microfinance for Small Water Schemes .......................................................................... 104 Box 19: Expansion of Water Services in Low-income Areas of Jakarta .................................................. 105 Box 20: Morocco Urban Water and Sanitation Project ............................................................................ 106 Box 21: New Hospital Public-Private Partnership in Lesotho .................................................................. 114 Box 22: Cash-on-delivery Aid (COD) ...................................................................................................... 117 Box 23: Bangladesh Female Secondary School Assistance Project ......................................................... 118 Box 24: Conditional Cash Transfers in Education and OBA ................................................................... 120 Box 25: The Impact of PSP in the Concession Schools Program in Bogota ............................................ 121

8

Executive Summary

Objectives and Execution: The objective of this review is to provide a more definitive and prac-

tical understanding of lessons and best practice related to output-based aid (―OBA‖), a results

based financing (RBF) instrument that uses public-private partnerships and aims to more effec-

tively target access to basic services.1 The audience for this review will primarily be task teams

and managers working on project design and supervision in the relevant sectors, as well as do-

nors and governments who are interested in lessons in light of potential scale-up and main-

streaming of OBA approaches. The review has been undertaken jointly by the Global Partnership

on Output-Based Aid (GPOBA) and the IDA-IFC Secretariat.

What is OBA? OBA ties the disbursement of public funding in the form of subsidies to the

achievement of clearly specified results that directly support improved access to basic services.

Basic services include improved water supply, energy access, health care and education, com-

munications services (ICT), and transport (mainly roads). In the case of OBA, ―outputs‖ are de-

fined as close to the desired outcome or impact as is contractually feasible. For example, an out-

put might be the installation of a functioning household connection to the electricity network. In

some cases, an ―output‖ might also include a specified period of electricity delivery demonstrat-

ed through billing or collection records. ―Subsidies‖ in OBA schemes are defined as public

funding used to fill the gap between the total cost of providing a service to a user and the user

fees charged for that service, justified by the need to improve basic living conditions or the exis-

tence of positive externalities.2

Universe of OBA. When OBA was launched in the WBG with the 2002 PSD Strategy, 22 OBA

projects with a total estimated value of about $100 million had been identified. Now, nearly 130

OBA projects with a total subsidy value of about $3.3 billion have been identified in the WBG3

(figure 1).

1 Results-Based Financing (RBF) refers to a range of mechanisms designed to enhance the performance of aid through incentive-

based payments. RBF has been used most extensively in the area of health systems. RBF is an umbrella term that includes inter

alia output-based aid, performance-based inter-fiscal transfers, and conditional cash transfers. What these mechanisms have in

common is that a principal entity provides a financial or in-kind reward, conditional on the recipient undertaking a set of pre-

determined actions or achieving a pre-determined performance goal (http://go.worldbank.org/04UNXY1MS0). 2 In some cases, for example for public goods such as roads, user fees may be zero. 3 The $3.3 billion figure is skewed upwards by a few large health and road projects. This excludes related government subsidy

co-financing of $2.7 billion. Therefore the total value of WBG OBA schemes including co-financing is $4.9 billion. All dollar

values are US dollars unless designated otherwise and figures are as of April 2009. (Note: Since the PSD Strategy, some addi-

tional projects of fairly large subsidy value have been identified that were approved before 2002, while some of the other projects

identified at the time did not materialize or the OBA component was dropped.)

9

Figure 1: Volume of OBA Subsidy by Sector and Region in the WBG

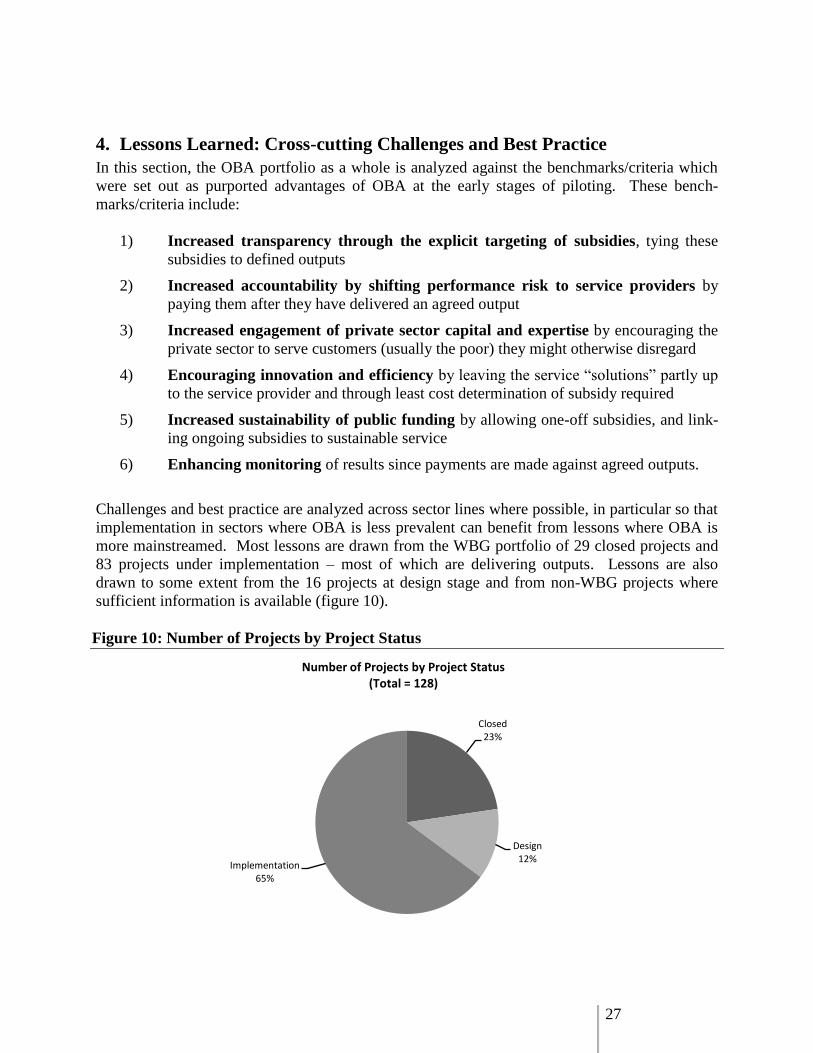

Of those projects, 29 have closed, 83 are under implementation and for the most part delivering

outputs, and 16 are in design stage (figure 2). Another 66 OBA schemes have been identified

outside the WBG – mostly in the rural energy, ICT and roads sectors4.

Figure 2: Number of Projects by Project Status

Funding for OBA has come from IBRD, IDA, GPOBA, other donors such as KfW, and govern-

ments themselves through, for example, tax revenue and the collection of explicit (including

cross) subsidies from users. Those OBA schemes in developing countries that do not involve

donor support are mainly found in middle-income (IBRD) countries.

4 GPOBA continues to identify OBA projects within and outside of the Bank; the figures here reflect projects identified up to

April 30, 2009.

AFR29%

EAP3%

ECA2%

LCR56%

MENA1%

SAR9%

WBG OBA Portfolio by Region(Total = US$ 3.3 bn)

Education5%

Energy6%

Health20%

Telecom2%

Transport61%

Water & Sanitation

6%

WBG OBA Portfolio by Sector(Total = US $ 3.3 bn)

Closed23%

Design12%Implementation

65%

Number of Projects by Project Status(Total = 128)

10

Piloting and mainstreaming. The piloting phase of OBA has provided a wide array of lessons

and in many cases has been a success. The 128 OBA projects that have been implemented or are

underway in the WBG reach at least 58.9 million beneficiaries worldwide5. The first OBA pilots

were launched in the ICT and roads sectors in the 1990s in Latin America (LCR). These pilots

were replicated and scaled-up first in that region, and eventually lessons learned were transferred

from IBRD countries to IDA countries. It could be reasonably claimed that OBA has become

―mainstreamed‖ as one of the mechanisms used to expand access in these two sectors in many

parts of the world – and in fact many non-WBG OBA projects identified are in ICT and roads.

In the health and off-grid energy sectors, OBA has become an important results-based financing

instrument enabling improved access for the poor, and OBA schemes are increasingly found out-

side the WBG as well. OBA is still at pilot stage in the water, education, and grid-based energy

sectors, although lessons for scale-up in some cases are now starting to become available.

Although OBA is increasingly being used as a tool to increase access for basic services, the per-

centage of the OBA portfolio as compared to overall IBRD and IDA activities is small. About

2.7% of the World Bank project portfolio in the transport, ICT, health, water & sanitation, ener-

gy and education sectors, approved between fiscal year 2000 and 2009 used an OBA approach6.

ICT was the sector using OBA most commonly7, with 11% its portfolio using OBA, followed by

health (5.7%) and transport (3.7%). So, although OBA is gaining ground and recognition, there

is still some ways to go in terms of scaling-up so that real strides can be made toward improving

access to basic services for the poor.

Enabling environment. The reasons for OBA‘s predominance in some sectors, as well as origi-

nation in Latin America in the 1990s, are to a large extent related to sector and country circums-

tances. More specifically, in order for an OBA approach to be viable, service providers must be

able to take on performance risk, and in particular, ―pre-finance‖ investments until subsidies are

disbursed based on output verification. Although there are several cases of OBA with public

sector providers, private sector operators traditionally are better structured to respond to perfor-

mance-based incentives8 and are usually better able to pre-finance outputs. Thus there appears to

be a correlation with the prevalence of OBA and the sector and regional experience with public-

private partnerships (PPP). This would imply that OBA will take stronger root where contractual

and regulatory practices are traditionally more supportive of the private sector taking risks. At

the same time, OBA can be an important mechanism through which efficiency gains from sector

5 Data on the number of beneficiaries is not readily available for public access ICT and transport projects. Beneficiary informa-

tion is particularly limited in the case of transport sector (available only in two of the 23 World Bank implemented projects) due

to the difficulty in identifying number of beneficiaries for non-exclusive road projects. 6 There are several contributing factors to this low percentage besides that OBA has not been fully mainstreamed. While the

WBG OBA portfolio only includes projects that aim at increasing household access to basic services, the overall WBG portfolio

also includes projects financing large upstream investments, wider sector reform programs, AAA, etc and the overall WBG port-

folio obtained from the WBG Business Warehouse includes sub-sectors such as mining, railways, ports or nutrition for which no

OBA projects have been identified. 7 However, the overall ICT portfolio is relatively small ($657 million), compared for example to transport (over $30 billion),

which helps explain the small percentage of OBA subsidies in ICT even though OBA is most mainstreamed in that sector. Addi-

tionally, OBA subsidies in the ICT sector mainly was financed through levies on service providers, not donor funds, so that the

exact subsidy amounts depend on service provider revenues and are unknown at the start of the project. The review identified at

least $6.2 billion in levies that were used to fund universal access funds. 8 As a consequence of ownership change from public to private, increases in labor productivity, service quality and investment

have been reported in competitive markets . Gains in productivity and profitability associated with privatization have for example

been demonstrated by Megginson, Nash, and van Randenborgh (1994), Frydman et al (1997); La Porta and Lopez-de-Silanes

(1999), and Brown et al (2006) (Gassner et al, June 2007, p.3, footnote 6).

11

reform are shared with users through improved access, and thereby can help underscore the ben-

efits of PPP.

Cross-cutting lessons. The OBA portfolio as a whole has been analyzed against the bench-

marks/criteria that were set out at the early stages of piloting as purported advantages of OBA

compared to traditional approaches. These benchmarks/criteria and the cross-cutting lessons in

relation to best practices and challenges are provided below. These lessons are gleaned from the

194 Bank and non-Bank OBA projects reviewed. Most of the lessons are taken from the projects

that have closed or are under implementation, although in some cases there were important and

interesting lessons to be learned from projects at design stage (table 1).

Table 1: Benchmarks/Criteria and Cross-cutting Lessons from OBA Portfolio

Benchmarks/

criteria

Cross-cutting lessons from OBA portfolio

Increased trans-

parency through

the explicit tar-

geting of subsi-

dies

OBA provides a good platform for targeting infrastructure and social

services subsidies. The focus on subsidies for access is inherently pro-

poor: the poorest segments of the population often cannot afford initial

access (e.g. cost of connection, health insurance) and therefore often do

not benefit from subsidies for on-going service provision. Further, by ex-

plicitly defining outputs, targeting can be made more precise. The process

of output verification can also provide an additional check on the targeting

of subsidies, and is helping provide early evidence that OBA schemes are

reaching the poor.9

Increased ac-

countability by

shifting perfor-

mance risk to

service providers

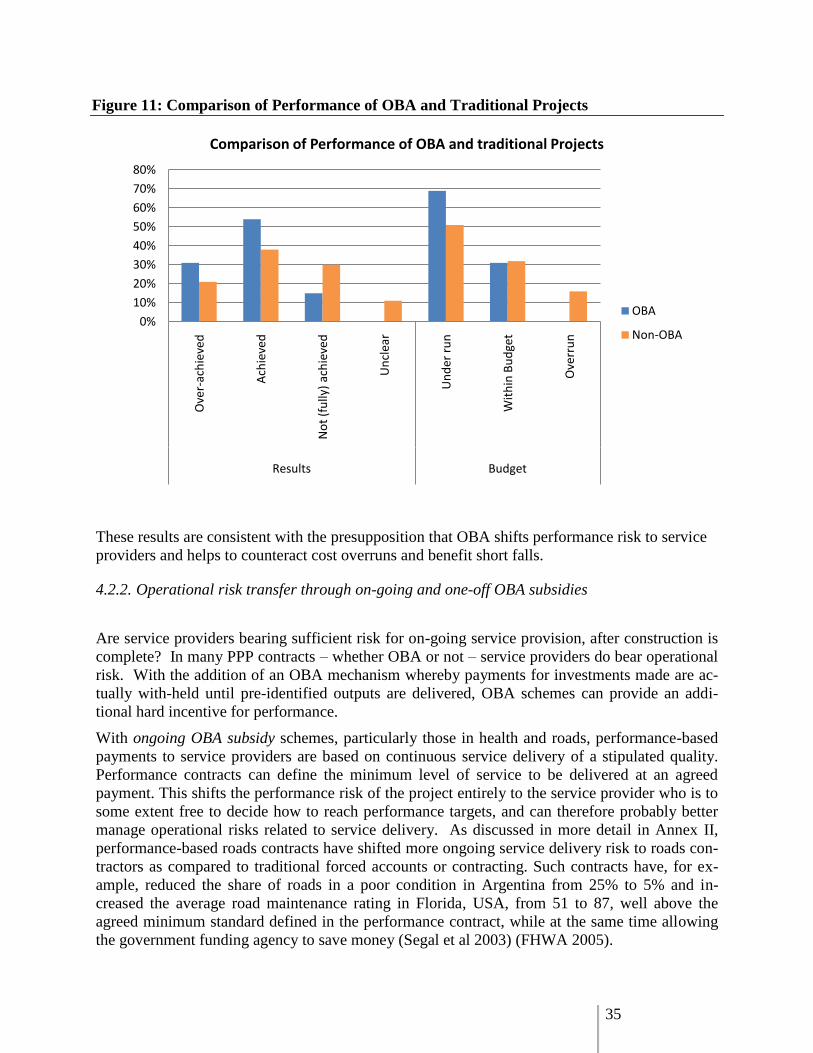

Compared to similar input-based schemes, OBA shifts performance risk

to service providers by virtue of the fact that payments to providers are

made after delivery of verifiable access and service. But the degree of

performance risk shifted depends on the ability of the service provider to

―pre-finance‖ investments/services until output-based payments are dis-

bursed. Ultimately access to finance will determine how much perfor-

mance risk is reasonably shifted to the provider.

Increased en-

gagement of pri-

vate sector capi-

tal and expertise

OBA does leverage private funding, but because of its generally pro-poor

nature, private financing leveraged will be limited by the extent user fees

(e.g., tariffs) can incorporate investment costs while remaining affordable.

What is particularly noteworthy is the ability, through relatively small

amounts of OBA subsidy, to mobilize private sector expertise to serve

customer segments the private sector might otherwise not serve. Ulti-

mately, the effective use of private sector participation is dependent on the

enabling environment, for example the depth and quality of experience

with PPP contracts, regulation, and access to finance.

9 Explicit targeting of subsidies for specific users and uses is common across all the sectors where OBA is prevalent, except for

the roads sector (and a limited extent ICT), where the ―public goods‖ (access for all) nature makes it difficult to exclusively target

specific beneficiaries.

12

Benchmarks/

criteria

Cross-cutting lessons from OBA portfolio

Encouraging in-

novation and ef-

ficiency

There is some evidence that output-based payments have led to improve-

ments in operational efficiency and the delivery of innovative (often pro-

poor) access to service solutions. Further, OBA has demonstrated effi-

ciency gains through competition in most sectors when competitive pres-

sures have been applied in the selection of the OBA service provider (noting that competitive tendering processes can take time). The focus on

outputs as opposed to inputs should lead to innovations which translate

into future efficiency gains, as has been seen in ICT and to some extent in

roads.

Increased sustai-

nability of public

funding

It is too early to analyze whether OBA schemes have provided long-term

sustainable solutions. There is no evidence to date to suggest that

schemes that involve OBA subsidies are less sustainable than their in-

put-based counterparts, and in fact, the design of OBA schemes (for ex-

ample, greater degree of demand risk shifted to service providers given the

link between outputs and uptake, which in turn incentivizes efforts at

stakeholder participation and education through community organizations,

NGOs, etc) can enhance longer-term sustainability.

Enhancing moni-

toring of results

By paying on verified outputs, OBA internalizes the monitoring of re-

sults. Best practice would also use the monitoring platform of OBA

beyond just the verification of outputs to also check other aspects of ser-

vice delivery. With OBA schemes, accountability also increases for do-

nors and governments: public funding is linked to the fact that pre-

identified outputs are (were) delivered and therefore waste or inappro-

priate allocation of such funding should be minimized.

Next steps. OBA is not a panacea. It is one mechanism within the spectrum of results-based fi-

nancing mechanisms which is showing clear promise. But cross-cutting challenges for success-

ful OBA schemes remain – even for the sectors where OBA is mainstreamed. Although some of

these challenges are not specific to OBA, they must be addressed in order for OBA to continue to

make a mark on aid effectiveness, especially in light of new challenges brought forth with the on-going financial crisis:

access to finance to pre-finance outputs/secure and sustainable sources of subsidy

funding;

capacity of implementing agencies and service providers;

donor coordination and harmonization; and,

limitations to the use of geographic targeting as scale increases.

Further, as most OBA schemes involve PPP arrangements, the most basic aspects for the relevant

enabling environment should be in place. Not all these elements may be required at the time of

piloting, but attempting to short-cut key issues related to, for example, tariff setting and adjust-

ment, quality of service standards, and contract adjustment and monitoring, may lead to delays

for the pilot and will need to be addressed in detail for scaling-up. Understanding the basis for

13

an enabling environment for OBA schemes in any given sector is a prerequisite for sustainable

OBA programs.

The WBG, including its multi-donor programs, has a large role to play in addressing these chal-

lenges in terms of financial support and technical assistance (e.g., transaction advisory, capacity

building, tariff/subsidy reform). The importance of WBG co-ordination can also demonstrated

here. OBA is a platform that can effectively bring together the range of instruments across IDA

and IFC in scaling up targeted infrastructure and social services. For example, while IFC in-

vestments can play a role in supporting the project with financing and bringing in other private

capital, the IDA financing may be used for the OBA payment.

Some strategic guidance has been provided through the Sustainable Infrastructure Action Plan

(2008), Innovating Development Finance (Girishankar, 2009), the PSD Strategy Update, and the

2007 World Bank Strategy for Health, Nutrition and Population, to name a few. Efforts to inte-

grate OBA within country assistance strategies and broader sector programs are underway, but

more needs to be done. More work is needed to ensure OBA projects are able to maintain their

―output‖ driven nature while continuing to meet Bank procurement and financial management

requirements. The Investment Lending Reform (Concept Note, January 26, 2009) currently

being considered by OPCS will be attempting to tackle these very issues, and OBA will provide

some important lessons for this initiative as well.

The ultimate decision on the success of OBA or of any other aid effectiveness tool rests with the

WBG client governments and their interest, ownership, and commitment to design and sustain

such approaches. The WBG has a key role to play in working with the broader develop-

ment/donor community to demonstrate that OBA is an important mechanism to help improve

access to basic services and reach the MDGs. The existing information and expertise on OBA,

including this review, provide a solid underpinning for the successful design of pilots or pro-

grams that respond to client needs.

14

1. Introduction

1.1 Background

Output-based aid (OBA) is being used as an innovative mechanism to deliver basic infrastructure

and social services to the poor. The concept was introduced in the WBG in 2002 through the

Private Sector Development (PSD) Strategy and more formally in January 2003 when the Global

Partnership on Output-Based Aid (GPOBA) was launched as a World Bank-administered donor-

funded pilot program to test the approach with a view to mainstreaming it within IDA as well as

with other development partners.

The IDA14 Mid Term Review (MTR) in November 2006 was an early opportunity to present the

emerging lessons and preliminary findings of the OBA approach. The IDA14 MTR discussion

highlighted that although it was too early to draw definitive conclusions, the emerging findings

were encouraging. One of the recommendations of the IDA14 MTR discussion was that there

should be focused scaling-up of OBA within IDA operations, as well more collaboration across

the WBG, and that the results of the scaling-up would be reported at the IDA15 MTR. This has

therefore been the focus of OBA within the WBG over the last two years, led by GPOBA of

which IFC is a major funding contributor.

In early 2008, the IDA-IFC Secretariat was created to foster greater collaboration between IDA

and IFC. OBA has been identified as one of the instruments that could be used in joint IDA-IFC

operations. Therefore, in preparation of the Secretariat‘s first Annual Report for May 2009 (IDA-

IFC, 2009), and as a precursor to the IDA15 MTR in the fall of 2009, GPOBA together with the

IDA-IFC Secretariat has conducted this review of lessons learned and best practice.

1.2 Objective and Audience

The objective of this review is to provide a more definitive and practical understanding of les-

sons and best practice related to OBA, and the use of OBA as one approach to enhance the effec-

tiveness of donor funds, including through promoting public-private partnerships. The audience

for this review will primarily be task teams and managers working on project design and super-

vision in the relevant sectors as well as donors and governments who are interested in lessons in

light of potential scale-up and mainstreaming of OBA approaches. The guiding principles will be

to better articulate the lessons learned from the various applications of OBA and best practices

by sectors.

1.3 Execution of Review/Methodology

The review has been conducted by GPOBA and the IDA-IFC Secretariat. Much of the work has

been conducted in-house by the GPOBA monitoring and evaluation team (M&E team), which is

tasked with documenting and disseminating lessons learned – both best practice and challenges –

from OBA schemes in and outside the WBG. Guidance and peer review has been provided by

sector experts who have worked on both OBA and non-OBA projects in the Bank.

The methodology broadly involved the following:

a) Identify the universe of OBA projects including projects funded outside of GPOBA and

the WBG.

15

b) Gather information on project design, implementation and results.

c) Compile sector specific lessons learned and best practices of OBA as well as lessons

from the various applications of OBA such as one-off subsidies, transitional subsidies

and ongoing subsidies.

For this review, 194 OBA projects were identified and analyzed. They are classified as follows

based on the OBA funding source (a few of which involve co-financing and some of which are

now under consideration for scaling-up):

GPOBA projects – This includes 48 projects that have received either technical assis-

tance and/or investment subsidy funding (or are in the process of receiving funding) from

GPOBA.

World Bank projects – This includes 80 OBA projects that are funded by the World

Bank Group, independent of GPOBA.

Non-Bank Projects – This includes 66 OBA projects that are funded either by other do-

nors such as KfW and GtZ, or by governments themselves such as the OBA scheme for

water and sanitation services in Chile. This also includes OBA projects in developed

countries such as the special education voucher scheme in the United States. It is not

possible to conduct an exhaustive search, but the review attempts to capture a representa-

tive sample. Further, the review has largely focused on developing countries.

For each project, the following information was sought:

Project design: Design elements captured include output definitions, payment triggers,

financial sustainability/tariffs, targeting, total costs, funding source, role of private sector,

transfer of performance risk to service providers, and administration and monitoring of

the OBA scheme.

Project implementation and results: This includes results of bidding (where applica-

ble), efficiency gains, delivery of outputs and disbursement of funding, lessons learned

and problems encountered during project preparation and implementation. Where possi-

ble, direct comparisons was made with input-based projects.

OBA projects were identified with the help of OBA practitioners and experts both within and

outside the WBG (e.g. the consulting firm Castalia for additional ICT and transport projects).

The team also relied on several in-depth studies separate from this review exercise, such as the

extensive Regulatel study (Stern and Townsend) undertaken by the WBG‘s Global ICT practice.

For WBG (including GPOBA) projects, information on project design and results was obtained

from the following standard documents. The review team also contacted task managers and other

team members for any additional information and clarifications.

Project Appraisal Document (PAD)

Project Information Document (PID)

Operations Manual (OM)

Implementation Status Report (ISR)

Unaudited Interim Financial Reports (IFR)

16

Implementation Completion and Results Report (ICR)

In addition, the following documents that are specific to GPOBA were analyzed:

GPOBA semi-annual Reports

Independent Verification Agent Reports

Post Project Report

For non-Bank projects, information is typically limited. The M&E team relied heavily on inter-

net searches and discussions with sector experts to gather information on these projects.

1.4 Structure of Report

Section 2 of this report starts by providing a clear definition of OBA, and then puts OBA in the

context of other results-based arrangements and subsidy mechanisms. This section also provides

a description of the various applications of OBA: one-off, transitional or ongoing subsidies.

Section 3 of the report provides an overview of where OBA approaches are being implemented.

Section 4 provides a cross-sector review of lessons learned from implementing OBA. The OBA

schemes identified are analyzed against certain benchmarks/criteria which had been set out as

purported advantages of OBA at the early stages of piloting. Challenges and best practices are

analyzed across sector lines where appropriate, in particular if implementation in sectors where

OBA is less prevalent can benefit from lessons where OBA is more mainstreamed.

Section 5 of the report summarizes challenges to be addressed by the WBG and ends with a view

to next steps.

Annex I presents a table of all OBA projects identified in the WBG as of April 30, 2009.

Annex II provides greater detail on the use of OBA in each of the sectors analyzed, on a sector-

by-sector basis.

Annex III provides data on the WBG OBA portfolio in context of the overall WBG portfolio for

the relevant sectors for the same time period.

17

2. Context

2.1 Definitions

OBA ties the disbursement of public funding in the form of subsidies to the achievement of

clearly specified results that directly support improved access to basic services. Basic services

include improved water supply, energy access, health care, education, communications services,

and transport.

In the case of OBA, ―outputs‖ are defined as close to the desired outcome or impact as is con-

tractually feasible. For example, an output might be the installation of a functioning household

connection to the electricity network. In some cases, an ―output‖ might also include a specified

period of electricity delivery demonstrated through billing and collection records. The intended

outcome of such an output-based scheme would be to improve the basic living conditions of the

poor household, reducing indoor household pollution, increasing opportunities for education

through better lighting or through information passed through radio and television, and the like.

The intended development impact could include for example a reduction in morbidity or in-

creased lifetime earnings.

―Subsidies‖ are defined as public funding used to fill the ―gap‖ between the total cost of provid-

ing a service to a user and the user fees charged for that service.10

Policy concerns such as im-

proving basic living conditions for the poor or the existence of positive externalities from a re-

duction in disease may justify the use of subsidies. Both the definition of outputs and the design

of subsidy mechanisms are discussed in greater detail below.

2.2 Traditional vs. OBA approaches

Neither performance arrangements nor subsidies are new to the developing world or the WBG.

Performance contracts have been implemented for several decades, using both public and private

operators. But ―outputs‖ in OBA schemes are generally more narrowly defined than benchmarks

in traditional performance arrangements, which in some cases may be more input-oriented. Sub-

sidies have also existed in infrastructure and social services sectors. But OBA refines the target-

ing of subsidies by bringing together performance-based arrangements and subsidies through the

explicit linking of the disbursement of subsidies to the achievement of agreed outputs.

Figure 3 below provides a simple contrast of a traditional input-based approach to an output-

based approach.

10 In some cases, for example for public goods such as roads, user fees may be zero.

18

Because of the clear link between pre-identified outputs and ex post payment (or, ―subsidies‖),

the following advantages of OBA over traditional approaches are assumed:

1) Increased transparency through the explicit targeting of subsidies, tying these subsi-

dies to defined outputs

2) Increased accountability by shifting performance risk to service providers by paying

them only after they have delivered an agreed output

3) Increased engagement of private sector capital and expertise by encouraging the pri-

vate sector to serve customers (usually the poor) they might otherwise disregard

4) Encouraging innovation and efficiency by leaving the service ―solutions‖ partly up to

the service provider and through least cost determination of subsidy required

5) Increased sustainability of public funding through the use of one-off subsidies and

linking ongoing subsidies to sustainable service

6) Enhancing monitoring of results since payments are made against agreed outputs.

Some of these advantages were postulated in the PSD Strategy of 2002 and were also the basis of

analysis in the IDA14 MTR discussion paper on OBA. These are also the criteria/benchmarks

Inputs (such as materials)

Service Recipient

Inputs (such as materials)

Service Recipient

Private Finance

Public Finance

Service Pro-vider

Service Pro-vider

Traditional (input-based) Approach

Output-Based Approach

Private financing mobilized by ser-vice provider

Reimbursement for out-puts delivered

Source: Brook and Petrie, 2001

Figure 3: Contrast of a Traditional Input-based Approach to an Output-based Approach

19

against which the current portfolio of OBA projects identified in the WBG and outside is ana-

lyzed in this review.

2.3 Contracting out service delivery: the spectrum

Under OBA schemes, services are contracted out to a third party provider, and that contract or

other official arrangement is the mechanism through which the output-based disbursement crite-

ria are established. The ―third party‖ in OBA schemes is typically a private enterprise, but could

also be a public utility, NGO, community-based organization, or even a separate branch or insti-

tution of government from that entity providing the official public funds.

Over the last two decades, schemes that harness private financing to deliver infrastructure servic-

es have expanded considerably. Under traditional procurement, private infrastructure services are

contracted at the ―input‖ end of the spectrum, with the government purchasing specific ―inputs‖

and using these to build assets and provide services itself (figure 4).

Contracting ‗closer to the input end‘ (e.g. the construction of water treatment plants) does not

guarantee that the inputs the government purchases actually lead to the outcomes (e.g. a reduc-

tion in waterborne diseases) or impacts (e.g. decreased morbidity) that the government actually

wants. But because outcomes and impacts are a combined product of what the provider can in-

fluence and other factors outside the service provider‘s control, either governments seeking to

pay on outcomes and impacts will not find a willing, credible service provider or the provider

will charge a substantial premium for making its payment contingent on factors that it cannot

control.

What can be done, however, is to contract for an output that is as closely related as possible to

the desired development outcome or impact, while performance risk is still largely under the ser-

vice provider‘s control. This is the rationale behind ―output-based aid‖. Outputs would include,

for example, contracting for functioning yard taps as part of a water supply program, a specified

number of people to be vaccinated in the case of health programs or working public payphones

or solar home systems to be installed in villages in the case of ICT or energy. But in order to en-

sure sustainability and for service providers to take on appropriate demand risk, OBA usually

involves a mixture of payment on outputs and outcomes – e.g. use of electricity or ICT services.

However, the farther one goes along the output/outcome/impact spectrum, the greater the risk

Design Development

Impacts

(Intermediate)

Outcomes Outputs Build,

Operate

-Output specification

-Service provider selection

OBA “Outputs” include

-Water connection made & service provided

-Solar Home System installed & maintained

-Medical treatment provided

OBA “Outputs” Independently verified

Inputs

Figure 4: Contracting Spectrum

20

borne by the service provider, and consideration must be given as to whether the provider is rea-

sonably able to bear that risk, and at what cost.

2.4 Applications of the OBA approach

OBA schemes can provide subsidies in three ways: one-off subsidies such as connection subsi-

dies; transitional tariff subsidies which taper off as user contributions increase; or ongoing subsi-

dies. The subsidy design chosen will depend on factors such as the sustainability of the funding

source, the capacity for administering the subsidy scheme, the type of service to be subsidized,

and the extent to which the service provider is willing and able to be paid over time (box 1).

Box 1: Applications of OBA – Subsidy Design Mechanisms

One-off subsidies are the most common application of OBA approaches and usually involve capital subsidies

for access to a given service. An example is when a large portion of the subsidy is paid after the targeted

beneficiaries are connected to a network and connections are verified. Given that in OBA approaches the

emphasis is on service delivery rather than on physical connections, even in the case of one-off subsidies a

portion of the subsidy may be withheld and paid only after verification of a certain number of months of sa-

tisfactory service delivery (hence a mixture of ―outputs‖ and ―intermediate outcomes‖ against which one-off

subsidies are disbursed to provide a measure of improved access).

Transitional subsidies can be used to support tariff reforms, where a subsidy is used to fill the gap between

what the user is deemed able and/or willing to pay and the cost-recovery level (e.g., long-run marginal cost)

of the tariff. The subsidy is transitioned out after a specified period of time (e.g., months or years) as the user

contribution increases (and possibly as tariff levels required for cost recovery decrease with efficiency gains).

In these cases, the output against which the subsidy is paid is the service delivered and billed by the provider.

The review identified only a handful of transitional OBA schemes and very few of those are still in place.

Ongoing subsidies may be required in cases where there is a continuous gap between affordability and cost

recovery – including for consumption costs. As in the case of transitional schemes, ongoing subsidies should

be paid out against pre-determined targeted outputs in order to be considered OBA.

For utility services, most OBA schemes in water, energy, and telecommunications rely on one-

off subsidies enabling initial access, partly because OBA is targeted to the poor and the poor are

usually not connected to network services in the first place so often cannot benefit from ongoing

or transitional tariff subsidies. A one-off OBA subsidy may be used, for example, to help connect

a poor household to the water or electricity network or to reduce a community‘s contribution for

provision of pay phones or internet points of presence.

Ongoing output-based subsidies in the utility sectors are seen more often in countries with

higher rates of access. For example, in Chile an income-based targeting scheme channels an on-

going output-based subsidy through service providers to poor urban households for a life-line

(minimum acceptable) amount of water consumed.11

11 Most other commonly used quantity-based tariff subsidies such as increasing block tariffs, however, are not OBA. Such

schemes usually charge tariffs below cost for low-consumption, because it is assumed that poor households consume small

amounts. These subsidies are usually intended to be financed by cross-subsidies from higher-consuming customers (who are

charged higher tariffs). However, the amount of cross-subsidy received by the operator is not related to the amount of subsidy

provided to the low-consuming households, but rather, the subsidy collected from the high-consuming households. Therefore,

the operator ―earns‖ the subsidy from the high-consuming households whether he serves the targeted households or not. These

issues are discussed in greater detail in Section 4.

21

Ongoing output-based subsidies normally fund the provision of basic services or maintenance in

OBA projects in roads, health, and education. OBA road maintenance schemes require ongoing

subsidies for the life of the road, often funded through road funds. OBA health schemes, to en-

sure continued access to care for the poor, often channel subsidies in an ongoing manner through

health care providers as they deliver agreed services, such as well-child visits, over a period of

time – although some health projects may focus on interventions of a one-off nature such as safe-

child delivery.

2.5 OBA as part of the Results-Based Agenda

OBA is an important part of the WBG‘s spectrum of results-based solutions of development

finance. For example, OBA is one key element of a broader universe of results-based financing

(RBF) in the health and education sectors, where RBF is ―a payment made to a provider, payer

or consumer when measurable actions are taken or defined performance targets are achieved‖

(Brenzel et al., 2009) Other RBF mechanisms include conditional cash transfers and cash on de-

livery (see health section in Annex II). This paper will not cover parts of the results-based spec-

trum that are not OBA.

However, it is worth noting that some of different results-based mechanisms can play comple-

mentary roles. For example, conditional cash transfers (CCT) described in greater detail in the

health and education annexes may be enhanced through the use of OBA-type mechanisms.

CCTs can provide incentives for users to partake in health, education and other schemes (e.g.

sanitation) that exhibit positive externalities when they otherwise might not choose to; OBA can

help incentivize providers to ensure that the services are available when users demand such a

service. This is an area to be explored further.

22

3. Snapshot of OBA in the WBG and Beyond

3.1 Universe of OBA under review

At the time of the PSD Strategy Implementation Progress Report in 2003, 22 OBA projects with

a total estimated value of about $100 million12

had been identified – although since then the

number of projects identified that were approved before 2003 has risen to 33, with a total fund-

ing amount of $1.3 billion.

Now, about 128 OBA projects with a total subsidy value of about $3.3 billion (excluding the

$2.7 billion subsidy funded by recipient governments) have been identified in the WBG 13

(fig-

ure 5). Of those 128 projects identified in the WBG, 29 are closed, 83 are under implementation

and for the most part delivering outputs, and 16 are in design stage. This review draws mostly

from the closed projects and those under implementation, although there are also some important

lessons to be learned from project design.

Another 66 OBA schemes have been identified outside the WBG, mostly in the ICT, transport

(mainly roads), and energy sectors. There may be more OBA schemes that were not discovered

by this review.

Figure 5: Volume of OBA Subsidy by Sector and Region in the WBG

To put this in context, OBA is only a small share of the World Bank portfolio, at 3% in total.

Since 2000 between 0.56% and 7.9% of project volume approved each year used OBA. The

largest share of OBA projects was 13.1% of funding volume in the ICT sector, followed by

health (6.3%) and Transport (4.2%) (figure 6).

There are several contributing factors to this low percentage, aside the fact that OBA has not yet

been fully mainstreamed. While the WBG OBA portfolio only includes projects that aim at in-

12 All $ in this review represent US dollars unless designated otherwise. 13 GPOBA continues to identify OBA projects within and outside of the Bank; the figures here reflect projects identified up to

April 30, 2009.

AFR29%

EAP3%

ECA2%

LCR56%

MENA1%

SAR9%

WBG OBA Portfolio by Region(Total = US$ 3.3 bn)

Education5%

Energy6%

Health20%

Telecom2%

Transport61%

Water & Sanitation

6%

WBG OBA Portfolio by Sector(Total = US $ 3.3 bn)

23

creasing household access to basic services, the overall portfolio also includes projects financing

large upstream investments, wider sector reform programs, AAA, etc and the overall WBG port-

folio obtained from the WBG Business Warehouse includes sub-sectors such as mining, railways,

ports or nutrition for which no OBA projects have been identified. For a breakdown by sector,

please refer to Annex III.

Figure 6: Comparison of WBG OBA Portfolio to Total WBG Portfolio

The regional and sector breakdown of these OBA projects is provided in table 2. As the table

shows, most of the projects in the WBG are currently in AFR (due to recent piloting efforts by

GPOBA) and LCR (which is where the first OBA pilots in each sector reviewed began).

Projects outside of the WBG were overwhelmingly in the ICT and transport (i.e. roads) sector,

and predominantly in LCR.

Table 2: Distribution of OBA Projects

AFR LCR EAP SAR ECA MENA Grand

Total

Water & Sanitation 12 7 7 3 0 3 32

Energy 7 6 6 5 3 0 27

Transport 9 11 0 1 1 1 23

Health 11 3 3 4 0 1 22

Telecom 6 6 5 2 1 0 20

Education 0 1 0 3 0 0 4

Grand Total 45 34 21 18 5 5 128

The nearly four-fold increase in the number of OBA projects in the WBG within a period of five

years is due to a variety of factors, in particular:

2000 2001 2002 2003 2004 2005 2006 2007 2008

Total $5,539 $6,705 $6,831 $7,333 $9,400 $8,214 $8,608 $11,136 $10,635

OBA $31 $83 $133 $68 $743 $247 $382 $132 $403

$-

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

Total WBG funding approved(FY 2000-2009 in m)

24

an increased emphasis on results and accountability by donors and governments, includ-

ing the WBG results agenda;

an explicit recognition that well-designed subsidy schemes are an integral part of a pro-

poor infrastructure and social services delivery strategy; and,

a recognition that in order for PPP to be successful, specific attention needs to be paid to

pro-poor service delivery.

This explicit acknowledgment that subsidies are sometimes necessary, coupled with new evi-

dence that many existing subsidy schemes such as quantity-based subsidies embedded in tariffs

often have a regressive targeting incidence, have contributed to the appeal of more targeted sub-

sidy schemes such as OBA (Komives et al., 2005).

3.2 Funding OBA

Funding for OBA schemes has come from IBRD, IDA, GPOBA, other donors such as KfW, and

governments themselves through, for example, tax revenue and the collection of cross-subsidies

from users. The WBG is the biggest donor with over $3.3 billion committed to fund subsi-

dies to approximately 80 projects14

. Many of the WBG‘s original OBA projects were in the

Latin America region and in the roads and ICT sectors. Subsequent roads and ICT schemes have

built on the lessons from these schemes – with varying degrees of success – and expanded into

other regions so that there are now a substantial number of roads and ICT schemes in regions

such as AFR. This is discussed in the sector sub-sections in Annex II as well as in Section 4. Of

the $3.3 billion WBG portfolio, the majority of the projects (59%) are in IDA countries

compared to 29% percent in IBRD countries. In terms of subsidy volume, IBRD countries

account for the largest share at 56% of the total WBG subsidy portfolio compared to IDA’s

39%. About 12% of projects, accounting for 5% of the subsidy volume, are located in

IDA/IBRD blend countries (figure 7).

Figure 7: Comparison Portfolio vs. Number of Projects in IDA, IBRD and Blend Countries

14 Excludes projects with GPOBA subsidy funding or technical assistance.

BLEND5%

IBRD56%

IDA39%

Distribution of OBA subsidy(Total = US$3.3 bn)

BLEND12%

IBRD29%

IDA59%

Distribution of OBA projects(Total = 128 projects)

25

It is worth noting that some of the WBG projects have received substantial amounts of comple-

mentary subsidy funding from the recipient governments worth a total of $2.7 billion. The bulk

of this government funding has been in the transport and health sectors, accounting for 64% and

30% respectively. More than 76% of this funding came from IBRD governments, though they

accounted for only 48% of the projects that received complementary subsidy funding from gov-

ernment. Therefore the total OBA subsidy portfolio for WBG projects (including government

co-financing) is $6 billion.

In addition to the 80 projects described above, another 48 projects have either received funding

or are in the process of being funded by the World Bank-administered program, GPOBA. GPO-

BA was created in 2003 by the UK‘s DFID and the World Bank. GPOBA was originally in-

tended to help assist in the preparation of OBA projects and document and disseminate the les-

sons learned. In 2005, through an additional DFID contribution, GPOBA also became able to

help fund actual subsidy schemes. This galvanized the development of over 28 GPOBA-funded

projects, most of which are under implementation or for which grant agreements are imminent.

New donors have since joined GPOBA, including the Netherlands government (DGIS), AusAID,

Sida, and the IFC.

GPOBA has to some extent focused on designing and developing OBA schemes in areas where

OBA has been less tested, in particular the water and sanitation sector. Over 60% of the GPOBA

projects are in IDA countries and they account for 72% of GPOBA funding volume. A majority

of GPOBA projects are in the water and sanitation sectors (52%), followed by energy (25%), and

together they account for over 80% of the GPOBA subsidy volume (figure 8). Further, as de-

scribed in greater detail below, although OBA was originally envisioned as a tool to enhance pri-

vate sector participation, GPOBA has also attempted to pilot OBA with commercially-viable

state-owned enterprises (SOEs) in sectors where public utilities have continued to play a domi-

nant role in service provision.

Figure 8: Distribution of Subsidy for All GPOBA Projects (Including Design Stage)

BLEND8%

IBRD20%

IDA72%

GPOBA Subsidy Distribution(Total = US$ 145 m)

Energy30%

Health16%

Telecom3%

Water & Sanitation

51%

GPOBA Subsidy Distribution(Total = US$ 145 m)

26

OBA schemes have also been identified outside the WBG – both in developed and developing

countries. In some cases donors are playing an active role, such as KfW in the health and renew-

able energy sector or DGIS with the Energising Development program, implemented by GTZ in

energy. More generally, for developing countries, OBA schemes that do not involve donor sup-

port are mainly found in middle-income (IBRD) countries which are able to fund subsidy

schemes largely from cross-subsidies or tax revenue.

3.3 Sector focus

Since OBA approaches can vary a great deal depending on the sector context, best practice and

challenges encountered are easier to delineate by sector. Some of these lessons can be trans-

ferred across sectors, and where this is the case, such lessons are discussed in Section 4 of this

review. But what is clear is that in order for OBA or any innovative mechanism to become rele-

vant, it must be able to adapt to regional and sector circumstances and constraints. Figure 9

shows the key sectors under review and provides the amount of subsidy of OBA projects by sec-

tor and region identified in the WBG; table 3 shows the distribution of the OBA portfolio by sec-

tor and region. Annex II provides a more detailed description of lessons learned on a sector-by-

sector basis.

Figure 9: Distribution of OBA Portfolio by Sector and Region

Table 3: Distribution of OBA Portfolio by Sector and Region

$-

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

$2,000

AFR EAP ECA LCR MENA SAR

Mill

ion

s

Distribution of OBA Portfolio by Sector and Region

Telecom

Water & Sanitation

Energy

Education

Health

Transport

Transport Health Education Energy

Water &

Sanitation Telecom Grand Total

AFR 635,588,000$ 144,815,164$ -$ 58,350,000$ 97,861,433$ 21,490,705$ 958,105,302$

EAP -$ 32,140,000$ -$ 40,600,000$ 23,275,640$ 10,076,630$ 106,092,270$

ECA 55,000,000$ -$ -$ 10,100,000$ -$ -$ 65,100,000$

LCR 1,303,026,000$ 375,104,000$ 41,140,000$ 59,560,000$ 47,380,880$ 29,950,000$ 1,856,160,880$

MENA 40,000,000$ 6,232,100$ -$ -$ 8,400,000$ -$ 54,632,100$

SAR -$ 119,000,000$ 138,007,143$ 24,370,000$ 2,264,743$ 11,900,000$ 295,541,886$

Grand Total 2,033,614,000$ 677,291,264$ 179,147,143$ 192,980,000$ 179,182,696$ 73,417,335$ 3,335,632,438$

27

4. Lessons Learned: Cross-cutting Challenges and Best Practice

In this section, the OBA portfolio as a whole is analyzed against the benchmarks/criteria which

were set out as purported advantages of OBA at the early stages of piloting. These bench-

marks/criteria include:

1) Increased transparency through the explicit targeting of subsidies, tying these

subsidies to defined outputs

2) Increased accountability by shifting performance risk to service providers by

paying them after they have delivered an agreed output

3) Increased engagement of private sector capital and expertise by encouraging the

private sector to serve customers (usually the poor) they might otherwise disregard

4) Encouraging innovation and efficiency by leaving the service ―solutions‖ partly up

to the service provider and through least cost determination of subsidy required

5) Increased sustainability of public funding by allowing one-off subsidies, and link-

ing ongoing subsidies to sustainable service

6) Enhancing monitoring of results since payments are made against agreed outputs.

Challenges and best practice are analyzed across sector lines where possible, in particular so that

implementation in sectors where OBA is less prevalent can benefit from lessons where OBA is

more mainstreamed. Most lessons are drawn from the WBG portfolio of 29 closed projects and

83 projects under implementation – most of which are delivering outputs. Lessons are also

drawn to some extent from the 16 projects at design stage and from non-WBG projects where

sufficient information is available (figure 10).

Figure 10: Number of Projects by Project Status

Closed23%

Design12%

Implementation65%

Number of Projects by Project Status(Total = 128)

28

To judge the merits of OBA, this review aims to answer the following two questions: (i) to what

extent do OBA projects meet the six criteria listed above, and, (ii) does OBA address these crite-

ria better than traditional aid approaches?

To answer the first question, the review mainly relies on information and lessons gathered on

GPOBA projects that are under implementation and from Bank and GPOBA projects that have

closed. Information from evaluation studies and other publications is used to the extent available.

With regards to the second question, the main challenge is establishing a valid counterfactual. To

allow conclusions as to the relative effectiveness of OBA, OBA projects need to be compared to

projects with similar objectives, using other approaches. However, in reality no two projects are

totally alike. For example, two water supply projects providing poor households with access to

clean water may result in vastly different unit costs, depending on how much distribution infra-

structure they involve, whether they involve water treatment infrastructure, etc15

.

Nevertheless, some studies were found that can help put OBA in the context of other aid modali-

ties. For example, on the targeting incidence of utility subsidies and the pro-poor benefits of

connection subsidies such as those that are predominant with OBA, most notable is a 2005

World Bank publication by Kristin Komives et al on ―Water, Electricity and the Poor: Who Ben-

efits from Utility Subsidies‖. And, a number of studies16

have demonstrated cost savings/quality

improvements, resulting from competitive selection of service providers in roads, health projects

and ICT, compared to previous traditional provision of service.

In summary, when reviewing the lessons learned for each of the six criteria listed above, the sec-

tion draws both on the record of the OBA portfolio against these criteria, and also on general or

specific comparisons with input-based schemes. Altogether, cross-cutting lessons and best prac-

tice guidance can be confidently derived. In future, this analysis will be supplemented with re-

sults from on-going impact evaluations or other studies, which will add to the increasing body of

knowledge on results-based financing in general, and output-based aid approaches more specifi-

cally.

Examples of OBA schemes are illustrated to help provide a clearer picture on how lessons are

drawn. However, most detail on the OBA portfolio is provided in the annex – both the table in

Annex I, as well as the sector sections in Annex II for ICT, transport (namely roads), energy, wa-

ter, health and education.

15 The GPOBA M&E team has also explored the option of using unit cost data from the World Bank Africa Infrastructure Coun-

try Diagnostic Study. However, the Country Diagnostic Study uses a disaggregated concept of unit costs that does not allow a

systematic comparison. The country diagnostic study includes outputs such as meters of pipe of a certain quality and diameter

laid or stand-posts installed, whereas the output definition for OBA includes necessary network extension and installation of final

connections. 16 Add roads, health, etc. where this was confirmed

29

4.1 Transparency: Explicit targeting of subsidies for the poor

4.1.1. Traditional approaches to subsidies versus OBA subsidies

Traditional input-based schemes which subsidize specific investment projects such as power

plants or more general budget support for utilities are often equivalent to across-the-board subsi-

dies, as they decrease the tariffs needed to cover costs. Wealthier households tend to consume

more utility services than poorer households so that the bulk of such subsidies benefit non-poor

households. Further, a large percentage of the poor who are often not connected in the first place

cannot benefit from these across-the-board subsidies.

Quantity-based tariff subsidies that charge lower tariffs for lower quantities of water or electrici-

ty are a common way of attempting to target utility subsidies to the poor.17

However, empirical

evidence from the water and electricity sectors shows that such subsidies usually have a regres-

sive targeting effect in that larger proportions of subsidies benefit richer households. This is

largely because many of the poorest households do not have access to these services in the first

place, but also because of inherent regressive characteristics of quantity-based tariffs such as:

- fixed charges that negate subsidy benefits if they increase effective average tariffs of low

consumption households

- increasing block tariffs subsidizing first units consumed of all income strata alike whether

rich or poor and regardless of total consumption behavior

- in some cases, low ―social‖ tariffs that result in incentives to actually increase the up-

front connection costs for users as compensation for lost revenue through the tariff subsi-

dy (Komives et al 2005, p 79ff)

- the lack of clear correlation between income and consumption in the case of water (Ko-

mives et al 2005, p 82ff, p 167).

The seminal study by Komives et al has demonstrated (largely through simulations given the

lack of data) that ―connection subsidies‖ to provide initial access to households in the first place

are inherently more pro-poor than quantity-based tariff subsidies that are linked to the amount of

service used.

OBA in the infrastructure sectors mainly relies on one-off capital subsidies for increased access –

usually through connection, in the case of the network industries. These OBA subsidies aim to

increase access to poor households in the first instance. Then, if there are quantity-based subsi-

dies implicit in the system, poor households can also benefit from them – if the quantity-based

subsidies are properly designed to actually benefit the poor.

Well designed OBA schemes in the utility sectors usually rely on the target population being

able to afford sustainable tariffs that cover ongoing costs of service provision – in other words,

although access may be subsidized, tariffs or running/operations costs may not be. But this is

often not a major hurdle: the poor usually are paying more for alternative services (HDR 2006, p.

52, p. 83). 18

In some cases, additional pro-poor mechanisms are required to ensure effective tar-

geting. For example, tariff affordability issues for the very poorest can be partially mitigated by

17 Quantity-based subsidies through tariffs in ICT are less common as the sector has moved toward collecting explicit subsidies

through universal access funds, but are still in place in some former Soviet bloc countries.

30

subsidizing pro-poor access (such as public water points) which have lower running costs per

capita, and also by ensuring appropriate schemes which fit the payment patterns of the poor.

In the social sectors, traditional funding mechanisms may not primarily benefit the poorer seg-

ments of the population. ―…while governments devote about a third of their budgets to health

and education, they spend very little of it on poor people—that is, on the services poor people